Its much-hyped but minuscule stock ETF holdings are on ice too.

By Wolf Richter for WOLF STREET.

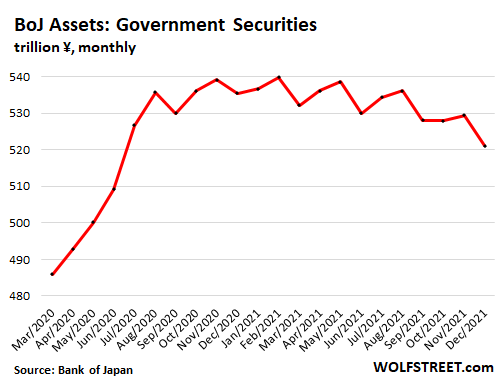

The Bank of Japan – which engaged in QE for longer than any other central bank and leaped into monstrous QE when its new national economic religion of Abenomics took effect in early 2013 – began tapering QE in late 2020, and ended QE altogether in May 2021. Since February 2021, the BoJ has actually reduced its holdings of Japanese government securities, the primary driver of QE and the largest category on its balance sheet (72% of total assets), by 3.5%.

As of its balance sheet for the end of December, released today, the BoJ reduced its holdings of Japanese government securities to ¥521.1 trillion ($4.5 trillion), below where they’d been in July 2020. I started pointing at the end of QE with the release of the August balance sheet when it became apparent what was going on:

The fluctuations of these holdings are associated with large long-term bond issues on the BoJ’s balance sheet. When an issue matures, the BoJ gets its money back, but it doesn’t purchase the replacements until a month or two later.

At the end of December, these government securities consisted of ¥507.8 trillion of Japanese Government Bonds (JGB) and ¥13.3 trillion of short-term Japan Treasury bills. The decline in the BoJ’s holdings of government securities since February was concentrated on these Treasury bills.

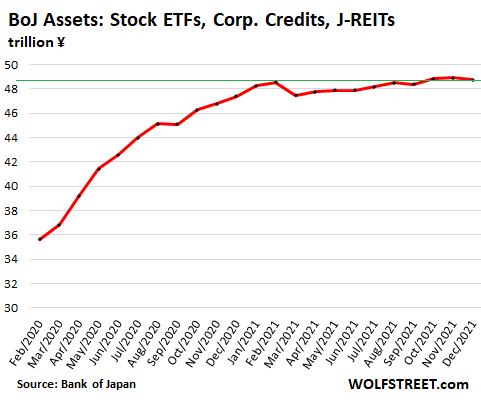

Stock ETFs, Japanese REITs, corporate paper, and corporate bonds.

In the US financial media, the most-hyped aspects of the BoJ’s QE were its purchases of Japanese stock ETFs. But in the end, those purchases, which ended in 2020, were minuscule: Just ¥36.7 trillion, about 5% of the BoJ’s total assets.

The BoJ marks its stock ETFs to current market value. The Nikkei 225 index has risen about 8% over the past 12 months. Over the same period, the BoJ’s stock ETF holdings have ticked up only 2%.

In addition, the BoJ also bought Japanese REITs, corporate paper, and corporate bonds, in even smaller quantities. All combined, stock ETFs, Japanese REITs, corporate paper, and corporate bonds, amounted to ¥48.7 trillion, just a tad below the peak in February 2021. They account for only 6.7% of the BoJ’s total assets:

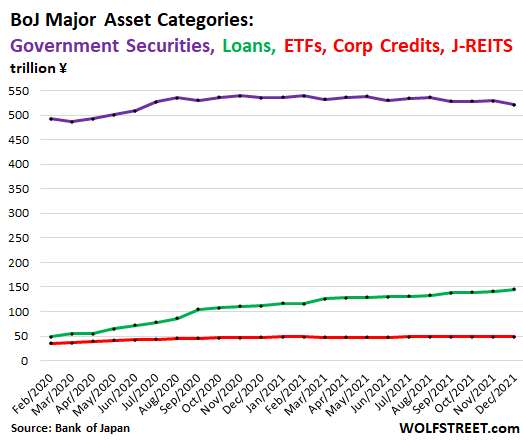

Stimulus Loans.

The BoJ has several stimulus-loan programs: its pandemic-stimulus loan programs, and its pre-pandemic loan programs that are supposed to stimulate bank lending. Combined, these loans are the second largest line item on the BoJ’s balance sheet after government securities and account for 20% of its total assets. These loans have continued to grow.

The chart below shows the major asset categories on the BoJ’s balance sheet from February 2020 forward: government securities (purple), loans (green), and the combined total of stock ETFs, J-REITs, corporate paper, and corporate bonds (red line at the bottom):

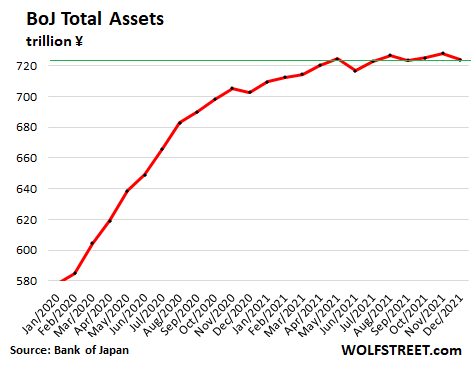

Total asset decline.

All assets on the BoJ’s balance sheet combined dipped to ¥723.8 trillion ($6.24 trillion) at the end of December, just a tad below where they’d been in May 2021:

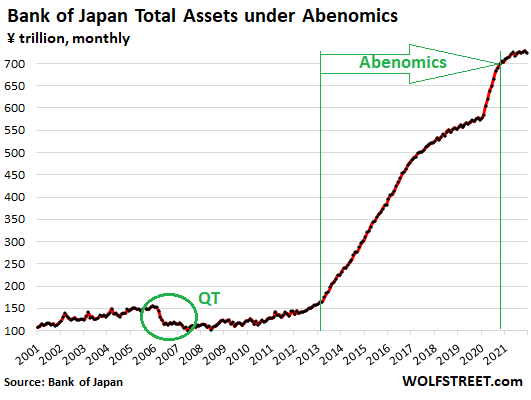

A long-term view of the BoJ’s balance sheet shows the impact of Japan’s national economic religion of Abenomics under Prime Minister Shinzo Abe, which kicked off in early 2013 and ended after Abe’s announcement of his retirement in August 2020, when the BoJ quietly began tapering its asset purchases and ended QE altogether in May 2021:

In the 18-month period from January 2006 through June 2007, circled in green, the BoJ reduced its assets by 36%, unwinding five years of QE, just about all of its QE since 2001, the first modern act of “Quantitative Tightening.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wusses.

I’m curious, is the BoJ simply easing off the accelerator to coast for awhile, or are they actually going to attempt to tap on the brakes (unloading some of their Japanese gov. bond holdings)?

With the gigantic balance sheet the BoJ has, I can’t see how they will be able to unload even a portion of this debt. They were the only ones who were willing/able to buy this in the first place. Who will buy it?

“Who will buy it?”

Yield fixes demand issues. Even a slightly higher yield brings out the buyers.

The BOJ is now starting to re-assess its position on inflation. It has been rising in Japan as well. Without a big drop in cellphone fees, it would have reached 2%. The underlying inflation measures (including PPI) are running much hotter. So the BOJ can see where this is going: Japan is going to get its share of this inflation. “Sources” in the BOJ have already been talking to the financial media about this to spread the word that a shift is coming.

Look at the number of idgits that are currently piling into Chinese property debt. Someone will always step in to buy at a price.

It looks like the BoJ is in a catch 22 situation. I looked up the 10 year Japan government bond stats, and the yield has been hovering around 0% since 2016, and was very low in the years leading to that point. The Japanese government, stock markets, and economy have been living in an extremely low interest rate environment for nearly two decades.

How can the Japanese government possibly pay higher rates on government bonds which have essentially been monetized by the BoJ?

If the Japanese bond rates go up, interest rates in the private sector will go up as well. How will the Japanese stock markets, which were partially propped up by the BoJ, react to this?

We saw what happened to the US banking system when the Fed tried to raise rates just a little bit. There was a breakdown in September 2019 with a gigantic spike in the repo market interest rates, which led to the Fed immediately stepping in to keep the US banking system from going into a credit freeze.

This is not going to end well.

BOJ is replacing JGB with stocks? Whoa! The impetus to buy government bonds is not the interest (although that may change) but the fungibility. Speculators buy bonds on margin, borrow on the full value?? ( and you think former potus is the first to mark assets differently?) This news is sort of bullish. Stock owners always get bailed out, bond holders (occasionally) take the haircuts, and those who own bonds provisionally, (Fed?) avoid the same fate as widows and orphans.

“BOJ is replacing JGB with stocks? Whoa!”

NO NO NO NO. Put on our spectacles, back off on weed, and read the article :-]

Holy moly, how can you come up with this?

From the charts, it looks like the BOJ has a long, long way to go to unwind this. Am I mistaken here?

It can unwind some of it without problems. It won’t unwind all of it; and there is no need to. And it has a very long time horizon.

WOLF

I can’t help but do comparisons to the US. Japan has about 1/3 of the population of the US and about 2/3 of the govt debt of the US. This would indicate the US Fed balance sheet could about double to be on par with Japan. Japan is slowly reducing the balance sheet and the US Fed will start QT within a year.

It’s amazing Japan has less inflation than the US with these ratios….what gives ??

As I said many times, inflation is in part driven by the mindset. If there is price resistance among consumers and businesses, it’s hard for inflation to take off. Once that mindset changes — in the US, $10 trillion in stimulus changed that mindset — then there is nothing left to push against price increases, and they can start rippling through the economy.

There has been a lot of price resistance in Japan, but that now appears to be breaking down too.

Looks like the BOJ is rock-skipping its reduction of govt debt. Are these stimulus loans just another form of fielding govt debt?

The loans are made to the private sector (banks, etc.)

BTW… it begins, here in the US, rising interest rates on savings…

For the first time since 2018, I was notified by one of my banks that the interest on its high-yield (hahahaha) savings account has been raised . The new rate starting today is a whopping 0.50%.

“The new rate starting today is a whopping 0.50%”

A step in the right direction though!

Is that APY or annual interest rate? With that rate, we need to account for every cent! 🤣

Ally Bank already had that rate for a year now.

The point was that the bank “raised” the rate for the first time since 2018.

// The new rate starting today is a whopping 0.50% //

I won’t even bother to put my money at saving accounts until the new rate is 5%, instead of 0.5%. That’s what saving accounts SHOULD be!

And with inflation running at 9%+ you’re only losing 4% on every dollar saved at 5%.

And if your stocks go down 20%, you lose 29%.

0.5%, or 0.05%?

0.50%.

One half of one percent.

Now if only we could get 30 yr mortgages up to 5% or higher, it might be affordable to buy a house again.

When 30 year mortgages go to 5%, the price of houses will come down. However, the economy will also slow down which will lead to job losses, which might prevent you from buying a home.

“Examining the relationship between 3-month and 10-year benchmark rates and nominal GDP growth over half a century in four of the five largest economies we find that interest rates follow GDP growth and are consistently positively correlated with growth. If policy-makers really aimed at setting rates consistent with a recovery, they would need to raise them. We conclude that conventional monetary policy as operated by central banks for the past half-century is fundamentally flawed. Policy-makers had better focus on the quantity variables that cause growth.

Reconsidering Monetary Policy: An Empirical Examination of the Relationship Between Interest Rates and Nominal GDP Growth in the U.S., U.K., Germany and Japan”

https://www.sciencedirect.com/science/article/pii/S0921800916307510

What was it before?

I think 0.40%.

For any of the larger / developed economies of the world (G7, G30) what would ever be the reason or impetus to trim central bank balance sheets? What would ever cause a developed country’s government to drastically reduce their public debt close to or down to zero?

We have seen some countries (Brazil, Russia, etc.) jack up their interest rates which should reduce the amount of public debt accrued on a go forward basis, but will that really be enough to force those countries to actively reduce their public debt? Or is it just a transitory phase in history where debt binging just takes a little break?

Debt binge continues in the US because our rates are low – why wouldn’t you borrow at these ultra low rates? US Congress is trying to ram one last spending bill because the rates are so low.

rates are low because they were manipulated to be low. the way you are describing it, it’s as though it happened on its onw.

Lacy Hunt’s theory is excessive debt is counterproductive and turns $1.00 into less than $1.00 slowing growth potential and therefore lowering interest rates. In this case US is doomed to even lower rates like Japan and in second place Eurozone.

Lower growth doesn’t decrease credit risk which is the other commonly perceived factor in interest rates.

If anything, lower growth should normally mean higher defaults outside of government debt and government guaranteed loans which should in turn mean higher interest rates on most debt, since it’s actually of lower or marginal quality. It’s only been an unprecedented debt mania which has convinced so many that high risk magically equals low risk.

Lacy Hunt is a former central banker and he continues to think like one. He doesn’t seriously consider default risk or hyperinflation risk. He seems to believe central banks can successfully manage the economy in low growth mode forever with QE and other tools. He’s one of the few people recommending people buy 30 year bonds paying 1.5%.

The view is actually quite risky. The potential for downside in long bonds is enormous.

Old School and Bobber,

I like listening to Lacy Hunt. He has good insight but I would never give him my money to invest. Remember guys, he owns a fixed income investment fund that basically does UST all day long.

So of course he is going to tell you to buy long on the 30YR UST at those low prices ;)

Good point PG. So how much US debt is healthy? $20T, 15T, 10T…?

Or will we stay at $30T and hope to remain there and not head towards $40T

The problem with the federal debt is a cultural one. A combination of extensive long term social decay and a belief in magical thinking, something for nothing.

How exactly is the US going to even stabilize the debt burden, in nominal terms but even as a proportion of GDP?

It will take noticeable tax increases, spending cuts, or a combination of both. And it won’t happen through a “peace dividend” by gutting the defense budget and eliminating “fraud and waste” either

This is a complete fantasy. There is no political will for it and the math doesn’t add up.

It can only happen through a voluntary coordinated reduction in national living standards, as any decrease in the deficit will reduce “growth”. With a divided and Balkanized society, I’d rate the chances as exactly zero.

Or…..

The gov can pay back the debt over the next five centuries.

That makes it very manageable.

Peanut

In a land far away and long ago, it was assumed, it was incumbent on every generation to pay their own debts.

Remarkable isnt it?

In 1980 the national debt was under $1 Trillion. 191 years of government, a Civil War, Two World Wars, a Depression, Korea, Vietnam, etc ….

and the national debt in 1980 was 1/30th of today’s national debt.

Stealing from the future generations was NOT CONSIDERED.

Fighting inflation was the mission, NOT PROMOTING INFLATION.

Stealing from the future, pulling its wealth forward, to FLUFF the present would have died on the table.

But something changed around 2009.

The change around the year 2000 was accumulated social decay and belief in

magical thinking.

Somehow, society led by the economics profession came to the ridiculous conclusion that there should never be a recession and government has the ability to preserve living standards if not guarantee increased prosperity through fiscal and monetary policy.

Or, maybe enough of them knew without the 21st century distortions from both society might or will come apart at the seems.

Wolf,

That tightening in 2007 was prior U.S. S&P666. Just saying some kind of drop coming up. Fed seeing a lot of risk with inflation now too.

‘Fed hints faster tightening’:

NASDAQ down 2.5%, BC down 4.5 %, gold down .04%.

The coming run on BC is going to be a classic.

Yep

BTC has never seen interest rates.

Did the Fed governors sell theirs okay?

When money is free, people are free to do stupid things.

Without free money, doing stupid things is costly!

WES

Hence the wisdom of the 3rd unmentioned mandate (due to the dual mandate mantra)…

“Promote moderate long term interest rates. ”

It is difficult to find on the Federal Reserve web page as it is a discomfort to them. They intentionally hammered long rates to 4000 yr lows to FORCE investors to take more risk.

Former Fed Governor Fisher admitted the same when he spoke on the “Power of the Federal Reserve” documentary on PBS….(available on the PBS web site, around the 7 minute mark).

This mandate is perhaps the most important and most abused.

Moderate long rates maintain a balance between lender and borrower, keep the yield curve steep, and inhibits massive debt creation that rapes future generations.

Recall just months ago, the talking heads on cable pointing to the flat yield curve and saying “see, no fear of inflation”.

This 3rd mandate is NEVER MENTIONED, but is there for all to see in the Federal Reserve Act.

Exactly. My motto is that if the Fed were to shut down tomorrow all the “stupid” would evaporate within a year. Zero legislature time would be devoted to pronouns or whether a biological distinction between men and women really exists.

The equites guys who have had a free run …will now declare that the prices must be defended…

Spiked prices must be defended, they will say….and they were “spiked”.

Bitcoin sales and therefore prices mostly faked and would be illegal but…. it’s UNREGULATED. If guys want to trade sports cards, and ‘sell’ them back and forth, chumming the market to suck in buyers, it’s not illegal because…see above.

Above is me, not the quote below.

Source: Bitwise

‘Analysis showed that “substantially all of the

volume” reported on 71 out of the 81 exchanges was wash trading, a term that describes a person simultaneously selling and buying the same stock, or bitcoin in this case, to create the appearance of activity in the market. In other words, it’s not real.

Those exchanges report an aggregated $6 billion in average daily bitcoin volume. The study finds that only $273 million of that is legitimate.’

So about 5% of BC sales actually happen. The ‘market’ is over 90% fake.

PS: much of the disciplinary action against stock promoters is for wash trading.

The Japan Nikkei 225 stock market is below its all time high reached in December of 1989.

Japan has been experiencing deflation for years.

That will probably be our future once the bubble bursts. Might take 20 plus years to make new high. Or like Japan- going on 33 years.

That is because they have no population growth. Strong equity markets require GDP growth, and GDP growth requires population growth. Equity 101.

You’re claiming Japan has had zero GDP growth since 1989?

Japan’s stock market was a mania in 1989. That’s enough of an explanation.

Since 1982, the US has had mostly rising asset prices with “moderate” price inflation despite a debt, spending and monetary binge.

Going forward for the next several decades (no, not tomorrow) I now expect the opposite, a major bond and stock bear market with higher price inflation.

I also expect real estate to mostly perform poorly. Noticeably higher mortage rates at anything close to current prices means the (vast) majority will only be able to buy a (much) cheaper property or not at all.

The wealthy (real and imagined) are also going to be mostly a lot poorer because most of their wealth is the result of the fake economy and an asset mania. It isn’t real either but mostly a bag of hot air. If you don’t believe me on this one, look at what they actually own, not what it is “worth” monetarily.

In the US, there aren’t 724 billionaires now versus 13 in 1982 because the US is actually that much richer and productive.

Japan had strong GDP until the end of the 80s. The Nikkei was pricing this GDP level with growth forward. Then, Japan’s GDP crashed and never came back.

So, what you call a bubble was actually a market that had GDP expectations which were wrong.

It is awfully hard to grow GDP without population growth. Without population growth, you have to increase GDP per capita, which is a challenge in an advanced economy.

Population is overrated. Whether the population is 1000 or 1000000, stock prices are a function of money and credit. Holding real capital constant, twice as much money implies twice the price.

Stock prices rise with inflation just like any others. It’s just not widely recognized as inflation because consumer prices don’t rise until later in the cycle, and conventional economics equates inflation with rising consumer prices.

David Hall,

“Japan has been experiencing deflation for years.”

Why to people keep regurgitating this New York Times BS year after year instead of looking it up. Here is the Japanese consumer price index. It shows actual price stability, the way it’s supposed to be, for 20 years:

To be fair you should also show a chart of the Nikkei Index and the Japanese housing market, in the same time frame that you are showing the CPI.

I thought Central Banks were supposed to be “independent.” It is pretty remarkable to see one so tied to a particular politician.

Japanese government agencies, the central bank, and major institutions and companies work hand-in-glove — always been that way. There is not much love in Japan for free markets or independence of anything.

There were three official “legs” of Abenomics, one of which was money printing. Abe ran on it. I covered it extensively back then. And the BoJ delivered. But now he’s gone, and the tune has changed.

Gee…..the market appears too be concerned the fed will be raising rates…..what a surprise……now…..lets hope Mr. No Spine has a change of attitude before he destroys the entire economy.

BEfore he destroys the economy? Who, Powell? Or Biden?

We still have the largest spread in history between Fed Funds and Inflation…EVER? This is just a baby step….to posture and slow stimulus…

slowing stimulus is not tightening, IMO…it is “slowing stimulus”.

What do you think inflation does to an economy? Get ready, its just startin’.

And we see the Democrats blaming businesses for raising prices….did they know the Fed goosed money supply by 30% with interest rates 6% below inflation? Did these people go to school? Live in the real world?

Does IVY league count as school?

Change of attitude…..What I mean is he stands up to the rich and tells the market to shove it.

What does LeGarde say, do? Didnt she say something in the vein of “will not raise rates in 2022”? How far can the Fed stray from an ECB with that policy in place?

IMO we are closer knit to the ECB than BOJ, though the BOJ started this whole ZIRP thing back in 2000 and for them to begin to retreat from this is important.

Still feel the lack of action by the Fed will be predictable.

I’m sure Powell is definitely and resolutely going to “keep a close eye on things”. Will the Fed serve the GDP master or slay the inflation dragon?

I think the former. GDP will continue to limp along supported mostly by the federal spending spree.

So next to the “Free Beer Tomorrow” sign goes the “Fed Action Tomorrow” sign.

Based on past monthly fluctuations, this one time double tap of government securities will need to be repeated much more often. The timeline is too short to verify this, especially on the historical zig zag of its government securities.

OOOps, the Nasdaq just dropped nearly 600 points. Looks like a replay of 2000. The Robinhoods will be the leaders this time.

In Southern California, it is hand to hand combat getting your offer accepted on smaller beach cottages. This has a way to go. Some FED speak changes nothing.

Real estate…the most illiquid of markets..

one day a scramble to buy, next day no bid.

True … but, in the long term, with a decent location, it usually works out. With 10% or 20% down, you handily beat the equity market, especially with the tax treatment. There is no free lunch, and the outperformance is due to liquidity risk .. you are being paid to take it.

However, you have to make sure you have a cash equivalent position to survive the no bid stretches … because they happen frequently, and they can be long.

There is one thing that keeps me up at night … a deadly COVID variant could appear which would cause a major move away from all metro areas … all metro area real estate would get killed. This is a possibility …

SocalJim,

The Nikkei is down from its 1989 high for two reasons:

1. price stability for the yen (see chart posted here somewhere); inflation wasn’t there to cover up the weakness.

2. a HUGE bubble leading up to 1989.

That bubble blew up, but it was so huge and prices were so inflated that, without rampant inflation, stocks just couldn’t get back to that level in three decades. And it’s not the exception. There are a bunch of major stock indices of major countries that have not gone back to bubble highs from a decade or two ago, including many European indices and the SSE index.

The S&P 500 is the exception, but this bubble now is so huge that it might prove to fall into the same no-revisit-for-a-long-time category.

On the street, we estimated a country specific implied forward GDP from the equity market.

In the late 80s, most had Japan’s implied frorward GDP as their base case and declared the Nikkei fair. They called that the Japanese miracle. Turned out that was a big mistake.

In hindsight, you can claim the forward GDP was wrong and label it a bubble, but back then, that was a minority opinion.

It looks like the 24/7 fear porn propaganda attack by the MSM has gotten to SocalJim. Now he’s laying in bed, sweating out the possibility of a new “variant.” Snap out of it.

Real estate in many markets is arguably more liquid than physical silver. Look at the price spreads.

It takes somewhat longer to sell if priced “properly” but most of this difference can eventually be eliminated by bringing the closing process into the 21st century.

I’d never waive inspection but many buyers apparently do. Only other obstacle seems to be title insurance.

1) For entertainment purposes only : NDX is down for tomorrow

chick-a-fill day. Both the DOW & SPX made 1:1 from Dec low.

2) SPX & NDX backbones : between Nov 5 hi/ 10 lo.

3) SPX entered the BB from above, NDX pricked it below.

4) The DOW missed 37,000 by 47 points. The DOW will not chicken-out.

5) NDX monthly Jan 2022 countdown #13 might have a slight delay, but three Sequential monthly #9 might reach #27 in Apr 2022, if there will be no flip.

6) SPX monthly might reach #27 in June. The DOW flipped in Sep last year. SPX & the DOW might reach monthly #13 in Mar/Apr.

7) By mid year SPX will be out of fuel, unlesss…

Today’s recession was brutal, but necessary to clear out the zombie companies and pave the way for a massive bull market.

Nice

NDX was down > 3%, but TY (US 10Y price) and Honeywell didn’t care.

Meanwhile, the Congressional Clown Show is talking about more stimulus payments. These idiots will never learn until the entire country is burning down around them.

“The Washington Post earlier reported that Democratic and Republican members of Congress were discussing another possible round of COVID-19 stimulus spending amid the fast-spreading Omicron variant that would target restaurants, performance venues, gyms and minor league sports teams.”

DC

“stimulus payments.” = vote buying (2022 midterms)

Yes, more stimulus of the economies of China, Mexico, Japan, and Germany!

I was getting 7.5% on my money in 2008 (give or take a year).

Do you reckon that the interest rates on savings will go that high again or am I dreaming.

Even 5% will do.

I believe the only way to win going forward is to borrow money. The easiest way to do that is to let someone else to the borrowing for you, that means buying something like Annaly Capital Management (ticker NLY). Using 5 or 6 times leverage, they borrow cheap and buy mostly mortgage backed securities. Unfortunately, it’s a volatile fund and needs to be timed correctly.

Maybe so, but if you don’t have the need for a lot of stuff I had rather be debt free and own equities of companies with no debt or no net debt. But to do well you have to have the courage to use your cash when most are panic selling

That’s the old school of investing, all right. I spent my whole life following the old school of investing, but I am changing now. The new orthodoxy requires recognizing that debts get inflated away over time. Unfortunately, I am too much of a coward to practice what I preach. At the moment I’m more of a Walter Mitty than a true leveraged investor.

Sounds a bit risky to me.

I worked too hard for my savings to gamble it away.

thanks though.

I get the impression that the Fed is still stuck thinking that looser monetary policy will lower the unemployment rate, and that since we’re approaching maximum employment now it’s safe to raise interest rates. Isn’t there a possibility that today we get less employment with loose policy because people are content earning passive income, so unless you scare investors, they won’t be going back to work?

Is the implication here that the FED will soon do the same or something similar?

Yes… only more

https://wolfstreet.com/2022/01/05/markets-suddenly-hear-hawkish-fed-stocks-sag-arkk-plunges-yields-jump-cryptos-the-new-hedge-against-inflation-fail-to-hedge-plunge-in-sync/?trashed=1&ids=399987