In some cities, prices out-spiked even the craziness at the apex of Housing Bubble 1 before it fell apart. In others, the heat is getting dialed down.

By Wolf Richter for WOLF STREET.

“After 14 consecutive months of acceleration, the S&P CoreLogic Case-Shiller index finally took a turn,” said CoreLogic Deputy Chief Economist Selma Hepp today. But wait… Instead of spiking at a rate of 2% or more from month to month, the national index spiked by only 1.0% in the latest month, whittling down the year-over-year spike from a record 19.8% in the prior month to, well, 19.5% in today’s report.

Amid this slight overall “deceleration” of the raging mania, house prices spiked at an all-time record pace in some markets: Tampa’s 27.7% year-over-year spike and Phoenix’s 33.1% spike out-spiked even the craziest moments in those two markets at the apex of Housing Bubble 1 before it fell apart. But in some other markets, on a month-to-month basis, prices flattened for the first time in two years as the heat was being dialed down.

S&P CoreLogic ascribes this situation – this sense of slowing price spikes – in part to a typical seasonal slowdown, after there not being a seasonal slowdown a year ago, and in part to “a slow albeit welcomed return to more sustainable balance between buyers and sellers.”

The charts below depict the mind-boggling price spikes in the bubbliest metropolitan areas – the most splendid housing bubbles in America – based on the Case-Shiller Home Price Indices, released today, for “September.” The “September” data are a three-month moving average of closed sales that were entered into public records in July, August, and September. That’s the time frame of today’s data.

House price inflation. The Case-Shiller Index is based on the “sales pairs method,” which compares the sales price of a house to the price of the same house when it sold previously. It includes adjustments for home improvements. By tracking the price of the same house over time, it is a measure of house price inflation.

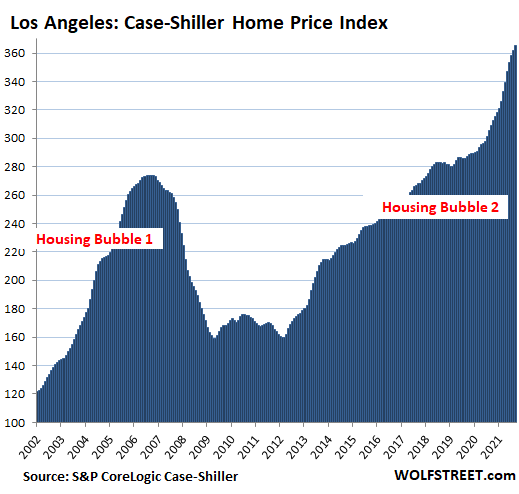

Los Angeles metro: The Case-Shiller Index for single-family houses jumped 1.1% in September from August, and by 18.3% year-over-year.

The Case-Shiller Indices are set at 100 for January 2000. The Los Angeles index value of 366 means that house prices have soared by 266% since January 2000, despite the Housing Bust in between. Over the same period, the Consumer Price Index (CPI) rose by 64%.

This 266% increase since January 2000 makes Los Angeles the most splendid housing bubble on this list. The charts below are on the same scale as Los Angeles to show the relative splendidness of house price inflation in each market since 2000.

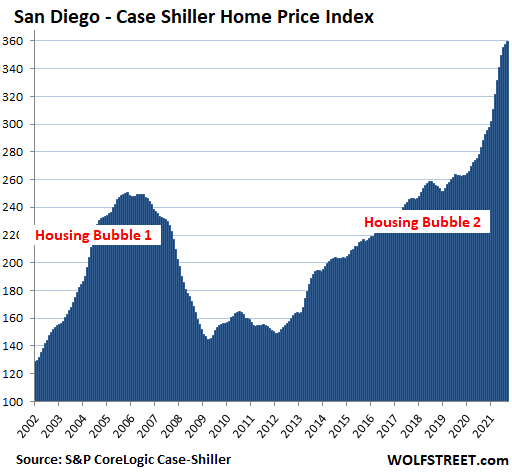

San Diego metro: House prices rose 0.7% for the month – a slowdown from the 2% to 3.4% month-to-month spikes earlier this year – which whittled down the year-over-year increase to a sizzling 25%, from an even more sizzling 27.8% at peak-heat in July. Since 2000, prices have ballooned by 260%:

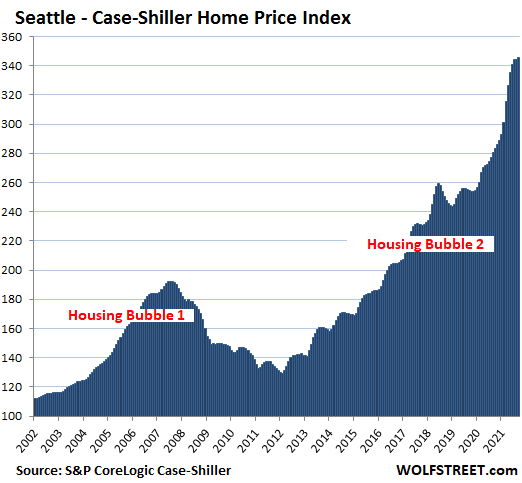

Seattle metro: House prices rose by 0.4% for the month. The past two month-to-month increases were slowest since June 2020 and whittled down the year-over-year spike to 23.3%, from 25.5% at peak-heat in July. Since January 2000, house prices have soared 246%:

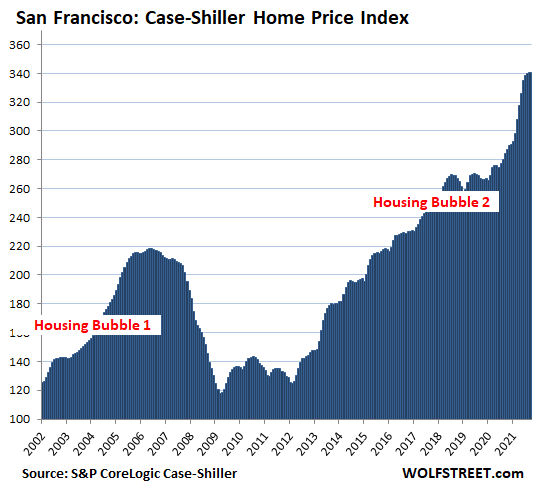

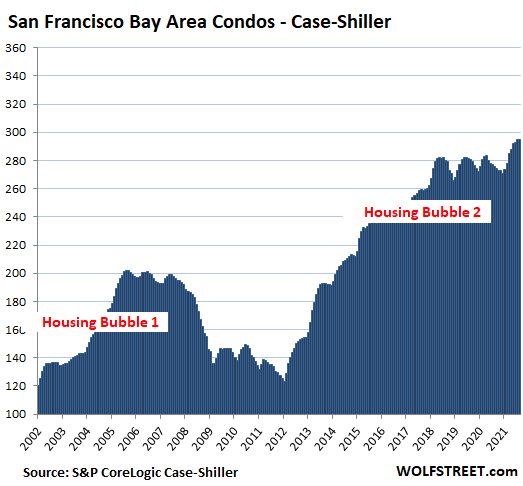

San Francisco Bay Area (five counties of San Francisco, San Mateo, Alameda, Contra Costa, and Marin): Prices of single-family houses inched up 0.1% the smallest month-to-month increase since June 2020. This whittled down the year-over-year spike to 19.8% from peak heat of 21.9% in June and July:

Condo prices in the San Francisco Bay Area, after wobbling in the same range since 2018 but then picking up over the summer, remained essentially flat in September and were up 7.1% year-over-year:

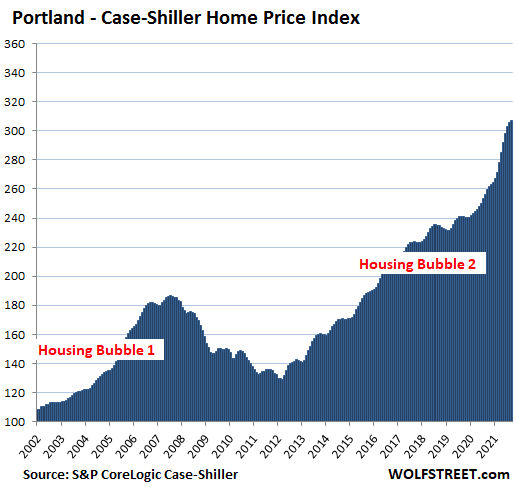

Portland metro: House prices rose 0.4%, the slowest month-to-month increase since January 2020, which whittled the year-over-year spike down to 18.2% from peak-heat 19.5% in July:

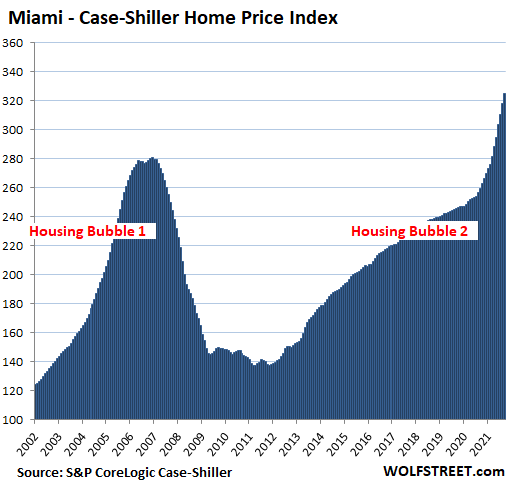

Miami metro: Prices continue to spike relentlessly, +2.2% for the month, +25.2% year-over-year, the fastest since March 2006 at the apex of Housing Bubble 1:

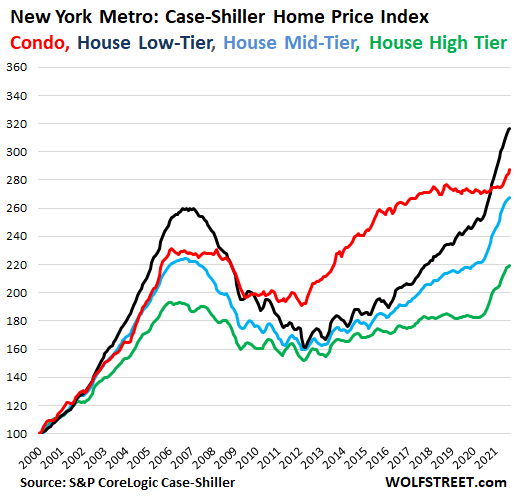

New York metro (New York City plus counties in the states of New York, New Jersey, and Connecticut): House prices overall rose 0.5% for the months and 15.8% year-over-year. But by price tiers, there were differences.

Low-tier prices have soared the most since 2011 (black line), and for the past 12 months shot up 19.0%. But they too slowed down, and month-to-month rose only 0.2%, the slowest increase since May 2020.

High-tier prices (green line) rose 0.4% for the month and 20.2% year-over-year. It took till the end of last year for high-tier prices to shoot past Housing Bubble 1.

Condo prices (red line) spent years going nowhere but in recent month heated up. In September, they rose 1.0% for the month and 5.7% year-over-year:

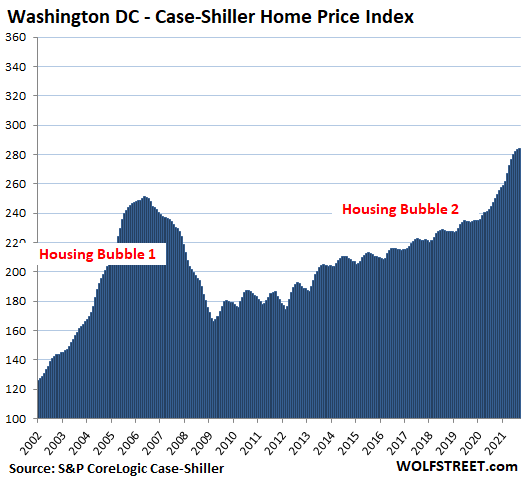

Washington D.C. metro: +0.2% for the month, the smallest increase since January 2020; +13.7% year-over-year, down from peak-heat 15.4% in June.

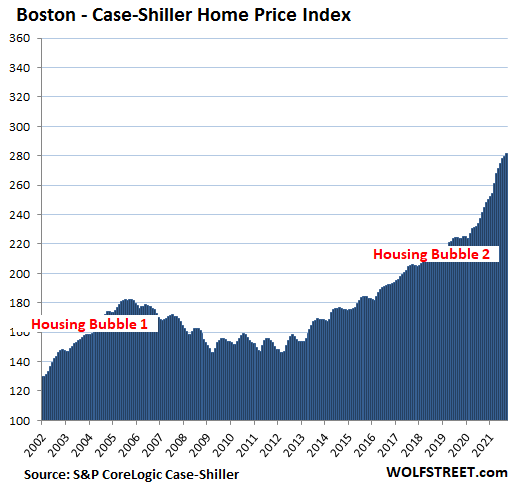

Boston metro: +0.8% for the month, +16.8% year-over-year:

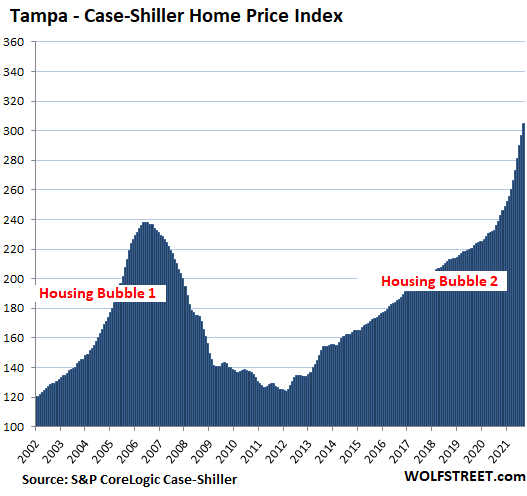

Tampa metro: +2.7% for the month, a huge spike; +27.7% year-over-year, a record spike, out-spiking even the crazy record spikes at the apex of Housing Bubble 1:

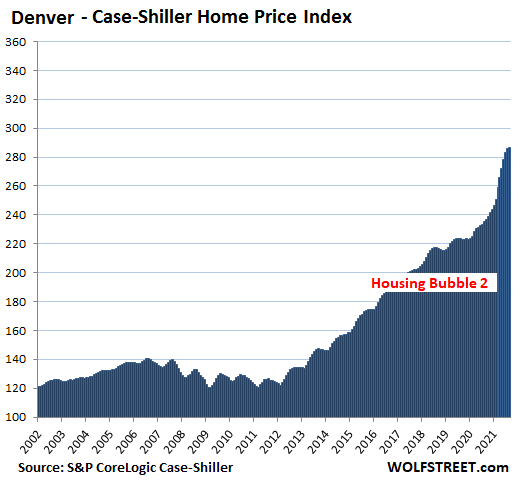

Denver metro: +0.4% for the month, +21.3% year-over-year:

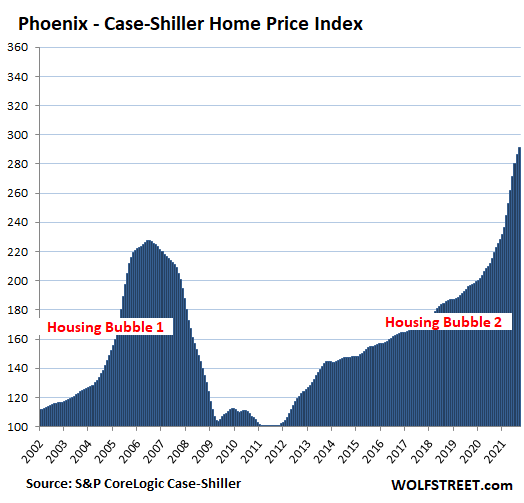

Phoenix metro: +1.7% for the month, +33.1% year-over-year, the red-hottest annual house price inflation among the most splendid housing bubbles here, and out-spiking even the craziest spikes at the apex of Housing Bubble 1. But this time, it’s different or something:

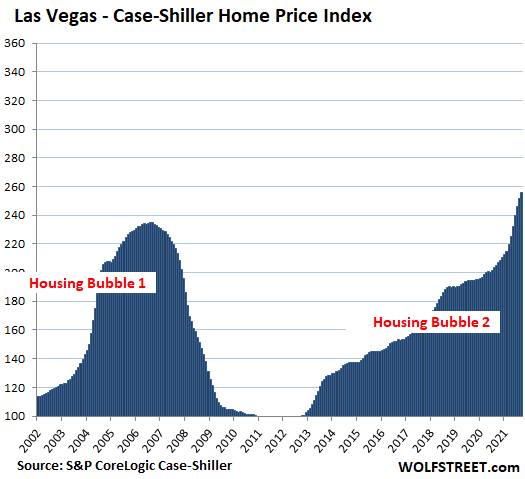

Las Vegas metro: +1.5% for the month, +24.7% year-over-year:

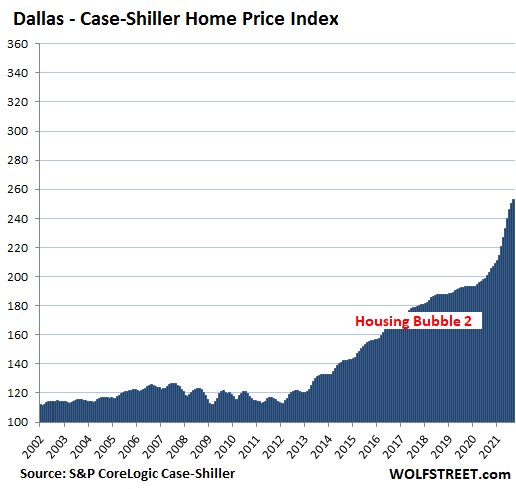

Dallas metro: +1.2% for the month, +25.0% year-over-year. The index is up 153% since 2000.

The remaining metros in the 20-metro Case-Shiller Index have house price inflation since 2000 of less than 150% and thereby don’t yet qualify for this list of the most splendid housing bubbles.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Spice up the charts by adding the coyote in the Acme rocket jet roller skates riding these launch platforms. Youse buys yur ticket…..?

Followed by the coyote running off the edge of a cliff, waving his hands frantically while suspended in mid-air, then plunging to his demise.

He always lives to ride again!

Congress/fed got this little dance down pat!

difference is this ‘inflation’ spike ain’t going away

just informed my son to expect minimum 10% annual inflation(like 70’s)

Blame the Fed. They’ve created a reality in which there is no yield for lending cash. So with the choice reduced to either stocks or property, big publicly listed institutions chasing percentage yield have gone into the rental business, driving home prices up, and ordinary working people out of home ownership.

There’s something morally wrong with this.

all the while they gaslight us about it, saying that there is no yield for lending cash because there is a glut of it. which is of course bs, because if there was truly a glut of it at current rates, the fed wouldn’t need to print the money.

Weimar Boy Powell has finally warmed up to having a conversation about a quicker tapering of his raging bubble policies, but only 6 years too late.

i suspect the president or manchin read him the riot act when he and brainard went in to meet with them prior to the nomination.

“There’s something morally wrong with this.”

That is absolutely the last thing that the millionaire Fed predators care about.

Been watching vacation homes at beach in NC. Pricing displays the same blow off top from a a very consistent slow price growth the last decade. It looks much like the Microsoft blow off top, but not as high. Obviously the Fed and government did too much.

The bigger they are, the harder they fall.

SP500 up more than housing last 20 years. Gold up more than stocks. It’s the everything bubble. The difference is most people bought stocks and gold with cash. Housing is the one with leverage.

Not true.

SP500 price index since Jan 2000 up 230%. Case Shiller for Los Angeles up 260%. So, if you paid all cash for your home, you are ahead of the SP500 by a little.

Now, if you assume you bought a Los Angeles home in 2000 with 10% down, you are up 2500%

I didn’t say since 2000, I said last 20 years. Nov 2001.

But yes using leverage housing beat stocks. But you could have used leverage in the stock market as well.

Anyone taking into consideration taxes and maintenance on those homes???

Taxes and maintenance are cheaper than rent … if you don’t own, you rent.

You rent the place or you rent the money to “own” the right to pay the full burden of interest, taxes and maintenance.

A good cheap rental, while hard to find (especially in the legacy brand western countries), blows away ownership by a mile.

Nothing tastes better than freedom

Margin debt is at an all time high?? Almost $1T

It’s Different This Time.

It’s a new paradigm!

“There will never be a better time to buy!”

Yeah . . . food, guns, and ammo.

The most simple accurate valuation metric on stocks is price to sales. March of 2009 it was 0.8. Today it’s 2.9. Housing has went along for the ride.

ZIRP policy might have ran as long as it can with inflation high and Powell says it will be here at least til mid 2022. He is hoping to kick the can a little further down the road.

The Fed is STILL lending (buying MBSs) 3% below inflation at a rate of at least 30,000 MILLION a MONTH!!!! (30 Billion)

WHY? Anyone ask why at the Senate hearings?

Last time inflation was in this neighborhood, actually lower…..

the 30yr mortgage was 6% (1999 and 2006)

Worst markets of those I know are Miami and Phoenix, both in terms of the manic prices and “value” for what’s being bought. Most of the areas I know (lived in both) are either dumps or unappealing for the price. There are some nice areas (North Scottsdale where I lived and Coral Gables) but it’s a distinct minority.

The Venetian Pool in Coral Gables is wonderful.

Pinecrest and the east Kendall areas of continental park and vineland are pretty decent in Miami. Large lots with tree lined streets. In continental park area one cbs/half acre house that needed new roof, central air, complete updating of baths and kitchen sold for 510k 18 months ago. Another just down the same street just sold for 2 million. Completely updated and asking price was 1.8 million. So it sold for 200k over asking price. Lunacy.

Who bought it? Who is throwing fuel onto this ridiculous fire?

One of the Han people trying to preserve ill-gotten capital?

An American flipper?

A Cuban patriot?

I like downtown Coral Gables, a lot. Key Biscayne is really nice. My prior office is in Miami Lakes, on the border of Broward and Dade counties where I-75 dead ends into HWY 826. It was and may still be nice but heard it’s a lot more congested.

I rented an apartment there in late 1992, It was the cheapest complex on NW 67 Avenue in Hialeah. Hialeah was generally a dump but this area was ok. Problem is, even back then listed rents on this street recall were around $800 for a 1BR. My studio (about 200 SQ FT) was $415. Way overpriced for such a mediocre complex.

Even back then, prices were stupidly high for predominant mediocrity. Some of the places I checked were real dumps. I had a professional job but didn’t have much money back then.

I found metro Phoenix mostly better (lived there from late 2001 to mid-2011 excepting 2004) but found housing prices stupidly high for what you got even before the bubble. My rent in my North Scottsdale apartment was reasonable though and the area was quite nice.

I hear Hialeah has gone so upscale they are taking the bars off the windows of the houses.

I don’t have a clue where the previous residents have gone.

Oh my gosh your comment is hilarious 😂

No, basically…

No on believes the Fed is going to taper.

No one believes the Fed is going to raise rates.

To any amount that will make a difference.

It takes to to tango. Last one standing, turn out the lights.

‘two’

Andrew Jackson was right. We the American people dropped the ball. I am guilty of it myself. All of us are left scrambling what’s left to take while the whole house is burning down.

Godspeed everyone.

When they do raise rates at first it’ll be very slow then ramped up very fast & without prior warning in order to cut out smaller homeowners once again.

A housing price crash would make it much easier for new buyers, even at higher rates.

Of course, current homeowners would lose much or all of their equity and might be “underwater”.

That’s what happens when housing is financialized into an “investment” instead of what it is supposed to be, a place to live.

If you are referring to corporate buyers outbidding individuals, only way to reduce or eliminate that is to kill speculation in housing. Higher rates are one step to do that. Before the GFC, never heard of large scale corporate buyers or private equity buying into housing, only apartments.

There is no option to make housing affordable for most new buyers without gutting current home owner equity.

No free lunch in life.

Sure there is … just look at who were primarily the big g(r)ifted from the most glorious ‘I don’t not CARES Acts of obscenity!

What is the probability of a housing crash (values drop greater than 30%) over the next 3-5 years?

What is the probability that inflationary monetary (and fiscal) policy remain over that same 3-5 year period?

I know where my money is going…

Yes, I agree. And am hoping for a housing crash. But I remember one recession where the rates stayed low for quite a while, but then when they went up they went up very fast and steep. It may have been the 70’s- wasn’t paying attention. I remember mortgage rates in the double digits that prevented many first timers from buying a house. I seem to remember it going from one extreme to another.

Bingo.

2banana

Hand wringing over 1/4pt raise……. ridiculous.

Fed Funds should be up around inflation.

The Fed is stimulating less by reducing purchases. And they call that tightening. Where is honest intellectual inquiry?

The issue this time is inflation.

Inflation was not on the table any of the past times going back for 2+ decades.

It doesn’t mean the idiots and morons in charge will act differently, but it does mean the motivations this time around are significantly different.

Among the differences: the donor class’ interests have always been there but now there is an electorate which is up in arms over inflation (and other causes, but inflation is all the Fed can really influence). In the past, it was the donor class vs. a indifferent public.

At this moment – we are looking at a pretty much historic Congressional power change.

That does mean something, but whether it means the Fed will act on its mandate against its sponsors – it ain’t over until its over.

There’s also the possibility you state: that the Fed does something but not enough. However, I discount this because the Fed doesn’t actually need to do enough. Bezzles pop not always because of reality, but because the collective madness subsides/the people change their mindsets.

A Fed talking tough for 6 months and actually raising rates could very well do the same trick – at which point the rush to the exits would establish its own momentum.

Sold my house in Medford Or. for $420,000 last Feb. Zillow now says estimated worth $450,000.

Bought a house (cash) in Brookings Or (on the south coast) last March, Zillow now says estimated worth $400,000.

I’m sitting pretty. Post card beautiful, cars paid for, no debt, bring it on.

Good to know you got yours.

Millions of families don’t, but I guess they don’t count and can drown.

What a genius you are! Perhaps you should become a financial advisor.

Pride goeth before a fall.

And make sure you wear your mask while going for a walk outside in your “postcard” …Your governor will thank you….LOL

Congratulations if you achieved your goal through merit and honest dealings. This is how American life should be, that you are free to pursue your happiness.

Yeah, what’s with the sour grapes? The guy played his cards well and is free from debt slavery.

Two thumbs up!

Manners.

Sour grape is why wealth inequality is pernicious to social and political stability.

Maybe Biden and Powell had a talk about it recently…

Yawn….

GAZ,

You had a chance to leave Oregon with cash in hand, but you didn’t. Speaks for itself.

I don’t know about Oregon, but most states are very diversified. Most have a big liberal city somewhere and a lot of the rural areas are conservative values people.

I was born in Brookings! Good luck out there it’s beautiful.

Congrats, Brookings is beautiful. Drop down to the redwoods, plenty of hiking, biking and fishing around.

We will probably go sideways from here for 2 to 3 years before the next leg up.

Asset prices are reflecting the ginormous amount of money printed, they aren’t expensive, money has been devalued.

Asset prices are reflecting the ginormous amount of money printed, they aren’t expensive, money has been devalued.

As has labour.

Asset prices reflect the amount of median,mean and modal income transferred (incrementally and exponentially) to the post median cohort.

If you are in any of the first three categories, ‘things’ (food,heat and shelter) are definitely getting more expensive.

Leveraged markets don’t usually go sideways very long. It’s usually escalator up and elevator down or sometimes the downside is a mirror image of upside.

Oh yeah, I paid $350,000 for the Brookings house.

Yes but you live in Oregon the home of out of control mob and more than usual political idiocy….

You know how I know you’ve never been to Curry County Oregon?

Don’t worry, Gaz is safe. Brookings is one of the most out of the way places on the west coast. It is further from Portland or SF than the battery capacity of the longest range Ev so the wokesters will have a hard time getting there. Also it is one of the rainiest towns in the continental US which keeps the transplants down.

Haha, great comment.

Not going to belittle GAZ’s comment, nothing wrong with making a smart financial move.

I bet he made another and is not married.

My ex blew our situation in Sept-20 when we sold after she filed. The zprice on our old house is up 116k since then, about 29%.

I will probably never own again.

Agent,

That fun in the bedroom comes with a heavy price.

Ooh but the Brown legacy lives on ……Just a matter of time till the dynasty recycles back to cali. Oregon/wa just suburbs

WOW!!! Was(is) this moon shot in housing prices all due to low mortgage rates? How do the lenders expect to make any money? In recouped negative escrow when the house values plummet? Who is going to be the final bagholder!?!

1) No.

2) The banks sell the mortgages to Fannie Mae and Freddie Mac, which then issue taxpayer-guaranteed “MBS” bonds to speculators and investors. The real “lenders” may be the taxpayers (the marks for the next bailout).

3) You meant negative equity? Taxpayers on the hook if enough loans go bad, owners jingle-mail the keys to the mortgage services and MBS holders get to unload the property.

4) Unless there are riots to change the 2008 playbook, taxpayers get the shaft again in the form of further inflation and/or destruction of standard of living.

Banks have little to no skin in this game anymore so far as I know.

Anyone know better?

From the GFC dip, looks like PHX and Vegas have had the biggest percentage gains (to date). That (and Tampa) will probably continue due to comparatively lower property tax rates.

Sorry….this was meant to be a standalone comment.

Even if the banks had skin in the game, why would those who run the banks care? They make their money from obscene performance bonuses and cashing out their share options into the bubble markets.

It’s all about individual greed. The bank is just a reanimated carcass that can be used to suck money out of the ponzi, through the corporate veil, and into the boss’ bank accounts.

Same as what most corporations have become. Boeing doesn’t even have any engineers on its board after they fired Muilenburg. Who needs products when you have money printing.

The depositors don’t care because of deposit insurance either. It’s called moral hazard.

I’ve been in mortgage lending since 1984.

Banks don’t lend mortgage money anymore. They’re only brokers (like drug dealers).

Banks haven’t lent mortgage money in 20 years. There’s to much risk and not enough rate of return. Loans are brokered by banks based on politicians (with no lending experience) rules, backed by the American government and ultimately sold to dumb investors who are “guaranteed” by American taxpayers who ultimately get stuck with the tab. I read about a man who had a scheme like this, his name was Ponzi.

Is this a bubble about to pop?

I don’t have the answer. But I do know this… the AMOUNT of money now owed that needs to be paid back on homes, cars, goods, student loans is mind blowing. I hope the income party lasts. If it doesn’t, BANKRUPTCY attorneys will be the new millionaires.

Pay off as much debt as you can because this game of “Musical Chairs” is going to leave a lot of asses without seats.

I rent so take what I say with a grain of salt.

In investing sometimes the best investments are ones with mismatched risk reward. A mortgage with 3% down is like that.

You are levered 32:1 and if you catch an uptrend your rate of returns in current situation is 500% or so and if it blows up walk away with 3% loss and let taxpayers eat it. Fed and congress have messed up.

There would likely now and never have been a 30 YR mortgage in the US without government guarantees because it is contrary to sound banking, especially in an economy with an unstable currency where the short term cost of funding ends up exceeding returns on long term loans. It’s a formula for insolvency.

Prior to the Great Depression, I read that banks required 40% down and only offered 5YR mortgages. That’s all they were willing to offer because the bank’s shareholders and depositors wouldn’t fund anything else.

Yes, presumably this was also due to the regular busts (before the government learned to “manage” the economy) but post WWII economic performance created fake stability that didn’t actually exist. It just took awhile to reach the current manic bubble state.

We can debate whether blowing this bubble was avoidable but I’d say mostly “no”, not if the country wanted the fake prosperity of the last several decades.

The actual (as opposed to mostly imaginary) fundamentals have deteriorated substantially, mostly from long term social decay.

Thanks Dominick, great comment.

We don’t know when the bubble finally pops, but we know it will pop. And we know that when it does pop, one can’t count on job income, house prices, stock prices or corporate bond prices; they can all crash. Short-term US government bonds (and money-market funds built on them) should maintain price but might not maintain purchasing power.

Reduce debt in such a way that your ongoing expenses are minimized (e.g. credit cards first). And be sure to maintain a cash/savings buffer to cover 6-12 months of living expenses* between jobs.

*I’ve personally decided to be extra cautious here because inflation is a huge wildcard “future expenses”.

Just like student loan debt which is a subsidy

of WOKE universities selling degrees in sports

management or theater for 200 K which only support

the professors that teach that useless in life stuff

Look at the difference in SFH vs. Condos. There’s a paradigm shift. Part/full remote work has driven tons of people out to the suburbs. Here in Boston, suburbs went from under-supplied to ridiculously under-supplied relative to demand.

The fed suppressing rates was unnecessary and fueled this huge run-up in prices. But, it is not responsible for the fundamental change in where people want to live. Hopefully with the bond taper (which should have started and finished over 12 months ago), rates will rise and finally cool this ridiculous price appreciation off.

The newly minted Moderna millionaires are bidding against each other in many Boston suburbs. Realtors think the boosters for the omicron variant will be another boost to the Boston real estate market.

Jim, are they paying cash or are they leveraged? If leveraged, are their stocks collateral?

Demand isn’t a function of “wants” but economic capacity. The asset mania has inflated fake wealth while the loosest credit conditions in history have also made housing more “affordable”.

Good comment but I’d suggest that demand is a function BOTH of desire and ability-to-pay.

If someone has a million dollars, that doesn’t raise the prices of everything, just of the things that person wants to buy.

In addition to COVID, there are demographic and sociological reasons for a shift from apartments/condos to single-family houses. (Sociological includes unintended-but-not-unexpected consequences of recent urban policy choices.)

I wouldn’t blame the fed for what goes on in Boston. Boston is a notoriously corrupt city, which has always been run by a democratic political machine. The political machine thrives on having residents dependent on them for work and housing. If Bostonians wanted more affordable housing, they could vote for it, but they don’t.

Chicago is more of the same. And the list is growing.

Petunia,

The Boston political machine is a funny thing. In wealthy Weston and Wellesley, everyone is a Democrat, and they have BLM signs, but you won’t find any black families in those two towns. That is the Boston way.

Early phase and symptom of hyperinflation brewing.

b

How about mayhem and chaos and

I think hyperinflation is likely to be short-lived, with major deflation happening rapidly afterwards. Food, energy and accommodation are the highest inflation areas (much higher than officially measured), the largest proportion of low income expenditure, and essential to life. Any attempt to reduce the supply of any of these much below where they are now is going to result in mass civil disobedience – it always has throughout history. There simply aren’t the law enforcement personnel available to do anything about it this time, nevermind the precedents set recently by eviction moratoriums.

Of course, no one likes to consider the potential for the reaching the extreme in the gap between probable and possible. Having been on that line practicing “stomp and drag”, and preparing to “affix bayonet”, I can only say that the general assumption of the headless idiots is that they will only be dealing with unarmed crowds chanting slogans. The reality could be very different.

Ceausescu is a good example. On 21 December he was still raising his right hand during a speech and expecting silence. He was up against a wall 4 days later.

I would like to see an update of the less splendid housing bubble charts. I bet a lot of those areas are now looking more like Seattle with a current spike above the last huge bubble.

The Fed will taper because the effects on the economy and political elites will be horrendous if they do not.

Just like China is reigning in speculative behavior in their housing market.

The elites have one aim to keep this going as long as possible (too bad forever isn’t a thing for any political or economic system), whether they’re American, Chinese or anyone else. They are elites first and this is absolutely the best time in the whole of human history to be in the .001%. Ironically, it’s elites of the world unite against the workers. Lol. Humanity is ironic.

The sheep will follow everywhere for crumbs, as long as they’re slightly better off than the person next to them.

House prices will fall 20% or so by 2023 that would be my prediction.

They are holding it together by threads by working mirroring policies in central banks and through the global markets.

It will last for a few more years and one fine morning the whole thing will collapse from the most unexpected thing.

I think they might be able to keep it patched up for 1 to 50 years. Who knows? There is a little nominal return still left in the 10 year and 30 year bond. I guess the game is to keep growing debt and play clever fiat games to make interest payments manageable.

They will start having to do capital controls as people will flee negatively yielding savings regime. They probably will try to use tax and regulation to keep dollars from fleeing banks and treasuries into crypto and precious metals.

Someone mentioned hyperinflation. In housing, we’ve had it for 5 years. It’s not if, its now.

There is a vast difference between inflation and hyperinflation.

We are no where close to hyperinflation.

When house prices start doubling every 2 months, that will be hyperinflation.

I have heard the term super inflation which fills the gap between high single digit inflation and hyperinflation. Sounds like super inflation is basically double digit inflation which we certainly have in housing market.

Most of the damage is done in the super inflation stage. There is not much currency value left by the time you hit hyperinflation.

Great comment.

It’d be interesting to apply to the dollar the “half-life” concept used to describe exponentially-decaying objects.

From the Rule-of-72 approximation:

1% inflation is a half-life of ~72 years

2% inflation (Fed Target) is a half-life of ~36 years*

3% inflation: 24 years

5% inflation: ~14 years**

10% SuperInflation: 7 years ***

and so on. (Rule of 72 breaks down for SuperInflations)

* Yes, the Fed’s explicit goal is to cut the value of everyone’s life savings in half during their own lifetime. And they call this “price stability”. That’s not a lie, it’s a Damn Lie as they used to say.

** Per official inflation, we are here. Sustainable?

*** Per realistic inflation (including inflation of housing and retirement-asset values as well as cost-of-living), we are here.

This looks like nationwide keepie-uppie game everybody played at school.Japanese equivalent is “Kemari”

Scan the Yahoo RE news headlines:

-Lake Wobegon home prices soared 101% during last year

-Podunk,MN home prices skyrocketed 89%

-Real estate in Dukes of Hazzard County gained 79%

-Mayberry,NC home prices reached another all time high

Is it a total fakery ? Or probably Fed has secret training camps for RE cash buyers which were given sacks of cash and airlifted to every city,big and small ?

Inflation adjusted schiller is half that. Lot more room to go up IF rates go down.

It’s conceptually silly and dishonest and nonsensical to adjust one inflation measure (house price inflation via CS) by another inflation measure (Consumer Price Inflation via CPI, one-third of which is for housing, based on rents, but ridiculously understates actual housing costs).

It’s like adjusting the Producer Price Index (PPI) by the Consumer Price Index (CPI) to point out that wholesale prices aren’t really rising all that much. It’s nonsense to do this.

I mean, sure, you can adjust anything by anything mathematically. But does it make sense to do so?

That’s why I visit this site, for my personal education.

NO Wolf, it absolutely does NOT!

Many on here do not appear to understand the very clear mandate of, “Lies, Damn Lies, and Statistics.”

For those interested, this was the title of the main required book for the required course for any of the ”social” sciences at what was, at the time, the very best ”public” university in USA, and likely second in the world only to the Sorbonne.

The professor made very very clear the abundance of ”opinion” incumbent in each and every guv mint statistic at that time— late ’60s.

Nothing has changed as far as I have been able to find,,,

NOT to say anything re Wolf’s wonderful summaries, charts, etc., of the ”official guv mint” statistics.

You can prove anything with statistics but only to people who don’t understand statistics, which is just about everyone

Even those who know statistics, or as it is called now, ‘analytics’ or machine learning/predictive analytics today, do not have the time to delve into the numbers to see how the study was done. Sampling is the key. If your underlying data has not been sampled correctly, then it’s basically garbage in, garbage out. And that is before all the mathematical gimmicks people do to massage their numbers. Today’s political polling is a good example of this and why it is so bad

Probabilities and Statistics is a wonderful lesson on manipulation without causality. It is thrown around in schools with absolutely no moral guidance. It’s a shame to see the demise of structural, economical, and political systems all due to a bad math equation taught half heartedly by some educator reading from a prompt. We would be better off learning critical thinking skills.

Look at housing versus median household incomes. The ratio is either the highest ever or only lower than housing bubble 1.

Mortgage rates are lower versus housing bubble 1 but other ownership costs are higher or much higher.

Monthly cost of ownership varies by locality but affordability is nowhere near what you imply.

Yes, I have also seen the NAR’s propaganda chart on housing affordability.

Housing is a terrible investment taxes insurance upkeep really never appreciated,money devalued but it makes a great nome to raise a family this will end bad also pay attention to stock selling bezos,musk ,Microsoft ceo deleveraging

“The Stock that is laid out in a House, if it is to be the Dwelling-House of the Proprietor, ceases from that moment to serve in the function of a Capital, or to afford any Revenue to its Owner.

A Dwelling-House, as such, contributes nothing to the Revenue of its Inhabitant; and though it is, no doubt, extremely useful to him, it is as his Clothes and Household Furniture are useful to him, which, however, make a part of his Expense, and not of his Revenue.”

Adam Smith, “The Wealth of Nations”

Then he backs his claim with many examples with numbers and sums in pounds and shillings…

Many Victorian Gentlemen were driven into bankruptcy after buying London RE in XVII Century.

Brent,

Though you are likely correct in re various ”gentlemen” being bankrupted, one must insist that Victoria was 19th century, not 17th.

And SO many of both of those centuries were subjected to the same sort of corrupt political dealings by the oligarchies of their times, that it does make it very relevant to these days.

Recent reports indicate that in spite of the very very well hidden double and more layers of dead end corporations hiding it, ”the crown” continues to own most of the property in London, and is likely to continue so ad infinitum…

@VNV

=one must insist that Victoria was 19th century, not 17th=

NO EXCUSE,SIR !!!

Also I want to share with you one deep proverb from Victorian times:

“When Poverty comes in at the Door, Love flies out at the Window”

One of my high school pals “bought” a house which he can not afford.Recently he lost his job and they all live now on money extracted via HELOC.Mood is absolutely funeral.

I exercise my right to remain silent,Reality is the best Teacher 😁

Indeed. Only rentals should be counted on net worth. Main residence is consumption, a liability.

I was trained that the average person needed four assets in life. Cash, bonds, stocks and real estate. If you purchased a house instead of renting then no other real estate investment was needed. The idea:

cash = emergency fund

treasuries = deflation protection

stocks = for normal times

Real estate = inflation protection

ZIRP has screwed things up by inflating assets and adding systemic risk.

For old folks like myself and some of my friends, home ownership (no mortgage) is an investment that can be used for long term care expenses. I see this use of home equity happening in my neighborhood with folks that end up not being able to take care of themselves anymore.

That’s one example of the “end game” with real estate.

I was trained that you needed willpower, skills, knowledge, and equipment. But then, I was trained to be down in enemy territory with no food and lots of nasty people with guns chasing me.

I have a suspicion those things will be more use to me in a couple of years time than a bunch of bonds.

Mind you, I also got the financial training. I have paid-for real estate and cash. My financial advisor (I like a second opinion) stopped trying to talk me into buying stocks and bonds 5 months ago. He’s moving into cash himself now. I expect he’ll be asking me how to do some survival stuff sometime next year ;)

Unless a portion of the primary residence is used as a rental. Homeowners can get a roommate(s), boarder(s), or convert a portion of the house into an in-law or apartment. I met a lady this year who set up a spare bedroom in her house as an airbnb. I have an additional dwelling unit in my single family home that is permitted by the town. The income pays for the property taxes (in an HCOL Boston suburb).

But then you have to deal with being a landlord and the latest crazy pandemic conditions, such as the eviction moratorium. Dealing with tenants sucks.

Comparing the value of have a home to all other investments makes me think you are wrong…

Wolf St. Where Adam Smith rises from the dead to contradict himself.

GAZ, can not fault you for playing your cards right. In gambling parlance the house always wins and many people out there are losing big time right now, unlike you.

A word of warning though, people who have been left behind and feel cheated by the system are prone to behave irrationally……. and you are surrounded by them. We are all surrounded by them.

Dave,

I think you are right as in the US system as politics is the vehicle that those left behind balance out growing the pie vs sharing the pie.

Owners have controlled things for a long time and maximized profit margins by flooding US with cheap labor and off shoring manufacturing. Tide is beginning to flow the other way.

You have to finance it, keep taxes and insurance paid, maintain it and keep it updated. That’s about 3% interest cost and 3% everything else. So it’s minus 6% plus if housing goes up 6% you lived there for free. If housing goes down 6% it’s cost you 12% of property value.

When is the bubble going to finally burst? How long can the Fed keep dragging it out before they can no longer?

Probably never or close to never, if it takes 50 to 100 years to turn, it might as well be never in one’s lifetime..

The world isn’t likely to remain stable for anywhere near another 50 years to keep the housing bubble inflated.

It’s a false stability coinciding with decades of fake prosperity and the sunset of the Anglo-American era (roughly dating from 1815).

Nobody knows, but we will wish we were prepared when it comes. History tells us this will end badly.

Firstly, the everything bubble is worldwide, so the usual flight of capital which accelerates the crisis in one country isn’t going to happen. Secondly, there are no fundamental differences between major governments – they are all primarily in it now for the power and the money, not some political ideology (work off what they do, not what they say). What will bust it all open is a major crisis coupled with total idiocy by a major government or three.

Now, Covid could be that major crisis, and goodness knows there are enough total idiots in government, but predicting what idiots will do is not possible. About the only things one can be sure of are: that there’s less than 5 years, that the media worldwide will attempt to suppress any information that would help predict it, and that it will happen very rapidly. If we are lucky, one region will collapse first and give us a month’s warning, but that first region could be North America.

Rest of the world might think it good to see N.A. going down, but it won’t turn out so pleasing if it does. There probably wouldn’t be a single capitol city left standing in every other nation on this dirt ball. NBC is not a game to be played by anyone, borne out by this recent taste of that middle option whether accidental or planned.

Agreed. It’s all linked now. Any major player or 3 medium ones going down will drag the rest with them.

I’m thinking it might not be regional. I’m wondering how much of a WW spiderweb the Chinese RE development companies are as a group and if it might be a tip of an iceberg.

Well, at this pace of expansion, the bubble should pop soon. Stock prices are up 30% from 2019, while problems in our economy only grew. The helicopter drops have started. Won’t be long now. I expect a popular uprising to protest high prices, including runaway housing prices. The media will focus on it. Government will have no choice but to prick the bubble.

Government wants to return to 2019, but we cant. Prices are much higher now, and they won’t fall without a bang.

This is all starting to remind me of the last 70’s with the inflation and skyrocketing energy prices. Back then we had a neighbor who was a big home builder. He had an actual stream in his house, 3 planes and 2 helicopters ( which he flew himself and sometimes gave me rides). Then Tall Paul put an end to inflation with high interest rates. All the home builders were crushed like bugs. Our neighbor was broke and living in A trailer with one rusty pickup in a very short time. The same thing will happen to the house pumpers, re investors and flippers this time. Except the crash will be so bad most of them will be glad to have a trailer and a rusty pickup.

First rule in life DEBT FREE!!!

If you can borrow money at an interest rate lower than inflation, debt can be very useful.

hence the real estate boom.

Why?

Why is the Fed lending money at 3% for 30 yrs by buying MBSs…..3% below current inflation…….who else would?

And its not like they are saving the real estate market….it is White hot!

Cui Bono?

last time we have inflation near current levels, the 30 yr was 6%. (1999 and 2006)

Wouldnt that be a good question for Powell…..

can we submit questions? ha

That’s true, but the main thing is to have the debt structured so that you always can make the payment no matter what comes.

Taking on a mortgage is saying you are going to have income available every month for 30 years. That’s usually through about six recessions. Not as easy as it sounds.

Yes, for those who maintain moderate leverage, live within their means, and have “reasonable” economic stability.

Most people don’t even come close to meeting all three conditions.

Given a choice today, I would buy my primary home with a mortgage at 2.5%, vs paying cash.

I expect government insured CDs/Savings accounts will eventually be paying 4+% to cover inflation. It would not make sense to pay off a mortgage at 2.5% when a 5-10 yr CD/savings account is paying a historically typical 4%-6%.

It is true that if you do not have the cash to put into this savings account, a severe recession with a job loss would be very risky.

In other words, if you already have the cash, you have a fairly low risk means way to leverage into a primary home.

The lenders would suffer. Fannie and Freddie would be bailed out with taxpayer money.

A disclaimer: I am likely somewhat biased since my parents and most of their neighbors purchased houses in the early 1970’s with 30 year mortgages at 6%.

The high inflation of the late 70’s/1980’s meant they could put their cash into a savings account at 10%-15%. There was no financial incentive for them to pay off the house even though they had the cash.

They finally paid off the house in the early 90’s when savings rates were comparable to their mortgage rate. They should have purchased 30 year T-Bills at 15% in 1981 (I am waiting).

They had no incentive to move during this time or after due to a low mortgage rate and Prop 13 locking in their property tax.

As an added benefit, the high inflation also increased the value of their primary home by 4X over 2 decades. Maybe also because nobody wanted to move with low payments and locked in property taxes.

Fortunately, they kept their jobs. Otherwise, the story might have been different.

sounds made up tbh

Hopefully he learned his lesson and is a better person for it. We are not what we own.

It would be interesting to see charts with sales figures after the various interest rate adjustments starting from say the mid 70s. Everything we’ve seen in the last 1.5 years in the real estate market has happened with nearly FREE money.

Organic demand isn’t going to be affected by reasonable interest rates. When the market can’t keep going with out free money to party with…..that can’t be healthy.

Even Yellen said yesterday that US can spend freely because it’s getting money for less than zero while the printer in chief was sitting beside her.

That reminds me of someone.. I bet Yellen is addicted to shopping. In general. I mean, someone who walks into a mall and can’t walk out without spending everything in her wallet on necessary crap.

*unnecessary

I placed an offer earlier this week on a house in northern Phoenix for $405,000 that listed at $350,000. Fix and flip (albeit renovated and 5 miles from two major shopping areas). Was told the accepted offer was $420,000. Perhaps I dodged a bullet? But living at home with parents at age 30 and I do not want to spend $2700 a month for a 1 bedroom 700sqft apartment is not a great choice either. At some point this has to price people out and create a wave of vagrant’s across town. In some ways I’m blessed to have flexibility to make a move, but on the flip side I’m kinda screwed in terms of having a reasonable place to live.

Phoenix Millaial,

According to the chart, in 2012 Phoenix properties were as worthless as dust and to dust they shall return.

Isn’t LUCID near that area and expanding manufacturing? They are the real deal – the Apple of EV unlike Tesla with terrible reliability ratings.

Phoenix..

Your generation should be OUTRAGED at what is going on.

The elites are pulling up the ladder on you people.

You cant save……for inflation and zero rates is a loser

You cant buy a home……for the prices are skewed by terrible Fed policy.

And your generation is being saddled with 30 Trillion in debt …more coming….all to FUEL this damaging environment.

Tell your friends to WAKE THE EF UP.

Fed policy is pulling wealth forward from the future to the present to fluff assets and stocks…..previously purchased by the elites and the Fed buddies.

It wasnt long ago that it was understood that

IT WAS INCUMBENT ON EACH GENERATION TO PAY ITS OWN DEBTS.

Pre 2008…….

What changed and why? Who hijacked the Fed? Follow the money….

“Pulling wealth forward” is too nebulous. I prefer “destroying the future of the young to pad the bank accounts of the already disgustingly wealthy.” It leaves ZERO to the imagination.

I’ll second that. Also, you may have been outbid by a large ibuyer. They will put in bids for $20 to $60K above the highest bid.

Homes should not be an investment vehicle for large and global corporations. Yes. Your generation should be OUTRAGED at what is going on.

Ok I’m outraged!

Now what?

“We have four boxes with which to defend our freedom: the soap box, the ballot box, the jury box, and the cartridge box. Use in that order”

Stay at home and keep stashing cash. You are too young to have seen things sell at distressed pricing. It will happen unless we need to burn all history books. When it looks like the world is ending and it’s hopeless, you will find your best buy if you have the nerve to pull the trigger

Now is the time to do your homework. Find the neighborhoods that you desire. Get to know the market inside and out.

Keep stacking cash that loses value monthly to inflation? People were saying that in March 2020, and missed opportunities to buy at <3% interest rates and prices 20-25% lower than they are today.

I understood that he was living at home so that should mean he can stack at a fast rate. Warren Buffett has $150 billion in cash, so it must not be all bad.

Cash is stacked to buy things later. Work out the non-perishable stuff you need and can store, and get it now. There is no better hedge against..anything.

sc7 is just another housing shill who willfully ignored the lessons of the past. My guess is he’ll disappear like a fart in the wind once prices crash. He’s probably levered up to the teeth in shacks, just like Outside My Cardboard Box, Joe Scabs, SoCalJimmies and all the others who show up here to gloat over their pressboard boxes.

It was hard to buy bc ppl got outbid

@Depth Charge is a bitter renter who will endlessly complain and hope for “The Big Crash (TM)” coming in 6 months for the rest of his life. Perhaps you have missed my posts stating that I think this is unsustainable, and I wish prices would come down for people I know who have been priced out of where they want to live.

I’m in no way shape or form a “housing shill”. As I have stated many times before, I own only one home (my own) that is very modest, with a large equity buffer that is a fraction of my net worth, and a payment that is a small DTI on a very low interest, fixed-rate loan that I keep only because it is below inflation.

Keep making up things about people who disagree with you though.

Also… my house is a custom-built solid, slow-growth wood structure from the 1960s before pressboard existed.

“Bitter renter”

YAWN.

Sounds like a good reason to move to another town or city.

Phoenix will go down the tubes

I was talking to this Indian guy (from India) and he was telling me how the Indian guys working for tech make good money and don’t mind spending the money on a home even if overvalued. Something to keep in mind. These guys are getting stock options and make a good salary, they can swing the monthly mortgage. The question is when the economy goes south and if their homes decrease in value will they mail the keys back to the mortgage company? I don’t think so as you have to live somewhere. I can see this with people where the mortgage takes up a greater percentage of their monthly income.

Other scenario is that the dollar is getting devalued so much that people are rushing to put it into something touchy-feely vs. stonks. Interesting times.

I’ve seen that in the bay area, 2 income family, 1 paycheck goes to paying the mortgage. What they don’t realize is that jobs and buyers usually disappear around the same time. There will be a correction in IT and when that happens, these guys will be hit pretty hard.

That family you mentioned. If they break a shoelace, they lose their house. Everything is fine, until it isn’t.

No one saves for the “rainy day” for the Fed has created a situation where savings is PUNISHED. This, IMO, is unAmerican.

People should seek to be self sufficient…..that requires an emergency fund…..ie savings. But that is punished.

It is the financial history of this country that you could choose to scrimp and save your way, albeit slowly, to some sort of financial stability. No more. Never happened before…..why now?

Save things, not cash. Your coffee machine will break in 3 years. A second one bought now will not deteriorate in its box, and will be a darn sight cheaper now than in 3 years time (and probably better quality too). Governments have, historically, not “requisitioned” spare coffee machines; though they will grab your bullion.

You get the idea.

Yea, this whole internet/tech fad is definitely going to fade, and our economy will return to good old manufacturing, oil and coal. AI and data science are just a big scam.

/s

People have a tendency to overpay for new technology. The problem is there is only so much of the economy to gobble up. Nominal economy grows at 4% now so high growth rates have to slope toward nominal growth rate eventually. Once your market cap is 2 Trillion. How many times can you double from there? Not many.

People buying today are far more solvent and financially stable/qualified buyers than the 00s housing bubble. There are definitely some risky/loose loans out there, but they’re not as risky, and a much lower percentage of volume. In the Boston area, you will not win a bid unless you have at least 20% down. Last time I sold here, offers had down payments from 3.5% to 60%. I didn’t even look at any offer that wasn’t at least 20% down. This was for a small home in the suburbs.

The rate of increases is absolutely unsustainable, but given the demand shift and lack of supply [i]in areas people want to live[/i], combined with the devaluation of the dollar, I don’t see a catalyst for a sharp dive in values.

Interesting point, care to elaborate a bit. You did not look at offers that weren’t atleast 20% as a? seller, or banker issuing the loan? Why would a seller care what the other party puts down, as long as they get their money, its the buyer and the financing organization that’s got skin in the game right? And the bank turns around and pawns off the mortgage to the government, so they are in the clear. What am I missing?

Probably means he would only deal with a “qualified” buyer.

SS:

The easy answer is: If the buyer doesn’t have at least 20% down, the deal can blow up if the property doesn’t appraise…. the buyer may be able to juggle the money around and still close. Captain 3% likely can’t.

“People buying today are far more solvent and financially stable/qualified buyers than the 00s housing bubble. There are definitely some risky/loose loans out there, but they’re not as risky, and a much lower percentage of volume.”

This is an outright lie – a fantasy you just made up in your own head.

If what you say was true, then the foreclosure flood after the GFC never would have happened. People needed a place to live then too.

They walked away anyway.

The better reason for no foreclosure tsunami is that the government will declare an “emergency” and grant another mortgage forbearance. They did it with COVID and now that the precedent exists, have incentive to use it again.

This is why I would hesitate to be a landlord, either anywhere or at least in more progressive areas of the US. No telling what justification will be invented to steal your property.

In 2008, mortgage holders walked away when the homes went underwater and they either could not pay due to a job loss or had no desire to keep putting money into a losing “investment” with no equity they did not even have 20% down.

The government response was to bail out the banks at that time. The mortgage holders lost their homes.

During Covid, people lost their jobs and the government bailed out the mortgage holders with forbearance and hopefully people kept their homes (tbd). The lenders will still recover their money eventually with restructuring the loans (likely with no loss of interest).

I think this would have been a better way to handle the 2008 GFC.

If housing does crash again, what will people do?

1) Will they walk away and foreclose because they see the house as a “losing” investment? Do they have enough equity to not walk?

Or

2) Will they be grateful with a bailout for being able to keep their “forever” home during a job loss and negative equity? And be willing to hold on for a restructuring plan?

I view my primary home as a place to live and not as an investment. I would sell all of my loser stocks before I walked away from my primary home.

I agree that with a rental, there is much more risk when rent forbearance prevents the owner from collecting enough to cover the mortgage, insurance, and taxes. Maybe this means more rental properties will go on the market to become primary homes.

Is the dollar being devalued? I keep reading the dollar is rising versus other currencies.

Might be the fear trade. Some people say the dollar has one more crisis that it will remain reserve currency and then it’s toast to be replaced with a basket of currencies.

All currencies are being devalued, hence global asset price inflation measured in currency units.

USD just being devalued a bit more slowly.

It’s a race to the bottom. Bottom = people without assets revolt.

Unless this time is a bit different due to secular demographic decline and corresponding asset deflation, which is possible. Happened after the plague hit Europe.

More than just the cost of interest goes into the decision to buy, sell, walk away from a home.

Is the rent in the area more than your current house payment?

Is your job stable, or do you need to move, or did you lose your job?

Do property taxes go down along with the possible sales price? Or does the tax authority increase taxes because they need income?

If you have a loan at a low rate and taxes go down as the value goes down, you have a stable job and rents are still high – you don’t jingle mail the keys. You count your blessings.

Not all states allow “jingle mail”. Some states only allow non-recourse for first mortgage purchase loans. If you refinanced or HELOC’d, odds are you gave up your non-recourse loan. Most people don’t read the fine print.

“The Los Angeles index value of 366 means that house prices have soared by 266% since January 2000, despite the Housing Bust in between”

Well, there you go, no wonder all the house humpers I know will never shut up about housing is a winning proposition cause so far they have been right. 21 years later, one giant bust and it’s still 266% over, geez.

Maybe thanks to the FED and government intervention this is the new normal. I mean close to quarter of a century and we’re still way above ratio compare to income or what the norm should be, it’s starting to get more and more challenging for me to envision what this big giant black swan will look like or if it will ever appear to correct the market back down to reality somewhat.

On the other hand, still too stubborn for me to buy into this narrative of housing going up forever especially more and more you dig into the data but there comes a point maybe I’ll just have to turn off my brain and turn into another house humping lemmings and jump in to a buy a place and overleverage so my kids can have a decent place to live in….guess they’ll have to enjoy eating ramen everyday just so daddy can buy that house to live the American dream…what a joke.

Change what the Dream means for you. And for your kids.

Yeah the American dream of owning a 70k dollar pick em up truck with a camper shell on it so you can raise a family in it.

The new American dream!

That beautiful 96 month loan…

I literally ate ramen myself for awhile and kept making my home loan payments while the refi people were knocking at my door (last time around, 2000s). I’m so glad I took that route, now in a SoCal home almost paid up and still not accepting the debt mongers beating at the door. I know my values. I set my baseline low, I am totally not spoiled, and then so many things are upside surprises across the decades. That’s how my folks raised me.

Did you know that ramen at the Dollar Store is $1 for a 5 pack? 20 cents a pack.

That is what I paid back in the late 1980’s when I was in your situation.

There is no ramen inflation.

I only answer the refi phone when I know rates have dropped more than 1%. No cash out, low fees and the term must be shorter than the current term. Lenders can create arbitrary terms (ie 7 years, 13 years). I don’t want to be 75 years old refi’ing my house for another 30 years.

Breath taking, those charts. Yet another reminder of how the rich continue to get richer. Boom…bust. Sell high and buy low for anyone with the nads to play and the cashflow to make it through the down swings.

This next one will cull the hurd that is for sure but I wouldn’t bet much on when it turns…

I just don’t know how this facade of a “healthy economy” can continue. Just walking the corridors of San Francisco you can’t miss the “For Lease” signs. the boarded up windows and doors of businesses, the nearly empty streets of the financial district, etc.

The mid-Market street corridor, which was becoming a beacon of light illuminating the wealth courtesy of Twitter & other big high tech firms is dead. Shut down. Abandoned. The street people, the homeless, drug addicts and mentally ill, while having never left, now completely dominate that human landscape.

I just walked the length of Mission street from it’s beginning all the way to 14th street. Just poor, homeless, wretched souls line the streets. There are a few eateries open but basically commerce is dead along the entire stretch.

Union Square. There are a few blocks where high end retailers are open and some Xmas shoppers are present but everywhere you look “For Lease” signs hang in front of empty storefronts.

In the financial district there are a lot of banks still open but so many restaurants are shut down. Closed for good. Looking it all over I had the foreboding feeling that soon enough only large corporate entities would be serving up lunch for the working crowd – if they ever return. I walked through the Crocker Galleria, once bustling in the heart of the district. Every single store shut down with the exception of a few empty eateries

And this is San Francisco! One of the great wealth centers of the country. From here (and not just here; there are a couple of other cities) wealth distributes across the country. Without Silicon Valley (metaphorically) what wealth does America create (not counting military)?

So if things are collapsing here what does that portend for the rest of the country? It seems to me that every vacant storefront, every failed high end apartment/condo/hotel complex has debt attached. And that debt is connected to more debt in this great complex web that’s been created in the asset bubble run up.

We used to say money doesn’t grow on trees but the Fed seems to have given it it’s best shot at proving that a myth. The problem is when the trees dies they take the forest with it. I’m seeing a lot of dead trees.

You can forget brick-and-mortar retail. That has been dying for years. Macy’s shut two of its three stores in SF well before Covid. Many others did too. Small neighborhood shops were all dead. Now there is the empty-office syndrome (due to working from anywhere), and nearly all the shops and many restaurants that supported office life are shut down. So that made retail worse.

But check out the non-office parts of SF: They’re thriving: North Beach, the Marina, Russian Hill, Aquatic Park area, Cow Hollow/Union St, the area along Divisadero from Pacific Heights to Geary, the Fillmore corridor… Lots of places like that. These places are hopping. That’s where the workers from home are hanging out.

I do see that. It’s a visible reality in my hood. The point I’m trying to make is that all that real estate is leveraged up with loans dependent on revenue streams. And if you don’t see it coming back and I don’t see it coming back then maybe it ain’t coming back. Office space, B&M, even residential leasing will take a big hit. There is a lot of real estate ($$$) here. Cascading defaults may have some serious blowback in the employment sector as well.

Yes, I think you nailed it.

Chicago heading that way.

What was once bustling in the financial district………dead.

The bar/restaurant that was once the largest seller of alcohol in the city, despite closing at 8pm during the week and closed on weekends….in the financial district…….closed for good.

The bifurcation of this nation can be sorted out more and more in this fashion…

there is URBAN and then there is the other. Its gonna be a complicated civil war….not based on States, and no uniforms.

I find it hilarious and interesting how Chicago continues to lose the most number of people due to net migration every single year, have some of the worst taxation in the country…. and yet there are still like what 9 million people in the greater metro Chicago area? Amazing.

Chicago is a Shitehole. I want to get out. Restaurant tax is 11.25%, highest prop taxes, sales tax 10.25%, terrible crime everywhere, corrupt politicians, expensive housing bc of high taxes, racist a d misogynistic police force…. Cold weather, A terrible place to live. Where to go?

It’s nice and warm in Austin. Great live music scene too. Housing may be a better deal in Chicago, but what the heck. Property taxes out the wazoo in Texas, but ok, no income taxes.

Whatever you do, don’t come to San Francisco. We’re full. And it’s a terrible place, as you can read every day everywhere.

LOL, Wolf wants to have SF all to himself.

I lived in SF for many years in the mid 2000s. It was a nicer place to live then than it is today. Probably won’t ever live there again though.

MarkinSF

Same here in Swampland. Nearly every Chinese restaurant except for e few take out joints have gone out of business. Most mom & pop brick & mortar retail is bankrupt, even in the close in suburbs. For lease signs everywhere. Homeless camps have expanded to better neighborhoods. Its a complete disaster.

Silicon Valley creates a lot less actual wealth than most people presumably believe.

Look at what these “unicorns” and more recent (since 2008) corporates actually produce. How much of it is “meaningful” economic production?

Others such as MSFT I’d describe as substantially rent-seeking parasites. It generates a lot of revenue, makes a noticeable number rich through it’s inflated stock price, and creates a meaningful number of high paying jobs.

Concurrently, it’s core products (Windows and Office) don’t provide much more utility to most of the user base since I first used it in 1993. So, it’s my contention that the economy would be no worse off productivity wise if no one had to upgrade.

It’s a simplification of reality (yes, I’m aware of the need for security patches and performance) but the point I am making is that this is an example of where this entity has extracted a lot more economic value from the economy in recent decades than it has input into it.

It isn’t an isolated example either.

MSFT has a lot of garbage now – telemetry and “AI” etc. It’s gotten to the point I’m only willing to run Windows in a VM, due to privacy concerns.

But I do still run Windows, because they still make very good dev tools, have embraced linux interop with Windows Subsystem for Linux, and their dotnet-core framework is unrivaled.

Eyeballing the charts, percent change, bubble 2 as of September minus bubble 1 top, divided by bubble 1 top, approximate:

LA: 33%

San Diego: 44%

Seattle: 78%

SF: 55%

Portland: 67%

Miami: 14%

NY Metro, Low Tier: 23%

DC: 12%

Boston: 56%

Tampa: 25%

Denver: 100%

Phoenix: 26%

Las Vegas: 13%

Dallas: 108%

How many of the cynics here are renters? Keep telling yourselves the end is near. Been reading about it since 2014.

The end was near in 2006. And when the end came, it ended very badly for millions of homeowners. Look at the charts. See similarities?

And people who had cash in 2011 and 2012 could get some incredible deals.

In CT after 1988, house prices dropped about 50% in a few years. They took a full 10 years to reach the 1988 peak again. Some people were upside down in their mortgage for a decade. The American public has only a 10 year memory. You can fool them over and over.

10 years memory? You are giving them too much credit. I would say about as long as gold fish since most already wrote off or forgot about that little crash in the market from just march of 2020. Then again it could just need willful amnesia, forever up will tend to do that to people..believe they call that hot hand fallacy.

2008 housing crash? Pssh..might as well be 1908 to most, only us “doom naysayers” have longer term memory.

10 year memory? I have to agree. Wait until the next big hurricane blows across Florida and there will be exceptionable housing deals again. Just like last time….and the time before.

“And people who had cash in 2011 and 2012 could get some incredible deals.”

Yes. I was living in Denver at the time and the opportunity was substantial. For a 12 – 18 month period (roughly) the RE market was completely stagnant and cash buyers had all the leverage. The sellers had little choice but to accept the low offers. No other offers were to be had.

Another “hindsight is 20/20” observation. I still believe the current appreciation levels are unsustainable and there will be a reckoning. Another opportunity period may materialize in the next few years.

That was the only why we were able to buy either of our two houses: on the dip, owners’ hurting to sell. We sold our first house ‘high’, rented, waited, and then bought ‘low.’ Otherwise, we could not have afforded neither house.

One person’s loss is another person’s gain — at least in real estate.

Some don’t want to believe because it contradicts their preference. Or, they are ignorant of history.

Last go around, the stock market measured by the S&P 500 lost 58%, the real estate market tanked in many markets and millions lost their jobs.

So for these people, first their net worth crashed, then they lost their job, and then had their house foreclosed. Move along, nothing to see here.

Millions have probably never recovered but that’s lost on the believers. It just depended upon their personal circumstances but it’s naive to believe it can’t happen again or only happens to someone else.

At the end of 2021, the demographics are worse for a lot of these people. Anything close to 2008 and they won’t have time to recover (again).

For anyone who is aware of the market they are buying into, doesn’t mind buying into a bubble, and can afford it, nobody is telling them not to buy.

Problem is, most aren’t in a position to take this kind of economic hit.

I have been a renter for 20 years and I did OK. Money not used in a house can be used somewhere else and you have liquidity and flexibility. Plus most houses are too big for a single individual.

Depends on how you calculate your returns. My original down payment has quadrupled based on the appreciation of my home over the last 7 years and because of the low rates the carrying costs on my home are significantly less than the rent I’d have to pay to live in my home. All while I plow money into equities which are also over valued. We could take a 50% hit to the housing and stock market and I’d still be in the green. And this has occurred all while the chatter of an overvalued maker has been raging in the background. Like I said before keep telling yourselves the end is near. I’ll keep investing rather than trying to time the market. We all know how that plays out for most people.

Unemployment lowest since Reagan. According to Christine Romans, CNN’s chief business correspondent, the last time we had that kind of growth was under the Reagan administration forty years ago. Unemployment is also down. The economy added 531,000 jobs in October, dropping the unemployment rate to 4.6 percent, the lowest rate since November 1969

The economy is booming. Now to fix the bottlenecks, restore competitive pressure and drop the energy prices.

1) The new OmiXi spread globally.

2) More WFH, more tech, more games, more obesity, more online pickers, ex UPS – either a union strike, or higher shipping cost, followed by layoffs.

3) Macy’s might test T1, T2 of the whole move from Mar 2020

to Nov 2021.

4) Efforts/ results : invest in instant delivery ==> deliveries are usually late.

5) Try to deliver a Xmas gift to Europe or Japan.

6) Meanwhile, Indian high tech colonies spread to the most exclusive

RE in US.

7) Their groupies buy houses on the beach. The top transfer knowledge to India for lower cost.

8) It signal an industry LT decline. Lower cost pyramid base, larger size, more talented students. hungry young generation looking for action, India will compete with their pals in US. The rest, the old,don’t matter, they will be recycled anyway.

9) It happened with China.

Before the tech transfer to India and before China, it was Israel transferring tech. All the tech of the three countries can be traced back to the US.

I don’t know, India seems to be running double digit inflation for over a decade. Things aren’t so cheap there as we think. When the SHTF they devalue their currency and the whole this is reset.

Nationwide rental vacancies are low with rents rising. Some are like stuck between a rock and a hard place. Would be nice if I could buy a home in Florida for pennies on the dollar like in 2012, but it is not happening.

I did not sell my home. I need to live in it.

See: FRED Rental Vacancy Rate in the United States

It’s not a bad strategy to buy a good asset in a recession and never sell it whether it’s a nice home or a high quality stock.

For the first time in the last 5 years a lender put the pressure on the appraiser to make a deal go through on a completely illegal property configuration. They must be getting desparate to make deals as volume continues to fall off. This is something new, and maybe a part of a trend. I hope not. Prices are starting to level off here in Swampland, as shown in the Case Shiller chart above, even with the lack of inventory for sale.

LESSON #1: How to get all housing ownership into the Corporations that also own the Banks that own the Fed:

1) Your FED operation lowers interest to almost “0”.

2) Your Banks loan out huge loans to the Corporation, you own, that will buy every single home, apartment complex, and condo complex. You buy these units is bulk, all cash, thus simplifying the purchase procedure. Individual Americans can never do this.

3) Your Corporations, you own, have no downside. They are too big to fail, and if they need money, your FED and Banks just extend and pretend. Or is that pretend and extend.

4). Your FED buys all the new Mortgage Backed Securities, thus providing more money for your Corporations, that you own, to buy more housing units.

5) Rinse, Repeat.

Now, the people own nothing. They own no homes, etc. They will rent from you (Corporation & Banks & FED) and they will be happy, or shot.

Just got my notice that my loan was sold to Fannie. Your note does bring to mind USSR back in the day with government owning it all. How did that exercise end?

Fannie Mae buys mortgage loans from lenders to replenish their funds so the lenders can continue making new mortgage loans. That helps keep affordable financing available for homebuyers in the market for a home.

MA: True Stoicism! Well said

Could the millennials come to the rescue and increase demand after their students loans are wiped out?

The next expansion of the bubble is in sight. Fannie and Freddie now guaranteeing $1M houses in my area with only 3.5% down.

Why is government subsidizing extravagant home purchases? What is the public gain? It’s a perfect example of government getting too big, trying to do too much. Incentives have become distorted. Nobody is steering the bus.

I started looking to buy a house in 2012. My offers were all cash. I was front run by investors (Blackstone) who were connected with the banks. I was extremely frustrated until I found a beater house with a guest house that was only partially permitted. Even that one took a stroke of luck to purchase. The little guy is sooooo screwed.

The Housing Market is well tied into the Current ecomomic Crisis I think with all the Inflation created by the Fed & subsequent pocket lining going on . This is always the Case but not so with Huge Inflation most often . I am wondering just if ever this New Smash and Grab Epidemic will also have ” broadcast ties ” to This same serinaro : the Fed / Inflation / Home prices / Etc . ( was my first thought when it started )

Smash and Grab is indeed a Big deal > I am reminded of the Demonstrations at the White House , Trump Etc

it all seems tied in together to the ecomony . Is Wolf going to have Smash and Grab Charts upcoming ? it seems pertement

as that’s a part of the economy is it not ? .

Seems a Good thing rather then a bad thing because now finaly perhaps someone will become forced to do something how Ironic what the USA has going on now

Good Times / Bad times / Smash Times / What’s Next humm

Hi Wolf,

It would be very helpful to see the rent:purchase price ratios for each of these markets, if you have access to this data. In my area (suburban D.C.), rents have shot up tremendously in the past 6 months.

Kevin

1) China silk road plan to build 3,000 projects in 140 countries

worth $3.7T. China encircle the world to enslave poor countries, to establish military bases and bridgeheads.

2) China already piled $300B silk “toads” assets, but Idi Amin have struck back.

3) China gave Pakistan a fist full of nuclear weapons.

4) Europe cooperate with China, but with more humane terms.

5) The G-7 plan to spend $40T on global project. It’s a feint.

6) The global paper infrastructure Backwardation.

7) Amazon silk road Backwardation.

8) Case/ Shiller RE….

Neofeudalism

Yes, m’lord.