Sky-high availability rates. The gap between “asking rents” and “effective rents” widened further amid hefty concessions, free rent, and lower “taking rents.” Tenants have negotiating power.

By Wolf Richter for WOLF STREET.

Office markets had issues before the pandemic. For example, the Oil Bust made Houston the worst office market in the US starting in 2015. And a construction boom across the US put large amounts of office space on the market, under the calculus of insatiable demand. But during the pandemic, companies determined they wouldn’t need that much office space under their hybrid work-from-home models and dumped empty office space on the sublease market.

These companies are continuing to pay rent but want to cut their carrying costs, and they try to sublease the space to some other company, and they undercut landlords that are trying to direct-lease competing office space. Huge sublease inventories are the hallmark of this office market crisis.

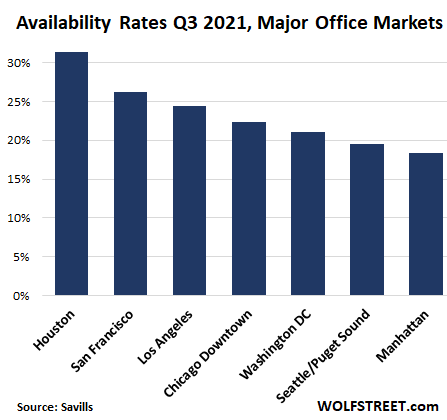

Here’s how seven major office markets in the US fared through Q3 2021 – struggling with huge amounts of sublease inventories and sky-high overall inventories of office space for lease, with availability rates ranging from a catastrophic 31.4% in Houston to Manhattan’s record 18.4% (data from real estate services provider Savills):

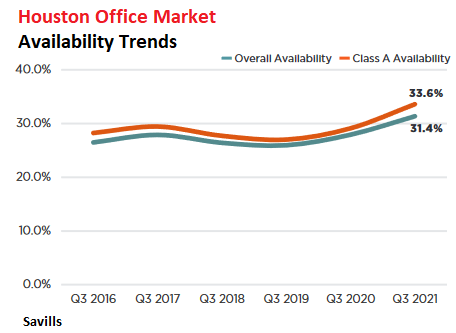

Houston, first the oil bust then working from home.

The immense Houston office market – 192 million square feet (msf) of office inventory – has been the worst office market for years, after its construction boom collided in 2015 with the Great American Oil Bust, which led to downsizing, layoffs, and bankruptcies of numerous oil and gas companies headquartered in Houston. Then came the pandemic and working from home, and the recognition that companies wouldn’t need that much office space in the future.

Total availability ticked up to a catastrophic record of 31.4%, according to Savills. Class A office space availability rose to 33.6%, meaning over one-third is available for lease.

By submarket, the availability rate ranged from 10.3% in Medical Center/South Houston to 53% in North Belt/Greenspoint. In the Central Business District, 33.8% of the total office space was on the market for lease.

Average asking rents have been stable at around $29 per square foot (psf) per year, according to Savills. But those are copy-and-paste asking rents. Actual deals that were agreed to differ, often with lower rents and aggressive concessions, periods of free rent, and amenities, that sharply reduce effective rents.

Leasing activity ticked up to 2.5 msf. This is still abysmally low, compared to 4.1 msf in Q3 2018, and 5.7 msf before the oil bust in Q3 2014, but it is the highest leasing activity since Q2 2020. Every little improvement counts.

The uptick happened amid the jump in oil and gas prices. But oil and gas companies too have switched to hybrid work-from-home models for many of their employees, putting a damper on their office needs.

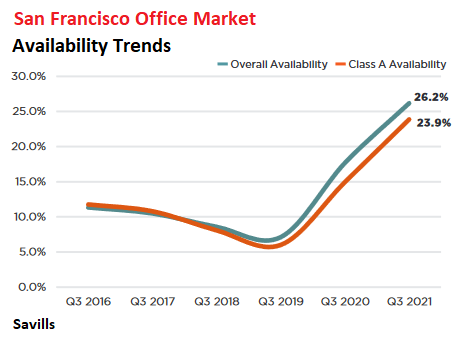

San Francisco, from office shortage to office glut in no time.

The office market in San Francisco is about half the size of Houston’s. Just a few years ago, it was one of the hottest, tightest, and most expensive office markets in the US. But the erstwhile heavily hyped office shortage has turned into a magnificent office glut, second only to Houston’s, and getting closer.

The amount of office space for lease rose to 26.2% of total office space (up from 23.6% in Q2), and up from 7.3% two years ago (chart via Savills):

Sublease inventory, which had exploded to 8.9 msf in Q1 as companies put their unneeded and empty office space on the market, ticked down in Q3 to a still huge 8 msf after some leases were signed.

The overall asking rent has dropped 10% in Q3 2021 from Q3 2019, to $72.79 psf per year. Class A asking rents dropped 15% to $75.98.

But in this market that has gotten hit so suddenly by a collapse in demand and a glut in supply, pricing remains to be discovered, and asking rents are a landlord’s wish. But deals are being negotiated.

Total leasing activity rose to 1.9 msf, a pandemic high, after the market froze up last year, with 40% being renewals. But it was still down by 26% from Q3 2019.

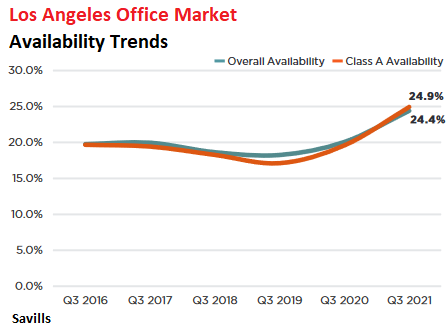

Los Angeles

Total availability rose further, to 24.4%. Available sublease space remains huge, but ticked down to 8.9 msf (from the record 9.2 msf in Q2), “as sublease space has either been leased, pulled off the market, or has become directly vacant,” according to Savills.

In a funny twist, asking rents increased to $3.87 psf per month (about $46.44 per year) “due to higher-priced trophy sublease space, as well as new speculative office projects now under construction,” according to Savills.

But “average taking rents have largely decreased,” according to Savills. “Combined with higher concessions such as rental abatement and tenant improvement allowances, landlords have remained aggressive at competing for occupancy.”

Leasing volume, at 3.2 msf was roughly flat with Q2, and has recovered a lot from the low levels last year, but was still down 20% from Q3 2019.

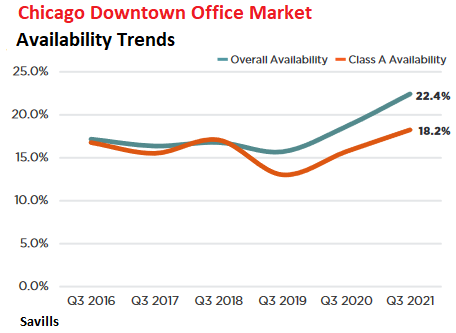

Downtown Chicago.

Overall availability rose to 22.4% in Q3, though sublease space ticked down to 5.7 msf, as aggressively priced high-quality spaces found takers. By submarket, availability ranged from 15.9% in North Michigan Avenue to 25.5% in Far West Loop/Fulton Market:

Leasing activity rose to 2.2 msf in Q3. While way up from the collapsed levels last year, it was still down 33% from Q3 2019.

Overall asking rents ticked up a smidgen to $40.70 psf per year and have essentially remained flat for three years, but effective rents declined “across all properties apart from trophy and new construction,” according to Savills. And “they have fallen more precipitously in Class B buildings, where availability sits at 26.1%.”

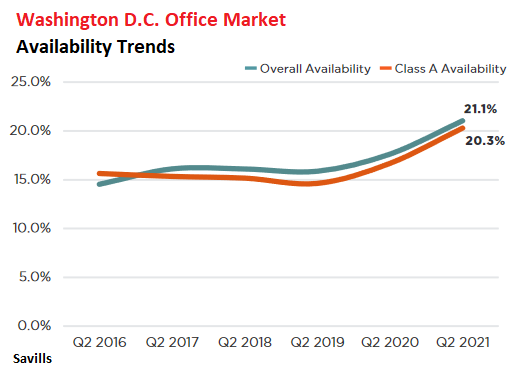

Washington D.C. – Government is the driving force

Overall availability, after jumping for seven quarters in a row, remained at the record of 21.1% established in Q2. Sublease availability, which hit a record of 3.4 msf in Q4 2020, has now ticked down 3.0 msf, “as many organizations have been successful at subleasing their space or have taken it off the market as they decide to re-occupy it.”

But 2.3 msf of new construction is still coming down the pipeline, with two-thirds expected to be delivered within a year, and only half of it is preleased.

In terms of leasing activity, the big thing that happened was that the government leased 1.2 msf of office space for the SEC, which accounted for over one-third of total leasing activity; the government also renewed a number of other large leases, which brough total leasing activity to 3.0 mfs, the highest since Q2 2019.

Asking rents have remained roughly flat for the last three years, in Q3 at $55.82 psf per year. But according to Savills, “hefty concession packages continue to validate underlying tenant-favorable conditions,” with new long-term, Class A leases now getting “an average of $147.00 psf in tenant improvement allowances and 22 months of free rent totaling $267.00 psf in total value.”

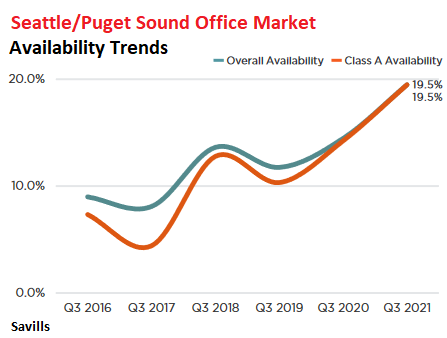

Seattle/Puget Sound.

Overall availability rose to 19.5% in Q3, ranging from 8.8% in Everett Central Business District to 28.7% in South End.

Leasing volume, at 1.5 msf, while up from the pandemic lows, was still down 25% from Q3 2019 and 33% from Q3 2018. And Asking rents, despite the massive availability and the still low leasing activity, ticked up overall to $39.79 psf per year.

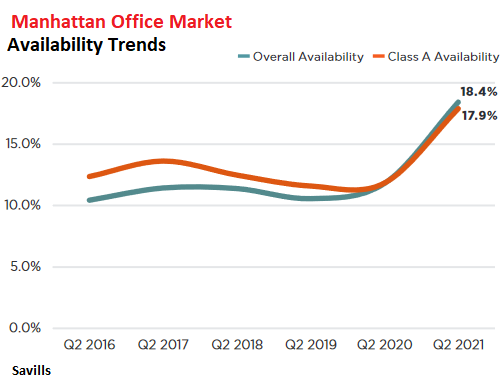

Manhattan, the giant

Overall availability in the largest office market in the US with 468 msf of inventory, remained at the record level of 18.4%, first set in Q2. By submarket, availability ranged from 11.4% in Hudson Square to 23.7% in the Financial District and 24.5% in Soho.

Leasing activity rose to 7.7 msf, up sharply from the prior quarters and down only 10% from Q3 2019, as the market “exhibited signs of vitality,” according to Savills.

Average overall asking rents declined to $75.08 psf per year, down about 10% from Q1 2020. “However, taking rents and concessions have further widened the gap between asking and effective rents,” Savills reported, adding that effective rents “will continue to decline in the coming quarters as owners continue to face competition to attract and retain tenants.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It was quiet, too quiet. Even the blogs had vacancies now.

Dow down 450 and falling as I write this. Mondays. Sooner or later the blinders come off. Seems to me office expense is now a first cut, especially if they don’t really need the space. Business can no longer cut wages, so the overhead has to be reduced. Plus, WFH of course.

Next up is photo copy limitations, self pay coffee funds, and turn down the thermostat. :-) I had a boss once who started to limit paper towel access in the washrooms. Pencils and pens are doled out.

A favorite meme with the Dilbert cartoon was how to get rich off office supplies.

Nobody needs a corner office with a view, but here we are.

Speaking of which.

DDG the executive tower of Bethlehem Steel which was just torn down.

Was specifically designed to have the maximum amount of corner offices.

Dow up and down is just noise. The FED will fix that stuff once JP gets the calls from Pelosi and the empty suit’s handlers.

It is very interesting how residential rents are recovering/soaring in major cities while commercial rents are still diving and office spaces remain in massive glut mode.

How to make a conclusion of this? My guess…

Folks enjoy living in cities but also enjoy working from home. Even if the office is a short walk or subway ride away.

However, with commercial businesses still in recession mode, a large part of enjoying a major city isn’t there anymore.

Maybe just enough survives.

Residential rents are going up because residential has not had it’s reckoning yet. Mortgage forbearance and eviction moratoriums have been keeping people in place. Once that sorts out it may be a different story.

Anecdotal story: knowing that the eviction moratorium ended here in CA on oct 1 I asked a property manager friend what percentage of tenants he sees getting evicted now that the time has come. His response was minimal, there are tons of programs out there to help struggling renters with rent.

So maybe… but perhaps not yet.

Boston is conspicuously not here. My building is being sold, papers pass tomorrow, and purchase price is OVER asking by aprox. 28%. It is a class A office building in the Financial District. Business in the area is DEAD. I have a retail shop, first floor, street level. Our business is 50% of what it was in 2019. There are a few workers coming back, but at a snails pace. I don’t understand the mentality of out bidding and how this will end.

OPM….

Nowhere to put it would be my guess… betting on a few years from now…

Isn’t sc7 from up around there… perhaps some insight…

Boston isn’t included because Savills’ office report for Q3 Boston hasn’t come out yet. They don’t all come out at the same time. It’ll likely come out in a couple of weeks.

It is likely that the Fed (surrogate) is buying to prop prices. Without that support, we will fall into a deflationary spiral in commercial real estate.

What do you think the Fed is buying with the 120B/month of MBS?

By the way, they did the same thing after the 09 housing bust. Only they used Blackrock and others to do their bidding. Pulled the wool over most American’s eyes.

Workers are voting with their feet. They are never coming back to offices in 2019 numbers again.

Who knows. Time will tell.

The companies that would fill that space are struggling to find employees as it is. They can’t start forcing them to do anything after many have already forced them to get vaxxed. There’s too much competition for talent right now to get away with pushing employees too hard.

So, be at work at 8 am at your desk or be fired won’t work?

Because it sure ain’t stopping the show us your white index paper filled out or be fired method of employment.

No, for me, it won’t. Because I have relatively specialized skills and I have recruiters calling me constantly.

You may think so now, but look forward 5 or 10 years and the lads in Bangalore or similar neighbourhood will be offering the watered down version of whatever you do, for a fraction of the price. Maybe, 50 or 60% of the quality of your product, but, at 1/20th of the price. This will chew into your gig.

I have a fairly specialised of skills myself, and here in U.K. I still command my rates. But just for fun, or as a survey of future of my industry, I occasionally post jobs on upwork or freelancer, or indeed make bids on offerings. All I can see, is, entropy.

The economy is walking on eggshells. Who can be sure when the collapse will occur or if people will be happy to take work under any circumstances if things get much worse? Evergrande debt is being actually bought by US financiers now, reportedly. See “Marathon Asset Is Buying Evergrande Debt, CEO Richards Says” in yahoo finance.

Could this be a scheme to bail out the foolish, Wall Street entities that were investors in Evergrande by buying the debt off of them and into an entity that may be able to get indirect bailouts later from the “Fed” when their debt purchases become uncollectible? Alternatively, could the Wall Streeter parasites be riding to the rescue of their fellow parasites, CCP cronies?

I have not doubt that somehow and in some way that we have not yet figured out, ordinary Americans are going to get the shaft via this scheme, yet again.

RH,

“Evergrande debt is being actually bought by US financiers now, reportedly.”

Yes, regular bond vultures, buying defaulted or nearly defaulted bonds for cents on the dollar. That isn’t a bet on a Fed bailout at all, but a high-risk gamble on making a profit if either the bonds get bailed out with a smaller haircut by the Chinese government, or if bondholders can pick up the collateral (if any).

That is what was implied in news reports. Certainly, if you have a loan that has terms that enable it to be enforced in the USA against assets of Argentina or Venezuela then you are pretty certain of getting paid a portion of the face value of the bond.

Here, however, Fantasia holdings is now late and probably will default on its own loans too. Hundreds of real estate developers in China already went bankruptcy and the fire sales (and reluctance of investors/purchasers to give them more funding to build prior property sold, etc.) will probably cause more to go bankrupt, even if they had enough capital to survive for a while.

Chinese courts are reportedly, notoriously arbitrary and anti-foreigner. For example, for years, foreigners that consider entering into contracts enforceable in Chinese courts were often advised by lawyers just to proceed on an invoice by invoice basis getting paid as they went with minimal provision of credit, to keep US law applicable, even for lesser sums.

Thus, if the vultures expect to use Chinese courts to collect on Evergrande, good luck. LOL

One more thing, the banksters are now operating on the assumption that they will get bailed out of any financial liabilities that they come to owe by their “Federal” Reserve. There are reports, which I believe, that various foreign entities are owed huge sums by Evergrande and the other, legally insolvent, Chinese, real estate developers (and other Chinese companies also failing now.)

The Chinese government clearly wants the real estate properties in China being constructed finished and Chinese investors paid and does not care about whether foreign creditors or investors are paid. That is shown by who is getting Evergrande’s money.

Often the owners of the banks are going to also own or be cronies with the owners of those financial entities that are in deep guano because of their uncollectible, massive, Chinese debts. Thus, how likely is it that they might collude, sell the uncollectible Chinese debts for way above FMV to the banks (like the “Fed” bought the banks’ MBS), and then the banks will get bailed out of the losses by their “Federal” Reserve? Apparently, the banksters’ privately owned, “Federal” Reserve is always happy to funnel more funds to its banksters: e.g., via huge QE commissions for doing little, ultra low interest rate, below the real inflation rate loans, to banks while those banks are insolvent etc.

Search for federal reserve and audit and secret bailouts and trillions; you will see. In looking at the financiers’ actions over the last century, from the founding of the “Federal” Reserve by misstating its purpose and founders to the public, I submit that we err if we are not suspicious enough of their actions.

I think the effects of this shift to work from home will take more than 5-10+ years for it to unwind “back to normal” if it does.

5-10 years is probably when all of the longer term leases would be expiring.

It would be interesting to see data on the length of leases being signed these days.

Exactly, most of these big leases are 5-7-10 years. They could of been in year 3 of the lease when the pandemic hit. As the leases roll and not renewed that’s when it gets ugly…I think it will be a long slow downturn that will go on for years.

Shouldn’t there be more property developers going bankrupt? How can any of them possibly get through a 25% long-term drop in revenues?

Zombie corporations.

They rise when cheap and easy money is a thing.

Do you really think there is a market based on fundamentals?

And it’s not just real estate.

At least half of Tech 2.0 companies have never made a profit and never will.

Wolf, how about a post on this?

jm,

The property will go back to lenders if it defaults. Any developer worth their salt knows how to structure this to where the lender takes most of the risks.

They keep borrowing money at 0% interest to prop the illusion of financial solvency.

Great news!!!

This means fewer cars jamming up roads for 3 hours every morning and afternoon, less energy wasted heating and cooling glass towers, nicer, happier workers to interact with because they aren’t tired, angry and frustrated from their commutes by the time they get to their offices.

Oh yes, I almost forgot – happier pets that get to spend more time with their humans!

CCCB

Think again. With the movement away from Metro due to pandemic fears, the traffic is worse than even.

I don’t know what fantasy world you live in, but I can say from personal experience traffic in L.A., Portland, and Seattle is back to rush hour norms.

I agree that traffic is back, but it is different. Both mondays and fridays are very light during rush hour. Traffic through downtown (PDX) at rush hour is so light I use Broadway as a fast alternative to the highway. Also the Sunday traffic patterns are very weird and hard to predict.

KGC,

Part of the problem with traffic is that people are still not taking mass transit like they used to. Nearly everyone is driving.

For example, ridership on the Bay Area Rapid Transit system (BART) in September was still down 72% from two years ago, but roads are nearly as congested as before.

That system used to get 10 million riders a month. Now it’s about 2.6 million.

I was on LA on Friday, the 405 was jammed at 8pm going south to OC. Just like the old days.

There was a massive concert down in OC this weekend BTW. Agree traffic is a mess but for one weekend there might have been an actual reason

The traffic during the “lockdown” in ATL last year was noticeably better than previously. Now, it is back to totally “sucking”.

This past Sunday, returned from FL and approached the perimeter around noon. It wasn’t rush hour going south but not far from it. (I don’t live in this area.)

Not much different now going on the south side of the perimeter on Saturday afternoons. This used to be (and still might be) the least congested section of the expressway system in the metro area.

I once believed that WFH was the only realistic solution to the city’s traffic congestion. It’s not nearly enough. There are just too many people living here now.

That’s true in every U.S. city now. The population of America was comfortable around 200 million. There was no reason for mass immigration and Great Society to raise it to 320 million.

Does this data include close in suburbs? I noticed a lot of empty buildings and stores vacant and going out of business in the suburbs of Washington DC where I live. It seems to be getting worse every day. If this isn’t a depression, nothing is.

This is still the good times. When the house of money printing cards falls, buckle up.

Yes, the good times of fake prosperity.

It doesn’t include suburbs.

Sooooo. Do the maintenance costs that still go with all the empty space, at least to make it potentially presentable and to avoid mold and mildew, make the grade of financial stability for the owners of these vacant buildings?

We had the National “Womens March” this weekend. What’s with these drivers from California that drove all the way here and nearly ran me off the road in DC. Don’t they know the speed limit is 25 MPH, 20MPH during Covid-19 period and 15 MPH in school zones. I thought the drivers here were bad but now I’ve seen worse.

What is it with all these cars from other states that black our garage here in San Francisco? Last week, it was one with a South Carolina tag.

What do you repurpose office buildings as…

Rework them into add hock ‘escape rooms’?

And I thought WeWork had this all fixed. Silly me.

I am afraid transition to WFH is one-way street.According to 2nd Law of Thermodynamics in closed system Entropy always increases.

It is possible to decrease Entropy by applying energy from outside but no such energy exists neither in Washington DC nor in corporate offices.

End state of such system: every worker is 1099 “independent contractor” hired/fired/replaced at will.In other words-no more than the record in MS Access database.Or distorted fishbowl-like face in Zoom meeting.

That’s a nice observation. The only source of “external” energy I see being applied to herd workers back into offices is from the banking industry, where the likes of Jamie Dimon are nervously watching their CRE portfolios.

Quiet exodus began well before Covid (March 2020)

Forbes,Oct 28, 2019

“JPMorgan Reportedly Moving Thousands Of Well-Paid Jobs Out Of New York City—This Does Not Bode Well For Workers On Wall Street”

I feel like their is some kind of giant hammer waiting to fall in the office market. Sure rents are dropping, but it seems like things are even worse than those changes would indicate but it is like everything is suspended in a deep freeze. Near me are a big pair of suburban office towers (Salesforce and Synergistics) that have a completely empty parking lot. Plus a half million ( of more) square feet of one story office buildings in a complex that used to house Nike employees that is totally empty. It is like they are treading water waiting for the sharks to pull them under.

Wolf,

Is there any data on how some of the secondary markets look? For example, Portland, Austin, Minneapolis, Charlotte, or Boston?

There are like also to have a sizable amount of office spaces.

And Dallas. They’ve been building office space like crazy over the last 4 years even though they already had a ton of open space. They’ve had 4 huge buildings fall into bankruptcy and STILL have new projects going up.

Throw in a request for Atlanta, too.

These darn fools around here keep building. The local rag does not cover the commercial real estate market, anymore, due to cutbacks.

Only the local business press covers it and they lie through their teeth about it. It’s always blue skies and sunshine. Real data is hard to come by.

This will take lots of time to see the end result. So many people had signed leases of 8-12 years. We are barely 18 months into this. Office will never be the same again. Not hyperbole.

All of the Baby Boomers will be retired in 8-12 years. I think Gen X’ers & Gen Z’ers have little love for the office.

At my office prior to the pandemic, most of the staff (me included) commuted to stare at their desks, with the pleasure of traffic congestion both ways.

Going in is mostly a waste of time.

Miami Beach Class A office rents are up YOY. Someone is paying the rent.

While some office building vacancies are high, delinquencies are low. Companies have made plans to return more workers to offices in 2022.

Well in Miami the main purpose of office space is as an address for your shell corporation to move funds in and out of South America etc. So it is no wonder vacancy rates are down because financial shenanigans are on the rise.

Hair dressers, barbers, and spa service workers are going independent at a high rate. I can’t believe the number of “salons” that are now a collection of units with people working for themselves. I’ve come across three of these places this year and they all have lots of spaces, maybe 50+.

I think the new payment systems salons use now are pushing customers away. I know I won’t use a salon that needs a credit card number in order to make an appointment. Makes me think the service is bad if they want payment up front. Workers seem to be abandoning these place too because they don’t take cash.

Charging a fee for no shows?

When this fake economy and house of cards mostly implodes, providers of substantially discretionary services will be begging for customers.

Mrs Swamp now goes to her hairdresser who abandoned the salon and now set up shop in her home. We pay cash. I wonder how much of this cash goes to the government under this arrangement. Yep, you guessed it . Zeeeeeero!

All those salons are full around here and my wife needs to call two weeks ahead for an appointment. And she uses the same person, who is apparently booked solid all the time. She has not had to leave a CC number though.

I think the salons that take cash and don’t have those crazy payment systems will get more business. I looked at one of the online booking systems and they wanted a credit card number to put on file, but worse, they wanted your digital signature to keep on file with the cc number too. This is a hacker’s dream, but it also allows any employees with access to use the signature and cc number.

Cash is King.

When a barber pays almost 40% of his or her income to the feds, the state, the city, to SS, to SDI, then the 4 to 6% credit card withholding, etc, it’s reasonable for the barber to offer a 20% discount for cash compared to the lamestream corporate credit card salons.

After all, even with the 20% discount, he is still making at 20% more than he would were he being bled by the system.

We can go all day patronizing businesses around San Francisco that only accept cash.

Petunia…Hairdressers, barbers, estheticians require credit card for appointments in order to protect themselves from those who book an appointment (denying that time slot from being booked by someone else) and then do not show up, “which is termed a “no show.”

Wolf,

Commercial office construction with high density housing continues here in Santa Clara despite the hundreds of for lease empty building. I am beginning to think they are trying to be like San Francisco. I do not see how this is going to end well .

Is it not true that once a depression is realized, it is a year old already?

Yes, except in countries like the US where recessions have supposedly been permanently eliminated.

The word depression isn’t used anymore and hasn’t been for years in the financial and economic press, except in a distant historical context. Even Greece around 2011 when reported economic conditions must have approached or been worse than the US 1930’s was still termed a “recession”.

How come when we’re kids we long for recess, but when we’re all grown up, are terrified of recessions?

Fear of those bonded “ions”.

Any guesses on how much longer until the first large commercial property REIT goes banko? Alternately, will the Fed socialize the losses of large investors at the expense of middle class taxpayers?

They are already bankrupt but nobody wants to acknowledge the defaults.

My girl real estate, dah dum dah dum dah dum,

She makes my heart skip Everlate,

She’s ev’ryone’s desire,

Sets their cash on fire,

My girrrlll….real estate.

I love you, I love you, I love you so,

I’ll never let you goooo,

I need you, I need you, I need you so,

I’d bet the farm on “To Show-oh”.

A counter trend in Seattle?