Mass-forbearance is the best thing that ever happened to sweeping reality under the rug. But now, there’s a huge mess under the rug.

By Wolf Richter for WOLF STREET.

To the Fed’s great relief, hardy American debt slaves are finally going deeper into debt, after having made unnerving efforts in prior quarters at paying down their credit cards, the most expensive debts with the biggest profit margins for banks. What helped push up total borrowing were massive price increases that had to be financed – particularly homes and vehicles – and the loans to finance these purchases jumped even if the volume of purchases didn’t.

Total household debt – mortgages, HELOCs, credit cards, auto loans, student loans, and other debt – jumped by $313 billion in Q2, from Q1, according to the New York Fed’s Household Debt and Credit report today. This 2.1% jump was the biggest quarter-over-quarter jump in years, matching Q4 2013, and both were the biggest jumps since 2007. The total balance of debt reached nearly $15 trillion.

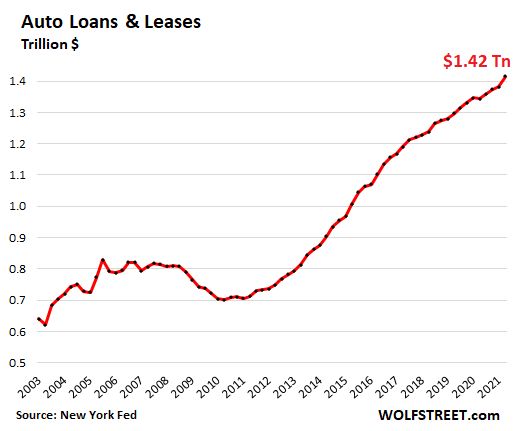

Auto loans & delinquencies: price spikes & stimulus checks.

The balance of auto loans and leases jumped by 2.4% in Q2 from Q1, to $1.42 trillion, the biggest quarter-over-quarter percentage increase since 2016, based largely on surging prices of new and used vehicles:

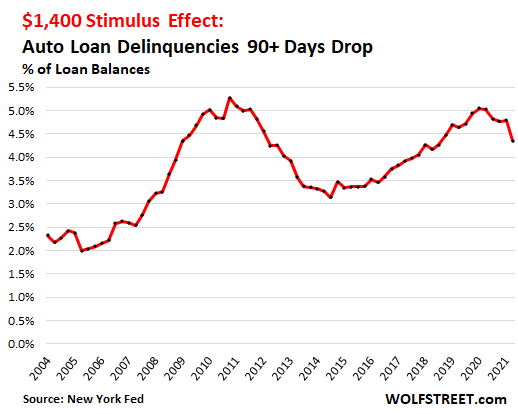

But the stimulus effect kicked in. In late March, the $1,400 stimulus checks started going out, and they continued hitting bank accounts for months, and some people used them to get caught up with their auto loans that they had fallen behind on. And seriously delinquent (90 days plus past due) loan balances, dropped to 4.35% of total balances outstanding. That decline of 44 basis points from the prior quarter was the biggest drop in the data going back to 2003:

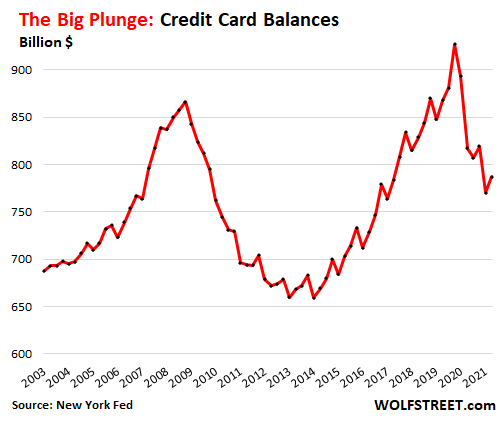

Credit card balances & delinquencies: consumers are finally charging it again.

After paying down their credit cards since the peak in Q4 2019, which had confounded the folks at the Fed in the prior quarter, Americans finally saw their error and backtracked and racked up more debt on their cards, in order to pay 15% or 25% or even 30% in interest in a 0% interest-rate environment.

Credit card balances rose 2.2% from Q1, to $787 billion. Let’s hope that this uptick wasn’t “transitory,” or else the Fed is going to have a cow:

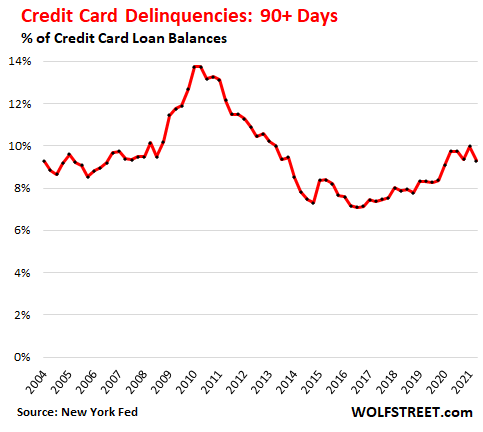

Seriously delinquent credit card balances fell to 9.3% of total balances, thanks to the stimulus checks that went out in March and helped some people get caught up. Despite the stimulus checks, 90-day-plus delinquencies remain higher than in the 2014-2019 range:

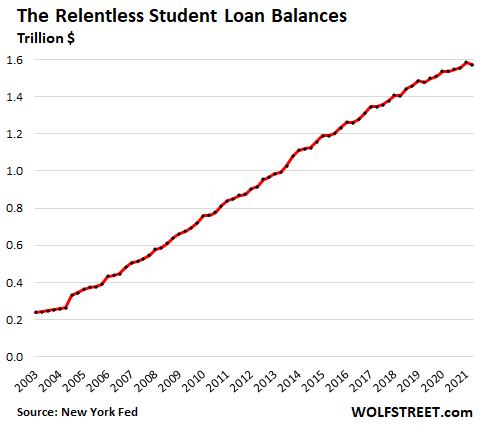

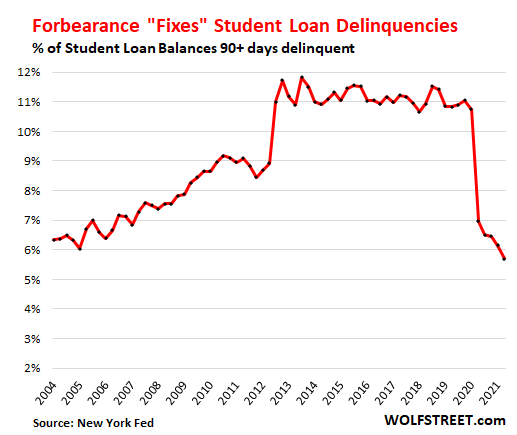

Student loans, oh my! Forbearance fixed everything.

Student loan balances ticked down a smidgen – as they often do in Q2, after the jump in Q1 – to $1.57 trillion, still up 1.9% from a year ago:

Even though few student loan borrowers are still making payments – eagerly waiting for the big kahuna to set them free – the serious delinquency rate dropped further, the sixth quarterly drop in a row, to 5.7% of total balances, the lowest in the data going back to 2003.

Delinquencies have dropped not because borrowers are suddenly catching up with their student loans in some magnificent manner, or are wasting their stimmies to catch up, but because student loans were automatically entered into forbearance last spring, and loans in forbearance don’t count as delinquent. Problem solved:

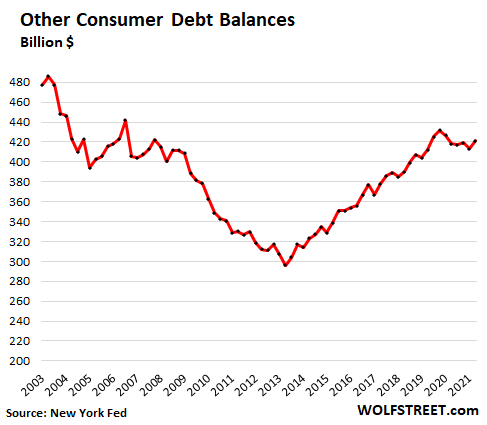

“Other” consumer debt balances finally rose again.

The balances of personal loans and lines of credit from banks, shadow banks, peer-to-peer lenders, and payday lenders, after falling for five quarters in a row, finally rose again, up by 1.9% from the prior quarter, to $421 billion:

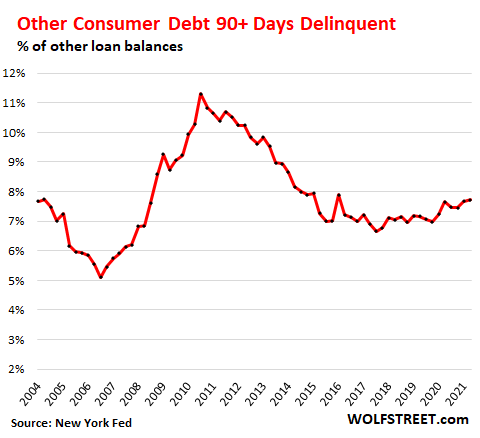

Serious delinquencies remained roughly flat with the prior quarter – thank god for the stimulus checks – at 7.7% of total balances:

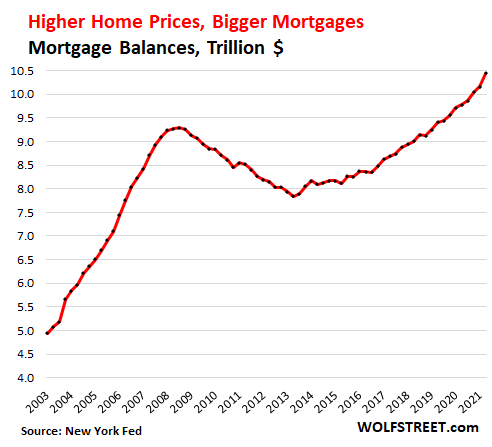

Home-price explosion pumps up mortgages, forbearance cures all.

Mortgage debt jumped 2.8% in Q2 from Q1, the biggest quarter-over-quarter jump since Q2 2007, amid the fastest rise in home prices in recorded US history, as it takes more dollars to finance the same home, and as refis are ballooning.

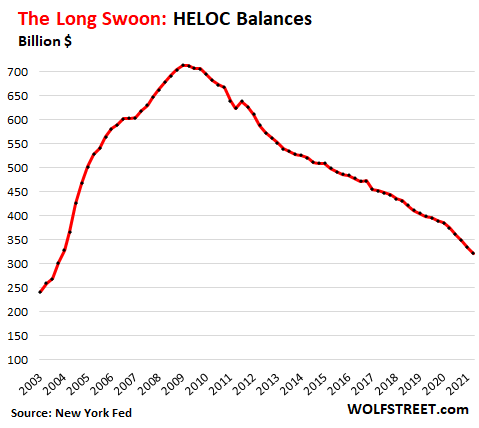

But home equity lines of credit (HELOC) balances continue to decline and are falling out of use, as homeowners have switched to cash-out refis at lower rates if they need extra money to plow into cryptos or stocks or a new deck out the back. The $322 billion in outstanding HELOC balances are down by 55% from the peak in 2009:

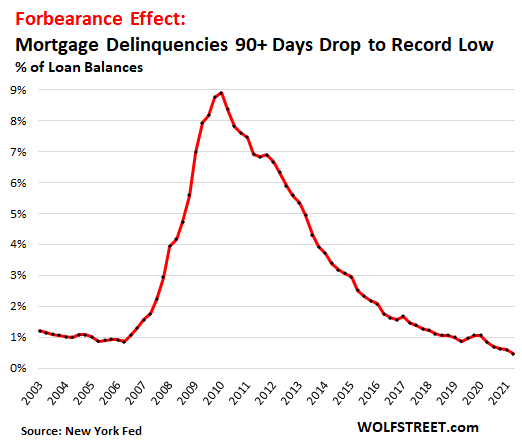

Mass-forbearance is the best thing that ever happened to sweeping delinquencies under the rug. Seriously delinquent mortgage balances dropped to 0.47% of total balances, the lowest in the data going back to 2003:

But forbearance for federally-backed mortgages, after having been extended, is running out this fall. At the end of Q2, there were still nearly two million mortgages in forbearance. To exit forbearance, the borrower will sell the home and pay off the mortgage, or the lender will refinance the mortgage often with lower payments and extended terms to make it easier for the borrower to pay for.

This is all part of a gigantic government-backed extend-and-pretend scheme that includes eviction bans for renters – now expired at the federal level but not at state and local levels – and student loan forbearance, still scheduled to expire at the end of September.

This is an economy where credit problems have been swept under the rug, where many consumers stopped making payments without negative consequences, even as free money hailed down upon them.

Because delinquencies are no longer delinquencies but count as “current,” credit scores rose on average – and in the process, credit scores have become useless for banks to determine the creditworthiness of a potential borrower.

After 16 months of sweeping this stuff under the rug, there is now a huge mess under the rug, and the temptation in government is to just keep it there and forget about it, or have the taxpayer clean it up, rather than consumers, lenders, and investors.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Remember guys, all of these are happening during the “good times” as Wolf likes to say. In addition to WTF ETF, we’ll probably also see “Under The Carpet Sweep” ETF, and other “innovations”.

It also seems like states have only spent a fraction of the funds meant to halt evictions.

Isn’t this simply a confiscation of property by other means?

WTF.

M B,

My local paper has an Opinion Exchange today from Chicago’s Steve Chapman. He sums it up:

“The harm, however, remains — and it goes beyond the immediate financial loss to property owners. Rental housing is bound to be lost as some landlords are forced to sell. Potential buyers will have to weigh the risk of being victimized by future moratoriums. In the long run, tenants will also lose out.

The federal moratorium was intended to address a dire short-run calamity. But it may end up creating a permanent one.”

As I commented once here a long time ago, I don’t understand how government should have the ability or power to intercede into a contract between a renter and a property owner. To me, contract law and property rights are the cornerstone of a free and just society.

Oh well, since 9/11, the Bill of Rights have been destroyed, and a year ago the government decided that property owners must provide free shelter if they are ordered to do so.

Did the Covid pandemic equal war? Are citizens getting stimmy checks equal to a “well-regulated militia” fighting for the United States’ sovereignty?

“No soldier shall, in time of peace be quartered in any house, without consent of the owner, nor in time of war, but in a manner prescribed by law.”

Yes, I have a heart and soul. Yes, I cringe when I see homeless and destitute people. Yes, I’ve been blessed and have had the good fortune of never being a debt slave. Yes, I agree that mass-forbearance is a huge mess.

Fully agree with your statements. It was outrageous to allow this type of governance to stand. Then adding numerous extension, crazy. Very thankful that my tenants paid their bill every month. Had they stopped paying I would have been in a world of hurt. Bless the stars.

You are not heartless. You are just pointing out the ridiculous burdens the policies used

The Supreme Court ruled that what the CDC did was illegal, so the CDC did it again with the blessing of Coma Joe. This is an outrageous, disgusting overreach. Landlords should tell the CDC to pound sand and evict anyway.

Once government steps over the clear line between the protective or negative role into the aggressive role of redistributing the wealth through taxation and providing so-called “benefits” for some of its citizens, it becomes a means for legalized plunder.

Who allowed the central bankers to decide that dubious 2% targeted inflation is price stability? Lawlessness has been a rule for a while, and there is no challenge to it.

Once it was decided that a central bank could steal your grandma’s savings and give it to a no good debtor it was a slight moral stretch to letting a deadbeat live in grandma’s rental house for free. Hope grandma’s social security isn’t cut to pay off student loan debt.

After the Supreme Court’s ruling, WHY would any landlord adhere to this illegal “moratorium?” The CDC can’t fine you, they can’t do anything. The courts ruled on it.

Totally agree, Dan…. I think I will save your comments because they say exactly what I have been feeling about this situation but I didn’t have the right words.

I too have been fortunate. I chose to acquire rental properties in senior citizen developments and I have not suffered what so many other landlords are suffering…(at least not yet).

I do think this situation is going to make it very profitable for large, well financed organizations to move in and purchase large blocks of rental properties once they are foreclosed upon by unpaid lenders.

This is basically how a productive economy goes down the toilet. The bigger the government gets the more they stomp around and discourage private businesses from doing long term investment. It’s long term investment that gets the job done as far as standard of living getting better. We will be Venezuela in a few years if we don’t get our act together.

“Rental housing is bound to be lost as some landlords are forced to sell.”

and which partner of the Fed will be there to buy up the distressed properties?

The government makes the laws and laws govern contracts. Without civil law of some kind and enforced by the courts, which are by definition part of the organisation of government, no contract can exist, so to say the government is interceding is missing the point. The liberatarian idea that there will be enforcable laws without a government of some kind is laughable.

“Did the Covid pandemic equal war?”

It should be considered to be so considering the gross malfeasance and deception involved in its early stages by China and their 2017-installed head of the WHO, the former Ethiopian Marxist party member Tedros [look it up]. How much has it cost the US alone?

“In today’s dollars, World War II cost $4.1 trillion, according to data from the Congressional Research Service (in 2020).”

The laughable response I’ve been hearing from Republicans is to boycott the Winter Olympics in China and even that probably won’t happen because we are hopelessly compromised by China which one will realize by reading the outstanding book, “Stealth War: How China Took Over While America’s Elite Slept.”

And the “elite” (Gak! I hate that term) weren’t “sleeping.”

With bought government and institutions, the only thing we have left is the world’s reserve currency.

“The liberatarian idea that there will be enforcable laws without a government of some kind is laughable.”

I agree. Where they are correct is where they point out the obvious lesson from history – governments are agents of coercion with a monopoly on (legal) force and when they grow to exceed the constraints of, oh, lets call it a “Constitution,” bad things can happen.

“There’s no way to rule innocent men. The only power any government has is the power to crack down on criminals. Well, when there aren’t enough criminals, one makes them. One declares so many things to be a crime that it becomes impossible for men to live without breaking laws.” – Ayn Rand

On exactly the above topic, read the book, “Three Felonies a Day.” Then, as also pointed out in that book, add selective enforcement:

“When the law no longer protects you from the corrupt, but protects the corrupt from you – you know your nation is doomed.” – Ayn Rand

Contracts? Mere pieces of paper.

c_heale,

Laws are set by government and enforced in court; that is true.

The Founders understood this, and designed this nation to have three separate branches of government. Checks and balances & all that.

But there are certain fundamental principles that should always be adhered to. Hence, the first ten Amendments to the Constitution. Number 3 says no property owner in the USA shall have to give quarter without consent — unless during war.

Won’t somebody think of the landlards!?!?!

IMO a surplus of rentals hitting the market is a good thing. A rush of supply will crush prices, and these former rentals tend to be pretty “meh” fixer-uppers. Get some first time buyers who want to swing a hammer into these homes. FTHB have been priced out in many areas at current prices.

Unfortunately for landlards, the risk side of the equation has been realized. Drat, investments can incur risk of loss and aren’t free money?

” I don’t understand how government should have the ability or power to intercede into a contract between a renter and a property owner. ”

This is absolutely true. How can the CDC insert itself into private contracts?

This is baffling government behavior, but it will likely get worse as economic and financial conditions deteriorate.

Reckless government behavior has put us on this course.

Voters are also to blame, but then the primaries are so corrupt that most people don’t even realize they don’t get to elect the candidate the public actually wants.

Ayn Rand died living in public housing AND cashing her monthly SOCIALISM security checks.

She, like those that followed her, were completely full of crap.

Please don’t quote that awful writer and pretend she had some wisdom to share w/the world. Her selfish, senseless scribbles bored me to tears.

I tried to read Atlas Shrugged but after several hundred utterly boring pages of her saying the same thing over and over, I threw it in a fire and felt a huge sense of relief.

The preamble to the Constitution says the “We the people…provide for the common defense, promote the general welfare”. So it was obviously in the best interest for the government to step in during a raging pandemic to make sure peopeople wouldn’t be thrown out on the street after losing their jobs as a result of said pandemic. I will say the biggest mistake of this forbearance program and rent relief program was rushing it through Congress yet leaving the states to administer the relief funds. Of course the states with the most unused funds just happen to be all of the red states that fought against the forbearance program in the first place. Having said that, the whole rent relief program was poorly administered to begin with, and most tenants and landlords who were eligible for these funds didn’t even know about the program.

728huey,

Yes, but before those generalized, and important goals for the Republic to attain are rather ambiguously stated, promoting the general Welfare; The first orders of business are to:

“… establish Justice, and insure domestic Tranquility, …”

One could argue that the establishment of Justice is part and parcel to respecting property rights as defined explicitly in the Bill of Rights.

If domestic Tranquility is defined by making sure people won’t be thrown out on the street as a result of waving a magic wand and declaring that renters no longer need to incur the expense of making rent payments for their shelter to the landowners, then perhaps mass-forbearance of rent is what the Founders who wrote The Preamble had in mind.

If I were a betting man, I would put my money on the opposite, and wager that the Founders of the USA believed that maintaining property rights was the key to establishing Justice.

From James Madison:

“Where an excess of power prevails, property of no sort is duly respected.”

> Yes, I cringe when I see homeless and destitute people.

US failed to build enough new housing units, the only way we can avoid homelessness given the pace of population growth is for longevities to go down.

COVID is helping with that. Boomers and older did not build enough housing to accommodate for longer longevities. There’s no other way to fix that massive error.

leanFIRE_Queen,

I understand that this stuff is your shtick, and nearly every one of your comments propagates this, but just because you think so, or hope so, doesn’t mean I will let you use my platform to keep spreading this crap. But you’re welcome to yell it out of the window of your house.

I dunno how redundant Fire Queen is with her comments but she is right Wolf. There is not enough low-income housing and people are ending up homeless. The Millennials will forever be the largest generation in American history but the federal govt didn’t build enough units to house that generation and the next. Right now there are 9.2million low-income renters who spend a 1/3 or more of their income on shelter. So millions of them are spending 40-65% of their earnings just on shelter. Not much else to enjoy life. the Hope VI demolition grants destroyed many of the old FDR-built housing projects but they never placed any requirements on cities to replace those units. I have seen “Affordable” housing units being ate up by people who aren’t low-income but aren’t quite middle class. I’m in a major U.S. city, 15yrs ago I have seen the youngest homeless people be about 24yrs old or older. Now, I see them at age 18, a whole lot of them 20 or 21. The lack of low-income housing units not addressed in the Millennial generation is really rolling over to the generation behind it. Mix that with a flood of exotic street drugs available when people hit rock bottom then you have countless mentally ill young folk who’s minds & lives have been ruined. But really, it’s all a result of not having a home they could afford

AverageCommenter,

From your comment, it seems you didn’t read beyond the first sentence of what leanFIRE_Queen wrote. So I’ll help you out. This is what she wrote beyond the first sentence (and what I responded to):

“…the only way we can avoid homelessness given the pace of population growth is for longevities to go down.

COVID is helping with that. Boomers and older did not build enough housing to accommodate for longer longevities. There’s no other way to fix that massive error”

She is telling boomers to die sooner. She said this in numerous comments before. Saying that one group of people needs to die sooner to make room for others is a heinous thing to say.

I see now. I didn’t really comprehend that Fire Queen was suggesting that Boomers should die off faster. Regardless if Boomers from now on out manage to live to be 100 on average, that still isn’t the problem to the housing crisis for low-income/working class people. And yes, it’s a heinous solution for anyone to suggest. The main problem as I said is the Federal govt doesn’t build new low-income housing, opting rather to give out Section 8 vouchers thus turning it’s housing responsibility and upkeep over to private citizens. Housing should be apart of infrastructure spending, just like fixing bridges and roads are. Homelessness wouldnt be the serious problem it is if the govt built housing instead of transferring so much wealth the last 20yrs into the coffers of Defense. Then it’s the public health issue of it: Resistant tuberculosis and other nasties setup shop amongst these homeless populations who sit on public transit, live in libraries, and eat inside fast-food restaurants etc that you & your family use daily

“If you owe the bank a million dollar you have a problem, if you owe the bank 1000 million dollar the bank has a problem.” And probably, if thousands owe the bank a million dollars the bank have a problem to.

There is where we are at today. With an economic system where money is debt that must have exponential “growth” to work. Raise the interest rate and what economy that do not default grind to a halt. Expand keep interest rates low, expand the debt and there will be inflation whatever way it is measured.

Some sort of radical economic reform might solve the problems, but then someone with a lot of money and power will have to give up on some of it. The chances of reform are then slim.

“With an economic system where money is debt that must have exponential “growth” to work.”

Correction: The economy needs exponential debt growth, OR a zero interest rate, OR a negative interest rate. The Fed likes the zero interest rate.

The Fed….the unelected financial dictators who completely ignore their mandates?

The bank does not lend any of their money. Always someone else’s looking for yields.

Is Good Times for all those big companies making more money that ever, at least.

Only good times because of the dump trucks full of cash being dumped into the system.

We better not count of these economic, “good times” continuing. The largest, Japanese pension’s recent decision to hold decreased holdings of US treasuries, and thereby of dollars, are more indications that the US dollar’s purchasing value is viewed as less safe and expected to decline. Despite just being threatened by the communist, Chinese “government” with nuclear attack, Japan is viewing our economy as riskier than before.

If that continues, so that only the banksters’ “Federal” Reserve buys US treasuries and only by printing US dollars, then Mr. Roubini’s recent prediction of a coming US stagflation will probably become inevitable. The US has too many imports which will rapidly become too expensive as the dollar is accepted less by more and more countries.

We will have to eventually start paying for imports in other currencies. I suspect that it is only the EU’s similarly dire, economic problems that has caused EU investors not to flee US dollars. The CCP’s inept, corrupt rule has also made China unsafe for investors.

Thus, for now, since Japan and South Korea are threatened by the growing military might of the CCP’s PLA, (and may see their supply lines for oil from the Middle East threatened if the PLA invades Taiwan), investors may fear to put most of their eggs in those baskets. Therefore, thanks to the CCP’s accidental, unintentional “help,” we are still being used as a safe haven. LOL

What will happen if our real estate markets tank and the mortgage backed securities that are guaranteed now by certain entities become more clearly uncollectible, so only governmental bailouts of hundreds of billions or even a trillion to those entities are necessary, by printing more US dollars? Any major increase in interest rates charged on treasuries as a result of selling too many will be catastrophic to the federal budget.

How is it possible for the balance of auto loan & leases to expand constantly? You’d think after a while (i.e., long ago by now) it’d have reached a steady state. Population growth can explain a part of the balance growth maybe but the rest?

If you are an investor in auto companies, you are investing in a bubble environment. First, with all that stimmie money and restricted microprocessors, the new car business is booming. Second, all these companies are investing in EVs and get a higher P/E multiple as they show growth in EV sales (even if the EV means less ICE sales. Third, you have auto financing divisions that are now selling their used cars for record sums of money. Fourth, you have more people driving cars because public transportation is not being used during an epidemic, where people dont want to be in confined spaces. It is just a tsunami of changes that are all going to reverse over time.

Fifth, As autonomous vehicles finally become a reality, many urbanites will just sell their cars and use subscription TAAS services. It will be much cheaper for someone in San Francisco or New York or Singapore or any other crowded city to just grab a cheap ride. Estimates are that private purchase of vehicles drops 50% by 2030.

Big changes ahead for the auto marketplace, but we are in the midst of the best of times for these companies.

Actually, lower auto ABS credits did very well, and because of inflation, they should continue to even get better since the value of the collateral, ( the vehicle ), continues to beat expectations on the upside.

If you have a deadbeat borrower with a low credit score, you repo the car, and sell it. No loss on low credit score borrowers, except for the prepayment risk.

I don’t see the problem.

Those are all very recent phenomena. They can’t explain the relentless expansion over a whole decade.

“Fifth, As autonomous vehicles finally become a reality, many urbanites will just sell their cars and use subscription TAAS services.”

Autonomous vehicles will NEVER happen. EVER.

They already have. Look up the youtube video of Buttwiper, I mean Budweiser (The original European beer is delicious, what we get in the US is awful)’s first autonomous beer delivery from a brewery to a bottling plant.

The trucker driver starts the truck, gets in the back (the part where the driver sleeps) and reads a newspaper while the truck drives itself.

Nobody has a crystal ball. Nobody can tell the future.

This place is so full of wisdom that Biden (the old guy who made it on his own (not on Daddy’s coattails)) should fire the FED and just hire the folks on this website to run things. Since everybody here is SO much smarter than everybody else!!! :)

Just wondering when the new Black Barts and Wild Bunches will figure out how to start hitting automated deliveries???

may we all find a better day.

@Olivier. Maybe a simple model?

Loan Balance = (# of Drivers)*(Fraction with Loans)*(Avg. Loan per Vehicle)

# of Drivers going up as population grows.

Fraction with loans going up because low rates and vehicles lasting longer and fewer people able to save for cash purchase (because student loan and housing bubbles?). Maybe also more people reaching for a bigger vehicle?

Avg. Loan per vehicle going up because inflation, preference for trucks/SUVs over smaller cars, and vehicles lasting longer (lenders willing to take more risk).

WS:

you need to factor also for the multiple cars per driver.

Every bubble just continues to get crazier and crazier.

Will the madness finally end this year or next?

What will it take to bring this madhouse down?

A reversal of psychology that no gimmick can sustain or reverse.

Inflation is the key. Can the Fed continue to practice yield curve control and keep down long term interest rates, or do they need to let them explode upward? Can the Fed continue to finance the deficit with very low interest short term rates, while the rest of the world begins to raise interest rates?

The Fed starved the market of long term bonds by using the Treasury balance to dry up issuance. But over the coming couple months, the balance between supply and demand changes. Can the Fed keep rates down while it finances the big deficits? My guess is we will soon have a Treasury auction with little demand and that it will trigger very large increase in yields. If inflation remains hot, the Fed cannot argue that it must increase the amount of bonds it must purchase each month. So the inability to increase the stimulus will act as a huge catalyst for yields to finally rise and rise quickly.

I agree with Augustus Frost – with is a reversal in psychology globally, such powerful moves can occur that no CB would be able to counter. All the FED manipulations are OK as long as the situation is stable.

Will there certainly be a change in psychology? Or can it stay as is, people being blind and feeling super rich with their inflated assets.

Why not? In any market big enough prices are fractal, so there are always countertrend moves. These moves are collective psychology as well. Synchronous tops in several major markets can lead to sentiment shifts, especially when the market craziness is widely discussed. If enough investors head for the exit, you will get a positive feedback loop.

gametv

‘

will soon have a Treasury auction with little demand and that it will trigger very large increase in yields..’

On surface, it appears logical but you have to remember that there 16 Trillions in the World at NRP! They will gobble anything above zero!

So why do investors invest in negative interest rate products? Because they believe that future rates are going lower and the price of the bond will rise more than the negative interest.

What happens in an environment of rising rates? The incentive to dump money into bonds for the capital gain disappears and you have a double negative return, loss of capital plus loss on interest.

Isnt this just another momentum trade that is going to set up and then reverse hard?

A geopolitical event….a black swan. And there is a whole list of potentials

How does this fact pattern play out? We all talk about kicking the can, but how much longer can we play this way? I work with small businesses and the volatility and uncertainty that they face are staggering. From costs of labor (if they can find anyone) to materials and logistics. Every time I read one of Wolf’s articles (Thanks! BTW) I wonder if we are ever going back to a slower time. My gut says no and that means planning, improvising, and staying alert are even more important.

“planning, improvising, and staying alert are even more important.”

The problem is that there are too many independent forces in play: licensing, taxes, zoning, insurance, supply cost inflation, labor availability, labor cost, utilities, rent, advertising, that are not part of a businesses core function which is development of a customer base and providing a product or service.

Each factor has a little bureaucracy that sees themselves as the only player in the game. The small business owner must deal with all of them simultaneously while keeping a lid on prices and service to keep customers not only from going to a competitor but from giving up the product or service completely.

Like a housewife trying to clean the house, she also has to deal with all the children and pets, but each child or pet only has to deal with her and can spend all their time developing their own unique strategy.

Frankly nowadays there are too many factors controlled by third parties that are each independent game stoppers. Look at CDC/Governors closing businesses, deferring rents. ACLU suing about baking cakes.

It’s my opinion that the Fed is printing a $120 billion per month in hope of preventing stall speed on the economy, because they know if we go into recession right now the amount they would have to buy would be 2X – 3X of that number of whatever assets they could find. They are praying inflation doesn’t stick but they have kicked the can once too many for current system to survive.

They are running full fiscal and monetary policy simultaneously and while this is booyah for investments, when they take off the insurance policy and the economy gets the all clear signal, that’s double booyah. They will probably use monetary policy to smooth out the gaps in coverage in fiscal spending. This economy is front loaded for a long while to come. The keyword right now is equality. This is like the 1950’s for consumers in a segregated economy. We’ve already gone through systemic economic racism so we are ready to handle that. Is corporate America going to create the level playing field. Is there egalitarian capitalism? Is it lottery style capitalism? You go to the moon or you go broke. Capitalism was never anarchy.

Any bailout of the indebted is really a subsidy for rentiers.

Forgive student loan debt? Now you can borrow more for a house. Landlords and boomers win.

Write off credit card debt? Now you can borrow it all again, usurers don’t eat losses.

The best way to really help the next generation is to fix the root causes.

Tax rentier activity. Do not tax wealth creation.

What reason is there to expect anything else?

Neither the “rentiers” or their frequently irresponsible “customers” deserve to be bailed out at anyone else’s expense.

Rentiers work on monopolies, by definition, so that comment makes no sense.

This supports my assertion that Americans only think in simplistic commie/“free” market terms, which lack the nuance to isolate the root causes and by extension the solutions to your malaise.

Simplistic thinking is, however, the root for muchch delicious irony.

The recent railing against “commies” for wanting government to introduce a command economy and abolish the “free” market seems sarcastic when contrasted to things such as “facts.”

Anyone who predicted this situation 30 years ago woukd gave been locked up as a lunatic. Like all prophets.

It’s sad that it’s funny or vice versa.

Amen but I am not sure what you mean by “wealth creation.” I sure would like to see those who transferred US jobs to China, etc., by building CCP-subsidized factories there with ultra low interest rate loans, etc., pay HIGH estate taxes. See “Apple dodged paying billions in taxes, subcommittee says” in cnet, for just one example.

Our country was much more productive in the mid-20th century, when taxes on the ultra rich were very high and the power of their wealth exerted less control on government. The investment tax credit and the research and development credits should be the main ways by which any US company can avoid taxation, because such credits promote US growth if the money must be spent in the US, as President Kennedy urged.

True prices fix most things. Government doesn’t like true prices as it’s all built off the price of money. Is there true price discovery in housing, health care, farming, education? No. Price discovery is for little people like barbers and land scapers.

> The best way to really help the next generation is to fix the root causes.

Imho we have to stop putting $ into extending longevities when we don’t have the housing supply to accommodate for it.

Bringing healthcare spending from 18% down to 9% while focusing on pre-natal care and kids under 5 is the answer to many problems imho, from housing, to global warming, to US competitiveness.

Life expectancy has been declining for years, so please stop ranting about “longevities”.

I remember back in the 1960’s my Dad telling me that my generation would be a slave to debt. He also told me to “save first, even if you have to borrow to do it”. That was his way of saying there was not an excuse for not saving. My Dad, with his 8th grade education, taught me more economics than any of my professors, and I was an Econ major. His lesson stuck with me. I think in my lifetime I paid a total of $.50 interest on credit cards and that was a Montgomery Ward card I just misplaced.

Congratulations on always having enough cash flow to support your expenses !

Savor your good fortune !

The rest of humanity……they might not be so favored as thee.

@Outside – that’s exactly backwards thinking. It isn’t just good fortune.

Talk to anyone who genuinely lived through hard times – like, say, a famine or a revolution. Those people always downsize their expenses to fit their cash flow. They don’t assume their cash flow will always be there to support their expenses. They save for the times they know will come, when their cash flow slows down. They hate spending that savings so they watch like hawks for threats to their cash flow, and by being careful they protect their income.

That prioritization minimizes their risk, so they have a much better chance of having “good fortune”.

These are people who won’t pay for cable TV until they have a nest egg big enough to cover a major medical emergency. They won’t ever pay for a fancy car. They won’t buy a big screen TV until they retire. They don’t take out loans because fixed expenses are killer when your cash flow goes dry.

The Federal Reserve considers these people The Enemy.

WS

No, it most certainly is NOT backwards thinking.

Here are a few questions that may clarify it for you.

ROO stated he never paid any interest hence NO debt.

Was he at all times healthly ( mentally & physically ) enough to earn ?

Was he burdened with a sick/disabled spouse/parent/sibling/child?

Was work available that was sufficient to cover expenses?

Were there no fires/accidents/natural disasters that impacted him ?

Was he paid when he worked above subsistence wages so that he was able to accrue some savings?

If none of the above adversely impacted him, then yes, he indeed was the recipient of good fortune.

Use it up

Wear it out

Make do

Do without

Burma Shave

Agree with YOU WS:

Though never ”rich” growing up, and working to earn my own money from single digit age until 75, I have been very low on money several times during that 70 year span, including working two or three jobs to pay my way through college (with GI Bill at $90/mo for part of that time ),,, and then, at times with no or not enough paid work, doing without, even to the point of losing too much ”lean” weight.

Going without stuff produced a TON of motivation to continue with education of all sorts, and eventually got to where grandma suggested: ”both a trade and a profession needed”; she suggested grocer as profession and plumber as trade, since people need to eat, and after eating…

Brought up two sons similarly, to EARN their keep by paying them fairly for ”piece work” from an early age — at their request!!

Both doing very well, though they have made very different career choices.

If you have ever met someone who overcame a disability to be successful, then you realize we have fostered a lot of victim hood. I know of a small engine mechanic who is blind and an auto mechanic with no legs. One of the best tool makers I ever met had a leg deformity and could hardly walk. Let’s face it, we all could find an excuse not to try.

Wrong. In 1982 at the age of 29 I was laid off and was out of work for 19 months. My wife was 8 months pregnant when I was laid off. I was in one of the 10 worse employment cities in the country (Decatur, IL) so I could not even sell and move-no buyers. I just learned to cut my expenses to the bone. I had two college degrees with honors (agricultural economics and accounting U of I) and I was painting houses, cutting my own firewood, doing whatever needed done.

It was rough, even painful turning 30 and not having a job for 356 of those 365 days, but I learned to control my expenses, fix what I had, and make hay while I could. So quit crying because you think someone else has it easy, because you may not know the whole story.

ROO

And you were healthy enough and bright enough to chop that wood, paint those houses and plow through those books to get those degrees.

Health and intelligence are gifts from Providence.

Unearned.

Ron,

You did what was right. I also did something similar that ultimately required me to work away from home for years. If you take Outside’s argument to heart your efforts are diminished. Don’t.

The biggest takeaway I learned was to live below my means. As did you.

So I second your last statement,…..you think someone else has it easy, because you may not know the whole story.

I suspect these 40 years later you have much story to tell. As do I. Good job…good attitude….I hope it paid off for you.

Golf clap ?

actually your dad was mistaken. i’m not saying that it doesnt pay to save, but I am saying over the past decades it was a much better deal to buy leverage assets, such as real estate, because the Fed and US goverment are propping up those sectors in a huge way.

His dad will be proven totally right in the long run.

In the long run we are all dead :(

Unfortunately, there really isn’t a one size fits all advice that will work in all situations. Remember, Napoleon did NOT want good generals, he wanted LUCKY generals.

Say Gold bugs are eventually proven right, and Gold reaches 50K per OZ or whatever, well, hopefully by that time they are still hale and healthy and they are still able to travel or consume in a presumably broken world.

Mya be but before that we all may be dead!

Think of how many people found themselves over leveraged in real estate in 2006 and 2007 due to the downturn. It didn’t work out for them

Past performance does not guarantee future success. It’s been a long run where being leveraged up is the answer to financial wealth, but that tide might go out.

What if the Fed and government has got no more juice and people and business have to survive without the cheap money support?

My dad was like that too. If he were alive today he wouldn’t believe how things are these days!

Not a good advise now a days. If you are ball deep in fixed rate debt at this crazy low rates, you’d come out golden.

Did your fathers see a 5% inflation coming with zero interest rates on savings? I sure didnt. It is unimaginable, yet here it is and no outrage by the People.

I think we are at record debt, record stock prices, record negative real rates, record Fed balance sheet, record home prices I would say Fed went all in on cheap debt and stimulus. It’s either going to work or they are going to have to do an FDR and revalue money.

Just curious if Mr. Wolf could give his thoughts on the sub prime lending world as it relates to mortgages. Everyone says housing is never going to crash again because lending standards have been tightened. Then again I read other article stating that subprime mortgaging has just been renamed to subprime loaning and really only ARMs have been eschewed.

What has changed is that a lot of the subprime mortgages are now guaranteed by the government (FHA). The FHA, the VA among others also guarantee mortgages with 3% down payments. There are all kinds of big issues out there, but it’s all brushed off as long as home prices rise because you can always sell the home and pay off the mortgage. The issues won’t come to the foreground until home prices fall.

Never fear! The economy will soon bounce back and there will be more jobs, higher salaries, and bigger profits for everyone so these debts will be easily payable. Think of the post war years where America dominated the world markets for steel, machine tools, autos, planes, power plants, ships and oil. The new boom times in the economy will be just like that because dominating the world markets in Cat videos, Spacs, Space Tourism and selling overpriced houses back and forth is going to be even better and create much more wealth than those old fashioned things in the 50’s.

You have captured the essence of the times.

“Honey, how much higher is the stock market this morning?”

vs the guy who pulls himself from bed to toil and hope to break even.

Restauranteurs should have sold everything they had and put it in the stock market 18 months ago…..is that the “help” to main street the Fed had in mind?

The tick is killing the dog.

You forgot everybody just sitting around with their iPhone in hand, trading crypto on Robinhood while stiffing the landlord and getting fat checks from the government. It’s easy street. Everybody’s rich.

You just described the quintessential Reddit user

Yeah!!! Three thousand bucks from the govt and I’M RICH!!!

When “W” (baby bush the lesser) started 2 wars and cut taxes for the rich, I got $300. The average millionaire got $50K.

And we all got screwed because it cost the country a TRILLION.

It’s odd how some of you find it so terrible that some money was spent on citizens during a pandemic.

But when TRILLIONS go to massive corporations/1% all the time….before, during and after the pandemic, you never say a word.

You seem to think that welfare that helps poor and middle class people is bad. But welfare that helps the uber wealthy and giant corporations (they who don’t need any help) is fine.

People who collected unemployment since the start of the pandemic got roughly $43k or more in benefits, not including extra stimulus. If those people live in California and stiffed their landlord (instead of paying rent with their unemployment), then they will get another $20-40k depending on how much they owe.

I am not disparaging people who collect benefits. That’s why those programs exist: to help people who need it. But when people collect those benefits and use them to go shopping while letting their landlord foot the bill for their housing, then it is a problem.

Many small time landlords are struggling financially because some tenants decided to exploit the system at their landlords expense. If you want to attack the top 1%, then go ahead. They deserve it. But landlords are not in the 1%. Many are in the middle class that you speak of, and they depend on rental income to make ends meet, the same way you depend on government money to function.

Cat videos can be turned into NFTs!!! Call it the new Repo. The Reverse Repo will be turning NFTs to cat videos.

Amazing stuff!!!

SC:

” The economy will soon bounce back and there will be more jobs, higher salaries, and bigger profits for everyone so these debts will be easily payable.”

Economy definition:

“An economy is the large set of inter-related production, consumption, and exchange activities that aid in determining how scarce resources are allocated.”

That is, production and sales of goods will increase the economy, not the other way .

I asked a cousin how’s he doing, and he answered he’s waiting for government to restart the economy.

I told him “dude, you are the economy!”

You are gonna need a bigger rug.

This type of article is what hooked me on Wolfstreet. This is the type of amazing details that just paint the broadest of pictures of the state of the union. THANK YOU Wolf “Strike Leader” Richter

Agreed. Lots of detail, great charts, and really well explained.

Two comments:

If you look at net savings which includes government debt it was extremely low last 12 months at near zero. Can’t do that for very long.

No acknowledging bad debt was a mistake the Japanese made after their bust. Best not to play accounting games with bad debt. Face up to what can’t be paid and book the loss. Extend and pretend not the way to have a good economy.

Old School,

“Not acknowledging bad debt was a mistake the Japanese made after their bust. Best not to play accounting games with bad debt. Face up to what can’t be paid and book the loss. Extend and pretend not the way to have a good economy.”

Preceding every bad debt there is a bad loan. Facing up to the bad debts and either writing them down (or off) is at the heart of Michael Hudson’s ideas.

But given what I read online, I think the FED will be investing in a bigger rug to hide everything under.

One little item really caught my eye today. A picket fence builder hired by someone near my home told me that, for the first time in more than a year, they stopped turning new work away AND they actually may have a few openings. Wonder what this means …

trees don’t grow to the sky :)

I think Toyota is starting to drop the “over msrp” push too. Got a guy to offer me msrp today. Yay? Hopefully this is a turning point. People can’t afford their life so this stuff has to come down some. I don’t think it’s the end of the world yet. USD isn’t wallpaper yet, but all bets are off when we hit the next crisis 10 years from now.

The car, boat and RV price thing is the biggest joke of all, and the one that is going to crash magnificently.

I work in the boat business and, while I agree with you that it will crash, I think it’s going to be quite a while yet. Supply shortages are not easing up and as long as supply is restricted, prices will remain high.

Used boats of almost any age are currently selling for as much or more than they sold for new. Who’d have thought that a boat could be a better investment than a money market account?

Yup…But mean while, they can’t keep 225k Supra’s in stock….

We’re in the world are folks getting that kind of money to buy a ski boat??

I have a cabinet builder friend that just said the same exact thing within the last couple of weeks.

Will see what it looks like this winter….

Regarding student loans: FedLoan Servicing and Granite State Management & Resources, who service about 10 million loan accounts, suddenly just quit the business. So that should make the end of forbearance an even smoother transition, right?

Evictions, loan defaults, inflation, pandemics, bubbles all over the economy, $168 trillion in 2008 style derivatives, blah blah blah the list goes on and on. The 2020’s should be a fun time to live through.

I don’t know the specifics of these contracts, but in general, servicers get a small percentage of each payment made. If the payments are not being made, they don’t make any money and still have to keep the accounts up to date. They may be sitting on big losses.

So America is back! The cards are being used. Now all that’s needed is another couple trillion of stemmie to keep the economy booming. I ain’t shy . Gimme ,Gimmie .. When I start whining about inflation I can be reminded that I got what I wanted. However, for the short run…..Hit Me Again.

Might be interesting to see how renewed evictions and foreclosures affect the economy.

The rental vacancy rate decreased from Q1 to Q2. Rents rose at the same time.

Spoke to a young homeowner the other day

I asked with the increase in their equity have

they increased spending. They said no but they are spending all of their income and all of their side gig plus

a little more on credit. They do have pensions so they are not worried.

So just heard Biden and the CDC is now going to order another eviction moratorium. This time for another 60 days, taking it till October. Long enough for Congress to come back and extend it again until the midterms.

I think there should be a consensus that no one pays for anything anymore ever. Everything shall henceforth be for free. Watch GDP boom. Oh wait…

I have been waiting for this moratorium to end for a long time. I live in a rural area where naturally there are no apartments (and housing is ~$400k). I want to move to a metro area (for one year, and then somewhere more ideal) but there are “no” vacancies, ever since this sh it began. I’m at my wit’s end! I haven’t seen you write about this moratorium/its ending that I can remember—why not? Isn’t that a topic for discussion in the financial realm? I am absolutely at my wit’s end.

What is the obsession with real estate?

Live in a van man.

I have not owned or rented in over eight years. I don’t miss it. I don’t pay for municipal upkeep, I enjoy the finest views and I move anytime I like.

I’ve been in a lot of US homes – most are dumps – I’d rather live in a van.

$400,000 for a typical decrepit US shack, with traffic noise and out in the middle of nowhere suburbs? No thanks.

Hi Van_Down_By_River, Long time no see. Glad to know you enjoy your lifestyle. Sounds appealing to an old vagabond like me :-]

@Van—thanks for the reply. You live in one of the most temperate areas of the country. It is 100 degrees right now where I live. I would die if I lived in a van (literally). It’s also -30 degrees in wintertime (that’s 30 degrees below zero). I would die. I could, however, move to a location like yours, so your comment is not viewed in jest.

My rural location isn’t very loud and the metro location I’d move to would be on the outskirts of town as well—I hate noise also.

I bet W is glad he didn’t delete my comment this time, it got a long-gone commenter back. You’re welcome, W!

@Van — oh yeah, I’d get sh0t if I lived in a van anywhere within 100 miles of my locale. Would not be looked upon kindly. Plus we have law enforcement unlike your spot. It’s very “red”.

It seems like the moratorium is causing a housing shortage in urban areas… more so than before. The vacancy rate in my area is under 2% and whenever a rental listing hits Zillow, it gets dozens of contacts within hours. What makes it worse is that everyone looks like a stellar applicant right now with the inflated credit scores, deferred payments, and current landlords wiling to lie to get rid of bad tenants.

It’s a jungle for anyone looking for a new place to rent. Their only viable option is to fight to stay where they are.

To @van’s point, use frustration over inflation as a motivator to save big time. So for example, when your landlord raises your rent by 15-20%, tell them to eff off and go the vanlife route. Then instead of paying 15-20% more, you’re paying 115-120% less in rent. Thing is, had the landlord not raised the rent, you probably would have continued to be a tenant. So in this case, inflation itself ends up being the key motivator for the huge savings.

Heh, you know if that’s true, then we’re already behind the game. There are some people who are just masters at that game for years now.

I hate to say this, but China is starting to look better and better. At least there, they don’t even pretend to have rule of law. Here, the court makes a ruling, the executive branch ignores it. We will keep having pointless tit for tat and power swaps until this country disappears.

Don’t move to China!

I hear Russia and Saudia Arabia are much nicer.

America, son….love it or leave it.

We’re gonna miss you!!!

WOLF

I would be for that…IF….Govt paid off all lenders, public and private. Why not ? It is only another 5T or 10T or whatever. The great reset. Debtors and Creditors all get to start over. Aren’t we about 1/2 way there already?

I have zero debt. What do I get for being responsible?

DC

A lack of interest payments.

DC: “I have zero debt. What do I get for being responsible?”

Less postal mail.

A lecture from the Fed about how you’re not propping up the economy. Get with it, you old foggie, or should I just say BOOMER, spend more and get into debt. We don’t care for this personal financial responsibility crap.

The Fed want to smoke you like weed and throw you away.

You mean to say running in an economy which never has full employment that the unemployed shouldn’t be paid to make sure there is always enough labor? McLuhan said we should pay students to get an education. According to economic demand we should pay them to remain uneducated.

It’s starting to feel that way already…

Savers have been getting hammered for some time now..

And that’s not sarcasm….lol

Courts will strike the CDC down, and it will never pass in congress.

SocalJim,

The White House knows this, and maybe counts on it, but it will give them some time, and they get to dodge the flak they’re were catching from the left wing.

Unless there is immediate Fed Court injunction order against this excutive order citing SCOTUS!?

Wolf,

Did you just seriously call the White House centrist? If the current “left wing” goes any more left, they’ll be on the right.

MCH,

Absolute joke. There’s no left wing in this country. Biden is right wing. The whole country is controlled by lobbyists and corporations. How is any of that left wing?

I hope the US Supreme Court does not use the Old Kings trick of denying standing of a landlord or mortgage holder vs the CDC in a Article 1, Section 10 Right to Contract Clause Petiton. This so called Right To Contract venue is stated as the separate states concern. The CDC should have no standing in state courts concerning a narrow case of eviction . That being said the courts in a civil matter are afflected with arbitrary and capricious results. I am no fan of a Rentier Economy eating wealth out of an economy due to the Fed and ZIRP. That being said the Rentier and their contract needs a fair adjudication.

The SCOTUS does what it wants, then comes up with the reasoning….as Oliver Wendell Holmes pointed out.

The reason for continuing the moratorium is in the first paragraph of the constitution…”to promote the general welfare.”

Oh, and there’s some other crap in there about domestic tranquility, justice, and a more perfect union. I don’t remember anything about saving investors.

Pet-demonstrating again, if you can count an overall picture dispassionately, you will have a pretty good idea of what you MUST choose as the best of what are only bad, available options (most count passionately, however…).

may we all find a better day.

Daz

That’s what I predicted. All you greedy landlords are losers.

Of course the solution is to have Michael Hudson deliver a lecture on the meaning of Jubilee in the Old Testament, and all the religious right organizations endorse his call for legislation to forgive debts entirely, a clean slate heading in 2022.

I know, because they are God fearing men, that Kevin McCarthy and Mitch O’Connell will wax poetic in support of these “old time religion” remedies.

Wall Street not so much.

Sounds like if a landlord is smart as soon as he can get the person out, he should get the property freshened up and sold on a hot housing market. Let some of his rental losses offset the cap gains and get rid of big gov as a business partner.

I get what you’re saying. Steve Keen s version, though.

William Neil. Michael Hudson is not calling for a total clearing away of debt. Just the ones that can’t be paid, and won’t be paid.

But nobody on Wall Street wants to face the music.

So I expect we will just have more of that good ole extend and pretend.

Masked Ghost,

Our bankruptcy laws and courts do a pretty good job at clearing away debts (student loans excepted, but that can be fixed). We have a system in place that works, and has been proven to work, and that needs to be allowed to do its job, and Hudson needs to figure out how this system works and quit spouting off nonsense.

I would argue that each individual stimulus payment was spent many times over in the strange psychology of “gift money,” like a kid with a $50 birthday check who ultimately justifies the purchase of a skateboard, a pair of Nikes, a video game, and three delivered pizzas. The deferred maintenance at Surfside is a haunting prelude.

“The deferred maintenance at Surfside is a haunting prelude.”

I think Surfside is a metaphor for where we’re headed. My guess is some fast-moving natural disaster is the final rebar that fails…

Never spent any

We have already cleared the Irrational Exuberance phase in the investor/consumer cycle of life. We are now on the mountaintop, where millions of New Paradigm flags have been planted. When the descent starts, it will met with Denial. And more Denial. We are not in descent. It cannot be.

Inevitably we will enter the steep downslope of Fear. Then, look out below.

1) C/C balances divergence : in the last 7 dots c/c balances plunged, yet delinquencies 90 days+ moved up.

2) Both payments and 90 days+ delinquencies reduce c/c balances.

3) The banks care about NPls. They will cut profit, take no profit,-

eliminate interest charges & fees, – but keep the balances intact, or send A/R to collection agencies, for a loss, hopefully not for a total write off.

Options :

4) C/C debt test the 2013 lows, perhaps even lower low. A vortex.

5) Lenders and borrowers better get along : balance trading range. Banks profit plunge, or take a loss.

6) US treasury rejuvenate the bank $15T fragile infrastructure.

assets.

On the other end of this free money is me. I’m a contractor. I handle a lot of small stuff. Typically July and August are my slow time. My team of 3 stays very busy, but now for the first time in a year I’m not actively turning down most jobs. While I’m by no means slow, the phone isn’t ringing off the hook. I embrace a bit of a slowdown, and this might be it. July was nuts, but August 1 rolled around and I just started to notice this.

Yes. People are running out of stimmys.

I’m out…… I could use another check or two.

Yesterday, I paid for my dental implant (after I paid for the surgery and bone graft last May). In early September, the doc will drill and tap my upper jaw for a new front tooth mounting device (internally threaded stud). The bill yesterday was $3,181.00. That is for the drilling, sizing, insertion of the implant, and sewing me back up, all this under anesthesia. Medicare pays nothing.

In October, I will need another Stimmi Check to cover the new tooth. I estimate that will be $1,500.00.

Will someone please post a link to the Gov Stimmi Check Application form for me?

Thank you!

Anthony A

Shouldn’t have used anesthesia. You would have saved money like I did. Mine cost $8,000. Ins covered $2,000., Worth every penny. Now I got another one to do.

Swamp, the anesthesia cost was $219 of that bill. I’m a BIG SPENDER as I am running out of years to spend.

I really like propranolol as when you come out there is no hangover. It’s the drug of choice for me after two total hip implants and a couple of dental ones.

I meant Propofol not propranolol.

Has everyone received all 3 stimmie checks? The government knows about me because they notified me I would be receiving my check #3 shortly but I never received it.

It takes me a while to receive them. The government seems to first post it to an account I never heard of. Then they back it out and write me a check.

I’m glad you bring this up, Dave. My wife and I are old school, we’ve saved our money up to do the maintenance that needs to be done on our home, built in 1995 (crappy kb home), in Livermore. Contractors have been jacking us around and blowing us off for too long. I’ve replaced all the lighting, windows, blinds, gutters, outside painting and more in the mean time over the past three years. Now, master bathroom, kitchen, inside painting , floors, all ready to go – but F you guys. We’ll wait a little longer, before getting any more done, when y’all are begging for the work. Make hay while the sun shines, but it don’t always shine on you.

My independent mechanic shop was hard-up during the pandemic. I drove way out of the way to use them.

Turn the page to a few months ago—I made an appt for them to fix a clunk. After a half-hour they said it would cost $900+ to replace front struts (base model very used car). “It’s just a noise, you don’t want to spend that, right? Just pay us $55 for diag fee.” I think they just didn’t want to do the work.

I’ll remember that.

My daughter’s car was running rough and took it to the mechanic and he wanted 1,000 to replace spark plugs and wires, etc.

Said no. Went on Amazon and bought the stuff and replaced it myself. Actually turned out it was only one spark coil that was the problem, but with all new plugs and wires it is set to run for a while.

Just cut every expense and get ready to ride out the downside to come.

Let’s all watch Sleepy Joe’s approval ratings fall to the same level as Trump over the coming year.

So much for balance reductions and savings taking some of the ‘heat’ out of inflation.

These guys are piling it on to the ‘fire’ bigtime.

Who wants to make book on how high the final inflation will go?

Watched Steve Banks today saying its going to be 6 – 9% by year end, probably toward the high end if the Fed and Congress keeps up their insanity.

darn spell check.. Steve Hanke, economics professor at Johns Hopkins. He says it’s the amount of broad money that counts. Just a matter of time.

There are no student loans because they will be cancelled sooner or later in ten years. Anyone who pays in full now is a fool. Even with cars, you can loan a BMW today and pay it for a price of a marble in a few years later. Houses are a different story. You need two marbles to pay for it. Anyways, you are financing your future with a very cheap debt today. Tomorrow, the debt will be worth $100 today. Don’t miss the train…

You may be able to skip a house payment….skip the property tax bill… on the street you go.

In California, a 10% penalty is slapped on late payments. Then interest is added to the unpaid balance until the unpaid taxes are paid. The property owner actually gets 5 years to bring his taxes current or watch his property sold at a public county auction.

Good luck dislodging people who refuse to move even though you are the new owner. Also, if they have federally homesteaded the place, they get to keep a small portion of the equity in it, thus occupy that small equivalent square footage and there’s nothing that can be done to dislodge them.

That’s the common thought. Things don’t add up. Interest rates follow inflation up, but that cannot happen or uncle Sam is broke. Somebody is wrong. Bond, stock and gold market say inflation is not a problem. Maybe all the traders are too young to know how to play this. Junk bond market still asleep?

” Bond, stock and gold market say inflation is not a problem. ”

The first two are living off the gifting of the Federal Reserve…..they are arrangements, not markets.

The trouble with financing a home with cheap debt that is going to get more expensive is that the value of the home is established by price and demand and demand falls when interest rates move higher. So if you think Wow, we bought that home before rates went up, but you overpaid, then 5 years down the road, you find you have lost all of your equity because the market price has fallen.

CP

The worst of the worst advice ever dispatched on this site in the last 10 years.

Could this me the WW3 with China. A financial war. Try to grind each other into the ground through QE and other exotic financial instruments? They the global manufacturer and US the consumer.

“…A China Politburo meeting last week seemed to confirm bets on easing, with leaders vowing to keep liquidity ample. Benchmark bond yields and an indicator of future rates are both at one-year lows…”

A guess, China would start with revaluing their currency, in practice devaluate the US dollar. And they would try do devaluate the US dollar relative all other currencies. Partly by bidding up the price of raw materials all around the world and inflate prices on products sold in US dollars.

Maybe they even try to make the US dollar value fluctuate more relative all other currencies. To the point that raw materials from around the world and goods made in China was sold and priced in Remimbri on long time contracts.

That way they may get more control on the real economy and the US dollar would be more of a jetton on the Wall St. casino. The idea of a reserve currency may also fade, being replaced by bilateral trade agreements.

No debt, no problems. The rest is drama for the average American lacking impulse control…they don’t teach that so much anymore.

Impulse control, I mean.

True, OutWest… Too many Americans do not understand the importance of controlling their monthly cash flow and income streams… Simple control on simple finances makes ALL the difference. They haven’t taught these things in quite a long time.

Some years ago, a friend called me on the phone. She had received a small inheritance and wanted my advice. “I am thinking of investing in CD’s”, she said. At the time, Certificates of Deposit were paying a decent rate, which I told her and I also told her CD’s were a safe investment. She replied: “I know, but then I would need to buy a CD player”.

I wonder if senior people at the Treasury Department and the Fed have nightmares worrying about the possibility of US inflation getting totally out of control as it did in Germany in the early 1920’s.

Are you kidding? They salivate at the thought. Weimar Boy Powell has the pedal to the metal STILL. This guy is a deranged lunatic.

That’s not the way I heard it. He really thought he was going to be able to taper and market informed him there was to much bad debt in the system and he had to retreat. Covid hit and now it’s worse and it’s taking $30 billion a day to keep the over indebted rube Goldberg contraption functioning.

Oops $30 billion week… $30 billion a day before the decade is out.

Depth Charge

Aug 3, 2021 at 11:30 pm

Are you kidding? They salivate at the thought. Weimar Boy Powell has the pedal to the metal STILL. This guy is a deranged lunatic.

I am Glad to see someone can see Clearly what’s going on.

If he is replaced by His workmates it will just be more of the same .

Clearly the Fed benefits the Rich huge Company’s who are making money at the cost of all the rest of the population.

Thank you Depth Charge for your post your a breath of fresh air with no BS . They have dug a Hole now that they may not be able to get out of . Nothing from the president humm

Having witnessed 1st hand the SF Bay area go from 1st world to 3rd world (in politics and literally on the street) over the last 20 odd years it seems this phenomenon is now occurring nationally and in an accelerated manner over past year.

Will be interesting to see how much further the ruling class can push the tax paying donkeys…

So much demand getting pulled forward with stimulus payments and durable goods purchases these days. It may be a teensy deflationary in our shared dystopian future that is being bought off and paid to go away.

For now.

I’m gonna make another small donation because this is another Wolf article that clearly describes how creation of money, via expanding debt, seems to be the centerpiece of United States economy. Debt is a virtual universal in human cultures, perhaps especially since abstract money started to evolve. I’m not sure when the practice of large economic systems intentionally expanding debt came into play historically. The fact is that it’s not something the average citizen keeps their eye on or is concerned about.

It is disturbing to read about this American debt indulgent mentality when one has always avoided non-productive debt (always bought older, value vehicles; didn’t buy a house until market correction; lived in garages converted to tiny apartments, utilitarian clothing, etc.).

But at age 70, I have enough economic stability to make avoiding stress and focusing more on health. Got my BP down to often be around 110, staying lean and eating healthy, can still jog 5k, etc.

Getting stressed about lazy, irresponsible, entitled, and/or impulse driven Americans is bad for health. That’s just the way Americans are, in addition to so many being aggressive, angry bully mentalities. I’ve already hedged by residing in another country, with some of my wealth outside the reach of the American rentier oligarchs. Too many Americans are weirdly ignorant chauvinist people; too many with lack of common sense, compassion, and very little personal decency to fellow countrymen.

Why is there no moratorium on PROPERTY TAXES???

or even a discussion about such?

Historicus

Why is there no moratorium on PROPERTY TAXES???

or even a discussion about such?

Are you serious ? that money is for the people in control and that’s not the tax payers now is it

Chicago burbs property tax on a house is 2/3 for public schools. 2/3 of that is for the pensions. Former School District Superintendent’s pensions over $350,000 / year for Lyons Township high school district and Clarendon Hills grade school district. All info is available online to verify. I can name names if there is any doubt.

Just search “taxpayers united of Illinois top 50 pensions”

Public schools, police and fire dept., local courts, road construction, patching potholes, parks and recreation, etc.

The govt. promised to compensate landlords for the rent they are not receiving. They have not paid most landlords. The landlord is supposed to make repairs or might be sued if a renter is injured due to a property defect. A landlord can not afford to pay the mortgage on the rental unit for lack of rental income, and may not have enough to fix a leaking roof. That could result in damage due to mold and rotting wood, if the place is in Florida during the summer torrential rains. Some may not want to rent out their places for fear the tenants will destroy it. The government is quicker to seize property than to pay for the damages brought by the taking.

An insured “force majeure” act of nature would be a godsend to the landlord to have the tenant vacate the premises.

1) NDX weekly, log, 2006 – 2021 : NDX nerves system.

2) Every bubble need a backbone for support. It must be a sudden sharp drop and above anything below. Sept 2020 hi/lo is NDX backbone. In mid 2021 the bubble lifted NDX up to space.

3) Put a (temporary) dot under July 2021, at the backbone level.

4) NDX anti bubble was 2008/2009 bottom. Put a dot in the wide

open space above 2009. Lets call it dot #1.

5) Connect #1 and 2021 bubble dot.

6) Add dot #2 above Mar 2013 open space.

7) Add dot #3 above Sept 2016 open space.

8) Add dot #4 between Oct 2018 high and Feb 2020 high, in the fused area around May 2019. Dot #4 indicate pain.

9) NDX pain will grow in the downturn.

All of these are NOTHING compared to SS and Medicare unfunded debt.

Just a drop.

That’s also how we already know that MASSIVE inflation is on the way.

We have plenty of money in the good ole U S of A.

Just stop funding the Pentagon and all the rest of the MIC.

You will be astounded how much we will have leftover to pay off debt.

All money is created out of thin air when private banks issue loans. When a bank loans you money (mortgage, credit card, car loan, biz loan, etc.), this is brand new money being created in the bank’s computer AFTER you sign the loan documents.

The Fed is also owned by private banks, but the Fed creates relatively little of the money supply. Most money creation happens when people like you borrow from a private bank.

Why Zillow Stock Is Down 20% In 2021 In The Middle Of A Housing Boom