And the folks who experienced the high inflation of the 1970s and early 1980s as adults expect inflation to hit 5.7% in one year.

By Wolf Richter for WOLF STREET.

When the Fed discusses inflation, and the extent to which it would be allowed to exist, it always mentions “inflation expectations” and that they are and should be “well anchored” because persistent consumer price inflation is in part a psychological phenomenon, where consumers are willing to pay higher prices because they expect higher prices. Companies are getting away with charging higher prices, and because they expect to charge higher prices, they’re raising their wages, but not as much as they raise prices. These inflation expectations contribute to a cascade of higher prices leading to higher prices. And consumers’ inflation expectations are now blowing out.

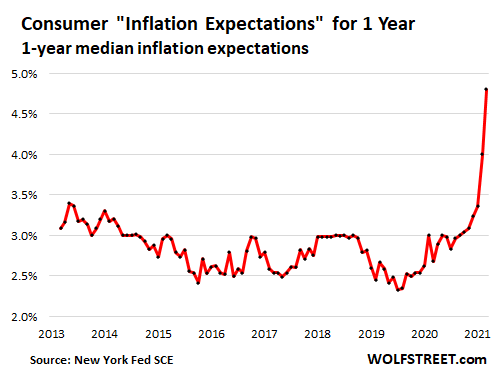

The inflation expectations for one year from now jumped to 4.8% in June, the highest in the survey going back to June 2013, according to the New York Fed’s Survey of Consumer Expectations today.

The under-40 crowd expects inflation to hit 3.8% a year from now. The 40-60-year-olds expect inflation of 4.7%. The over-60 crowd expects inflation to hit 5.7%.

It’s that over-60 crowd that experienced as adults the high-inflation era of the 1970s and early 1980s. The younger ones have only heard about it.

These inflation expectations tracked by the New York Fed roughly match the inflation expectations tracked by the University of Michigan’s Survey of Consumers, whose latest reading jumped to 4.6%.

The inflation expectation whoppers.

According to the New York Fed’s survey, consumers expect to face these price increases over the next 12 months.

- Home prices: +6.2%

- Rent: +9.7%

- Food prices: +7.1%

- Gasoline prices: +9.2%

- Healthcare costs: +9.4%

- College education: +7.0%.

Adding up housing costs, food, gasoline, and healthcare, which for many consumers make up nearly all of their spending and which are expected to rise between 6.2% and 9.7%, it’s hard to come up with an overall inflation expectations figure of only 4.8%. But OK, we’ll cut our consumers some slack here.

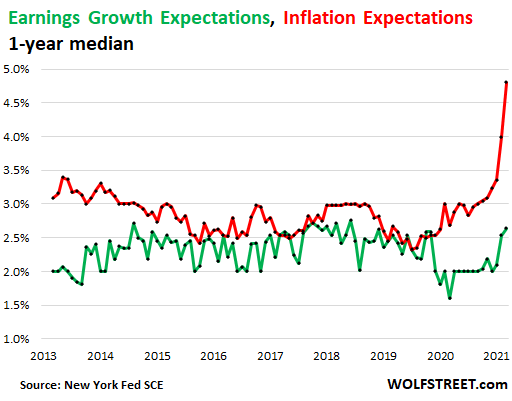

Consumers expect inflation to outrun their earnings.

Consumers expect their earnings to grow by only 2.6%, and their total household income by 3.0% over the next 12 months, even as they expect prices overall to increase by 4.8%.

This chart shows to what extent one-year inflation expectations (red) are outrunning one-year earnings growth expectations (green). If this continues to play out like this, it’s going to get tough for these consumers:

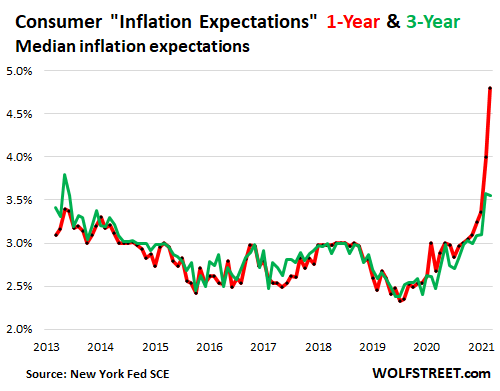

Three-year expectations have jumped, but not as much.

For now, the widely hyped messages from the Fed and the government, echoed by the major news outlets, that this bout of inflation is just “temporary” or “transitory” are resonating with consumers to some extent.

Inflation expectations for three years from now have jumped, but not as high, reaching nearly 3.57% in May and 3.55% in June. The green line reflects inflation expectations over the next three years, against the inflation expectations over the next 12 months (red line):

It’s these longer-term inflation expectations that the Fed is now hanging its hat on, including in the minutes from its last FOMC meeting. But the Committee is split.

On one side, “a number of participants noted that, despite increases earlier this year, measures of longer-term inflation expectations had remained in ranges that were broadly consistent with the Committee’s longer-run inflation goal.”

On the other side, “several participants expressed concern that longer-term inflation expectations might rise to inappropriate levels if elevated inflation readings persisted.”

All of them are behind the curve already. The FOMC meeting minutes also spell out the Fed’s goals: “to achieve inflation that averages 2 percent over time (per core PCE now = 3.6%) and longer-term inflation expectations that are well anchored at 2 percent (now = 3.5%).”

Inflation expectations are among the factors that build persistent inflation. Spikes in commodities and other goods, due to unique circumstances, fire up temporary inflation. But enough of those spikes and enough of that temporary inflation trigger rises in inflation expectations as the whole inflationary mindset changes, and the cascade of higher prices leading to higher prices begins.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

For a comparison.

The last time inflation was close to 5.7% was in 1990.

Interest rates were at 7.00%.

Wages will come no where near to keeping up.

No one, part of the 99.9%, wants inflation. It destroys your standard of living, robs you of you savings and of your time spent working for a wage.

Yet we have those in charge going full bore to create it.

How did we get here? And why can nothing stop it?

Because there’s not yet enough support for an uprising. At this point, anyone fighting back would be a terrorist. You’re only a freedom fighter if enough people are on your side.

Touche and your only a freedom fighter provided the historians decide you won.

I’m just playing the game

and doing my part by raising prices 10% this year

determine next year increase after 12 months more data

RightNYer…your off topic negatively is depressing. You are a better man than that!

Outwest …. your head in the sand optimism is depressing. An uprising against the totalitarian Fed and the rich it protects is totally on topic when discussing interest rates.

Depressing, yes, but how exactly is it off-topic?

My (first) response was an entirely appropriate, if you delete that comment you should delete this thread which is seditious .

You used a pejorative to describe a group of people (and maybe you were being sarcastic), and there was other stuff in it that made it difficult to fix. So it went.

Seditious?

4 years of “resist” and “not my president” is free speech.

But “not my chairman” is seditious?

As long as one takes their shoes off and is not carrying an oversized tube of toothpaste they’re good to go.

Have to agree with you. This mess has developed with the aid of both parties. Public needs to recognize that nothing really changes no matter which party is in power.

Two big issues that never get solved; health care that is priced comparably to the rest of the developed world and stopping endless war.

We need a third party that can force change. But, history shows that is tough to accomplish.

Campaign finance reform is the only solution. And the chances of that are nil. The Black Congressional Caucus, which one would think would be liberal and back more equality for the voters for example, is strongly opposed and has been for a long time. They feel PACs allow Black Congressmen to have equal financing in comparison to their white comrades. Otherwise, they feel their constituents cannot fund them adequately. They are supported massively by the pharma and medical and insurance industries. As long as 80% of Americans get more from government than they pay in, I don’t see where the motivation for change is.

Ross Perot was a billionaire who sold his company and invested in bonds. He ran for president as an independent in 1992 against Bill Clinton and President George H.W. Bush. Perot campaigned on a plan to balance the federal budget. Bill Clinton won the election, then balanced the federal budget, eliminating deficit spending. Deficit spending increases the risk of inflation.

“deficits don’t matter”

–Dick Cheney

There is no solution that doesn’t involve a noticeable decline in future living standards for most people. Virtually no one will admit it.

Voting a third party into power isn’t going to change this reality, especially when most people seek to avoid it and a noticeable minority if not majority wants even more “free stuff”.

SHOfan

‘This mess has developed with the aid of both parties. Public needs to recognize that nothing really changes no matter which party is in power’

It depends upon how one votes (irrespectuve of the parties)

Do you favor those candidates who vote more on the interest of general public vs those who are in the pockets of special/vested interest groups? It is that simple.

Their voting record is public. It is the choice of voter but to excercise that right, one has to be fairly well informed and NOT swayed by blind ideology. We elect those whom we (think!?) deserve and reap the karma of their action.

BTW: A politician is one who is hypocrite, intellectually dishonest and his/her integrity for sale . It matters little which party s/he belong.

When all money is created as Debt, with an interest charge attached, Inflation is inevitable. Bring back the GREENBACK.

inflation is good for bankers. bankers want higher interest rates and a steep yield curve. borrow for nothing, lend at high rates.

at some level i think that inflation over the next couple months doesnt mean anything, but the long-term mechanism for reducing inflation is for us to have a financial melt-down and then inflation and interest rates fall hard.

i just dont see how inflation rates are contained if the markets dont crash.

“bankers want higher interest rates and a steep yield curve. borrow for nothing, lend at high rates.”

Well, now that inflation expectation has been baked into popular culture for the last six months or so, what’s keeping them from doing just that?

People have to stop buying look at lumber

I can’t foresee bankers being thrilled by inflation? A mere 2-2.5%, perhaps, but anything higher will yield diminishing returns? If consumer wages are not instep with inflation, discretionary spending is nixed. CC debt, with usury interest rates, will meet its demise first.

And consumer loans, mortgages, etc., will also decline because borrowers “debt to income” ratio will disqualify many from sizeable loans.

We’re approaching the end of an enormous debt cycle. Private households, corporations, and governments are ridiculously over leveraged. Finding worthy borrowers at this point, is every bank’s concern!

Inflation will not increase these odds for the banking sector.

g

Inflation is an excess of money demand over physical goods supply in the economy. If the Govt stops or reduces deficit spending that would reduce money demand in the economy and there is no direct reason from that why markets should necessarily crash, apart from sentiment. Ie despair at falling demand.

Alternately, if wages do not rise at the same rate as prices, consumers will lose purchasing power and demand will fall that way.

Do you think the stock market will crash if wages get relatively lower?

Didn’t think so.

Your comment caught an idea in my head. What if the whole Reverse Repo was a test. How far could the government go with overnight lending? Could it fund government on an overnight basis?

“How did we get here? And why can nothing stop it?”

Because we have a bunch of greedy psychopaths running things. Something can definitely be done to stop it, but people are too lazy to do what needs to be done. Think “French Revolution” and “lamp posts.”

Depth-remember well that almost all of the initial leaders of la revolution mounted the scaffold at the hands of their fellow insurgents before Napoleon swept away most of that republican nonsense of ‘…liberte, equalite, fraternite…’.

may we all find a better day.

Used to be that really big changes occurred when a strong charismatic leader showed up. Nowadays not so much.

Collective ignorance of economic principles led us here and is the reason why it won’t be stopped

By that you mean…………longstanding deceptive $cabal with tentacles in almost all countries except venezuela,iran,and one other I cant remember???Massive corruption,treachery,and traitorous actions by those public officials who had a Verbal Contract to uphold and Defend the Constitution,or at least abide by our laws and professionally serve the Citizens?They all need to be foiad,classaction sued,sued for breach of contract and breaking Govt. Sunshine Laws as well as Open Meetings laws.Dont forget breaking the law in regards to Constitutional anticonspiracy articles,maybe #14 or 18,basically anticollusion type laws.Get em all on $laundering,fraud,embezzlement,RICO,The Logan Act,The Hatch Act,anything.We the People,The Network have spoken! :-)

Why do interest rates have anything to do with anything? If debt is more expensive surely it would make matters worse for most people not better?

In any case, inflation expectations does not equal inflation reality. According to a survey the WSJ ran a couple of days ago, most institutions expect inflation to drop below 3 per cent in 2022.

So who knows, but without wage rises I find a hard time seeing where the inflation will come from, “psychological phenomenon” or not.

“most institutions expect inflation to drop below 3 per cent in 2022.”

Now that is funny. What is the expectation that fraud numbers that the govt. puts out for inflation will be below 3 per cent? Because, actual inflation that of which the govt. excludes most of out of ‘their’ numbers will be much higher. The govt. excludes inflation so they don’t have to raise SS payments to match inflation like they are supposed to. Riddle me this too, if federal minimum wage is now $15hr or $2,400 a month how come the minimum Social Security benefit isn’t $2,400 month?!

THANK you JD!!

Somehow and soon, WE the Peons, especially WE the elder and more elderly Peons, MUST make the Fed and the GUV MINT paid political puppets recognize the devastation that their lies, damn lies, and ( MADE UP ) statistics force on US.

While I really and truly don’t have any problem with the crooks making a ton of money on their corruption,,, it is only fair that they share at least some of it with us…

Ignore wsj as its owned by the Chinese and is a proven propaganda rag!! :-)

You’re to young to figure it out.

A word you will hear used a lot in the next month is the dreaded stagflation.

When demand drops, prices drop. Easy peasy. We have inflation.

But when demand drops but supply drops even more we have increased prices. This is stagflation. We had it in the 70s and we have it now.

Its amazing so many people refuse to admin their is inflation. Maybe those terrible college econ courses forced everyone to accept the Keynesian universe but reality and data are stepping in and even though the ridiculous CPI numbers (without food and energy!) Is shouting inflation… and here’s a little secret, the cpi inflation numbers are low… very low. Shadowstats numbers are more accurate.

So let me tell everyone reading this. Yo! There is a huge white elephant in the room. His name is inflation and if he doesn’t get peanuts soon he’ll get very “hyper”.

While he remains invisible I’m buying every golden dollar bear strategy I cam find.

Stagflation is painful but when this decade is over my piggy bank won’t be empty.

Wake up!

“When demand drops, prices drop.”

Not necessarily. During the earlier big inflation many companies raised prices to make up for lower sales volume and readily admitted it.

Monopoly power is a wonderful thing. So is raising prices on items already in the warehouse at lower production costs.

“Shadowstats numbers are more accurate [than CPI].”

Although Shadowstats inflation figures may err a little on high side for some consumers, I feel it is more realistic than the fishy, highly massaged CPI-U overall.

And the June 2021 ShadowStats Alternate CPI Measure hit 13.38%! That was a 41-year peak.

If we, for sake of those who argue that CPI is too low and others who posit that Shadowstats numbers are way too high, choose a midway point in between CPI (5.4%) and Shadowstats inflation measure (13.38%) we arrive at 9.39% annual inflation rate for June.

That is probably closer to truth. And it is jaw-dropping.

Yep,Shadowstats good,gubmint=s bad!! :-)

“Why do interest rates have anything to do with anything? If debt is more expensive surely it would make matters worse for most people not better?”

I want interest rates to be higher than the rate of inflation. That way, living on a fixed income as I am (retired, SS), I can actually make some money on my savings. That way the inflation monster won’t eat my savings alive.

I have no job income to offset inflation with wage increases. And at 77, no one will hire me.

Anthony A.

Forget it. Never happen. You are nothing but collateral damage to the Fed. Their priority is maintaining order in the financial markets and eliminating counterparty risks. Add, getting J Powell re-appointed for another 6 years in 2022.

Just go out a play golf and ignore the news.

Self-limitting psychology!!If health is good enough,create your own job.Sell on ebay,etsy,crapazon.Make/refurbish things and sell in garage sale,fleamarket,fairs.Be a selective dogwalker and walk smaller dogs a few hours a day or week.Be a proofreader.

It can’t be stopped because it is baked into the cake. Ludwig von Mises from The Austrian school of economics described it extensively in his book “human action” in 1949. Keynesians just don’t address it, because it serves them well.

2banana…

Dead on!

In 1999 and 2006, inflation was up but not to today’s levels…

The 30yr mortgage was 6%. Now 3% and STILL SUPPORTED by the Fed buying MBSs. Why?

A tremendous departure from the financial history of this nation….where Fed Funds would cover the inflation rate. Why? Because holders of dollars should not get hurt….that’s why.

And now, curiously, interest rates are zero and inflation north of 5%….and not a word of “How can the Fed promote inflation? How can the Fed not react and fight inflation?”

The Fed has been hijacked, IMO. There is no other possibility. They have broken the normality, and some are getting filthy rich off the planned THEFT from the America Worker/People.

Powell should be asked if he is being coerced to do what he is doing…

Something is swaying the Fed…….off the rails.

Unfortunately, Congressmen love the free money and are likely fully invested in the stock market. So, who do you call?

How did we get here?

Print 25% (or whatever the exact % now is) more money . That results in 25% inflation

And if amount of services and goods is lower because people are paid to not work, that % will be even higher

The great thing is that is the yardstick we measure by changes, it is difficult to measure.

Stock market , house prices go up and everyone including Wolf is distracted by the ‘bubble’ that any moment can pop.

But if house prices go up 12% and inflation based on money in circulation is 25%, the house prices actually deflated already 13%. And the owners who sell their house may have to pay a bit more in fake capital gains tax.

So lets go fast forward, money printing will not increase 25% but 100% or and higher %.. that money is indirectly given to Black Rock (helicopter money that people than invest with Black Rock) who buys houses at inflated price. People sell there house (because they cash out or need to pay whatever), 40% of that money goes back to the treasury through capital gains taxes which then basically wipes out whatever gain people had from the helicopter money. But in the end, Black Rock owns the houses and people have worthless money to use for rent.

You will own nothing but be happy…

Black rock tried that in Spain lothere donkey

People need to stop selling to Blackheart devils and sell at a normal price to Human couple or family.Gold,Silver,Copper,water rights,preps!! :-)

“No one, part of the 99.9%, wants inflation” is an awfully strong statement.

If you have a huge mortgage and work in a job where you can demand and get wage increases – why wouldn’t you want inflation?

In what land of Hobbits does a job like this exist?

Except, maybe, a government union job?

“and work in a job where you can demand and get wage increases – why wouldn’t you want inflation?”

Teaching K->12.

c1ue – Because inflation is incredibly destructive. What hurts your neighbour will ultimately also hurt you. It’s not initially as obvious or as direct in the circumstances that you are describing.

Clue

Inflation is an indirect taxation reducing the purchasing power of dollar ,each year. It hurts all, especially the lower 80-90% in the society.

The purchasing power of 1$ issued in 1913 ( when Fed was created) is less than 3 cents now. An inflation of 4%, mean, in 18 yrs one will pay double the amount, what you pay now (more or less) for anything .

When taxes are NOT indexed to inflation, you will continue to pay more and more!

Even assuming the best of intentions, the strategy of debasing the currency to reduce the debt load only “works” if the incomes of the mass population of debtors increases faster than their debts and expenses.

I agree with you that it won’t.

Artificially low interest rates (even if not available to most borrowers) will incentivize more debt and no one in the US has control over the price of essentials which are set in a global market.

There is no way out, without a decline in future living standards which is the unspoken solution practically everyone seeks to avoid. Debts must be repaid, carried at perpetual interest, or defaulted upon. There is no fourth option which provides the majority of the population with a “free lunch” at no one’s expense.

The outcome is a guaranteed decline in future living standards for most people.

Unfortunately debtors also like inflation, and the majority of the 99.9% are in debt. The people most affected are retirees with no debt.

Spend spend spend…Nevemore quoth the Raven.

Well, don’t worry, the government will save us. They do so by more stimulus and bailing us out.

I remember when Bush Jr sent a check to everyone. I enjoyed it, I think it was a paltry $100 or something like that. But thought it was a good idea.

Fast forward two decades, the stimulus checks are several times that amount. Now I see the problem, but hey don’t worry, we can print money until we are blue in the face. Let the future take care of itself.

When will some Democrat suggest sending out “Inflation compensation checks”?

Lmao acting as if both parties aren’t essentially the same economically at this point, with different takes on social issues to rile up their goons. You need to be smarter than this.

Historicus, that is the funniest statement ever!

Uh ho, the Dems didn’t get the joke and think it’s a great idea.

You’re to blame, you know…

“inflation compensation checks” — Now that’s good stuff.

Where do I sign up?

They’re calling it reparation payments. Branding is more toxic and they never waste a crisis.

h

Index-linked pensions and benefits???

MCH

You forgot to mention the Jimmy Carter $50 rebate which was the cornerstone of his campaign. Or the Geroge McGovern $1,000 check for every American.

Yeah, except those were just campaign ideas. Not actual handouts.

I have to say, I agree with the idea that both dumbos and jackasses are more or less the same. In for their own power.

The one thing we can start with is to ban all members of Congress and their immediate family from trading the markets. Of course I don’t expect that Congress will do that to themselves.

It’s screwed up that members of our government can skirt laws applied to the rest of us. If you or I traded on insider info, we’d be going to jail. Members of Congress and their family? Perfectly legal. I don’t see Warren or AOC or Paul railing against that particular edifice.

That, and term limits. Re-election concerns ruin almost everyone.

The Ds want to spend 4 trillion and vastly expand the welfare state. You aren’t paying attention.

I recall that I received a check (or direct deposit) for $600 under the Bush 43 giveaway but nothing under the means tested Obama giveaway. Earlier, I had benefited from the Bush income tax cuts in 2003 and 2001. The tax cuts were not cancelled after the US launched its expensive war against Iraq in 2003. As far as I know, the US is the only modern industrial economy to have cut taxes during an expensive war.

During WWI, Germany did not raise taxes to pay for its war expenses but it did not institute tax cuts either. Inflation set in during the war, but it was not until June of 1922, following the assassination of its Foreign Minister that people began to lose confidence in the paper Reichsmark.

Lucky, I can’t remember what I got from Bush, but don’t think it was $600.

On the tax cut and the conflict, yeah, pretty much. I can’t remember if some of those had sunset clauses, but that tax cut got passed before 9/11 I think, they should have canceled parts of it in late 2002 when the US economy started to rebound. But Jr remembered what happened to daddy, and he didn’t want to be a one termer.

Both sides are too wedded to their power base. Even though it appears that base might be shifting.

I believe it was $600, but maybe you were adjusting for inflation,

MCH

You’ve seen the future.

Either that or rates go up and explode the economy.

Guess which?

Inflation always outpaces earnings for working people, blue or white collars. That’s the point.

I guess the solace is that compared to the rest of the world, and to 100+ years ago, we’re still doing pretty good most things considered. Preps are always a good thing, though. However, I think it is too late for individuals to factor in inflation fears now. The best time to prepare is when things are rosy, not scary.

And yes I lived in the 70s and watched my mortgage jump by 10 percentage points upon 1st term renewal…7% to 17% if memory serves. Plus, I lost my job and worked way to make ends meet. It was a real grind and left a mark on this mark. :-) I would not wish it on anyone.

This is demonstrably not true, otherwise we’d all already have no earning power whatsoever.

“It’s that over-60 crowd that experienced as adults the high-inflation era of the 1970s and early 1980s.”

This sudden, out of nowhere “high-inflation era” was sobering. I was young, but it taught me that the world was not as rock-solid and predictable as my young years presumed at that time. Time to grow up!

So this is how it works.

It’s 2024

Inflation skyrocketed You can no longer make ends meet and need to sell your house.

Fortunately, your home price sky rocketed from $200,000 in 2004 to $2,400,000 in 2024 . After you sold your home to Black Rock (who is sitting on a pile of cash from people investing in their stock mutual fund), you pay the realtors (3%+3%), city (2%), misc cost (1%) and on the remaining 2,000,000 gain,on $1,500,000 you pay 42% federal capital gains , upto 16% state (california), 3% high earners tax (since your AGI is now over a 1M$), may be some ATM .

So after the dust has settled, you have $1,300,000 left which is insufficient to buy another house. You decide to pay your bills and invest in the stock market where the DJ just passed 100,000. You invest with Black Rock mutual fund which happily takes your money and buys more houses.

In 2027 when DJ passes 400,000 and your investments have grown from $1,300,000 to $4,000,000 you decide to cash out. That is 2.7M$ cap gains so you pay again 40% + 16% + 4% = 1.6M so you keep after tax $2,400,000

Unfortunately, prices have 10x since 2021 . Gas is still only $10 but the problem is 98 grade you need for your car is only on specialty order and your EV you are only allowed to charge when it just happens to be your turn for the scheduled brown out in your neighborhood.

The good news however is that Covid-26 is almost under control and Medical mushrooms with free pizza included sell for only $300/ounce

As a retiree living in Chicago you are spot on but forgot the ever-escalating RE taxes and the ever-increasing assessed valuation. True example: purchase price in 1977 $50,000 taxes $600; current assessed value $950,000 projected taxes $20,000. Neighborhood already overrun with foreign investors and hedge funds that deduct all expenses and taxes while the homeowner is double taxed. Politicians love the campaign contributions and the transient renters who never bug them.

right, I forgot that property tax thingy.

And that little thingy is actually why eventually people need to sell their home. Your home of $200,000 in 2024 at wonderful $2,400,000 at 2% property tax is $48,000 of which only the first $10,000 is deductable. If you are living of SS or paychecks that are sticky in amount, you are f*cked.

“In the end you will have nothing and be happy”

–Claus Evil, founder of the WEF.

That’s just one reason folks from IL, including my ancestors, move to FL:

Mostly, I suppose could be proven, mostly, it was due to US41 going all the way down the west coast of FL die rectly, or almost, from ChiGargo, and heaps of evidence that the cops on that route were fairly well known to be as gracious as possible, as long as you were white, apparently middle class or better, etc, though the ”better” usually took the train that ended in Tampa in those days, with another day to go down to from Sarasota to the end of line at Naples.

Many of the oligarchs of the early to mid 20th century had winter homes in FL in those days, from Edison ( although out of NJ ) to Briggs and the Vanderbilts,,, etc., etc…

Even the mobsters of that era at least wanted to have winter homes in FL in those days; and many did.

Now, anyone who is marginal at best, locally to where born,,, just like for eva!! wants to try again to start over in FL,,, and many do,, and many succeed,,, just like always…

IMHO, the coming RE mkt bust will actually hurt FL much less than the last one,,, but the condo bust may be catalyst for the worst ever (condo bust),,, at least for the ones not built with strict and stricter on going inspections by a reputable engineering/architectural inspection team…

Pretty much all the SFHs built in FL since local jurisdictions adopted the ’94 version of the SBCCI code, and subsequent “Florida Building Codes” ,, from what I have seen, will not have much, if any problems, NKA issues, with most her or him i canes,,, with the clear exception of tornadoes ”imbedded” within those storms, in which case all bets are off, and the insurance industry is very clear about that…

As some wise person reminds me when I forget –SO easy these days to forget LOL —

Every place has it’s plusses and minuses for every one..

So, it’s not really too surprising that Bloomberg has a dozen or so houses around the world, eh?

@VV – If you want to take the train from Chicago to Florida these days you have to change trains in Washington, D.C. WTF?

You have a great future as a writer of gonzo fiction !!!

Or sci-fi

That’s Gold Jerry! Gold!

Weren’t 30 year fixed rate mortgages widely available in Canada until the early 1980’s?

To Anon1970

No, they have never been available. The longest term I have ever seen is 5 years. It may differ from province to province. You can get a mortgage for 10-15-25 years to control your monthly payments at the time of purchase, but lord help you when your term is up and rates are on the rise. In times of falling rates buyers choose variable rates and then lock in when a rise is forecast. In rising rate times buyers buy before they start climbing and lock in right away for as long as possible, in my case it was 5 years.

From the Govt website: Mortgage terms

The mortgage term is the length of time your mortgage contract is in effect. This includes everything your mortgage contract outlines, including the interest rate. Terms can range from just a few months to five years or longer.

At the end of each term, you must renew your mortgage. You’ll likely require multiple terms to repay your mortgage in full. If you pay your mortgage balance at the end of your term, you don’t need to renew your mortgage.

Mortgage amortization

The amortization period is the length of time it takes to pay off a mortgage in full. The amortization is an estimate based on the interest rate for your current term.

If your down payment is less than 20% of the price of your home, the longest amortization you’re allowed is 25 years.

There is confusion with the language for sure. New buyers usually write in flexible payment options like every 2 weeks instead of monthly, and insist on being able to pay lump sums on every anniversary date.

It used to be that Canadians would pay their houses off as soon as possible to avoid getting screwed when their term is up. Although I do know people who never seem to pay off their mortgage. When I was 24 my father in law said, “get your house paid off asap. It’s like you just got a $1000 pay raise and you will always have $100 in your wallet.” So I did pay off the house by age 30. Then, I bought a nicer home in a new town following a newer and better job, and paid that house off by age 40. I did this by never buying anything else with credit, including cars, etc. This allowed me to quit my job and retire at age 57, my wife at 55….although I still build stuff for myself ‘on the side’.

I always tell my Canadian friends that if you do not have your house paid for, and/or do not have some great pension scheme to rely on, you cannot retire. My sister in law is turning 56 this August and now gets it. She wants to retire at 65 and is already casting about for supplemental work. The other option is to downsize.

regards

Japan has been doing this for 30 years and their median standard of living has increased. Arguably, largely due to technology, but in total, they are doing well.

Hmmm, well, actually Japan has been in deflation for the good part of 20 years. Salaries have not increased during that time either. Arguably, salaries have gone down, as permanent (‘seishain’/正社員) jobs at companies have been reclassified to temporary (‘haken’/派遣 or ‘gyoumu itaku’/業務委託) roles with no pension or benefits and crappier pay.

Cost of things has certainly come down since the advent of shops like Don-quixote et.al. in the 90s importing the usual flood of cheap made in China clothes, appliances..etc., but salaries and working conditions I think have come down faster, particularly since the Yen hasn’t really appreciated much over the last decade or two.

This also means that Japanese travelling and shopping abroad have less money on a real exchange rate basis than they did in the past (since prices in the US (for example) went up with inflation over the years, but the yen exchange rate didn’t change much and Japanese salaries did not go up either as there has been no inflation in Japan to raise salaries.

As a result, lots of young people who would have gotten permanent roles at companies in the past, are now on crappy temp contracts, so are afraid to marry or start families.

Particularly during the bubble era in the late 80s, it was easy to get a good job with great bonus fresh out of school, even if you had no / lousy skills (yaitenai, kuenai roku de nashi na hito), but that is not the case today, where finding good jobs is hard even for smart people, and many very skilled engineers and bi-lingual people make rather crappy salaries by 2021 standards.

Older people who owned their house in Tokyo are doing OK, but young people are having a harder time of it, something I could see clearly in Tokyo and in the regions over 20 years of being there.

Money is a poor excuse for young people not to marry. Previous generations had even less and married anyway?

Let’s just call a spade a spade: young people these days don’t want the responsibility of marriage children and a family.

Peanut Gallery,

Live in your patents’ basement and start a family there?

Is that the real American Dream?

Having children, whether you’re married or not, dramatically changes how you deploy your income and plan for the future. I know it threw a spotlight on the future for me.

Dang! One minute I was single and didn’t have life insurance or a college savings plan. Even after getting married I only had a little insurance because my wife was still working. When a baby comes along you have to think of how your spouse and children will get by if you die and whether they’ll have enough for college. $3M term life? Ok.

One spouse is going stay home or they can hire a nanny.

My point is that it’s not getting married or living together that causes concern. Those are actually deflationary moves for the couple. There is only one household. One roof. One lawn. Maintenance on one pool. A/C for one = A/C for all.

One Alexa to Rule Them All.

For many, these cost-saving factors make it possible to at least cohabit.

So if it’s not marriage/cohabitation what is it? Children.

There’s another mouth to feed that is only productive if you consider baby poop a marketable product.

And that new family member is going to need a minivan, special baby furniture, special car seat, enough diapers to soak up what’s left of Lake Meade, pediatrician visits, swings and toys, $1,000/month on first baby’s photo prints and framing, $5/month each subsequent child, effing Disney World trips that the little brats will be too young to remember [lowest sentimental memories per dollar ratio ], extra seat on the plane, eat like wolves during adolescence, outgrow clothes before you get them home from the store, and a new iPhone every year.

It might be a lack of responsibility, but it could be viewed as an act of financial prudence.

There’s also much less positive sentiment about the future. They probably ask whether they should bring a child into this world way more than we did. Your typical 21 year old has seen societal breakdown their entire life. The last time I can remember life feeling this chaotic was probably in the late 60s. It really felt like the whole world was coming unglued. We also had preceding and concomitant severe racial tension replete with riots, burning, looting, and violence. Manson, Vietnam, Chicago 7, Kent State, Patty Hearst, JFK, RFK, MLK, Cold War, Rosa Parks, etc.

But before that era people generally felt safe, and after that era people started going to discos and snorting cocaine and stopped caring. AIDS was around but it wasn’t like covid.

It seemed fairly calm until recent years. We had 911 and we’re still sunk in the Middle East up to our chins. We have BLM but no MLK to moderate the debate. Some people hate Trump so much they think his supporters should undergo re-education or worse. I’m not sure what Antifa really is but I don’t think they do either. CRT is one of the most divisive doctrines I’ve ever seen. 1,000 years from now the Orange Catholic Bible* of the Church of CRT will teach that Man is not born with original sin. Only White Man. (*did you catch the Dune reference?)

If I were 30 or so I’d be questioning bringing a baby into this world. Yet my parents grew up during the depression and went through WW2 and still had 2 kids. I grew up seeing Freedom Riders at rest stops, Klan billboards, segregated drinking fountains, the Vietnam War protests, the riots and such, the inflation and gas lines of the 70s and 80s, but we still had kids.

My kids are 27 and 30. I don’t see them being in any hurry to have children.

Let’s just call a spade a spade: young people these days have been propagandized to within an inch of their lives.

And if you REALLY want to get to the root of the problem, ask WHO is doing that propagandizing. Is there a group of people overwhelmingly and disproportionately pushing it?

I am 27. I make $100k, and my girlfriend makes about the same. Our choice is to:

1. Not have kids, continue to build wealth in savings and investments.

2. Have kids now and divert everything that we were saving into housing, child care, health care, and every other expense that come along with kids. Barely save the minimum in our 401ks to get a match, and hang our retirement hope on social security still being there.

3. Try to front-load as much savings as possible before having kids, then when our cash flow goes to near-zero it wouldn’t matter as we can coast to retirement. We should be able to hit $1M invested by 35, then just let that grow for 25 years untouched.

The issue with option 3 is you have to come out of college with minimal debt and a high-paying 4 year degree to attain it, which we did with engineering degrees. Anyone who is in a field that takes time to ramp up in salary, goes to grad school, or takes out a lot of loans is SOL.

Note that we cannot simply move somewhere housing and child care is cheaper, as we would not be able to retain these salaries outside of a HCOL area.

Your claim that younger generations don’t want the responsibility of a family is false. Many want kids but CHOOSE not to have them because they don’t feel they can adequately fulfill that responsibility in an America with stagnant wages and ever-increasing cost of living.

If boomers want us to have kids so bad, why do we have to pay you $500k more than you paid for a house 30 years ago? I can’t finance your retirement through home equity AND afford kids, pal.

Flounder,

Your respond represents an interesting dichotomy: money or kids.

If you’re wrestling with that, don’t have kids.

Flounder, exactly. The current ZIRP/QE environment is a bailout to a subset of boomers who own most of the assets.

Wonderful comments by Michael G. and Peanut.

I just visited my son yesterday while on a town run. He is home on 2 weeks days off. He does not want kids, and is very very wary of a formal relationship. So many of his friends have gone through breakups and it has left him cynical and ‘aware’. He would be a wonderful dad, but has decided he doesn’t want to be one. He earns great money (over 200K with unbelievable benefits), but ….. He just won’t go there. He has two homes and rents them out, and stays in the basement suite of the house in town. He shares two labs with his old girlfriend, she looks after them while he is way for 2 weeks every month.

He’s happy. Great son who is also reliable and loyal.

Personally, I cannot imagine not being married to my wife or being a dad, but each to their own. I guess.

Peanut nailed the answer from what I can see. It is the only explanation that makes sense to me.

Actually for MG:

You left out one very important word in : ” But before that era people generally felt safe, ” to my certain knowledge:

That word is ”white”,,, as in white folks people, not even ” white trash people.” Surely most white folks, of the middle and upper classes felt safe enough, but not at all for the lower classes of whites, not to mention other colours, far sure!!

Hard habits to kick, far shore,,, referring to the world’s people as though they were and are all of european ancestry, and northern european at that, eh?

At this point in our social evolution as a species, I actually feel quite privileged to have been partly raised and partly mentored early on by elders of all the currently objectified razas…

I’d wager that a goodly number of child-bearing age couples prefer to adopt instead– adopt pets instead of begetting children, that is.

Two thoughts:

1. Society expects less of men today. My wife says if a dude is getting it from her, why would he marry? All the benefits without any of the the responsibility.

2. I’ve noticed younger people being terrified of getting married because they saw their parents get divorced and it was painful. So, they’re “life partners” (or whatever) – until they’re not.

Culturally the Japanese place a high priority on group/society. The same can’t be said of many other cultures particularly in the US. Will the US young really take this laying down going forward the way the Japanese have. I have serious doubts that they will.

Why do the Japanese think differently from Americans?

DanR, because they’re homogenous and haven’t bought into the diversity is good mantra.

DanR – Culturally it’s pretty much the opposite of the US. The US celebrates and pushes for each person to be as independent, as much of an individual and lone wolf as possible. It’s every man for himself and the strongest, most ruthless are celebrated regardless of any inequity or disharmony that is created. Most Asia cultures are focused on working, assisting and supporting the group as a whole while the individual comes last. For example, it is common that the surname comes first because the family is the most important, not the individual.

Every Japanese expat I have worked with here in the USA wants to stay here. One Ceo even quit to stay here which at the time was unheard of. Just an anecdote.

None of the people I know, who live in Japan, would agree with your statement.

Unemployment has consistently been increasing – it is low by American standards but consistently has been higher than the early 1990s (the peak).

Precarity has also been consistently increasing – the number of homeless in Japan has been consistently increasing.

Pretty much nothing is “more” than 30 years ago in Japan except government debt.

Looks like a damning documentary on how the Fed has blown this bubble since 2008 is airing on PBS tomorrow night. Its on Frontline and entitled “The Power of the FED”. Sounds like can’t miss TV.

Sign me up. They will have some big names getting interviewed for sure. Hopefully 60 minutes gets the picture as well.

Thanks for the heads up. I would likely have missed it otherwise. It’s a Frontline episode. We’ll see how brave and, therefore, accurate they are.

Trailer for that episode sounds like it might be a hard-hitting, critical expose of the Fed.

Airs tonight, July 13 at 9 pm Central time on PBS.

Was pretty good. Interestingly, in my area it is not listed to be aired again. This is unlike most other Frontline episodes that air 4-5-6 times during the following week.

If America morphed from a capitalist to a corporatist economy and if American Democracy has become a corporatist society, then American democratic capitalism has been replaced by corporatism. The Federal Reserve is a marriage of state and corporate power by its very makeup.

The word, “Corporate” derives from the Latin word for “Human Body”. So if the Corporation is the “human body”, what does that make us? We are simply expendable cells whose mission is to see the Body survives and prospers… Such dark thoughts. This is why I spend so much time playing Solitaire.

Nice. I heard the term Techno Totalitarianism which seems fitting.

The big corporations, have been doing the governments dirty work for quite some time — nefarious bed fellows.

Now dems and repubs are making a total BS claim they are going after big tech. Pandering to public to the core.

Study: Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens [Princeton University, 2014]

Excerpts:

A great deal of empirical research speaks to the policy influence of one or another set of actors, but until recently it has not been possible to test these contrasting theoretical predictions against each other within a single statistical model. We report on an effort to do so, using a unique data set that includes measures of the key variables for 1,779 policy issues.

Multivariate analysis indicates that economic elites and organized groups representing business interests have substantial independent impacts on U.S. government policy, while average citizens and mass-based interest groups have little or no independent influence. The results provide substantial support for theories of Economic-Elite Domination and for theories of Biased Pluralism, but not for theories of Majoritarian Electoral Democracy or Majoritarian Pluralism.

In the United States, our findings indicate, the majority does not rule—at least not in the causal sense of actually determining policy outcomes.

When a majority of citizens disagrees with economic elites or with organized interests, they generally lose. Moreover, because of the strong status quo bias built into the U.S. political system [that describes the overwhelming influence of the administrative state and lobbyists – W], even when fairly large majorities of Americans favor policy change, they generally do not get it.

To be sure, this does not mean that ordinary citizens always lose out; they fairly often get the policies they favor, but only because those policies happen also to be preferred by the economically-elite citizens who wield the actual influence.

There was never a reason to expect anyone other outcome, other than by the naive.

“There was never a reason to expect anyone other outcome, other than by the naive.”

And it’s nothing new at all. It used to be via suitcases full of cash. Now, it’s just more sophisticated.

Two great books by investigative journalist Peter Schweizer:

Secret Empires: How the American Political Class Hides Corruption and Enriches Family and Friends

…one way being via the much used bribe-my-immediate-relative loophole.

Extortion: How Politicians Extract Your Money, Buy Votes, and Line Their Own Pockets

…via the threat of legislation, like the recently passed JOKE requiring China to open any company listed on US exchanges to US standards of oversight… to take effect THREE YEARS from now… allowing three years to milk the Chinese who want to make sure that doesn’t happen… and I’ll bet everything that it won’t.

Stop worrying. More bigger stimulus checks are on the way, thanks to our beloved uncle Joke.

“The FOMC meeting minutes also spell out the Fed’s goals: “to achieve inflation that averages 2 percent over time”

More like: The FOMC meeting minutes never spell out the Fed’s real goals: “to achieve inflation that increases enough to pay down Trillions of dollars of Government debt via hyper inflation. Consumer loses again!

DC and state governments running deficits will need to borrow more and more inflated dollars while their revenues will become less and less sufficient to cover expenses.

Inflation would reduce (i.e. default on) debt if and only if the governments balance their budgets – already impossible.

The Nominalist,

Granted, but California is not in debt, at least not yet. Also since wages (for government workers) do not go up as fast as inflation expenses will not rise as fast.

2%-2.5% inflation RIPS 22 to 28% respectively off the dollar in ten years.

HOW CAN a body that exists with the instructions/agreements/mandates to STABLE PRICES ….promote inflation? Let’s start right there!

Remember the great deflation scare…2009 to 2020? CPI went from 214 to 254….a 17% increase.

Hold the Fed to their mandates….somebody.

Unless all major reserve currencies have the same or worse inflation in which case the status quo is maintained… and there is no reason to believe this won’t be the case for EUR/JPY/GBP/CAD/AUD.

People act as if the Dollar is the only currency where the Central Bank is inflating / engaging in QE, the USD does not exist in a vacuum.

BBR

but I guess the Swiss Franc does, huh?

The Fed has to play it to bone. Hope and luck is their only friend and they may not show up. The chart heads with their mystical crystal ball of delusional pattern ciphering have declared that 60 days is the big start of falling prices and transitioning . I think the Fed has bought in on that same chart Voodoo that is making rounds on the net. So, get ready boys and girls for some serious jawboning. Gut feeling tells me 60 days may put Jerome in the ‘splaining chair because in 60 days even the dumbest will have figured out they are getting hosed by inflation. Inflation sounded good at first to the dumbest . They thought it meant that maybe fast food burgers were getting bigger cause cows were getting bigger.

The NEW Federal Reserve Mission Statement

“It is the Federal Reserve’s actions, as a central bank, to achieve these goals specified by Congress: promote unemployment by providing cheap money to the federal government to dole out and encourage idleness, promote inflation, punish savers and holders of dollars, and promote record low long term interest rates so as to facilitate the pulling of wealth forward from the future generations of the United States””

The new American CPI excludes everything that has increased in price.

Its funny how calmly they mentioned the inflation at first, almost casually like “oh inflation is the result of what we are doing. Yes. But it’ll just be temporary. Although, we don’t know how bad or for how long we will fail at our mandate. As long as businesses don’t expect long term inflation everything will be fine.” The fed officials wouldn’t so willingly cowtow to the government demands if they were not getting filthy rich in the process. Speaks to the current socio-political climate in the US.

“The fed officials wouldn’t so willingly cowtow to the government demands if they were not getting filthy rich in the process. Speaks to the current socio-political climate in the US.”

The Fed partnered up with an entity for the first time in history. And “advisory” arrangement. Say what you will, but things havent been the same since. Causal or coincidence?

The Govt and the Hedge Fund Investor Class both want the same thing…free money. But what of the American worker?

Those on the Fed personally are inflation protected via their compensations and inflation protected pensions…as they push inflation upon us.

Inflation is a TAX…and only Congress, who eventually answers to the voter, can tax, and that power can not be delegated.

So we have a “taxation without representation” situation….ring a bell?

meh. i’ll just substitute flat screen tvs for food and gas, and voila! no inflation for me.

Absolutely brilliant. Advanced level spinning, or should I say chaining?

You have a bright future in government service. You could be more famous than Baghdad Bob and hopefully last longer.

Yep

The price of something you buy everyday vs something you buy every 10 years…

‘Don’t that glass-n-plastic taste yummy!

Please Witchdocktor J, can’t I has moarrrr?

i make my own hot sauce, and enough of that makes anything taste good!

Don’t worry, Biden has assured us that everybody saved $.16 on their 4th of July picnic, and that his plan is working. No, I didn’t make that up. They want you to celebrate 16 CENTS while their central bankers steal your standard of living.

It would be quite fitting to one of those 16cent bidencoins .. to emplace side by side, next to a Caligula denarius!

‘;]

to ‘have’..

Is it possible to see a chart comparing sentiment to subsequent inflation? If this sentiment has predictive value let’s see it. I’ll wager it predicts recessions. Scared people don’t spend unless it’s to hoard. No spending, no business. No business no jobs.

How often is the public right about these things? All they know is their own little microcosm: what they pay for food, gas, clothing, etc. When I was trying to explain CPI to someone who claimed inflation was 6% per MONTH he started asking me when was the last time I went to buy food (two days ago). When it looked like he wasn’t going to catch me with the “how much dies a dozen eggs cost?”* He then resorted to “I don’t trust the government”. Ok, neither does anyone else but in most circles people believe the raw numbers just not how they get processed. In the meantime whose data shall we use? Billy Bob’s Shopping List? (*actually he could have, since I just buy the damn things at the lowest price and I have no idea what it costs)

A lot of the CPI move in May to 5% TTM was highly concentrated in oil and housing, but if you like hard seltzer May was a gift.

The age stratification is not surprising. The older demographic was more traumatized by inflation. There were children of the depression who wouldn’t put their money in a bank after that. I suspect this is in part a big mental MSM- fired stampede although many seem to have no idea in which direction to run.

But it attracts eyeballs – certainly more than “timber prices have plummeted, suggesting supply disruptions might be real and reversible”.

Would love to see that graph of sentiment vs subsequent inflation.

If there’s no predictive power, then these consumer surveys are worthless.

They aren’t worthless at propagating a narrative that prefers creditors over debtors.

And for that, they’re golden.

10-4 jmg:

In fact, all surveys and investigations and so on and so forth that do not provide at least Some ”predictive power” are worth less,,, far less than it costs to do the field or other work to make them…

Lies, damn lies, and statistics was the title of the statistics course at Cal for the various and sundry ”social” sciences that had grown up recently there when I decided to stop working so hard at my chemistry and physics and math, and take the easy way out to a degree…

Talked to the prof, he said OK to just take the final,,, got an A…

‘Nuff said for those who have been there done that with the kind of soft and softer ”science” of the social sciences, including, especially ”economics” eh?

George Soros got a degree in philosophy and then a master’s in philosophy from the London School of Economics. He became a billionaire philanthropist. Not such an easy A.

Economics is a “hard” science much like Phrenology.

Not exactly germane to your question but in this old piece by Dean Baker for the Boskin Commission he shows how CPI inflation during 67-82 was overstated and that most of it was passed on in wages (at least I think that’s at least one of the things he’s saying).

google DOT com/books/edition/The_Joint_Economic_Report/ETIzAAAAIAAJ?hl=en&gbpv=1&dq=dean+baker+mis-measured+inflation&pg=PA239&printsec=frontcover

re: inflation that averages 2 percent over time

Notice the Federal Reserve didn’t bother to specify the acceptable standard deviation for a 2% average. Neither what “over time” means. So if we go to 20% inflation that’s just fine as long as “over time” means 50 years. We’re being set up here. Do everything you can think of to protect yourself.

They never quantified “transitory”….ie , at what point will it have run longer and differently and the Fed admits it is no longer “transitory”?

Why is COST blowing up, but AFRM tanking?

Will inflation “inflate” the stock market as whole?

Would really appreciate some feedback here.

Gold price is related to real rates. Gold will probably explode.

Maybe but Gold is one of the true measures of inflation. Against the dollar, Gold has gone up 576% in the last twenty years and since 1970 by 5100%. It kind of gives you a view of real inflation and can help you look into the future for any big problems heading our way.

I have a similar question. If inflation hits the midway mark, can the fed still keep interest rates at 0.25% and if so for how long? Thats a huge lost in real return. The second part, would be if the fed did keep rates at 0.25%, ignoring inflation, what would happen to the markets, and other assets like real estate?

We are in a new place with money, but history teaches dealing with your problems by screwing around too much with money doesn’t have a happy ending.

One thing I don’t like about it is the system gets built on more and more lies by politicians and central banks.

1) Today, at 8:30 AM, we get the CPI report.

2) Microsoft, which is running on micro-nuke, don’t care about the CPI and WTI.

3) MSFT is leading the Nasdaq pack, bubbling up, in high freq.

4) In 1999 MSFT was rumbling up in high freq, reaching it’s peak in Jan

2000. But MSFT had some issues in their bubbly heads with the gov anti trust, anti bubbles, bureaucrats.

5) Then MSFT filed divorce with the gov, in Mar 27 2000. The tiny weekly inside bar opened a huge gap with Apr 3 2000 open, and the rest of the dot-com bubble was history.

6) During the next decade, MSFT ex Bill, became more humble, soft and flexible, studying options instead of committing, until they discovered that micro is hugely profitable and retained earnings are perpetual, fundamental to the game.

Watch Janet Yellen explain away today’s inflation…

and do so with dishonesty.

She says the current 5% reading was vs “highly depressed” prices from a year before…

BUT, the CPI NEVER WENT NEGATIVE during the COVID crisis….so how were the prices “highly depressed”?

JPM/Chase came out today with a statement that their top priorities are stock buybacks, M & A, and increasing stock dividends. Same with BOA. What is that going to do to help the average Joe?

Stimulus for the board members.

See who the Fed serves?

Punish savers for doing nothing….reward the cocktail crowd in the Hamptons.

1) Home Depot and Lowes are rising vertically, both shorting their thrust.

2) US consumers spending on durable goods, made in China, are helping the Chinese economy.

3) Our insatiable demand for Chines goods exported inflation to US.

4) The pandemic fueled demand for houses, durable goods, used cars

and discretionary goods. Consumers imitative and crowd behavior

accelerated prices, built bubbly charts.

5) Revert to fundamental, to value, will force us to wake up, face reality.

Income growth expectations 2.6%

Inflation expectations 4.8%

How?

As a teen, I worked at a large grocery store during the early 1970s. As an example, soft drinks had been priced a dime for at least the previous forty years. Most item prices in the store were actually memorized, showing little or no change for years. I don’t remember exactly when, but everything changed. Prices began creeping up, then it seemed to be a weekly routine to raise most prices when the grocery truck came.

We used an ink stamper to price items. On can goods, we used hair spray to remove the pricing on remaining stock on the shelf, then stamped on the higher price. Customers would see us doing this and complained about raising the prices on the remaing stock. But the store managers tried to explain that the store had to replace the stock by raising prices on the former inventory.

It was a heck of a mess, it’s hard to imagine running a business in that environment. Soft drinks, by the way, started the 70s at a dime, by 1980 they were 40 to 50 cents.

My recollection was that local stores would just stamp the new price label over the old one. You could just peel up the label and see what the previous price had been. Occasionally you could scan the shelves and find a unit they had missed.

Increasing hamster wheel speed to 12.

This just in, CPI 5.4%. Welcome to the Carter administration 2.0. Tanking stocks and bonds, inflation devouring your cash, and a job-loss recession just around the bend. Get your popcorn out for the coming sh#$@ show of this administration’s “solutions” and “programs” to deal with it all and ironically make everything far worse.

Keep calm- The inflation issues of the 70’s did not start with Carter. The costs of the war and the great society resulted in Nixon adopting wage and price controls and ending Bretton woods during his administration. Carter appointed paul Volcker to the fed who adopted the high rate policy that most credit with finally ending the inflation spiral.

Both parties can be credited with creating the spiral then and now.

Too much money chasing too few goods, at least goods readily available in the Covid Mutated Supply Chains we are now stuck with 1.5 years after the appearance of the Wuhan Flu. With all of the mealy-mouthed jibber-jabber coming out of the oral cavities of the FedHeads, one would think that they would have trouble looking in the mirrors in the morning since they are definitely responsible for a hefty portion of this surging inflation.

Still think the Treasury market is going to go its own way despite more manipulations from the Fed, even the potential for this Yield Curve Control thingy last practiced during WWII. Very, very, very different U.S. economy and financial system today than back in the 1940’s. The FEDS have to feel like jilted Robin Hoods that go to grab another MMT Arrow and the quiver is basically empty. One would think that once a bus driver puts the ride into a swampy ditch, either his or her keys are taken away ( go Maddening Crowd!!) or said driver gets the message about the failings of his or her driving skills or lack thereof AND LEAVES THE DRIVING TO SOMEONE ELSE, HEY, ABOUT THE FREE MARKETS THAT ONCE EXISTED.

There are so many Black Swans flying around today that one thinks he is in a remake of Hitchcock’s “The Birds”. As I type, me thinks we have already entered a major crossroads where a big, black ugly bird has already landed. May that birdie goes by the handle: EVICTIONS.

1) “Help”, a higher pay, with fake $1,500 signing bonus, all over the country is a herd behavior imitating each other, an anti bubble.

2) It allow MCD not to open tens of thousands dining rooms, or a 150-200 sitting restaurants to open with reduce service, tell the cook go f.. yourself, or eliminate old waitresses hours, to cut labor cost and roll back rent.

3) Militants workers will soon face reality : 25,000-30,000 restaurants have closed forever, the outdoor will be over, rent strike expiration day is coming, feast for free, at the owners expenses, is a lost privilege without having a job.

4) Defund excess support to cut cost. Back to fundamental and value, revert to the mean.

So if I just bought a TIP bond how am I feeling? Looks like I might be in for a bonus this quarter, and I am definitely ahead of those who bought fixed yield, (the Fed who is remanding their interest payment) but I am not doing much better than the stock market, but I could lose principle there, and my TIP bond is solid, assuming the dollars purchasing power doesn’t continue to undermine my gains. I see why Bernanke wondered why the government bothers to issue them. The possibility that they will do something that standard investments will not do is very small indeed, but as long as the Fed remains behind the curve maybe it will all work out. Looking at the 30yr this month, but with the public getting all knotted up about inflation, probably not a good time.

We have to attach the WTF moniker to these spikes. It’s not sustainable.

Oil prices must continue upward trajectory or the inflation spike will indeed be transitory.

Inflation is an uncontrollable beast, that is best kept locked up. Release it at your peril.

Thus the wisdom of “Stable Prices”…

the agreement by the Fed to promote stable prices (no inflation) that substantiates and allows their existence

THEY IGNORE this mandate.

Who do we call?

The only things that are “transitory” are the excuses being used by the Fed to justify their deliberate and relentless efforts to re-open Pandora’s box of inflation. That box was effectively closed by the Volcker Fed-induced ’81-’82 recession, and hasn’t been opened since…until now. And the wizards at the current Fed think they can throttle inflation as easily as stepping on and off of a car’s accelerator pedal. Doesn’t work that way…once you’re speeding downhill, you’re going to need to slam on the brakes. Pure physics.

I made a mistake in my last post.

When demand drops, prices drop. Easy peasy. We have inflation.

No. We have deflation not inflation. I guess my college wasn’t so good none either.

You’ve never seen deflation…IMO

Zanet transitory “woke” up call : Detroit big three send their brand new

pickup trucks to Manheim, lifting pickup trucks prices by 50%,

boosting the CPI.

I’m trying to remember what I did during the last

inflationary period 40 years ago.I think I used

to keep things longer.What that translates into today

if we do hit another cycle would mean I buy out

my car instead of another lease.

Your repair shop will raise prices if everyone does this.

So that’s where a calculator or spreadsheet comes in handy. If you can’t completely avoid the adverse impacts of inflation (which you can’t), you least want to minimize the impact.

Not sure why people constantly accuse the Fed and their cohorts of incompetency when the obvious conclusion is that they are acting maliciously. We are under financial attack. Our wealth is being purposefully stripped and transferred to those who are in bed with the Fed.

It started long, long ago but it ramped up with the Covid scam and is now morphing to a large-scale financial war.

Its pretty funny to me that the FED keeps insisting against all economic evidence that inflation will somehow magically go away even though it is the FED that is causing the inflation via its own policies. Real estate prices in my home town (San Diego) are through the roof. I just had a house sold next door for 1.15M that is being gutted, so a absolute fixer now goes for well over a million. A year and a half ago the same house would have sold for about 800K. The price of pretty much everything is going up. $7 burrito down the street from my work is now $10. If you want an Xbox X or Playstation 5, the MSRP is $500, but you won’t find one to actually buy for anything less than around $800 in aftermarket. Point is, between supply shortages, excess demand caused by stimulus and the endless buying of US treasury bonds, we are exploring inflation. At this point I am just looking for a way to load up on debt.

This post predicts the future. The next crisis is a deflationary collapse after a credit binge, probably due to a FED overreaction to the aforementioned binge.

At least animal spirits are flowing again.

Artem…

ever seen deflation? Are you sure it exists, or could exist?

Deflation…that’ all we heard from 2009 to 2020…

CPI went from 214 to 254….17%….

that’s deflation?

Economies that depend on credit growth are inherently prone to deflation when credit growth stops or even pauses.

Unless oil producers permanently cut exports, or the American labor force permanently stays home, this reflation period of 2021 will be short lived.

A month ago I was looking for a new bike trailer rack. I settled on the Kuat NV 2.0 after seeing it at a local REI, which is admittedly a top of the line expensive bike rack. It was consistently priced at $749 retail and sold out almost everywhere. I decided to hold off a bit before making a pretty sizable purchase. Over the weekend I decided to take another peek at inventory and the MSRP has jumped to $849. I found one retailer still selling it at $749 that had a handful in stock, so I decided to make the purchase at what was my holdout price a month ago. If that’s not rapid inflation I don’t know what that is.

APJ – folks that can afford $749 for a bike rack are the target.

LH-fortunately, now, i’ve wised up a little and keep a cover on the keyboard and a rag to wipe the sprayed coffee off of the screen…

may we all find a better day.

The evidence is in. 10 years of QE did very little or nothing to stimulate the economy or create inflation. QE served only to increase asset prices and shift wealth forward from future generations.

Inflation didn’t crop up until they expanded the deficit spending, with QE already in place. The combination results in $3-4T of money printing, which is something that never happened before. This is what created the inflation. When more money chases the same amount of supply, inflation is inevitable. Given that money supply increased by 20%, expect inflation to move up 20% as well over time.

That said, the money printing will continue, and so will inflation, so the 20% is just a cover charge. The economy currently requires $2-3T of annual deficit spending, funded by money printing, to stay afloat and preserve jobs. Nobody should say the inflation is transitory unless they can say the government will have no future need to print money.

Until there are structural reforms like massive tax increases, money will be printed, and inflation will be as persistent as the sun.

The real question is this: will the top 1% (the asset holders) accept substantial tax increases, or will they attempt to distract and divide society and further concentrate wealth on the path to instability.

You also print money when you create credit by borrowing from a bank. Personal credit is a much more powerful inflation driver since the money is usally spent instead of saved.

Bobber, 10 years of QE fueled substantial inflation in four major expenditure categories: Shelter, Vehicles, Education and Health Care…a mix of both physical products and services, not just “assets.” The current Fed’s irresponsible actions are now fueling inflation in the stuff you buy at Walmart, Kroger or Home Depot.

People will soon change their definitions of needs and wants.

Touché

Massive tax increases = structural reforms?

Da*n I’m still trying to navigate through that hot mess called the IRS.

So if we only tax more it will take care of these monsters?

Got it.

If you have runaway federal spending, you can fund it with tax increases, or you can fund it with printed money from the Fed. Funding it with tax increases is a solid money approach that gives and takes from the economy, and is much less likely to create inflation, which is a tax on Average Joe.

Let’s be practical. Inflation is a tax. What you pay to the IRS is a tax. From the average Joe, there is no difference. The Federal Reserve is the same as the IRS.

Fred : CPI for all urban consumers, ex food and energy : 278.14.

1) Last year bottom was 265.64 in May 2020.

2) June last year : 266.28.

3) [278.14-266.28] : 266.28 = 4.45% Y/Y.

4) Last month, in May : 275.72. [278.14-275.72] : 275.72 = 0.88% M/M.

5) In Apr : 273.70. [275.72-273.70] : 273.70 = 0.73% M/M.

6) May 2021/ May 2020 : [275.72-265.64] : 265.64 = 3.8% Y/Y.

7) Both the annual and the monthly CPI are rising.

8) The 10Y = 1.63%. 1.63% – 4.45% = (-)2.82%. JP save US gov :

$28T x 2.82% = $790B in real terms.

9) JP, please stay !

Just wait until the middle class has to start paying their student loans again…

We’re talking perceptions here. (reality could be worse)

If what you are ‘perceiving’ isn’t liked or wanted, cue an expensive MSM advertising campaign and rigorous promotion of ‘Transitory’ in the talk shows, look how they controlled the ‘covid’ narrative.

You will be made to have the ‘correct’ perceptions.

Well, price inflation, shrinkflation, and services inflation are bad. But the worst is tax inflation. Remember in addition to price inflation there is wage inflation. Good for your pay, but the wages (and pensions) of local and state bureaucrats increase faster than private companies. There are some county bureaucrats here making over $400K which basically lasts forever as the salary gets changed to a pension and a replacement guy is hired.

Not much you can do when you get that tax bill.

Expect 4.5-6% inflation for the next three years.