China and the tax havens rule!

By Wolf Richter for WOLF STREET.

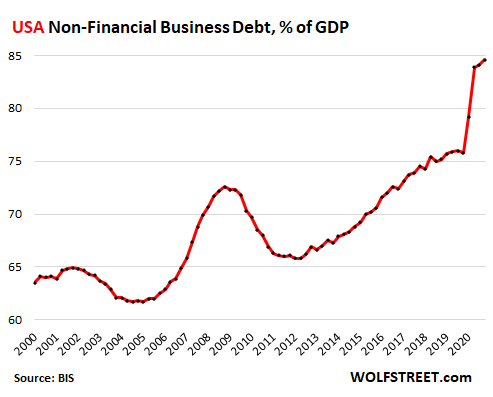

The debt of US nonfinancial businesses had already surged in recent years, but when the Pandemic hit, businesses went on a borrowing binge as the Fed has repressed interest rates to record lows even for the riskiest corporate borrowers.

These debts of nonfinancial businesses – including corporations and businesses that are not incorporated – jumped by 9.1% year-over-year to $17.7 trillion in Q4 2020, according to the Fed’s Financial Stability Report. This amounts to 82.4% of nominal GDP. The Fed has been ruminating in its financial stability reports about the risks posed by corporate debt.

These debts are from nonfinancial businesses and exclude banks, nonbank lenders, insurance companies, and other lenders because lenders borrow and then lend, and including their debts would lead to some double-counting.

But what is happening in the USA pales compared to what is happening in some other countries, such as the corporate tax havens and financial centers of Luxembourg, Ireland, and Hong Kong, and of course in China, according to the data released today by the Bank for International Settlements (BIS) for Q4 2020. It leaves the USA in ignominious 22nd place!

This is the incredibly spiking US nonfinancial business debt hitting an astounding 84.6% of GDP, per BIS (matches the Fed’s figures in terms of dollars and tracks closely in terms of percent-of-GDP):

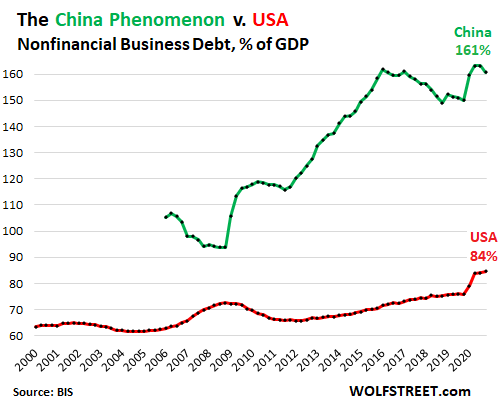

The China Phenomenon:

And then there is China. In dollar terms, its business debt, as the economy grew rapidly during these 15 years, multiplied by a factor of 10, from $2.5 trillion in 2005 to $25 trillion in Q4 2020. And as a percent of GDP (all in local currency), its business debt soared from an already sky-high 105% in 2002 to 161% in Q4 2020 (green line).

In 2016, China’s authorities started to attempt to deleverage their largest and most indebted nonfinancial companies, many of them state-owned or state-controlled. This included taking apart some overleveraged conglomerates. These efforts produced some results, but reversed during the pandemic. The US nonfinancial business debt-to-GDP ratio (red line) shows just how out of whack China’s business leverage is:

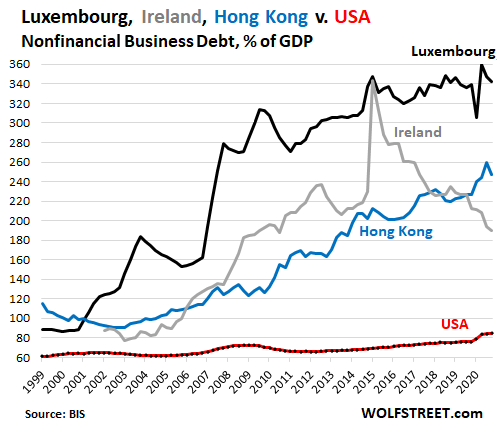

But China is only in 7th Place. Luxembourg, Hong Kong, and Ireland win.

The top three places in terms of the business-debt-to-GDP ratio are the corporate tax havens and financial centers Luxembourg (with business debt at an astounding 342% of GDP), which amounts to over four times the ratio of the USA (84%); Hong Kong (247%); and the favorite for US corporations, Ireland (190%). Many global companies are headquartered, sometimes on a mailbox basis, in these places, and some of their debts are registered there, though they were marketed to investors in other countries. Note the puniness of the US ratio (red line at the bottom):

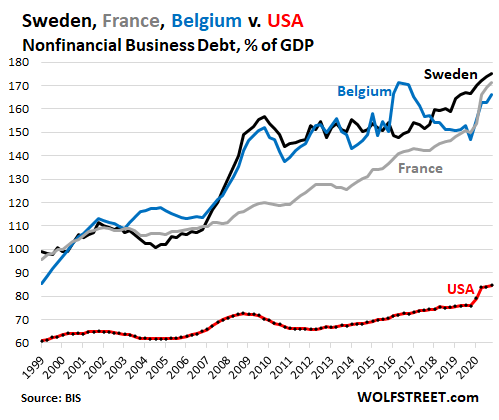

4th to 6th Place: Sweden, France & Belgium:

Sweden and France have immensely indebted companies. The Bank of France has long lamented the risks associated with the indebtedness of the French giants, many of them partially state-owned. In Sweden, the business-debt-to-GDP ratio rose to 175.3%, in France to 171.1%, and in Belgium to 166%, still beating China.

8th to 10th Place: Norway (155%), Netherlands (152%), Singapore (141%):

They’re behind China (7th place) in terms of business debt to GDP. All charts below are on the same scale as the chart above for Sweden, France, and Belgium, ranging from 60% to 180%. Singapore is a major financial center:

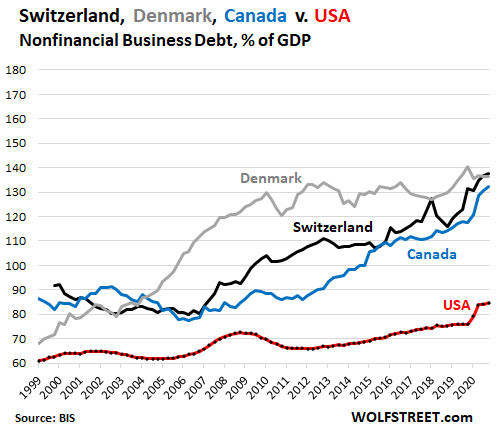

11th to 13th Place: Switzerland (137%), Denmark (136%), Canada (132%):

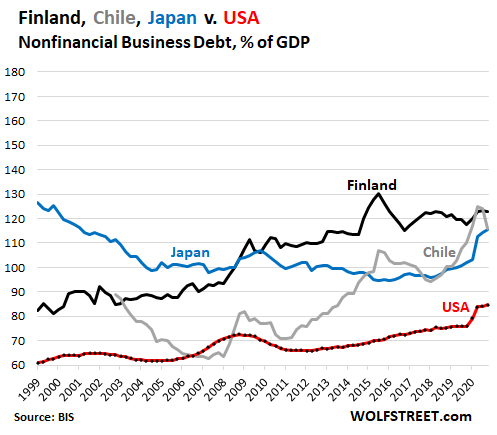

14th to 16th Place: Finland (123%), Chile (116%), Japan (116%):

Japan’s businesses were deleveraging for about 25 years, following the blowup of the bubble in 1989. Their business debt to GDP bottomed out in 2016. But all along, they’ve outdistanced the US debt-to-GDP ratio:

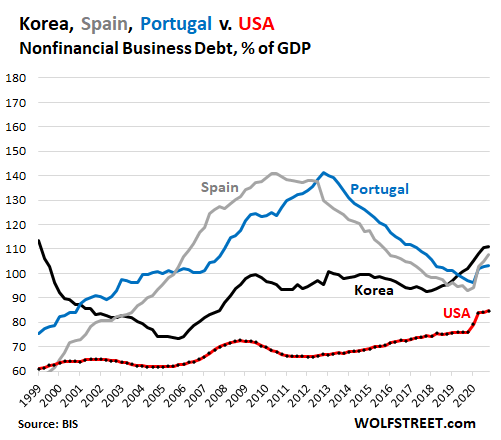

17th to 19th Place: Korea (111%), Spain (108%), Portugal (103%):

Korean companies deleveraged for years coming out of the 1997 Asian Financial Crisis. Spain and Portugal deleveraged after the implosion of their enormous housing bubbles led to their own financial crises mixed in with the euro debt crisis. And the deleveraging hasn’t stopped yet. What happened in 2020 that caused their percentages to tick up was that GDP collapsed:

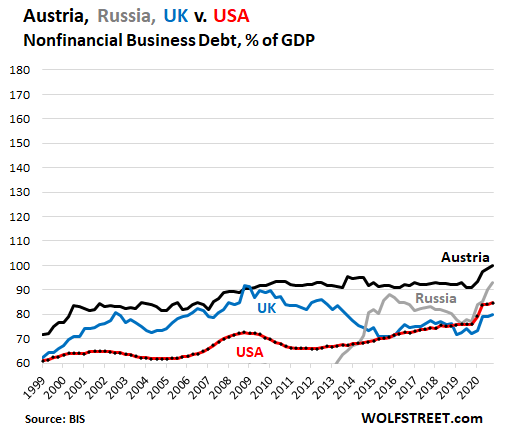

Finally, the USA, in 22nd Place. In 20th to 23rd Place: Austria (100%), Russia (93%), USA (84%), UK (80%):

In recent years, Russia’s corporate giants, many of them state controlled and big exporters of crude oil, gas, minerals, other raw materials, military equipment, and some other products have borrowed heavily in foreign currency and have moved Russia into 21st place, just ahead of the US:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

It is interesting that the three countries that have seen their business debt ratios drop the furthest over the past decade are all in the “PIIGS” group. Portugal, Ireland, and Spain. They all seem to be down by a third or more since the Great Recession hit. Are Greece and Italy similar?

Basically, it might have been that they’ve gotten to a point where nobody sane would lend to them any more. So, as a natural consequence, their debt started to shrink.

One wonders though, where is all of this leverage coming from? I wonder if it is possible to lend with money that you don’t have, and then keep on doing it until it’s some kind of crazy pyramid scheme.

It’s weird that people are still lending the US money in some ways, I suppose that’s because it is seen as a safe bet. What would happen when that feeling of safety goes away. When foreign buyers no longer wants the dollar because they could get safer and better returns elsewhere. When the US buyers of bonds are tapped out because of their obligations….

Feels a little scary.

“When foreign buyers no longer wants the dollar because they could get safer and better returns elsewhere. When the US buyers of bonds are tapped out because of their obligations….”

Then the Fed will just print more money to buy Treasuries nobody sane wants (or the Fed will print if the 10 yr threatens to pierce an awe-inspiring 3% due to lack of demand.

It is clear after decades of this, that DC never had any other plan to pull out of its debt death spiral other than the Fed-Treasury circle jerk.

In this way, DC will “fix” its unrepayable debt by simply printing – silently (if not for the internet) stealing the purchasing power of every US dollar holder.

It is for this reason that looking only at corporate debt (and not also government debt and financial sector debt) gives a misleading picture of US economic health – which right now is already on printer life support.

It is the aggregate debt level (business, gvt, and financial sector) that matters…since any significant debt default will have a domino effect upon all the sectors.

but you digress in that when Exporters no longer want fiat $dollar

then merica gets no goods

ie ultimate shortage

Yup China is going to voluntarily give up their export sector. Nonsense. Maybe if we go to war. But otherwise, forgetaboutit.

Hard to tell by your short comment, but if you are rolling out the old chestnut, “China has no choice but to give the US infinite credit (in the form of ZIRP’d Treasuries) in order to “preserve” its “best” customer (who is nevertheless a hopeless deadbeat)” then I would make a few points,

1) There are a universe of other far less indebted nations to sell to,

2) Chinese export factory production can just as easily be used for domestic consumption (1.4 billion Chinese),

3) A paper paying customer whose paper continually depreciates and don’t have much worth buying, ain’t much of a customer.

There are a lot of toxic Econ 101 myths still floating around that 30 yrs of empirical reality have kicked the crap out of…but biased parties still invoke them.

‘1) There are a universe of other far less indebted nations to sell to,’

Paying with what? Of the world’s 180 currencies, only 17 are fully convertible and only 4 are used by large markets. Once outside US$, euro, yen and UK pound zones, the universe shrinks fast, e.g., Danish is convertible but market is small.

Don’t even ask about paying in rubles.

Nick,

In the final analysis, when you sell a product you want to receive equal or superior value in return.

If you are offered payment in a continuously depreciating currency, heavily manipulated by the fiat’s sovereign, the true alue of what you receive as sale proceeds is heavily in question.

Ditto for selling to nations whose export mix consist of 1) nothing you need or 2) nothing you can’t get cheaper elsewhere/domestically.

I don’t know if your currency convertibility stats are right or wrong…but I do know that the world is filled with nations whose export mix (definitely in aggregate) can match that of the US.

So,

1) If the US is continuously depreciating its means of import pmt and other nations aren’t…the US is in trouble.

2) Even if other such countries *are* also continuously depreciating their fiat (or manipulating in other ways via less than full convertibility) China could still cut barter/non currency trade deals with them.

Note: The US could make use/be compelled to use non-currency, intl trade barter deals as well.

When currencies become unreliable (because their sovereigns are abusing them) traders/exporting nations will cut currencies out of the loop by engaging in barter.

“One wonders though, where is all of this leverage coming from?”

It is all coming from Central Banking and Interest rate suppression.

1. Conjure money from thin air (double entry accounting on a balance sheet).

2. Put conjured money into Fractional Reserve Banking system and watch exponential debt grow like cancer.

A natural, market determined interest rate (the real time cost of money), seems to rest around 3% above inflation. So, naturally the orgy of borrowing with a 6% subsidy compounded is pretty hard to stop. Until it stops.

Put me in that cursing Fractional Banking camp. If that isn’t money printing, I don’t know what is. No other corporations have that license to print…although borrowing schemes, debt schemes, and creative accounting are damned close to printing, if not actually doing it.

And I doubt ANYONE knows what the hell this mythical “natural market” is.

Yep, since money supply is the result of base money lent out and returned and lent out again and so on as it gets redeposited at the bank and the bank proceeds to issue more credit subject to mandated leverage limits. Most everyone with a brain and who had a bone to pick with the Fed over the last decade figured this out. In and of itself this is nothing to be shocked about. It’s just how it works. However, you can look at total bank deposits to get an idea of how leveraged the system is. The growth rate of bank deposits over the last 20 years blows GDP growth out of the water. The amount of income relative to debt keeps shrinking. Lower interest rates help the expansion, but the banks are finding that even though they’re flush with base money they can’t justify issuing more credit to individuals or businesses. The Fed’s only hope is to pare down debt levels with inflation, or the dreaded deflationary implosion will eventually come. The good news is most of us will survive either way.

The money is coming from the fact that central bankers have crowded out investors by printing money and buying assets. The big question is whether rising inflation will force the central bankers to stop feeding more money into the system. If/when that happens, these debt bombs will implode. But noone knows if that will actually happen.

Real estate is another source of massive debt. But if we have interest rates forced higher by inflation, then real estate prices will start to collapse.

The insane supply-demand imbalance has created a short term bubble in real estate prices, but within the next couple months a massive amount of supply will hit the markets as people finally feel like selling their homes. Real estate investors are also pumping the market higher, but that money will soon realize the downside that exists when people simply cant afford the payments and prices have to adjust downward.

The trend of people moving away from big cities is in the long run a trend that will decrease real estate prices, unless the democrats allow enough people to cross the border to pump up the demand for housing.

MCH:

Maybe I’m way out in another planet but if the dollar globally slips too much (what will that point be?) the only real option to me is to raise our interest rates across the board in protection???? And viewing the condition of our economic system at the present that will be a disaster as we look back not to short a time ago at the end of 2018 beginning of 2019.

I see it as the only solution, simple and murderous!

A rock and a hard wall!?

‘What would happen when that feeling of safety goes away. When foreign buyers no longer wants the dollar because they could get safer and better returns elsewhere’

Where is that ‘else where’ even remotely ast this point?

Remember nearly 16-18 Trilllions are still in NIRP!

Doesn’t the USA do that? If all the dollars outside the USA came to the USA they would crash the economy.

Yes, but they were much lower to begin with. They never had the kind of housing bubble that Spain and Portugal had. Spain’s housing bubble and subsequent collapse was one of the biggest in the world, in terms of percentages, if I remember right. Italy and Greece didn’t have anything this big.

Thanks Wolf once again for these superb charts.

Yes, thanks.

Although totally confused about the overall picture it paints, it is interesting to read what picture it conjures up in the minds of those that have more business and economic knowledge (and I suspect much more wealth than I, likely due to possessing that knowledge).

I long ago chose to learn how more tangible things really function for earning my income (stuff you hold in your hands, and knew I didn’t want a desk or office job), and Biology, which to me is the only “real” action going on. As a consequence, I have just bumped along near the economic bottom all my life.

But I have no regrets, made it to 74, excellent health, (except for trashed back, like most all who work with brains and hands end up with), a 500 sq ft apt, internet, and am very interested in what happens next, or might happen.

I recently watched F-1 at Monaco, and would really like to know just WHO are those people who can back their huge yachts up to the track to watch, and then fly off to wherever….I suspect they have a LOT to do with this article.

Good website, much better than MSM talking heads collected here.

Think I’ll go read up on the BIS, although I have before, along with the IMF, and see if I can’t improve my own picture.

I know several former Spanish property owners. Corrupt local authorities had granted many building permits against their own rules. Then, some foreign homeowners had their properties bulldozed with no recompense when the same authorities decided the permits they themselves had granted were illegal. This effectively killed foreigner home purchase, and a large number of existing owners sold their properties also. The market is still dealing with this glut. Portugal, Italy, and Greece did not do this. There were also some dodgy building permits issued, but the authorities have stood by the original permits whilst forbidding new ones. In Greece, a very large number of people pay nothing like the correct amount of tax – tax-dodging’s practically the national sport. If the locals like you (I have a friend in this category), then you pay minimal tax also, property and business. You get the nod when the tax inspector’s ‘surprise’ visit will happen. This is very easy in the islands – you get a phone call when the tax inspectors board a boat to your island – everyone knows who they are, and the inspectors don’t want the hassle of catching people either. If they don’t like you (often true of Germans, because of WW2), you pay full tax.

Southern Italy has elements of both Spain and Greece’s corruption, to a smaller degree, plus of course the Mafia. I do not have any direct information on Northern Italy or Portugal, but understand them to be better.

What a world we live in. It’s like everything they taught me in college isn’t how anything is actually performed.

Always ensure all your teachers have spent time in the real world. I recall my first principles of engineering design lecture. The professor had his own international company also. He listed about 8 principles, then wrote in huge letters – one per board -over the top C-O-S-T! We got the message ;)

As some have stated where did the money come from. Equally interesting would be where did all that money go:

-Stock Buybacks

-Option payouts

-Bonuses

-etc.

Does this explain the rapid growth in income inequality over the past 10 years.

Spot on S.

One post always gets it on this site. No fail!

Where did the borrowed money go?

Debt has been around as long as civilisation and it will be around as long as humans are around. It is no problem at all if you pay the interest and return the capital when it’s due.

If you can borrow capital at 2% and invest it in a windmill in the sea which returns 2.5%, you’re making 0.5%. Everybody is happy, no problem. In 30yrs when you need to repay the capital that’s no problem if you’ve saved or amortised the money from the 0.5%, in which case, all future income is your’s free because you own the windmill. If you haven’t saved the money, you need to roll it over which, again, is no prob if you can roll it at 2%. However if your roll is at 3, 4, or 5% you are seriously stuffed.

It’s all about what you do with, and how you manage the debt. Who wouldn’t borrow at these rates, you can make money on practically anything. If rates go up the roll-overs for poor earners could be stuffed and similarly new projects could have to make better returns and you might have to abandon your Windmill and invest in an Oil Refinery.

As always, brilliant how W brings all these issues into a single series of charts and you get a gist of what’s going on in all the different countries. Are the big borrowers big investors, if so, what in? What terms?

My interest is Russia which I know has been making big private investments in recent times but I don’t know what rate they are paying. Much higher than ours I think.

Thanks Wolf!

I guess what are we trying to make of this? Yes, the non financials worldwide have borrowed like crazy? But these facts seem to not really yield much guidance.

Be wary of companies just because they are registered in Luxembourg?

Which sectors (and countries) are going to implode first if and when the Fed starts raising….?

RK

I am kinda with you here. Wolf’s charts / info never cease to amaze me, but I am lost in the context.

A country with non-financial Corp debt at 350% of GDP means ???? If “financial” Corp GDP is like 25% in that country, does that basically mean that country’s non-financial corporations will soon be owned by Financial corporations? Owned by the govt?

Beardawg,

You’re making things too complicated.

Ford Motor Company is a nonfinancial business, and when it borrows money, it is the debt of a nonfinancial business, and this is what is counted here. In terms of the debt ratio, it doesn’t matter who owns Ford Motor Company, whether it’s public shareholders, one individual, or the government.

Ford Credit is a financial corporation — it borrows money to lend money — and therefore its debts are NOT counted here to avoid double-counting of debt. It doesn’t matter who owns Ford Credit, whether it’s another corporation (Ford) or the government. It’s the issuance of the debt that matters, not the owner of the company.

In addition, companies that are headquartered in tax havens can issue debt registered in that tax haven (such as Luxembourg), and then this debt is listed under Luxembourg’s ratio.

Context being US corporations are not investing as heavily as many foreign companies. Private debt equals public good. Corporations buy back shares instead of investing in R&D. Lack of investment means labor shortage. Corporations repatriate profits, (like Roman tribute) and workers move into the service sector because we make nothing but hamburgers to go. There is a labor shortage because the workforce shrunk.

This ratio is intended to inform a lender of the ability of a borrower to pay off the debt – like debt-to-income. But it doesn’t say anything about future debts or future incomes. The other problem is it compares $ to $/yr so the units of this ratio is in years. Years of what?

Not all debts are the same. Singapore’s debt is so high because of how CPF and a bunch of other stuff are structured. As many well informed sites will tell you, net debt to GDP for Singapore is zero.

This is also why Singapore’s Debt Rating is Triple A.

Never mind, I saw countries and I thought Wolf’s talking about Government’s debt to GDP.

Mea culpa.

Singapore CPF = Central Provident Fund, apparently the national pension fund or “sovereign wealth fund” or similar.

Singapore’s debts isn’t entirely due to the CPF. It is the product of both a high cost of living primarily due to a property bubble & a weak State-owned business sector.

For those of you who don’t know Singapore well, Singapore’s property prices is the 2nd highest in Asia just after Hong Kong. Singapore has a mix of 80:20 in terms of Public housing/Private owned housing. CPF scheme allows people to use their CPF balance to pay property loans & mortgage interests. CPF scheme creates an over excessive investment into real estate.

Real estate prices in Singapore has been ridiculous & landed high end Good Class Bungalows (GCB) price per square foot had gone up exponentially due to foreign buying.

The other factor for S’pore’s debts is the Singapore government controls 70%-80% of the Singapore Economy through state-owned enterprises. Any economic student will know the ineffective performance of state ownership in business. Mostly high debts, poor management & an attitude which is inconsistent with private entrepreneurship.

Great read, can we see how Australia sits on these charts?

It’s at 72% of GDP.

US budget deficits under #45 roughly doubled…and he tweeted interest rates down to nuttin’. Brilliant.

Warning Will Robison Danger, Danger Will Robinson…Error…Error…Error…

“Nonfinancial debt”

One of biggest and greatest flaws of the USA Paper Tiger capitalist monopoly conglomerate model is it’s vastly too big “Financial Debt” Economy.

Which happens to be the biggest in all of the Entire Known Universe.

Comparing other nations non financial debt to USA financial debt is like comparing taxes to what funds the Federal Govt’s spending.

I spend a lot of time thinking about why the US doesn’t have hyperinflation, despite “experts” predicting this for a decade. Now we have trillions suddenly printed and still no boom. Why?

This article (nice job wolfie) shows despite the printing, businesses are still solvent in the aggregate. Velocity is also a factor. Only looking at money supply and ignoring velocity is probably malpractice. I once read that the fed was looking at velocity and hoping the printing would stimulate more “movement” to get GDP going. But mostly no dice. The theory is velocity and lending are low because there aren’t enough credit worthy customers.

I think the short reason we dont have hyperinflation is the price transparency of the internet. Companies like Amazon provide very transparent marketplaces where the lowest price is a click away. Unlike the retail shopping experience, where a retailer has a captive audience at the point of sale. For example, Best Buy makes all its profit from selling things like the audo cables, while it competes heavily on price on the computers and TVs. If not for the internet, alot more people would be overpaying for those cables. So the internet price transparency keeps inflation on goods down. Of course, that doesnt apply to keeping the lid on scarce assets like homes, education and even healthcare, where there is very little price transparency.

But they dont look at asset price inflation in those inflation readings.

“nobody sane would lend to them anymore”

Cyberattack Drill Going Live?

Winter Watch

JBS meatpackers .. owned by Batista & Batista Portugal – cyber attacked.

It is suspected that they were hit by/from Russia ??

JBS are also in Australia.

Security .. there is security so sophisticated that it can suspect, anticipate, alert & block .. how was this cyber attack possible ??

Since COVID-19 was introduced & enacted there have been meat shortages & even today Coles do not have .. even beef bones for soup, osso buco, these are basic meat products.

Is it that they were broke in the first place, long before the virus hit .. did the virus hit to coverup the woefully mismanaged & bankrupt corporate world ??

?

All theories are possible really.

Look here at all the collateral available to rehypothicated and used to create dollars offshore…

So basically we have a list of countries whose real economy businesses are in desperate need of zero interest rates and/or mild (that is controlled) inflation.

The civiized way of handling this need is the lobbying.

Non-financial companies – doesn’t say anything about “real.”

Well, I think Sweden will blow itself up worse than it did in the 1980’s.

I have placed my Swedish house on the market right now because I am thoroughly fed up with the antics at my place of work, the mishandling of Corona, and everywhere I go, I see construction, renovation, ground being broken, the services being put in. It looks like one of those 1950’s agit-prop movies from Mao’s China here!

This is just not sustainable. Give it about a year more and there will be a huge supply of houses for nobody to be living in because they are priced a good deal beyond what average Swedish wages can pay. The banks are moaning already, problem is, if they touch the brakes on lending then they will cause a huge pileup, and of course they want the politicians to “do something”, which they eventually will, and the politicians will screw that up like they did with Corona, causing massive collateral damage!

There is a cultural component I only realised late: I used to think that somehow the recruitment process failed and somehow we managed to hire some real dum-dum’s for experts that could not adapt to changing situations. Yeah, ok, this happens, one has to work around them then, one thinks.

Then, with Corona, I realised to my horror and with some fascination, like one has towards a roadkill, that here In Sweden, an Expert cannot change their mind once they have pontificated on something, because, changing the plan means that the first plan was wrong and Swedish experts can never ne wrong because if they were, they would not be a proper Swedish Expert. Given enough flack, they might lie about what they are doing, but they will absolutely carry on with the first plan they yanked from their butt and made public, whatever the consequences.

Therefore I conclude that this country is fucked from the head down and it is well overdue to leave it before the proverbial deluge hits the fan and those furriners, like I, are blamed for the mess.

If immigration rates go anywhere near their pre-corona levels (say 2019, not 2015), then those houses will be rented out. I think Northern European countries are all in denial when it comes to the effect of immigration on the housing market, I see this very strongly in the Netherlands where my friends have the greatest trouble finding something within their budget yet every year over a 100.000 new people arrive. Stats for Sweden are similar relatively speaking.

Ok, how are immigrants with no money and fewer prospects going to finance home ownership – unless the government somehow funds or backstops it (they could, for the benefits of SKANSKA and PEAB, but it would be political trouble that the government does not need now)?

If you think of total world debt like a math problem if you have real debt growth rate faster than real GDP growth then only way you can keep the game going is for real rates to decline so interest payments can be serviced.

If negative real rates are an option is there any limit to amount of debt? Yes people may stop investing and saving and start getting assets out of money system so that real GDP breaks down and starts going very negative.

There is a reason why you see private money alternatives emerging in the form of the Asset Backed Digital Currencies (ABDC). People just don’t believe this fiat money charade anymore. They want sound money.

I think the battleground is going to be between Central Bank Digital Currency (CBDC) that will be debased, has an expiry date, built in negative interest rate, etc and private ABDC that cannot be debased and are backed by real assets (with the most practical asset being gold).

There is also a hype going on at the moment with people stacking physical silver coins and bars more than ever. But that can never play more than a fringe role in a digital world. But is is clear why they are doing it.

Eh fajensen,

Not sure what you describe is particularly Swedish…

It’s all over the West.

Mr fajensen,

the following is a FitchRating dated 4 days ago:

Rating Action Commentary

Fitch Affirms Sweden at ‘AAA’; Outlook Stable

Fri 04 Jun, 2021 – 17:03 ET

Fitch Ratings – Frankfurt am Main – 04 Jun 2021: Fitch Ratings has affirmed Sweden’s Long-Term Foreign-Currency Issuer Default Rating (IDR) at ‘AAA’. The Outlook is Stable.

KEY RATING DRIVERS

Sweden’s ‘AAA’ rating reflects a long record of flexible and effective policymaking, underpinned by strong institutions and very strong governance indicators, which Fitch believes will support a solid economic recovery once the Covid-19 pandemic subsides. Sweden’s wealthy high-valued added economy, sound government finances, healthy banking sector, and strong external metrics, have enabled the sovereign to absorb the pandemic shock, and underpin the Stable Outlook.

The Swedish economy has weathered the pandemic well, contracting by 2.8% in 2020 compared with declines of 6.6% in the eurozone and 3.6% (current median) across ‘AAA’ rated sovereigns. Sweden’s much less stringent approach towards Covid-19 restrictions, low dependence on international tourism, strong social safety net, and well-diversified economic sectors, helped limit the economic shock. Despite tighter Covid-19 restrictions since January, 1Q GDP expanded by 0.8% quarter-on-quarter, compared with a decline of 0.6% in the eurozone.

—————

The number of bankruptcies has been limited, and Sweden’s ratio of non-performing loans at 0.46% at end 2020 (European Banking Authority) is one of the lowest in Europe (the EU average is 2.57%). Moratoria take up on loans is also low and mainly related to the temporary amortisation exemption (until end August 2021) for residential mortgages. Risks attached to the pandemic remain elevated, but the banks’ asset quality and profitability are likely to remain resilient. The banks’ strong capitalisation levels (average common equity Tier 1 capital ratio of about 18.5% end 1Q21 up from 17.0% at end 1Q20), are sufficient to absorb severe credit losses.

End of citation

I shall increase my short position on OMXSX30 – It seems one of the lessons of 2008 has been forgotten: Credit ratings exists only to sell securities and credit ratings are “Free Speech”, not in any way advice nor incurring any legal responsibilities :)

+1, Ditto Australia

I assume, unlike Governments , that there is very little unallocated debt in the business world???? or am I wrong????

Sometimes called unfunded debt or “hidden debt” lol

Apparently the corollary to Cheney’s famous “deficits don’t matter” is “debts don’t matter”. Work ethic is good. Try to do something with your life in this place. But…is even trying to save for a future a fools errand these days, for a young kid starting out? “Don’t be a sucker” – N.N. Taleb.

This may be a reason why so much madness is going on at the moment with meme stocks and crypto. Especially the younger generation thinks that they need a moonshot if they ever want to be able to build some wealth.

So they all jump on these momentum trades that have absolutely no economic justification behind them, but they work (for now) because all the lemmings do the same thing.

Of course this house of cards will collapse and that will put many in a very precarious position. This can turn really nasty when so many disenfranchised people have no hope left. I really fear the fallout.

Re crypto: over on Zoohedge there is a piece about BC from a reasonably major outfit, (even Goldy has been sniffing around BC, cuz if folks want to trade it, or tulips, well Mortimer…)

Anyway at some point in the guy’s ‘technical analysis’, he casually remarks that because BC has dropped 50% it must be a buy and, get this, he adds the ‘fundamentals’ look good.

A bunch of zeros and ones stored in a computer have fundamentals!

BTC fundamentals are terrible. It is outdated technology, not performing well in it’s purpose. It is slow, doesn’t scale (8 transactions per second, which require the power consumption of a small country). And store of value proposition is laughable for a currency that routinely wins or loses 20% on one tweet from one person.

“Cheney’s famous”

The Left likes to pretend like cancerous deficit indifference started with this quote…when the truth is it has been the wholesale operating principle of the DC Degeneracy for over 50 years.

And a religious icon of the Left for longer than that.

Republicans may be hypocrites but Democrats are fools and/or bullsh*t artists.

LBJ was certainly, to a great extent, all about “let’s do a whole lot of stuff- we can pay for it all later long after I’m dead”. Over half a century now of that on the books.

The hyperbole here is over the top. But for perspecive, it takes approx 250 million years for our solar system to circumnavigate the galaxy. We are currently aligned to the centre, which is a 36 year process, (1987-2023).

Cured, whew, I mean, how wtf is that?

Any idea where Germany would sit on those charts? Probably the lowest in the EU.

73.2%. It has come up a lot in recent years, including a spike during the pandemic. In 2019, it was at 67.5%. In 2015, at 63.7%

Wouldn’t the US debt move up in the rankings if all the US companies registered in tax havens were included in the calculations?

Right – which chart up there includes AAPL?

It is difficult to unpack what these stats actually mean. For example, no one pays attention to Ireland’s stats because they simply ‘book’ profits for foreign corporations there as part of their GDP. Which is nonsense, of course. And when the indebted corporation is a Chinese government entity, the Chinese government can put zeros in the account, thus eliminating the debt entirely, without impacting further spending by the Chinese government. There would be a course correction, but equating this debt as ‘private’ is misleading.

ALL companies can get bailed out by governments if the governments have the means. Argentina cannot bail out companies with dollar debts. But China can and the US can, state-owned or not. And have. And will. Look at what happened in 2020 in the US. But bailing out companies is not the topic here.

It’s tough to draw any conclusions from this data. Dividing debt of only part of economy (non financial) by the entire economy (GDP), mixes 2 ratios into one cake: The debt ratio itself but also the ratio of the economy that is financial corporates vs non-financials. So highly financialized economies should have lower ratios.

I am a quite surprised that Luxembourg is so high, as most of their economy is financial services. The few non financial corporations that they have look extremely hyper levered. Would be curious to see an explanation.

“I am a quite surprised that Luxembourg is so high, as most of their economy is financial services.”

The charts may lead people to think that US corporations are in much better shape (regarding debt) than corporations from other countries which isn’t necessarily the case. For example, many large companies have moved headquarters to Luxembourg and the debt carried by these international companies will make the corporate debt/gdp larger because of Luxembourg’s small gdp .

Also, you have to look at the asset side of the equation for context. Apple carries a sizeable amount of debt but also has large cash holdings that offset some of that debt.

The larger point is that the Fed has incentivized companies to leverage their balance sheets to juice their stock prices which isn’t a good policy.

I think Lux is in a different category because it is essentially a haven, so the debt isn’t that of Lux itself, it belongs to cos using it as a mailbox.

Re: Norway, it has a huge sovereign wealth fund, at least a trillion, bigger than Russia’s for a much smaller population and I suspect has net zero debt if that is factored in.

Where’s Japan in all this?

Ok, so we aren’t beating Japan yet.

In general I think we should avoid using Japan as a comparable. Germany is a much better comp because it is also a very successful economy but with a Western culture more like that of the Anglo sphere. An oft repeated comment on WS is ‘what if we end up like Japan’ to which a rejoinder might be: ‘you should be so lucky’

We are talking about a society with virtually no violent crime, even vandalism including graffiti non-existent, no internal ethnic or religious fault lines, debt held internally, etc. As for their infrastructure, God knows what they would make of the power pole outside WR’s apt.

To give a specific example, as former teacher, I think the English- speaking world is in the midst of an education disaster. We could look at the German situation for clues, but I think the Japanese practice of kids coming home, having supper and then doing two hours of homework is a bridge too far for us.

Well, at the very least they have a semblance of a society over in Japan. There are many things in Japan that are just not possible in Western countries. School kids cleaning their own school for example. That’s unthinkable ….. in the US, we know we’ll be taking jobs away from poor immigrants if we do that.

There’s a whole lot of darkness in the German psyche behind that front of stoic control. And big-time, massive corruption! (Deutsche Bank anyone?). When the rage comes out of Merkel and her body starts shaking, it’s a scary sight to see.

I’ve never really gotten that ‘debt held internally’ thing, nick. Isn’t that along the lines of the ‘we just owe it to ourselves, anyway’ line of thinking in respect of growing global debt balloon..?

It’s surely much better for domestic harmony to fail to deliver according to expectations on something owed to someone far away in a foreign land than on something owed to your own angry citizens.

‘It’s surely much better for domestic harmony…’

That is the major point: there is no possibility of US- type domestic disharmony in Japan. If we use Japan as a baseline or benchmark, the US is on the verge of civil war. (I assume, maybe incorrectly, it actually isn’t.)

If the Japanese govt announces next week that because of adverse conditions, pensions are cut, there is not going to be a mob storming the Imperial Palace, or the Diet. They will grudgingly suck it up.

Both Alaska and Texas have independence movements. Sarah Palin’s VP campaign almost sh%t themselves when they found at 2 AM that her hubby was a member of the AIP. Manager Steve Schmidt: ‘so is SHE a member?’

The idea of part of Japan seceding is virtually untranslatable. Asked about religion in Japan, (the majority profess no religion) one Western expert responded: ‘the religion of Japan is Japan.’

I would claim it’s still preferable to screw over someone somewhere else than to do it to your own citizens, hence making external debt preferable to internal debt for the debtor in question…

1) Ten years ago Fukushima Daiichi nuke plant blew up.

2) Since 2011 Japan (debt : GDP) was down to a lower LOW in 2016.

3) The 2016 low is a spring. The spring job is to send (debt : GDP) higher.

4) But it will fail, the because (debt : GDP) peak in 1989, when the NIKK peaked, was crazy.

5) “F” in (debt : GDP) is “A” for recovery from the 1990 plunge.

Feels like the whole world is just running on one big giant ponzi scheme that will never go bust. Only thing fueling this ponzi is the never ending debt building and hollow out the non elites class.

Failed in Debt : GDP is rejuvenation.

FYI. Wolf posted a link to BIS, but I believe the numbers he’s posted here come from “F4 Total credit to non-financial corporations”.

If you look at “Total credit to the non-financial sector (core debt)” though, well, our numbers don’t look so benign anymore. In fact we are slightly worse than China by a smidgen.

Who is this “we?”

Hyperinflation ==> inflation > 60%/ Y. Are we there.

Gaza invaded Yale.

1) Japan vs the rest, ex UK :

2) Since 2009 almost every country (Debt : GDP) is trending up, with

a pandemic spike, but in 2009 Japan didn’t care, – similar to the NIKK in Oct 1987, – because the downtrend is strong !!

3) UK is down since 2009.

4) Spain and Portugal since 2010/13.

5) Falling (Debt : GDP) is a good thing.

6) Fasting in moderation, 1% – 2% annual deflation, cleanse the economy.

7) Salaries stay the same. People buying power is rising. The saving rate is up ==> that’s Japan !!

China is the bubble that never bursts.

So can we take away from this data that Multi-national “non-financial” companies (many of them US of course) choose to borrow foreign capital / currency because interest rates are lowest in China / Luxy / Hong Kong / Sweden etc (those with high Debt/GDP ratios) ?

I don’t think the article says where companies are choosing to borrow. In any case this is a meaningless statistic comparing a debt number in currency units to an income number in currency/year units.

I don’t understand how it is a meaningless statistic. For example, if I compare how much my business has borrowed (currency) with the current year’s gross profits of the business (currency/year), it doesn’t seem like it is meaningless.

It’s the comparison of an amount to a rate that comes out as a number in years. Years of what?

In other words a proper ratio has no units. You might compare your yearly spend on your debt to your total spend and you’d get a proper ratio at a point in time and then it would help you decide to do what? Not trying to be argumentative here but what’s the relevance/predictive power of these charts?

@lenert

I could understand your sneering if the issue was someone discussing a properly defined mathematical ratio. However, the common dictionary definition of ratio is:

“the relationship between two amounts, represented by two numbers or a percentage, expressing how much bigger one is than the other” (Cambridge English Dictionary)

@lenert: “what’s the relevance/predictive power of these charts?”

First, the charts are not predictive. They are descriptive. Second, the charts are relative to people who are trying to get a grasp on the world’s death March toward the debt cliff. Showing the history of these ratios gives some perspective on what is happening currently. What kind of relevance are you looking for?

Not sneering – just trying to understand what exactly the charts are describing. Comparing an amount of debt on one day to a year’s income ($/$/yr) means when you do the division operation the units come out in years, not percent. You COULD compare cost-of-debt ($/yr) to total spend ($/yr) and get the ratio of debt load to total spend and then you could wonder if the debt costs too much or too little. But then what? Are there magic numbers where we get catastrophe or serendipity or is this much ado about nothing? When the “ratio” on the chart was lower we had a financial crisis. When the US passed a big tax cut the “ratio” barely moved.

” .. and the favorite for US corporations, Ireland (190%). Many global companies are headquartered, sometimes on a mailbox basis, in these places, and some of their debts are registered there, though they were marketed to investors in other countries.”

Surely this distorts the figures of the US indebtedness (higher) and the tax-haven countries (lower)? Maybe significantly?

In dollar terms, the US business debt = $17.7 trillion; Ireland = $853 billion. But the debt in Ireland also includes European corporations and corporations from other countries, plus Ireland’s own corporations. The US corporations are just part of it. So if one-third of the debt in Ireland is US Corp debt, it would amount to $284 billion, or 1.6% of US business debt.

Thanks Wolf, for your reply. Your article is informative and IMPORTANT. I’m especially interested in Canada and the US positions.

I think you and I agree; the countries who have “mailbox-company-debt” [located] somewhere else has an understated [direct figure] business debt and those “mailbox-company-havens” have a [possibly large] overstated business debt, because it is cumulatively inflated by the “mailbox-companies” from elsewhere.

Thanks for your time!

Must all be what they meant by “Race to the top”. Coming soon…first nation to hold the corporate debt on construction of the Nostromo gets the annual award for Best ROI-plan of the year.

1) The Shanghai stock exchange (SSEC) had two bubbles and busts.

2) It didn’t affect the economy, because few people in China owned

stocks.

3) More Chinese own RE. Selling land and RE transactions are source of

income for the local gov.

4) The higher RE prices go, along with RE debt, the higher is the local gov income. Who cares about tomorrow. But if premier Xi cares.

5) China might preempt, deflate the RE market in a system control way, with negative feedback loop. China is tightening.

6) Tightening prevent explosion.

7) Radiation control with zircon and water shields, inside a steel dome, in old nuclear plants like Fukushima secure and tighten hot steam radiation. .

8) The Tsunami shut down the emergency generator’s batteries. The temp have risen beyond a certain threshold. Water evaporated. The zircon layer was oxidized, and Fukushima Daiiche of Beijing Shanghai blew up.

I appreciate the good article by Wolf and insights from audience.

Facts are what they are- hope for no sparks to the debt bomb.

Two questions:

1. What would the US debt be if we were to include US government debt, and then obligations by US Government?

2. With all of this borrowing in the US and worldwide, who is doing the lending? It would be good to see who are the leading lender countries

Thx in advance

A comparison of various countries’ non-financial debt should include public and household debt, since debt may be transferred from one account to another. For instance, China’s corporate debt could become instantly public debt if its government would decree the bailout of all indebted companies, by using newly printed money. FRED and BIS websites show at the section “Credit to Private Non-Financial Sector” the amount of debt owed by all non-financial entities, including households, relative to GDP at the end of 2020: 222.4% for China (down from 224.3% in Q3) and 164.1% for the US (up from 162.0% in Q3). Since public debt to GDP ratios for China and the US were 67.1% and 132% respectively, total non-financial (public & private) debt to GDP reached 289.5% in China and 296.1% in the US at the end of 2020. Pretty similar values.

If Al Jazeera’s article “China tells inefficient firms to shape up or prepare to go bust” is right, China’s private debt ratio to GDP will go down and total debt will be stable at 290% of GDP, while the opposite seems to happen in the US. By the way, in Canada, private and public debt to GDP ratios were 244.6% and 115.1% respectively, for a total of 359.7% (up from 304.7% one year before), and with the current rise in mortgages we’ll reach the 400% before Greece.

Moreover, publicly listed companies in the US get most of their financing by issuing stocks, sold for instance to households or to pension funds whose obligations toward their contributors are not counted as debt. In both cases, the financing will not increase total private debt, which is an advantage for the US since its market capitalization is four times larger compared to that of China, while the ratio of their GDPs is only 1.42 (everything expressed in USD). If China’s government would aim at ending overbuilding, stopping the credit to inefficient companies and reducing the financing costs of the efficient ones by letting the market allocate the money, it could allow homeowners to convert a proportion of their income or house-equity into corporate bonds or stocks just how IRA savings and home refinancing are used in the US by many people.

At the very least, banks should require a low value of some aggregate – call it PDE – involving not only company’s value P estimated via assets, minimal net income of the last 2-3 years (which should be positive, by the way) and market cap if publicly listed, but also company’s debt D (in absolute value) and earnings E (EBIDAT). For the sake of fun, let PDE = (P/E) * (1 + k * D/E) where k is an industry-specific factor between 0.03 and 0.3 … then ask PDE not to exceed some upper limit (say 20 or 30). Of course, Exxon wouldn’t qualify for a loan, and many zombies or overpriced companies would disappear from SP500 if investors would use such an aggregate in their pricing :)

Bombastic Failure,

Seems like you’re mixing up a couple of things: There is a huge difference with between equity financing and debt financing. A company doesn’t owe a stockholder anything and there is nothing it can default on. With debt financing, the company owes the debt, and can default on it. If a company doesn’t have debt, it cannot go bankrupt.

Of course, but what I wanted to underline is that a company can pay its debt via shares multiplication/dilution and their sale to the public. The same wine, just several times more water was added :) It’s the seignorage/sovereign right of company’s rulers to multiply the shares as they wish, in a similar way to government’s right to print as much currency as it likes and to buy with it real stuff from domestic or foreign sellers as long as there’s still enough faith in its value. Equity financing is the best analogy for the monetization of public deficits and QE, there’s no risk of default but “only” the risk of trashing the stock/the currency via oversupply. When lots of people realize that other stocks, currencies or commodities are better stores of value or offer a better return, they switch to them and the price of the initial stock/currency drops fast. In the ’90s, the DM was prefered to the USD in Europe. If Germany wouldn’t have joined the Euro zone, the € and maybe the $ would have failed. Later, ECB trashed the € via QE and the bailout of countries that didn’t respect EU debt & deficit rules.

Equity financing is more crucial for US than for Chinese corporations, and it’s the only solution for zombies or companies with bad financials/ratings. That’s why the FED/US Gov cannot allow an extended decline of the stock market: in that case, the money would run out from stocks. Similarly, China cannot allow a debt/financial crisis: the banks would become fearful in providing loans to companies and households (mortgages). That’s why Canada cannot allow a decline of RE prices, the money would run out of the housing market and the economy would crash since RE is the hard currency that replaced CAD long ago.

Yes, as Yellen said, we’ll not have a financial crisis (plain defaults), but surely a currency crisis and public misery by inflating out the debt (soft defaults). One way or another, what cannot be paid must be written off. Negative yields were invented for reducing the unpayable debt of Greece, Italy, etc. without triggering CDS: no formal default, just a commonly agreed “haircut” for the investors :) Just how a company may destroy the value of its stock without reducing the burden of its debt to a manageable level (e.g. Bombardier), a government may ruin the domestic standard of life by inflation/QE and still be enslaved by debt in hard currencies/gold to foreign entities since imports must be paid with real money. You can inflate away all domestic debt, but eventually you’ll need a low deficit and a positive balance of trade, that’s why some Asian countries are better positioned than the US to weather the next crisis.

Thanks Wolf great insight and perspective, I just hope that the funds have been put to productive use and provide a sustainable return on investment, from well thought out businesses. I guess we will wait and see when interest rates start returning to more normal levels. Cheers for now Pete.