It’s a crazy situation the Fed backed into as tsunami of liquidity goes haywire, banking system strains under $4 trillion in reserves, and General Treasury Account gets drawn down.

By Wolf Richter for WOLF STREET.

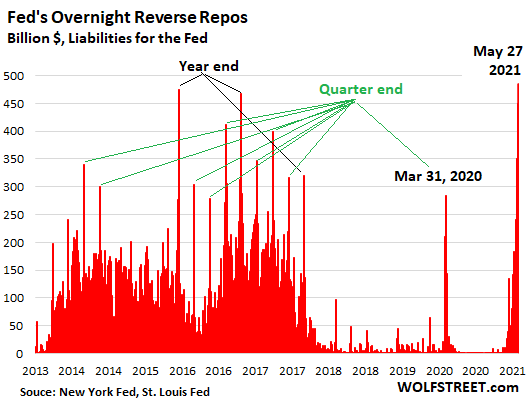

This morning, the Fed sold a record $485 billion in Treasury securities via overnight “reverse repos” to 50 counterparties, beating the prior record set on December 31, 2015. These overnight reverse repos will mature and unwind tomorrow morning. Today, yesterday’s $450 billion in overnight reverse repos matured and unwound, and were more than replaced with this new batch of $485 billion in overnight reverse repos.

Reverse repos are liabilities on the Fed’s balance sheet. They’re the opposite of repos, which are assets. With these reverse repos, the Fed is selling Treasury securities to counterparties and is taking their cash, thereby massively draining liquidity from the market – the opposite effect of QE.

In past years of large reserves following QE, banks shed reserves via reverse repos, reducing reserves on the balance sheet and increasing their Treasury holdings, to dress up their balance sheet at the end of the quarter, and particularly at the end of the year. Reverse repos declined after the Fed started reducing its assets during Quantitative Tightening in 2018 and 2019. But the current record spike is taking place in the middle of the quarter, a sign that the enormous amount of liquidity is going haywire:

This is a crazy situation that the Fed backed into.

Even as liquidity is going haywire, and as the Fed trying to deal with it via reverse repos, the Fed is still buying about $120 billion per month in Treasury securities and mortgage-backed securities, thereby adding liquidity.

But with its reverse repos of $485 billion, the Fed undid four months of QE!

The Fed could stop buying securities altogether and reduce its balance sheet, which would also drain liquidity from the market. But the Fed cannot do that because it said it would be slow and deliberate in announcing changes in its monetary policy, and that it might eventually talk about talking about tapering, so it can’t just suddenly do an about-face.

But this liquidity-haywire situation appears to be an emergency that needs to be addressed now, and so the Fed is addressing it through the backdoor via the overnight reverse repos.

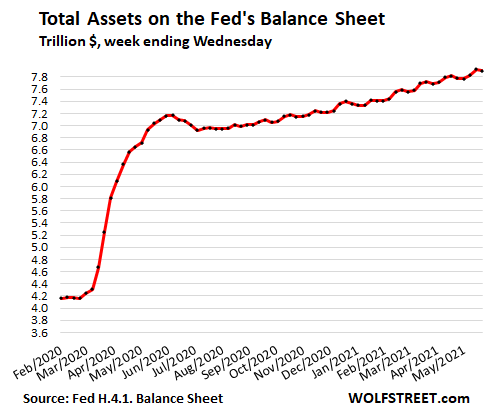

At the same time, the Fed continues QE. Its total assets were of $7.90 trillion on its balance sheet as of May 26, released today, were down by $19 billion from the record last week, following the typical pattern. These assets include $5.09 trillion in Treasury securities and $2.24 trillion in mortgage-backed securities (MBS):

The Fed has discussed this liquidity issue during the last FOMC meeting and summarized some of the discussions in its meeting minutes. It noted that “a modest amount of trading” in the reverse repo market took place at negative yields, meaning that there is so much demand for Treasury securities, and so much liquidity chasing them, that the holders of liquidity were willing to lose money to obtain Treasury securities. This threatens to push related rates into the negative, such as SOFR (Secured Overnight Financing Rate) which is the Fed’s reference rate to replace LIBOR.

The Fed, sitting on $5.09 trillion in Treasury securities, has been stepping into the reverse repo market, selling Treasuries overnight to satisfy this demand for Treasuries and keep yields from meandering below zero.

The tsunami of liquidity.

Everyone has their own theory as to why there is so much demand for Treasury securities. But one thing we know: the banking system is creaking under a huge amount of liquidity.

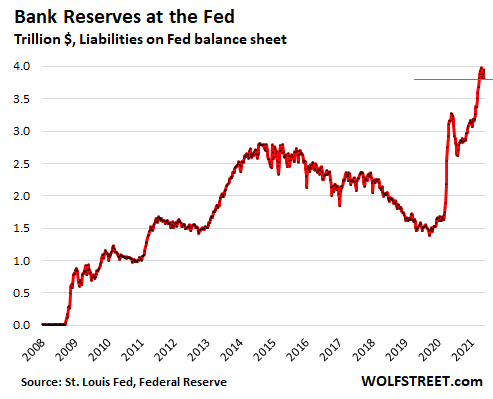

Bank reserves on deposit at the Fed – a liability on the Fed’s balance sheet, money that the Fed owes the banks and that it pays the banks currently 0.1% interest on – ballooned to a record of $3.98 trillion on April 14 and have since then zigzagged down a smidgen. On the Fed’s balance sheet released today, they were at $3.81 trillion. This is a sign of just how much liquidity banks are swimming in:

The drawdown of the Treasury General Account.

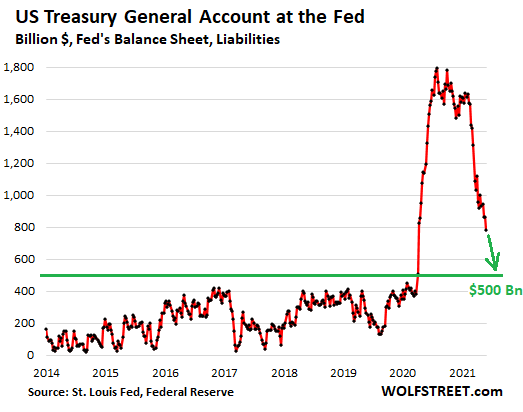

The government sold a gigantic amount of debt last spring, adding $3 trillion to its debt in a few months and kept the unspent amounts in its checking account – the General Treasury Account or GTA at the Fed, which is a liability for the Fed, money that it owes the US Treasury. The balance in the GTA ballooned to $1.8 trillion by July 2020, compared to the pre-crisis range between $100 billion and $400 billion.

The Mnuchin Treasury started spending down the balance in the checking account by borrowing a little less. By early January, the GTA was down to $1.6 trillion.

The Yellen Treasury formalized the drawdown and in early February announced that it would bring the balance down to $500 billion by June. This turned out to be too much too fast, and it now looks like August will be the month when the drawdown reaches the $500 billion mark.

On the balance sheet the Fed released today, the balance as of May 26 was down to $779 billion. Down by $821 billion since February, $279 billion to go:

The drawdown of the GTA has some implications for the markets: this is money that the government will spend but doesn’t have to collect in taxes or borrow; it already borrowed it in March through June last year. And the Fed mopped up this debt with its $3 trillion in asset purchases. So the drawdown means that the government has been spending this money that the Fed had already monetized in the spring last year.

All of this has big implications for the markets. These are huge amounts, in terms of reserves on deposit at the Fed, the drawdown of GTA at the Fed, and now the reverse repos at the Fed, all of them liabilities at the Fed, all of them representing different aspects of the massive flows of liquidity that are now bouncing off the walls.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Some wag here last weekend likened all of this as trying to keep the Titanic from sinking by blasting a hole in the stern to let the water out.

?

Or rearranging the deck chairs on the Titanic. Whether Trump or Biden, the Fed is still in charge. And that May 27th spike is the result of Fed employees doing a last bit of what they consider damage control before they take off for their Memorial Day weekend holiday.

Maybe it’s just the old-fashioned Open Market Operations on light-speed time. The charts used to be linear, now they’re exponential.

So laymen’s terms… Fed print $ gibs loan. Corp takey da loans. Dont spend all da loans but buyzezes lots of stonks. Sells dems loanies backs to dem Fedzies, which den gibs promisesesez to pays backs da monies and plus more too for realsies. Den dems gibs mo monies to put into more stonks to makey more monies to dens getsums more monies to sells backsies for more promisezes den etc. etc. etc.

Was our economy designed by children? So everyone loses but these corps is what this sounds like to me, just free loans, which prop up the markets and the leftovers get sold back for bonds or w/e they are calling them and rinse and repeat ad infinitum till the wheels come off? The fed makes no profit, but who cares because they don’t need to, but wall street sure as hell must. Meanwhile everyone outside of the elites gets screwed by the relative drop in the value of their own petty savings proportionate to the amount of new money supply injected into the system. i.e. inflation…. what I don’t get is why inflation isn’t going up faster than 2% on avg over the last decade. I mean milk does cost about 25% more than 5 years ago so they are probably just lying about the inflation rate. That’s how my grug brain which knows almost nothing about economics has assessed the situation. Would be a lot easier to parse without the superfluous jargon….

This seems like somebody came to the table with a new set of rules or instructions. Almost like two leaders are issuing mandates that are opposite. Are these moves of stability, genius, mistake or possibly something else? Not a good look but either is speaking out of both sides of your mouth FOMC

“…. new set of rules or instructions. …”

Indeed. And if you were one of the first to know the game changed, you did very well. Thus the cronyism of central banking.

Who gave the Fed the right/power to “change the rules”?

I looked all through the US Constitution.

It doesn’t mention any of this.

“this is money that the government will spend but doesn’t have to collect in taxes or borrow; it already borrowed it in March through June last year. And the Fed mopped up this debt with its $3 trillion in asset purchases. So the drawdown means that the government has been spending this money that the Fed had already monetized in the spring last year.”

The FED isn’t in the Constitution, therefore the TGA isn’t but there are numerous inherent powers within the legislature’s purview to legalize the FED.

Congress and the president can always revoke its legitimacy.

Article I, Sect 8

Minting and Taxation both powers of Congress

It seems somewhere along the line, the Fed went from a provider of “temporary liquidity” to assuage short term banking issues…

TO..

A digital minter of money, a central planner, and a layer of taxation in the form of inflation to sustain the leviathan federal government and its need for debt.

“money that the government will spend but doesn’t have to collect in taxes or borrow; it already borrowed”

___________________________________

we should quit bastardizing the language by using the word borrowed. The money was created – digitized.

Loopholes are pretty great. It’s almost as if we plebs have absolutely no power. But that can’t be true because this is a free democracy, or democratic republic, or somethin… Dunno, I failed civics. Wish I could hand out money to my pals for the sake of the country tho, that would be pretty cool man. I wonder how one can get their hands on one of those wealth creating machines… might be alien technology actually… sounds pretty advanced. So like these corporations get the power of confidence and fiat money and like totally build new American factories and create jobs left and right.. right? Everyone is getting richer and the US is more productive than ever before after adding an extra 5-10% to it’s wealth? Sounds pretty amazing. I hope I get accepted to Hogwarts next year, I’m a bit past age 11 but I’m pretty sure I’m quite the special lad since I’ve figured out the secret of alchemy. They’ll make an exception, I know it.

While they keep talking about the possibility of tapering a ponzi scheme that can’t be tapered, I’ll keep buying oil company and gold and silver mining stocks.

Gonna admit, AG is the sweetheart of my portfolio right now.

Won’t pretend I don’t have a bit of a physical stack, either.

If you ain’t stacking, you haven’t been paying attention.

Ever watched when that one guy tried to give silver away on the street, and no takers? I think people picked Snickers bar over a silver bar.

Mark Dice. There are 2 videos on YouTube. In 2013 he offered people a silver dollar for 99 cents and they refused. One guy said it wasn’t worth the trouble for a 1-cent discount..

In 2015 he offered a 10 oz silver bar or a candy bar and they picked the candy bar.

Assaying is the problem with taking delivery.

Like most things on YouTube the video is likely staged and fake. Anyone who picked the silver bar would not actually receive it, and they’d just edit that person out. Not saying there’s not a whole bunch of dummies out there who would pick the candy bar and those interactions could be real, but the video is edited such to overstate them and give you the impression “everyone’s an idiot but me, me so smart!”

People who believe what they watch on YouTube, are almost as big of suckers as the people that choose the candy bar.

Agree Flounder. It’s like a short, easily produced, “reality show”, and just as phoney. And likely contains even more “sponsored content”.

On the flip side, if you stay away from the agenda stuff, I have picked up a lot of good auto repair tips, disassembly videos, etc, from the DIY bunch, so You Tube isn’t all worthless.

Ya, looks like and old fashion shell game to me.

> But with its reverse repos of $485 billion, the Fed undid four months of QE!

In exchange for CUSIPs that actually yield more than cash and can/are rehypothicated at least 6 times (officially) in collateral chains overnight…

How many times can you rehypothicate cash on a balance sheet?

Until the music stops.

FDR:

“Happy Days Are Here Again! Oh, Happy Days Are Here Again!”………until the music stops!

My thoughts also.

Treasuries can be rehypothicated, cross collateralized…..cash, not so much.

And how does an overnight repo that undoes itself the next morning undo QE that has a much longer “hang time”?

Finally we are getting why banks want treasury garbage; it’s all about rehypothecation of treasuries; all about creating bigger and bigger leverage and bobbles.

Can’t the Federal Reserve actually have up to a 65 day term rather than just overnight?

newyorkfed.org website: “The Fed uses repurchase agreements, also called “RPs” or “repos”, to make collateralized loans to primary dealers. In a reverse repo or “RRP”, the Fed borrows money from primary dealers. The typical term of these operations is overnight, but the Fed can conduct these operations with terms out to 65 business days.”

Maybe there is no end of accounts the money could be stuffed into considering no one audits them?

The Fed can do just about anything it wants to ;-]

BTW, what you’re citing is about repos, not reverse repos.

Do WHATEVER IT TAKES to keep risk asset prices in a bubble. Give me wealth effect or give me death. Right?

Best of luck FOMC. Send your regrets to Greenspan & Bernanke.

Incoming, Incoming, Incoming. DefCom 5.

Unprecedented liquidity.

And it’s world wide. The USA Fed is not the only country with the same fiscal and monetary excesses. How much of this is also about a global trade war?

Add: Globalization, as orchestrated is a train wreck for public interest in the west. And so is deregulation and the hands off oversight too. Governments world wide are corporate wealth managers.

Even leaving off a few other issues, it’s all combined into a WTF scenario.

What is the end game?

To keep markets liquid. Once price discovery returns, then BOOM.

The question that matters for individual investors is how and when this gets resolved. Does this lead to massive inflation in the core CPI that must be killed with higher interest rates? Will the Fed be willing to let the markets purge and cleanse themselves? Or does the Fed even have a choice?

I think that alot of smart big investors are looking at the month when the Fed has to start selling a ton of Treasuries and realizing that could be the spark that sets off the bomb. The timing got pushed back a little, so it is happening in August now. I also would note that the VIX index seems to have a descending resistance line that will cross the support around September, so it might be a very good time for volatility to surge.

I am starting to think I won’t live long enough to see the FED ever stop QE, let alone reverse it in any meaningful way. It’ll be interesting to see how this market and asset can ever crash, guess Powell boy figured out the cure to the disease is more disease. Yay for pumping asset prices to Mars so everyday folks can’t afford anything decent.

Maybe they learned a thing or two watching Tesla self fund/fufill his dream by adding more and more and more stocks to the pool. That is how they got to be the worlds most valuable car company, right? just create it and look it still landed way up there

The newer Teslas can mine bitcoins. Practically pays for itself.

a

Cool

Perpetual motion at last, I knew it would come and I knew it would be a Tesla that did it!

Phoenix_Ikki – How old are you, and have any serious illnesses to report?

Not that old, in my mid forty and no serious illness, at least none that I know of. When I said I won’t live long enough to see this FED reverse course, I was being half serious about it but definitely half of me think perhaps this is the new normal since they backed themselves into a position that they can’t get out, so perhaps not that far fetch to think this might continue another 30-40 yrs, who knows…

The other assumption is that with my rotten luck, something happens to me and I pass and that will be the day they announce major tapering or reverse QE and assets prices will settle back down to earth..

If it’s still working why get a new one .. hey.

The usual solution is to knock a bunch of zeros off the exchange rate relative to the dollar, at least for banana republics because the dollar is the reference currency.

The dollar will knock a bunch of zeros off relative to the gold, and other commodities’ prices.

When you have to pay a billion dollars for a house that will be one of the leading indicators. If this sounds far fetched, a car used to be 300 bucks and a house 1000 or 1500.

Same here, brother.

QE will be temporary. When unemployment dips below 6.5% rates will normalize…

B Bernanke 2009

I do think that they have painted themselves into a corner. The one wildcard is inflation. If that starts to soar and they cant disguise it, then even the Fed can no longer keep manipulating this market. I think that the Fed has essentially created a dynamic where they will need to continually increase support to the market or it will fail. But as they keep pushing out liquidity, the velocity of money will just keep falling until it really has no effect. This is a poker game where the market is going to call Powell’s bluff. Instead of being assured by the Fed increasing support, the market is going to get really scared by the Fed’s irresponsibility, and that will increase volatility even more.

Over the next couple of months people will start spending down those stimulus benefits and PPP checks and unemployment checks and consumer spending will drop. That is going to align with the time when the Fed needs to start selling more Treasuries into the market, driving rates higher. So my guess is the financial markets will start to react in about July or August, as the big financial players will want to reduce risk ahead of that time.

gametv,

Out here on the Left Coast, stimmies are long gone.

Heading into this holiday weekend, street traffic is a fraction of pre-pandemic levels. Stores are empty. No trouble parking at Trader Joe’s or Kroger. No waiting at checkout.

Help Wanted signs everywhere. Even the Lyft driver I spoke with earlier this week says fares have returned bigly but not enough drivers.

More pundits each day calling for the collapse to begin in ’22 so bank on it not happening on the pundits’ schedule.

Maybe it starts next week instead?

Am here all week folks. Try the veal.

Almost becoming my CB notion too, Phoenix. The now almost ancient “train wreck or cancer” financial analogy, combined with a good dose of “not on my watch” and “not till I get mine”?

Not being one of the major players in this big money game, I really do wonder if I’ll ever know “how it all ends”. But I have a ringside ticket at WS, whether I fully understand all this or not.

Also nice to see a similarly baffled soul, thanks.

Some commentary is that the immediate issue is the Fed preventing the overnight rate (particularly SOFR) from going negative.

Wondering why banks can’t find more productive uses for their cash. Too much investable funds chasing the available options for productive investment?

Yeah, banks can’t find good investments for what’s left of my savings account I have left there paying .01%? Credit cards from the masses being paid down? Dang.

Banks might as try using the liquidity and buy back more of their stock or issue more stock market margin like before because no one is coming into their doors anymore for manufacturing producing investment loans. The options of what to do with free money have become few as sit-on-your-ass-at-home-paper-markets stopped paying in the U.S.

“Wondering why banks can’t find more productive uses for their cash. Too much investable funds chasing the available options for productive investment?”

Exactly. Enter Everything Bubble.

“Build Back Better .. for BANKSTERS”

Jeffrey Gundlach and Lacy Hunt claim that the reason we haven’t seen hyperinflation is that the Fed isn’t really printing money. QE isn’t really money printing, they say, that’s a misunderstanding. But everything changes when central banks begin to hand out money to people that can be spent via CBDCs. That’s the true money printing that will cause hyperinflation, the theory goes.

I have a suspicion that the money is effectively printed the moment the government borrows money by issuing treasuries. Everyone who holds treasuries understands that the risk of default is zero, not 0,05%, but 0.00%. I’m not sure it’s that relevant at what specific time monetization takes place. If I want to convert my treasuries to cash and spend it, I can do so anytime. It’s my decision not to do so (my decision to work, save, and accumulate more money) that keeps the system stable and the everything bubble going.

When the yield curve steepens, it’s like the investors are saying “why should I get 0% or 1% return when I can make so much more money in risk assets? But from the viewpoint that all treasury debt will eventually be monetized anyway (as needed), the correct interest rate across the entire yield curve is close to 0% like cash.

The only end game I can identify is that at some point, enough people lose the willingness to work hard to get ahead. But is there really a limit to how little people will accept as a wage? In prison, you might get paid pennies per hour, but it’s better than the alternative of earning nothing and doing nothing.

The weekly unemployment bonus wasn’t enough to destroy the work ethic and it’s now being wound down early in many states. It looks like the everything bubble will expand for another 20-50 years, until China and the US engage in a kinetic war, or some other extreme event puts unexpected stress on the financial system.

Orthodox Investor,

Central banks “print” money just fine. But this “printed” money doesn’t generally go to consumers to stimulate consumer price inflation. It goes to asset holders and stimulates asset price inflation (higher prices for bonds, stocks, houses, etc.). That is exactly what we have been seeing since 2008.

But now we’re getting fairly large and fairly sudden consumer price inflation too.

I also don’t buy that these actions haven’t, and won’t, have a deleterious effect on our work ethic.

Who is going to want to work for $40k/year when an average house costs $600k?

Californians.

RightNYer

This is a short and correct observation to the unintended consequences of the actions taken by the FED.

When the prize or reward of your work seems to become further and further away, and eventually unattainable, you either lose interest in the prize or work a short cut around to attain it!

This is where criminal activity, unorthodox measures.., call it what you will gets engaged in the mind of an individual or an organization!!

These are the unforeseen effects on the general community that lowers its expectations of the value of its enterprise as a collective group or individuals.

The end result, is the expectation that the government will ultimately (plan, execute and deliver, ie communism!).

Off course this never happens, as the shoulders are disengaged from the wheels of productivity, and the whole economy and by extension the country falls into disrepair.

Is the United States going down this path?

I’ll leave the answer to you.

That Was CA in 2004 when I was last there. Two BR 4X4 homes going for $500K+.

Working is for fools. Just get your stimmie and use it to buy Gamestop and Dogecoin.

And definitely don’t risk investing your money in starting a real company. You’ll then have to deal with the whims of the real economy and you can easily lose your shirt. Just buy stocks instead. If the market drops 5% the Fed will come out with all guns blazing, time and again so there is really no risk in buying stocks at 100 P/E.

Also, you’ll be making a fool of yourself on social media. “Look how cool I am! I have been slaving 60 hours this week for $11 an hour! I will save prudently so in 30 years time I may be able to afford a 5% deposit for a mortgage! For now, I’ll just live in my mom’s basement. YOLO!”

Millennials and Gen-Z have figured this out now.

So they’ll go on the dole instead ???

The Fed has taken away the ability for people to SAVE their way to some sort of prosperity. This is a tragedy.

For the entire 20th century and before…and until 2009, people could SAVE their way to financial stability…SAVE their way to buying a house…SAVE their way to a better life.

Now, dividend chasing, desperation investing, leveraging, ….all because an unelected body (the Fed) changed the rules? The Lender is now slave to the Borrower? This is upside down.

Who empowers the Fed? Who/What is the largest borrower in the world? Same answer.

Many will….they just will not be able to buy a house. They will live in a 700 sq ft appartment.

I think the TOLL Brothers CEO in the last earnings call said owning a home will be a luxury. Basically saying the lower 50% of families will probably not be able to afford a home in the future.

Right now, 75% of renters make less than $58k a year.

Is it fair to say that the sequence of events ( First pump the asset markets for a few years, and – only after that failed – second hand out cash to the people such that at least a fraction of the money goes directly to the real economy) expresses the priorities of the Fed?

Does the money really go to asset holders, or is it simply that low interest rates increase the prices of assets? I would argue the latter.

A central bank like the Fed purchases long-term bonds from banks and other financial institutions using newly created money. It’s not money printing. The Federal Reserve makes an electronic entry in its computer system, indicating brand new money.

Suppose the Fed purchases $1 million of bonds. The Fed records a liability of $1 million reflecting the money that it created and books an offsetting asset of $1 million for the bonds it just bought. The Fed’s balance sheet is now larger by $1 million than it was prior to the purchase.

The bank that sold the bonds now holds $1 million of additional cash (RESERVES) at the Fed. The decrease of bonds by $1 million reduces assets by the same amount. There is no change to the net value of the bank’s assets or liabilities)

Is QE “printing money”? Yes, since the Fed creates new money in order to purchase bonds. The Fed balance sheet increases by $1 million but the bank’s balance sheet doesn’t change (other than the new mix of assets).

Arguably, although the Fed is technically creating new money, it is not actually increasing the money supply. To complicate matters there is also significant disagreement as to how to define money supply. Ultimately this is a semantic discussion. The real meat is what was QE supposed to and did it do it?

The public was told quantitative easing would help the economy. The publicly touted goal of lower long-term rates was to encourage borrowing, encouraging home purchases, business startups, capital improvements, and so on. The end result would be more economic activity, more jobs and lower unemployment.

There were at least two other “stealth” goals of QE. One was bailouts to the banking sector. The second was to increase the price of financial assets. Supposedly this would encourage rich people to spend, a concept 40 years ago that was called trickle down economics, which didn’t work. In both cases I have to call BS; they were gifts to the rich disguised as benefits for the middle and lower classes.

Whichever motive you choose, the intent of QE was to encourage lending and stimulate the economy. Since every private bank loan involves money creation (printing), it expands money supply. Whether it’s “money printing” by the Fed or by private banking the intended result was the same.

Did it work? I think not. Despite trillions of money pumping by the Fed it produced a feeble response in the economy and inflation. The transmission mechanism of QE is obviously flawed.

It did, however, re-inflate asset bubbles, bail out banks and bankers that should have failed, and encouraged financial engineering like M&A and stock buybacks, as well as worsen wealth inequality.

If you really want inflation, keep the stimulus checks flowing. That money printing goes straight into the economy like IV meth. No detours or workarounds. It’s also the path to hyperinflation.

Have a great holiday weekend!

It’s not money printing .. it’s electronic entry of new money.

Aren’t we splitting hairs here ??

But did it keep the tub afloat.

My understanding is that the today’s prinicipal money issuers are the commercial banks: they create the new “money” in form of loans to companies/organizations/consumers.

The loans are made in national currency.

Now the commercial banks have certain legal limitations to the amount of loans they can make.

The QE of the CB targets the commercial banks as an authorization to create more loans.

One of the practical limits to this system is the willingness of the commercial banks debtors to take more and more debt.

The gist of your argument (and Hunt, Gundlach, Rosenberg, etc.) is correct. QE isn’t “printing money” in the sense most folks imagine it (or as Hunt terms that sort of printing – making the Fed’s liabilities “legal tender”). A better way to think about is that they are replacing existing interest-bearing debt with zero interest-bearing debt. That causes leverage to grow, which in turn pushes up asset prices.

@ Michael Gorback –

Very well written and appreciated. A few thoughts.

_____________________________________________

MG – ” It’s not money printing.”

response: Semantics. As you point out, digitized or printed, it is new money creation.

MG – “Arguably, although the Fed is technically creating new money, it is not actually increasing the money supply.”

response: Semantics, as you later point out. New money has been created and exists. The money may or may not lie dormant as reserves, but the cash does exists. (If not true then Wolf may have to rethink his assertion that FED to Bank reverse repurchases sop ep liquidity or cash)

MG – “The public was told quantitative easing would help the economy. The publicly touted goal of lower long-term rates was to encourage borrowing, encouraging home purchases, business startups, capital improvements, and so on. The end result would be more economic activity, more jobs and lower unemployment.”

response: The primary goal was to bail out the Banks and the connected. A parallel goal is to advance the rentier economy and create as many debt slaves as possible. Many a millionaire was saved by refinances at lower interest rates brought on by interest rate suppression which simultaneously repressed many prudent savers.

MG – “There were at least two other “stealth” goals of QE. One was bailouts to the banking sector. The second was to increase the price of financial assets. Supposedly this would encourage rich people to spend, a concept 40 years ago that was called trickle down economics, which didn’t work. In both cases I have to call BS; they were gifts to the rich disguised as benefits for the middle and lower classes.”

response: It was worse than a gift. It was theft from one class to another.

GM – “Whichever motive you choose, the intent of QE was to encourage lending and stimulate the economy.”

response: I take issue that the intent was to stimulate the economy. At least not the real economy.

GM – “Since every private bank loan involves money creation (printing), it expands money supply.”

response: Though I am an amateur at bank plumbing, I think you overstate your case that every private bank loan involves money creation. I think many do not, though many do.

GM – “The transmission mechanism of QE is obviously flawed.

It did, however, re-inflate asset bubbles, bail out banks and bankers that should have failed, and encouraged financial engineering like M&A and stock buybacks, as well as worsen wealth inequality.”

response: It may have worked exactly as expected. To further the rentier economy and insider advancement while creating ever more debt slaves. It certainly worked for Goldman Sachs.

“Does the money really go to asset holders, or is it simply that low interest rates increase the prices of assets?”

It’s both and that’s the power of QE. The Fed is absolutely printing money. When the Fed buys assets in the trillions, it is paying a much higher price than the free market (non Fed-intervened) would have paid.

If a hedge fund holds an MBS and sells it to the Fed via primary-dealer bank intermediaries, that is cash going to the asset holder (hedge fund). It can be argued that the amount the Fed pays above what the free market would have paid is the true amount of printed money being injected into the system.

We don’t know how much that is, but if the Fed sold its entire balance sheet into the market, we would have a better idea. Also, there is a great myth out there that all the cash from the Fed purchases sits harmlessly as excess reserves. However, this is not correct as the Fed’s balance sheet ($8T) is much larger than the excess reserves in the banking system ($3.9T).

And the cash being created by the Fed gets prodded into asset markets by the ultra-low interest rates which ultimately leads to a large wealth transfer to the top.

@cb

I agree with your comments. If you note the 4 a.m. timestamp it explains why it had a lot of loose ends. I realized that there were some small consistency problems, which you picked up. I just didn’t have the energy to clean it up. I’m glad the message got through and thank you for being charitable in your corrections.

@ jrmcdowlee – ” It can be argued that the amount the Fed pays above what the free market would have paid is the true amount of printed money being injected into the system.”

——————————–

Some insightful observations.

Though I would contend that the true amount of new money being injected into the system is 100% of what the FED paid.

Wolf,

‘All of this has big implications for the markets’

I am trying to fathom ‘these big implications’ but my brain, doesn’t compute enough to give results! Is this heralding YCC, to avoid the NRP?!?

Is this part of ‘kicking the can down’ or Worse? What should investor expect in 6-12 months?

Thanks.

Lacy Hunt (“the bond king” – LOL) should take notice of this:

“By Pam Martens and Russ Martens: October 29, 2019 ~

Steve Meyer, Official Spokesman for the Federal Reserve Board of Governors in 2011

On January 19, 2011, the Federal Reserve released a video on YouTube to quell the public uproar over its unaccountable money creation operations. The spokesman for the Fed in the video was their Senior Adviser at the time, Steve Meyer, now an Adjunct Professor of Finance at The Wharton School.

…

“You may wonder how the Fed pays for the bonds and other securities it buys. The Fed does not pay with paper money. Instead, the Fed pays the sellers’ bank using newly created electronic funds, and the bank adds those funds to the sellers’ account. The seller can spend the funds or can simply leave them in the bank. If the funds stay in the bank, then the bank can increase its lending, purchase more assets, or build up the reserves it holds on deposit at the Fed. More broadly, the Fed’s securities purchases increase the total amount of reserves that the banking system keeps at the Fed.

“Whether the Fed’s purchases lead to an increase in the amount of money circulating in the economy depends on what banks do with the new reserves and on what sellers do with the funds they receive.”

Sure the fed and banks can create money out of thin air. The FED even said so. Everyone who says the opposite is – well, a “bond king”.

Got gold ?

Thanks Wolf….a great report.

They are so confused at the fed…..just imagine what a CEO is going through trying to decide his/her future use of cash. Impossible to plan.

Very soon the works are going to be so jammed up with conflicting moves that the 29 event that this whole mess was created to avoid will become likely to happen.

These dudes must have been trained at the Joe Stalin school of government controlled economy.

At this point the 10 year should be at 3.00 or higher. Inflation will be transitory due to unlimited foreign labor……as soon as the unlimited foreign labor is healthy enough to work. Which may or may not happen. Until then the fed is playing with fire and I truly believe they may not have the political will needed to react to their situation. The real danger is inflation not deflation. If we truly ever had a deflationary meltdown and the government sent every citizen a check for $100,000 Bernanke believes they would not spend a portion. Notice to Bernanke Americans don’t save squat. He is an academic who has read too many books. On the other hand once the inflation starts to cook even foreign nations will back away from treasuries….creating a cyclone……fueled by citizens whose credibility in their government is just about gone.

re: “Bernanke is an academic who has read too many books”

Just like Volcker was directly responsible for two back-to-back recessions, Bernanke was the sole cause of the GFC. Bankrupt-u-Bernanke drained legal reserves for 29 contiguous months turning otherwise safe assets into impaired assets.

Spencer Bradley Hall said: “drained legal reserves for 29 contiguous months turning otherwise safe assets into impaired assets”

—————————————

How so?

‘once the inflation starts to cook even foreign nations will back away from treasuries’

Where will they go park their ‘cash’ – Euro, Rubel, Yuan? May be Yen, right?

Remember there are already 16-18 Trillions at NRP!

I understand the Fed’s “save face” backdoor approach to tapering. Though disgusting, it is understandable.

What I do NOT understand is why a “counter-party” (banks?) want to diversify by having NEGATIVE yield USTs when they can get .001% paid on their pile of Fed reserve $$. Makes ZERO sense/cents (pun intended).

A shortage of “good” collateral?

Changes:

March 18th – increase from $30B to $80B per counterparty per day. Aggregate $500B

ON (IOER) + 5 basis points (rather than 10 for 28 day TERM)

But the graph really takes off on APRIL 30th….

April 30th – 2a-7 funds, the existing requirement to have, for the past six months, either net assets of at least $5 billion or an average outstanding amount of RRP transactions of at least $1 billion is reduced to $2 billion and $500 million, respectively.

Government Sponsored Enterprises, the existing requirement to have either an average daily outstanding amount of RRP transactions of no less than $1 billion for the past three months, or an average daily amount outstanding of overnight money market transactions of no less than $100 million over the past three months, is removed.

Kinda thought the point of the interest rate suppression exercise was extending and pretending bank solvency after the GFC.

When I hear the name Jay Powell, I somehow imaging that he is the drug dealer Jigsaw Jimmy from Motley Crue’s Dr Feelgood. And the later line of that song goes…

Jimmy’s going down

This time it’s gonna stick

Feels like Powell has been riding high… and being set up for a fall.

Wolf said: “banks shed reserves via reverse repos, reducing reserves on the balance sheet and increasing their Treasury holdings, to dress up their balance sheet at the end of the quarter, and particularly at the end of the year.”

____________________________________

How does this dress up their balance sheet? Both reserves (dollars) and treasuries are bank assets, are they not?

Reserves are only created by the FED as credit to its holders – a select few.

It cannot be used in the credit market between those in the non Federal Reserve credit market,

I am not following you.

As Wolf says: “Bank reserves on deposit at the Fed – a liability on the Fed’s balance sheet, money that the Fed owes the banks and that it pays the banks currently 0.1% interest on –”

Bank Reserves are an asset to a Bank —— Money. The most liquid form of asset. The reserve requirement is zero. Why can’t a Bank use its Reserves/Money?

Short answer: They’re not allowed to.

It would also violate the “Law of Accounting”,

Assets = Liabilities plus Capital, or Assets – Liabilities – capital = 0

Let’s walk through a simple loan. The bank lends $1,000. It creates $1,000 in the borrowers account. On the ledger it would enter:

Assets + $1,000 Liabilities $1,000

The loan is an asset while the deposit account is a liability. Note how this zeros out:

$1,000 Assets – $1,000 Liabilities = 0

But suppose the bank uses reserves.

The Assets side has no Loan entry. There is just $1,000 borrowed from Reserves. The Liabilities side is -$1,000 debt to the Fed account.

So far so good. That zeros out.

Then the bank transfers the $1,000 of Reserves to the borrowers Deposit Account, incurring a Liability to the bank of $1,000.

The transfer of the reserves reduces the bank’s assets by $1,000.

Now the bank has zero in the Assets column ($1,000 in and $1,000 out).

Liabilities are $1,000 to the Fed and $1,000 on deposit.

Assets – Liabilities = -$2,000.

GONG!

Note that there’s nothing to indicate a loan to the borrower by the bank. It’s like they received $1,000 for free. There’s no way to patch it up.

The regulatory bank formulas treat them differently.

How so?

There is currently a reserve requirement of zero. Reserves are cash, perhaps digitized cash but cash, are they not?

cb

I am with you. Reserves are an asset which they are not lending it out anyway, so why not take .001% Interest vs a negative return on a UST ?

Cash held in money market funds by depositors earns zero interest, so they need to swap that for treasury bonds (collateral). Interesting that cash has insufficient collateral value for their purposes. Seems likely this has to do with rules governing reserves, how they can be used, what sort of assets can be redeployed and which sit in lockbox. This was the issue in REPO crisis I. The notion of bank reserves is pretty ridiculous in the modern age, one might surmise it’s a place where money can be taken off balance sheet, until such a time as they might need it to boost asset prices, or fill liquidity gaps. Has nothing to do with account holders, rather investment firms.

so if the tga is the usg checking account, that they don’t need to borrow or collect taxes to spend, expect it to go to zero. after that mmt and spending by executive order for made-up emergencies.

watching this stuff as a layman for so long now, it’s cool how the story begins to make some sense.

How’s this a solution? QE has no set maturity, while this has to be repeated daily indefinitely as the RRPs are unwound daily.

FED continuing QE because of credibility? Only in their own group-think world.

An overnight balancing act doesnt seem to undo ANY QE….

So the Fed has a big promise out there to who? They wont taper or quit QE until ….when? The big boys get adjusted for it?

Maybe the FED is just too big ….. too powerful….

used to be they would “tweak” …. now they are heavy handed…the entire game really.

What power in the hands of a few unelected, unaccountable people!

Promoting inflation when they are instructed per their mandates and agreements to do JUST THE OPPOSITE…stable prices. Yet, no one says a word. I am flabbergasted.

Lot’s of people screaming out there:

Peter Schiff, Ron Paul, people on this site, etc.

FED doesn’t care. They are serving their masters.

A phrase I haven’t heard in the longest time – the “shadow banking system.” Except in reference to China, by people like Pettis, and as an area of risk.

The more politically correct term is “nonbanks,” or non-deposit taking banks. The biggest ones are lenders like Quicken Loans. The way they’re different from banks is that they don’t take deposits and are therefor not regulated like banks.

The NBFIs are the DFI’s customers. Savings flowing through the nonbanks never leaves the payment’s system, there is just an exchange in the ownership of pre-existing deposit liabilities in the payment’s system, a velocity relationship (aka the U.S. Golden Era in Capitalism).

Spencer Bradley Hall,

I don’t follow what you’re trying to say. By definition, there are no savings flowing through nonbanks because nonbanks don’t take savings. That’s what makes them nonbanks.

@ Wolf –

Where is Quicken getting the money they lend?

cb,

It uses warehouse lines of credit at big banks for temporary funding when it issues mortgages, and eventually it sells the mortgages it wrote to the GSEs (Fannie, Freddie), and it packages other mortgages into MBS and sells those. The proceeds provide funding for future mortgages.

It also issues bonds — junk bonds since it has a junk bond rating; Moody’s rates it Ba1, which is the top junk-bond category, just under investment grade.

Doesn’t matter because the REPOs close each day, therefore zero sum, right Wolf?

Yes, they close so why does the FED enter the market?

To pay the banks additional interest that otherwise they wouldn’t earn. Yet, borrowed treasuries are negative!

Collateral is an issue.

Banks will soon receive increased IOER if this continues.

Banks aren’t the participants in the RR facility. Banks are already paid IOER and the RR rate is 0. Raising the rate of IOER wouldn’t give banks the balance sheet relief they want. Banks don’t need this facility from a rate perspective, rather they need it from a regulatory perspective.

If T-bills and other short term assets went below 0 on a sustained basis, MMF would no longer want deposits pushed off to them by the banks. The banks would likely be stuck with the deposits they’ve been trying to push off and their balance sheet could not be used for more lucrative purposes i.e total return swaps. The lack of safe collateral that guarantees to pay par on demand is the issue and likely will not get better once the debt ceiling constraints begin to truly kick in over the next few months.

Sounds right to me. And MMF being the non-bank banks (to be PC) I was thinking of in my comment.

@ Wolf and Plumbing –

Plumbing said: Banks aren’t the participants in the RR facility.

——————————————

Doesn’t this contradict the article?

What is MMF? (acronyms should be outlawed)

Plumbing said: ” The lack of safe collateral that guarantees to pay par on demand is the issue”

————————————-

What issue (I know this is Jeff Sniders favorite issue)? Why does there have to be an abundance of safe collateral at par for banks? Perhaps the issue is that the succulent banks and nanny FED thinks banks (and hedge funds, etc.) should have an abundance of safe collateral at par so 30 to 50 times leverage and gambling can be condoned and fomented.

And it really becomes an issue when certain players get themselves in a blind bid bind and have to suffer negative interest rates.

The problem, Mr Snider and others, is over-indebtedness and over leverage and a corrupt system that encourages and rewards financial parasites.

And a system that allows insiders that benefit from money created from NOTHING.

You’re welcome.

(By the way, I really like and respect Mr. Snider, mostly)

cb,

MMF = money market fund

Look, no one in the public knows who actually is selling Treasuries to the Fed via reverse repos. It is NOT disclosed. So we guess. All we know is who the approved counterparties are — but some of them may not be selling any Treasuries to the Fed.

Also note that the counterparties may be dealing with the Fed for their clients, not for themselves.

The approved counterparties are the Primary Dealers. Click on “current list.”

https://www.newyorkfed.org/markets/primarydealers

PLUS a whole bunch of other financial institutions. Click on “current list.”

https://www.newyorkfed.org/markets/rrp_counterparties#reverse-repo-counterparties

No. The total outstanding tonight is $485 billion. Meaning the Fed sold $485 billion in Treasuries for cash. This will unwind tomorrow, but there will be a new batch of reverse repos tomorrow morning, likely larger.

There may be a day in the future when the Fed won’t engage in reverse repos and the balance then goes to zero. But that’s not happening now.

There will be a day when RRP will be > $1T/day.

Yes. Last day of the quarter is a good candidate, June 30. But at the current rate, this could happen faster.

Should the banks bust the contract, they keep the treasuries, pay a penalty, and Fed keeps the cash. There was some talk of a permanent facility? Fed tries to back out of this and they have to eat their own cooking, ie cash.

Ambrose Bierce,

That’s an interesting topic.

If the counterparties bust the contract with the Fed and keep the Treasuries and let the Fed keep the cash, it would raise some issues in how the Fed accounts for these busted reverse repos.

Right now, the Fed accounts for the reverse repo contracts as a liability. But the Treasuries it sells are assets on its books. So if the contract is busted, and the Fed doesn’t get its Treasuries back, it would have to reduce the amount of Treasuries on the asset side of its balance sheet, thereby officially unwinding its balance sheet for all to see.

This would be a cute way of initiating Quantitative Tightening. If all of the $485 billion in reverse repo contracts were busted today, the Fed’s total Treasury holdings and therefore total assets would drop by $485 billion. That would be fun to watch!!!

So I don’t think anyone is going to bust a reverse repo contract with the Fed.

It is very unlikely unless the bank or MMF had a death wish.

A bank pissing off the Fed is a very bad idea. Just ask Bear Sterns about LTCM, and what happened to them 11 years later. Banks will eventually need reserves from the Fed, so pissing off the Fed is a no go.

MMF wouldn’t want to break the repo either. There is no incentive for them to. They want and need rates to stay above 0.

AB and Wolf,

Very interesting indeed regarding busted contracts.

Aye, why would any primary dealer or affiliate bite the hand that feeds? Only if the hand stops feeding. Or elite hackers get in and prevent the contracts from being fulfilled.

If the banks kept the treasuries they would cash them in at maturity. The US treasury would pay the face value via the Federal Reserve.

Yes, and you wonder why the FED allows the financial institutions to usurp their power over the volume of Reserve Bank credit outstanding.

Hi Wolf,

FED “recycles” tons of money through repo meaning that the system does not this much of money. Why is FED “prints” so much at the first place? Cannot they do this work more precisely so that the market is not flooded cash while it helps the situation?

One conspiracy theory about the reason is that this is how FED/US knocks down other countries like China ( main target) or other Asian countries: flood the world with dollars by QE to boost the assets in those counties and then drain the money from the market by raising interest rate which crashed the asset’s price. They then buy those assets at a discounted price. That’s why China doesn’t want to be in this loop and likes to create their own system to avoid these “in-and-out” capitals.

Any comments?

Tommy,

For my taste, that’s too much conspiracy theory. It’s funny though how people come up with this stuff ?

So when do we admit that the “economy” as construed now is one giant ponzi scheme? Cause you guys know those end badly right? Are we so ignorant that we’re going to gladly march off the cliff as long as every else does?

re: “Are we so ignorant that we’re going to gladly march off the cliff as long as every else does?”

Yes we are. And its the American Bankers Associations’ fault. They literally paid big sums to their collaborators to silence their critics.

The source of time deposits to the payments’ system is demand deposits, directly or indirectly via the currency route (never more than a short term situation), or through the bank’s undivided profits accounts.

Perhaps the physical laws of the Biggest Ponzi Of Them All are different than your regular, good ol’ fashioned, neighborhood Ponzi scheme.

If so, perhaps these unique laws might be capable of inducing population-wide hallucinations that persist through many generations.

I’m divided as to whether being part of the last generation, and possibly witnessing and living through the painful birth of a new age, would be somewhat refreshing, or if I’d like the grand magic show to continue until after I’m gone.

“… But the Fed cannot do that because it said it would be slow and deliberate in announcing changes in its monetary policy, and that it might eventually talk about talking about tapering, so it can’t just suddenly do an about-face.”

The Fed massively abused its forward guidance … projecting thirty months of predetermined policy – data be damned – was insane. The way to correct that is to acknowledge the data and start laying the groundwork pronto. It’s not as if the Fed has much credibility left after suddenly doing an about face at the beginning of 2019 and abandoning its avowed normalization program.

Or does responding to data only matter when it means easing?

Finster….

“The Fed massively abused its forward guidance”

The Fed is rogue. They are completely off the rails….partnering with Blackrock, dealing in non federally backed securities, expanding M2 by 27% in less than a year…fed funds 4% below inflation (ever happen?).

Housing market locked up because replacement costs of homes just jumped 35% in five months! And the Fed is lending to the mortgage industry (buying MBSs) at under the inflation rate!

Imbalances galore due to the interruption of free market forces by central banker/planners.

It seems Powell is a puppet for some…..and he has been convinced of the benefits of MMT….but hasnt thought it completely out .

Not until inflation becomes a crippling, pounding, grinding matter to the working people of this nation will the smallest amount of light be turned on the Fed by the politicians. We are close to this point.

Powell tries to control the perception with the “transitory” game….

this is like the sign behind the bar…..”free beer tomorrow”.

Powell is rogue. He made swift and radical changes to the system without public consent.

Spencer…

at the very least.

He ignores the boundaries of the Fed…

He has organized what I call a premeditated THEFT and an illegal TAXATION of the People with his planned inflation.

This is diametrically opposite of the agreements/mandates/ and instructions that allow the existence of the Fed.

One could make the argument Powell should be arrested for these breaches. Yet, Congress and Wall St are having a ball.

Quis custodiet ipsos custodes?

Finster!

The FED are a bunch of liars and elite water carriers who haven’t had no credibility for decades. They advance the agenda of the rentier class and the debt slave society. To allow the lending at interest(rent) of that which is created from NOTHING.

It really is amazing how much liquidity must be out there. Just ONE YEAR AGO $485 billion would have been 12% of the Fed’s total assets.

12 years ago it would have been over half the Fed balance sheet.

The critical issue is interest rate suppression.

Fake interest rates are destroying the world. Everyone knows asset prices are BS, and cash flows will not support current asset prices at honest interest rates.

How many current homeowners have sufficient income to save and buy their current homes, at current prices, if they had to start out today from scratch, like young people?

As a younger person, I’ve watched the Fed and other central banks destroy the value of my labor for over a decade, They have ensured my peers and I cannot earn economic security by working and living ethically and responsibly.

Instead, now liars, grifters, and speculators have become wealthy and run the world. Good job central banks. Hope you’re proud of the mess you’ve made.

PNWGUY

Bingo.

Inflation promoted, implemented on purpose….to steal the value of past labors and current wages. Pre arranged theft.

Tell me why J Powell shouldnt be arrested.

The Fed is supposed to “promote stable prices” and “promote moderate long term interest rates.” Promoting moderate, not extreme either way, is key….it prevents irresponsible debt creation that could burden future generations by keeping a reasonable cost to that debt creation…keeping a balance between lender and borrower.

Promoting inflation is flat out robbery, and this is not good for a society that is further split between those riding the asset bubbles, and those grinding it out each day, unable to save. Not good at all for a society.

From its charter to be a lender of last resort to address bank runs to:

“On November 16, 1977, the Federal Reserve Act was AMENDED to require the Board and the FOMC ‘to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.'”

“Stable prices” AREN’T an intentionally understated, manipulated to be low “2%” inflation figure per year.

Trivia just for the halibut because both major parties and their true owners benefit from Fed policies:

1913 – Senate and House Democrat controlled, Dem prez

1977 – Senate and House Democrat controlled, Rep prez

2% rips 22% off the dollar in 10 years.

2.5% rips 28% off the dollar in 10 years.

2.5% rips 63% off the dollar in 20 years.

The low integer game…..its just 2.5%….nothing, right?

Here’s the sideways chart of the rate of inflation … see, horizontal, nothing, right?

Never a mention of compounding or aggregation.

The great “deflation fear era” 2009 to 2020……Inflation without compounding up 17%. CPI from 215 to 254.

Inflation is the most destructive force capitalism encounters.

No.

The main, core problem we’re facing is that labor is being factored out of the production equation, and our society has no effective remedy for that action.

The value of labor has been, is, and will continue to fall. Earning power – hence buying power – of households has been falling for decades.

Investing in new capacity just makes things worse. The productivity gains are concentrated (more) into the hands of the few, and more jobs get automated.

Giving money to the 1% just bids up asset prices, exacerbating the household’s lack of earning power.

Giving newly created money to households so they can buy stuff only works until the currency fails.

Unless laborers (that’s most of us) figure out how to capture the benefits of automation, we’re going to continue to get squashed.

No amount of grumbling about un-elected Feds, unresponsive Congress, lazy workers, etc. is changing this fundamental problem.

The last few decades’ excesses in monetary and fiscal policy are desperate – and I mean really desperate – attempts to address this issue.

The distortions are increasing because the severity of the underlying problem is increasing.

We are not going to get out of this box using the same thinking that got us into it.

Market monetarism is sheer ipsedixism.

It’s stock vs. flow. QE-forever does exactly the opposite of what the advocates of N-gDp level targeting says is important, e.g., Marcus Nunes: (“It is the real interest rate that affects spending”).

Adding infinite, artificial, and misdirected money products (blunt LSAPs on sovereigns) while remunerating interbank demand deposits, IBDDs (inducing nonbank disintermediation), generates negative real rates of interest; has a negative economic multiplier; stokes asset bubbles (results in an excess of savings over real investment outlets); exacerbates income inequality, produces social unrest, and depreciates the exchange value of the U.S. $.

(“It is the real interest rate that affects spending”, pg. 19 Marcus Nunes and Benjamin Cole’s “With Market Monetarism – a Roadmap to Economic Prosperity”).

How do you explain real yields continuing to fall at the same time the economy is “slowing”? Link “Fed Leaves Interest Rates Near Zero as Economic Recovery Slows” – NYT

Interest is the price of credit. The price of money is the reciprocal of the price level. An artificial exogenous increase in money products reduces the real rate of interest. An endogenous increase in the utilization / activation of savings products increases the real rate of interest.

Whereas the regulatory release of savings invokes a spontaneous chain reaction, an expanding sequence of reactions, a self-propelling and amplifying chain of events.

The activation and discharge of $15 trillion of finite savings products (near money substitutes), via targeted real investment outlets has a positive economic multiplier, a ripple effect (increases productivity and real wages), while increasing both the real rate and nominal rates of interest.

No, contrary to Bankrupt-u-Bernanke’s claim that: “Money is fungible”…“One dollar is like any other”, pg. 357 in “The Courage to Act”, the utilization of savings is a catalyst, it is not a matching of economic accounts, not a 1-2-1 economic transaction (correlation between two sets). This is demonstrated by debits to particular deposit accounts.

“In economics, a multiplier broadly refers to an economic factor that, when increased or changed, causes increases or changes in many other related economic variables. In terms of gross domestic product, the multiplier effect causes gains in total output to be greater than the change in spending that caused it.”

It’s a disputation of the Gurley-Shaw thesis (that there is no difference between money and liquid assets).

N-gDp LPT is nothing other than stagflation reincarnated. It caps real output and maximizes inflation.

Free market principles do not apply when the Fed can and does whatever it wants, at any time.

If someone explains why rates are too low, and writes a 1000 word article about it with charts, etc….it is meaningless if J Powell decides to suddenly halt QE.

Knowing what the Fed is about to do, or not do, is worth MORE than all the PHDs, MBAs, Economic Theories in the world.

And that is the danger of CENTRAL PLANNING, as noted by Hayek and Mises.

Free markets with informed participants works best. J Powell and others disagree. Now they are trapped in their own web, painted into a corner…and all they want is more paint.

Your comment addresses money.

My comment addresses the diminishing role of the worker in the economy, and the deflationary effect that has on an economy.

Expanding the money supply, reducing interest rates, or giving people money to spend are desperate attempts to address this problem, and those tactics are becoming rapidly less effective each time they’re used.

We are not treating the underlying problem, and that is why it continues to worsen. Rapidly.

The departure of our manufacturing base has a lot to do with it…

the globalists dont care. They maintain trade deficits dont matter.

They are wrong. Your point is an example.

There are help wanted signs all over my area, but they are min wage type jobs.

Manufacturing allowed people to advance themselves…up the ladder.

Most min wage jobs are dead ends.

Recently I was chatting with my elderly mother, a product of the Great Depression. I mentioned that Lyft and Uber drivers end up making nothing. She said that’s okay because kids need a starter job as a way to learn the work ethic. I didn’t have the heart to tell her my Lyft driver that very day was 45 years old.

@ Tom Pfozer –

Tom said: “Unless laborers (that’s most of us) figure out how to capture the benefits of automation,”

_________________________________

well you have identified an issue, but I would argue the core problem is our captured political class (hence existence and ongoing activities of the FED), by the rentier class which has allowed the concentration of wealth and power (ownership).

The solution to this being seen by many younger people is distribution of ownership or the fruits therefrom which explains the inroads by AOC(Alexandria Occasio Cortez) and Bernie Sanders, etc.

I never said I should get paid more for my labor. I know globalization exists.

What I said was the Fed and central banks are eroding the value of my labor. They are. They are eroding the value of savings, my saved labor value, by suppressing the interest rate.

And they know it. They are keeping asset prices high to protect banks and, more importantly, pension/retirement funds. They want to prevent the social dilemma we would face if we had to take care of millions of broke retired baby boomers… And they expect my generation to just “deal with it,” fund baby boomer retirement, and accept a lower quality of life and reduced economic opportunity.

Well, I’m not having it. I’ll move abroad if I have to, but I’m not going to spend my life participating in an obvious ponzi scheme (which btw, is nearing the end now that interest/mortgage rates are approaching zero).

I hope others will make the same decision, and vote with their wallets and feet (since voting at the polls won’t stop this).

PNWGUY

I am a young Boomer but I could not agree more with your comment. Our generation raped you (and continues to do so), plain and simple.

I do have to ask – is PNW “Panties in a Wad?” If so – that’s priceless. :-)

This is all about power. If the Fed prints and keeps interest rates negative who benefits? The largest debt holders which arent John Q private citizen, wait sorry consumer. That has been the case since 2008. Everything since then has been fake. What is the interest rate on your credit card? It ain’t 2.5%. Big gov and Big corporations love da QE and 0% rates.

Are we fighting the plague or are we fighting deflation so power doesn’t shift to someone else?

You are one of the few smart young people I have come across. Most of your generation is so involved in avenging micro-aggressions and chasing after the latest woke meme, that they are ignorant of the one main fact – young people are being screwed by old folks with assets. Your generation is left with a world where a communist regime will be the most powerful in the world, where the world is stripped of its natural resources and devolves into a broken ecosystem and where the divide between rich and poor is a chasm that grows with every year.

And the politicians that supposedly represent the youth – people like AOC – are clueless. She isnt even smart enough to understand that the policies she espouses are increasing the misery of the poor.

She’s a plant, probably answered a casting call to get her role in congress. Currently the “smart” young people who speak out against this are being painted as trouble makers. Wonder why?

That ‘they still know what they are doing is amazing.

I’m definitely scared now.

Music .. 2CELLOS – Chariots of Fire [OFFICIAL VIDEO] Youtube

I greatly prefer:

2CELLOS – Smells Like Teen Spirit [LIVE]

1,518,121 views • Feb 7, 2015

since the U.S. on Kurt Cobain’s path.

What it needs is Lithium… and not just for batteries.

Theme song/music video for the Fed to use in its branding:

I vote for the opening track of Apocalypse Now, with clouds of fire and smoke, and the Doors singing, “this is the end, beautiful friend. . . ”

Who could have guessed that all along Jay Powell was inspired by Marlon Brando’s portrayal of Kurtz!

You should have been scared since 2008. Most missed the implications of that. If they were willing to lie about something like that, what aren’t they willing to lie about? Imagine life is the game of monopoly, the board was upended in 08 and under our current trajectory we will all get 200$ as we pass go and hope it makes it until our next time around the board because we won’t be allowed to own anything.

Japan doesn’t pay interest on reserves. Japan owns most of its own public debt. That means it has the ability to simply write down the public debt to any amount it thinks is necessary. This would have zero effect on the nation’s ability to fund its activities. My view is that the supply chain bottlenecks are responsible for most domestic price increases. I’m more worried about the asset inflation the Federal Reserve, (and Congress too with the windfall tax cuts) have enabled. This is speculation, not investment. FDR learned that giving private banks more cash during a depression does not work. Does not increase productive investment.

So much private excess liquidity in the “can’t do big things anymore nation,” my, my. Isn’t that a reflection, a very negative one, on the leadership in this society, that is the private owners of large chunks of capital as presented to us in Thomas Piketty’s “Capital and Ideology?”

Maybe it’s the ruling class that’s can’t do – can do globalizing – can’t do for this nation’s citizens. Unless you equate the two.

Why banks buy REPOS for 0% interest instead of earning 0.1% from excess reserves parked in FED ???

I have asked the same Q? 3X and no one seems to be able to explain it. They are “reserves,” which means they don’t need the $$ and they don’t lend it out. Take .01% vs a negative return….right ??

The bank may need the treasuries for a client who is unwinding a treasury position. Everything the bank buys is not necessarily for their own account.

My take on the RRepo is that there is a big client or clients in trouble and they are hiding it, again.

Bear & CB,

And just because the bank is buy at negative rate doesn’t mean they can’t make money reselling to a client.

Petunia

Your explanation is plausible, but I still think the timing and then the repeat behavior by the Fed / counter-parties, day after day, is suspicious.

Your explanation makes it sound like someone needs the USTs because they have to cover a short or something as opposed to the facade explanation of “excess liquidity.” If that is what is happening, then we may be on the precipice of something ? And if that is the case, it should be pretty easy to figure out what it is.

I admittedly put myself between a 2-3 (out of 10) on the Wolf Street knowledge base on issues of high finance, but I learn so much from everyone and I am appreciative.

I respect your reply Petunia, and there is sense to it. I would still like a nuts and bolts explanation from someone with inside knowledge. I see lots of innuendos (ie Jeff Snider) but never clarity. If it is “saving big clients” it is complete corruption for the FED to be wielding its power for special interest …. but no surprise as that is essentially all they do.

I see no reason to believe they would consciously buy them, especially overnight, at a negative interest rate. I also am waiting for an explanation.

Because of Basel bank capital requirements. Reserves and cash are treated differently than Treasuries. The supplementary leverage ratio requires large banks to hold capital equal to about 3% of their assets which Powell ended on March 31st.

I suspect the banking world created by the Fed has rules that say Treasuries are more valuable than mere lowly cash. As in only Treasuries can be used as collateral, not worthless cash in the Fed’s banker’s games. Cash converted into Treasuries adds value that cash sorely lacks.

It is just like physical gold has no value in the Fed’s version of it’s banking game. You can not use physical gold as collaterial at a Fed bank, unless you are another country’s central banker.

The Fed’s power stems from it’s ability to change the rules of the Fed’s banking game.

@ Wolf –

Either your site or my computer has become glitched. This is the second article that, after posting a response and hitting enter, the response is posted but I am taken back to the start of the article rather than being returned to the previous place in the comment section. Re-finding ones place is your comment sections is time consuming.

Also, the site is user unfriendly, as it disallows notification of answers or follow-up comments to user’s posts. For that reason I may miss it if you respond to this post. I will try to follow up, but the required memory or note-taking, and manual follow-up makes it difficult.

Thanks.

Your browser should have a search feature. You can always search the page for your name and find your comment.

Best.

Not sure about your first point.

Your second point: I disabled that feature because it led to endless arguments between commenters that made the comments unreadable. If you want to find your comments and replies to them, just use the browser search function (ctr F) and enter your screen name… it will pull up all your comments, and all responses to your comments.

I disabled that feature because it led to endless arguments between commenters that made the comments unreadable.

—————————————-

I understand the avoidance of noise. The downside is that there is a lot of good and needed clarification and learning that is missed.

A vote up or down feature on comment quality could help that feature. I don’t expect to see that because I know you currently do 48 hours of work in a 16 hour day.

@ Wolf – ” If you want to find your comments and replies to them, just use the browser search function (ctr F) and enter your screen name”

—————————————

Thank You a thousand times.

What do people want to to do to fix this? If the current solution “works”, we’ll have another problem in 8-10 years that will may be ten times as bad. May I remind everyone that the Constitution contains the basic ideas we should be following. I don’t hear an outcry here or anywhere else.

Otto…

Exactly

The Fed has stolen, appropriated…new powers, authored their own course, crafted new mandates and ignores the essential ones that ALLOWS their existence…

They are coloring outside the lines…..and to the joy of Congress who dispenses this free money out to the masses.

The Fed and Treasury should be GUARDIANS not RAIDERS of the value of the dollar.

Fiscally irresponsible, combined with an irresponsible monetary policy funding the former, is a cocktail of disaster.

Cloward and Piven saw this as the way to collapse the nation.

It seems Pelosi and Powell are their agents.

That so called liquidity that was drained were “reserves” not “cash”. To use RRP MMF have to be dealing with a bank that has actual “reserves” to give to the FED

@ Default –

Exactly what are reserves?

cb, Reserves is (are?) the currency of daily interbank payment settlement (the netting of daily payments between each pair of banks).

No intended disrespect, but that is like FED-Speak. Rather opaque, which we should not condone in any way – by either repeating their proaganda, or otherwise.

netting what? money? digital dollars are they not?

No one seems to want to straight up answer this question. None of the ‘experts” I read endlessly, EXCEPT Wolf, who made reference to “cash’, which it is I believe ……. digital perhaps, but cash dollars.

Can they not take those reserves and buy T-bills or other assets? or make loans?

cb: I did not intend to be opaque, but I have covered that topic before and just wanted to be brief. I’m a bit ashamed of being accused of fed-speak :-). Here it is again:

The original purpose of a Reserve bank (or Central bank) was to hold the (gold) reserves of the retail banks, and thereby keeping said banks honest. Hence the name “Reserve” bank. Interbank daily net payment settlement was executed by transferring ownership of the appropriately sized chunks of reserves between each pair of banks at the end of each day.

This is still the core function of central banks to this day, but most people are not even aware of this extremely basic fact (and function). To some extent, this ignorance is by design, because Central bank officials never talk about it and it is never in the news. As an example, the Wikipedia page about Central banking does not mention this fact at all, but instead says that the purpose of Central banks is “monetary policy”. One might speculate that one never hears the phrase “Reserve banks exist to keep other banks honest” because it would soon bring up the question about whether the Reserve/Central bank it itself honest (which it is not, of course).

cb,

“Exactly what are reserves?”

Reserves = a bank’s cash that it put on deposit at the Fed. Banks on their books do NOT call them “reserves” but “cash” or “Interest-earning deposits with banks,” or similar.

Below are the asset accounts of Wells Fargo Bank, and the link to the bank’s 10-Q quarterly financial statement where the balance sheet begins on page 61. In the entire 10-Q, the word “reserves” shows up only once and in a different meaning:

Assets:

Cash and due from banks

Interest-earning deposits with banks

— Total cash, cash equivalents, and restricted cash

Federal funds sold and securities purchased under resale agreements