Mortgage applications spike to record, while 130,000 homeowners are on mortgage holidays, 500,000 on tailored payment plans, and over 1 million are in unmortgageable apartments due to the flammable cladding crisis.

By Nick Corbishley for WOLF STREET:

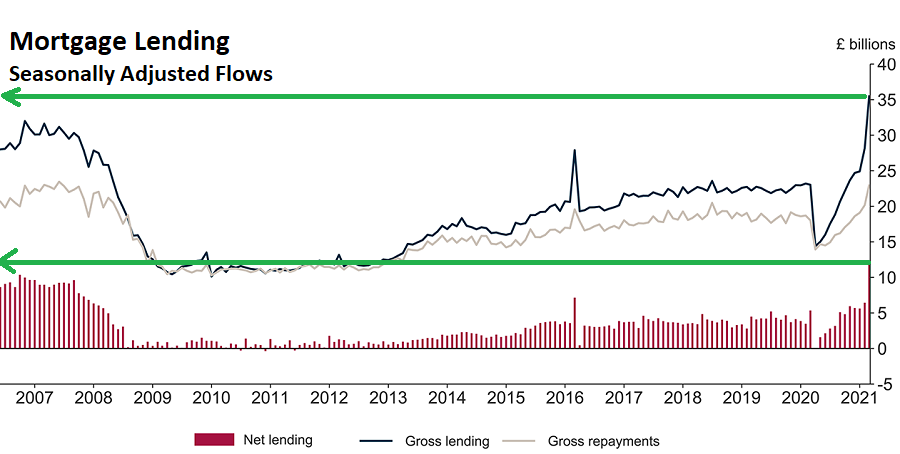

Net mortgage borrowing in the UK hit £11.8 billion in March, the strongest since the series began in 1993, according to Bank of England data. The previous peak was in October 2006 (£10.4 billion), when the UK was in the grip of the pre-financial crisis bubble. The difference between then and now is that back then the economy was about to fall off a cliff, whereas now it has already fallen off a cliff, having last year suffered its biggest drop in economic output in 300 years.

The UK’s biggest lender HSBC said it doled out more mortgages in March than in any other month of more than 40 years offering home loans.

There are plenty of reasons for this lending boom, including the ongoing exodus from the cities to the villages of rural England, even as London’s population is shrinking for the first time in 30 years, and rents have been falling for 13 straight months.

But home prices are also rising, albeit less steeply, in London and other major cities. In April 2021 Chestertons reported 65% more buyer enquiries in London, 75% more sales agreed and 90% more sales completed than in April 2019. These findings chime with HMRC’s latest figures, which show record transactions numbers in March across the UK – up 93% from 2019.

The most important reason for the surging volume of residential property transactions is the support provided by the Bank of England and UK government to property buyers and investors.

In mid-March 2020, as it grappled with the early fallout of the virus crisis, the BoE slashed the UK’s base interest rate from 0.75% to 0.25%, then a week later to 0.1%, the lowest ever. The rate cut was in response to the economic stress caused by the shutdown of the UK economy. And the falling mortgage rates have stoked demand for housing.

The government too has pursued policies aimed at inflating the housing market and propping up the mortgage lending industry. First, it introduced a stamp duty holiday that was supposed to end at the end of March but was extended at the last minute til the end of June. This has driven much of the recent surge in new mortgages.

Then, last month, the Chancellor announced the launch of new government-backed mortgages with 5% down-payments. If borrowers default on the mortgages, taxpayers rather than the banks will be on the hook. Here’s what the government had to say at the launch of the lending program:

“First announced at the Budget, the scheme will help first time buyers or current homeowners secure a mortgage with just a 5% deposit to buy a house of up to £600,000 – providing an affordable route to home ownership for aspiring home-owners.

“The government will offer lenders the guarantee they need to provide mortgages that cover the other 95%, subject to the usual affordability checks.”

The government admitted that the COVID-19 pandemic “has led to a reduction in the availability of high loan-to-value (LTV) mortgage products, particularly for prospective homebuyers with only a 5% deposit.”

Banks, it seems, are no longer offering the 95% or 100% deals on mortgages to first-time homeowners that were essentially guaranteed by parents or other family members. You can’t exactly blame banks for tightening their lending standards. Given the acute economic uncertainty that continues to prevail even as the UK economy begins to reopen, it’s not easy to tell who will still be solvent in a year or two’s time.

So the government is committed, it says, “to supporting people who aspire to become homeowners, helping over 685,000 households to purchase a home since 2010 through government backed schemes including Help to Buy and Right to Buy.”

The government’s own National Audit Office had found that the Help to Buy scheme dished out billions of pounds of publicly subsidized loans to relatively well heeled homeowners who were perfectly capable of buying their first property without need for outside help. As of 2018 only 37% of the roughly 210,000 people who had benefited from Help to Buy would not have been able to afford a property without it.

In the Help-to-Buy scheme first-time property buyers got to put down a deposit of as little as 5% on a new-build home worth as much as £600,000 and received an “equity loan” from the government. The loan covered between 20%-40% of the property price depending on its location. The rest of the financing was covered by a traditional mortgage.

Now the government is going the full hog and offering to subsidize mortgages with 5% down payments for first-time buyers. Banks such as Lloyds, Santander, Barclays, HSBC and NatWest are already offering the mortgages. And they’re also slashing their mortgage rates. Presumably, they are also loosening their lending standards. After all, it’s the government’s problem — not theirs — if a borrower defaults.

But no cost is too high when it comes to sustaining the UK’s all-important housing bubble. And for the moment it’s working: according to the mortgage lender Nationwide, in April, the average UK house price jumped 2.1% compared with March, the biggest monthly rise recorded in 17 years.

This comes as some 130,000 homeowners were still on mortgage holidays as of March, according to trade body UK Finance. Another 500,000 people are on tailored payment plans with their banks. There are also over a million people trapped in unmortgageable apartments due to the flammable cladding crisis, which is already having an effect on prices at the lower end of the market, where the specter of forced sellers looms large. By Nick Corbishley, for WOLF STREET.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The UK (and US) government/central banks only tool left is massive debt.

And their only way out, as they see it, is to inflate this problem away.

“This comes as some 130,000 homeowners were still on mortgage holidays as of March, according to trade body UK Finance. Another 500,000 people are on tailored payment plans with their banks. There are also over a million people trapped in unmortgageable apartments due to the flammable cladding crisis,”

This is the last hurrah of a once glorious nation. With the BOE buying almost all of government debt issuance, this is the last stop before full banana republic.

For anyone in any doubt please read The Welfare State We Are In – James Bartholomew

Ridiculous policies, designed to benefit property owners (like the members of parliament). Of course they will never do anything that benefits first time buyers if it doesn’t benefit themselves.

The stamp duty holiday advantage and more just goes into the pocket of property owners because in this red-hot market buyers are “forced” to increase their bid by at least that amount. There is no advantage at all in this for people trying to buy. Quite the opposite.

Did you actually read the article YuShan?!

Hi Nick. Thanks for the article. Are you saying the government agency is gifting the first time homeowner the 5% down payment?

In a sense, yes. To encourage home ownership and lending, the Government usually let’s you pay 5% down on a house and the Government covers the rest. Much like here in the U.S. with an FHA loan, although the dynamics maybe a little different over in the U.K.

No. The “government (read taxpayer)” is backing the mortgage up to a 600k house price. So if someone buys a house at that price, it appears that the government will cover part of any losses due to foreclosure .

Looking at the example on one of the government websites. 100k house.

5k deposit

95k loan

The government will help cover any losses down to 80k or written differently they will support any losses on the top 20% of the house price. The lender takes the first 5% hit on the 15k (20k-5k deposit), 750 quid, which means the maximum the government can be on the hook for in this example is 14.25k.

So let’s say HSBC make a loan for the 95k. They recover 85k plus the 5k deposit which means there is a 10k loss. They bear 5% of that which is 500 quid and the government covers 9.5k.

So what does this mean? Basically it’s just another reason why it’s in the government’s interest and the providers for the bubble to keep on going. Probably pension schemes too.

Ssshh, don’t talk about what junk pension funds may have bought over the past few years, you’ll scare the horses…

No, but it’s guaranteeing the other 95% — namely the entire mortgage.

“Stoke the housing fire”

If only they could build with some kind of insullation that’s not flammable.

The only insulation people have in general is to vote these people out of office. Until people can truly understand why they are inflating home prices (on purpose) while diminishing the buying power of their own currency, I don’t think there can be any more insulation than having a fluff policy that get’s voted into law only stopping a few leaks. Tell them to either pack their stuff (not happening) or give some answers so people can have an understanding at what their own un-elected masters are doing so we can have a better understanding of the situation in which everyone participates in (also unlikely to happen)…

SAY GOODBYE TO YOUR INSULLAION lol

Didnt Blackrock go all in on real estate about 6 years ago?

And isnt the Fed STILL….still…buying MBSs even though there is now a dearth of supply and prices are up sharply?

And isnt the 30yr mortgage rate, courtesy of the Fed buying paper, now roughly equal to the CPI rate of increase? Has that ever happened before?

Last few times CPI increases were this high (1999 and 2006) 30 yr mortgages were 6%? What changed?

And isnt the Fed partnered up with Blackrock? (now, that’s different)

What is your point? If this isn’t a PERFECT, SCRUMPTIOUS, BEAUTIFUL example of corruption or a scam, then I don’t know what is. Let’s take it back to the basics shall we? The Fed’s job…. is to act as a lender of last resort right? Better yet, why does it even exist… The Fed is an INSTITUTION… not a bank, an institution with shareholders… and yet they get to deposit money into commercial banks, thus readily giving everyone from lenders and borrowers alike endless revolving credit, again lowering rates on auto loans, student loans, credit cards etc.? AND SINCE WHEN DOES AN INSTITUTION GET TO TO WORK WITH A FINANCIAL FIRM to buy ETF’s. The japanification of the western world ceases to amaze me… I take that back. The complacency of citizens from the western world ceases to amaze me… that’s more like it lol

Low interest rates, the biggest increase in savings on record due to Covid-19 and the stamp duty holiday. I read an article in Money Week, a reasonable finance magazine get, that said the average saving on stamp duty was just under 12k average, offset by a 57k average increase in the price. Houses gone in days. First offers coming in 20% over asking. It’s ludicrous stuff. It’s a dumb time to buy.

“over 1 million are in unmortgageable apartments due to the flammable cladding crisis.”

A seemingly insurmountable problem as none will volunteer to take the inevitable financial hit.

I’d be curious to know of any credible solutions that have been proposed.

Same/similar situation has happened in FL when condos have been condemned for structural deficiencies and declared unhabitable, mit.

Most cases, the condos were purchased at deep discounts by investors/speculators who sometimes bought enough to control the HOA board, and then made their own rules…

Another important aspect is that the retirement home market has completely frozen up. Nobody wants to move into these properties right now as the residents have been devastated by covid outbreaks.

Many of these people will be older folks in better properties (due to buying decades ago) and this is an important source of new supply into the market that has evaporated. But it obviously won’t last as many of these folks need to move into a form of assisted living sooner rather than later.

Don’t have figures but there are stories around the media about his retirement properties are unsellable right now.

In the UK there was a wholely different scandal about retirement apartments. I’m sure Nick knows more about that than I do.

The timing on this seems bizarre, but with the “un-sellable” home crisis unique to the UK, maybe not so bizarre. I guess this is the equivalent of the US FED continually buying MBS when the market does not dictate to do so.

Homes are stocks, stocks are casino chips, crypto is mysteriously valuable and my fast food burger costs $8 USD now.

“It’s the end of the world as we know it, it’s the end of the world as we know it, it’s the end of the world as we know it… and I feel fine”

How much do they waste on the monarchy each year. Loss leader?

Here in Sweden stats were published last Friday that showed that house prices had gained an average of 19% in the last 12 months according to “Svensk Mäklarstatistik” (“Swedish realtor statistics”). Another index composed by an internet site that list most sales in Sweden and gov. lender came out a few days earlier and claimed that prices had risen by around 25% in the last year. From news coverage in the last year, it seems like here too, people have left the capital and supposedly Stockholm has lost population during the lock down, though house prices in the Stockholm metro area has risen even more than average for the country. Already before this, we were already in a bubble.

Several fairly remote locations have also seen prises rise far more than average for the country. I don’t feel like this will end well and I don’t feel like people I feel out about this understand how badly this can end. All loans are non-recourse in Sweden. After the housing crises in the early 90’s, some people spent the rest of their lives in absolute financial misery with many people killing themselves because after they lost their houses, they were still burdened by high interest loans that they could never pay back and if they managed to make any money, they banks clawed it right out of their pay before they even got to see it. House prises have tripled in just the last 15 years and are now are several times higher in comparison to income than they were during the 90’s crises.

I was deep in housing market 15 years ago with two houses totaling 5000 sq ft. I am out of it completely for 15 years and renting month to month in the gray market. I can live in anything as long as it’s in a safe neighborhood and roach free.

I don’t think traditional housing offers much value if you are single because most SFH are too big. Anything over 500sq ft is wasted for me.

A pretty shitty house down my street just sold at 3.3 million SEK. Looking at that, I will be selling my much nicer house before July.

This will not last!

Complete mismanagement as we come to expect from government. This is true for every single thing they touch, the UK is basically being systematically ruined. On the subject, I live in a smallish town about 35 miles south of Glasgow. It is going bananas there, developments of 3 to 6 bed houses and all being snapped up. Existing houses don’t even last a week on listing. There is not a lot of work for people of these income levels so we assume they are commuting or even on the work from anywhere lark.

Boris Ponzi

The most important thing about England and I mean England (not the UK) is that we just do not have enough houses or appartments for the size of the population (and haven’t for many years). It means that we will always have massive price increases every so often as people get desperate for a home. This is one of those times and probably will be followed by a crash of some sort. After the crash we will still not have enough homes and so it carries on….and on and on….

This is a common misconception, there are almost a million empty properties in the UK (not sure about England specifically).

The reality is with Brexit, immigration is greatly reduced and our falling birthday, which has been going for almost 2 decades, has been greatly accelerated by COVID and the inability of the young to secure a platform for family formation.

Consequences will be dire, people are taking on huge leverage to purchase with is naturally a depreciating asset (houses don’t last forever). Indenture awaits and it makes me sick

*birthrate not birthday :)

Thank you very much for a write up from another part of the world. Glad Wolf partners up with you. Have to be honest some of the words you use are strange to my vocab but I adjust. So the same thing is happening there as here in that the government has got their hand good and deep into the cookie jar. Higher and higher we go. Gravity has been defied for another period of time

I’m not sure what option B is. Prices in many areas are higher than any normal buyer can afford without help, do we scrap all schemes and let the BTL scum step in buy out everything?

Altering rules to prevent repo’s during the last recession was needed to prevent people being thrown on the street, and was cheaper then providing government paid housing to them, but it prevented the house price correction that normally happens. Dammed if you do dammed if you don’t.

Hi Nick! Thanks for sharing superb information about “How the BoE & UK Government Stoke the Housing Fire” I have been searching for this type of information for a long time. Keep sharing!

The reason I keep my UK house is because I believe freehold property is safer than cash in a bank.

Mortgage repayments in the UK are less than rent payments with current interest rates that cannot rise much in the future.

The reason house prices are so high in the UK is due to demand partly because of the influx of immigrants over the last fifteen years.

The UK has had more than 4 Million immigrants in that time and they have knocked out children. So on the basis of 4 people o a house, one million more houses required.

Bank lending is the main reason for house price increases in the booms since 1970, including this latest one. UK total money supply about £600 billion in 1996, near to £3000 billion now. New lending creates new deposits elsewhere in the banking system. Bank of England has created £800 billion via Quantitative Easing since 2008 as well.

– Welcome to another housing bubble !!!! Seems the UK government is “in the pocket” of the british banking system.