Only exception: San Francisco Bay Area condo prices are down from a year ago.

By Wolf Richter for WOLF STREET.

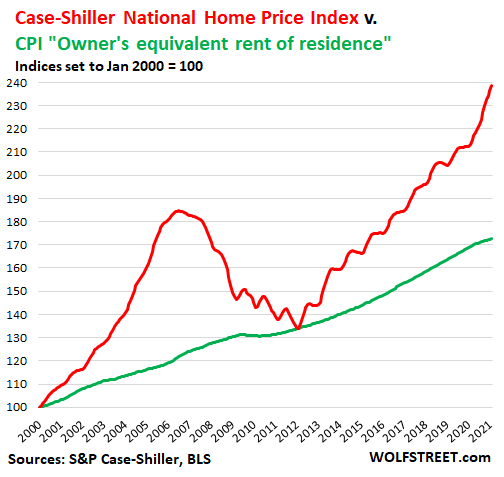

House prices soared by 12.0% from a year ago, the biggest increase since February 2006, near the peak of Housing Bubble 1, according to today’s National Case-Shiller Home Price Index for “February,” which reflects the three-month average of sales recorded in public records in December, January, and February.

A measure of “house-price inflation.”

The Case-Shiller Index compares the sales price of a house in the current month to the price of the same house when it sold previously. This “sales pairs method” tracks the amount of dollars it takes to buy the same house over time. Home improvements are included in the methodology. This makes the index the most appropriate measure of house price inflation in the US.

The Consumer Price Index (CPI), on the other hand, tracks the housing inflation component based on rents. The CPI for “Owner’s equivalent rent of residence,” weighing about 25% of the overall CPI, is based on homeowners’ estimates about how much their home would rent for, which ticked up 2.0% from a year ago (green line), compared to house price inflation as measured by the Case-Shiller index (red line):

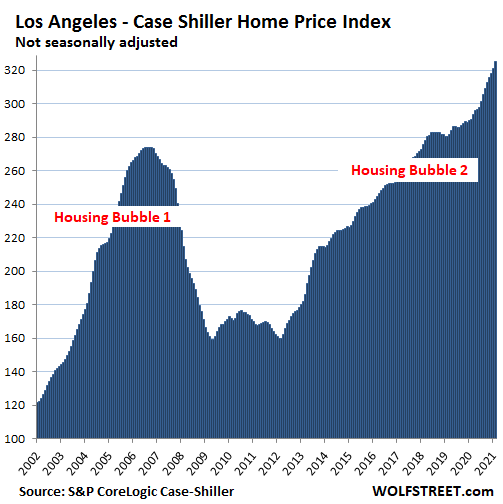

Los Angeles – the #1 most splendid housing bubble:

The Case-Shiller Index for prices of single-family houses in the Los Angeles metro jumped by 1.3% in February from January and by 12% year-over-year. The index value for Los Angeles of 325 indicates house prices in the metro have surged by 225% since January 2000, thereby making Los Angeles the most splendid housing bubble on this list.

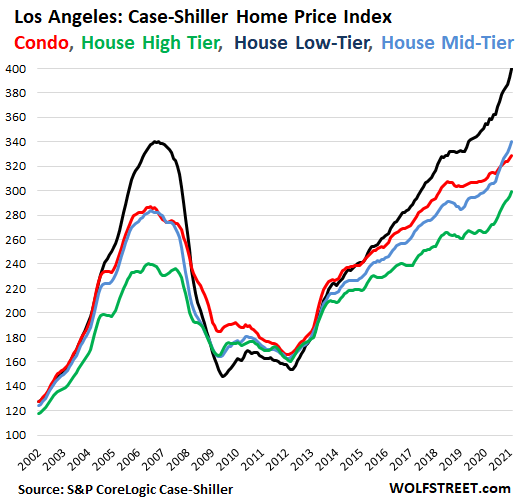

Low-tier house prices have exploded in recent years, which they had also done during Housing Bubble 1, and then collapsed the most during the Housing Bust. Year-over-year, low-tier prices are up 12.9% and have quadrupled since 2000 (black line in the chart below).

Mid-tier prices jumped 12.7% and high-tier prices 11.8%. But condo prices (red line) rose “only” 5.9% year-over-year:

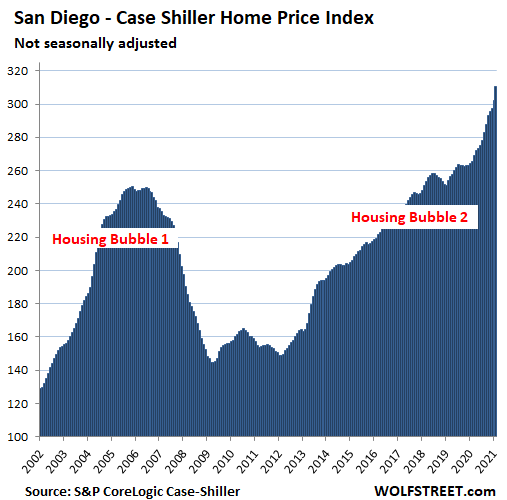

San Diego:

House prices in the San Diego metro spiked by 2.9% in February from January and by a holy-moly 17.0% from a year earlier, making it the market with the second-hottest annual house price inflation on today’s list of the Most Splendid Housing Bubbles, behind Phoenix. Prices have more than tripled (+210%) since 2000:

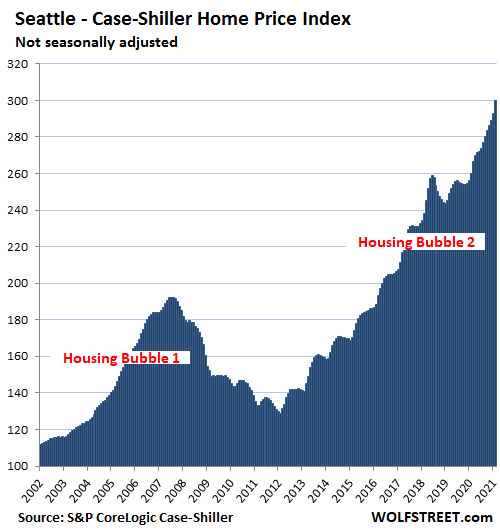

Seattle:

Seattle house prices spiked by 2.4% in February from January and by 15.4% year-over-year, making it the metro with the third hottest annual house price inflation, behind Phoenix and San Diego. Since 2000, prices have tripled (+200%):

The charts below are on the same scale as Seattle, San Diego, and Los Angeles. As we go down the list, the amount of white space above the price area grows, indicating that over the past 20 years, the other metros have experienced somewhat less house price inflation.

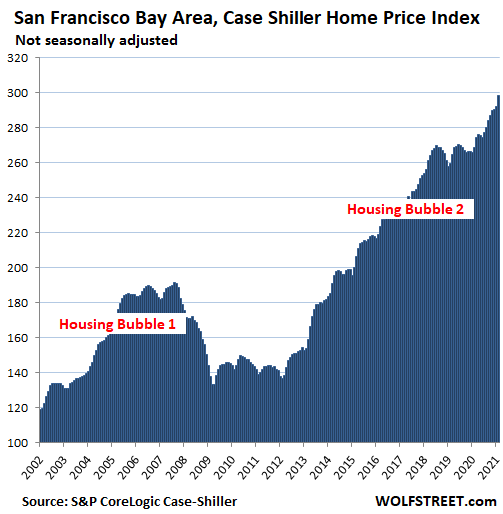

San Francisco Bay Area:

House prices in the five-county San Francisco Bay Area spiked by 2.1% in February from January and by 11.0% year-over-year. They have nearly tripled since 2000 (+198%). The Case-Shiller Index covers the counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay):

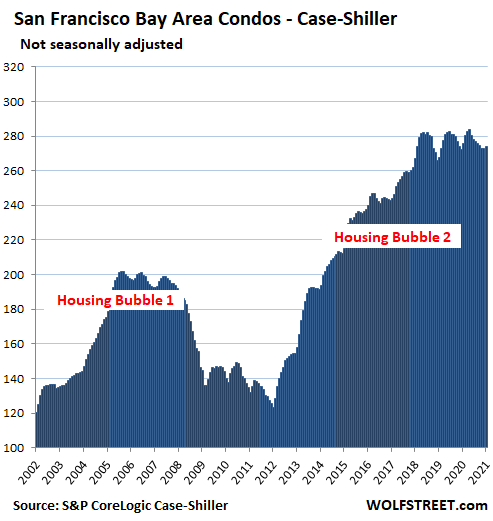

Condo prices in the San Francisco Bay Area rose 1.1% in February from January, roughly in line with seasonal increases from January, which is generally the low point of the year. Year-over-year condo prices declined by 0.7%, the ninth month in a row of year-over-year declines, leaving the index below where it had first been in March 2018:

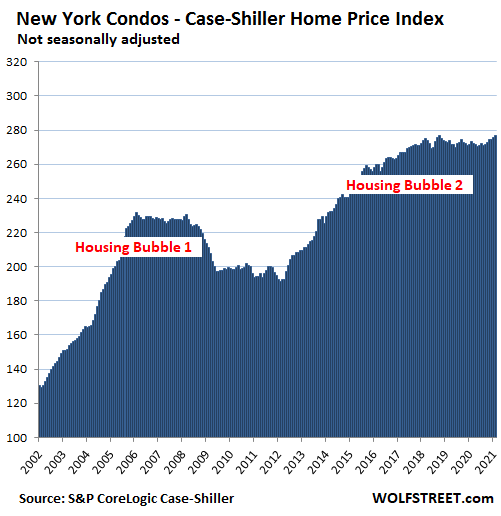

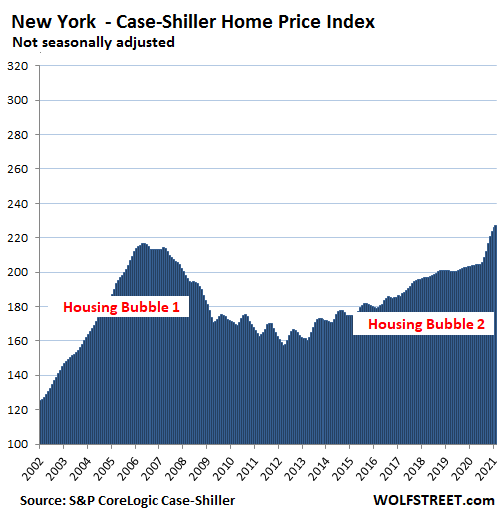

New York City metro:

Condo prices in the vast New York City metro (New York City plus numerous counties in the states of New York, New Jersey, and Connecticut), rose 0.5% for the month and were up 1.2% year-over-year, but have remained roughly in the same range since late 2017:

House prices in the New York City metro rose 0.6% in February from January, the smallest month-to-month increase since last July, after the blistering spike late last year. Year-over-year, house prices were up 11.6%:

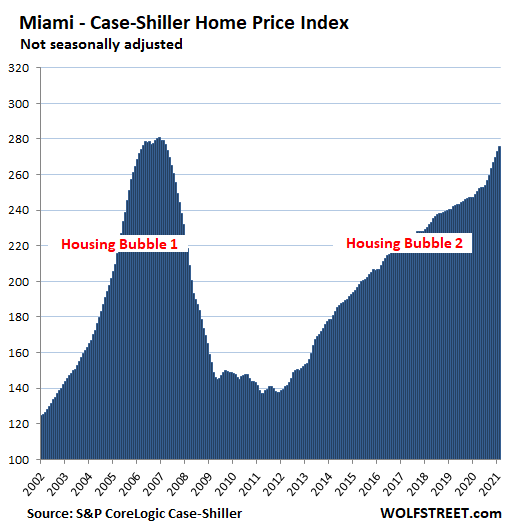

Miami:

House prices rose 1.0% for the month and 11% year-over-year and are up 176% since 2000, but they remain a smidgen below the crazy peak of Housing Bubble 1:

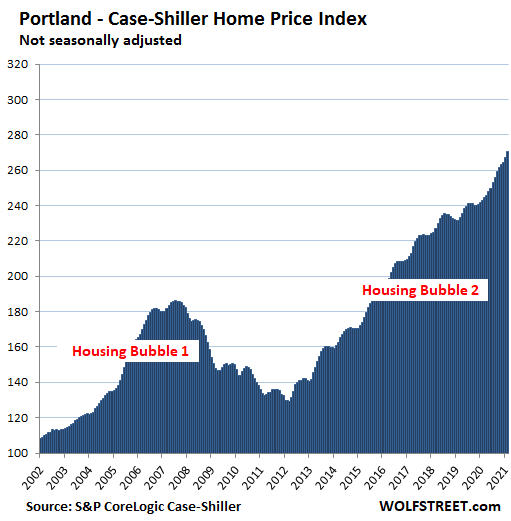

Portland:

In the Portland metro, house prices jumped 1.3% for the month and by 11.4% year-over-year:

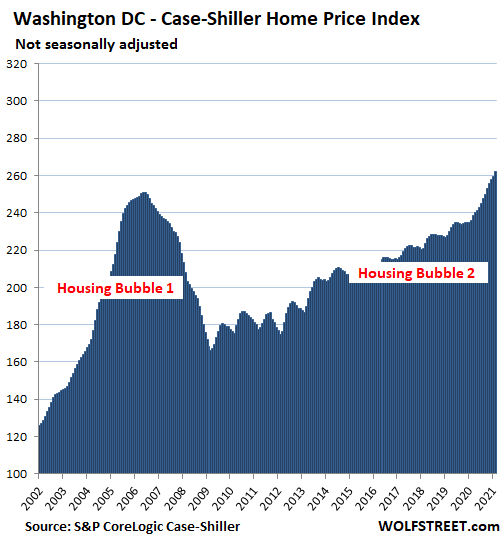

Washington D.C.:

In the Washington D.C. metro, house prices rose 1.0% for the month and 11.1% year-over-year:

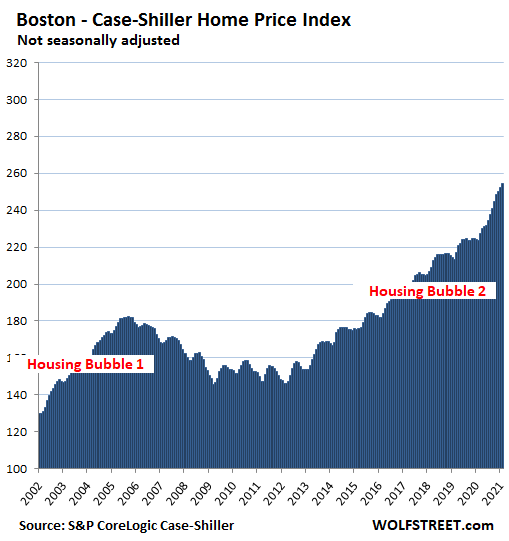

Boston:

In the Boston metro, house prices rose 0.9% for the month and soared 13.7% year-over-year. Not included here: condo prices, which are up “only” 4.0% year-over-year:

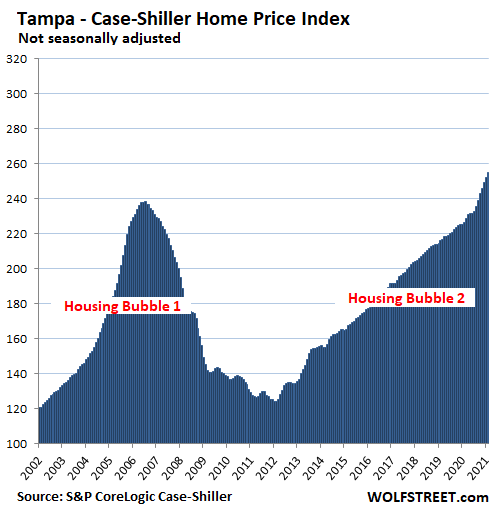

Tampa:

House prices jumped 1.3% for the month and 12.7% year-over-year:

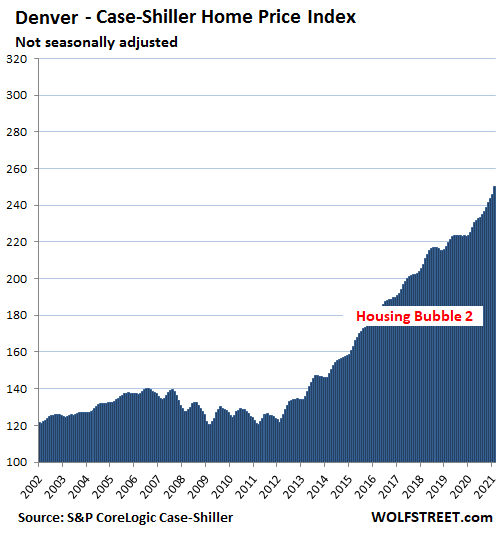

Denver:

House prices spiked 1.8% for the month and are up 11.2% year-over-year:

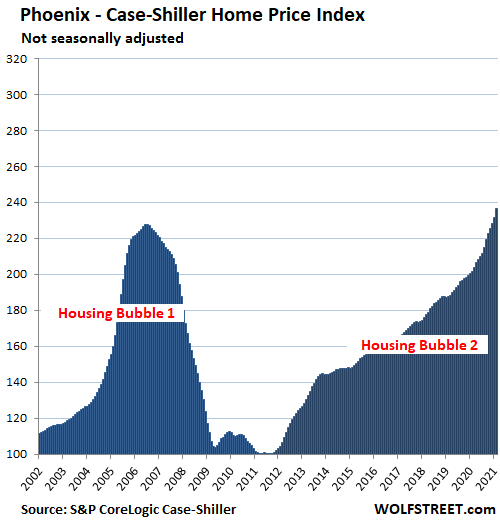

Phoenix:

House prices spiked 2.0% for the month and another holy-moly 17.4% year-over-year, giving the Phoenix metro the hottest annual house price inflation among the Splendid Housing Bubbles here, ahead of San Diego and Seattle:

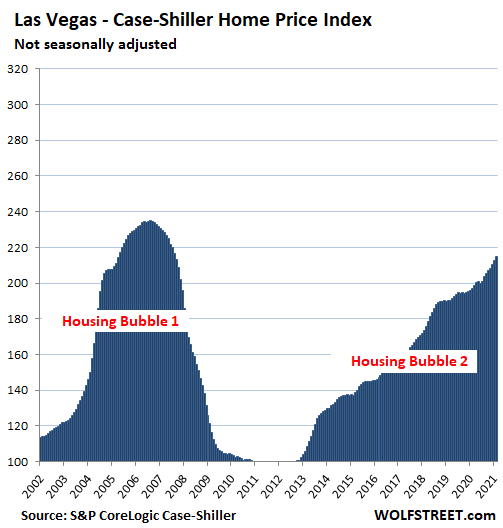

Las Vegas:

House prices in the Las Vegas metro rose 1.0% for the month and 9.1% year-over-year:

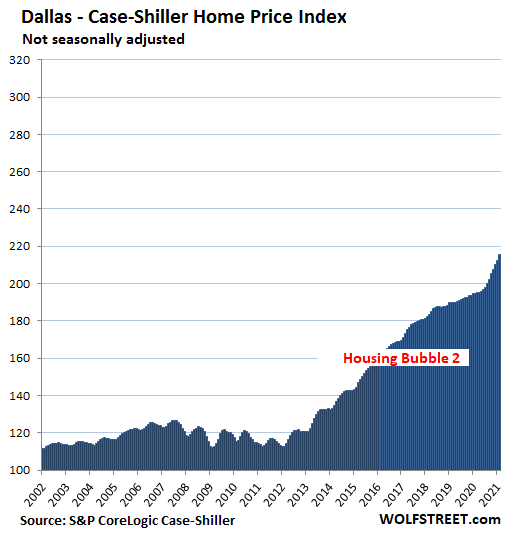

Dallas:

House prices in the Dallas metro jumped 1.4% for the month and 10.9% year-over-year, and are up 116% since 2000, meaning that house price inflation was 116% over the past 20 years. In the remaining cities in the 20-city Case-Shiller Index, the 20-year house price inflation has been less than 100% — for example, Chicago’s 20-year house price inflation is at 56%. This makes Dallas the last entry on this infamous list of the most Splendid Housing Bubbles in America:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Is this evolving into a West Coast bubble? Any chance of doing housing bubbles around the Pacific Rim? Alaska?

“Evolving?” LOL. This is one of the biggest bubbles of all and not just on the West Coast.

However, as a property owner in one of those markets, keep in mind that inflation is continuing to surge. Hyperinflation may be around the corner thanks to the privately-owned, banksters’ “Federal” Reserve efforts to continue thieving from ordinary Americans’ (already pathetic) wages and “wealth.”

The banksters’ “Federal” Reserve is likely bailing them out in some new way yet again even as I write. To do that, of course, it will create trillions more in legal tender as it just created $2 TRILLION to gift the banksters in exchange for their now worthless, uncollectible, mortgage backed bonds. (Cui bono?P)

Hence, if you sell now, you may later be unable to use that amount to buy an equivalent house next year if inflation continues. (That happened to a person I knew years ago.) Remember brokerage fees, selling costs, and taxes?

That would explain why so many are reluctant to sell now, or at least, why I am reluctant. That would explain why people are desperate to climb into what may well be one of the biggest bubbles of all: the real estate bubble. This real estate bubble may only last due to the even more reckless, corrupt actions of the banksters’ “Federal” Reserve.

Some buyers who are planning on moving in a year or two are buying now, like retirees. Wolf should factor that in. I am further convinced that the Fed set their employment benchmark so corporate America would know where not to step in order to set off a tapering event. They can raise prices and constrain supply, and production, as long as the stimulus backstops remain in place. The checks keep arriving on time. Corporate America doesn’t need to provide a living wage. What they lose in volume they make up on increased margins. This has the double benefit of preventing new startups from competing directly. The end game is they do all their own lending facilities, Iphones to autos (homes). What exactly is a “forgivable” loan?

Well, we have exactly the same bubbles here in the east coast of Australia. So yeah, a ring of fire.

East coast Canada here.

Massive influx, percentage-wise, of just about every age of people. There are very few jobs here, so the movers are couples who either work electronically remotely, or work shifts in remote areas and are choosing here as the base, plus many retirees. The younger ones can’t afford the new homes with the big price increases, so are buying the fixer-uppers. The big price increases here are still a lot cheaper than the properties that the movers are selling in the big cities (mainly Tronno/Van). All this puts the prices way out of reach of those who were born here. Rental availability is non-existent. No camper under $20k stays on the market more than 3 days (and it’s still snowing). The health infrastructure is rapidly dropping from inadequate to dangerous, doctors are leaving and replacements aren’t interested because of workload problems, and nurses can’t afford to move here. Most couples moving don’t have (m)any children, so education is OK at present. There’s a housebuilding boom, so all tradesmen are booked up over a year ahead. There is an awful lot of unpermitted work going on, partly because the inspectors don’t have the manpower to even start inspecting anything but commercial work, and partly because people have to do DIY because of the lack of tradesmen.

Wild times.

With the moratorium for foreclosures ending in June and Interest Rates on the rise should we expect a a supply side shock heading into the fall that will reverse this bubble?

They are not going to end foreclosure moratoriums. What started out as an illegal overreach by the CDC under the guise of preventing the spread of the virus has morphed into “but all of these people are going to be homeless!” This sh!tshow is going to continue until we have a full-scale economic meltdown.

Instead of making landlords pay for free rent, lets tax Powell & his subsidized rich friends & Google Fakebook Big Pharma etc at 91% to pay for it AND let’s vacate the WH and members of Congress private homes and turn them into homeless shelters. It’s only fair.

Don’t be ridiculous!!! I, King J-Pow will never allow for that!!!!! Absuuuuuuurd!!!!

It’s going to end when people start using their damn brain, and start remedying hard choices, instead of pushing it down the road. Wow, does this sound familiar?

This is my fear as someone who doesn’t own a home. Mortgage forbearance will likely be used in any future downturn. We live in fucked up times.

An understanding of the national accounts is improving, but not sufficiently enough to use employment boosting Congressional spending. Way too much of the spending is directed at propping up assets owned by the wealthy. A national job guarantee–a real ‘right to work’ legislation–would mitigate a lot of this waste.

That would be sad indeed. It would mean the barrier to entry is forever high. I fear it, too. But somehow I don’t think the government is so powerful that they can keep this mess from hitting the fan. I think there will be a crash but when, who knows. Hopefully soon. Delaying it is just going to create more suffering.

Well that’s moral hazard for you. A lot of mad people who feel it’s unfair eventually revolt by joining in the process of taking advantage of malincentives. Quit paying your mortgage or rent until they realize all the landlords declaring bankruptcy is a problem. Just like the Fed encouraging bubbles, or the govt refusing to punish reckless bankers, or lying over and over and the SEC doesn’t care. We live in an amoral world now when it comes to money and economics. If you don’t believe in spirituality, then what reason is there to do what’s right? Stop caring about money if you want to be free from the madness.

If the better part of a whole generation is forever locked out of home buying, there will be long term political ramifications or worse. The divide between haves and have nots just continues to get worse with the Feds policies.

Well, I’m waiting for the CDC to start censoring people because they spread lies on social media. Heh heh, that would be something.

It’s hilarious what the CDC got away with, Trump obviously paid no attention there, since he figured it help him get re-elected, and it would be shocking if Biden actually ended this moratorium and forbearance BS. I would guess that somebody told him the consequences of such an action.

I’ll repeat it here or else it gets lost in the jumble:

The CDC did the eviction moratorium (of renters).

The foreclosure moratorium (of homeowners) was put in place by the FHFA.

Depth Charge,

Some confusion here.

The CDC did the eviction moratorium (of renters).

The foreclosure moratorium (of homeowners) was put in place by the FHFA.

Yes, you’re right, Wolf. I will not make that error again. I am a big proponent of facts and accuracy, which is one of the reasons I love your site.

Has the CDC announced when the “eviction moratorium of renters” will end?

Secondly, is Fed money going towards the medium-sized landlords and to corporations that own vast amount of “rental property” in the US??

I agree, they are not going to end foreclosure moratoriums and they will do anything to prevent a supply shock.

A quote I saw posted here said (roughly) that if a policy has a predictable result, that’s the reason for the policy. The only conclusions a reasonable person can come to in this case is that either A) It’s a case of EXTREEEEEEME incompetence &/or corruption, or B) It’s a conspiracy, the purpose of which is directly related to the perceived “chaos” we are witnessing.

The only way for the supply to increase is for Biden to pass his 43.4% capital gains tax. Then those greedy hoarders who owned multiple homes (including those who refused to sell their old home) will all sell like idiots towards end of the year as they fear if they don’t sell this year, next year they have to pay 20% more tax on the gain

Tim,

You don’t think a tax hike passed in later 2021 won’t be made retroactive to Jan 2021?

Ha!

Retroactivity has become very, very common in Dem controlled politics.

“Then those greedy hoarders who owned multiple homes…will all sell like idiots…”

You’re right Tim. They will find themselves to be idiots, after the fact.

“Gosh, maybe I should’ve sold my old place, like, sooner…”

Would this not depend on how many of the hoarders have over $1 million per year in income rather than $1 million in capital gains in a particular year?

Not everyone is a “greedy hoarder”. Some people worked hard and bought when they could, put in the time and effort and money to maintain and have benefitted from that long path. Something that everyone here would do in a heartbeat if they had the chance.

And not everyone will need to sell. More important than the capital gains increase will be the elimination, if indeed it ever happens, of the Step-up basis.

This ain’t Russia, property ownership is not a crime despite what many seem to be promoting.

Those “greedy hoarders” are doing what’s in their best interest, legally. Keep the blame where it’s due, on the policy makers.

“The only way for the supply to increase is for Biden to pass his 43.4% capital gains tax.”

Wishful thinking considering the immense power & money the 5% wealthiest of us possess.

The US Hegemony will have to have sailed away into past history before passing a wealth tax that massive.

Why do you think property ownership in Russia is illegal? My parents have 2000 sf house, that they built in 1980 th, they didn’t borrow any money and were able to finish it in 3 years. Now they have a house and pay nothing in property tax, utilities(electricity, gas and water) cost them around 50 to 70$ a month, so they actually own their house, not like in the US, where you have to pay 5000-10 000 in property tax and your house can be taking away within couple of years if you don’t have money to pay it.

wrong on both counts, moratorium will be extended ad infinitum because its not people’s fault if they cant pay said uncle Jerome, and interest rates aren’t going up said uncle Jay. Long live our dear leader Jay.

When a house price gain in a year is more than the entire yearly median household income for that area, you know have a massive bubble that’s going to pop. Anybody saying otherwise is either blinded by greed or as dumb as a stump.

I ran the 200% gain through an on-line calculator. Putting 20% down with a 4% 30 year mortgage with standard assumptions for tax, insurance, maintenance and real estate sales commission I get that if you sell now you will have lived there for free with about a 7% additional annualized return on your down payment. Take your profit and go live somewhere cheap before ponzi economics runs out.

Fed policy has definitely made winners if you were a leveraged asset holder of nearly any type. Grandma renting with her CDs, not so much.

Or blinded by fear of missing out.

Forget annual, my parents house in SoCal appreciated $40K last month alone, which is the per capita median income in San Diego County!

In 2006 – 2007 people were joking, “My house makes more than I do!” Today it’s nearly, “My house makes more than I do – EVERY MONTH!”

Hello buyers, are you stupid? They’re acting just like in 2006 – 2007. Neither Weimar Boy nor Uncle Sam have superpowers to sustain this house of cards.

Surely you are describing Boise, Idaho. I can’t believe hasnt done a feature on Boise considering the house price/ to median income is wild.

I know, I’m waiting for the Boise / Reno analysis too. It’s really something in those places. They are today what Phoenix / Las Vegas were last time around. It’s going to be ugly.

San Diego:

I looked up in redfin and zillow for zip code 92130 (Carmel Valley area).

There are some homes listed at 299K. I was super surprised.

Then went on to read the description.

Its the price for Fractional Ownership – 5 weeks in a year, you get to own the house – ownership is 1/10th of the house apparently.

Wow.

Do you have to pay prorated fees, HOA, taxes, Mella Roos?? How in the world do you sell a house with 10 owners?? How do the police respond? Come out with your hands up Bob. Sorry copper, Bob was last week. Harry is next week and he’s a bit crazy too in case we can’t resolve this..

“Time shares.” They’re once again being marketed, after having collapsed. If you buy one, you will find out that they’re nearly impossible to sell. Time shares are a nightmare come true.

Wolf,

A post reviewing the large financial players who have driven the buy-to-rent movement would really be useful.

Given their presumed savvy, one might think they would be selling into this goofy upswing…but…I don’t know, with transaction volumes up, they made be siding with the madness.

(“So long as the music plays, you’ve gotta dance (of the dead)”).

Given the mega buy-to-renters’ access to debt and their financial engineering tools, it is actually possible that they are behind a decent chunk of the rush to madness.

(“Everybody thinks they will be first to the door”).

I wonder what the mega-buyers public numbers say.

I’ve been wondering that as well. What in the hell is their end game? Are they somehow back stopped? Logic would tell you they would wait out a crash but instead they’re helping to blow it bigger. I’ve read that the buy and lease back to the former owners is gathering momentum which seems even more weird. If the current owner is already in a precarious position and can’t cover the nut how do they make rent?

The big thing now is: Build to rent. Whole neighborhoods are being built as rentals.

Wolf,

At least build2rent adds to supply (if at dubious/unsustainable new build prices).

In contrast, borrow2bid-up doesn’t add to supply and only jacks up prices for everybody.

I’m not 100% shocked at price hikes (forget the hundreds of thousands killed…ZIRP is magic…) but I am a bit more surprised to see transactional volumes also going up.

Post 2008 implosion, transactional volumes were way off their boom time peaks…people got their hand burnt off and they learned to stay away from the stove.

But post-plague volume increases (albeit with superZIRP) does raise questions about whether or not everybody has really learned the lessons of 2008.

The increases aren’t huge but…Covid for cripes sakes.

It’s our understanding that BIG Real Estate/Banks/Insurance are worth trillions of $$$s.

Supposedly, they have an escape route when the population becomes so impoverished that they simply WON’T be able to afford any rental.

If you ever drive on I-5 going into Portland, Oregon, within the last 2 years, homeless camps have burst upon the scene in many parts of its bridges, under freeway on/off ramps. The vast swelling of Portland’s Homeless population extends from the east side, downtown Portland, all the way up North before you reach the I-5 Bridge that leads you to Vancouver, Washington.

There are the lucky few who live in small campers, but most are in tents.

“Time shares are a nightmare come true.”

Like 8-year car loans.

I can’t even wrap my mind around an 8 year car loan. I once had a 4 year loan – my first vehicle I took out a loan for – and it seemed like an eternity.

Wolf..

But..but.. the redfin ad says its NOT TimeShare :-)

Maybe it’s more like a golf club membership. It never rains in Cali anymore so it’s a year round activity.

Hey don’t knock time shares. When I was in training it was the only way I could afford vacations. I’d go to the free overnight stay with dinner deals and pay my dues by doing the horrible marketing sessions. Naturally I introduced my girlfriends as wives, thus garnering double points.

Little did the agents know that Dr Gorback had a net worth of about zero.

I’ve seen these around Lake Tahoe and on the Oregon Coast but that’s kind of surprising for Carmel Valley, which is just another upscale suburb. You need about $1.5M for a 1990’s cookie cutter stucco, tiled roof 4-bedroom there. It is close to Del Mar and other touristy beach areas, but it’s really not part of them.

Is this the future? ‘Burbs turning into vacation “property”?

Biggest complaint at CC meetings. Noisy neighbors at the vacation rental nextdoor. Also an issue with the taxman, who wants his cut.

No bubble here according to NAR…just being silly but I think all real estate insiders and MSM have their bots to repeat the following talking points below…can’t recall how I have seen this last month with elements from the list below.

1.) Inventory is at historic low, everyone and their mom will be working from home and escape from city center

2.) Low interest rate and will stay low forever

3.) Housing will always go up through out time

4.) FED and Government got your back

5.) This time is different, no more liar loans and banks are on their best behaviors

6.) Demographics shift in support of this raise in price

7.) If there’s a slow down, it will just level off and stay high until the next leg up

So they took “they aren’t making any more land” out of their talking point rotation?

Not yet, those are more specific to places like Hong Kong but even over there it’s not the complete truth as HK government restrict land development to a large degree, couple that with 7+M popular for such a tiny place.

“They aren’t making any more land” is one you hear a lot here in the Boston area. Maybe that helps explain the chart for Boston.

Well, if you look at the just released Census stats, they ain’t making any more people, either.

And you gotta have people for housing demand.

And, the NE states have the worst population numbers.

“No bubble here according to NAR”

Gotta love Lawrence Yun, the Baghdad Bob of real estate.

“The Consumer Price Index (CPI), on the other hand, tracks the housing inflation component based on rents.”

So a government department (BLS) cooks up numbers to understate inflation so that another government department (Fed) can create money to buy the government’s debt which ultimately benefits and enriches many large government donors and politicians.

The whole cockamamie scheme is a ruse cloaked with statistical sleight-of-hand and infused with endless layers of conflict of interest. Cui bono?

Nobody out there needs to be thinking about hurting themselves or anyone else. Cheers

Local government property taxation jurisdictions must be giddy with the realization that this bubblelicious moon shot of real estate property valuations is going to pad their revenue coffers nicely.

Will the homeowner sheeples protest that governments are reaching much deeper into their pockets? Methinks no. After all, this jolly surplus of taxes goes to a good civil cause, right?

1) Case Shiller compare the current price to the price of the same house when it was sold previously.

2) Sellers who owned a house since the 60’s, the 70’s and the 80’s

in LA or Seattle, who sold their house in Feb 2021, distort the charts, even if their number is relatively small.

3) A house in an upper middle class suburb that was bought between $50K and $60K+ in the sixties, that was sold in Feb 2021 for $1.500,000, inflate the statistic.

4) People who Bought a house 40, 50, or 60 years ago

and sold it in Feb to the CA refugees, also add distortions.

5) People who held a dollar bill since the 1970’s lost 98% of it’s value..

6) Case Shiller induce inflation. They don’t use side by side comparisons of a similar house, in the same neighborhood…

7) Case Shiller is a false positive report.

Micheal Engel,

You’re wrong with your understanding of the Case-Shiller sales pairs method, and your “distortion” conclusion is nonsense. Read the methodology:

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

And you’re absurdly deep into nonsense territory with “7) Case Shiller is a false positive report.”

The Los Angeles Case-Shiller increase = 12% yoy; the California Association of Realtors’ median price increase for LA = 17.7%!

WHAT? You mean Engel isn’t a “cloaked in mystesism”, “to smart to understand with his incoherent ramblings”, ‘revealed only to special insight” genius?

Question – what happens when the fast-moving shit-tier crapshacks reaches the higher level? Example – I am seeing crapshacks start to sell around $490,000 like hot bread, while at the same time $520,000 mansions are moved slower.

Thirty minutes north of Boston, craftsman style cottages (which are quite small and rather old by today’s standards) are selling for $650K. Got an advertisement from a realtor today showing their latest sales.

By California standards, that’s probably a great deal, but it looks more like the beginnings of a blow off top in the local real estate market to me.

Yes, and that adorable old-fashioned cottage at such a reasonably low price north of Boston may be marketed as a “starter home”. Which is one of the more insulting phrases slung around by real estate “professionals”.

As a young 59 year old, I would be a first time home buyer. I relish the thought of telling the seller’s realtor “this starter home will be my ending home. Yes, I plan to die in this starter home.”

Thank you very much and have a nice day!

I was 33 when I bought my two bedroom & one bath Sears Craftsman bungalow 26 years ago. My plan from day one was to live here until I die. So far, so good.

When your search criteria is homes under $500K you don’t even see the house that’s double the size for $30K more.

Buying something on credit, and paying it off are two very different things. Real estate bubbles are classic pump and dump schemes, and they always collapse. Usually 40-50%.

That hasn’t been the case in California the last 60 years. Overall, the banks keep digitizing money, and house prices keep going up.

Panic from Mexico

Sold our home of 27 years in Seattle December 2019. Bought a house in Mexico for a winter get-a-way and took possession February 1, 2020. All Hell brook loose in March 2020. We were going to take our time looking for a smaller home in the US ‘in the country’. We had no idea that was the plan of millions and they could run faster than us. In April housing took off like a rocket and we were stranded in Mexico for 7 months. Now, being a baby boomer, we cannot get our heads around the hoops and panic surrounding buying a house. We have been asked to stand on a beach ball and spin while balancing our wallet on our nose in order to even thin about making an offer. We are sitting on the sidelines proceed cash in the bank. A real crapshack sold for $950,000 that was an old cabin spray panted white inside to look modern. There were 20 offers. Will we outlive this?

Who cares? You have enough money to rent for life. What’s the big deal about buying a house? I’m a renter and I’m just kicking back enjoying the show. Nobody’s going to FOMO me.

But, but, but….you’re missing out on the American dream! What are you waiting for? Don’t you want “pride of ownership”? How else will you “build equity”? Don’t you know you’re “throwing your money away on rent?” Also, you’re “paying someone else’s mortgage”. The horror!

How else can you brag how much your house is now worth? How about that low interest re-fi? Yeah, I got mine too. We’re getting a new BMW SUV with our cash!

How can you bear being looked down upon by the Joneses? Don’t you also want to pour toxic chemicals into your beautifully green lawn? They’re not building any more land you know! Houses are selling like hotcakes! Buy now or be priced out forever! Rinse, repeat, ad nauseam.

I think you missed your calling as a REALTWHORE, SuzeB. You’re a natural! :)

If the History is any guide-here is how RE Bubble ended in 2008:

The thought of lowering house prices never occurred to mortgage holders.

Banks simply paid $7.5K demolition fee and razed to the ground not only individual houses but the whole city blocks and even clusters of luxury developments.

It was fun to watch.

Non-paying tenants were eventually evicted.The house is boarded up and stands dead quiet.Then it starts showing some signs of life because Nature abhors vacuum.

Eerie sounds,stifled screams,furtive coming and going,occasional gunshots…

Then some banking honcho realizes “Gee,we could get sued for dead body discovered on one of our properties.Demolish that f..er ASAP !!!”

This time will be different with Covid19 forbearance made permanent ?

No way.Because for the bank cash flow is more important than asset prices.

https://www.washingtonpost.com/business/economy/banks-turn-to-demolition-of-foreclosed-properties-to-ease-housing-market-pressures/2011/10/06/gIQAWigIgL_story.html

Some people are STILL thinking that houses are going to drop in price. Seriously people, do you still believe in the tooth fairy?

I have been reading bubble on this site since 2014… and people running difference scenarios about a crash… people holding mortgages of 2%-2.5% are never gonna sell.. period.

They might if prices go down/interest rates go up. If you have a $500K mortgage at 3% that’s $2180/month. But if you have a 400K mortgage at 5% that’s $2147, so basically the same. Plus you’d have lower property taxes, a lower down payment and a better chance to refi if rates ever dropped again.

Mark, and right now idiots are buying $350k houses priced at $500k because they can’t do simple path.

Lumber prices up 232%.

Well, not tooth fairy but Sasquatch and Aliens absolutely. Hey but I will give you benefit of the doubt, people like you and your kind are dancing on the roof top so far because you guys have been right and yet people like Wolf and his bubble watching audiences have plenty of eggs on their face. However, all data points to a bubble and unless you have an agenda or have a major case of cognitive dissonance, it’s just hard to deny the data.

As for your point about not selling at 2-2.5%, uh sure…let’s see how well that goes when you lose your job and have a $700K to $1M staring at your face. I know high paying white collar folks think they are untouchable…sure this time will be different right?

Look Don’t hate me. I am just being cynical. My lack of faith and believe is taken over. I have lost all hope…

there you go. I don’t even own a house. I have a young family and I can’t provide my own shelter without being financially reckless and YOLO.

What downturn? The FED will print money. company’s have so much cash that they buy their own stock.

ok, if you put it in that context, then yeah I understand your frustration and part of me feel like same way. It’s not a good feeling to be on the other side, at some point you just feel like that crazy guy holding the sign “The end is near!” while everyone else is partying it up like the Gilded age.

Trust me, I am in the same shoes as you, 2 young kids and just want to find a decent place to live. Not enough looking at housing as an investment, just don’t want to go through overpaying and give into FOMO. Doesn’t help that FED is making an enemy out of my money in the bank by destroying interest rates…

They’ll sell when they lose their jobs during the downturn.

Gomp, haven’t you heard? No foreclosures from now on, lol

Welcome to Socialism

Did socialism cause all this? Or did you mean the socialists will have to bail out the capitalist class. Again.

Chris Herbert, your comment is incoherent. If the socialists are doing the bailing out, then they are the problem, are they not? What you are doing is like the people who blame the squeegee men when the real blame is on the people who pay them.

Into a flooded market, too, I bet…

You are the exact type of person who disappears like a fart in the wind once the bubble pops. Make note of “Ehawk,” people, he won’t be around when this whole thing blows. Or he’ll change his name and tell everybody he predicted the coming meltdown in house prices. That’s what a lot of these types did. They’re like chameleons, changing their colors to suit the environment.

Ugh, should’ve known better…I think we just fed the troll…guilty myself. I would expect these type of comments more on doctor housingbubble but perhaps I let my guard down since Wolf’s commenters are usually less troll like. Not making that mistake again.

He could be like Suze Orman; apologize once, then again start dishing out advice nonstop.

Well to be fair 10+ years is a long time for the chameleon to be the right color. RE made money. I want it to pop too but Fed.gov is still getting its way.

Look man. I don’t comment a lot, but I always read on here. I won’t disappear.

I have said before in previous comments, that I don’t own a house. I have given up all hope. I have a young family but for the last 5 years I have seen craziness, I am, not interested in bidding wars…

I could be : Sad, angry, depressed, hopeful… and I cynical is better for my mental health.

A low-rate loan on an inflated asset is a bad loan, Ehawk…folks that’d prefer not to sell may find life dictates otherwise…loss of a job, death in the family, disability, etc, may necessitate a move.

In a word, life happens…buying at the peak of the market removes optionality, and is a sh!t deal, irrespective of whatever batsh!t good fortune you believe the market will always shine on FOMO buyers.

Even worse, there are massive property tax hikes coming down the pike. Those government worker pensions will not be allowed to default by either major party.

There are a lot of smart economists and money managers that think assets are in a blow off top and are going to crash bigger than GFC because leverage is extreme. Total World financial assets 500 Trillion financial assets makes Fed printing $120/ month look pretty small.

If they have to they will

HoUsEs OnLy Go Up

Housing bubbles always crash. If you do not know that, it must be your first trip to the rodeo…..

Actually in many cases the Mongols would offer the city an opportunity to surrender and become a Mongol vassal. If refused, they would give the city the ancient equivalent of Hiroshima. The Mongols, as a nomadic people, required large amounts of food and water. They didn’t have time for sieges. Usually they overcame these limitations by seizing supply roads and resources to limit the city’s ability to withstand a siege prior to an assault.

They also had a special weapon: gunpowder. Although they didn’t have firearms or cannons they threw bombs at the city walls with great effectiveness.

The Mongols pretty much left their conquered people alone. They didn’t force any religion or other such things on the conquered. They just wanted the payments. They were very practical people.

The extreme efficiency with which they defeated their enemies pretty much quenched any thoughts of rebellion.

Smart mofos for sure. Killers, predators, whatever – they were no different from any others of their time, just amazingly efficient. I have a grudging admiration for Genghis Khan, especially when you consider his rise to power.

His eponymously named descendants have done pretty will in the last hundred years too.

Maybe our feral reserve is a big fan also. They sure act like it.

Yes, but if the city surrendered most of the inhabitants were spared but the mongols usually put the aristocracy to the sword. Genghis had little use for what CHS terms “parasitic elites.”

It depended on how the Mongols assessed the aristocracy. If they seemed to go along they were spared. If not they were killed.

Very practical people.

“The Mongols pretty much left their conquered people alone. They didn’t force any religion or other such things on the conquered. They just wanted the payments. They were very practical people.”

So another word they were much better than what US imperialism under the guise of “bring democracy to people” has done to the world over like Latin America, parts of Asia and middle east.

They were what they were given the context of their time. Their history is absolutely fascinating.

Not only were they early adopters (eg borrowing the knowledge of gunpowder from the Chinese) they also instituted what later became our Pony Express.

They were able to manage their vast empire by setting up courier stations across Asia. Riders could switch to fresh horses and be on their way. Mongol riders could ride harder and faster than anyone. The speed with which Mongol armies could move caught quite a few enemies off guard. They could live in the saddle.

The couriers also carried special plaques on their saddles that indicated that they were under the Khan’s protection and nobody wanted to mess with them.

“They also had a special weapon: gunpowder. Although they didn’t have firearms or cannons they threw bombs at the city walls with great effectiveness. ”

Interesting.

The West was arguably won by the smallpox vaccine.

The Mongols had one thing that many other civs they encountered didn’t have. The Chinese. Much of the siege works that the Mongols employed in their push west utilized Chinese siege engineers to make sure that they can take down cities.

Not that they weren’t already the most proficient military of their time. The Mongols basically got the art of cavalry warfare that was copied by Rommel and Patton done to a science back in the 12th century. The only reason they didn’t take all of Europe was because the old guy died and his kids decided to divvy up things amongst themselves, and left after trashing Hungary. Their communications system for their time was a marvel of efficiency and effectiveness.

It’s not a grudging admiration that you should have for Chingis, he was a maverick of his time, a disrupter the likes of which few has ever witnessed on earth. And best of all, he was fair, he killed everyone equally.

Page 6 Case shiller : For each house sale transaction, if an earlier transaction was found, the two transactions are paired and

are considered repeated pair.

Sales pairs are designed to Yield Price Change for the same house,

while holding quality and size of each house constant…

Sales with longer intervals are given less weight.

Less weight might not fully adjust a rise from $60,000 to $1,500,000.

Heh, I know someone that sold 6 months ago and now can’t get back into a house in the Phoenix area. She sold right at the start of this mania and now has lost buying power. I am standing on the outside of the market looking in thinking if I have slim pickings at my family’s salary then the vast majority of others must be overextending themselves or they’re investors flush with cash. I have heard from a real estate agent that 70% of homes in the Phoenix area are being bought by investors.

These is one crazy speculative bubble driven by the Feds misguided policies. I hear all of my coworkers talking about the price of groceries. And the inflation stories in the news are becoming dime a dozen. I’m honestly scared of all this debt and what kind of future my daughter’s generation is gonna have. In my own little world I wish I could find a house to raise a family in. The younger generations are screwed. They need to drive investors out of the housing market. That’s where a huge chunk of demand is coming from.

You’ve echoed exactly my thoughts. First-time home buyer with genuine need of a house, pitted against 5% down-payment FOMOs and deep pocket market speculators, i.e. “investors”.

Yeah, if the economy hits an unforeseen speed bump which all this speculation makes more likely all the FOMO idiots losing their jobs and investors may race to sell. Lots of what ifs. And then they may just establish Mortgage Forbearance 2.0 anyway. I’m so tired of the generation in power thinking they have to head off every economic downturn w overkill amounts of stimulation. If you don’t go through the bad times you’ll never return to strong growth without govt support.

Thank the Fed and Treasury….Those bulk sales should have to be called back….2009 was the biggest heist of wealth in history of the world…..where is FASB 157-8…

The fed pigmen are blowing up the world…now I know why 99M folks will be left in 2027

Abomb, unfortunately inflation drives people to buy hard assets such as real state. If I had the money I would buy a piece of land or something like that to preserve that money.

The rich are buying rolexes, collectibles (including cars) and anything that will be worth something when money is destroyed by inflation. They can always sell those whenever the economy starts to rebound again. It’s a way to park your money and leave it there. (cash/banks is risky)

Rental property is better because it gives you income to help pay for property taxes if all hell breaks lose. But land you can grow food and even sell it or barter.(which is the smartest thing in case of hyperinflation)

So this trend may get worse I fear.

I heard there’s a Rolex shortage, also that collectable art is going for lots of $$$$,if true it’s just another sign that the rich are looking for ways to preserve their money. It’s what they do.

Watch what real rich are doing(with their money) . It tells you the story.

The truly wealthy have more money in the bank than they ever have. Don’t ever forget that. They own the banks.

Buying real estate right if inflation rises seems like a risky gamble for those getting in now. If the Fed must raise rates perhaps a big if that they’ll actually do it), the housing market could implode dye to unaffordability.

Investors will learn there lesson when renters become squatters or social unrest takes over and butns them to the ground also why isn’t pelosi and her husband in jail for insider trading oh I forgot their protected by sec

Please include some thoughts on the new Silicon Slopes of Utah (Lehi). The prices are jumping by leaps and bounds. It would appear that cities of Utah, along with Idaho and Nevada are leading the Great Western Expansion. Thanks!

Referring to the national chart (first chart):

1) The current spread between CS NHPI (red) and OERR (green) has

exceeded that maximum spread set back in 2006.

2) The OERR (green) keeps marching higher, independent of boom or bust.

Reminds me a bit of Japan back in the day.

Don’t know what broke it but they did manage to

break it slowly.

I’m curious. Can you provide more information? What did Japan slowly break?

https://en.wikipedia.org/wiki/Japanese_asset_price_bubble

I do not think it is possible to make comparisons with Japan, every crisis is dependent on different factors and it is what makes divination a very difficult art in economics where the best economists are always proven wrong.

There is a story about the Imperial Palace in Japan being assessed at a value equal to the value of the state of California. About 1990 the Japanese stock market bubble and housing bubble were ripe for a correction. Some people committed suicide over their losses.

That’s what I’m talking about

30 years ago my friend from Japan was telling me his home was worth over a million dollars. I was like you are full of that stuff. Well come to find out that was during the years where Japan real estate had gone through the roof. That all came crashing down. So I often think about telling my kids the value of the home.

30 years ago I remember flying a Japanese log buyer to look at one piece of clear Yellow Cedar. They called them temple logs and buyers would come over to Canada to purchase individual logs that they were interested in. At the same time (roughly :-), flew a J… diving prospector to check out a particular coloured sea urchin colony. The reproductive parts are considered delicacies. We also flew plane loads of spot prawns from the coast inlets to YVR airport for prawns to arrive in Japan still crawling. I was told a diner would select one particular prawn and pay $100-$200 dollars for it, but it had to be still alive. Picked up a load every day in time for a red eye west.

This excess was just before the RE collapse and stagnating economy…plus highest Govt debt per capita in the World.

What do we see in NA right now? Crazy RE prices. Crazy sales of toys and vehicles. Nutso increases in Govt and personal debt. A suspect economy. A Govt structure insisting all is well and normal.

I lived through an 18% mortgage renewal at age 28 and survived. It. Was. Not….a fun time. When I sold my house I broke even; one of the lucky ones. Tough times turned me into a no debt saver. If you have no debt it doesn’t matter much what inflation does, you just cut back a bit to make up for everything. Then, deflation kicks in. It happened…happens. Hold on tight. There has to be real jobs with decent incomes for a middle class foundation for society to function and offer opportunities. If there are only rich, and many others in decline, there will be trouble and change.

I think it was like most booms that people extrapolated the good times would go on forever. Japan was booming on an export economy and US got Fed up with the trade situation and yen was forced higher hurting exports and then the feedback loop started because the banks had too many asset backed loans that went sour. The pin might have been the Plaza Accords, but the problem was leveraging up too much during the good times.

What nobody is saying is that this increase in “value” is actually the largest tax hike ever. Name one other tax that’s increased 200-300% in the last 20 years, and they did it without even having to legislate the thing.

State governments can’t spend it fast enough, although they’re trying.

State governments are broke.

Thanks for bringing that up. Also, at some point all the mortgages in forbearance will have to pay their taxes. While some servicers may have done it once, they will not be doing it twice or thrice, because they are going deeper in the hole. It will be interesting to see the future of the mortgage servicing business going forward.

SC

It’s always that way.

Become an engineer!

Just to share with my fellow bubble watchers gawking at this insanity. Here’s a gem for you, apparently we will soon all be lining up like Thanksgiving shopping but instead of finding deals and paying less, lining up to pay more…what a way to go

Perhaps I am wrong on this but even I don’t remember things are this nutty back 06-07 at least not the lining up part..

“From KRON in California. “How far would you go to get the home of your dreams in the Bay Area? A local realtor camped out for days for his clients to make sure they got theirs. He started camping out three days before they went for sale. ‘I pulled out my lawn chair. I put it right in front,’ said realtor Jeremy Naval. ‘It sounds crazy. I feel like this is something you’d probably just see on HGTV or some random story, but it’s true. And at the end of the day, if there’s something that especially my clients want and there’s a certain way I can get it, I will do it but I wouldn’t be surprised if this starts happening more often.’”

“He wasn’t the only one camped out. Dozens of others were also on the sidewalk outside the sales office. There were 18 townhomes up for grabs, starting at $1.2 million. Now what really attracted clients to these condos is that they are set at a fixed rate meaning none of those bidding wars will take place here. ‘As soon as you walk in you tell them and then bam the price is right there you write a check for the deposit and you’re all done,’ Naval said.””

The over-financialized housing market’s version of a communist bread line.

For background Folks

UK = 8%

Everything is bigger in the USA!

Even housing bubbles.

Remember Reagan firing the Aircraft Controllers?

Prior, wage demands exploded, rising an order of magnitude never before seen during that era, except maybe baseball salaries. Interest rates peaked too, that August 1981.

I propose 1970s wage inflation is symmetrical to our recent eras financial assets.

This can only be proved by todays financial Ghost of Reagan, reversing his previous labour (labor) of love.

quack quack.

No politician is going to fix this. The invisible hand of the market will take care of it. No matter what the FED does, something will break at some point. Like, say, 15 Archegos blow ups in a couple days.

Congress passed and Clinton signed The Financial Services Modernization Act to make time-travel possible.

Honestly hoping for the triplet mutant virus to come to the US. Who knew a pandemic can make you richer? Why not have a new pandemic every month?

In moments of dark sarcasm I’ve joked that with markets the way they are, we should hope to have pandemics more often.

What’s more asinine than the biggest price boom in history during the worst jobs losses period in history is the fact that people actually believe in it like it’s based upon fundamentals.

Might as well keep rising forever.

If this bubble ever pops and we have another 2011-2012 trough, what’s to keep the institutional hedge fund buyers from gobbling up yet more housing stock? It feels like buying a home will eventually become impossible for the average American, either way.

For what it’s worth, in about 5 years I will have paid as much in property taxes, as I paid for my home. I already paid more in property taxes than I paid for my industrial land years ago. All government enjoys high valuations. Does nothing for the buy and hold crowd.

Marbles,

Did you just sent me a donation (check) with a note signed off by “Marbles.” Screen names and true names are hard to put together without further help. If yes, thank you!

Yup.

Wolf and I both called a top to the Bubble within a few days of each other, reaching our conclusions separately.

Absent hyperinflation before the end of summer I expect it to pop by the end of June.

How would a Fire that destroyed 10K Bay Area homes affect the Markets?

Something that started a little East of Orinda when the winds are gusting to 55 MPH…

Heck, if Elon dropped dead Tesla would crash and burn like the Hindenburg and he does not look healthy.

One man gone and POOF! goes the stock bubble.

When things are this unstable and volatile it doesn’t take much.

Why end of June? Is it because people will have to start paying rent/mortgage again?

When the time comes, they’ll just push that back again.

Also, the market can still go up 50 to 70% from here.

June? I triple cross my fingers hoping you will be right but I’ll likely be disappointed. Unlike the stock market, on the way down for RE could be a slow process especially if FED is bending backward to prevent that from happening. Plus timing the market is usually about as good as throwing a dart at the dartboard with your eyes blindfolded. It’s a fool’s errand. If some of the big names like Dalio and Jim Rogers can’t do it, that pretty much tells you everything you need to know about timing it.

I don’t think we’re getting hyperinflation but I keep hoping Biden will pass all of his huge spending packages and they continue the cushy unemployment to force inflation up beyond the Feds expectations.

The Mongolians and Genghis had technology on their side. Metal stirrups helped him have the most powerful cavalry in the world.

Being able to fight while mounted and riding was a game changer. This also led to the rise of Feudalism in Europe.

Bucky Fuller, a man I respected and read as a student of physics long ago has said that the invention of stirrups was one of man’s most important inventions. Not something that would come to mind for many people I’d bet, eh.

“No one dared question the horseman’s claim that he owned the land on which the horseman said the shepherd was trespassing. The horseman had his club with which to prove that he was the power structure of that locale; …” (page 67 ‘Critical Path’)

As Lisa_H has commented, we don’t own the land on which our home sits; the government does. Eighteen days until property taxes are due for me.

Wolf,

First off, great info as usual. Thank you! I don’t post but given my recent experience with the Bay Area market I just have to share it with you.

My wife and I are first time home buyers. We put an offer in Solano County. Our lender told us we are extremely strong buyers – we each make 6 figures, we have zero debt and can put down 20% if needed with still a good reserve.

We were putting an offer down for a house that was listed at $595K. This is a home that’s priced good for us. It’s something under our budget that we can pay off early. Our realtor advised that comps were around $560K so to he felt this was already over priced

They opened up viewing on Friday. Our schedule was Saturday and offers were due on Sunday night. The house was a 5. The neighborhood was a 9 (at least in our eyes). Walking through the home, it needed new floors, new windows a new roof, a new deck and new fences. This just based on our initial viewing. But given this was well below our budget and we would have money to fix the issues we offered $605K and waived our loan and appraisal contingencies. We were firm on the inspection contingency because of the age and condition we noticed.

We were told yesterday that this house had 9 offers and most of them were higher than oura and had better terms (I.e waived the inspection as well)

Long story short the house is now under contract and the “lucky” buyer offered $668K – $78k over listing with no contingencies on a house that needs repairs.

My wife and I are pausing our home search until more reason comes back to the market.

Jay,

Maybe you were lucky? Hindsight will tell.

I’m actually thankful it didn’t go through. We went against our better judgement and tried to dip our toe into a feeding frenzy.

I see some posts saying this will keep going up. Just going off anecdotal evidence here but I have hard time believing that first time home buyers like myself will put up with much more of this.

Most of my friends (millennials, good paying jobs ready for a home) are on the sidelines because their high paying jobs aren’t keeping up with price increases. If many of us are choosing to drop out of the market, where else is CA going to find buyers with good paying jobs to afford high valued homes? Even if the interest rates are record low, monthly payments are still high.

Its not like there are other states out there with a higher cost of living than CA whose buyers could prop up our market even more like how the Techsodus is doing to so many other states.

Back in 2003 we bought our first home in Southern California (Ventura County). Was so scared that the moment I bought the housing market was going to go south. Thankfully it didn’t go down immediately and rose higher in value. Then the market crashed hard and the house was at par. Several years later the market rebounded and I sold the home after one viewing for a nice gain. So I believe the market will tumble down from here. But one thing has held true for all time. Home values are on the rise

“But one thing has held true for all time. Home values are on the rise.”

Tell that to the people who bought in 2006 then watched as their house fell by 60% by 2011.

Jay,

I think you were lucky. I would not buy in Crazytown during massive bidding wars.

However, I have 2 co-workers who purchased in 2006 and their homes are now up 40% from the purchase price.

However, during the dark times of 2008-2014, their houses had bottomed at a -40% loss. It could happen again. Maybe this year or in 10 years. Nobody knows.

They bought for the long term and enjoyed their houses for 15 years now. One has paid off the house and will never have a mortgage or rent payment again.

A house is not an investment. It is a place to live for the long term. Don’t buy if you won’t enjoy living in it for at least 10 years. Forget the price if you can afford it. Inflation and market sanity have saved everyone over time.

And stop reading housing bubble blogs after you buy. It is too depressing.

Sorry for the mixed message. Buy a house for the long term that you can afford today with extra cash reserves to carry you through any down times. A house is to live in and enjoy, Overbidding against crazy people doesn’t bring enjoyment. Wait a few months for the insanity to subside. The price may be the same but the lack of insanity will be relaxing.

If you read Warren Buffet’s stuff you will learn he calculates what he thinks is fair price for an asset and makes one take it or leave it offer. Never, ever will he get into a bidding war.

Most great purchases are made when other people are not interested. In panics you basically can buy stuff at about half price. Our electric utility stock dividend got to 8% in 2009. You are lucky to find 4% now.

“fair price”

————————-

Buffet likens a fair price to “buying a dollar for 60 cents”

Jay,

You will get another crack at it, repairs completed, 6 months from now at $800,000 listing price.

“Walking through the home, it needed new floors, new windows a new roof, a new deck and new fences.”

Looks like you’re lucky to have lost!

If you had “won,” you would have ended up extremely disappointed in the future. You would find that the money you spend would buy twice the house in a better neighborhood. I don’t know about anybody else, but buying a crappy house now vs. an awesome later is a no-brainer. I want the nice house for the same price.

I know a guy who bought the crappy house at the high price back in 2005. By 2010 he was miserable and his marriage was on the rocks. Then the following year his neighbors sent the house into foreclosure on purpose after buying a gorgeous house in an upscale neighborhood for six figures less than he paid. They were stuck in a gritty working class neighborhood, paying a bloated mortgage. Not sure if they ever made it as I started working in a different area and he wasn’t the sales rep there so I never saw him again.

This story is coming to be so common. You’re situation sounds very common to mine as far as being a strong buyer but just wary of what’s going on. I mean I do have some FOMO but I’m not entirely sure what I’m missing out on…. potentially something I don’t want

This can continue indefinitely as long as [mortgage] interest rates stay low or go lower.

How can it continue indefinitely? Even if rates stay the same at some point prices exceed ability and/or willingness to pay.

Pretend that mortgage rates half every year for eternity, all else being equal. Prices would never go down in this case and the steady march upward would continue indefinitely.

If mortgage rates go to zero you still have to pay principal unless they start extending duration. $3.6 million still equals $10,000 per month plus tax, ins, maintenance.

Agree. If the rates keep going lower…otherwise the number of buyers will continue to disappear. If they go up then demand will have to drop…then what?

Is it a bubble or an indication of inflation.

If we allow for the roughly 23 percent of inflation since 2008 and assume the fed suffers a 15% inflation shock over the next two to three years before they finally panic and raise rates……if they do

We adjust prices upward 38% from 2008. Putting us about where 2008 pricing was in some markets……quite a bit short of the 2008 top in quite a few markets…….and higher in only a few select areas that are in big demand. If the dollar starts a slow descent due to deficit pressure brought on by the approaching SS and Medicare crisis along with continued payments deficits……housing prices might be……what they are……

Just remember…..no way Jerome and the magic palace can allow the dollar to deflate…..the debts are way to heavy a lift and getting worse all the time.

So he’ll pump and pump and pump aided of course by our other magical kingdom that wants to increase deficit spending on social issues from here.

I used to believe in bubbles but when the government thinks 1 plus 1 equals 10 we have no choice but to use their math in regard to our standards. The van is being driven by drunks and we are acting as if a stop sign matters.

I wonder if J. John Law Powell will stack our skulls in a giant pyramid.

Don’t worry, as soon as team blue eliminates the SALT deduction limit (in order to pass “social infrastructure stimmy), housing will be cheaper for the top 1% (Sarcasm).

Per CNBC:

The top 1% of earners would see 57% of the benefits of a SALT repeal, while the top 20% of earners would reap more than 96% of benefits, according to Tax Policy Center. Overall, only 9% of American households would see any benefit from a repeal of the SALT cap, per the analysis.

I don’t doubt that this will be a negotiating point for the top 10%.

I doubt they will lower the std deduction back to the way it was (now: 25K, formerly 13K for married filing jointly).

With interest rates being so low, it is a very nice house that would allow a deduction for 25K in taxes AND interest. Though as values increase, property taxes (except in CA with Prop 13) will keep pace in many states.

If you had a million dollar assessed house in a state with 4% property taxes, this deduction would be useful. ie 40K in property taxes.

SALT=State and Local Taxes. Property tax is just one of many state and local taxes.

$400k loan for 30 year on $500k house = $15,000 interest first year

Property Tax in Texas major cities = 2-3%. Take $500k house x 2.5% (avg) = $12,500 property tax.

Sales Tax in Texas major cities = 8.25%. Buy $100k of stuff, pay $8,250 in sales tax

$15,000+$12,500+$8250 = $35,750

There are more SALT deductions, such as vehicle registration, etc…but the example above shows you can easily break $24,000 standard deduction in Texas, on a $150k income level.

For a 500K home in CA with 20% down:

1) 400K loan. 12K in interest at 3%

2) Property taxes at 1.2% . 6K

3) State Income tax – 7K?? – 150K married income

total: 25K.

You would take the 25K std deduction and not itemize.

It really depends on your income and how much tax you pay.

Every year, your interest would decrease while the std deduction increases.

It would not be a huge benefit to itemize if SALT was eliminated in CA.

There is no bubble. First there was a $2 trillion Covid relief package passed just as vaccines were ramping, lockdowns ending and consumers primed to travel and spend. There is another (at least) trillion dollar “infrastructure” package coming, and Biden will push ANOTHER over trillion dollar package for free community college, pre-K childcare, whatnot.

So let’s call it potentially $5 trillion dollars being dumped into a $21 trillion dollar economy, $2 trillion already underway.

Next, the Covid unemployment benefits incentivizes lower-end workers to stay at home, so employers are starving for workers, wages are already being bid up (never mind the $15 minimum wages already being phased in California and elsewhere). On the business end semiconductor companies are announcing across the board price increases, shipping companies are raising prices, and so on.

Inflation is obviously already in the works, but the central bankers will still keep rates artificially low. Besides incentivizing debt (buy and just worry about the monthly payment!), it makes lots of loose linvestment capital ochase ever higher returns, like real estate.

So real estate will keep going up. Worse case it will plateu, but it won’t come down.

I am actualling thinking about selling my house in Cailfornia and buying near Austin…but prices there are not that much lower anymore. The realator we are working with showed us a nice $1M house that looked sort of interesting, was under contract less than 24 hours after it listed. Don’t know if it was an investor or buyer, but I am pretty sure they can sell it for more in 2, 4, or 8 years. That house will never see south of $1M ever again.

Completely obtuse and devoid of any economic understanding.

Anyone who thinks anything that is being done, is to the benefit of the average working person is about as naïve as anyone can possibly be. The powers that be are not working in your interests, they are simply fatting you up for culling.

It is an endless cycle. First you allow the working stiffs to think they are getting a piece of the pie, and then you take everything they have worked the last decade or more to build.

The really stupid ones will fall for the ponzie 2 or 3 times before they figure it out….

Move to Omaha ne neighbor just sold 3000 sq ft for 300k

I don’t always have the time to investigate all the data on this. I need a townhouse/condo eventually in Grand Rapids area. I feel think this is a bubble of some sort. What does everything think when the news states that this is NOT a bubble? Due to demographics, low supply, building of new homes (slow still), mortgage rates, strict lending standards..etc… I read that housing prices will continue to go UP. How? I live in the shabby state of Michigan and crappy houses in small towns like Mason, Michigan are going for 30k over asking price. Ridiculous. I’m not buying now. I lived in Toronto area for 8 years (dual citizen) before moving to GR.. Canada is messed up even more. Do I sign another lease? Continue to rent.. appears so.

Maybe we are not in a bubble in the U.S. Maybe we are just catching up wtih prices in other countries.

From what I have read and could be wrong, but compared to major cities in China, Hong Kong, Singapore, Europe (Germany, France, London, Belgium, Denmark, Norway, Canada…), U.S. housing is considered cheap?

Oh I think we are in a bubble alright. Housing bubbles are worse than stock bubbles because of leverage.

With stocks you are for the most part buying with your own savings. Real Estate is for the most part bought with someone elses money who is counting it as an asset.

last week in melbourne, Oz, median house selling price just over $1 million for 1st. quarter 2021.

Definition of a housing bubble, courtesy of Investopedia:

“A housing bubble, or real estate bubble, is a run-up in housing prices fueled by demand, speculation, and exuberant spending to the point of collapse.

Housing bubbles usually start with an increase in demand, in the face of limited supply, which takes a relatively extended period to replenish and increase. Speculators pour money into the market, further driving up demand.

At some point, demand decreases or stagnates at the same time supply increases, resulting in a sharp drop in prices—and the bubble bursts. “

RE is all local, all of the time. For example, there are places in the US cheap, and in Canada cheap…and the opposite.

Often, moving and starting over works because of luck in timing…pure and simple. Luck.

Advice time: If people are bailing out and moving on they have to pick a good fit. It’s pretty redneck around here and no one likes being told how they should live, (so we fit in just fine). But the Island where my brother lives? 50 miles away, it’s the opposite. Just 50 miles and it’s as different as night and day.

Barrons suggests that easy money policy is responsible for the run up in housing prices and that the fed will continue to give businesses and the wealthy easy access to cheap credit in hopes it eventually leads to higher employment. On the face of this seems a bit crazy.

Wouldn’t it make more sense (fiscally, economically, and socially) for the government to simply directly create jobs for a portion of the unemployed? This would be far more productive than giving away cheap money. Think of it as a repeat of the civilian conservation corps which are responsible for a lot of the parks, dams, dikes, etc., we see today.

There is a theory that most of our problems have been caused by the central bank setting interest rates too low for three decades which has caused excessive debt and we are now in a debt doom loop that can’t be escaped with the current system.

Our system seems to be getting more and more directed from DC which is certainly trying to over manage society in my opinion.

Amen. The problem with poverty today is not really lack of money, it’s lack of usefulness. Everyone needs to be useful, and every man wants to work. WPA/CCC made a lot of permanent and important things, and kept a lot of men and families SANE.

Men need to make things. If they can’t make things, they will break things.

During one of my business trips in 2007 I was heading west on I-70 toward Denver.

Scenic mountainous Colorado begins West of Denver,to the East there is a flatland covered with sparse brown bushes,an extension of Kansas if you prefer…

Off the I-70, before reaching Denver, I spotted 5-6 new developments,signs saying “Luxury Homes >$300K” which made me wonder “What kind of luxury people will buy those luxury homes in the middle of f… nowhere ???”

Next time I drove thru this area around 2012 they disappeared without a trace.Razed to the ground,copper wiring and brass fittings salvaged by the coyotes in old pickup trucks and the rest going straight to the landfill.

Poof !!l Gone with the wind !!!

Sic transit gloria of luxury homes ?

Lumber should go up in price at least 1000x for this meangless BS to stop.

I remember my first visit to Denver. I thought I was going to a mountain town. When I got there I felt like I was in Kansas – not exactly what I had hoped for. Worse, the downtown area was a dump. This was in the 90s. Not sure what it’s like now because I’ve never wanted to go back. I really don’t understand the allure.

Your example of houses being razed to the ground shows how worthless they can become. Houses are money pits the entire time a person owns them. Skip maintenance and repair and eventually the whole thing becomes part of the earth again.

“I really don’t understand the allure.”

The main theme of the iconic movie “Convoy” was about truckers hauling contraband Coors beer, which back then was not supposed to be sold in the East ☺☺☺

Mountains west of Denver are beautiful,I saw signs on I-70 “Elevation 14,000ft”…

Also I was impressed by the ultrafit bicyclists riding on the side of interstate as fast as the traffic,their carbon fiber, space-age-technology bikes probably costing more than 50% of old cars on I-70.

Yes,you’re right,uninhabited houses deteriorate quickly.I do not know why but it applies to log houses too.I believe that log houses are living beings,no matter how stupid it may sound.

Finding a lender for a log house is not easy. I knew somebody who tried to buy one once, then gave up.

Seems more like something made of the stacked carcasses of formally-living beings.

@SnotFroth

People who care about aesthetics and log house preservation dont leave logs exposed.They attach wire mesh (or thin wood planks before wire mesh was invented) and finish log house with a lyme plaster.Looks perfect and lasts >200-300 years.

Plaster protects log house from elements and still allows house to breathe.Frontal columns in colonial houses are plastered tree trunks.

Modern $500K chicken coops are wrapped in 100% waterproof Tyvek.Black mold spots start to appear underneath right after one signs on the dotted line ?

Try dusting a log house. Dust on every course. Plus, they are dark and drafty. The R value sucks as well.

If house prices rose 12% nationally then it would be interesting to get some estimate on potential home equity growth nationally. This new wealth will feed into inflation.

(125 million homes * 340,000 median home price) * (1.12 -1)= approximate increase in house based wealth= 5.1 trillion dollars for consumers to potentially spend.

So we really don’t need to send out checks to create inflation. Housing will do that all by itself!

(note:340K was from the single family home number Wolf posted. Meant only to be a ball-park number).

I just saw the chart today of financial assets/GDP spiking to extreme levels. It’s not a good sign. I guess you can say it’s just a product of Zirp and QE. Our financial assets have been blown sky high, which means future real returns are basically zero.

The wealthiest 10 percent own 45 percent of the real estate in America, per Fed data.

As illogical as it may seem, low interest rates makes the super wealthy rich quickly, while the bottom 90% do not gain much at all with ZIRP policy. Higher interest rates decreases inequality…yet the Fed sells low interest rates as helping the poor. J-Pow is the inequality wolf in sheep clothing…and now I read he is top contender to get re-elected in February 2022, sweet! (for the top 1%) Team red and Team Blue are actually team purple when it comes to making rich folks richer. Both love inflation and money printing as the sole answer to all of life’s challenges…

California rent control laws keep any upward swing in rents and it’s affect on CPI forever stifled. Only down swings will accurately be recorded. It actually becomes a viscous circle as CPI is the main determining factor in how much rent can be raised, but rents help drive CPI. CPI is a joke on so many levels.

“According to Bloomberg, nearly $47 billion in rent relief from the Biden Administration has been slow to materialize, forcing “mom-and-pop” landlords into financial hardship – or forced to sell to wealthy investors.”

“EVERYTHING IS PROCEEDING AS I HAVE FORESEEN…..EhEhEh!!!”

Evil Lord Darth Sidious – Revenge of the Sith

Nov 2022 it will pop.

1) Houses construction and demolition sites waste and debris are major climate change polluters.

2) Feb 2020 vs Feb 2021 RE report is another polluter.

3) In a normal Feb the RE market is dead. Who cares about RE in the

middle of the winter.

4) What Case Shiller report will tell us in Mar and Apr 2021, when SPX was half size in Mar 2020 and WTI was minus 40 in Apr 2020.

5) The current RE market is a roaring volcano. It might erupt any

minute now.

My friends in San Diego on un employment are not paying rent for last 1 year barring 25 percent of total rent

They have also applied for rental assistance which would pay partial amount to landlord.

Its gonna be interesting when this rent and mortgage forbearance stops.

Not sure whats the end game is

They must stay unemployed otherwise the Fed will have to taper

End game is to run economy into ground and then reset.

It is an unnerving game of extend and pretend.

That spanking new $1.9 trillion bill signed into law includes nearly $50 billion in assistance for renters and homeowners who are having trouble meeting their obligations. Extend and pretend, but don’t let this debt ridden, malinvested, and misallocated economy face its day of reckoning.

And like most government programs, the vast majority of that 50 billion will disappear in a labyrinth of bureaucratic graft and corruption. Just ask the victims of Katrina, how much of the billions allocated for relief they ever saw.

listings are starting to come back. 248 listings in San Joaquin County in the last 2 weeks. Many posted in the last 48 hours. Would be nice to see some graphs of listings per month by MLS for your listed cities.

Stock Market most spendid inflation bubble = $22.4 TRILLION

Home Equity most spendid inflation bubble = $1.3Trillion

Stock Markets inflation is the Fed’s way of creating maximum inequality, not housing inflation. House inflation is just a the icing on the cake for the top 10%.

J-Pow is a psychopath who is cold hearted, calculated, and agressively plots his path to ensure the wealthy are fiscally pleasured at all costs. If this continues for much longer, a lot of people will starve in third world countries, yet not even thinking about thinking about the morality of globalized inflation for a psychopath like J-Pow…

Per WP:

The market’s rise since then makes the increase in homeowners’ equity look negligible. From last year’s market bottom through mid-April of this year, stocks gained about $22.4 trillion in value, as measured by the Wilshire 5000 Total Market Index.