Smaller companies too: Boots-on-the-ground view of surging costs in the roofing manufacturing industry. The Fed will brush it off as “temporary,” but the inflationary mindset has set in.

By Wolf Richter for WOLF STREET.

Big companies, such as Procter & Gamble, have used their earnings calls to prepare investors, customers, and consumers for what is coming: Surging input costs are creating hefty margin pressures, and companies are confident they can regain their margins by passing on those surging costs by implementing large price increases. Smaller companies face the same scenario of surging input cost and margin pressures.

Todd Miller, President of Classic Metal Roofing Systems, which manufactures metal shingles in the US, sent me an email today where he goes into detail as to what his industry, and the broader home remodeling industry, is facing, in terms of surging costs, shipping issues, and supply constraints. This is Todd Miller, a long-time reader and supporter of Wolf Street:

“Our industry is dealing with supply chain shortages as well as rapidly increasing prices. While we have not had to go to this extreme yet on the types of specialized products we produce, I have seen the selling prices of “commodity-based” metal roofs increase by 30% over the last six months, with additional increases projected.

“We’re also seeing the industry-leading asphalt shingle market in a pickle. Prices are going up, manufacturers have distributors and contractors on allocation, and lead times of 30 weeks are being reported. We’re also seeing the industry cut back on product offerings.

“The end result is we have a very robust remodeling and construction market, with limited product availability and spiraling prices. Everyone is aware of the lumber issues, but we’re also hearing of major issues with windows, doors, and siding products.

“As a metal roofing manufacturer, here are some of the raw material increases we have experienced over the past six months:

- Unpainted aluminum: up 15%

- Unpainted galvanized steel: up 57%

- Coatings used on our products: up 10%

- Corrugated packaging: up 15% on average

- Lumber for packaging: up 34%

- Fasteners: up 5 to 8%.

“Typically, the metals and coatings make up about 85% of our product costs.

“And then we’re also dealing with escalating freight costs as well as difficulty in shipping internationally. Our customer in Japan is also experiencing a very robust market, but it can be 30+ days for us to get a container scheduled to take product to them.

“We do import polymer roofing underlayment from China and the big issue there has also been deliveries – getting containers to bring product to us.

“I suspect that some of the raw material prices will soften hopefully in late 2021 and early 2022. But increases in costs for labor and transportation will make it challenging for most manufacturers in our sector to drop prices – we will all be working to regain margin from the raw material increases.”

Miller’s last phrase translates into a common situation now facing manufacturers, where input prices have suddenly surged, squeezing the manufacturer’s margin. The manufacturer tries to catch up and raise selling prices. And even if some of the input prices, such as volatile commodity prices, drop again, manufacturers are unlikely to lower their selling prices because they’re still catching up with their input-cost increases and attempt to regain the margin they gave up as input costs suddenly surged.

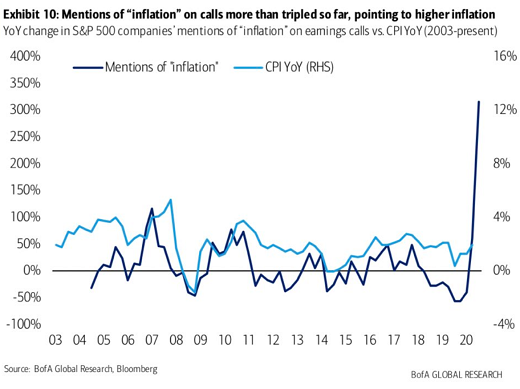

In terms of publicly traded companies, the number of mentions of “inflation” during earnings calls more than tripled year-over-year so far, “the biggest jump in our history since 2004,” according to BofA Global Research analysts on Monday, cited by CNBC’s Carl Quintanilla, who tweeted this chart from the BofA analysis:

In the past, the number of mentions of inflation “has led CPI by a quarter with 52% correlation and points to a robust rebound in inflation ahead,” the BofA analysts wrote in the same report, cited by MarketWatch. The “major drivers” of these mentions were the costs of raw materials, transportation, and labor.

Procter & Gamble CFO Andre Schulten said during the earnings call last week, “The commodity cost challenges we faced this year will obviously be larger next fiscal year. We will offset a portion of this impact with price increases.”

They’re looking at raising prices on their products “in the range of mid to high single-digits,” he said. “We are analyzing raw material and foreign exchange impacts in other categories and markets, and we are assessing the need for additional pricing moves.”

All companies are planning to pass on the surging input costs via price increases, or they have already done so, and they’re all adding to inflationary pressures.

John Hartung, CFO of Chipotle said during the earnings call, “We think everybody in the restaurant industry is going to have to pass those costs along to the customer. And we think we’re in a much, much better position to do that, than other companies out there.”

Whirlpool in its earnings call discussed raw material inflation, “particularly in steel and resin,” that “will negatively impact our business by about $1 billion.” It said that it had announced “price increases in various countries across the globe ranging from 5% to 12%.”

Kimberly-Clark during its earnings call explained how it is trying to keep up with “raw material inflation,” as input costs are rising fast and price increases and cost cutting lag.

“So, one way to think about the run-up in inflation that we have for the year is that within the year, we will cover about half of that with pricing,” CFO Maria Henry explained.

“And then when you add in the additional cost savings both in terms of our increased outlook on the FORCE program as well as additional tightening of the belt around discretionary items, you would get to cover a good portion of the inflation,” she said.

“In terms of input cost inflation, that is ramping in the first quarter and the second quarter. We expect that it will peak, and then moderate, and in some cases come down a bit in the second half,” she said.

Kimberly-Clark CEO Michael Hsu summed it up: “We are moving rapidly especially with selling price increases to offset commodity headwinds.”

These examples represent a large-scale movement. And it boils down to is this: Forget 2% inflation. There are hefty margin pressures on companies all around, and they’re now resorting to hefty price increases to offset surging input costs. And their customers – other companies and consumers – are paying those higher prices. The whole mindset has changed. An inflationary mindset has become established in no time, and there will be a massive overshoot of inflation that the Fed will attempt to brush off as temporary.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Inflation, my biggest nightmare…

so sorry NO INFLATION(govt made up word)

just fiat DEVALUATION(central bankster real meaning)

ie LOSS OF VALUE

fiat collapse when people lose TRUST IN CURRENCY

The right way to think of it. Inflation isn’t the value of things going up, it’s the value of currency going down. The lower the value of dollars, the more of them it takes to buy the same stuff.

Joe S./Fin-check. TANSTAAFL.

may we all find a better day.

OutWest..

I’m guessing you’re not J Powell or a Fed Governor.

I’m angry. I’m completely despondent. I’ve missed this entire bubble market and have been sitting in cash. My entire life savings is being systematically destroyed and I have no idea what to do with my money. I’m ready to end my life if I end up being destroyed by this, but not before getting some justice against the criminals that have done this to me and other prudent people that “followed the rules”. There’s nothing to look forward to in this country. I can barely be bothered to work anymore. What for?

Chill out, it’s just money.

You’re joking right? It’s your labor, being stolen. Enslaved while under the mass delusion that you have any chance at having a secure future let alone get ahead. That’s an incredibly stupid response. The fed is literally robbing you at gunpoint and you’re like “meh, go ahead, it’s only money”

you can still buy physical gold with your savings. $2 million at today’s prices fits in a shoe box. and think of it this way – it’s the last thing the fed wants you to do with your money. so you’d be sticking it to them. you’ll be fine.

p. s. the fed is not literally robbing you at gunpoint. you mean figuratively.

Just like seasons come and go so there are cycles in human affairs and history.

There is not much you can do, early decades at the beginning of each century aren’t very propitious to human happiness. Unless you can fast forward to 2060 I suggest you take it easy and look at the bright side, things can be worse, they probably will very soon.

that’s kind of the point… that’s why the fed is here. i’m in my 20s I know for a fact that you aren’t going to pay for most of this in the end. It’s my generation that will be that one’s paying for it. You’ve worked all your life, your blood, sweat and tears for the labor and hours you’ve put in are now being slowly slipped away from you. It’s like the Fed, smiling at you while you pass away slowly…

we can all learn that nothing in life is surely a guarantee besides death. So get some sun while you still can, because this is just the beginning. It’ll take years if not decades to reverse the damages.

Put it in physical gold and silver ASAP. You may be better off there than many other places. Do the math. It’s the antithesis to inflations.

He is replying to you ‘ending your life’. What do you think a fire, cop or medic would say: ‘Ya do it’?

There are millionaires terminal right now, for real, not just whining, who would give every dollar for another month.

The good news: yr abrupt reply to the right advice is a pretty good indication u are exaggerating.

I did the same thing. I sat a huge chunk in cash thinking that the market would correct, but now we have all this. I still think the market could correct a bunch, but yeah, that’s the world we live in. Easternbunny is right, money ain’t shit now and sometimes you lose hard by no fault of your own other than not knowing the future.

Your choice is to risk it all in their game or to not play it. If financial security is your goal because you’re afraid of discomfort and death, then get over your fear of discomfort and death and you will have won at your own game.

And you probably aren’t homeless or in jail…..I’ve experienced both. Yeah, I did get suicidal thoughts, but like Nietzsche says, “The thought of suicide gets many good men through many bad nights”. Just don’t tell a “medical professional” any of that or you’ll be sucked into another bad place (a money making system)….there isn’t much around anymore that hasn’t been “entrepreneurized”…or “corporated”……..which I find sick as hell…..actually I’m as mad at this sick “chase money/consume” culture as you are at the Fed. Growth for growth’s sake is the ideology of a cancer cell.

Wolfstreet is free…….good article and thanks.

You could easily still park your cash in dividend paying ETFs/stocks/muni bonds. It’s inflation and the world isn’t ending. Relax….as they always say “diversify” Holding all cash is essentially having all your eggs in one basket and you’ll never benefit from compounding interest. You know as well as i do that there’s no such thing as a free lunch. Hoarding cash is a sign of fear.

I understand the whole idea of hoarding cash and wait for a crash, but stagnant cash doing nothing out of fear is just as bad.

I’ve known so many people over the past 20 years just hoarding cash, waiting for the end of times. It just sits in their savings account stagnant because they’re scared to do anything with it.

“A broken clock is right twice a day”

Incorrect observations.

Money has dual purpose – as a store of value and as a medium of commerce.

If someone wants to store the returns of their hard work, it shouldn’t be called ‘hoarding’. They shouldn’t be called ‘broken clocks’. They shouldn’t be labeled as ‘scared’.

In fact, the Fed should be called the ‘robber’ and its policies should be called ‘robbery’.

but those two functions work at cross-purposes and create the rock and hard place the central bank finds itself between. the store of value purpose is leaving money. it’s not coming back.

hmmmm… if only there were some separate asset, easily identifiable, that was infinitely durable, impossible to artificially create and highly valued the world over and already held by governments and central banks that could fulfill, not the medium of exchange function, but just the store of value function…

something ordinary people could buy in even small amounts to protect their wealth and fruits of their hard work.

if only…

oh wait. its called gold.

It’s very telling that what used to be called “saving”is now called “hoarding”.

I’m wondering what the impact is of the anxiety that central banks are causing with all this. You usually hear only one side of the story (“gains” in stocks, crypto, real estate etc). But if the Fed prints $4T, these interest free, being debased as we speak $4T have to be held by SOMEBODY, directly or indirectly, and these people are losing out big. It’s all a big wealth transfer.

This comment is primarily for rob.

But also in reply to yushan, bungee and Nl.

Rob, friend , I frankly feel for your pain and understand your disillusionment with what’s going on in this “ Once” a country of opportunity and freedom.

That being said, I urge you to look for a good financial advisor, don’t lose hope in human nature.

There are a lot of people who can advise you on what course of action you should plan depending on your circumstances, just be sure to ask at the outset how much their service might cost you.

Good luck.

Yu Shan ,

I agree with you totally as to how saving for a rainy day has become synonymous with hoarding in the eyes of people with limited horizons.

It is frankly appalling to see that prudence in managing your life affairs financially is looked at with such low esteem!!

Wether individuals or nations, consuming less than what you produce is a mark of maturity and strength, alas with the scum that is currently dishing out unbelievable destructive policies (if you can call them policies ), there is only one way this will end, and it is NOT a happy one.

I am disheartened by the turn of events in the US, there is seemingly NO plan post disaster.

Just throwing money into a pit and burning it is not helpful to reconstruct this country.

In regards to this article, I am afraid that the clamor to join the construction fray ( I mean residential construction) , is the last thing any creature with s half a brain should be doing now.

You will be competing with large construction projects for materials and Labour! In an environment of rising iron ore prices is totally unjustifiable,

Current iron ore prices are hovering around $190 per ton, even the Chinese steel manufacturers were screaming bloody murder from July 2020!

With Brazil’s production of steel out of action and Australia, Russia and SA the main producers having a great run, it is NOT advisable to embark on any kind of building projects unless you’re willing to compete with more resourceful Parties.

So there you have it ! If you can’t build a house, maybe put some of your money into the BHP, RIO TINTO’s of this world and ride the resources boom for the next three to six months !!!

The other issue I’d like to take up here is the lack of local industries that could have fulfilled the role of the “ dependable Chinese producers “!

If we had preserved any semblance of skills and training in the real world ( carpentry… etc..) instead of teaching the kids to sing and dance their way to financial freedom we wouldn’t arrive at this juncture to begin with.

We are letting amazon, google, and facecrap dictate the policies that should run this country, and that is a great fallacy.

People need to resume work, and life.

The government should facilitate that.. asap.

Jack,

You complain about problems that ARE government facilitated and yet you advocate for more.

1. The Fed (private entity) was facilitated by the government. Companies no longer have to compete for capital – your hard earned money. Fed just skims everyone’s wallets and provides cheap capital. Result? Everyone is forced to chase yields. Houses out of reach for median income earners. Stocks of companies that are losing billions are rocketing. Loss of confidence in dollars.

2. Education is largely facilitated by the government. Lack of teaching in real life skills and emphasis on dancing & music – all because of it. Public schools (monopolies btw) are not filled with doers but with teachers that lean towards fine arts.

We can do fine without the government facilitating, thank you.

Nacho Libre

“People need to resume work, and life.

The government should facilitate that.. asap.”

This is what you’ve missed reading ( or understanding) from my comment above.

I think it’s self explanatory, the stupid measures to lock down the whole Economy and the country is one of the most destructive policies ever inflicted on the population of this planet.

On any country’s level, restrictions on international travel would’ve sufficed to eliminate most issues ( if there was any).

The rush to Lerch from one policy to the next regarding “health advice “ has been (and still is ) one of the most ridiculous aspect of the whole shambolic approach to in the last 13 months.

So, NO. I am Not advocating for more government facilitation of anything other than :

Reversing the huge F&@)(Up that they meted out to the thousands and thousands of businesses and individuals that were forced to close and rely on the government to get by.

Thank You

Jack,

agreed but not gonna happen. after watching this theater go on this past year it is clear this is intentional.

thank you for mentioning the elephant in the room.

Whether you have made a mistake holding cash is hard to say. Asset prices at these levels probably are not sustainable. Probably going to be a blow off top and then asset crash. Not beyond possibility that asset prices go right back to 2009 lows as real economy is more debt encumbered and demographic and political situation is worst.

Yup. And they battle inflation with interest rates. Rising rates = falling RE prices. In a few years it should be a good time to buy a home.

In 1969 my Father in Law bought bought 2 acres with a small house, a cabin, and a shack on it. His mother in law lived in the house, the drunk brother in law lived in the cabin, and some poor old timers lived in the shack for cheap rent. It carried itself for taxes and insurance. The night he closed the sale he was having a brew in the local Legion and heard the seller bragging about taking the ‘new to town’ sucker for 7K. He sat on it for 20 years or so and sold it for a huge profit. Now, after another 20 years, it has view condos on it and the property is worth millions.

RE appreciated much more than gold over the same time frame. Just an observation. I’ve been reading about how gold is going to 5 K anytime now, for what? the last 10 years? Meanwhile………

Sure, buying something you cannot afford at the top of the market and on credit is not wise. But if you have cash, there will be some good buys and people will be glad to unload their mistakes. Buyers can offer a fair price and make a win win out of a mess.

Paulo: You can get lucky with real estate, but its location location location. If your FIL had bought 7000 worth of gold in 1969 it would be worth about $350k now. It it would require no maintenance, taxes, insurance, etc.

Paulo,

RE appreciated much more than gold over the same time frame. Just an observation. I’ve been reading about how gold is going to 5 K anytime now, for what? the last 10 years?

all real estate is different. all gold is the same. gold holders are never bag holders. real estate is an investment. gold is savings.

even though this is an investment blog, many here are obviously simple savers. it is not fair to tell young people with only meager savings, or old people on a fixed income or a nest egg to buy real estate. to go invest in an orchard or farmland. it is ridiculous.

Gold however is perfect for them, young people can hold it for a very long time and old people can sell small amounts as needed. safety is becoming more and more attractive. the price of gold doesn’t matter. we aren’t waiting for 5K. we are expecting the market to break a la 1933, 1971 (but this time seems bigger…)

Gold, silver or Bitcoin and if you dare play the stock market right now. It will go higher since Biden will be putting trillions into the economy. I know the stock market can go only so high but might as well play it for now. Live for the moment. RF

Lets simplify everything

The Fed and our dear leaders know they can’t pay for all these benefits that they have promised by just raising taxes. So their only recourse is to print money. So they are stealing money from the savers and the people who have been “following the rules” . The little old widow with $300,000 savings in the bank are the target for asset confiscation. Also the Blue collar workers who’s entire wages are reported to the government is having their wages confiscated. If they ask for a wage increase then their jobs get shipped overseas.

This above scenerio is forcing everyone into the casino with housing prices and the stock market going off the rails. When all the lemmings are fully into the casino then their will be no more greater fools and the ponzi game and casino will collapse and all the late comers will be wiped out. This is what is going to happen. You can put this one in the bank.

I’m watching all this happen from the sidelines. I’m not playing in the casino.

Correction

I would change “Blue Collar Workers” to “Middle Class” workers which include WFH workers and other service jobs which can be outsourced overseas.

30 years ago the S&P 500 was at $750. Today it is over $4000. It has grown five times and paid dividends.

I saw an interview w/that Dr. Doom guy who predicted the RE Crash in GFC. He said something to the effect of:

“Yes, I lose some $ to inflation, but I don’t risk losing 50% of my life savings in a single day.”

Nobody is forcing anybody to go into a casino.

If you want to gamble, fine. But either admit you’ve got a gambling problem or FOMO.

I get it. Real wages have been flat for my entire 52 yrs on earth. I’m tired of the wealthy/corps screwing over everybody else in this country.

But panicking isn’t going to help……

“It just sits in their savings account stagnant because they’re scared to do anything with it. ”

In previous decades the financial press constantly moaned about American savings rate was too low and we should be more like those thrifty Japanese who saved money for a rainy day and lived modestly.

Also in past decades local banks made local loans based on funds that local people had deposited in savings accounts. At least that is what we were told.

That model has been replaced. Now local banks are just salesmen who sign up suckers then sell the loans to the big banks . Local people are now supposed to send all their savings to the Wall St parasites so they can centrally control all financial decisions.

As we can all see from the ongoing financial crisis, those Wall St parasites have completely failed at their job of managing the financial system. I would sooner light cigars with my modest savings than send a nickel to the Wall St parasites.

Hear hear. I know that sitting in cash it risky of itself, but the last time I jumped into the market with both feet (2000), I got slaughtered.

Never again. The whole game is to force the “retail” investor into the market and then get out the shears. Not this time. I have some assets that are not cash but I wouldn’t put a nickel into this bullsh*t market for any inducement.

I recognize my cash is losing value. But not half in a matter of days which is what is coming to those “invested” in stocks.

Dump it into AT&T boomer stock for the dividends. F it, since I can’t buy a house (I get overbidden by 5% down-payment FOMOs), I might as well do it myself

There going bankrupt hear of starling look it up

If you mean StarLink, you’re wrong, they’re not in the business of satellite phone service.

That’s like saying Ford is going bankrupt because of Tesla…

I’m with you, Bob. Same story. I have to remind myself that at least I’m not like the guy I just passed on the sidewalk today, begging for money. It’s ugly out there.

Bob

Read this book “When Money Dies'” . The people in Germany in 1921 went through the same things we are going through now. Total chaos. Assassinations, civil unrest, shortages, inflation, currency devaluation, wage stagnation, starvation, Just when they though things could not get any worse they did. We may look back on events of today as “The good times” .

Let’s put it in perspective.

These economic/social cycles do ebb and flow throughout history. It is part of the natural order that humans, for all their hubris, are not exempt.

Nothing goes on forever– same with human affairs. Regression to mean is a law and the pendulum always swings back.

Americans lived through miserable stagflation of 1970s-early 1980s and witnessed high price inflation for a number of years (even reaching a high of 13.5% in 1980).

Many of them then must have had the angst and anger that we are starting to see today.

Outcome of 1970s bout of stagflation– history tells us we that later in 1980s the economy rebounded and inflation was tamed (thanks to Mr Volker).

@Heinz: We don’t have wage inflation like we did back in the early 1980’s. That kept up with price inflation. We also don’t have Volker to fall back on. We have thieves in the FED instead.

They also had some really perverted and demented sexual fixations and general degeneracy and moral decay like today.

There is a book called “Voluptuous Panic, The Erotic World of Weimar Berlin,” that can be found as a PDF online. It has wonderful art from the era and recalls the social climate of hyperinflation.

Yep. VERY VERY UGLY.

I’m in a 500 sq ft low income (50% of local median) hotel style 3 story over 62 complex with indoor outdoor carpet, cheap linoleum, plastic baseboards, paper veneer cabinets, zero “amenities”, unless you want to count the community garden, and a small general purpose hall, along with 250 other apts that have people like me who are grateful as hell to be here.

In fact, make that I’m happy as hell.

People don’t “need” much, especially when they are older. I’m glad I “wasted” my youth having TONS of fun and not worrying about retirement in some damned gated golf community.

But there were MANY little factories making all sorts of things for minimum to a bit more wage back then. All rendered obsolete or eaten up by corporations now. I was even able to live in a van unhassled for 4 years to be able to make 527 skydives, and had lots of bikes. Like I said it was total fun and we were lucky.

Kids today are totally screwed and ought to vote some really vicious net wealth taxes on the top 1% 0.1% 0.01% etc.

See Wolf’s last article on wage and net wealth class warfare scores at present.

Research ALL the Nomad Capitalist videos on YouTube, develop a plan then act on it. People complain because they are to lazy plan and act. DO IT.

Truth! Thanks for some realism P.

While it is always easy to ”blame” some body or some entity or some thing, the fact is that no one can actually control what happens all the time, even JPOO, or whatever/whoever.

So, IMHO, the way to deal with the current inflationary situation is the same way one MUST prepare to deal with every situation:

Control YOUR behaviour/reaction(s)…

Planning, Preparing, studying the realities — as opposed to the constant bullstuff coming from all sides that is really noting more than propaganda.

ETC.

Talking to a neighbor on my bike ride around the hood in the saintly part of tpa bay area yesterday, he said they had just bought a townhome to ”downsize” to as their last child flew the nest, and listed and sold their house a day later in the active local market.

Also saw three new homes, larger homes built to replace 700 SF cottages, that appear to be waiting for roofing and fenestrations, in other words, fully structurally blocked/framed and nothing happening…

Appears to be a healthy housing market here, at the moment, but will almost certainly crash sooner or later EXACTLY as has been the case for my many years.

Cycles folks, cycles!

I don’t think the replies you got so far are helpful. If you are 100% in cash, you don’t want to dump your cash into anything. What if there’s a crash and you put all your cash into risk assets right at the top of the bubble? That would only make the situation worse.

Instead, what I would do is listen to my emotions. If I invest 5% of my portfolio in some asset, how would I feel if the price doubles tomorrow and how would I feel if the price is cut in half tomorrow?

If the price doubles and I feel regret for not investing more, I invested too little. If the price is cut in half and I feel regret for investing so much, I invested too much. If the price is cut in half and I feel happy for the opportunity to buy more, I invested the right amount.

I would start by investing $100 (or even as little as $10) in something tomorrow. That way, if I make a mistake, it’s just a small amount, but at least I got started and I can start observing how I feel about the investment.

I don’t think being mostly in cash is necessarily stupid. One thing that I feel is very likely to happen is that in the next 5 or 10 years, some asset will unexpectedly drop by 50%, 75%, or 90% to a level no one thought possible (or plausible). Waiting patiently for that rare opportunity may end up being the best strategy of all.

Cash is an underappreciated asset imo. People focus on the zero yield, but ignore the option value. A few years down the line you may be able to buy the S&P500 at -50% or even -80% of what it is now. You’ll be happy you had cash.

People always suffer from recency bias. Yes, cash was thrash in the past decade. The past decade was also the longest and strongest bullmarket in history (i.e. not the norm). And we have seen -50% drops in the stockmarket TWICE in the past 20 years, against an arguably much better economic backdrop than we have now. So a 50%-80% drop is not at all beyond the realm of possibilities.

So I’m mostly in cash myself, combined with ~15% in gold as a tail-hedge.

Yu

Problem is , Nobody trust the current mob in charge of the printers!

and since that is the issue, what guarantees do you have if we’re talking “ sovereign risk elements “?

The whole premise of the current financial system’s foundation is the “capability of the US to honor its debt”

The US was bankrupt in its previous history, the likelihood that will happen is increasing dramatically as fundamental reason for faith in its leaders is dissipating fast.

There are no political leaders that give certainty to the masses, and promote reason!

The ebb and flow of power is hard to control once you’ve demonstrated carelessness in abundance towards the weak and needy.

The chance of That ( certainty), my friend is being diminished substantially by the rogue culprits who don’t care what the average citizens face.

The famines and wars are by products of incompetence of the ruling class in every twist and turn of history books.

So, where do we go from here?

I’ve read a statement sometimes ago , a statement that we cannot preclude from our solutions to this problem,

It goes …

( .., Revolt or Hunger!)

The dam will break one day, the hope is that you’re not on the other side of the dam.

Preach!

When times are tough: cash is king!

@Orthodox Investor, that’s good advice.

Wasn’t last March a great buying opportunity? The market dropped about 35% in six weeks with many really good companies dropping even more – that was the time to invest for growth.

Instead of keeping everything in cash consider an indexed annuity with no caps and no fees. These annuities will allow you to earn a decent rate of return when the market goes up, but suffer none of the losses when the market goes down.

Bob

I disagree with a lot of the posts and advice on this site about “diversification” and getting your feet wet in the casino. This is the same BS I hear on CNBC and the shills like Rick Edelman, Jim Cramer, and Lawrence Yun. When things go down like they did in 1929 to 1933 EVERYTHING GOES DOWN!!!

And don’t believe that things will necessarily get better. They could get worse. Much worse. I hope not.

I was frustrated just like you are. At my stage in life I don’t have the time to recover from a bad investing timing error. I’m suppose to be retired but am still working way beyond the number of hours I had planned to at this stage.

After thinking it over for a while I went to my credit union and bought a ladder of 1 year CDs yielding less than 1%. The rep there told me to ride out these economic times until more clarity emerges. Take a 3 to 4% loss every year against inflation and plan to come back another day. You can always save an equal amount that is being lost by inflation to keep the purchasing power of the principal remains intact.

I keep finding it strange hat there is no massive public outcry over the immorality of all this. Savings are the fruits of hard labour and sacrifice.

I also find it disgusting how so called experts in the mass media keep parroting the line that inflation is a good thing and that we should have more of it. Although some of these people are genuinely stupid, I think most of them are not, so they must be evil.

Nope

Savings are the result of being paid too much.

You forget that capitalism is a uniform race to the bottom with 1% having 99% of the wealth.

Everyone else gets subsistence only.

YuShan

They are both stupid and dangerous. Not necessarily evil.

In the view of most people, “savings” is holding some stocks, not sitting 100% in CDs, bonds, etc. Therefore, the ordinary person with something to invest has done OK in this environment. They have no reason to riot.

Anybody holding 100% of their worth in cash or any other asset is speculating. They have no justifiable reason to cry when things don’t go their way. It is NOT risky to put 20% of a person’s net worth into the SPY, with the goal of matching inflation for the total portfolio.

That said, I agree with the sentiment. The Fed has no reason to suppress interest rates for decades, causing massive debt creation, asset inflation, welfare dependency, and government bailouts.

You think the leftist fake news media would allow it? They’re all just pushing the same narrative.

Nothing is more “lefty” (like a dirty stinky tree hugging socialist hippie) than a giant transnational corporation like NBC.

And NBC is owned by another massive, transnational corporation General Electric.

GE has a horrible record of civil, political + criminal behavior:

-Own or are responsible for 78 SuperFund sites

-Released radioactive material on purpose in Richland, WA

-Conducted experiments on hundreds of US citizens

-Price fixing; Defense contract fraud; Consumer fraud

-$200M settlement in ’98 for polluting Housatonic River.

-War profiteering; Weapons manufacturing

So yeah….all of that is “LEFTIST”?!

The MSM is all owned by massive corporations.

No massive corporation is “Leftist”. That’s ridiculous.

nodecentrepublicansleft,

You forgot the billionaires that own much of the MSN.

NBC hasn’t been owned by GE since 2006. They’re owned by Comcast niw, but they’re just as bad as GE ever was.

Very well written nodecent-

I’d just like to add a corporation is a huge dictatorship (bigger than most nation states) that through lobbyists and years of law writing/buying have firmly inserted themselves under the protections and benefits of what was once supposed to be OUR attempt at democracy. Lincoln described them as “enthroned” and warned they would “put all the wealth in few hands and the Republic would be destroyed”.

It’s only strange until you realize there are more improvident people than there are prudent. In a democracy, this is what happens.

The Federal Reserve is the enemy of the citizenry … and it will come to full view with this planned inflation.

Inflation is a TAX, and what we have here is an unelected body laying a TAXATION on the people of this country. The PEOPLE have no representation on the Fed. So we have an arrangement of Taxation without Representation.

Congress has the power to tax, and they must answer to the voters.

Who does the Fed answer to? Not the People.

They answer to the fat cats in Congress, who really don’t give a hoot about the average Joe.

Hi Bob,

It sounds like you are hitting rock bottom in this area, mentally and emotionally. I wish you didn’t have to go through this.

I too wish I had taken a different path. I could have been better off than I am right now.

It’s true that we’re somewhat at the mercy of the system and the people who manipulate it, but I believe you and I also bear some responsibility.

Who have we listened to? Have we listened only to people who talk about staying away from the stock market and sitting on a pile of cash? People who have a completely negative view of the economy or who want us to buy gold from them?

The path I’ve chosen is to get a healthy dose of information from people like Wolf Richter, but to also learn from people who practice value investing. In other words, looking for opportunities to put cash to work for the long term.

There’s no safe place for your money, but you can do more with it than let it sit.

I have been watching Youtube videos by Joseph Carlson and Sven Carlin. My experience is they have integrity and I use them to balance out my view of what is happening in the economy.

You might want to avoid value investing for a while;

On CNBC Squauk Box this morning the guest was saying that things were great as long as the Fed can continue the easy money policies, wages can be kept down and profits from Wall Street and high tech companies can continue on their merry path upward. The biggest threat was not inflation but the reaction of the Fed to the inflation and the possible increase in wages across the board which would lead to and increase interest rates.

The top 1% want it all. They want your soul.

Yep. Abolish the rich. Tax them out of existence.

It’s not just that they take control of our government with their money, turn it against us, rig it to impoverish and steal our wages for them selves. They also ruin our neighborhoods and drive us out.

Even better, Eat The Rich!

It solves two problems at once.

Island natives during the Age of Exploration referred to sailors as “long pig”. So I guess the rich would taste like pork…..some of it maybe too fatty for some.

And vegetarians could fertilize their soybeans with the ground up by products.

Interesting…inflation is “OK”, but wage inflation is not OK? So lets keep those wages down so profits will be UP. Beautiful stuff, and they said this with a straight face?

Anthony A.

Yep, heard it with my own ears on CNBC this morning. Wage inflation will trigger a move by the Fed. The hosts all nodded their heads in agreement, both the lib and the conservative. .

Bob,

I lot of people are in the same boat as you. We are suppose to be retired yet have to continue to work just to make ends meet. Working upwards of 18 hours a day 6 to 7 days a week, making about $10/hour after expenses. Then we have to listen to these scumbags like J Powel say that the biggest problem we have is the possibility of wage inflation. And if we get that wage inflation then companies will just shift their jobs overseas to third and forth world countries. We were suppose to have 5 income streams in retirement. Now 2 of them are yielding zero. 3 left. Now we had to quit working temporarily from pure exhaustion. So we’re down to 2 income streams. Fed annuity and SSA. Just pays our basic expenses.

Everything in life is about perspective. Just heard a discussion from Dubai of international money managers. One person thinks deflation is coming, inevitable in fact. His reasoning is that all the cash in the world is evidence of rising incomes and no/low demand.

If he is right, you are simply making too much money, so much money you have nothing else you need. So maybe you need to change your perspective, you may be doing great, but don’t know it.

His best investment advice was buy a home to live in and pay it off first before you look to invest elsewhere.

“His best investment advice was buy a home to live in and pay it off first before you look to invest elsewhere.”

Which is the dumbest advice a person could ever listen to. Houses are the most overpriced they’ve ever been, and will fall 80%+ in some areas.

I think the advice was meant on a global basis, in which case, I would agree with him. I wouldn’t touch real estate in the US near any major “hot” market. But the no debt mantra was the most interesting part to me coming from a money manager. He is the only one I have ever heard say, pay off your home first, then come see me.

Bob, I am sorry your are feeling such anguish. But I am very glad you posted because I am in a similar situation and it has been wonderful to see the wisdom (for the most part) of Wolf’s readers in response.

I am saving this thread.

Thank you Wolf for creating this space.

“When The Time Comes To Buy, You Won’t Want To” – Walter Deemer.

I solved that problem early last year by setting decision points. I divided my cash into 4 “pots”

When the stock market fell 10% I put in 25% of my cash, when it fell the next 10% I put in another 25%.

I stuck with that plan and was part way through the third increment when the market started flying back up.

So I still have cash, but I view that as diversification.

Now the marketis so overvalued that in the next drop, I’ll divide my cash again, but I’ll wait until a 20% drop before I invest my first “pot”.

Setting up a rule-based approach like this helps you overcome the fear.

Hey Bob, I’m about 30% in cash. I understand somewhat how you feel because I’ve been saving to buy a house in my home state, which is getting more expensive by the month. And as I’m working hard to save cash, Uncle Sam is diminishing its value while rewarding the irresponsible ones.

Take heart, though. I believe this insanity will end simply because it is not sustainable. I don’t know when but reality always returns and when it does, those who were playing games start to get the short end of the stick and those with discipline to save start to see opportunities for buying low. I’m keeping my cash in 0.5% high yield savings (pitiful, but not 0%) and expect to eventually get that house I want after prices crash back to earth.

In any case, you are valuable and I appreciate you sharing. You’re not alone. Stay the course.

Bob, sorry to hear your anguish….I don’t know your circumstances–age, skills, relationship status—but have you considered leaving the country? Keeping in mind that much of the world is mired in neoliberal circles of hell, you might find somewhere with both lower cost and better style of living…where your money might actually go further….if you’re being forced to run faster on the treadmill and you don’t control the power, sometimes all you can do is hop off. Everyone’s situation is different, but leaving (under somewhat unexpected circumstances) was the best thing I ever did.

Portugal

Like Spain notorious for real estate fraud.

So don’t buy real estate

Misery loves company, Bob, and I’m in your club. I did as I was raised: worked hard, respectfully and responsibly; lived below my means; avoided debt; sacrificed pleasure today for a better tomorrow. I have a serious health condition on the horizon and a dependent parent, and I was hoping to muddle us through with my modest savings and very basic living.

To realize all of that will quickly evaporate is disheartening, to put it mildly.

This can’t be laughed off by saying “it’s only money”, offering a pat on the head and advice of going out for a walk in the sunshine. This is and will be devastating to many of us.

Oh for Crissakes!! Look around the world or at the homeless near you. Poor ole Bob has roof over his head, power, a computer, some cash that SOO sadly has not compounded (neither has mine, my only ‘asset’) He also has time to comment although I’m not sure how buddy who is working two shifts of 8 hours and then 2 more hours can possibly have the time to agree with him.

I can lament the Fed as well and many mornings I lament selling our house in 2014 that has gone up 500K.

Then I tell myself to STFU and count my blessings.

I don’t think the crux of Bob’s complaint – or mine – was lack of compounded interest. It was more the possible devaluation of his savings because of hyperinflation and a dearth of safer alternatives to maintain what he’s saved. I happen to think that is a legitimate complaint.

Retorting with “at least you’re not homeless” isn’t very helpful, to say the least.

“At least you’re not homeless” is a DAMNED significant retort, for those capable of ANY empathy at all. We are all human beings.

Too much whining here.

“I have all this money.” and yet you complain. Entitled much?

What a boneheaded way of thinking.

Bob worked hard for many years for that money. He paid taxes on that money. He didn’t splurge. He spent within means and saved the rest. That’s why he has that money. He is self-sufficient.

That money is not from lottery. That money was not transferred from the Fed. That money was not from government stimulation.

Everybody who works, works hard.

Bob got rewarded….many don’t.

And now he whines ?

Do you have more than $0 to your name? Many don’t. Why don’t you give it all?

Now let’s make it even better. Let’s have a government agency to take away people’s savings.

Stop whining and give up your money.

Reductio ad absurdum, Nacho.

Ever wonder why you have to resort to totally stupid and meaningless arguments to “make” whatever your “point” is ?

There have been many supportive responses in this thread and it’s definitely good to know that I’m not alone in my feelings, but you sir do not know the first thing about me or where I came from. Calling me entitled is nothing short of laughable. I came from hell. Beaten and abused and struggling with mental health all my life. I have no safety net other than myself and the money I’ve scraped together by being frugal and careful. I have a parent that’s about to turn into a dependent. I’ve worked hard, put myself through college, made a smart bet on a career choice and have done reasonably well. How does it make me entitled that I just want to keep what I’ve earned and attempted to store for consumption at a later time? So you’re onboard with the idea that all money should be spent as fast as possible and lever up as much debt as possible? Sorry but that’s BS and so is your response.

Hi Bob, I’m in pretty much the same boat as you. I look at things to invest in and everything just doesn’t make sense mathematically so in this case the best thing to invest in is yourself. That could mean learning a new skill or buying tooling and equipment that you can use to make money. Alternatively, you may like hifi equipment, traditional antiques or retro videogames. If you buy these things wisely not only do you get enjoyment out of the item but it’s also an inflation hedge.

This puts you in control of your money and imho that’s the best person to do the job.

There is one thing that puzzles me though. In the 70’s we had high inflation but you could get ~10% on your savings with no risk. If we get the same inflation now and you can’t get any savings interest then people will have less to spend and businesses will go bust big time. Have I missed something obvious?

“Have I missed something obvious?” What you missed is the rich guys want ALL of our assets instead of just letting us keep up with inflation.

And they don’t care about the businesses going bust either.

That may be the case but I imagine it would be like a zombie film with the super rich unable to leave their secure compound without being torn apart by the masses.

Twinkytwonk: It may come to that if the gov can figure out how to get the guns away from us citizens. Note that the White House is now a military encampment with fences, barbwire and soldiers all around it.

Do you think the gov will trust us when things get worse?

What will young school children think when they take their class trip to DC?

Bob

I completely get your frustration!– I’m retired with what seemed to be plenty of money for retirement. In 2012 I feared huge inflation was going to happen after the Fed in helicopter style dumped huge amount of cash. But it didn’t happen! It could be the same story now. Why??

I now understand that the reason it didn’t happen before is that the helicopters dumped cash on the rich zip codes who held it without spending it. Monetary velocity went way down. Those people were happy to hold cash from the Fed rather than the other very questionable stuff like MBS that collapsed because the vast much less wealthy crowd who bought housing found they could not afford to pay–and house prices collapsed. But former MBS holders now had no desire or need to spend their new Fed cash.

So why all the wild inflation talk now? Democrats in control! Panic! This is the signal for Republicans raise the chorus about inflation and spending–which is now predictable after THEY have been doing the big spending–or tax cutting for four years. Now those Democrats have to IMMEDIATELY STOP DOING that terribly wicked spending like what WE did before.

But Wolf has told us about housing going up like crazy! And he predicts that before long will peak. Got it! Now telling us that home building material prices going up like crazy! I’m not sure why he is surprised. It’s the same story–a predictable result of the property buying panic induced by the new inflation panic among those with lots of cash NOT with the bottom 70% who don’t have any extra cash. The builders will find buyers at any price because of HOUSE ASSET inflation.

Inflation is likely to hit a brick wall when price raising is attempted for things that the bottom 80% buy. This is not the 1970’s– tell me how their customers are going to pay. There are lots of unemployed, and underemployed who simply can’t. Inflation causing higher wages? How with so many who need better jobs?

The people with those extra houses will either leave them empty, or charging rent with a negative cash flow problem–which if you have lots of cash may not be a problem.

So inflation for the those that can afford it–especially for hard assets. Not so much for the rest of us is my prediction.

Of course I realize could be wrong! Not taking any big bets.

Ralph

I like your calmer, more reasoned analysis.

Many of the commenters seem hysterical with fear.

Democrats in power and all these folks lose their minds. Republicans did the same….yet then not one word of protest from the same folks.

As another commenter noted….if you haved saved (hoarded) this much cash at least acknowledge that you are entitled and quite fortunate.

Less rending of garments is called for.

If the CPI inflation goes up big time which I think is expected, then wont the FED be forced to raise rates ? This would increase mortgage rates, does it mean that real estate would go bust ? Also, 10Y Yield is determined by market not by FED. FED only controls short term yield.

But FED can buy all bonds and keep rates under control although real inflation may be high. This has happened before .

You seem to think that the CPLie is an actual measure of inflation and that the fed won’t do everything in its power to manipulate and lie about the reality so as to never raise rates again. If we were in a market economy things would be very different and I’d agree with you, but I’ve been a fool to believe that. We’re not different than China. We have a centrally planned economy and the powers that be wants one thing… wage slaves, period. If you don’t have the ability to take on lots of risk you’re screwed. Hell, you might be screwed anyway because there’s no telling what the water line is for someone to do well and not get crushed by this terrorist attack on the US citizens.

Bob, first, I am sorry you feel this way. Second, my hope is that you find a way to regain agency in society and in your financial situation.

Thank you. I honestly don’t see how right now but I hope so too. I’ve begun making peace with the idea of just spending what I have left and then ending my life when the funds run out. I’m too old to start over in the event of a wipeout and have no desire to grow old and be poor. I figure I have 10 good years left. I have enough money to live those out comfortably assuming a major health crisis doesn’t bankrupt me. I just see no hope for the future of this country, or really the world. Too much greed.

Bob you are a moron to think about suicide. You fxxxing idiot have 10 years of savings to live on and aren’t happy because you want more. I work for minimum wage, have partial disability and have a handicapped child. On top of this I take care my mom who lives with us because of her advanced dementia. I didn’t pay rent for three months and sometimes can’t get enough food for everyone and lives mainly day to day and I never thought of suicide. Your problem is not money or inflation, it’s meaning that is missing in your life , take your money and go to some third world country where people live on one dollar a day, you need some perspective, and quit reading economic blogs, there is more to life than this.

Bob, suicide is a terrible thing to do to the people who love and care about you. Trust me on this, I’ve seen it destroy families up close and personal.

You reminded me of a radio broadcast I heard once. The President of Haiti was speaking at the University of FL and he said that while the US had much to teach Haiti….that Haiti had a few things to teach the US as well.

He mentioned our high suicide rate and that suicide was basically unheard of in Haiti….the poorest nation in the western hemisphere.

Please consider you’re on a rock spinning at 1,000MPH while also going around the sun at 67,000MPH. Life is absurd as I’m sure you’ve witnessed a thousand times.

You gotta let go of the fear/loathing. I get it, man. I truly do. I struggle with it to. But going postal won’t change anything. Gotta let it go….

The thing about suicide is no one ever thinks about the aftermath afterwards.

I too have seen it up close. That’s how I lost my father. And frankly I don’t blame him one bit. He’s fortunate to have not been around for these recent years to see what the world has become.

Thanks for your kind words and concern.

As I see it there’s been abuse and bullying going on by the fed, government, and ultra rich. What do you do with a bully? Well, eventually you fight back. There’s nothing more dangerous than a man with nothing left to lose, and someday that will be me. That imagined better future and social mobility was nothing more than a mirage sold to suckers like me in order to trick them into working to make others rich and ever more entrenched.

You are not alone, Bob.

There is opportunity in adversity if you still have some piss and vinegar.

Your position was kind of extreme but look at it this way. Inflation has been slowly corroding the value of your cash. The alternative extreme would be to go whole hog on stocks and get chopped off at the knees after a crash. Lose it slow, lose it fast – who knows? That’s what diverse asset classes are for. I’ve had a significant position in both cash and gold for years. Cash for the deflation (which I firmly believe is the strong natural economic undercurrent that scares the hell out of CB’s) and gold for inflation.

Both positions have been like dragging anchors on my portfolio but I’m not upset. It’s like buying insurance and being pissed that your house didn’t burn down. Rule #1 for me is don’t lose money. The dragging anchors have cut my returns to about 50% of the S&P but that’s how buffers work.

The whole price inflation thing has me totally confused. I don’t understand the underlying forces despite extensive discussion on this blog and elsewhere.

The housing thing is insane. I hear a lot about the selling being liquidation of second homes. OTOH, low mortgage rates push up prices for the buyer which IMHO cancels out the savings on mortgage interest. And when mortgage rates rise those new owners are not going to be happy.

Another phenomenon is older people who would like to sell their house but realize they’d have to pay inflated prices for their next house. That decreases available units for sale which fuels higher prices.

Meanwhile, whether you hold on to your current overpriced house or buy a new overpriced house, your property taxes are going to go up. You will be paying those taxes in real time while your paper wealth lingers in limbo. Might go up, might go down. As the saying goes the only certain things in life are death and taxes, but not increasing housing prices.

What asset classes are unloved right now? Cash and precious metals. Unloved assets often present great opportunities. Since you’re in cash, you have great deflation protection but no inflation protection. Is there an unloved asset you could acquire to offset inflation? Got gold?

Sorta related topic but not really except in terms of which nosebleed stocks to consider:

I’m still in the stock market but in 2019 I dove into internet stocks. Not FB, Amazon, or the usual stuff. I bought into what I call the glue stocks – companies that make e-commerce possible.

Appian, Okta, Twilio, Zynga, Shopify, Workday, PayPal, Trade Desk, Slack (ok, a dog), Zoom (didn’t know covid was coming but it was a great surpise return). Some of these are way off their highs but they are very volatile stocks and even with some them off double digits from their highs I’m still up 100-200% or more on them.

I put other stuff in the mix 2019 and a couple in 2020 like Illumina, Match, McCormick, Ollie’s, Waste Management, Disney, Vail, SVB and Charlotte’s Web (which I should have dumped a long time ago), and Masimo but they have been mixed compared to the “glue” stocks. Some of these went off like rockets, others I mostly bought for the dividend but still appreciated well. Not sure about Ollie’s right now. Might sell it.

This year I added about 18 more stocks, most of them “glue” stocks. These services are kind of hard for online businesses to change. If you have a database setup with one of these services the transition to another is very difficult. I experienced this myself with medical billing software. Think about moving billing data for a few thousand patients from one proprietary format to another proprietary format.

Even with a crash, I think the glue stocks will prevail. Others are the covid-related companies. The technology provided by Illumina was used to develop the Pfizer and Moderna vaccines. This technology works at the genomic level. It changes the production blueprints.

10X, OTOH, works on the protein production side (proteomics) , which what is what the cell actually does with the blueprints. IMHO proteomics has more potential but I wouldn’t kick either company out of bed. As Polonius said, “grapple them to thy soul with hoops of steel.”

My balls

What the hell am I going to do with the money from selling my business.

When I went back this morning and took the time to read your long comment I realized that I agree with almost everything you said. My apologies, I can be coarse and stupid.

Don’t end your life. Remain calm. You sitting in cash is the correct place to be if there’s a crash in the near future. You’ll be buying assets for pennies on the dollar in the future. So don’t be too concerned about that slow devaluation of your cash. I feel your pain – literally! I too am in cash – 97.5% at the last reckoning. I think those who are currently holding assets are living in a fool’s paradise.

So what’s the chance of a crash? I don’t know and neither does anyone else. What I do know is we all have to make that decision. We’ll find it easiest to live with that decision if we remain calm and aware of current developments. That way you’re doing all you can. The rest is up to God.

P.S. The other 2.5% I use to day trade. My current vehicle is XLE and before that GDXJ. My goal is to make $100/day. Not much but it helps to counteract devaluation of my cash. My guess is commodities will remain a productive area for q2 but it’s just a guess.

I also own physical gold and silver. I’ve owned it for 20 years and don’t even consider it part of my portfolio.

This might not be your cup of tea so try and find something you’re comfortable with. Remember you have super protected yourself against deflation. That’s half the battle. The remaining half is inflation. Consider it an insurance policy protecting your cash.

When it comes to remaining aware of current developments find some web sites whose information you trust. Wolfstreet is well rounded and high quality information. I have 2 other sites I read almost as much as Wolfstreet. Out of respect for Wolf’s site I would feel uncomfortable mentioning what they are.

Wolf, would you mind? I’m curious.

OK.

Bob,

The other day I went to my usual breakfast coffee and donuts at Duncan Donuts. The parking meter charged .50 to park for 20 minutes. That used up my entire monthly interest on my 50K Treasury Money Market fund. The rest rooms were all boarded up because of Covid-19. All the tables were blocked with yellow police tape. So the little pleasure of getting coffee and donuts has been ruined. This has been going on for over a year with a lot of other things too. I feel your pain. Just hang in there and try to write down 10 things that you enjoy doing and do those things. Forget about what you can’t do anymore. That’s what I’ve been doing and its working.

Bob

I lived through years of up to 26% inflation in the UK in the mid seventies. One tax rate on ‘unearned income’ got to 99%. Our Treasury Secretary was dragged back from the airport by the IMF. You don’t get bigger basket-case countries than that. It seemed like the end of the World at the time with strikes and rubbish piled up in the streets, after 12yrs of a free spending govt that said there was no other way and refused to budge.

We chucked them out in 1979 and a very tough govt turned it all round with fiscal and monetary discipline in a remarkably short time. Lots of people fought bitterly for the old way and many of them didn’t prosper under the changes. Everything for prosperity is still there underneath just waiting to spring back given sound management. All I’m saying is, don’t give up, it’s rarely as bad as you imagine in the end.

Thank you for this.

Bob: Ditch the FOMO or DOMO (depression) , in,your case. Keep reminding yourself of the joke of the two salesman facing a bear attack . One salesman is busy putting on running shoes while the other salesman is saying that the shoe thing is pointless because you can’t out run a bear. The shoed up salesman says I don’t have to out run the bear I only need to out run you. When the bear is feasting on the spoils of a collapsing fiat fed debt system you will be hauling ass to buy the spoils at a discount.

I’m with you 100% Bob. Also pulled out in 2009 and been sitting on cash waiting for them to clean up the ponzi. We know the rest of the story. The whores and parasites will say we messed up not handing our savings over to the money changers. That doesn’t change the fact that they are whores and parasites who enable the fraud and theft of others savings. At this point say screw them all. Cut your expenses. Buy a small place in the country. Work for cash. Sit back and watch eh shit show crash. Good Luck.

My evil plan is working!!!! Muhahahahaha!!! I am secretly stealing from the American people through inflation!!! Protecting my buddies in Congress who are incapable of balancing a budget!!!! I will continue doing this!!!! I will send free money to all my buddies!!! And a pittance to the common man to stop him from rioting when he figures it out!!!!! I have saved America!!!! I am a great man!!!!! Buy houses, fools!!!! I will Jack rates and crash howzing and stawks a year from now!!!! Then I will scoop up bargains!!!! Me and my buddies!!! In Congress!!!! In the hedge funds!!! In the boardroom!!!! Hahahahahahaha!!!!!!! I am saving America!!!! Saving you!!!!! Hahahahahahahah!!!!!

Nah, you’re not the real richman’s PUS boy Weimar Powell. You’re way too animated to be him. Have you seen the guy talk? He has about as much personality as a lump of coal. Sorry that’s an insult to the coal.

How dare you insult me — the great J-Pow!!! No more stimulus for you!!!! And what is this article about anyway!! There is no inflation!!!!!! Inflation is 2%!!!!! That’s what my index of coffee cups, t-shirts and doilies tells me!!! 2%!!!!!!! Be happy with your stimulis!!!!

Sounds like what Mnuchin did 08-09.

I’ve been telling customers since late last year to expect at least a 10% increase in prices this year, maybe prepare for 15. I was the messenger and it sucked. Now at least it’s going mainstream which makes it a lot less difficult for me to explain. I’m in construction and what I’m seeing has already started to price some customers out. These prices will correct some as production ramps up but the pent up demand and massive new demand will keep things pricey for a while.

Why is lumber, specifically, getting so much more expensive?

I’m in tech and have seen zero increase from vendors other than the usual 5% – 10% annual increase in insurance, which is always planned for.

Turtle

Low interest rates producing massive building surge, Covid reno projects from refis, and the occasional shutdown in sawmills due to Covid, plus transportation interruptions, all are adding to price increases. I just bought a lift of T&G pine for a feature ceiling and some steel roofing panels. My supplier apologised for all of the above. (haven’t got my latest bill yet :-) Plus, there are still percentage tariffs on Canadian lumber imported into the US, close to 30% of supply. Price goes up = tariff increase in real dollars.

I live in Vancouver Island logging country and the industry is booming. When I drive past the marshalling yard/office there is a huge billboard advertising for workers. These are 150K per year jobs. They are all machine operator jobs, plus HD techs and fallers. It’s a pretty sophisticated industry as all the gypos went under last downturn. They can’t compete.

Thanks, Paulo. Very interesting to hear it from you, with what you do and where you live.

But none of that has anything to do with the price of residential fuel oil tanks, which just went up $180 at one time.

I am wondering if they are pushing prices way beyond cost increases in order to collect revenue now before building construction hits the brick wall in the near future, sending materials prices back down again.

Was in Lowes recently and noticed a sheet of 4×8 OSB (exterior sheathing) is now $50. It used to be $10, twelve months ago. THAT is hyperinflation.

TT

Think man !

Texas had extremely cold weather with the resulting shutdown of refinerys and pipelines. The impacts from this debacle continue to reverberate throughtout the country.

AND Saudi Arabia cut oil production way back….along with other countries. This affected global supply.

A lesser contributer was a massive ship blocking the Suez canal.

So domestic debacles and international policies and debacles are behind petroleum woes.

Notice that the FED has no involvement in this scenario ?

P,

The shortage of lumber been going on for a while:

Bidding for multifamily projects in SoCal in fall of 17, I was told it would be at least six months from signed purchase order, with deposit, before lumber could START arriving,,, and that was many hundred thousands of BF…

Competent framing subs were saying they were booked for 3 YEARS, so the lumber was not the critical component.

And to add some more anecdotal history, quotes for rebar, red iron, concrete, diesel fuel were good for 24 hours in the early ”oughts”, and were consistently revised if not booked by then.

There have also been times in the past when the manufacturers of various construction components colluded to slow down and thus raise the prices,,, some ”execs” have even been convicted and jailed IIRC…

It’s amazing how the Fed got so huge, so quickly.

Without doubt the most powerful institution on earth.

Our congressman debate for months a tiny 1% tax increase, yet here comes chairman Powell shaving off 10% of your purchasing power without anyone making a stand.

He even gets featured on major magazines as a hero.

Until Jerome Powell and Co. start eating bullets, nothing will change. Violence is the only answer now. I’m not advocating for it, I’m stating a fact.

Agreed 100%

There might be some of that, but the faster/easier (and therefore more likely) solution will be an increasing shift to some species of AltCoin that the DC degenerates can’t degrade as easily.

It is no coincidence that the dawn of AltCoins came at the same time that DC committed to perpetual dollar dilution.

It may not be BitCoin and DC will make a series of AltCoin assassination attempts, but so long as DC’s engineered inflation lies exposed, the base of DC’s corrupt power will erode.

In the end, it is actually pretty hard to get a population to use a currency it has stopped trusting.

DC has squandered an inconceivable fortune (trust in the USD) that it has absolutely no clue how to recreate.

In that context, it is very interesting to see what is happening in the “ape” / WallstreetSilver (Reddit) movement. Generally they are a bunch of idiots (imho), but it is a genuine activist movement against the Fed and the fiat system.

They are creating hype, putting up billboards, advertise on Facebook (all these things paid with their own money), stamping dollar bills with texts like “Buy silver with paper” etc.

This reddit has increased with tens of thousands of members in the past few weeks (now at 63.6k ). I really hope that this morphs into a broader movement (and hopefully a bit more intellectual) against central bank policies. Anyway, I encourage them.

Buy physical gold and silver.

Agree but not going to happen. Most Americans are too willfully ignorant to know who he is or what the FED is all about. Their knowledge of interest rate is limited to low interest is good, high interest rate is bad for taking out a loan so I can buy things I technically can’t afford. Unless somehow you can tie real inflation and out of control inflation back to him and his cronies, definitely not a job you can count any MSM to do anytime soon. They’re still busy convincing you there’s no bubble out there, this is the roaring 20s without the hangover 1930s…party on Garth!

When I see somebody write that violence is the only answer, my first thought is “Wow, they’re not using their imagination”.

When I see somebody type what you just did, I know they never paid attention in history class and have no clue about how the world really works.

Mao – Political power grows out of the barrel of a gun.

Apparently, this poster has not seen the razor wire fence and armed military troops around the Capital. Great stuff to show your grammar school kids on their graduation trip to DC.

I don’t know about that but it is true that depraved minds will generally do as much as they are allowed to get away with.

I think this may happen. Not hoping for it but its the next step.

And after that, more surveillance. The only thing missing is CCTV cameras on every corner like Britain. They already monitor everything else with AI and trip wire phrases.

Wait a minute, my teeth fillings are buzzing. :-)

I’m serious about the surveillance. The last time I crossed the border I was nervous and worried, and I don’t break any laws. :-) Must be old age.

I read recently that going about your business in a normal day in a good sized U.S. city, you are on video about seven separate times.

Of course you all are hoping for violence.

That’s why you keep talking about it!

Don’t pretend w/the “I’m not advocating it….” blather.

Grow some nuts and say what you really mean.

Several folks here want violence and want to see the US burn. It’s been said many times. That’s what you believe….fine. There wouldn’t be any point in trying to change your minds.

Overthrowing the greatest Constitution in the entire world seems to be a bit drastic. With every revolution comes violence, murder, death, poverty, and suffering. Ask, Russia, Cuba, Vietnam, France….. how all that turned out. I guarantee this time, it will not be different.

We should all just stand behind Bernie and elect him to avoid all of the other unpleasantness. Bernie will take care of the Fed. I guarantee it. And it won’t involve becoming a traitor to the greatest Constitution ever and to the US. Anyone who participates would become the new “Benedict Arnold” forever in history books. I would hate being called a traitor.

Don’t blame FED. Blame your elected representatives who are elected by the People. JPo is just a pawn like all elected reps.

The FED owns CONgress, not the other way around.

That’s too much responsibility. It’s easier to cry about the boogie man than admit the truth: The public is full of morons.

They keep voting other morons into office. The ones that can be bothered with voting.

Why does everything suck? Because the public is stupid and apathetic. Like G. Carlin said: The politicians come from American schools, American communities, etc. This is the best we can do, folks.

Powell also expanded M2 by 27% in less than a year…..

IMAGINE THAT! What power…but wait….only Congress has the power to MINT. The Fed is there to provide temporary liquidity in banking events…not to permanently inject TRILLIONS.

The Fed has been rogue, and has accrued new powers, violated mandates, and self authored their mission with each “emergency”…never to relinquish.

Who’s watching? Congress enjoys the free money. Not until pitchforked and torch bearing citizens screaming of the inflation will they react. It cometh sooner than most expect.

No one will do anything but bellyache in the shame chambers of anti-social media. There will be no revolution. You only will have your like button and you will like it.

Commenting gives the illusion that you are doing something when in most cases it’s less than nothing and you are sitting alone, harmless to the establishment, looking at a screen that is also watching you.

xxxxxxxx!!!!

Educate yourself and turn your anger and despair into positive action. Yes, life is unfair but in this country we have choices. Choose to learn more about different ways to use your money to generate money. People are making money in every market whether it is down or up, deflationary or inflationary, bull or bear. Ask the successful people around you how they are making money. if you do not know successful people then go meet some. I do not read Wolf to get depressed, I read Wolf to further my education. Knowledge, like money is power. Giving up or getting even will solve no problem. Again, educate yourself and make your money work for you, not against you.

Please explain how to get “my money to work for me” when the entire system is a farce? Just dump it all into the ponzi market and pray that it goes up forever despite the very clear certainty that it can’t and won’t. Our government and fed has ruined this country. Now we have garbage crypto and TSLA. Please, tell me where one puts their money right now to protect it? Everything is seemingly in a bubble.

Re education…

Crypto isn’t per se garbage…it is a stumbling, shambling, occasionally wild west attempt to figure out how to build a non-political (and therefore anti dilutional) currency…even as the betrayed trust in the USD falls apart.

There is a rather significant amount of ferment in the AltCoin space and it is time well spent to learn something about the emerging options and structures.

A lot of AltCoins may end up zeroed out…so great caution and wisdom is called for.

But incrementalism, diversification, and education can go a long way (and not just for AltCoin).

The political class *has* ruined a lot of things in this country…but most of all its own reputation.

The emergence of crypto currencies is a blessing, because it has opened peoples minds for alternative monetary systems.

Also, blockchain technology as a transaction technology enables some wonderful stuff, like having gold and silver emerge as real money again that can be used in daily life to buy even small things like, say, an ice-cream or a cup of coffee. The physical nature of precious metals had previously sidelined them as transactable money for daily use, but it is coming back now.

If Congress is the sole “Minter of coin” then why isn’t crypto regarded as counterfeit?