There is no shortage of spec homes.

By Wolf Richter for WOLF STREET.

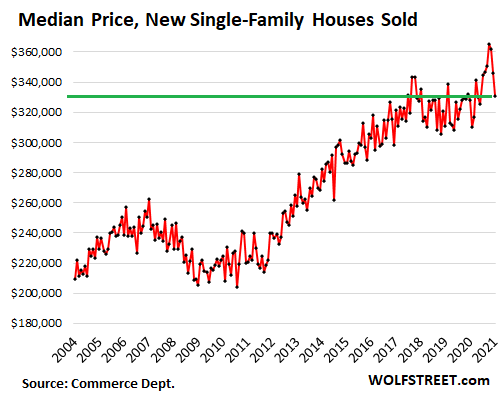

The median price of new single-family houses sold in March fell by 4.4% from February, to $330,800, after having already dropped by 4.5% in February from January, and by 0.8% in January from December, for a combined three-month drop of 9.4%, the biggest three-month drop since 2009, which brought these house prices right back into the range where they’d been since 2017, unwinding the entire price spike that had started last September:

These are single-family houses that are sold by homebuilders to the public. They do not include apartments, such as condos or co-ops, in multifamily buildings sold by developers to the public. The data is gathered by the Census Bureau and the Department of Housing and Urban Development. These houses are not traded in the market place, unlike “existing” homes, which are bought and sold by homeowners and investors.

So the dynamics are different, with homebuilders trying to find the sweet spot in the market when they build the homes, throwing in free upgrades and other incentives, or even cutting prices as necessary to make deals – or raising prices if they can – and the sweet spot was at lower price points. And business there was brisk.

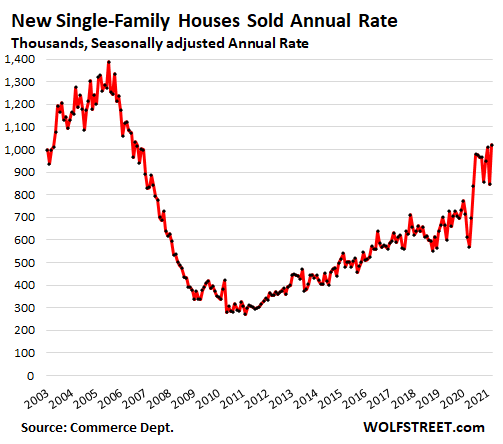

Sales of new homes, after the plunge during Snowmageddon in February, bounced back in March to a seasonally adjusted annual rate of 1,021,000 houses, eking past the total in January, and up 46% from March two years ago.

House sales remain way below the highs of the era before the Housing Bust, as a lot of housing construction since then has shifted to multi-family and often high-end condo and apartment towers in urban centers, triggering a large-scale construction boom of residential towers.

But that trend to high-rise urban centers has hit some serious rough spots during the Pandemic, when high-rise living became an iffy proposition for some folks, while houses in the suburbs or further afield jumped back into favor, starting last May – and that shift came very suddenly and brought with it all kinds of distortions.

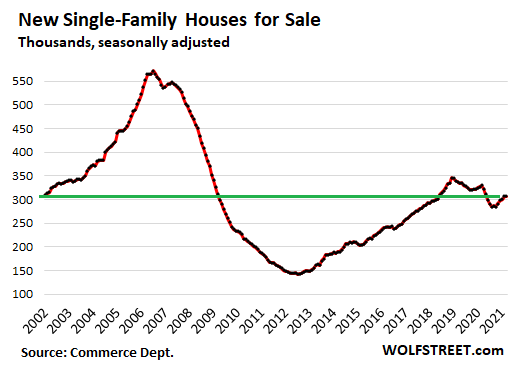

Homebuilders are busily cranking out houses, and there are plenty of spec homes for sale – though maybe not in all the right places.

The number of unsold speculative houses (does not include houses that homebuilders built on order for a specific buyer) in March remained at 307,000 houses, seasonally adjusted, matching February, the highest since May 2020, and way up from prior years:

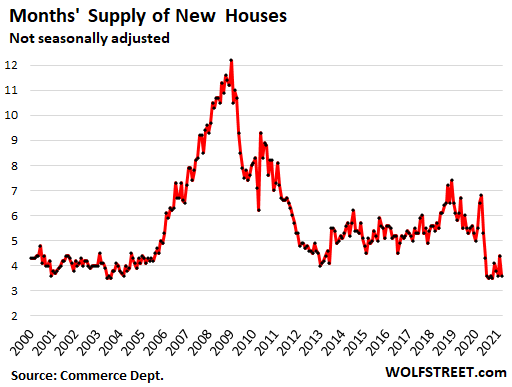

The ballooning inventory of spec homes was a massive contributor to the Housing Bust. But through 2005, the supply of spec homes was in the range of 3.5 to 4.5 months. And supply in March, at 3.6 months, is still in that range, as were the prior months:

For now, the housing market is showing that the shift of the Pandemic continues, from high-rises in urban centers to single-family houses in the suburbs and further afield. There were speculations early on that this trend was a knee-jerk reaction and would soon reverse, and it may eventually reverse, because who knows, but it hasn’t happened yet, according to the data.

Amid this trend, the issues of commuting to the office are being overtaken by the issues of working from home, such as space requirements – a particular issue with couples where both used to work in an office, and now both work at home. (Marriage counseling must be booming, or is there an app for that?)

No housing market can handle the perversity of vacant homes being used as leveraged investment vehicles to generate capital gains by just sitting there. Read… Buyers’ Strike? Everyone Knows the Housing Market Has Gone Nuts: amid Wild Distortions, Prices Spike but Sales Plunge

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The statement that new home prices are dropping is contradicted by Calculated Risk’s post from two days ago reporting on homebuilder sentiment: every market reported high demand, price increases of up to $100K amid escalating costs. See “Homebuilder Comments in Mid-April: Crazy Price Increases, Offers Way Over Ask, Costs Increasing Quickly”

You can’t tell until you break out condo unit sales from detached homes. My guess is that the dip in median prices and the huge bulge in South figures is related due to activity in Florida which is a bubble.

Re: costs to build. A retail lumber yard made a big sale at a profit. The customer: their lumber supplier. The normal chain reversed. The yard had some inventory, their supplier had a desperate customer, so they sold it back to the supplier, who had recently sold it to them.

Retail yard says this has never happened before.

Sorry NK, but certainly HAS happened before,,, for lumber, rebar, red metal ( structural steel ) cement and the other components of concrete, etc., etc.

Remember well the bidding for large projects in the early ”oughts” when the wholesale/distributors were going back to their ”normal” retail outlets to get their hands on enough of the above products to bid,,,

And, to be sure,,, bids for all of the above and gyp board were usually received with a note that the prices were good for 24 hours or 48 hours… and that kind of qualification continued up until the great crash of the construction industry in USA in 8 and 9.

After that, bids received could fairly confidently be discounted by 10 to 20 percent,,, and we did so and got a ton of the guv mint work, especially the schools taking full advantage of the declining cost of all mats and bids those years before the pendulum began the swing back…

Always thought since then that the school districts knew even better than we did, in spite of us bidding at least a couple million worth of work at least twice a week, how the markets were ”trending”,,, and took every advantage of that knowledge to help their schools be better.

The spec home builders are already pushed up against what most home buyers can afford in any given house catagory( townhouse, 3 bed etc) so the only way they can sell more is to lower prices or switch to lower catagory homes. The RE pumpers like to fantasize that the pandemic has created magical new sources of income for buyers, but their is only wishful thinking in that sentiment.

Duplexes (2 houses connected in the middle) are slowly getting more popular in my area.

More broadly, the big way to sustain growing housing prices for some more time, would be to lower interest rates. Lowering interest rates paid by homebuyers would give average people the ability to take out a bigger loan (pre-interest). The alternative/complimentary way would be to allow homebuyers to get a bigger loan for a given income level or to make loans available for longer than 30 years longer. I’m not advocating for these things, but, the FED will find ways to make this bubble bigger. Right now, homebuyers are paying 3+%!!! rates (that’s skyhigh) and ONLY 30 year!!! mortgages (could easily offer 35 and 40 year mortgages), there’s room for growth. There’s plenty of ways to grow this bubble.

As for the homebuilders, some do think it will go on forever, some don’t. Either way, the smart thing to do as a homebuilder, is to pretend it will and sell as much as you can. Homebuilders should be careful not to have too much inventory at any given time (land and properties they own directly) or to take out large loans for new offices. Most real estate agents are paid on commission only, so they don’t usually have to worry too much about salaries. For the homebuilders, they should limit their risk, but only push on the gas.

I’ve been thinking recently that the 40 year mortgage is the next ace up their sleeve to keep the party going. Forbearances could be refinanced into those en masse?

With long duration mortgages and increasing property tax, home ownership is turning into glorified renting.

Yes, the main advantage is that the rent of your owned house will be more stable (and probably lower). You can also make more changes to the house and don’t have to deal with landlord restrictions like no pets. It depends on the area, if owning a house there is worthwhile, depending on what size cities or what areas people choose to move to in America (or where the jobs are), in the future, that house may be an anchor.

In Australia the age eligibility for the aged pension rises regularly, today you need to be working till you are 67 & 1/2 years old .. I think.

Singapore .. Lee Kuan Yew .. demolished all the slum areas & built public housing .. regulation .. regulation .. regulation was the mode of progress.

Seeing how the elderly have to continue working till they drop .. What if one could qualify to purchase home .. from the time they started working .. we have compulsory superannuation which I believe is .. A BIG WASTE OF MONEY ..

“Let us play around with your hard earned money for the next 40-50 years & then .. well if your lucky .. it will be there waiting for you when you are old & grey .. plus a nominal amount of interest .. if your lucky that is.”

Who wants to buy a house when your nearly dead .. the process should start the moment you start earning.

How about that money is instead deposited in your housing account & invested securely in property.

It’s not nice to have strangers with their hands in your pockets & come pay day they are all over us like a rash.

BETTER DEAD THAN RED? … !!

SOCIALISM? … !!

The major criticisms of socialism are – too many layers of bureaucracy – the smooth running of an economy is to complex to be directed by central planners.

COMPULSORY ACQUISION ?… !!

So what do we call COMPULSORY SUPERANNUATION .. the taking by force of monies earned legitimately & rightfully & belonging to others to be used at the discretion of the STATE without consent ??

Mira,

The problem with average people investing/having their money invested for them, is that very simply their money (investment money) is not needed anymore. The major economies will continue to grow, but the actual investments needed can be covered by loans.

Properties get their value from land value, which is devired from how much people, who want that land, can pay and from the actual building. Growing average people’s wealth through housing investments, sounds like something that will basically force the next generation to pay more.

The ONLY realistic retirement options for the average person going forward is to have your family take care of you in old age or a social security arrangement. There’s no clever investment strategy around this. Everything is produced by the workers in the country and everyone not working wants what they produce and has some strategy to get it/force it from them. Social security is the simplest most efficient and direct arrangement. Having large corporations (and others) overcharge and underpay average current workers in an arrangement that satisfies current/soon to be retirees is not in any way better than a government taking excessively directly or indirectly (and is very inefficient). Forcing governments to make sure house prices go up to serve as a nest egg isn’t great either.

Right now in America, older generations have overvalued stocks as a part of their retirement strategy, but if too many cash out, their holdings plummet. This system worked for awhile because of how fast the economy grew and because of the ratio of workers to dependents. I don’t see it lasting forever and it has to crash on someone, the question is who will be the first ones to not play in. The current system is also held in place by oligopolies who make up the stock markets, if actual competition were to take place, the current stock market prices would crater.

In all developed countries, the best ways to benefit the masses would be to introduce actual competition back into the economies and to switch retirements for all average people to a well developed social security system. If the government is too corrupt for this to happen, the average person is screwed no matter what (though some older generations may make it out while it still works). Working towards a less corrupt society is the best thing an individual can do.

I seem to remember that by the end of last century’s 80’s, in Japan the “multi-generational” or “100-year” mortgage came into being. Tokyo was famous for it. Nowadays I don’t hear so much about these kinds of mortgages, but then again I am not very familiar with goings-on in Japan. Wolf will no doubt have more to say about this.

However, in my life I have several times heard the USA dissing Japanese economic phenomena, then some years later emulating these exact same practices. So, I wouldn’t be at all surprised to see these kinds of mortgages getting a foothold in the USA.

All to help potential homeowners, of course.

These mortgages are inter-generational which most people outside of Japan don’t understand. The next generation inherits the house and the debt. My understanding is if the “owners” default, the next generation still gets the bill.

Japan is very prone to natural disasters, so houses, even with 100 year mortgages were built cheapily and designed to last 30+ years. More modern homes (in japan) are much better built and intended to last 60+ years. The 100 year mortgages are actually based off of the land, which is scarce and expensive in the big cities. Constantly rebuilding the houses was a normal part of Japanese history and fit in with Buddhist traditions (as far as I’ve heard).

In America, for many reasons, I dont see multi generation house mortgages working. It is however possible, that commonly people will get a 40 year mortgage, become no longer able to work or want to retire and then flip the mortgage into a reverse mortgage. Basically if somewhere past the, say the 30 year mark, you convert the mortgage into a reverse mortgage, you instead have the current equity in your house divided by your estimated remaining lifespan then you receive payments every month instead of paying, but on death the lender takes the house. If you must move into a nursing home, the bank takes the house early, but still has to pay the monthly payments. But payments stop on death (there are additional details and technicalities to this as well). Reverse mortgages already exist, but could see many changes.

Such a flip may receive government support.

I’m a builder,investor and developer. Our market is not consistent with anything in this article.

MASSIVE shortages of materials and labor (thanks unemployment) are rocketing prices up. If someone asked for a free upgrade, I’d fall.over laughing at them.

My question- where geographically is this surplus inventory?

Nice. I’ll be calling about the floors (for half-price) in about 12 months or so.

About $7 for 2 x 4 x 8 lumber around Chicago burbs/NWI. More than double in past year. Larger dimensions bigger increase and harder to come by.

Ca has affordability mandates. Median price is still at the high end of the last five years and supply is a lot less for the same period. So price to supply is still positive. SFRs now have almost no property. Why not buy a condo? At least with a condo there is a view. The typical construction crew was loud salsa music and BC license plates. Don’t see that as much.

The quality of the trade labor is downright atrocious. The incompetency and lack of quality is pervasive all over the industry. I feel for those builders and owners that have been doing this forever.

Builders have doubled prices/revenues over the last 20 yrs (thanks to ZIRP), during one of the worst periods for employment growth in US history.

Maybe they should cough up the comparatively tiny amount of training money necessary to shift some of the 8 million Covid unemployed into their industry.

US employers have gotten into the horrible habit of bitching about *any* increase in employment costs regardless of how well their industry has been/may be doing.

If it weren’t for the insane ZIRP subsidies of the last 20 yrs, a lot of these worthies would have driven their companies into BK a long time ago.

“US employers have gotten into the horrible habit of bitching about *any* increase in employment costs regardless of how well their industry has been/may be doing.”

Corporate profits as % of economy are at all time highs for many years now.

Wages as % of economy are at all time lows for many years now.

Isn’t there a solution for that in the vaunted “free” market?

Umm…raise wages. Reduce (tax) profits ( I recommend 91%, the rate we had when the American economy BOOOOOOMED).

It’s not rocket science.

Timbers, here you are again with that stupid 91%.

Let me give you a real world example.

Say someone with access to capital and business accumen wants to open a fastfood restaurant in a neighborhood.

A business has a lot of fixed costs – rent, licenses, franchisee fee, utilities, insurance etc.

Then it has operating expenses like raw materials, payroll and so on.

Profit margin of a fastfood restaurant is about 10%. To get a $50k net profit, that establishment has to bring in $500k of revenue.

If there is a risk event – winter storms, riots etc numbers are down further.

Now if you talk about taxing that profit at 91% rate, the owner gets to take home $5k – which is 1% of the revenue.

Who in the right mind will take that extraordinary amount of risk to take home $5k?

Techies, bureaucrats, politicians, unemployed never get this logic. Neither do they think about it nor do the schools teach it.

Hey Timbers,

Do you see how your quest to punish the ‘rich’ with 91% actually translate to loss of jobs and loss service to a neighborhood?

Do you have any intellectual honesty and courage to respond here? Or will you just pop up elsewhere in another comment section and parrot your nonsense?

I agree with you. I was an electrical contractor for 25 years. I got into the trade when it was “old school”. The employees were loyal and thankful for having a job. They had seen bad times. They took pride in being a part of a successful company. I saw it all change with the internet. Our society became all about “ME”. Employees would stab you in the back for a 50 cent raise with another company. Mostly though, my employees all wanted to go out on their own and make a $million$. Most of the time, they would steal my customers in the process. Loyalty was out the window. The true craftsman mentality is mostly gone. When I did field work, I always did everything as though it was my own house. Most other workers say, “I can’t see this from my house.”

I’ve seen poor laborers that should have been laid off showing up on new jobs as foreman and supers. It’s embarrassing to the industry. No pride, no knowledge, no ability and heathery are getting paid like kings now. Shameless. You are a rare breed Onion. Guys that take pride in their work and quality of it. I agree with everything you stated in your post.

The level of competency that is now gone from the building trades reminds me of the few years I spent in third world countries trying to build a manufacturing plants. It’s amazing they (work crews) didn’t kill themselves or other people. This is where the U.S. is heading….quickly.

An older house near me (in Texas) was up for sale a few months ago and failed the sales inspection. Reason: all the pulled romex to all the plugs and switch plates had the bare copper ground wire clipped off where it terminated in the box. No ground circuits back to the panel, but the panel was grounded. Nice!

Sad.

Employees not loyal, GTFO. I worked as an electrician for years (pilot now). Every employer I had (non union) treated me as a disposable asset. Asked me to dangerous work, like stand on top of a forklift because they were to cheap to get a lift truck or lay me off the second work got slow.

Loyalty is a 2 way street, one way loyalty is for suckers.

“Our society became all about “ME”. Employees would stab you in the back for a 50 cent raise with another company. Mostly though, my employees all wanted to go out on their own and make a $million$. Most of the time, they would steal my customers in the process.”

So they learned how to operate like every business?

I’m a general laborer. I can’t afford a house in rural Oregon. The owner of my company has multiple homes… Peugeot Sound frontage, Park City…..

I know the option to start my own company is there and I’m just “whining”, but I pay $1100 per month for health insurance through this company, which is likely less than a tank of gas on the owners yacht. No loyalty here.

The house I bought in south FL, before the GFC, was built for the most part with illegals sprinkled with legal refugee Cubans. They are definitely hard workers but the quality wasn’t great. The punch list on the house was pages long and it took six months to clear it up. It was a good thing I wasn’t working or it would have taken forever to fix up.

I’ve owned a home built in the 20s and noticed it was incredibly well made. I asked a construction guy why all the homes I’ve seen built after mid 70s seem so crappy.

He said “That’s when they started trucking big pieces of the home on flatbed trucks to the site. Instead of the home being built by craftsmen, they were ‘assembled’ by far less skilled people.”

I’m sure the 1940s pecky cypress home I’m living in right now would be super expensive to build today. I doubt I’ll ever own a home built after 1974, that’s my cut-off. Lots of good stuff in my area seems to have been built in the 50s and 60s.

They gave you a little bit of land so your neighbor wasn’t right on top of you. Who buys the new particle board McMansions w/zero lot lines, I don’t know. I feel sorry for those people.

I live in a house built in 1896. The quality is amazing!

I’ve got a ranch style built in 1955…the build is solid.

There is no shortage of lumber at any of the lumberyards or big box stores.

Wolf, just got bigger apartment in SF, overlooking the bay. Will be paying less than before. Prices are down by about $1K/month.

Some people (2-3 months into pandemic) managed to get rent-control apartments 40% down from the pre-pandemic rent.

Got your free upgrade! Congrats! Lots of that going on.

Young couple I know is moving to Austin in May. Someone else is going to get a free upgrade.

Similarly, my partner and I are finally able to afford and upgrade to a rent control’d two bedroom and with a nicer view/neighborhood in SF! Price is down ~$900/month what similar 2BD were in 2019.

?

At this point I don’t even see the crash really helping much for a lot of people. Prices would have to collapse by a portion so dramatic to make a return to 2010-2014 levels here in my area of Idaho for working class individuals. Just seems unrealistic. Even in crummy Bonners Ferry run down mobile homes on a 1/3 acre of land are being list well over 200k. A regular ranch home on less than an acre of land is several hundred thousand dollars. Meanwhile the wages for blue collar workers barely breaks 20/hr in that area. Maybe mid-20/hr for Spokane area.

If you live down near cda a “starter” home runs 600-900 thousand dollars sometimes. Even Rathdrum has 2-3 bedroom homes selling for half a million dollars. Working class people like me that didn’t get a chance to buy in the early 2010’s have just been left behind. And apartments are in the realm of 1000 dollars for a studio with year long waiting lists and the landlords want huge deposits plus first and last months rent.

Unless the real estate market gets hit with a vacuum and prices shed 50%+ of their value, a single guy like me making mid 20s an hour with no debt won’t even be able to mortgage a trailer with no access to water or power. I’ve got 40k saved for a down payment but that means nothing in today’s market. It’s absurd.

It’s absolutely criminal what they’ve done.

One of the few hopes in my mind has been that the flight of money from coastal areas driving up prices everywhere will eventually lead to social/political pressure such that mainstream news talks about it and politicians are pressured to answer for it.

People say there’s nothing that can break the bubble, but tax hammer .gov brought down on investors probably can.

I imagine it would have to be after some spending spree builds out multi-family that would be exempt the tax in order to protect renters somewhat from the pass through rent increases.

Trucker guy,

We live in the same area. I noticed that demographically the county where I live (7B) has in the past ten years gotten older per capita. All those retirees coming here to die are driving out younger folks who can’t afford the cost of living.

I’m in the same boat in Bend. Make high $20’s. Drive a super economical hybrid Camry I bought for $7k and have no debt. I’m hoping that being frugal, investing and saving will one day lead me to the intersection of home ownership. Until then I’ll pay $2275/month rent.

Mike,

I live in Bend in the mid-1980s. Changed a bit, eh?

You can thank the brilliant liberals and the MMT crowd, like AOC, for insane financial policies that are propping up asset price appreciation.

If the democratic party really wanted to help working class folks, the best way to do it is to decrease the cost of things. Making $20 an hour is fine if you can buy a cheap house and get cheap health insurance and drive a paid off car and buy cheap gas and good locally grown food that is inexpensive.

These massive price increases are good for the rich only.

As someone who has more or less always worked for myself and usually worked from home, I never got anything done with a significant other around. They never understood that thinking is also working, think you are just spacing out, then call ya lazy and ask for money.

Work from underwear would be even more unappealing with a work from underwear (or no work) spouse. Many people like work because it got them away from their families.

There is a lot of plague hysteria built into the high price of suburban real estate but there is a huge crisis of homelessness in the cities behind that as well.

The suburbs are still mostly bland cookie cutter company towns more or less owned by a handful of multi national corporate colonialists and their company stores. I guess it’s all the same from the comfort of a media bunker.

A media bunker you may be trapped in with your wife, trying to work, while she virtually competes for internet points on her Peloton, heaving and humidifying your self appointed basement cubicle.

Uggh. Sounds dreadful. Glad I never had to deal with that.

Me too.

Hitch that exercise bike up to a generator and an Antminer. She can work from home too. Every story has a silver lining.

Aren’t those exercise bikes hooked up to the Internet?,”The Peloton Investment Group inaugurates group trading in the saddle “. Maybe extend the idea to actual bicycles?A flower guy I know is giving up vending contraband to concentrate his energies on crypto mini pools, making a lot more money he says. We live in goofy times. And my wife showing up in her underwear always meant not-work, not work.

I recommend a book called “How I Found Freedom in an Unfree World” by Harry Brown. In the chapter on marriage, he points out that people should “Stay together because they both want to”, not because they’re contractually obligated to.

And he mentions how insane it would be to commit to being with somebody “forever” since we all grow/change and you may not want “that” in a few years.

Another great point is that by bringing the government into your relationship, you’ve now given some “Judge” the final say in whether or not you can even end your marriage. Remember, not all Judges “grant” the divorce. Sometimes they say “Go back and work it out.”

So yeah….on numerous levels, marriage is insanity. Perhaps Chris Rock said it best: “Be lonely or be irritated.” If I knew or saw more married people that looked happy, it’d make it more appealing!!

Great Book “How I found freedom in an unfree world” . Read it twice.

Went out and bought gold after I read the book. Got robbed and almost lost all my gold.

In Canada home prices gained at least 9.4 percent since the start of the year. The Chinese cities in Canada are up at least double that since the start of the year.

Same on V Isle and there aren’t that many Chinese here. Sold my house in Aug 2014 for 370K now at least 850K. Saw it all before in 80-82 when there were virtually no Chinese here. Then came the Crash.

The biggest land boom EVER remains the Great Florida Land Boom of the 20’s. Zero Chinese. Just humans chasing easy wealth. As always.

The skyrocketing price of construction materials coupled with Fed policy that has ignited a stampede of investors rampaging through the housing market is cratering the purchasing power of the dollar with respect to housing.

Remarkably, this is being celebrated in some circles of the government and media. I guess first-time homebuyers and renters will just be told to take one for the team.

“Remarkably, this is being celebrated in some circles of the government and media.”

The MSM has a long history of celebrating DC Donkey Dung.

The good news is that the best a MSM news op can hope for is *maybe* 2%-3% of the population…many of whom hate watch.

The felt reality of tens/hundreds of millions of citizens outweigh that chickensh*t propaganda of the MSM.

Once we can surf the internet while we eat, TV news will cease to have any function/audience whatsoever.

If people want a roof over their heads they will have to join the military. This is also known as the “poverty draft”.

Talked to a family member in Florida who is getting 3 to 4 unsolicited offers to buy each week on a home that is not on the market. I asked him who was offering. He said they were all speculators. He is a curious person- I know he must have asked questions.

The stock market will have to crash and dry up some speculative money before housing becomes affordable.

I would not be surprised if ordinary scammers were making weird offers as well right now.

I just saw a mortgage rate posted in a brokers window….1 hour ago while picking up take out from next door. “Today’s Rate is 1.5%”.

Until rates go up most RE markets will continue to soar. There is nothing available around here, with bidding wars expected.

Let’s see a 7-9% mortgage rate before sanity returns, and this includes a decent return on savings accounts. We already have the inflation, the medicine to follow will be higher rates. Think 1981, and pray it’s more modest than that.

Is that one of the 5-year variable rate mortgages that are typcial in Canada?

aren’t all Canadian mortgages essentially an ARM?

There are 5-year fixed rate mortgages too, which are very popular. You have to refinance them after five years.

The 30-year fixed rate mortgage that is a benchmark in the US doesn’t exist in Canada.

Saying you have to refinance them suggests you have to seek new financing. You don’t, you are just presented with options on your rate, which like the US has been relentlessly down.

I’ll bet that 1.5% ARM will come with 1.0 – 1.5% points to close the loan paid up front, depending on the amount of down payment.

Paulo

I’d like to see how these prices would fare if we returned to Paul Volcker’s 18% mortgage rates. I’ve been dreaming of those great times.

Around that time I was working as a realtor and had just bought my first place. Got a one year term at 14 because they HAD to come down. Year later: 21.

In 81 I presented a multi-unit site (13) to some guys in Van for around 250K. Sold in 85 for about 85K.

The prices of new builds seem to be the same around here. Incentives include 10 grand back and 10 grand credit in solar. Nice premium everything throughout the home. 3 car garage, 10 year warranty. 2500 sqft.

I like them. My wife hates them. But around here they are around mid 900’s for the good ones… mid 800’s for the so-so’s

Do they have data on price per square foot? I have noticed locally that about 18 months ago builders started moving to smaller floor plans with smaller lots, while at the same time increasing there price per square foot. So what looks like a price drop is actually a change in product mixture. A 1900 sqft house now costs about what a 2300 did 2 years ago. My guess was builders know what they can charge and build to that price and if they shrink the lot the house appears the same size as the older models.

I think you’re correct. Lower priced homes are now the volume drivers. At first during the pandemic, it was the higher priced homes. Based on the median and average prices over those months.

The smaller the house the more it costs per sq ft to build.

“The median price of new single-family houses sold.”

What’s the textbook definition of a single family house? Two bedrooms 1 bath and 1500 square feet? Or is this a user defined survey wherein they ask people what kind of house they have?

Single family units in my area are sold almost as soon as the sign goes up.

Single-family house = a house that is designed for one family, no matter how large the house. Could be a 1,200-sf starter home or a 35,000-sf mansion. Obviously, some of the single-family houses out there eventually have more than one family, or might have a bunch of people that are not a family (roommates). It doesn’t matter how the house is used; what matters is how it was designed.

Multifamily building = a building with apartments or condos so that more than one family lives in the building, each in their own unit.

Here in Sonoma County we still have a serious housing shortage, it seems that every buildable infill lot has a home going up on it.

Multiple family buildings are also going up wherever the zoning allows.

Coomercial/hotel space is a different matter.

And part of that is due to the current shortage of workers and the high price of materials.

Prices are absurd for homes here, i spoke with a realtor friend who just turned down an unsolicited all cash offer from a speculator and whe he told me how much he was offered my response was “‘does this remind you of early 2006?

It did.

But this time is different!

As stated in a previous article by Wolf, “It’s a good time to make a bad decision”.

“It’s a great time to make a bad deal” ;-]

Lots of good decions available, including GTFO to take advantage of the huge purchasing power of the dollar, internationally.

Not only is real estate considerably cheaper, a person

in France can easily buy a castle on 100 acres of land for less than a million euros(1.2 million dollars).

As a bonus, the price of living is significanty less and one benefits

from universal health care and a great quality of life.

And you can also pay French income tax.

The good times in Sonoma county will roll until fire season. But the bright side is there be more vacant lots to build on next year.

Fire season has arrived in Sonoma County.

I don’t think Toronto has gotten the message yet.

For those of you who are incapable of remembering the past, we have been here before.

When the majority of manufacturing jobs were being outsourced, lending standards were being reduced to basically little more than a pulse, in order to fuel a housing boom that distracted most peoples attention to the sucking sound of jobs being outsourced in mass.

Today, the same thing is happening, only it will be the WFH crowd who will wake up in the not too distant future to find their job is now being done by someone in Jakarta….. That and the $500K MCMansion they bought is now only worth $300K.

Recent tax proposals by the new administration are specifically designed to increase globalization and reduce the US to just a low paying services economy.

We’re already there.

Really? I haven’t seen.

To the contrary, I see they plan to put a global minimum tax in place, so large US companies can’t outsource work to foreign countries to escape taxes, like they’ve been doing for 25 years.

If you really believe that, we are doomed, and the end is in sight.

Companies don’t outsource work to escape taxes, but to escape our labor prices.

The global minimum tax just would decrease the incentive to house money in Ireland or other overseas tax havens without bringing it back to the U.S.

The two have nothing to do with each other.

That ship sailed long ago. I have a lot of tears for those hedge fund managers and trust fund children. If we pay more taxes, Daddy, can we still summer in the Hamptons?!

I met a guy whose last name was Bacardi when I was just out of high school in Boca Raton. Yes, it was the famous rum family.

If only he paid less taxes, he could create a lot of jobs!! It will trickle down!! And yes, that is sarcasm….

“only it will be the WFH crowd who will wake up in the not too distant future to find their job is now being done by someone in Jakarta…..”

I’ve been hearing that refrain for the last 20 years…as they say, if you say it enough times in a row one day you will be right…

If you work in Cell Towers, you’ll hear the “They won’t need them soon, gonna do it with satellites” all the time.

I first heard it in 1999. I told a guy older than me who said “Oh yeah, I first heard that in the ’80s.”

“If you work in Cell Towers, you’ll hear the “They won’t need them soon, gonna do it with satellites” all the time.

I first heard it in 1999.”

It’s here, haven’t you heard?

Satellite internet companies like OneWeb and SpaceX have been launching constellations of low-earth orbit satellites to cover the globe with microwave radio frequency service.

But of course the cell towers already built won’t go away– and for 5G they propose smaller microwave antennae on every city block.

You think lending standard are low right now? Tell me more, because I don’t believe it.

I have two sources of income, one that isn’t common (yet is defined as acceptable by both Fannie and Freddie). Last year I went 1 for 5 on getting a loan application to result in a loan. So far this year I’m 0 for 2.

as long as rates stay low the party will continue. Greenspan raising the federal funds rate and killed the last housing bubble. Zimbabwe Powell won’t make that same mistake.

Until the bond market does it for him

I just went to look at brand new builds last week. In north Houston. Prices in building costs are up on home building prices from the previous 2 weeks. I don’t know where they are getting this data from.

Tex….come up to The Woodlands or go further north to Willis and see what’s going on there. I’m up there and getting calls, text messages, and even post cards asking if I want to sell. Crazy!

I looked at Woodlands. Nice area, but the property taxes and insurance kill you.

Bobber, they are not killing us coming from Connecticut (first), then California (second). Plus, we have great Mexican food and BBQ!

Yep, I’m off 1097 on lake Conroe, just west of Willis.

Been here my whole life, never seen anything like it,

I get text messages offering cash for a few of my properties,without even looking inside.

Property taxes now are getting to the point where people that have been here their whole life, cannot afford to stay, even though they own it free and clear. I have neighbors that have an annual property tax bill that would have bought a nice 2000 square foot home in this area twenty years ago.

Wrong, Fed funds rate affects short term lending. Long term rates are determined in the marketplace, unless the Fed buys all of the securities from the Treasury which they will never do. Long term rates will go up, no matter what the Fed does, unless we go into a massive deflationary collapse. When those rates go up the party’s over and the music stops, along with the dancing.

Long term rates should be way higher than they are right now, and should have been going up for a long time. This is not a functioning marketplace at all. Everything is distorted beyond reason.

CPI in 2006 and1999 up YOY 2.6%

30yr mortgage 6%

CPI in 2021 up 2.6% YOY last report

30yr mortgage 3.0%

The thing keeping interest rates down is the glut of money looking for yield. It is the same thing driving asset prices.

Production increases have been massive in the past few decades due to computers and automation. This has pushed profits into the stratosphere, and those profits have been able to be retained by the corporations due to low wages predicated by offshoring and mass immigration.

The bottom line is there is massive amounts of cash looking for yield. None of this will change until there is a crash, and money destruction wipes out all poorly invested cash.

Jdog, there is only a glut of cash because the central banks keep counterfeiting it. Your post reads as though it happened organically.

How does yield curve control play into what you are saying?

Yield curve control only works if you have OTHER buyers interested at the “controlled” price. Because if the Fed’s actions lead others to start selling, then you end up with a situation where no one but the Fed owns any of it.

Like Japan.

Swamp

The Fed buys MBSs…..

The Fed,, who used to have an 800 billion balance sheet…now has a near 8 TRILLION balance sheet.

They can affect long rates and do.

historicus

MBSs are like 7 year Treasury Bonds. That’s how long the average mortgage turns over and is paid off. I’m talking about over 10 years maturity Bonds. When the 20 and 30 year bonds start melting down which they already are, I believe that will spill over into the 10 and shorter yield bonds. The Fed can’t buy everything without losing all credibility if they even had any to begin with.

“The Fed can’t buy everything without losing all credibility if they even had any to begin with”

if they had any to begin with — and they didn’t.

So they buy everything like BoJ – and then what?

This sham when it eventually blows up spectacularly is gonna wipe out the next couple of generations. The wise ones of this era would have all the blood on their hands. Clearly they don’t want to think that far.

Forbes Magazine:

“House sales fell nearly 20% in February”

https://www.forbes.com/sites/melissaholzberg/2021/03/23/home-sales-fell-nearly-20-in-february/

This article lingered on Yahoo/Google news aggregators for exactly 5 minutes.Then it was gone forever.

I suspect Melissa Holzberg the Joykiller does not work for Forbes Mag anymore ?

From the article

The National Association of Realtors said the decline from January was due to “historically-low inventory”, and said home sales are ahead of total 2020 sales.

On the flip side, can anyone remember in their lifetime when NAR ever said we had good or too much inventory? Thanks for good ol search engine they were saying this in 2012….so low inventory will always been the forever boogieman.

According to NAR, purchases of previously owned U.S. homes dipped to a seasonally adjusted annual rate of 4.55 million in May from 4.62 million in April.

“The slight pullback in monthly home sales is more likely due to supply constraints rather than softening demand. The normal seasonal upturn in inventory did not occur this spring,” said Lawrence Yun, NAR chief economist. “Even with the monthly decline, home sales have moved markedly higher with 11 consecutive months of gains over the same month a year earlier.”

I am still worried about Melissa.

Imagine how fast RE vigilantes ( or was it a bot ? ) spotted this defeatist headline and removed it from Google News,all in 5 minutes…

You may also watch FRED-Federal Reserve Economic Division

https://fred.stlouisfed.org/series/EXHOSLUSM495S

Last update April 22,2021

There is a clear downward trend

Brent,

Why don’t you link my article from yesterday that covered this data point in detail, instead of linking the FRED chart on the same data point. Makes me think that you didn’t read my stuff :-]

So here is my chart from this article

https://wolfstreet.com/2021/04/22/buyers-strike-everyone-knows-the-housing-market-has-gone-nuts-amid-wild-distortions-prices-spike-but-sales-plunge/

@Wolf Richter

SIR,NO EXCUSE,SIR !

(paying tribute to Basic Training and my beloved DI)

In a way of explanation-I read all your articles and save many comments, which I pass later on as my very own deep thoughts.

I felt Phoenix_Ikki hesitancy about accepting NAR data as valid.

Ergo:

NAR data endorsed by Mr Wolf Richter and carrying the imprimatur of Holy FRED may be safely assumed to be The Ultimate Truth.

It is the best I could do under the circumstances.

Sigh. We make over $500k a year, but I’ve only been able to rent in the bay area. We are finally getting to a point where we might be able to afford a house in a good school district, which we need because of our large family, and that is only because my company’s successful IPO. Met with a real estate agent today who basically told us that our budget of 2.5 to 2.8 mil was laughable and we wouldn’t be able to get anything under 3.2 in a decent school district unless we wanted a townhouse. Or Unless we were OK with an 1800 ft.² tract house built in 1952. But the rental market is not that crazy, so I guess will continue

Omg that’s insane!!!!

Baypoor, those of us in the Bay Area who want to own a home to live in have always found that the savings we put together are never enough to buy the intended place. But somehow we manage to get it done, most of us on a fifth of your $500k a year. No whining allowed for you.

Cries from the epicenter of crazy. With that income hopefully you can fund an early retirement somewhere. Six months ago it was 600k though

Concerning Wolf’s statement in article that urban high rise residential tower living took a hit during pandemic, but noting that the trend may reverse itself:

I recently came across a news story that according to one developer in a major Midwest city, their spanking new apartment towers built just before pandemic are doing fine, with an occupancy rate of about 95%.

I rarely if ever hear about occupancy rates in all those fancy new luxury apartment high rises and complexes (confidential info?) so my ears perked up at that.

Heinz

Wolf posts other articles on RE in booming suburban / rural markets. The Midwest, both SFHs and all rentals, has been booming for 5 years and the WFH exodus is keeping it rolling. Even the FHA low-end foreclosure homes after forbearance is halted will not drop in price – hedge funds and investors will pay cash premiums for them.

Is that occupancy rate or sold rate?

A landlord can fill a new fancy tower just fine if the rents are low enough. People will upgrade to a better place for the same rent. Then the lower-quality rentals take a beating.

But often a landlord cannot lower the asking rent and the rents that are agreed to because of agreements with lenders and the issue of the value of the property if rents are dropping. Those landlords sit on massive vacancy rates waiting for better days.

What they do is giving one time incentives of 1 or more months free at market rates, plus cash discount. That way they can keep up their fictitious charade of ‘market rates’. Hypernormalization – google it.

“Then the lower-quality rentals take a beating.”

Yes, in Urban Planning world those places are supposed react naturally to the increase in supply & the older units become “filtered” down housing, becoming more affordable. The only problem w/this is prices are sticky on the way down and landlords just don’t want to decrease rents easily. In terms of econ, what other industry has pricing so resistant to a finding the bottom?

It’s all a government plot.

1.) Tell homies to buy houses.

2.) Lower Fed funds rate.

3.) Buy bonds and mortgage backed secures to crash mortgage rates.

4.) Secretly pay Redfin to manipulate estimates since buyers pay whatever Redfin tells them to pay (bidding war fee not included).

5.) Plant bogeyman stories in media to terrify leading-edge Asian buyers into buying houses in safe, expensive neighborhood to escape bogeyman.

6.) Run mortgage ads 24/7 on all media outlets to brainwash terrified Americans with FOMO.

7.) Homies sell houses.

8.) Raise Fed funds rate.

Nope.

Hedge Funds buy up houses.

Fed Chair buys MBSs till the 30yr is near below the inflation rate

Hedge Funds win on their bets due to Fed Chair decision

Yes, hedge funds are JPow’s homies.

+1

And if there is a large scale crash, who is going to step in & swoop up all the discounted foreclosures? Not mom & pop/worker bee’s, the homies.

So where do we find actual (not assumed or projected) data on breakdown of SFH buyer purchases– institutional buyers (for example hedge funds) versus traditional private individual buyers?

How can the new home builders reduce prices with lumber prices so high over the past six months?

They must have had some pretty high margins to begin with if they can eat a 300-400% lumber price increase and reduce prices.

A lot of builders bought land 10 years ago that they’re now building on. They paid less than $10,000 per acre and after improvements are charging lot premiums of $400,000+ for houses on 1/4 acre. Do the math.

Yep, banks were begging us to buy

Lots in developments that got slammed in 08.

All built and sold now.

Buy low, sell high…..right?

Or is that a bad thing now?

This new economy is so confusing.

Lumber is only a small part of the pie in building. When the overall market is making 20-30% year over year returns in real estate, namely homes, you can soak up 10% portion of a building cost jumping 2-3x in cost. A stick built house having framing go from 10k to 30k is only a 20k jump. Meanwhile a house that used to take 10k to frame has went from 150k on the market to 250-400k depending on the location. All other aspects of home building haven’t jumped 3-4 times their prepanic buying costs.

It’s just another bit of window dressing to startle the flock into FOMO even more. A guy a my work said he bought in June last year and has 200k equity in his house that he financed for 250k. I told him he should cash out and rent until prices drop since clearing 200k or more at 21 years old is a major windfall and like hitting the lottery.

His response was that capital gains would take all of that money “because Biden ya know” and the area we live in is the next Jackson Hole Wyoming so the prices will never fall from here on out.

Wondering if that was the last thing the realtor told him before he signed his mortgage.

One solution to the lumber- and labor- expensive traditional stick-built houses are to turn to alternative building methods.

I believe there would be quite a niche demand for other less-expensive options in these inflationary times.

But I do think builders would resist changes with all their might until market forces their hand– they are so comfortable and well-versed in their old stick-built ways. And the lumber and fastener industries and other suppliers have a big stake in the old ways.

Bobber…agree.

something not right here

The FED just blows bubbles. That’s it. They need to be shut down.

Mortgage rates are half of what they should be..would be…in a pre 2009 world.

SP500 at 2009 bottom sold at 0.7 X revenue. Today it’s 3.1 X revenue. Revenue has grown about 50% since 2009. A little math shows that about 75% of stock market growth is Fed wealth affect and about 25% is based on actual revenue growth.

Easy money has a similar affect on housing I would think. The problem is you can’t keep expanding asset prices 3X the GDP growth. Now asset prices can’t stay at these levels without Zirp and possibly QE forever.

If you do discounted cash flows on the SP500 dividends you can’t justify current price unless Zirp is here forever. I would say the same is true for housing. Any real rise in mortgage rates is going to crush housing prices. We are in a debt trap where assets blow if interest rates rise.

no supply where I live

and contractors cant bid because of crazy material costs

just sayin’

Does anybody want to chime in on this? It basically posits that because interest rates are so low, home prices are actually historically low (unless you’re paying cash).

I know, I know…

But the guy seems earnest and makes a pretty good case:

https://realestatedecoded.com/the-shocking-truth-about-house-prices-since-1990/

I would love to see a YUGE crash, but I just don’t see it coming. This might be why.

What do y’all think?

So what would happen if the rate increases?

Also what if the pool of buyers who can afford dries down ?

Or if people start losing jobs .

List prices are up for new spec homes in Utah. No upgrades were allowed, not even choice of carpet. It was more like take it or leave it. The selling agent advised to bid 30-40K more than listing price to have a decent chance.

For 1800 sf to 2400 sf finished area, the list prices ranged anywhere from 500,000 – 540,0000 for last month. It was supposed to increase this month.

Maybe, Utah trends differently.

I look at homes on Holden Beach,NC from time to time. Saw one for sale today for $1.4 million. Very nice and out of my price range by a lot. The owner had paid $1.5 million in 2006 when things were red hot there. He had listed it for as low as $950,000 a few years back to try to move it. You can overpay in a hot market and really screw up. Comps might say that the house is worth a big price, but that is in today’s market. He probably has had 15 long years.

1) It’s a great time to make a bad deal, because Existing Home Sales

are premature.

2) The DOW 1,000 in Jan 1973 was premature.

3) Market makers will dive to the cold valley bellow, using the downdraft to hunt a rabbit, fly back to the the top of the cliff, to fil A Chicks and use the thermal system to glide effortless higher, looking

for a new target.

Falling new house prices are an excellent predictor of a recession. It is wise to keep a close eye on this data over the next quarter or two. We are still well above the lows of 2019/2020 prices so no reason to get bearish right now. I can’t imagine the pain of a recession after the self-inflicted one we just went through. A double dip would be brutal and unlikely, but it is always a possibility. The falling new home prices this past quarter are likely a reaction to rising rates and the mix of types of homes sold. The ten year bond yield really needs to get above 2% before we get into the danger zone in this cycle. Full speed ahead with a keen eye on the horizon.

But that’s just it, we never did “go through one” last year. The government borrowed $6 trillion and handed it out so very few people outside of small businesses in a few hard hit industries really suffered any pain.

There was no real recession except on paper. None of the cultural or social externalities that come with recessions came this time, because of the trillions in “stimulus.”

The government either keeps the stimulus FOREVER, or we actually will have the recession we should have had last year.

RightNYer

No recession???? I’ll take you down the main commercial areas here in the most affluent county in the USA Montgomery County, where 75% of the businesses are closed, the Malls are empty, people out of work, panhandlers everywhere, homeless encampments expanding in the city and suburbs

DC looks like a neutron B$mb went off in the downtown business district.

FHA homes 20% in default, VA 10%

What the heck are you smokin???

Swamp, that’s exactly what I mean. It hit small businesses that had a retail presence (stores, restaurants, bars), and not much else. The large corporate chains that exist in malls shifted their business online, and didn’t fare that badly.

I suspect the defaults in the housing markets are more about people gaming the system than we’d like to imagine.

The point is, GDP wasn’t affected nearly as much, and people didn’t “buckle down” and reduce spending the way they normally would during a recession. In fact, spending went UP. People were falling all over themselves to buy luxury cars, boats, furniture, jewelry, and so forth.

I don’t know what that is, but it’s not a recession.

I am with the camp that bitcoin is going to be the leading indicator for stock market and housing busts, because it’s the big highly speculative asset right now. At some point in the cycle asset values will have to make long term sense, not just be a short term speculative play.

As I posted before we’re in a 2020 version of the Jimmy Carter economy of the 1970s.

– massive illegal immigration

– rising energy prices, shortages

– rising interest rates

– easy money policies

– incompetent Fed reserve

– incompetent federal appointees

– devalued dollar

– government spending boondoggles

– rising lumber and building mat prices

– rising housing prices

– FOMO buying of overpriced homes

– Bonds yields trailing increases in money supply/inflation

If you liked Jimmy Carter’s economy you’ll love these brain dead morons that are running the country now.

Enjoy

In those days one could almost keep pace with CDs and Money Market Funds. Not now. Mattress or casino.

I did see data that there was a 10 year period that t-bills gave you 9% return just matching inflation back then, better than 10 year run in stocks.

And in Jimmy Carter’s America our manufacturing sector was not outsourced yet, public and private debt was quite minimal compared to today’s astronomical debt levels, and our society was still relatively cohesive vs the raging culture wars and divisiveness we witness today.

No realistic comparison is possible. We have entered the Twilight Zone of modern human history.

Heinz

So we’re in worse shape than the Jimmy Carter era. Some additional negative factors. Not good.

At least in the Jimmy Carter era you knew what to do to counter the incompetence. Swiss bank accounts were a great haven. Not any more. They report all your information to the IRS.

Mattress doesn’t work. Dollar is devaluating. Also if anyone finds out you are storing cash under your mattress, this information is put on the Dark Web and social media sites, and every criminal, and burgler in the USA gets notified, and your house will be targeted.

SC

Gotta say……you win the prize for nuttiest comment here !!!

“Also if anyone finds out you are storing cash under your mattress, this information is put on the Dark Web and social media sites, and every criminal, and burgler in the USA gets notified, and your house will be targeted.”

lol get a grip

Rising interest rates?

What an imagination.

Biden took over 1/20/21….so in 3 months, he ruined a “great” America?!

Sure…..

Yep, he’s continuing a lot of the BS he inherited and added more BS.

Fight the crazy Trump with dementia Joe? Gavin against Catlin? I’m voting for the Olympian.

We are so lucky…. Kanye West for Attorney General!!

I haven’t seen anyone dispute my bullet points above about the Jimmy Carter economy. If you believe in analytical modeling vs dynamic modeling then we’re now well into Jimmy Carter 2.0

Only this time there will be nowhere to run, and nowhere to hide.

Have fun

Due to the COVID die off 2020 population growth is estimated .35%. 2010-2020 US ten year population growth is estimated to be 6.6%.

There are some delinquent mortgages to deal with.

I have not seen falling home prices in SW Florida. People have been moving into this area for years. About ten years ago this area was seeing foreclosures, mark downs and unsold inventory.

We do not have a major tech company presence. The schools are rumored to be below average. There is no MIT or Cal Tech in Florida.

I’m in SE Florida, and I think much of the moving we’re seeing are transplants planning on working remotely forever. You spend 183 days in Florida, and you don’t owe state income taxes to wherever you live the rest of the year. 183 days is only November through April, not hard to do if you don’t like cold weather.

I don’ think this is correct. NY will come after you if you just visit the state to have dental work performed. They want their money! Residents of Fla who lived in NY for 2 months got a bill. Maybe this has changed. They would rip up the bill in front of 30 people and brag about not paying NY. Those who did pay, like my old man, were laughed at and called suckers.

It is true that they audit people, but the dental work thing is to see whether your claim that you’ve lived in Florida and domiciled there is BS. That’s not to say New York won’t harass you, but legally, once you are a full time resident of another state, New York has no claim to your money.

RightNYer

What NYrs were doing was carpetbagging in Florida to escape NY high rate of taxation. They would buy a second home in Fla and declare that their legal residence even though they spend only 3 months there. Their knickname was “Snowbirds”. Ever hear of that? Meanwhile they spent most of their time in NY. They got caught when they went for dental or medical care in NY. These records were shared with the tax authorities in NY. Once they were caught doing this it was game over. They had to pay all the taxes owed for the 9 months they resided in NY + all back taxes for the previous years when they were doing this tax evasion scam. As a former NYr I’m surprised you didn’t hear of this scam.

No, of course I did. What I’m saying is that if you went 7 months in Florida and 5 months in New York, going to the dentist in New York doesn’t mean anything. You’re a Florida resident, no matter how much New York hates it.

The vast majority of covid die off were in rest homes and people 80+ who are for the most part a big drain on the economy, not a driver of it…

IMO the agenda of those that are running this country has been/is to teach us a lesson and reorder society…..its a long term agenda. They want the middle class to end…..and be desperate for a job.

So…..globalization was just the start. Opening up wages to competition with China.

The open border is another tactic.

Fem pride was another way to get your spouse to work producing tons of additional GDP while taking her productivity and shipping it overseas. Destroying family life.

The price of housing is getting beyond our reach…….and it will stay there…..and get worse.

They don’t care…..well….they care….they want it to happen.

They are stripping savers (mostly middle class of their savings)….increasing the desperation.

Desperate people work cheap.

For asset holders…..if you want to keep up….. stocks, gold, tangible assets, farms are your friends.

For those that depend on wages……it is going to be a dreadful century on a declining treadmill to no where…..unless you plan to put your children to work……see Upton Sinclair.

Those waiting for the grand recession/depression will be waiting for a long time……right about the time savers have no savings……and then it will be worse than 29.

Three fingers of Jack please.

I hate to break it to you but the “long term plan” included houses at 1975 prices as recently as 2010-2015. I bought a nice home for $35K in 2014.

The borders are not “open” and never have been. Go look at the actual #s. Our country turn 245 yrs old this year. We have 328M people.

The # of undocumented “illegals” is about 3% of the population.

I’m sorry, but if you can’t compete in the marketplace w/a poor mother from Honduras who walked 1K miles here in flip-flops and doesn’t speak English….I don’t think you were that valuable to “us” to begin with.

Please stop regurgitating this nonsense…it’s beneath you.

Illegal immigrants didn’t set Fed policy. They didn’t crash our economy in the GFC. It’s white men in suits….they’re your enemy.

You’re letting millionaires and billionaires convince you to scape-goat other victims of these policies.

Pay attention to who the real villains are. Real wages have been flat for 5 decades. We have a ton of really bad problems. Don’t let millionaires working for billionaires lie you into blaming the wrong people or we’ll never fix these problems!

This reminds me of the recent meme circulating the web:

A billionaire, a worker, and an immigrant are sitting at a table with 1000 cookies. The billionaire takes 999 cookies and says to the worker “Watch out, the immigrant is going to take your cookie”.

Without competition from the “immigrant” the worker would have to earn at least two cookies, enough to support his family.

Nonsense. Without the cheap stream of labor, illegal and legal, employers would HAVE to pay more.

Not to mention the damage to social and cultural cohesion unrestrained immigration has done.

“The biggest fresh garlic producer in the nation is giving its employees a hefty raise, reflecting the desperation of farmers to attract a dwindling number of farmworkers.”

“Christopher Ranch, which grows garlic on 5,000 acres in Gilroy, Calif., announced recently that it would hike pay for farmworkers from $11 an hour to $13 hour this year, or 18%, and then to $15 in 2018. That’s four years earlier than what’s required by California’s schedule for minimum wage increases….Within two weeks of upping wages in January, applications flooded in. Now the company has a wait-list 150 people long.”

@Node centre publican’s left:

1. If it’s ‘undocumented’, how do you know the illegal population is 3%? How many visa overstays, how many crossers?

2. Walked 1000 miles in slippers? If you are conjuring up hypotheticals, let me throw one at you too. You can’t compete with w/a welfare receiver who will work for all cash, pays no tax and receives assistance paid for by your tax dollars.

Just for the record….I am not blaming anyone for crossing the border.

My whole point was that it is the folks “running the country” that are allowing all these policies that are destroying the middle class.

As far as competition…….over time…….more people chasing the same number of jobs means lower wages for the lower classes……and a great deal more pressure on our social safety net which is mostly paid for by………the middle class.

This statement is at best moronic. Illegal immigration affects the supply / demand equation for labor in a huge way.

Anyone who denies that is either lying or ignorant of how supply and demand works.

Hispanic population in CA alone went from 2.5 million in 1970 to over 25 million today. In addition Hispanic fertility rates are 3 times what the are for white.

This displaces people at the lower end of the wage scales disproportionately and the result has been mass increases in homelessness. Every action has an equal and opposite reaction and if you do not realize that, then you do not know much of anything..

New to this site – and absolutely addicted! Wonderful discussion.

Surrounding the topic of supply / shadow inventory, a close friend who runs a mortgage business told me that Fannie and Freddie are now charging a 2 point adjustment on second home purchase, anticipating they will need the cash on hand to manage the wave of coming foreclosures. That’s where it will start, especially once price inflation hits and that second home isn’t quite so affordable anymore.

My mother is a retired Realtor and she has always said that home sales go up after interest rates begin to rise. Lots of homebuyers delay their purchases hoping to get an EVEN LOWER interest rate… but once they see that the moves are in the other direction they rush in trying to get a house before interest rates uptick again.

SpencerG

That won’t work anymore. Housing is already unaffordable, and any interest rate increases will make it more so. Everyone who wants to buy and needs roof over their heads has already bought. There is little or no future demand, but there is plenty of shadow inventory .

Currently living in a 4 bedroom renovated house in a mill town on Vancouver Island. Real estate assessment last month figured I could sell for $580-$600K. Prices rising by the month. Bought a 1 acre lot in Nelson BC 2 years ago with plans to build a smaller 3 bedroom retirement house. Building estimate is $650k for 1900 square feet with no guarantee of prices on supplies driving this higher. Total with the land price is $850k. Absolutely insane. Building is on hold. 3/4 inch plywood running just shy of $100/sheet.

historicus

MBSs are like 7 year Treasury Bonds. That’s how long the average mortgage turns over and is paid off. I’m talking about over 10 years maturity Bonds. When the 20 and 30 year bonds start melting down which they already are, I believe that will spill over into the 10 and shorter yield bonds. The Fed can’t buy everything without losing all credibility if they even had any to begin with.

My concern is that the Fed can pick up the phone and make calls that nobody knows about and inexplicaly — to us anyway — everything ends up exactly the way they like it.

The Fed apparently has a perogative to regulate itself.

Swamp

. “That’s how long the average mortgage turns over and is paid off.”

I would say that will change in a rising interest rate environment.

Who would pay off a 3% 30 yr if rates are much higher?

The Fed can’t, nor shouldnt buy “everything”. But they may try. Their mindset is completely new since 2009. Money spilt is now economic stimulus. Money borrowed is never retired, just rolled out to the next generation.

The Fed is not bigger than the market. The Fed learning that may be painful.

historicus

It gets paid off when the house is sold. or refinanced. I think Wolf had an article about this a while back.

With everyone predicting the next economic downturn to result in a epic reset and probable lost decade (or more) for equities, housing is likely to follow suit. It is after all, just another overly inflated asset. With that in mind, when I am finally positioned to buy again, inventory will likely be plentiful and prices far more reasonable.

The Central banks will prevent any epic reset from lasting over 6 months. Lol

No. They’ll try to prevent that. It remains to be seen whether they’ll be successful.

People are sleeping in tents down in Santa Clara for a chance to buy a townhouse for 1.2 million.

Insane.

The Las Vegas Housing Market is RED HOT right now. The number of homes for sale continues to decrease, and demand is strong. It doesn’t take a PHD in economics to realize that prices are going up. This kind of market creates challenges for both buyers and sellers. For sellers, it’s not just about the price, but also about getting the terms you want.