No housing market can produce enough homes when homes are massively used as vacant investment speculations. This creates an artificial shortage.

By Wolf Richter for WOLF STREET.

That the housing market has gone nuts is now in the news on a daily basis with click-bait reports of silly bidding wars with ludicrous amounts paid over already high asking prices, powered by the new pandemic of FOMO – the fear of missing out. Bad deals are made in good times, as bankers say, and these are the best of times, powered by the Fed’s policies of moving heaven and earth to inflate every conceivable asset bubble.

One side effect of the combo of these surging home prices, still low mortgage rates, and FOMO is that people have bought new homes without putting their old and now vacant home on the market and with no intention of putting it on the market for now – and thereby they have bought a “second home” – which squeezes supply and heats up the frenzy further.

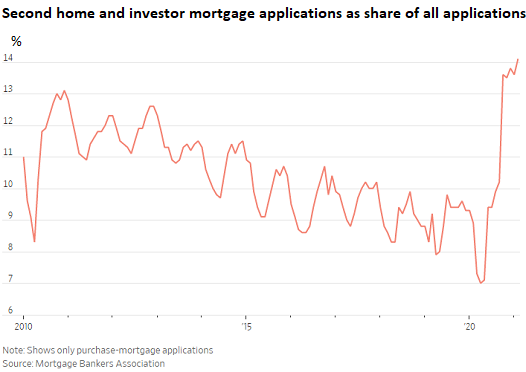

The share of purchase mortgage applications in February for second homes and investment properties has soared to 14.1% of total purchase mortgage applications, according to data by the Mortgage Bankers Association, cited and charted by the Wall Street Journal:

I have seen that people, eager to leave a big city, bought a home in a place where they always wanted to live, in the distant suburbs, or in vacation hotspots in the mountains or in coastal enclaves they’d fallen in love with, or wherever, and that, because home prices are surging and money is cheap, they’re not selling their old home. And so now, they own second homes.

The math goes like this: If they own a $500,000 home in which they have $100,000 in equity, and if they figure that the price of their home would rise by 10% over the next 12 months, the return on their $100,000 in equity would amount to 50%. If they can hang on for two years, they’d double their money. If they need extra cash, they can do a refi on the old and now vacant home.

And while they’re at it, they expect the price of their new home to surge, and they’re making tons of money just skiing or lollygagging by the beach and skipping Zoom meetings. That’s housing bubble math.

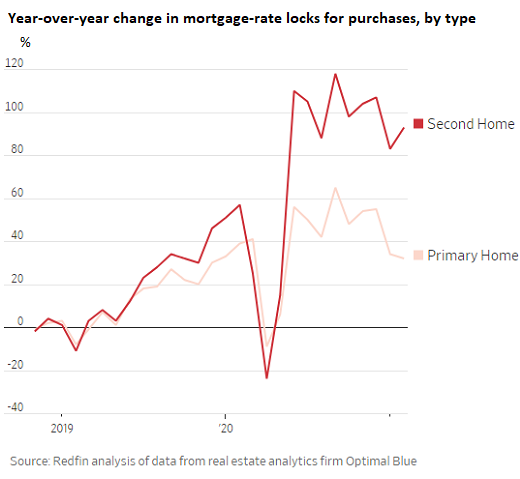

The number of buyers who locked in mortgage rates for second homes in February soared by 93% from February last year – but that’s a step down from the frenzy in the second half last year, when these rate locks had surged by as much as 118% year-over-year in September, according to Redfin’s analysis of data by real estate analytics firm Optimal Blue, cited by the WSJ. This surge far outpaces the increases of rate locks for primary residences (chart by the WSJ):

No housing market can produce enough homes when homes are used massively as vacant investment speculations. This creates an artificial shortage.

But there’s another side, which has played out during the Housing Bust: Vacant homes as investment speculations are subject to profit taking, when the owner wants to lock in profits by selling them. And this could happen suddenly, for instance when the housing market turns and those highly leveraged high-profit investments turn into high-expense money-losing albatrosses. And before the gains evaporate, owners put the homes on the market, whereby this shadow inventory suddenly becomes inventory for sale, without the owner having to buy another home.

The government has, of course, been subsidizing these mortgages for second homes and investment properties. But Fannie and Freddie are now beginning to impose restrictions in terms of how many of these mortgages they buy from lenders. Going forward, they will limit these types of mortgages to 7% of the dollar amount of their overall purchases. Freddie has already imposed the 7% limit; and Fannie has given lenders until June 1 to comply, according to FHA officials, cited by the WSJ.

Remember the first chart above? The share of these mortgages in the overall mortgage pool has soared to 14%.

These restrictions were requested by the Treasury Department toward the end of the Trump administration as part of the negotiations with the FHFA, which overseas Fannie and Freddie, to trim the roles of the two mortgage giants. The idea is that second homes and investment properties are not the core mission of Fannie and Freddie to begin with.

The effect of the new restrictions is that mortgages for second homes and investment properties outside the cutoff will come with higher interest rates – which would play out particularly in housing markets where second homes are a big factor, which are also some of the markets that have the steepest price surges.

Dollar’s Purchasing Power Swoons, but CPI ignores house price inflation. Read… The Most Splendid Housing Bubbles in America: “House-Price Inflation” in all its Glory. March Update

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As we all know, when a correction comes, the “second homes” will be the most prone to foreclosure in the event that property values sink below mortgage balances….

Especially if they were in non-recourse states.

RightNYer,

It does make you wonder about the banks who make such loans in non-recourse states…and, more importantly, if Fannie, Freddie, etc. make any rate or fee adjustments when guaranteeing mortgages made in non recourse states.

Does anybody on the board know the answer to that second question?

You only need look back till 2008-2010.

Toxic assets were taken off the books of the banks – both by congress and the Fed. There was TARP, there was TALF.

Fed started buying MBS at full face value (no haircut).

I have no doubt it will mostly be the same next time.

Umm Yeah… What correction? seriously, housing is not going to get cheaper down the road, we can forget about that.

If the FED and banks can control prices, they will and they have all the money in the world… up, up, up only

It’s Lala land, now I just want to leave the USA. It’s overrated.

*$15 burritos

*$400 for 3 minutes with a doctor (video consultations) high deductibles

*$4.50 per gallon of gas in Cali. (half the people in WFH and few flights)

*$300 for a plumber call… like doctor

*$6 gallon of milk

*any events for kids/activities $$$$

*Bills bills and more bills

It’s nonsense. People overbidding houses by multiple 1000s of $$, = lost of property tax monies for the city, county, state. Now basic 3/2 bb 500K houses are normal in Utah and Arizona…ummm Okay. (let me pay 500K in the desert for ahouse… because Land is limited… right!

Thank goodness for Tech and remote work. I’lll be leaving this sinking ship hopefully in no more that 24mo.

…yea yea yea. I know. I won’t let the door hit me on the way out *** don’t worry!

Congrats and I am jealous. If I don’t have a family and kids and have a job opportunity lined up in any of of those nordic countries, I would leave just like you in a heartbeat minute.

Nordic countries are sitting on a much bigger debt and housing timebomb than us.

It’s a high tax ‘paradise’ that leaves little in the paycheck to save. Resulting in double the household debt as in US (https://data.oecd.org/hha/household-debt.htm).

Denmark and other Nordic nations have per capita income about twice the US and vastly less income income inequality.

So lets say they have 3 or 4 time US incomes.

That makes their debt far far less the US debt in real terms.

The US have much to learn from Nordic nations.

You should, too.

A couple of things people forget from someone that lives here before painting Europe as paradise.

How do you intend on getting residency?

Language sucks, especially for non-romance languages. The illusion that everyone speaks English is a tourist trope.

Bureaucratic hurdles for minor things are infuriating, even the local version of AAA has a full blown contract(mine went to collections LOL).

Your taxes are 40%.

Lockdowns have been downright painful (since November)

#1 reason why I’m still here is for medical care.

You don’t even have to work a lot there :)

The best part is your rent will be subsidized, in addition to other benefits. I know all about Finland, but I think it’s similar in all Nordic countries.

Timbers,

“Denmark and other Nordic nations have per capita income about twice the US and vastly less income income inequality.”

You either just made that up or have really bad sources. ~55k (USA) vs ~65k (Denmark) is not ‘twice’.

Please share something to back up your other claims too.

If you’re complaining about $15 dollar burritos and $400 telehealth calls then I have two things to say to you:

1. You’re shopping in the wrong places.

2. You wouldn’t like the taxes in those little frozen European socialist paradises.

PS. Go ahead and look up disposable income by country.

All, when I say I’m disgusted with the U.S., that doesn’t mean I’m less disgusted with the rest of the Western world. Ideally, America would be split into multiple nations, and one would resemble America circa 1950.

For the first time in my life, Ehawk, I want to leave. I hate what they’re doing, and the writing is on the wall that this ship is going down. The problem is that I don’t know anywhere else that is an improvement at this point and who would even want a “Yankee.”

Yes. I used to be fiercely proud of this country. Now I’m just embarrassed, the way a family is embarrassed of the alcoholic uncle who makes inappropriate, creepy comments at the Thanksgiving table.

The problem is the rest of the West is even farther gone than we are, culturally and morally.

The only solution is a breakup of the United States. I was hoping it wouldn’t come to that, but now I’m 100% convinced it will.

You guys must be joking right? This sound like the drivel we get whenever a Republican gets to be a president.

“I’m so ashamed of my country.”

“I’m moving to Canada.”

I mean seriously, man up and complain about the system like everyone else does. Remember, in the end, it’s all kind of a joke anyway. Except, for the moment, at this particular, we’re still in a place that’s not quite the butt of all jokes.

Who would ever want a Yankee

What do you mean ??

Come to Australia, we love Americans here.

And many would bend over backwards to help you get on.

“Fiercely Proud” of the country……..

Yep!…..every single one of us in Vietnam felt exactly the same way you do, so I’d guess you must have been in some really “fierce” combat there, or somewhere else…..all “for” the country…….ya know…

PS, glad to hear you are all for 1950’s homes, taxes, and corporate and financial law….me too.

Where exactly are you going that you perceive as better?

Places like Canada, Australia and New Zealand are more stable as societies but have worse housing bubbles than the US.

“Stable as societies” = IS better.

Oh, I don’t think it’s much better here. It’s just home, y’know, where else you gonna go? My fellow Aussies leave here and live in cheap South East Asian nations. They seem to like it. I don’t care much for flying.

About buying a house .. this would keep you from migrating here.

Wow ..

If you did not want to live in the CBD you could purchase a very nice house in the outer suburbs or a bigger house on a nice block with bushland views & mist at night even further.

I worked overseas (mostly Muslim countries) for the majority of years between 2000 and 2018. In the end, I felt too alienated back in the United States. I never felt really comfortable there anyway, because spent many years off keel after getting kicked out of high school in late 1960s.

So not being yuppie level rich, I settled, and married into, a less well-heeled retirement haven – Thailand. Probably more important than the cost of living, is the low stress if dealing with Thais. It’s a Southeast Asian characteristic not not insult or provoke in social context. Like dealing with everyday Muslim folks, I came to not care what people were really thinking — as long as the stress is low and civility reigns.

Buddhism is pretty cool. No shouting, rolling in the aisles, foaming at the mouth. A major principle is the control your negative emotions, because basically they are constructed ephemeral figments of the imagination.

Smart.

Stress is a pervasive silent killer that most people underestimate.

You nailed it dude. If you could hold the door open for me a short while longer I’ll be grateful…

Ehawk – my biggest fear is that you’ll vote for the same style policies that caused you to flee. Red Texas is now turning blue because of the commies fleeing California and NY and voting for the same policies that made them flee.

Unfortunately, there won’t be anywhere left to flee once they turn those states blue.

(In reading your post, it seems you’re probably not a blue policy voter.)

Commies ??

Gosh !!

Do you mean persons with Socialist views ??

Or tyrannical views !!

Or, I want an even break views.

Or, I want my life subsidised to the point where I get it without exertion.

mfposa, if your goal is to sound like the ridiculous teevee character, Archie Bunker, congrats!

I don’t recall where I read it, but somebody researched the forwarding addresses of folks moving out of Cali and your fever dream that masses of Californians want to live in Texas is simply not happening.

The GOP only works for the uber wealthy and big corps. The dupes who make up the vast majority of the party get suckered with grievance social wedge issues (guns, god, gays, picking on immigrants).

“Commies”? You sound like a caricature.

Commies? Has Reagan come back from the realm of the dead?

Ehawk

Dude the stimulus is designed to balance out this stuff. For example, your stimulus check, assuming it’s just you and you got $1400 pays for 93 burritos. Assuming you eat one per day, your burritos are actually free for 3 months!

I think this is glass half empty half full stuff.

Your basically complaining about high prices, but if our great planners didn’t push prices higher everyone would go bankrupt!

Look to places like Hong Kong and Canada for the future. Houses will keep going up until it’s like $3m for a 3/2 bedroom house in the desert but it’s really no big deal because the interest rates will be lower and then subsidized for middle class.

Oh, and also of course stimulus will go up and up.

Just relax and check the mailbox!

My wife and I we seriously considering the same thing. For now we will stay in the US but I do see a good chance we finally pull the plug in 2-3 years. I think we have a few more years of boom time here, wheee things go crazier than we currently could imagine. Then we will begin a Great Depression level decline (which will ultimately be good for us, but quite painful and tragic to endure).

We are progressives, FYI. I hear a lot of conservatives say the same thing, for good reason. This is a universal problem.

second that. my plan, exactly

Ehawk! Where are u going?

It’s not just for speculation but to spread risk

Stock market over priced, higher taxes coming.

Putting some or more money in real estate for long term planning makes more sense than another bar of gold or silver in the safe at JP Morgan in London.

If everything goes to pot, you can still live in it. Bitcoin or other vaporware, dunno how.

Amen. This is just like what happened in mainland China. Bereft of safe, alternative investments, real estate was purchased for investment purposes, so they have huge real estate bubbles in many locations.

Their coming demographic cliff means that there will be few people with sufficient economic resources to purchase those pieces of real estate at the inflated prices at which they were purchased. Likewise, while our demographic cliff in the USA is not as bad, the lower incomes of our lower generations mean that these and other real estate investments will find few buyers as we near our cliff. See “College Enrollment Nears Demographic Cliff” in businessjournal.

In fact, with the retirements and cashing out of the Baby Boomer generation from their investments for retirement, there will be a lot of real estate (and other investments) that they will be liquidating to have adequate incomes. That is why, if hyperinflation is not nurtured by the banksters’ “Federal” Reserve, I foresee inevitably reduced real estate prices in most locations.

That does not mean that particular locations, which benefit from persons moving to them from other states or counties or countries, might not continue to see price appreciations.

Exactly! Thanks for writing this, so I don’t have to!

“College Enrollment Nears Demographic Cliff”

Well, they are considering forgiving/substantially reducing existing student debt.

So, similarly, they can start sending cheques to home buyers. There are lots of possibilities when you can create money by adding zeros on the computer.

Related: gov of NZ a small but respected player, has officially told the central bank to consider the effect its policies have on the housing bubble.

“The effect of the new restrictions is that mortgages for second homes and investment properties outside the cutoff will come with higher interest rates ”

Oh good news!

It’s good news if you’ve been a good money manager. Higher rates lead to lower prices. Bad for a borrower but great for a buyer with cash.

Good for *home* buyers as well.

Lynn, I like that. Some people are actually in the market for a home, rather than a speculative investment.

Here, potential home buyers have effectively been cut out of the market. This has been a fact for years now.

Purchase of the second home here, is by members of a family property investment business & on behalf of the business, though it may not be registered thus.

As a result of many things, beginning with 18% interest rates in the Paul Keating as PM era , where many families were turfed into the street with Keating saying “It’s good for the market”.

Persons 30-55 rent & have no intention of purchasing real estate ever. How many different age groups are disillusioned here, we are talking about decades of renters & a mindset that will only grow & rental properties are not given over to rent.

This state of affairs is a thorn in the side of the potential renter. But also an attractive prospect for opportunists who break & enter to strip the dwelling of all saleable goods.

Something has got to give & soon.

That the banks lend to hijacker scabs over the common man is scandalous & there needs to be a reckoning.

Bill Hwang .. estimated worth $500 million .. safe in family charity vault.

Estimated lending to Billy Hwang by banks US$100 billion.

There is a real role for the men in white coats & the humble straight jacket here.

Mira, you’re very good with words. That would be a great general letter with a few word changes.

This is exactly what I’m waiting for.

Just got back from Holden Beach, NC. It is an all residential island about 5 miles long by about 1/4 mile wide. Looks like only about 10% left to develop and new construction is everywhere starting around $600,000 for non water front. Housing market was dead during Great recession with builders really getting themselves in trouble.

Wow! You would think a good wave could do some serious damage.

WOW!

I thought Old school was maybe exaggerating a tiny bit about Holden Beach being 5 miles x 1/4 miles.

He’s not – Google map shows those dimensions are absolutely correct…it also shows there’s only one bridge to the mainland and it’s at the north end.

Most of our beaches are barrier islands separated by a large bay or the intercoastal waterway.

My friends place is just off the island and about 1/4 mile from the bridge. It’s a neat little vacation and retirement community with 5 minute drive to the beach and still very cheap and quiet. Her place is on fourth street or ave which is a joke because it’s is a mostly a grass driveway that I mow when I am there.

Well. Speaking of Nordic countries, it is a tradition to not invest in a home with water on 3 sides, no escape route :).

Perhaps the politicians of Holden Beach will pass a law prohibiting the entry of a hurricane without proper permits. Whee, this lawmaking stuff is easy!

Those homes on coastal NC barrier island get rebuilt every now and then after the hurricanes destroy them.

There will come a time where they simply won’t be rebuilt. There are places in FL in the same situation.

Beautiful….but comes w/a lot of risk. Also, flood zone insurance is re-setting later this year. I read a listing from somebody in Homosassa Springs, FL a few yrs ago that said “Our flood insurance was $3600/yr, now it’s gone up to $12K/yr.”

There will probably be a lot more of that happening…..

All the better to double my rent with, my dear.

Is there a way to see which markets are being impacted the most by second home purchases? Or asked another way, which cities have the most empty homes, and which cities are folks purchasing their second homes in?

Census does have MSA vacancy stats,

Table 6 – https://www.census.gov/housing/hvs/data/rates.html

I also saw another “by state” Census report earlier today that broke out some of the reasons/siting for vacancies.

Two quick spoilers,

1) More rural states have more vacancies/second homes and 2) Areas outside of a msa, also have more vacancies/second homes.

So a lot of vacant second homes may actually be more or less cabins in the forest.

It is hard to be 100% sure but the rural-rural siting suggests this.

Rural vacancies were nearly double of more urban vacancies at about 6%.

cas127,

Careful with the Census data on vacancy rates from the “Current Population Survey,” which is what you linked. They’re survey based and depend on how the question is answered and how the answer is interpreted. Those numbers were way off during the housing bust for those reasons and are always notoriously low. It’s not always easy to determine if a unit is “vacant.” The methodology explains some of this.

https://www.census.gov/housing/vacanciesfactsheet.html

It includes:

“The CPS/HVS includes people if they consider the unit to be their place of usual residence (where they spend most of the time during the year). If they have more than one home, the interviewer has to determine if the sample unit is their usual residence, that is, where they spend most of their calendar year.”

Or this:

“The question on vacancy status includes the categories ‘rented, not yet occupied’ and ‘sold, not yet occupied’, which is used in the computation of the rental and homeowner vacancy rates.”

Back when I had a vacant home, the insurance company didn’t want to cover it. I was waiting for time to get back to fix it up after the last fine tenants had trashed it.

This house is located in a small town. Will insurance cover vacant 2nd houses in large cities for an extended period of time?

I live in a tourist trap in Northern Michigan. 5 years ago, our golfing development had about 50% full time residency. Now it is about 75%. Some are locals buying in, but most are downstaters retiring to the ‘cottage’. Makes finding a tradesman difficult as many left for greener pastures during the 2008 bust.

Sounds familiar. Moved to my lake house on Petoskey, which we built a few years ago. I’ve also heard it’s nearly impossible now to get a builder. They are all swamped.

One of the recent trends in Minnesota has been a shift from having a primary residence in the Twin Cities and a getaway lake cabin for long weekends in our seven months of warm weather, to people who are now doing the WFH thing deciding they’d rather upgrade/expand their cabin and live there full time.

For many, if you didn’t live on Lake Minnetonka, the St. Croix river or a few other lakes large enough for boating on in the metro area, the goal was to have the lakeside cabin with a nice boat to let loose on the weekends.

Wolf would love this set-up (I’m guessing). A place with high speed internet, great cross-country skiing in the winter, and a lake to swim and kayak in when the snow & ice is melted. And, don’t forget the mountain bike trails too.

Timing is everything. A few hours after posting this comment, the Star Tribune has a nice feature on this 5,900 square foot “Northern Minnesota lake house is a’ home, not a cabin'”

https://www.startribune.com/northern-minnesota-lake-house-is-a-home-not-a-cabin/600041563/

There are nine photos, and although they don’t show too much of the lake, I did not see a TV anywhere. For that reason, it seems like the kind of place Wolf and the Mrs. would feel at home in.

The couple who had the home designed and built do ‘winter in Arizona,’ so that is not quite what I was commenting on above, and no mention of any mortgage. But it sure is one sweet-a$$ second home!

They are truly living the Minnesota dream.

Dan Romig,

Nice house. And cold-water swimming in the winter looks really good. I’d probably have get some equipment to break up and clear the ice. And cross-country skiing on rollerskis in the summer would be wonderful. But do you guys have any hills anywhere nearby? Just wondering, from the photos :-]

Wolf,

We don’t have that many hills.

Along the North Shore, there’s some hills and Lutsen Ski Resort is very popular. In the river bluffs of the St. Croix and Mississippi, there’s nice rolling hills. Western Wisconsin is great hill country.

Most of the northern lake country is pretty flat. Lot’s of boat planes too, as its a good place to fly one.

I did not get a handle on exactly where this home is, but I’m guessing it’s somewhere by Ely. If you like fish and fishing, winter ice fishing is its own culture up north.

Count on it being coastal areas and tourist destinations. Also, for other areas your best bet is to see which major cites have empty housing and guesstimate the effect on surrounding areas.

There isn’t any good info on that but I did find some by searching for articles and forum posts where people were commenting on empty units in their locals. For instance, there was a radio news article on the town of Mendocino where the business owners were interviewed and said most housing in the town center was empty. They had trouble filling their fire dept as all the younger people had to move away. Certain neighborhoods in LA and in SF had very low occupancy- all empty investments.

Your best bet if you know what area you want to live in is to spend several days or better yet weeknights driving around and looking for abandoned houses. I can tell you from experience it isn’t worth writing to the owners right now..

I sympathise. Homes should be for living in, not as investment speculation.

Amen to that statement. Speculation out of control.

I’ve been wanting to get a place up in the Catskills for some time now. The market has been so nuts up there with city dwellers coming up to buy that I figured come hell or high water, in a few years there would another fire sale, a la post-2009-2009. It sure looks that way now. There will be bargains galore in a couple of years.

“The government has, of course, been subsidizing these mortgages for second homes and investment properties.”

You should change “government” to “American taxpayers”.

Guess who’s going to be left holding the bag for this leveraged mess?

You realize the government isn’t funded by the American taxpayer right?

Taxes are just a means of charging for services and sucking up extra cash out of the economy.

You’re thinking of mafias and feudal lords.

These posts on April fools day. Can’t tell which ones are sarcastic and which ones are real.

Government is funded by taxpayers – current and future. All the spending and all the borrowing is/will be paid by the taxpayer.

“Taxes are just a means of charging for services and sucking up extra cash out of the economy.” Isn’t that MMT nonsense?

On the contrary, the population pays for everything the government spends.

If that payment isn’t done by taxes, it comes out through inflated high prices, due to the currency devaluation implicit in the print-and-spend financing of the annual huge deficits.

There’s no such thing as a free lunch. And if you can’t see who the sucker is in the economy, it’s probably you.

The USA would not have the deficit that it has if “taxpayers” actually paid for anything!

Your taxes are more like the money one pays for Uncle Vinnie not sending the boys round – while Vinnie’s main businesses are elsewhere.

…. “taxpayers” like to feel involved, I get that :).

There are two homes within a couple of blocks of me that have been vacant for over a year, the owners upscaled and haven’t rented/sold the old home.

Perhaps people are waiting for home prices to peak. So, that once it is obvious they have peaked (by heading down the other side) there should be a surplus of homes on the market. And then the buyers can wait for the prices to bottom out and….

Sell high & buy low – absolutely fabulous financial strategy; hardly anybody actually does that.

The problem is (literally) most people get all emotionally tied up in their underwear when it comes to calling the peak or the valley (…oooo…let’s wait for just another $5,000 price increase before we sell…).

Not only that, but when the mob realizes prices have turned, the train (with very limited seating) has usually left the station. Then you have a whole lot of people standing around trying to find the mythical “greater fool”.

System has so much financial leverage in it that the world could look completely different in one week. Can’t count on being able to call a top.

Some financial types are saying that the excessive budget defecits are causing investors to bypass GOVT notes and bonds. The money typically earmarked for notes and bonds is being reallocated to rental houses and second homes. This trend will provide stability to higher house prices.

Lets see if I get this right, investors don’t want to buy bonds because the government is running huge deficits and they are plowing the money in to rental homes. So they are afraid the government will go broke. But they think that an economy with broke state, local and federal governments that can’t pay pensions, salaries, benefits or for services will have a robust home rental market? Makes sense to me.

And we all know how liquid second homes are. Price drops and liquidity issues are much stronger than in first homes as people do need a home but not a vacation home.

Seneca’s exactly. That’s what I say to everyone who is convinced that homes and stocks are good inflation hedges. No, if we have stagflation that eventually leads to the collapse of the economic system, only precious metals will be worth anything.

How much is a HOME worth rnyr?

Truly, some of us may want to have a home to return to after ”running with the wolves” or swimming with the barracudas, eh?

Truth is that some folks will be bitten this time around the same as the last time, and the times before that at infinitum.

Paulo has it correct: save your money, pay cash if at all possible, or make damn sure your income is steady enough to pay the mortgage,,, then work OT when you can to pay the mortgage sooner,,, and to heck with the advice from the folks who say otherwise.

And THEN, when you burn the mortgage, then buy PMs or whatever.

If hyperinflation did happen, as some think it will, the amount you owe on secondary houses (or any money you owe), becomes basically nothing. The worst case scenario might be deflation for these buyers.

If hyperinflation did hit though, and you own multiple properties, one major issue you have to worry about is property taxes and utilities, which might have their own way of adjusting, these costs could be brutal on top of difficulty renting out your properties. You might want to abandon your extra properties in a worst case scenario, but you would have to find someone who wants to accept the money burden. This would be particularly severe for commercial properties. As always, Location Location Location.

I don’t expect hyperinflation to happen. But, a high inflationary period like the 80s would be possible. That would have major effects on the economy, in theory, any type of “major reset” could result in a situation, where major decisions have to be made about the economy that will put America on a better or worse track.

VintageVNvet, I agree with you. I’m referring to people who think buying more house than they can afford or need are making an “investment.”

Thomas, yes, but in such a situation, the have nots (who will drastically outnumber the haves) will basically seize the existing houses.

No, they don’t.

RightNYer,

The official home ownership rate for America at the end of 2020 was 65.8% (based on census data), nearly 2 thirds. This of course includes young adults living at their parents/relatives house. In an economic disaster, allowing most people to have old debt eroded away, might not be controversial. Most young people renting would be in apartment buildings, demanding nationalization/something similar (maybe those living in an apartment building would demand ownership of that particular apartment) of large apartment buildings, would be something that might happen. Relatively few houses by comparison are rented and their owners could in the face of a nationalization push, gift them to relatives.

There is definitely a growing economic divide, but an angry public isn’t likely to go after average houses.

It does make some since. Even the 100 year old run down place I rent grosses the owner about 6% a year and he nets about 4%. He hasn’t raised rent in 15 years because he wants someone in the place and I do light maintenance. But 4% return is much better than a CD and the property will be sold for land value some day.

Stock market goes up which creates the wealth efforts leading to house prices going up.

Stock market does down which means folks are selling their shares and buying houses leading to house prices going up.

Bond yield rises which means more confidence in the economy causing more inflations which mean house prices going up.

Bond yield goes down which means there is a dash toward safety and hard assets like houses which mean house prices going up.

[An event happens] which [some bullshit explanation] which mean house prices going up.

Nice illustration of why it is societally dangerous to allow sales creatures too much time to dream up (baloney) counterpoints to legitimate customer objections.

But you did leave out the golden oldie…”buying a house will get you l*id…women crave stability and nothing says stability like “owning” a house…”

I call it the “nesting” phenomena. LOL

I had to laugh, because in my case you could apply this statement to farm and ranch land also.

It has nothing to do with deficits, and everything to do with yield. Anyone with a small amount of financial savvy knows that.

Low yields in government paper has made it so painful to be in bonds that only those who truly understand what is happening, and how it will end are still in bonds.

Still even at that the bond market still dwarfs all other markets by a substantial amount, because smart money still has the lions share of the cash .

jdog … if the govt fiscal and monetary policy triggers inflation, then you woulod prefer real estate instead of a govt bond. The yields are about the same with the exception of inflation protection in the real estate.

Good point…even after decades of gvt interest rate slaughters…the bond mkt still has trillions more in it than the equity mkts.

All those trillions are a measure of the distrust investors have of Fed stewardship.

But…it is a measure of our gerbil wheeled political system that the “most secure” invts still result in handing $ over to the G (via Treasuries)…a G whose perfidy causes the safety panic in the first place.

cas127

Most current numbers I could find:

o Value of US government bond market – $40T

o Value of US equity market – $50T

JC,

I saw aggregate equities valuation at $30 trillion…I’ll revisit/recheck.

I don’t think anyone can know how it will end for sure. Last administration desired one solution and this one another. Fed found out easy money has to flow or something bad is going to happen. They are in uncharted waters.

I keep saying have a plan based on your time horizon and income needs. Don’t believe anything that comes out of a central bankers mouth. Try to always stay out of situation where you have to sell in a down market to raise cash.

SocalShill says what?

Hmm…an unrented/insufficiently rented house is a fairly significant cashflow negative “invt”…which is worse than even ZIRP’ed Treasuries, buried gold, and cash stuffed mattresses.

Hardly the stuff secure retirements are made of.

Boy, cash-stuffed mattresses sound good right now.

How about investors worried about debasement of currency parking it in hard assets?

Assets that cash flow and debts that can be paid back with cheaper future dollars?

There is a problem with that though. When inflation heats up, interest rates rise (already happening). Before long, mortgage rates will be double, which basically cuts affordability in half, because people don’t suddenly double their income. House prices will then drop.

For the same reason, that whole narrative about “inflating away debt” fails. Because the cost of refinancing debt jumps immediately while it takes many years before inflation hollows out the debt in any significant way.

So high inflation is more likely to lead to default than low inflation is.

I agree with Dan.

If I own a home and a second home, and I have a sub 3% mortgage on both, massive inflation will help me in so many ways.

1) My mortgage payments are fixed for both houses. Forever. No matter what inflation does. If inflation goes up 100% and my income goes up 100%, I am living the dream. If you are a renter with a fixed income, the opposite is true. Rent goes up 100%, and income is flat, you are evicted. With recent massive rent increases, people will do whatever they can to buy a home and stabilize this for the future. Hence the bidding wars.

2) Hard assets will rise with inflation as long as income goes up on average. If inflation goes up 100%, and income goes up 50%, hard assets will likely go up 50%. This will be a huge problem with feeding angry hungry voters that are now paying 2X for a gallon of milk, so I suspect income and SS will rise with inflation.

3) I disagree that government is currently supporting second homes. Currently, the prop tax deduction on primary and secondary homes are capped to 10K. That means with the std deduction at 24.5K, who has 14.5K in mortgage interest at sub 3% rates? If the 10K cap is removed, then I agree, government is supporting home deductions primary and/or secondary.

Inflation happened in the late 1970’s and 1980’s and my Silent Generation parents benefited greatly. Who would pay off a 6% mortgage with cash when government insured CDs are paying 12%, and 30 year TBills are paying 14%? Put your cash in a 12% CD and continue to pay your lowly 6% mortgage while making money. Rates are now at sub-3%. If you are a smart gambler, you may suspect CD rates will rise so we may see this again. Especially if you believe inflation will rise.

Currently, you can get a mortgage at about 3%. High quality dividend stocks have been paying 3-4%. mild risk. Low risk is 0.1% in the bank, 1.5% in 10 year CDs. High risk is 800% yield with Bitcoin. Peace of mind is paying the mortgage off now. Mild risk is high quality dividend stocks to hedge against rising inflation. If inflation rises and CDs are paying 6% again, nobody will be paying off their 3% mortgages.

Lot of ways to look at it. I am single so all I care about is shelter, function, safety and privacy. My rent is $5400 per year. Used to have mortgages on two houses and that was a poor lifestyle for me. I value flexibility and liquidity and not working anymore. Never slept well at night knowing I was taking too much risk.

Old School,

I would sleep very well at night with a 5400/year rent.

As long as your income can cover rent for the rest of your life, that would be the lowest risk and most peace of mind.

The only problem I see is if rents go up drastically for you. Paulo had an 81 year old tenant who had rented very economically until the landlord sold. Then the going rents were much higher than the tenant’s income. A fixed mortgage will be higher, but is fixed and secure for 15/30 years until it becomes 0. (Except for taxes and insurance).

Paulo was a kind sole who gave this tenant an affordable rent. Not every landlord is as kind as Paulo.

Paulo is a kind soul. Sorry. Nothing to do with the bottom of a shoe.

Did “some say” this when Red Team ran excessive budget deficits?

I think not.

Libertarians, Conservatives, Reds, only think Govt spending causes deficits…not tax cuts for corporations, the rich, that have been much greater deficits causers than govt spending.

It’s so obvious, they even say tax cuts increase revenue and only govt spending cause deficits.

They have never, ever cared about deficits except when Blues are in.

“only think Govt spending causes deficits”

Mainly because conservatives have seen government spenders treat printed/taxed money like it was their own, to be stolen/wasted.

(Note…before we head into the latest iteration of the G’s promises of infrastructural glory…who can name the three greatest, globally acclaimed shovel ready triumphs from the 2010 go round? Can anybody name one?)

In general, politicians/the G is big on promises and sh*t on execution.

But, being the G, they can evade accountability for a very, very long time…perhaps most crucially by gaming democratic processes (insulating 51%+ from the worst of taxation or printing money and framing somebody/anybody else for the inflation).

So you have to pick a team? Some people are concerned about the inexorable rise in public and especially private and corporate debt no matter who’s at bat.

It is almost always private debt that collapses. Public debt can be held, almost in perpetuity, and when it wants the Fed lets it ‘roll off.’ Not to be too picky, but debt is not intrinsic to funding Congressional spending. If you don’t like the public debt levels, tell your Congressman to stop issuing the stuff. It’s just a subsidy to line the pockets of wealthy families: To insure their immense savings. An outlier risk? I agree with Wolf. When the feds decide to crack down on money laundering (i.e., bitcoin), that could easily trigger a financial collapse.

Both right wings of the US warbird support the policy of 800 overseas military bases and spending $trillion per year on “defense” and “national security” and spying on everybody.

Expensive wars in Korea, southeast Asia, and elsewhere drove Nixon to abandon the gold standard. It is a straight line from policy decisions in the 1940s to today’s financial precipice.

The US wants to dominate the world and that costs plenty. The rest of the world wants peace, trade, and stability.

Which future do the people here prefer?

exactly, and when stock valuations get too absurd, or the mortage eviction cycle plays out, and enough housing supply enters the market, paper securities will reallocate into hard assets. after GFC no banker or broker will mark to market, property, in a downturn. and everyone knows it

We’re all Archegos now.

So i have a 5 acre house paid for in the middle of no where in kansas ,300 a year in taxes appraised at 33000 shoud i sell it for 100000?

Where would you go where you could improve your standard of living with that small amount of cash?

Nah. Maybe put some solar cells up, enough to pay for the property tax?

Sounds pretty good to me. US still has a lot of land. If people want a cheap place to live, they are still out there, though you have to like the country life style. There’s nice people everywhere if you try to be neighborly.

Here in the Carmel/Pebble Beach area for the multi-million dollar market, the bulk of buyers doing loans use “asset portfolio loans” through their money managers: these look and behave like cash during the offer process and are a savvy use of funds with such low interest rates/fees. Most of these purchases are indeed for second homes. For a whole lot of people who have banked their profits on any number of things, dirt remains at least a tangible asset. And it’s pretty here, too.

Allowing them in essence to spend their Fed-gifted stock market winnings nearly tax-free. Since they don’t sell the stock that’s collateral for the loan, they don’t even owe capital gains tax.

“Everything is a rich man’s trick.”

There are winter vacation homes in Florida. Some used listing services to rent out their second homes during the winter tourist season, when they did not want to come to Florida to use them. Winter rental leases of four or five months cost more per month than one year leases. Circa 2011-2012 this area had one of the highest foreclosure rates in the nation. They had built too many homes. Now housing inventory is low.

In the summer this place is not paradise. Some had lakeside cottages in the north where they summered.

I’ve met people in the Midwest who migrate south (typically Florida) for part of the year. It makes the most sense to travel north for just the Summer (Florida would be the rest of the year). This also makes the most sense job wise. Typically, these people were more on the lower end of the income pole. Planning housing (actual houses) around migration type behavior is very risky. The only way I can think of at the moment, that it could make sense, is to offer leases to students in college towns (in the north) for the year minus summer, and then try to lease to people in the south during the summer (for a premium).

Most do not go to Florida in the summer. Units sit vacant in the summer. The winter residents (retirees) from the north and Canada were here Nov 1 to mid-April. There were traveling nurses who stayed the winter here to staff medical facilities. Some retirees got medical bills, then had to sell a home.

That’s definitely a niche market.

In the ‘Never Thought I’d See the Day’ category, ZH now has a link to Wolf’s article on the ‘dollar as reserve currency’ from yesterday.

Wolf, do you get any revenue from such cross-posting? NC’s done it a few times.

ZH may have lifted it from the business section of Google News yesterday , or this morning (?) CB,,,

VintageVNvet,

Yes, my stuff appears on Google News occasionally. That usually sends quite a bit of traffic to my site, including from Google search.

California Bob,

No, I don’t get any revenue from this. My articles have appeared on Zero Hedge since 2012. ZH has my express permission to do so. Back in the day, I used to post them myself on ZH, and the headline would appear at the top band across the screen. For the past many years, they posted them as part of their main lineup.

I might get a few readers from it. Some commenters here have said that they first encountered my stuff on ZH years ago and came over to check things out and became regular readers. That’s how it works. My stuff is my only form of advertising.

There are only a few websites that have my permission to post my articles (ZH is one of them, NC is another, since 2012). The other websites are just taking it, and that’s a violation of my copyright.

Wolf,

Well…if established sites are literally just taking large chunks of your content, that *is* a copyright violation…and those can actually have pretty steep civil liability.

Leaving violator pocket size and jurisdiction/reachability out of it initially, have you talked to an IP lawyer?

Any site selling ads via an ad exchange, Google Adwords, etc is likely identifiable (those well heeled intermediaries don’t want potential aid/abet liability)…I imagine an experienced copyright IP lawyer would have a few similar practical tricks up his sleeve, for suing the apparently un-sue-able.

Same dynamic would apply to leveraging the companies’ that host the violators’ websites.

cas127,

Yes, I thought about discussing this with an IP lawyer. But I don’t think that the amounts are large enough to interest anyone working on a contingency basis, and I don’t want to pay for hourly fees.

The real culprits are the websites that don’t prominently attribute and link my site. Occasionally a reader sends me a link to one of those stolen pieces. And I check them out, and often I cannot even contact them, and their servers may be in other countries. That’s why this sort of thing happens so much on the internet :-]

Yes, I found Wolf’s great website from an article of his I first saw at Zerohedge.

Zerohedge is a strange site, lots of crazy stuff, but also lots of gems like Wolf’s articles as well.

Wolf,

It has been a number of years since I spent time with a copyright IP text, but I do remember that the statutes/implementing regs could be surprisingly punitive against violators on occasion.

Ditto on sweep/reach of the copyright laws, so I do wonder if there if there is potentially significant aid/abet liability (or some species thereof).

Since the intermediaries (Google, ad exchanges, etc) are profiting from a share of the violators’ profits (and since Big Tech is in bad odor) there may be law practices out there that might be looking for class representatives for class actions (addressing the small damages hurdle).

I’ll poke around and also spend some time on Martindale Hubbell to see if there are practices that specialize in such cases (there are practices that specialize in everything…)

Actually found a whole chapter online about secondary liability for copyright violations,

https://web.law.duke.edu/cspd/papers/epubs/IPCasebook2014-Ch14.pdf

A fair amount seems to revolve around intermediary takedown request capability (vaguely recall this from early Youtube/Viacom battle).

Might also find some creative pro plaintiff tactics from law review articles over at SSRN.

Can’t vouch for them but there do seem to be takedown notice/IP defense specialists out there,

https://www.dmca.com/

cas127,

Thanks for the suggestions. Will check them out.

Max Keiser was using your charts on RT a few days ago. Guess they wanted some accurate info.

I definitely consider your site to be much more readable and enjoyable than ZH. Thank you!

Where do most of the commenters on ZH come from? They are scary.

What is stopping a person from declaring their new purchase their primary residence to avoid the second home rate penalty?

Nothing, in fact most banks assume all purchases are primary residences unless you make it a point to tell them differently……

Kevin,

If there is a mortgage involved…

The lender’s automated check of the borrower’s credit report shows all current and former mortgages and other debts. You can’t hide a mortgage these days, not even one you paid off or walked away from 10 years ago.

But if you never had a mortgage on the first property, it won’t show up on the credit report.

Occupancy also needs to make sense to the underwriter.

They will look at the entire scenario, motivation for purchase, distance from work, etc……

Also, it’s mortgage fraud

And you are a little fish so you will hang.

These numbers show when a second mortgage is taken out but what if the purchaser of a second home has the first home free and clear of any mortgage?

Are these homes also included in the numbers shown?

I ask because if not then there are a lot more than shown.

KathyW,

Yes, there is a lot more second-home buying going on than is shown in the chart. The chart is just one aspect. There are a lot of “cash buyers” who borrow from their broker against their securities. This makes the purchase a lot quicker. Then later, they can get a mortgage for the house and pay off the securities-based loan.

Wolf, can you explain how this process works? I’ve really been curious how millennials can pay ALL CASH in AZ to buy a home. What is the overall demographic of these “cash buyers”? Sure mommy and daddy can help, but this can’t be the overwhelming trend for a 500k-600k all cash offer.

Regardless of generation, if you have $2 million in your portfolio, you can borrow $600k against it and pay for a house, and then get a mortgage later. That’s a cash buyer.

The older Millennials are now 40. They’re not kids anymore. They’re in their peak earnings phase. They’ve got stock options and big salaries and executive jobs. They run and own companies. They’re now the movers and shakers.

And 10 years from now, the older millennials will start facing age discrimination :-]

Thanks for noting the fact that many if not most of the so called millennial generation are doing quite well Wolf.

Gets a bit tiring to hear about the generation delta when most of that gen are doing better than their parents,,, including those who have chosen to be the $300 per hour plumber noted earlier.

Natürlich, und wenn dann ein Margin Call kommt, hilft das bei einem Einbruch der Immobilienpreise.

Naturally, and then when a margin call comes that will help with a collapse in home prices.

You know what this reminds me of in a very odd way.

China. People are stashing their money into hard assets like houses because of the value of housing, they don’t trust the stock market in China, and really, no one trust the banks. In China, if you have money, you buy property in another country or reallocate your assets that way to keep it out of reach of comrade Xi.

I wonder if people are just bidding up houses since comrade Biden and his predecessor, comrade Trump were crashing the dollar, all aided and abetted by comrade Trump’s personal appointee… JP.

What an odd world we’ve managed to find ourselves in these days.

I just did exactly that only last week.

We bought a quite cheap holiday home in my old home town, a nice place for vacation, but not so easy a job market.

We needed to act with some speed, because of course everyone has the same ideas, so we made a cash offer.

The current rumours have it that my place of work will be restructured in at the latest in September. In any case, it Will be work-from-home until 2022.

Because of my contract, there will eventually be offered some kind of deal, and then I will simply unwind where I currently live and use the second home as the landing pad for starting the next adventure.

If that takes a while, the home is cheap enough, and the small city it is located in is quite liveable. I have some family there too.

However, I think the property bubble can run for quite a while yet. They are talking about some restrictions maybe being phased in, in 2023, which will not apply to the people who are borrowing below 80% of the property valuations.

Banks very much wants to sell loans, therefore, valuations will go up!

“No housing market can produce enough homes when homes are used massively as vacant investment speculations. This creates an artificial shortage.”

Yep. It’s just like when oil went to around $150/barrel in 2008. IT wasn’t based on demand for the actual oil to use, but speculators driving the price up.

The problem is that, while you ultimately buy oil to use it (for energy or polymers), you ultimately buy houses to live in them (or to rent them out to someone who will live in them). You can maintain a speculative disconnect for a while, but eventually, it always reverts to the mean.

Regarding the above, oil lost 75% of that “value” in a year or two.

Shhhh. Do not speak logic and rationality to the chimpanzees, it upsets them and they begin to throw their feces……….

You know those old Mervyn’s commercial where the lady stands outside of the store and goes “Open!..Open!…Open!” Well, I am like that lady staring at the outside of this bubble/madness and going “Pop!…pop!..pop!” For all those not wanting to pay insane inflated prices for a decent home to raise a family or a roof over their head, hopefully we will get our wish soon enough

“And while they’re at it, they expect the price of their new home to surge…”

Housing casino! Step right up folks…

This is like a bad movie. Hold on, haven’t we’ve seen this flick before?

Boy, when this sucker goes down they will cleaning up the remains of the petite rentiers and RE investors with a spoon and a stick.

Having watched the crashes in FL and CA since the mid 1950s, I think you are entirely correct, especially with re the second homes SC.

Listening to the clerk in the convenience store give out RE investment advice in late summer of 2006, I knew the crash was imminent, and advised friends to get out as fast as possible.

Nice large ”ranchers” on a canal with sailboat water to the gulf (no bridges) were a bargain at $850K,,, a year later they went to auction at $225K ”reserve” and I am not sure they sold.

Similarly, the condo ”shells” were a bargain at $6-8MM,,, then at less than half that,,, but the gulf front condos were back above the pre crash highs in two years, and have doubled since…

Ya just gotta know when to fold and walk away, as the saying goes.

And hope you are in a non recourse state!

Using the NAR numbers for existing SFH sales, 2020’s 5.1 million in sales wasn’t radically higher than 2019’s 4.8 million.

And median ntl price only went from nutso $275k to marginally nuttier $300.

A lot of people learned bitter lessons in 2008…there is a bubble now, but it a smallish bubble…one stacked atop legacy stupidity, but not huge in and of itself.

https://cdn.nar.realtor/sites/default/files/documents/ehs-02-2021-single-family-only-2021-03-22.pdf

The last time things went bad those that bought stupidly did suffer, as well they should. But those newly-cheap houses all sold and are making those that bought them tons of money now. Even if things go south again, the wealth transfer will continue to those with the money and sense to see a bargain.

All of you here condemning the ones that bought and are now sitting on homes will join that same group and likely defend their positions with a logic that will piss of those that are in your position now.

The writing is on the wall and those that choose to actually read it and understand the opportunities it offers will do well.

Chance favors the prepared.

Inflation is driving housing prices and speculation on inflation is accelerating it. Shortages on materials has resulted in a 60% increase in raw material cost for a house to be built. If if the equivalent “new house” goes up 40% the existing homes have less competition and can raise their price point. The real question is what will the price of lumber, copper, steel, concrete be in 1-3 years. if it stays where it is or rises then housing will continue to rise until market equalization. Most of these items are also labor intensive items, so what do you think a $15 minimum wage will do?

Good points

A $15 min wage won’t do anything. I’ll give you a real life example. My big time Trump supporting neighbor did a giant upgrade to his home last year….new roof, new windows, new paver driveway, new stairs on front of home, paint, work inside, etc. Had to do a new survey/pull permits.

And my neighbor’s big time Trump supporting contractor….well, he hired all undocumented workers like he does for all of his projects.

It’s all big bad “Murica Furst!” TALK and the when it’s time for the job to get done….here comes the “illegals”. These guys aren’t unusual at all.

The min wage has been raised less than a dime/yr for the past 4 decades. For all the massive corruption/theft discussed here….a decent min wage is peanuts compared to the firestorm of greed surrounding us.

Whenever they crack down on the abuses of the VA lending program, like they did above with Fannie and Freddie, I see a bunch of homes that were held for speculation, and shouldn’t have been, being dumped on the market. The VA lending program used to be the last bastian of an honest benefit program for Vets. It is no longer. Is there anything the Fed and Jerome & Co hasn’t touched and turned into a s$ithole???? Nope, nothing left.

I call it the anti-Midas touch

What abuses are you referring to? Can you be more specific please?

Abuses include

0. violating zoning laws

1. renting out accessory units.

2. refinancing via VA and then renting out the property

3. creating a 2 unit without Occupancy permit.

4. Not performing repairs required in accordance with the VA minimum property standards.

5. Lenders not paying the appraiser for work performed on VA financed properties.

6. Lender using gimmicks to pick appraisers that “Hit the desired value” .

7. Lenders overcharging Vets for lenders fees of up to 3 1/2% without disclosure.

8. Providing VA insured mortgages for people with incomes of $300,000 or more.

The list goes on. I’ve seen all of these 1st hand. Some of these may be technically legal but they violate the spirit of the VA lending program which was to give Vets who have served their country a chance to get on the home ownership bandwagon.

Way too much mis-information in your post. I don’t think you understand the program at all. I’ve done quite a few

VA mortgages and will attempt to shed some light on your comments for others.

See below-

0. violating zoning laws

Don’t know what you are referring to here.

1. renting out accessory units.

So, if a vet can get some income to help pay the mortgage, this is an “abuse”? I would think this helps the vet.

2. refinancing via VA and then renting out the property

Well this is mortgage fraud and the vet/borrower is responsible for signing an occupancy affidavit at closing. Occupancy fraud is serious and not only relegated to VA loans.

3. creating a 2 unit without Occupancy permit.

Permits are regulated by the city, so, if unpermitted this will be an issue down the road. A VA appraisal will never give value and may not approve a property without permit.

4. Not performing repairs required in accordance with the VA minimum property standards.

This cannot be done, b/c the proeprty must pass a VA appraisal. The appraiser will cite the repairs needed and the borrower (or seller during a purchase) will need to complete the repairs prior to closing. The appraiser must re-inspect to ensure the repairs were completed.

5. Lenders not paying the appraiser for work performed on VA financed properties.

Untrue. Lender is on the hook for the appraisal fee and will pay it if they want to continue offering VA loans.

6. Lender using gimmicks to pick appraisers that “Hit the desired value” .

I have never seen this, but, it’s possible theres a couple bad apples that are willing to risk their business operation on value pumping.

7. Lenders overcharging Vets for lenders fees of up to 3 1/2% without disclosure.

Complete BS. The “funding fee” is NOT charged by lenders, it’s a VA fee. That’s how they fund the program. Furthermore, it MUST be disclosed. Lenders are very serious about disclosing properly b/c if not, that loan will not be insureable and that’s a big loss for a lender. This statement shows me you really don’t know what you are talking about .

8. Providing VA insured mortgages for people with incomes of $300,000 or more.

So? Why should there be an income limit? If you served your country but make too much you can’t get the benefit of the VA loan?

Summary: You had a bad experience with a bad VA lender and have some major axe to grind. You are spreading mis-information.

Broker Dan

So all those empty homes (50 – 75%) that we see every day where Vets are doing cash out refinances are a mirage. Sure, no abuse here.

Item #1, I was talking about illegal accessory units. No occupancy permit etc.

Item #2. See this all the time

\

Item #3. See this all the time

Item #4. Repairs cannot be properly accessed due to Covid. Cannot get into properties to see repairs.

Item #5. Happens all the time for the last 10 years since the GFC

Item #6. Appraisal Management Companies have been sued for this, or going bankrupt before they pay appraisers.

Item #7, How does paying a funding fee of 3 1/2% up front help the Vet. Sounds like a scam to me.

Item #8, Why should some blue collar worker in flyover country making $35K subsidize some fat cat homeowner in a big city suburb making $500,000k, doing endless cash out refinances

I stand by everything I said. Some may be technically legal but they are unethical or bad policy. It is not misinformation like you said. These are abuses of the VA loan program. Everyone is cashing in on this, until the whole program collapses.

1) NDX daily. There is a line coming from Feb 2020 top to Feb 2021 top.

2) There is a parallel line coming from Jan 17 2020 swing point to big red open Feb 26 2020. This line bang the cloud head bump.

3) Apr 1st 2021, NDX Hot Chillys day, gave the cloud head bump a right hook.

4) NDX might close the open gap and reach the flatbed area.

5) The red hot cleavage might seduce NDX because the cloud flatbed is thin.

I am not the only one waiting for Wolf’s another article in 2022, “The Explosive Surge of Mortgages for “THIRD Homes”: Housing Bubble Math “. Soon, US will have highest number of homes per capita. Most of them will be empty. We will be then commenting about the increase in house prices and so the party goes on further…

??

that will be the day

In the future you will either rent or squat. No amount of police presence will be able to prevent it.

Well, if there are enough empty houses, then they can easily occupied by the homeless and druggies. I’m sure the city governments and the Fed would be OK with squatters, you know….

That could be the platform for the next fixed Pres election: “A home for everybody….Plus monthly stimmies!”

We are copying China. Ghost cities will soon be a phenomenon here too.

Yes, and China is buying US.

I am seeing tons of renters having the house they are renting sold out from under them with no warning. Just notice to leave. Rents for houses are insane so renters scramble to buy as it is cheaper per month.

So this scramble is pushing the demand for houses even higher. And the pricing higher as well. Othewise it is living on the street time.

“mortgage applications in February for second homes and investment properties has soared to 14.1% of total purchase mortgage applications, according to data by the Mortgage Bankers Association, cited and charted by the Wall Street Journal”

Based on what I’m seeing here in DC Swamp, I believe the true figure is closer to 50% of the mortgage and refinance applications being for purchase of second homes or for people moving and renting the first homes, or renting both homes and pocketing the cash etc. Because of Covid-19 we are not allowed inside residential properties if they are occupied. That hasn’t been much of a problem because most of the houses we encounter are UNOCCUPIED!! Need I say more.

This could turn out to be the equivalent of the “Liar Loan” crisis of 2007.

A Mark Twain once said “History doesn’t repeat exactly, but it rhymes”

What is happening with Hedge Funds like Blackstone? Prior to ‘08 these companies were not buying residential real estate. After the crash they bought many thousands all over the country. I’ve read recent reports of young people bidding on homes only to be outbid buy all cash investors paying well over listed price. I’ve watched several homes recently sold around the Central Coast of CA immediately turned as high dollar rentals.

Manufactured/ Mobile Parks are also being bought up by these Companies.

Invest in pitch forks?

i’m long torches, myself. but i’ve always been a bit of a pyro.

Oh Wolf, one of the biggest debates online between Urbanists and more leftist activists is the role of vacant properties. Urbanists vehemently deny that vacant properties are a problem, that it’s a miniscule amount of the bigger housing picture (which is always in their view lack of supply).

Thank you for this. I’m not an economist, not by far, but it seems unsustainable to expect X amount of vacancies in order to ensure affordability (I’m not sure the number but there is an expectation of a specific vacancy rate for ideal pricing). I just see so much about housing pricing outside of supply. Speculation being a major driver.

Wolf, sorry if you’ve already seen/covered this but this was linked to me & since it’s relevant to this topic here, I thought you’d might find it interesting

http://amp.mortgagenewsdaily.com/article/969950?__twitter_impression=true

This one was also trending and got a lot of attention on housing Twitter. You’ve probably seen it but here it is just in case

(I know you don’t like links so you can just delete this once you get the links ?)

Building Ghost Towns.

The Fed, in its infinite wisdom, made empty homes

more profitable & reliable than a savings account.

And the god-like wisdom of Congress made sure that

anyone foolish enough rent-out their homes would

end up in an early grave, broke & destitute.

You nailed it.

How does AirBNB, VRBO, and other rental apps play into this?

I know specifically 2 families that did this; bought in resort areas, use the property vacationing and rent via Airbnb to defray costs.

My municipality banned short-term rentals in residential areas as they were making an already hideous low-medium-income rental situation much worse. In tourist areas they had a strong effect on driving up prices and driving down residential-rental availability (pre-Covid).

Other cities will put on limits like licensing, limited number of nights per year, etc.

How can I borrow one of these vacant second homes, from the owner, sell it on the open market, wait for the crash and then buy the house back at a lower price and return it to the original owner?

Unlce Salty,

That would LITERALLY be shorting the housing market. I love it. Now off to find some rich gullible rube. . .

if you find out, please let me know!

Also, only slightly more than a drop in the bucket, and yet to be passed, but still;

“President Joseph Biden’s $2 trillion infrastructure plan[…] includes $213 billion allocated for housing,[…]

Specifically, the plan calls for the construction and rehabilitation of over 500,000 homes in low- and middle-income areas. According to Biden, two million affordable homes and commercial buildings would be built and renovated over the next decade as part of the initiative.

Biden is also calling on Congress to eliminate exclusionary zoning laws, which he says inflates housing and construction costs – an issue that has crippled homebuilders across the country for more than a year.

Biden wants homes upgraded through “block grants” – annual sums awarded by the federal government to a state or local body to help fund a specific problem – and through extending and expanding home and commercial efficiency tax credits. “

Lots of people are going to get rich off of this deal. Not sure about how much housing will get built or renovated.

It must be fun to be able to spend someone else’s money with reckless abandon. I’d love to have that feeling once, I wonder if that’s why all these people get into politics. They are essentially the guys who couldn’t get into MS or GS or some other hedge fund of the week.

The UK is well ahead on these types of get rich quick schemes for the well connected though 2.2 bn is small fry to what you guys have planned.

https://moneyweek.com/3526/how-john-prescott-wasted-22bn

“we are left with a baffling policy that has led to 10,200 houses being demolished, 1,000 built and 37,000 fell derelict awaiting the bulldozer. And for what? Because the Government was horrified that houses were selling for “as little as £5,000”.

We’ll see what treasury yields look like after it passes.

You’re most likely right Wolf. Same old same old. Poverty pimps.

I’ve seen grants used to build affordable housing on the local level. One developer built a bunch of 1200sf 3/2 in the bad part of town, a high crime black area. The houses were affordable, but at $100K not for the people in the area. Others didn’t buy because the houses were too small 1200sf 3/2 or their income exceeded the limits.

These programs are always run by people who have no idea what they are doing. I watched the prices drop on these houses and still to this day some are empty. The proposed program will land up building ghost cities all over America.

Welp, if so then squatting will probably become more popular.

Federal government is nearly always working to over power state and local. Federal control of zoning is a big problem to me. Who is going to want to put their life’s work into a home if Federal government can drop a housing project across the street.

Have you heard what the Telecom industry has accomplished in a few states? I think it’s Indiana, Ohio and maybe Michigan where the states passed a law that overrides the smallest jurisdictions (Townships) re: building new towers.

Instead of having to follow the Township’s zoning code (aka tower ordinance), anybody can build a new tower as long as it’s in “non-residential area”.

Huge co’s like AT&T and VZW, who don’t want to pay high rents to 3rd party tower co’s (like American Tower Corp, SBA, Crown Castle), will just build a new tower since the land dev regs can no longer stop them.

You’ll see a proliferation of unnecessary cell towers. Why? Greed.

Who want’s to put their life’s savings into a bank account if the Federal government makes holding it worthless?

“… awarded by the federal government to a state or local body…” and subsequently to the “friends” of the state or local body. And then to the friends of the friends.

Fed policy is spawning a Darwinian every-man-for-himself-and-grab-what-you-can housing market where more people are being priced out. The social ramifications from this are unlikely to be positive.

Does the Fed even realize that they are unleashing brutal housing inflation on renters, first-time homebuyers and low-income folks who are being battered by higher property taxes? Or do the wealth effects for the few come before the housing needs of the many?

“Or do the wealth effects for the few come before the housing needs of the many?”

you must not have been paying attention. protecting the wealth effects for the few has been the only option for quite a while, no matter what topic you wish to speak about.

When everyone is yelling inflation be careful deflation could kick you in the nuts

Ron,

In my lifetime, there have only been 3 quarters of deflation. So that’s not what I’m worried about — though the deflation fearmongers have been out there for many years. But I have seen LOTS of inflation, including years of double-digit inflation, with prices going up every three or so months!

In the “fear of deflation era” …2009 to 2020, the CPI rose from 214 254…..that’s right around 20%.

And who exactly was afraid of deflation? Or was it just a massive effort to control perception and promote inflation.

BTW, if inflation is a “tax”, what we have here is an unelected body (the Fed) laying a tax on the People of this nation. Only Congress has that power. And who has representation on the Fed? Not the People.

So, what we have here is “taxation without representation”. Ring a bell?

Congress can’t be blamed for increased taxes and high inflation if the Fed does the dirty work.

Just a note. Financial economist Michael Hudson believes the asset inflation will be followed by a deflationary episode. A major cause of this will be lack of income growth, thus lack of demand for products and services. I have no clue whether he’s right or not. He has studied finances in civilizations going back 5,000 years.

Chris Herbert,

Yes, that’s how economic cycles used to be resolved and got a fresh start. Assets deflate, debts (other people’s assets) are dealt with in bankruptcy court, or restructurings outside of bankruptcy, by being reduced, forgiven, or converted to equity at the expense of the investors that hold those debts (their assets) and that got paid to take those risks. Prices come down a little for a little while after a long period of inflation. Stabilizers, such as unemployment benefits, kick in to make sure things don’t spiral out of control. This gives the economy a fresh start.

The problem is that this process wasn’t allowed to run its course during the Great Recession, and wasn’t allowed to happen in this crisis, and what we had after each crisis is even more debt, particularly business debts, which bogs down economic growth going forward.

There were times in the 70’s that houses in San Diego were appreciating at 3% per month, not always but there were run ups and a building bubble. When you can leverage the heck out of a place and get huge returns on your investment people will do it…until I pops, which it will. As to when, I don’t think for a while as there simply isn’t enough inventory and it’ll take years to catch up on that inventory, and in places like San Diego you’ll never catch up to what’s needed. Another reason folks buying second homes, could it be that they’re terrified of hyper inflation and their paper money becoming worthless? Of course it will, but the hard assets will appreciate with the inflation caused by the stupids at the fed as well as our lovely politicians.

Get ready for the wild ride.

Check out this new headline tonight: