Dollar’s Purchasing Power Swoons, but CPI ignores house price inflation.

By Wolf Richter for WOLF STREET.

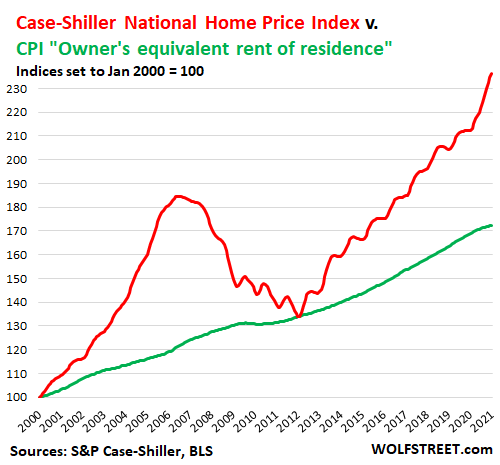

House prices rose by 11.2% from a year ago, the biggest increase since the peak of Housing Bubble 1 in 2006, according to today’s National Case-Shiller Home Price Index for January.

The index is a good measure of “house-price inflation” because it’s based on the “sales pairs” method, comparing the sales price of a house in the current month to the price of the same house when it sold previously, thereby tracking the amount of dollars it takes to buy the same house over time.

But house price inflation is not included in the Bureau of Labor Statistics’ Consumer Price Index. While about one-third of CPI is based on housing costs, it tracks rents exclusively, rather than home prices. Even the CPI for “Owner’s equivalent rent of residence,” which accounts for about 25% of CPI, is based on homeowners’ estimates about how much their house would rent for. This CPI for “Owner’s equivalent rent of residence” ticked up only 2.0% year-over-year (green line), compared to the Case-Shiller Index, which soared 11.2% (red line).

The Case-Shiller Index was set at 100 for January 2000. So the national index value of 236 indicates house prices have surged by 136% since January 2000, including the plunge in the middle, which CPI for homeowners has risen only 72% over the same period. But for many cities prices have surged far more, as we’ll see in a moment.

So you know what’s going on here: the costs of homeownership are surging, but only a portion are included in our inflation measures, turning CPI as an estimate of the loss of the purchasing power of the dollar into a sad joke.

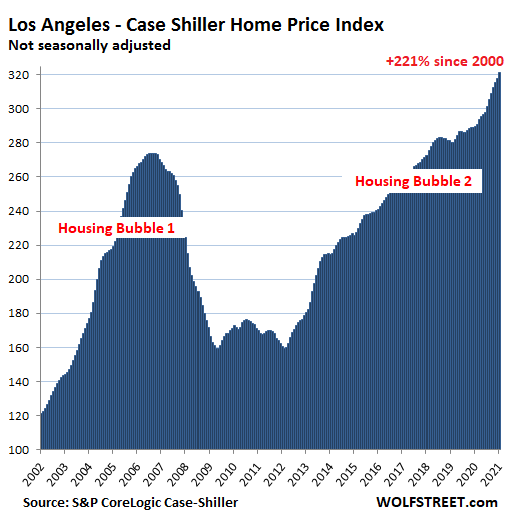

Los Angeles – the #1 most splendid housing bubble:

Prices of single-family houses in the Los Angeles metro rose by 1.0% in January from December and by 10.8% year-over-year, according to the Case-Shiller Index. The index value for Los Angeles of 321 indicates house prices in the metro have surged by 221% since January 2000, more than tripling in 20 years, thereby making Los Angeles the most splendid housing bubble on this list. Earlier today, I discussed the different trajectories of condo prices and house prices by price tiers.

All charts below are on the same scale as Los Angeles. As we go down the list, the amount of white space above the price area grows, showing that since 2000, the other metros have experienced less house price inflation than Los Angeles, though there was plenty.

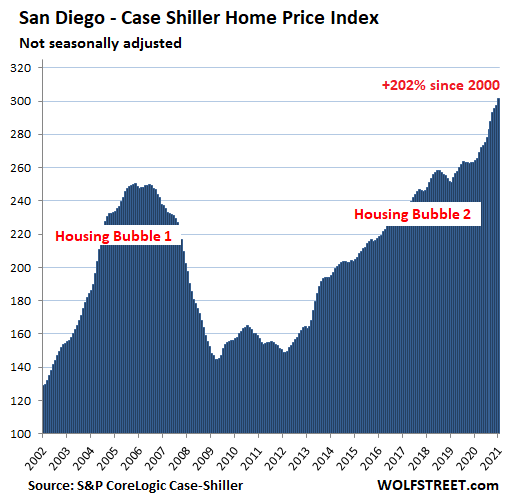

San Diego:

The Case-Shiller index for the San Diego metro rose by 1.4% in January from December and by a whopping 14.2% from a year earlier. Prices have more than tripled (+202%) since 2000:

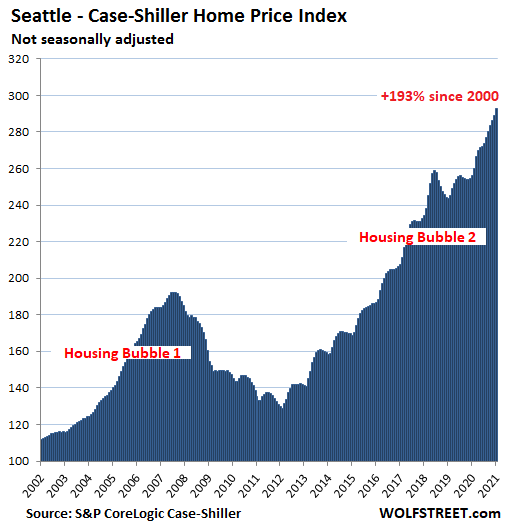

Seattle:

House prices in the Seattle metro jumped by 1.4% in January from December and by 14.3% year-over-year, making it the second fastest annual house price inflation among the Splendid Housing Bubbles here, behind Phoenix (15.8%, below):

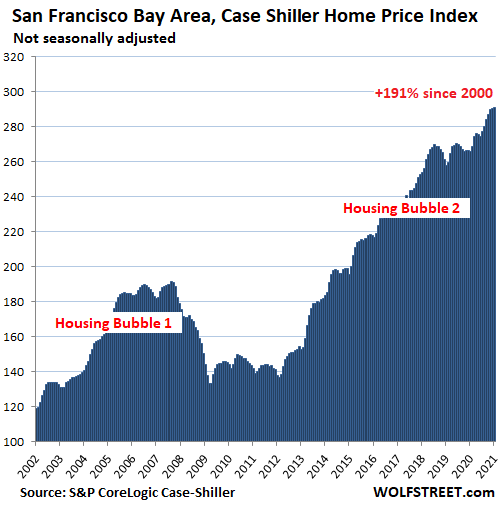

San Francisco Bay Area:

This is where condo prices fell back to 2018 levels, but single-family house prices rose 0.2% in January from December and 9.5% from a year ago, having nearly tripled since 2000. The Case-Shiller Index for “San Francisco” covers the Bay Area counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay):

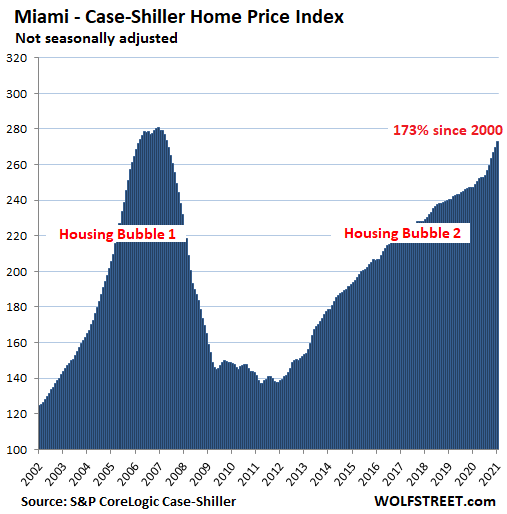

Miami:

In the Miami metro, house prices rose 1.2% for the month and 10.4% year-over-year. Though they’re up 173% since 2000, they remain just a tad below the crazy peak of Housing Bubble 1:

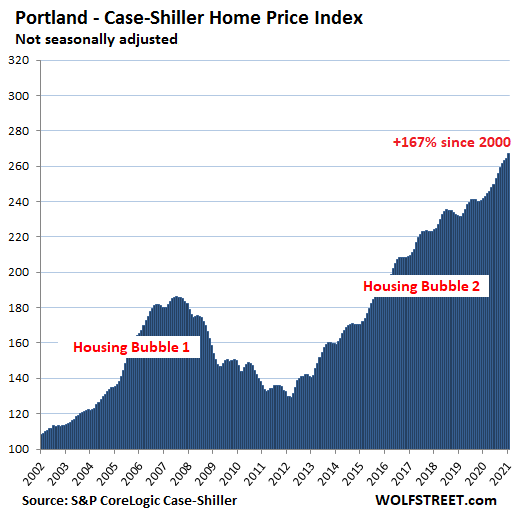

Portland:

In the Portland metro, house prices rose 1.1% for the month and 10.6% year-over-year:

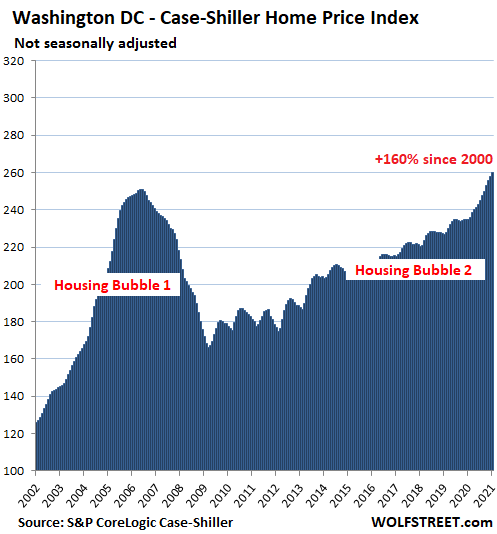

Washington D.C.:

House prices in the Washington D.C. metro rose 0.8% for the month and 10.7% year-over-year, having surpassed the peak of Housing Bubble 1 late last year:

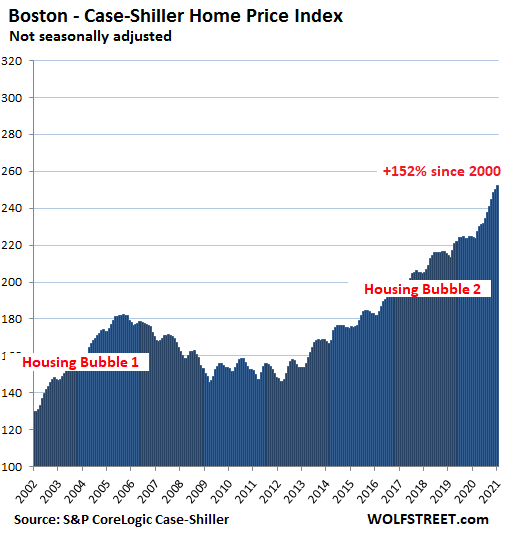

Boston:

In the Boston metro, house prices rose 0.8% for the month and jumped 12.7% year-over-year:

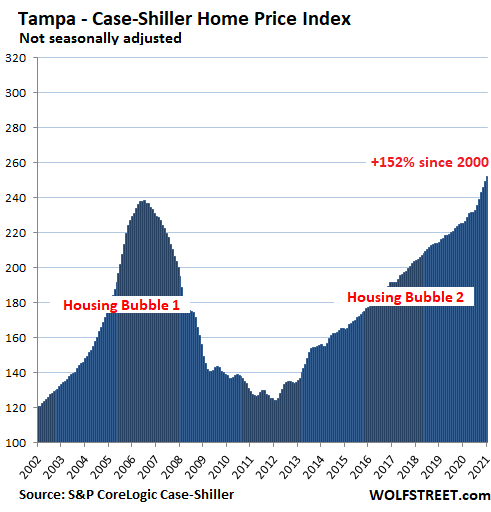

Tampa:

House prices in the Tampa metro rose 1.1% for the month and 11.9% year-over-year:

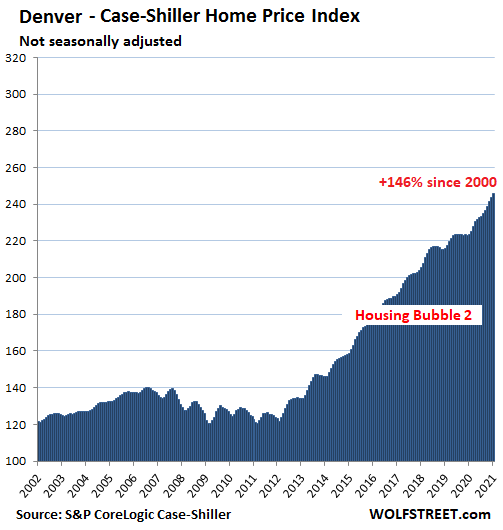

Denver:

House prices in the Denver metro rose 1.0% for the month and 10.0% year-over-year:

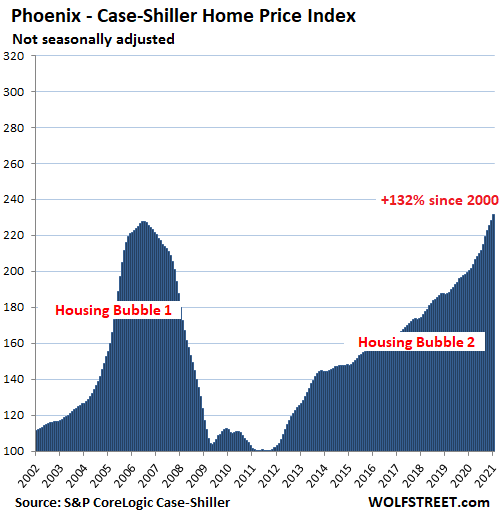

Phoenix:

House prices in the Phoenix metro jumped 1.5% for the month and 15.8% year-over-year, making Phoenix the market with the hottest annual house price inflation among the Splendid Housing Bubbles here, ahead of Seattle (14.3%) and San Diego (14.2%):

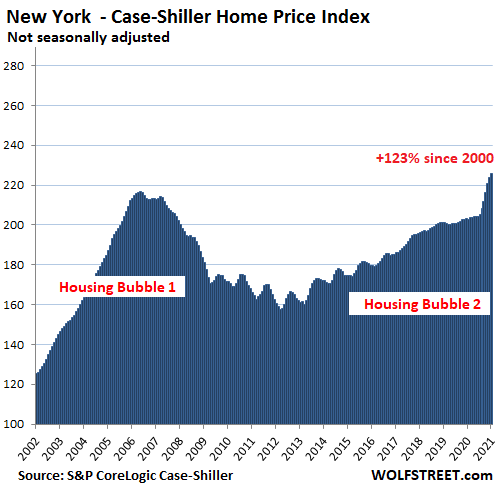

New York City metro:

House prices rose 0.9% for the month and 11.3% year-over-year. As I discussed earlier today, by price tiers, there were big differences, with low-tier house prices surging by 14.9%, but condo prices remaining in the same tight range for three years. The Case-Shiller Index for New York City covers New York City and numerous counties in the states of New York, New Jersey, and Connecticut. What a wondrous spike over the past six months:

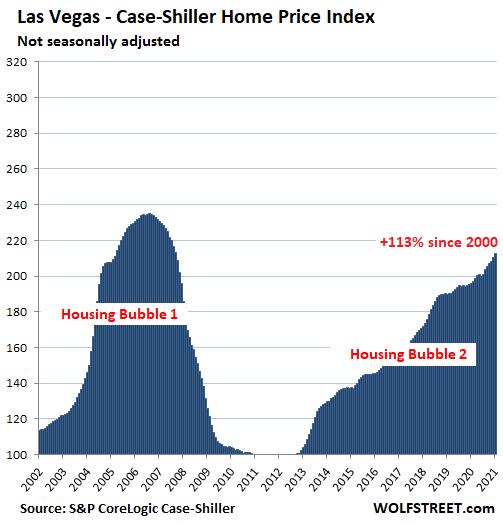

Las Vegas:

House prices in the Las Vegas metro rose 0.9% for the month and 8.5% year-over-year:

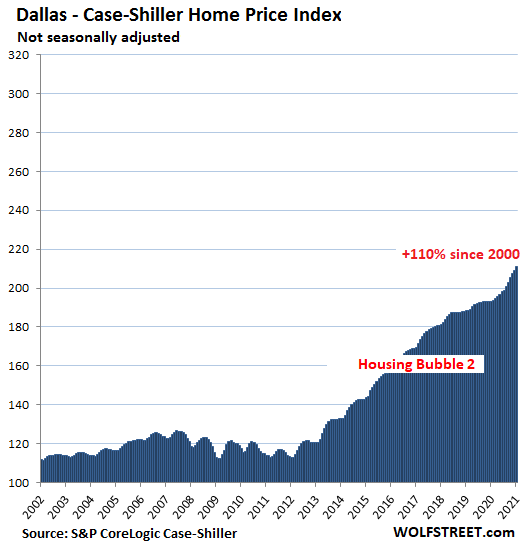

Dallas:

House prices in the Dallas metro – counties of Collin, Dallas, Delta, Denton, Ellis, Hunt, Johnson, Kaufman, Parker, Rockwall, Tarrant, and Wise – rose 0.8% for the month and 9.2% year-over-year, and are up 110% since 2000, meaning house price inflation totaled 110% over the past 20 years. In the remaining handful of cities on the 20-city Case Shiller Index, the 20-year house price inflation has been less than 100%, which makes Dallas the last entry on this list of the most Splendid Housing Bubbles:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The only “graft” missing is one showing the Fed’s money printing!

Every one of those charts remained me of Camel humps. With the statement below though and Uncle Jerome telling the public they are willing to get inflation run a little hot and doing everything in their power to keep those interest rate low low low. I am having a hard time imagining a scenario how home price will adjust down in a big way. It’s insane to have 10-11% in couple of months but it seems like in the last couple of years, we have been on this pattern of once it goes up it stays up type of climate and us bubble watchers looking like real idiots. I really want to believe and hope there will be a crash or major price adjustment but I think I probably would have better odds at this point betting aliens will invade us first before this insanity is ever over..

“But house price inflation is not included in the Bureau of Labor Statistics’ Consumer Price Index. While about one-third of CPI is based on housing costs, it tracks rents exclusively, rather than home prices. Even the CPI for “Owner’s equivalent rent of residence,” which accounts for about 25% of CPI, is based on homeowners’ estimates about how much their house would rent for. This CPI for “Owner’s equivalent rent of residence” ticked up only 2.0% year-over-year (green line), compared to the Case-Shiller Index, which soared 11.2% (red line).”

Before I found out I was being transfered to north Africa, I started hearing jokes about whether to rent a one hump or two hump camel from Hertz!

Phoneix, remain hopeful!

I posted the below response to one of your comments yesterday, on another of Wolf’s great articles, but maybe you did not see it.

“Based upon my recent research … the rapid technological advancements in 3D Printing of homes, buildings, walls, fences, pools, etc, will soon have a major impact on the costs of same.

It appears, said impact will be … significant reductions in the cost of new construction, thereby, causing significant decreases in the value of currently constructed/improved real estate.

I believe … you will soon be able to afford a reasonably priced “decent place to buy to raise a family without being in debt forever …”

It appears … 3D printed construction has several advantages over traditional construction, to wit, lower initial construction costs, much faster construction, more design options, stronger, more weather and fire resistant, lower maintenance costs, lower insurance costs, lower property taxes, less stress regarding all the aforementioned, etc.

I believe you would be wise to be patient.”

How do you achieve lower property tax?

Anthony, the below definition was obtained from Investopedia.com.

“Assessing Property Tax

Different property types have various types of tax assessed on the land and its structures. For example, vacant land will have a significantly lower assessed value than a comparable piece of property that is improved, and as a result, it will have lower property taxes. If there is access to public services, such as sewer, water, and gas, the land assessment might be higher. If the assessor feels that the land has the potential to be developed, it could lead to a higher assessment and more taxes for the owner. The amount that a property is taxed comes from a percentage of the assessed value of the property.”

Therefore, regarding 3D Printed homes … since the overall cost to build 3D Printed homes is less, property taxes, if assessed appropriately, will also be less.

As more and more homes, are 3D Printed for lower and lower costs, comparable improved real estate values should continue to decrease if assessed appropriately, and subsequently so too should property taxes decrease, unless the taxing authorities are able to increase the millage rates.

A millage rate is the tax rate used to calculate local property taxes. The millage rate represents the amount per every $1,000 of a property’s assessed value. Assigned millage rates are applied to the total taxable value of the property in order to arrive at the property tax amount.

Thanks, I looked up 3D printed homes and found out that it’s quite a neat concept. I didn’t realize that this technology existed for framing a home with concrete. It would certainly save on labor that would be used in traditional wood framing, especially if the cost is really that significant in the finished home price.

5 Deep Logic:

I looked up 3D Printed houses. They are almost 200K for less than 1000Sq.ft. Why are they considered cheaper?

Most of the inflation is in the lot price, not construction. But I still agree that housing costs will decline. Long term, cities will be obsolete (enabled by telecommuting, shopping, and home entertainment) and we will sprawl into the countryside. Birth rates are down considerably (Covid and generational values shift) so McMansions built over the last 30 years will be anachronisms.

Yup, still hopeful because of this site and others that are counter to the mainstream, lemmings narrative and can back it up with real data analysis. This is my support group here, it’s good to know there are others like minds individual that share the same view as myself. Call it cognitive dissonance, confirmation bias whatever you will…but when 2 + 2 not adding up to 4 like what we are all seeing with this housing and stock market, the stubbornness in me just won’t allow me to fall in line and turn into another FOMO buyer. Perhaps this time might truly be different but as I have always said before, at some point you kind of have to question what you get for what you’re paying for. Paying $800-$1M for a taco tuesday crapshack in a crappy school district is not exactly my idea of value.

Phoneix, what you describe as your “stubbornness” may in fact … be wisdom.

Example … I live on the North Florida coast. About five years ago, I purchased a vacant lot, for 98+% … less than … the same vacant lot sold for in 2006.

Yes, that is correct, 98+% … less than … the same vacant lot sold for in 2006. It is also high and dry, and will not require flood insurance, if improved.

Also, there is no scarcity of land in America ( other than coastal areas ). So I guess over time cost of houses should go down because of technological advancements.

Jerome “Weimar Boy” Powell sees no sign of inflation anywhere. In fact, he tells us he stands at the ready to “provide more support” if necessary. Why has this economic terrorist not been arrested?

Jerome “Weimar Boy” Powell..I like that nickname. Truth of the matter is, when people look back at history, he will somehow be view with rose tinted glasses as another champion and savior to the system, much as people still idolize Greenspan or Milton Friedman. Yet these characters have created untold amount of damage to everyday Americans and people around the world that arguably makes Trump’s transgression pale by comparison.

No, he will not be treated kindly by history. No central banker who causes hyperinflation is.

Why are you putting Friedman in the same category as Greenspan and Powell, Friedman was a great economist and wanted the abolition of the Fed till the end.

Friedman believed that the only responsibility of a corporation was to maximize profits. Low interest rates and money printing so far have been good for corporations who seem to wholeheartedly support what the fed is doing. When’s the last time you heard one speak out against the fed? There’s probably an army of lobbyists begging for the fed to backstop federal spending so they can get their bailouts from their bought out congressmen and keep ramping their stock to infinity. Was Friedman dumb enough not to see the extent to which perverse incentives would lead to what we have now? Or would he slap Jerome on the back and say well done, an excellent wealth transfer. Either way, that makes him just another tool of the corporatocracy.

Friedman and the chicago school were/are wrong about much.

I think the fact that you mentioned Friedman being remembered as a great economist proves my point about some of these terrible people in charge of power and ideas will remembered in a positive light regardless of how much damage they indirectly inflict to the general public.

Sure Friedman was never a FED chairman but keep in mind Greenspan was influenced by his thinking. If you want to talk to about how much harm Friedman inflicted on the world, especially South America, just go read Shock Doctrine and you get to see exactly how much “positive” influence him and his Chicago boys unleashed to the world.

Friedman, the great libertarian, invented the income tax withholding scheme in WWII.

He was part of the problem, not the solution.

Friedman did everything in his power to help crush Germany. Despite now being a member of the pro-free market Chicago school, Friedman helped create the withholding tax which libertarians consider the most destructive tax of all.

From 1941 to 1943 Friedman worked on wartime tax policy for the federal government, as an advisor to senior officials of the United States Department of the Treasury. As a Treasury spokesman during 1942 he advocated a Keynesian policy of taxation. He helped to invent the payroll withholding tax system, since the federal government badly needed money in order to fight the war.[37] (Wikipedia)

“We won’t take the punch bowl away” because it creates millions of jobs.

Fed Weimar Girl Mary Daly of the San Fran Fed.

It just creates gobs of new millionaires and billionaires.

Yes, until the ice melts in that ‘Bankster of banisters’ commode .. leaving what’s left as a putrid, bubbly, stinking financial bacterial soup thats waaaay past healthful consumption for anyone sane enough to smell it!

Bankster of “banksters” ….

Housing market $38T plus stock market $51T is being supported by $11T of monetary plus fiscal magic money in 2020 – 2021. Value of it all is determined by a handful in DC. Scary times.

I do like Munger’s thoughts on stocks, but it’s probably true for a home. If you buy stock in a great company, it’s OK to hang on to it even if it gets over valued.

As house prices increase so do taxes perfect way to get stimulus money back

RE taxes are State, Stimulus is Federal

Actually, there isn’t a direct correlation. Real estate taxes are based on the government budget, so RE taxes increase only when the local government budget increases. Housing prices are simply a way to allocate the RE tax across the population.

If your property appreciates the same as others in the area, the appreciation will not necessarily increase your RE tax bill.

The wealthy home owners win again!!

If the mill rate stays the same, your taxes will increase in tandem with property appreciation.

Harrold, the mill rate is simply an apportionment factor, a way to allocate out the total pie to everyone. It isn’t fixed from year to year.

What Bobber said is correct, and so many people don’t understand this concept. His explanation should be auto-inserted anytime a comment about property taxes appears on this forum. That’s also why property taxes won’t necessarily decline if housing prices crash. Your taxes will only go down if your house value sinks more than others in your district. And in years with huge price spikes like now your taxes won’t necessarily go up, unless your home value goes up a larger percentage than others, or your voters approve increases to your govt’s budget.

We are retired living on a fixed income (SS + savings). Over the years we have bought 9 houses due to work moves. We are in the last one and glad we don’t have to replace this one. We are in a 55+ community of 437 single family brick and hardiplank homes north of Houston, Texas ranging in size from 1,700 – 2,800 sq. ft. These homes were selling in 2020 for ~ $125 – 130/sq. ft. and probably sill are in that range. We are in a fairly high cost of living area.

We lived in Thousand Oaks, Ca in the 1980’s. The NEWLY BUILT home that we bought there in 1987 cost $229,000 and was 2,600 sq. ft. Today that house is $1.4 million on the real estate websites. We left Ca in 1992 and during that period, there wasn’t any big run up in price when we sold.

What’s going on now with speculators will end, and maybe badly.

“What’s going on now with speculators will end, and maybe badly”

I sure do hope so but in a country that’s aggressively fostering moral hazard as the norm and hold gangster capitalism as the ultimate gospel couple with power to create as much money as possible out of thin air by the FED…I am not holding my breath and each day my hope for that to happen dwindle ever more so

It is very easy to take on debt. Especially when you believe what you are buying is skyrocketing in value.

It is very hard to pay that debt off.

This bubble like all bubbles will pop, because it is based off poor fundamentals. NO one is paying these prices because they are committed to living in these houses regardless of its future value.

They are paying these prices because they expect prices to continue to increase making them money.

At some point, that will fail, and they will realize they are holding a million or more dollars in debt, on about a hundred thousand worth of lumber, drywall, and cheep particle board cabinets, on a postage stamp lot…

The housing bubble had a lot of speculators and a huge excess of housing inventory. This time we probably have the lowest inventory ever and lowest rates ever.

The city I live has about 150k people. City-Data says the median priced home was $272k in 2019. I took a look at the inventory yesterday. Right now there are only 2 homes for sale under $270k. There are only 120 homes for sale and 100 are new construction. So a city of 150k only has 20 detached resale homes for sale. Now there are about another 100 condos’s/duplexes for sale. Thus everything is going over asking price.

All the new contraction homes are over $400k and are the 3000 sq ft McMansion. No starter homes anywhere.

So I do not see inventory getting any better anytime soon?

I do see a lot of apartments being built.

I think a home builder pinned the current housing environment recently on a earnings call.

Owning a home will be a luxury. That means many people will have to live in apartments…etc. Why…we are seeing asset prices like homes go up but income is not rising much.

.

If house prices go up ten percent but the price of money goes down ten percent, does the monthly payment or anything else important to the consumer change?

But if interest rates then bounce up, fewer people will be able to buy at current prices and those that have to sell will take a loss.

So a lot of risk.

Not a good time to speculate.

.

One way market due to forbearance/moratoriums, with low supply and ample subsidies. Perhaps shocking it isn’t going up faster.

All extended until at least mid-June. Feel sorry for anyone trying to buy.

The Fed has been targeting higher stock and housing prices since (at least) 2010. I would add that the Fed has been blowing bubbles since at least the mid 1990’s: 1) Dot com (tech) bubble, 2) housing bubble 1.0, 3) everything bubble. The first two bubbles burst, as asset bubbles always do. Some think “it’s different this time.”

What the Fed did and why: supporting the recovery and sustaining price stability

By Ben S. Bernanke

Thursday, November 4, 2010

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action.”

“Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance.”

“Lower corporate bond rates will encourage investment.”

And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

“Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

http://www.washingtonpost.com/wp-dyn/content/article/2010/11/03/AR2010110307372.html

“Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

Higher income my rear end. What a bald-faced lie, typical of these scvm. Wages have been falling. Bernanke should be near the front of the guillotine line.

“And so with Princes of the Yen, that cover was blown. And I think people were not happy about it. Also, the other thing, particularly in America, they didn’t like is that the original edition, 2001, I don’t think you’ve read this. Because it came out first in Japanese, 2001. And it had a chapter about my meeting with Alan Greenspan, when I met Alan Greenspan, and we discussed my paper that he had read four years earlier, which he remembered extremely well. And from the somewhat surprising things he said, I concluded certain things. And it’s written up in this chapter. And this was predicting the conclusion was– well, the Federal Reserve is going to do the same thing as the Bank of Japan, which is intentionally create a massive asset market bubble driven by bank credit creation, which is going to create, when it blows, the biggest financial crisis, a global financial crisis. And that’s, of course, the 2008 crisis, which Alan Greenspan did create.”

https://www.realvision.com/rv/media/Video/9086e3c7668e479ebebbd0f5396e70f7/transcript

The Fed supports the banking system. The banking system loans money based on asset values. The higher the asset values, the more money the banks are able to loan, and the more money they make.

It is therefore profitable to inflate asset values.

This means in reality, perceived asset values are not necessarily in line with intrinsic asset values.

There are two basic problems with artificially inflating asset values.

The first is, that once it begins, it tends to gain momentum until it becomes an irrational mania.

Second, over leveraging tends to cause ever diminishing returns in productivity, making it mathematically unsustainable.

This means that at some point in the cycle, a crash is necessary in order to wipe unsustainable debt off the books, and to revalue assets, at which point the cycle can begin again. Many debtors get wiped out, the banks get bailed out, and ever more wealth gets transferred from the working to the upper class.

And then, once the rich have accumulated sufficient wealth, they are eaten by the starving poor, irrespective of any efforts on their part to maintain their status and wealth. This last step is erratic and hard to predict, but moves with the weight of a nation when underway.

Either that, or wealth is then destroyed as the rich fritter it away in wars between themselves.

Just look at the source “The Washington Post”, and you know that everything said is a pile of Bull S$it.

there is no increased spending, people are fearful and hoarding cash, the velocity of money is at a historic low

What should I do in Denver to get back into a home? Try to buy a home in the bidding wars against the new transplants that are flocking here or rent and ride out this storm? And for how long if renting?

I have 60 days until the rental I’m in goes up for sale. It’s value is now over $700k. As a nurse I cant afford it.

Look, if everyone goes on a buyer’s strike for six months and doesn’t look at houses, and doesn’t click on real estate ads, and doesn’t look at real estate sites, the whole schmear would come down. Then you’d have SELLERS getting desperate and out-price-cutting each other.

It’s the silly buyers with FOMO out the wazoo that are causing this.

Agree with this, Wolf! These buyers are greedy and banking on appreciation.

Saw an interesting comment recently that real estate is the easiest access to conventional markets for illegal money because it’s not scrutinized like investments into stocks, bank accounts, or even cryto currencies..at least in the US. Most of the markets at the top of the list are entry cities closest to foreign investment..interesting

They’re getting tons of appreciation though.

The government is adding tons of money. The proles get small amounts but further up the chain people are getting tons of money from this stimulus.

With the housing prices jumping so much I feel like I need to look for another job that pays better. I’ve heard competition is pretty strong for those with skillsets in demand.

“With the housing prices jumping so much I feel like I need to look for another job that pays better. I’ve heard competition is pretty strong for those with skillsets in demand.”

Which is why I am drastically raising my rates this year. 50%. I’m not going to get left behind. If people can pay that much more for a house, a car, an RV, etc., they can sure afford to pay me that much more. My rates will reflect what it costs to buy a house in this environment.

True, but what are the odds of a buyer’s strike, Wolf?

Katie, personally if you are not an owner now, I would find another rental and wait it out for a bit. I don’t think we’re going to see anything like a 40% 2007 crash, but 10-15% seems reasonable and on a $700K property that would equal $100K savings.

I sold a home in late 2017 – lived in it for 5 years and was investment (big house in top school district here but too big for one person 4,000 sq ft) I was planning to buy in March 2020 and then covid hit so renewed lease for 1 year. Now prices are higher and inventory even lower.

Wolf, I’m in the Bay Area and I’ve thought of the strategy you mentioned. How can a group of buyers come together and beat this market by refusing to play. This needs to be a collective effort, similar to Reddit/game stop. We can beat them at this game. Maybe I need to start a movement?

This week, my husband and I decided to tap out of this insanity for the sake of our own sanity. We’ll pull back in later this year. Right now, I refuse to make a purchase based on fear and FOMO! I’m hoping others will join us in our effort to flip the middle finger to this madness!

I’m in!

Just told our realtors last night we are not going to see any houses during this insanity.

Have been looking for years with increasing purchase prices but every time we save a bit more, prices go up by 5x more.

The problem is some people are making easy money and don’t care about the high prices. The prices aren’t high if you just made a million or two in stocks/crypto.

It would be fun to get a buyer strike going and a renter strike, but not sure how you can get everyone to play along.

Wolf,

I wonder if buried somewhere in the Case Shiller stats are the *transaction volumes* supporting the price index numbers from yr to yr.

It is one thing having 500k sales propping up LA home prices, quite another if it is just 5k.

The former bespeaks depth of demand at a highly elevated price, the latter bespeaks thin, brittle price support.

Since Case Shiller uses matched-pairs (wisely for certain purposes, but perhaps less so for others) I imagine that the transactional *volume* used to generate the price level is perhaps low (only “matchable” current sales get used).

Again, if the volume used to measure price is thin, then the reported price is likely brittle (because fewer sales means weaker representation of overall demand/supply).

Annual home sales in CA post 2006 were maybe 60% of the volume of the 2006 peak, although I’m not sure of 2020 numbers.

And I don’t have metro by metro volume stats.

cas127,

The number of “sales pairs” is the volume indicator, meaning how many sales in the current month were matched with a prior sale and qualified for inclusion in the index. A sale has to pass some hurdles before it is included, for example it cannot be a sale between related parties.

In the current month (January) for Los Angeles, in terms of houses, 8,507 sales pairs went into the index, up 21% from January a year ago. And in terms of condos, 3,864 sales pairs went into the index, up 24% from a year ago. January/February are seasonally the slowest months.

Yeah, Wolf. We’ll just tell everyone to stop buying for six months, and don’t click on real estate ads, and don’t look at real estate sites so the “whole schmear would come down”.

Stop buying everyone, and ……!

There. We tol em. Lol.

But think of the realtors commissions!!! What will happen to this group of wonderful people?

@qt: what I used to say when I lived in California when the housing circus stopped for a while was that the RE agents will just go back to playing tennis every day.

While a nice fantasy, it won’t ever happen. Even if those looking for a primary residence all got together and did what you suggest, you don’t think the corporate and investment buyers wouldn’t swoop in and outbid you anyway?

A house is a moneymaker and with so few places to make a profit on investment these days they have become a financial instrument for the moneyed set and I don’t see this changing.

Once housing became a financial device the game is over and while people will still buy houses to live in the fact is that there is so much profit in rentals and appreciation that things have changed and they ain’t going back.

Even a housing crisis like the last one only gave a short-term break, but interest rates were a lot higher and who bought all those houses? Blackrock and others.

Bob Jayco,

If 20% of the potential buyers walk away, the market would spiral down in a New York minute. Maybe 10% walking away would be enough to change the psychology of the market.

Is the declining sales of homes due to interest rates, lack of interest or just that so few homes are coming on the market?

It seems that anything, almost anywhere is selling very fast with over-asking prices so I don’t understand how sales are declining unless there is just nothing more to sell.

Perhaps more people are less inclined to move right now until things settle down a bit.

I don’t see lack of interest and in fact feel like there is a rush out of cash into a hard asset to offset inflation.

“Even if those looking for a primary residence all got together and did what you suggest, you don’t think the corporate and investment buyers wouldn’t swoop in and outbid you anyway?”

Outbid you on what? You’re not bidding, that’s the point. Your bid is zero, and so is the bid of everyone else participating in the strike.

The problem is sellers holding two or three houses, off the market. Nothing feels better than sitting on an asset and watching it grow. Wouldn’t want to own a rental in this market, while underlying value rises faster than my tenants ability to pay. I would consider increasing the number of units, by downsizing them. Turn a duplex into a triplex. Too small for you? There are some places with your old sq ft down the street, at twice your old rent.

I just think that with the present inventory being so depleted, any pause by buyers would be more than made up by corporate, or even affluent buyers, that would take advantage of the pricing change.

Even if a decent percentage walked away, as soon as the prices dropped, if they even did, you would see a mad rush to buy before the rest came back bringing the prices right back to where they were or even higher.

There is simply too much money out there looking for a place to come to rest and housing has proven itself to be a great place to be if you can afford it. And as long as a certain group can indeed afford it, even at these prices, it will continue to be in great demand.

Historically housing has gone up over the long term and I think it will always follow that trend, though there will certainly be short term dips now and then. More people, more demand for homes in better areas, higher rents will always drive the prices higher long term. And so the prices reflect that.

Bob Jayco,

Sales have been declining so far this year. Pending sales out today were down over 10%. Existing home sales reported earlier this month dropped 6.6% and have been dropping since late last year. New house sales plunged. There are all kids of reasons for this, two of which are buyers losing interest and rising mortgage rates.

It is the perfect time to own rentals. People need a place to live and if they can’t afford to buy they will rent. Value of asset doesn’t matter or change anything. If your costs are covered you don’t have to increase rent to anyone.

“Nothing feels better than sitting on an asset and watching it grow”

Especially when someone else is paying for it for you.

Or we could, theoretically, get our government to stop screwing with things in 50 different ways, and allow price discovery to work its magic. Buyer hysteria is real, but everything else is government manipulation.

I sold my house and moved in with in-laws. Will the bubble pop, or simply continue to eat away at my nest egg? Who knows.

yes Wolf. that would work. This suggestion reminds me a few years ago when gas prices were too high (for the times back then) there was a movement of sorts in SoCal, that one day of the week no one should drive. That will reduce the demand for gas and bring the prices down. It worked to some extent,

But in these times who wants to “miss out” in real estate especially if they are sitting on a pile of cash?

Just like when all the toilet paper, hand sanitizer and pasta was flying off the shelves last year when Covid hit.

Keep renting and banking that nurse salary, Katie. Buy yourself a little vacation or something if you are feeling stressed. Don’t get sucked in!

I’m also in the same exact boat, within the Denver metro market. To answer your question, wait it out. Fomo never leads to a good decision. Buying for emotional reasons, fine if you can’t take the FOMO, but if you are buying as a financial upside – you can get better ROI playing your finances correctly and investing in the stock market, index funds, maxing out the Roth ,etc. I know it feels like you are missing out especially in CO but I think the more you read this website and the great contributors who are all doing really well off – the collective narrative is to wait.

Not sure that there is any way to “correctly” invest in the stock market at these valuations.

I refuse to pay $100 for $2.50 worth of earnings. That’s what you’re doing right now if you buy indexes.

@katie-

>”…or rent and ride out this storm?”

At this point, rent.

Remember that the more you pay today for an asset means lower long term appreciation. Buyer’s remorse is real.

I swear it sure feels like a support group in here when I see comments like this. Guess for every 10 FOMO buyers eating up the mainstream or RE narrative, there are people like you and I gawking at the absurdity with contempt.

Maybe the tide will turn at some point or maybe it won’t. As I have said many times before, you start to question your own stance when everyone else is repeating the complete opposite. Good that at least Wolf provide some real data to reassure us that not all are buying into this BS

Phoenix,

Just to ride along on part of your comment: “Maybe the tide will change …..or maybe it won’t” Ah, therein lies the rub. One could end up like my 81 year old tenant. Sometimes, we sit together and have a few glasses of whiskey. He likes to reminisce about our area, “I could have bought George’s place across the river for______, or I wanted to buy _________, used to own a lot but sold it”. etc etc etc. Now I rent him a cottage for a 30% discount on the local market because he is my friend and a senior. Before that I found him an empty house (shack) on my son’s property and then built the cottage. He had been evicted from his previous home because the owner wanted to develop and sell. Years later he told me he was going to kill himself at the time. He had made a plan to get into his tin boat and die of hypothermia (supposed to be a gentle way to go).

Owning a house isn’t just about numbers and investing, it is a home and part of a plan. A long term plan. I agree that as the largest investment a working person will likely ever make, a house purchase should be done in a careful and deliberate manner with attention to known details. But…and here is where I differ from many WS readers…it should be done long before developing investment portfolios, buying a flash car, or taking expensive vacations. As a lifestyle choice, owning a home is more important than dining out or hobbies. Just ask my tenant.

I also said and say, “Probably not a good time to buy”. But damnitall, I said that 3 years ago, too. :-)

Picked up some building materials, yesterday. My price for fir sheathing, (and I get a good price discount), was up 300% from 4 years ago. Ouch, and bought what I needed.

Paulo,

Excellent points and I agree fully.

A couple of added points:

1) You may have to take some risk and initially invest to reach a down payment on a house and a cash cushion. 0.1% in the bank will leave you behind.

2) Have a 1-2 year cash cushion so you are not foreclosed upon when the inevitable recession hits. Don’t be a Nomadlander by force. IMHO, having a year in cash making 0.1% is better than losing it all with a foreclosure and a wrecked credit score which will likely destroy any chance of you buying another home during the best times to buy.

3) As you pointed out, a house is a long-term investment in your future security. Buy a house you can live in for at least 10 years. If it goes up and you can ladder up, do it. If it goes down, you still have a house you can live in for at least 10 years with a fixed payment. Your 81 year old friend/tenant is very lucky to have you as a landlord or he would be a Nomadlander.

I’m like you. I thought the peak in home prices was years ago. I was wrong. Am I still wrong? That is a longer debate to have.

Right. It’s like the “elites” are gaslighting us, with the help of the FOMO buyers.

We owned 3 houses in 2007, they all cut in half in value by 2010. It took until 2018 to recover.

We were preparing to buy in 2018-2020 then this COVID nightmare happened.

We are still shopping but we are signing a new lease and are waiting until things normalize. It is a bad idea to have two mortgages. Most people with 2 mortgages can’t afford both. One bad tenant, one increase in taxes, two months of no rent…. it is rough.

The smartest people I know say not to buy now.

Hernando, in 2010, we bought a 2,000 square foot brick ranch that was three years old in a great neighborhood for $62/sq. ft. People tend to forget that back then, right after the GFC, empty house were all over the place. Lots of foreclosures, bank REOs, private sellers, etc.

My daughter and her husband live in that house now and the one next door (same size) sold last summer for $262,000, a full price offer.

Hang loose and when this bubble pops, it will be very loud!

I really like the free on-line rent vs buy calculator by Michael Bluejay. I would do at least five long term scenarios from inflationary to deflationary. Print out results and study carefully to understand possible outcomes of buying vs renting.

Home purchase is so rare for most of us, we do a poor job on decision making process. I think most people under estimate risk they are taking in holding a stock portfolio or buying a home. You will probably have to hold both through a severe price decline at some point.

Some housing markets are just not good deals where supply is too tight and then you just have move to a different housing market where your income buys more.

They, (the infamous they), have done studies on home buying habits. This what I read. The average home buyer makes an emotional decision about the house they are buying. Often, they have made a subliminal decision to buy within the first 20 seconds of viewing. People spend more time buying a new outfit than they do buying a house.

Mix in fear of losing out, fear of interest rate rise, whatever, and here we are.

Good point. And it’s not like realtors don’t work this angle.

I remember a home we sold in Livonia, Michigan in 1975 after I got a job transfer. My wife had just wallpapered the 1/2 the small kitchen (above a chair rail) with some crazy wallpaper with colored balloons on it. I told her we should strip it off. (not happening !)

A couple who were stopping by to look at the house went in through the side door which was into the kitchen and the wife said to her husband, “I love this kitchen with the beautiful wallpaper”, and BINGO, they immediately bought the place.

Yep, that stuff happens.

Anthony, and I’m sure your wife never lets you forget it :)

Like all the other posters, I suggest you continue to rent and wait.

Just had a young lady on reddit from and still living in Venezuela. An economics student. Answering any questions and all questions in group called silversqueeze. Someone asked, buy a house because of inflation coming to U.S. She said better yet, buy cheap silver now and buy house later. She said in Venezuela housing prices had come down in relation to silver and or the dollar for now. You can buy a nice house in a safe neighborhood for $30k American. So not if but when inflation hits America, against silver housing prices will fall. Bottom line. Rent, take your money buy physical silver now and house later. Of course do 401k up to company match as it is an immediate 100% return.

I refuse to hand $10 to the coin shop for every ounce of silver they sell me. It’s ludicrous to pay a 40% markup. That’s not “cheap” at all. The time to buy was 2 years ago.

Depth Charge: How about buying a 1 Kilo Bars or higher denomination? for higher denomination Silve, you would spend less premium. Same thing is true for Gold as well. If you buy the “premium american eagle or such” your premium is higher than, if you just buy a 100gram Gold bars.

Condos and apartments might be (slightly) undervalued relative to houses right now, given how many people in condos were so eager to have access to a yard starting a year ago. That said, location, southern exposure, neighborhood, and how much time you want to spend at Lowe’s/Home Depot doing home Reno/fixing up/YouTube learning matters as much as the financial viability. As does your willingness to make “lowball” offers and see what happens.

I’ve been waiting for (and trying to prepare for ) the big crash for years now, and continue to be “wrong”. My wife has kept us on a more “middle of the road” path.

A correction/caveat: if I were you I would wait until late summer or this fall to see what happens with the market, in regards to foreclosures after the moratoriums end.

It depends on your time horizon and stability of your income. On a 20 year time horizon with a stable income/job, it would probably be OK to buy. If 5 years and/or less certain job, better to rent. I also live in Denver and before that, SF, there is no conceivable situation where a home purchase in Denver isn’t appreciating in value in 20 years. But 5 years, yes, anything can happen.

I know many, many people who have been waiting here for 5 years for the bubble to pop, they have set themselves back 40 or 50% by that wait. I watched people do same in the Bay Area in the 90s, eventually there is an opportunity, but it might be many years and another large tick up in prices. This is the Fed’s doing.

Comments like this about many waiting buyers tell me that there is a much greater chance any drop in prices will be short lived. Add to that the trade up buyers and asset bubble creation by the Fed, housing will up continuously even with multi families sharing the home. Like the old days when large homes were to converted for extra residents.

The Fed = Wile E. Coyote, Super Genius.

Article

The Full Case Against Ultra Low and Negative Interest Rates

By William White

Mar 17, 2021 | Macroeconomics

“However, debt accumulation is not the only unintended consequence of relying on monetary stimulus. Such policies also threaten financial stability in various ways. They pose a danger to the survival of financial institutions and to pension funds by squeezing net returns on traditional assets.”

“Moreover, institutions subject to such threats then “reach for yield” in an attempt to compensate, often leaving themselves open to risks that they had not anticipated and have no experience of managing. A related concern is that of growing “moral hazard.” Every time a problem materializes, the central banks or regulators create another safety net to protect the exposed, which then encourages them to behave even more badly.”

“Similarly, unusually easy monetary conditions over long periods can threaten the effective functioning of financial markets. In recent years, we have documented: recurrent “flash crashes”; waves of Risk-On and Risk-Off behavior; persistent “anomalies” from normal price relationships; growing evidence that normal “price discovery” has been suppressed; and finally, the near-collapse of the US Treasuries market in September 2019 and March 2020.”

“Moreover, easy monetary conditions lead to continuing increases (bubbles?) in the prices of virtually all financial assets and often to real assets (like houses and other property) as well. For a long while, these price increases can mask the other undesired consequences of easy monetary conditions but, as “fundamentals” eventually reassert themselves, a price collapse can easily follow.”

“Another side effect of easy monetary conditions could be a reduction in potential growth rates. The possibility of “malinvestments” and wasted resources was raised by Friedrich Hayek in the 1930s and has also been treated increasingly seriously by the BIS, OECD, and IMF in recent years. A well-functioning economy, with expanding growth potential, has ample room for companies to both exit and enter. However, there is growing evidence that easy monetary conditions discourage both processes from working effectively. In many counties, the birth and death rates of companies have in fact been falling sharply as indeed have measures of productivity growth.”

“Nor is this the end of the list of unintended consequences. Easy money in advanced countries spills over into emerging market countries threatening them with the same kind of distortions and exposures. Rising inequality, especially in the distribution of wealth, can have important social and political implications.”

https://www.ineteconomics.org/perspectives/blog/the-full-case-against-ultra-low-and-negative-interest-rates

When Money dies by Adam Fergusson

When Money Dies is the classic history of what happens when a nation’s currency depreciates beyond recovery. In 1923, with its currency effectively worthless (the exchange rate in December of that year was one dollar to4,200,000,000,000 marks), the German republic was all but reduced to a barter economy. Expensive cigars, artworks, and jewels were routinely exchanged for staples such as bread; a cinema ticket could be bought for a lump ofcoal; and a bottle of paraffin for a silk shirt. People watched helplessly as their life savings disappeared and their loved ones starved. Germany’s finances descended into chaos, with severe social unrest in its wake.

Free copy: http://ibooko.club/go/read07.php?id=B0042JSRU0

With regards to the first chart one can see that at the market top, back in 2006 the delta between the CS NHPI (red) and the CPI OERR (green) is about 65 points. Today, the delta is again, about 65 points. Based on the historic relationship between the two, perhaps we’re nearing a top, at least at the national level.

In addition, that chart shows that the CPI OERR (green) acted as a kind of support level for the CS NHPI (red) as the market bottomed in 2012.

For those who want to buy but are waiting for a correction perhaps a good indicator of an impending bottom would be when the red and green lines converge.

I live in the Portland metro region and bought my house back in 2000 and paid it off in 2008. Compared to SF, SD, LA and Seattle, Portland is at the low end as far as west coast metropolitan real estate is concerned. Makes me think that if there is a crash, it won’t be as bad here.

Two things to consider:

A local San Diego realtor took the time to figure out the annual average increase in housing prices here from 2004 to 2021 and it’s 3.58%. Remember what advisors used to say about holding for the long haul? This isn’t a huge increase and definitely isn’t a huge or abnormal amount. Now if you’re leveraging you stand to make a lot, but over the long haul this is a pretty normal yearly increase.

I’m sure FOMO and other things are in play here but could it also be that folks are afraid of losing wealth with the way money is being printed and magically disbursed through out the economy. Hard assets, in my opinion, are the best way to keep even and stay ahead of the dilution, at least the safest; again, just my opinion.

On a side note, my sister in law has to vacate her Sacramento home because an investor form China came in with all cash. I can only assume that the well to do over there are worried about the diluted dollars, too.

OK, tell your Realtor to cherry-pick a different start date next time. From the end of 2005 through January 2021, there was even less annual appreciation. But over the past 10 years, there was massive annual appreciation.

Since 2001, the annual “appriciation” in San Diego ranged from +26% in 2004 to -25% in 2008. If you don’t choose your start date correctly, you’re in trouble. And looking at the chart right now, I cannot image a much worse start date.

A local TV station did a blast from the past report and replayed a five part series of the housing market in San Diego in 1979. This was post getting off the gold standard and pre S&L crisis. History repeats itself and will always do so. This time has people scared they’ll miss out just like they were in the 70’s (just add a zero to the end of the prices then and here we are).

I’ll include the link to the channel 8’s report, which links to the videos and let you decide if it’s worth keeping up for folks to see. It was really fascinating.

https://www.cbs8.com/article/news/local/zevely-zone/san-diego-real-estate-prices-1979/509-dad8918e-3d96-46b0-b0ab-ae3e0e46c661

Help me out people! I live in LA. I own an 830″ condo worth $550 K. I would like to sell and buy a bigger place. If I sell now, rent for a bit and then prices drop I’ll be happy, but if I sell, rent for a bit and prices still go up I’ll be screwed. Also, if I were to rent for a long time I would be paying someone else’s mortgage and I don’t want to do that for too long.

All thoughts are welcome!

If you use a good rent vs buy calculator it will help you get your head around a complex situation where the possible outcomes are many. Like stocks your time horizon is a key factor, but in my mind here are the key thoughts:

1. Determine the estimated time you will live in a property. Because there are transaction costs on the buy and the sell transaction renting is going to be better in year 1 most likely with a cross over point at some point in time depending on economic scenarios that are out of our control. Buying might become better in year 2 or in year 15. You will not be able to determine that exactly because we don’t know the the future.

2. If you rent you have an opportunity for investment for the funds that are not tied up in a house so don’t get hung up that you are throwing money away paying rent.

3. If you are buying in this market with 20% down you are leveraged at 4:1 and that is probably more risky than buying a stock index because it is not leveraged and is liquid which is all that matters if you need cash to feed yourself.

Yeah, I get what you are saying. Put your apartment up for a private sale at a ridiculously expensive price like 2-3x its market value. See what happens. You could win the lotto. Call it an experiment in modern economic theory.

Is LA still an up and coming town or is it a declining $***hole? That’s the question you need to answer for yourself. Look out of the window in your current place and take a walk around the neighborhood too.

Watching some videos about homeless, vacant store fronts on Wilshire Blvd, rats, trash, and on and on, Not to mention traffic. Alot sure looks awful close to 3rd world now.

A man was stabbed to death in back of his $2.1 million home just north of Wilshire, a few blocks east of Beverly Hills. The stabber was a homeless guy. It’s barely been in the news, because that’s LA in 2021.

The problem if you are staying in the same market is that the expensive places are also appreciating. You are generally better upgrading in a down market when the expensive places have taken a disproportionate dive in value.

Investing is a combination of common sense, knowledge of market history, and the guts to take a chance. There are no guarantees, you pay your money and take your chances. If you are right you make money, and if you are wrong you lose. That is the game.

If you truly believe prices will continue to rise, then stay. If you truly believe this is a bubble and will pop, then sell.

IMO what is happening now is insane, and not sustainable, but I cannot tell you when it will all come crashing down. All I know is that my entire life the only thing you can count on is change, because every action has an equal and opposite reaction. It is the law of unintended circumstances.

Consider engaging in geographical home price arbitrage, if you can. Sell in the high-priced LA area, and buy the same or more for less in a different part of the country. Pocket the difference. Plus the air quality in LA is not very good.

“House prices rose by 11.2% from a year ago…”

Does the Fed see this as a great success or do they recognize that housing has been turned into a speculative free-for-all? Do they understand that prodding investors with ZIRP to speculate in the asset markets prevents large numbers of people from finding affordable housing?

This is one of the noxious side effects of keeping the stock market propped up as housing prices have gone along for the ride. Not sure that renters and young people will be very impressed with the Fed’s presentations claiming there is insufficient inflation in the economy.

Yeah I am going to venture to assume that most people and young people don’t know what exactly what the FED does or care..now if uncle Jerome is dancing on Tik Tok and rapping about QE on a viral video then you might get their attention

All of the young people with Robinhood accounts know what’s going on. They don’t have jobs and can’t even think about having families. They know the system is not working for them.

Why would you think the system is supposed to work for you? If the “system” is not working for you, it is because you are not doing what is necessary to succeed. Life is graded on a bell curve. Everyone has the opportunity, but not all are willing to pay the price.

Those who put in the most effort succeed, and those who sit around waiting for life to give them something usually do not.

If you are working a 40hr. job and doing nothing else, why would you expect to be successful? That is just the minimum.

I never began getting ahead until I began investing 100+ hrs a week to get ahead. In my 30’s I would work 8-5 at my regular job and 6-10 remodeling houses. 7 days a week. Sacrificing, saving, and investing.

Other people work full time and go to school at night to get ahead. The point is if you want to have more, you have to do more.

Jdog,

Working hard may have worked 40 years ago, but work isn’t enough to build wealth now.

Wages have not grown, but asset prices have grown 200% since year 2000. No matter how hard you work and save, everything becomes less affordable. The prices of things people really want in life – houses, education, health, retirement, etc. – are all out of reach now for the average person entering the job market.

Over the next 20 years, a nurse or teacher could work 24 hours a day and really help a lot of people, but that won’t be enough to keep up with the rate of asset inflation we’ve seen over the last 10 years. Contrast that with the speculator sitting at his desk 2 hours a day who made a fortune buying Bitcoin or stocks.

As I said before, my stock gains in 2020 were better than my wage earnings over the first 15 years of my career. All I did was push a few buttons. This is not normal. The system is working only for people that have some capital (i.e., the older generations). The generational wealth transfers taking place today are irresponsible and unfair. People who work should be rewarded. People who save should be rewarded.

People who do nothing but push bottoms should not have an annual 20% gain guaranteed to them by the government.

“All of the young people with Robinhood accounts know what’s going on. They don’t have jobs and can’t even think about having families. They know the system is not working for them.”

Right now, its much harder to make an honest buck than it was say 40 years ago. Back then if you just played by the rules and were patient, you could get to be fairly well off and have good retirement. This no longer the case. I do agree that even then you had to put in the extra effort to really make yourself independently well off.

I just got my annual statement from my mutual fund which invests in Short Treasury securities. The yield came in at 1 basis point. That is .57 per month on 56 K invested . Now tell me all the sacrifice and saving was worth it. It wasn’t. Hard work and savings did NOT pay off! The system is rigged now more than ever.

Instead of being retired, me and Ms Swamp are still in the workforce working 80 hours/week, just to make ends meet.

Wow, hard to comment when everyone is right. However, I’m still going to ‘mostly’ agree with Jdogs opinion on working harder to get ahead because that is what I did, and what my kids are doing right now. It worked then and still works.

I did the sweat equity thing and also controlled spending. I certainly wished I had a doctor’s income or knew enough about investing to time the market, but didn’t and don’t. I do know how to build though, and love doing it. If you pick up one or two extra shifts a month, or work some OT, pay down the mortgage with it…the money can go right on to the principal. Never increase a mortgage with a refi to buy other stuff, unless it is a good piece of property.

Just an opinion. To quote my Father in Law, “When you pay off your house it’s like you just got an immediate $1000 pay raise. You’ll always have money in your wallet”. This was said to me in 1979. Today it would be the same as a 3K pay raise, and not too shabby.

You’re all correct. The basic issue is those born from say, 1940-1970 like to think that the world they left us is the same world they inherited. It’s not. It’s worse. Far worse.

My parents said in 1982: “We’d be idiots to pay off our 6% 1970 mortgage when we are making 12% in our government insured CD.” Heck, they could have invested in all of the payoff money in a 30 year US Treasury at 14% at the time and guaranteed a massive profit by not paying off their house the entire time remaining on the mortgage.

Will we get to that point again? It depends on inflation.

If your crystal ball says interest rates will rise, don’t pay off your mortgage. Play the game like my fortunately lucky Silent Generation parent homeowners did.

If your crystal ball says interest rates will fall below negative, be prepared to refi.

In my opinion, for security, I will buy quality dividend stocks paying 3-4% while having a 2.5% mortgage rather than paying off my house. If the market crashes, I may lose some but not much with quality stocks (ie Verizon, CocaCola, Pepsi). If inflation rises and CDs rise to 12% again, I will be ecstatic with the spread between my 2.5% mortgage and a guaranteed insured 12%.

However, I will always have 1-2 years of house payments sitting and “losing” in a government insured bank account making 0.1% so I hedge and don’t lose it all in a foreclosure.

Ha ha, yes, mock your inheritors. Not like you’ll care since you’ll be dead once this mess reaches its crescendo.

The fed is actively buying mortgage backed securities, they are inflating the housing bubble directly by deliberately pushing mortgage rates lower than they should be. It’s criminal and nuts.

The Fed recently called this a “very strong rebound” in housing market.

It is all good according to Fed.

Real-estate bubble? That’s not a real-estate bubble! Says the Australian ;-)

About 1/2 of these “bubble” markets look to be on track from where they were headed were it not for the 2004-2006 run-up (PHX, San Diego, Miami, NY, Vegas etc). 6%-10% annual appreciation is in line with TRUE inflation.

Methinks there is more room to run in those markets, especially since most are in the desirable US Southwest where Boomers and Millennials wanna be.

I also think prices will continue to rise in the short term, with many owners stuck because of covid, that’s an easy call.

The problem is what happens when all the manipulation ends, the jobs don’t come back, and the debts are larger. That will cause both an economic effect and a political one, which doesn’t bode well for housing. It’s going to be Chop Zones all over the place. Try getting out then.

I don’t think the manipulations are ever going to end.

The FED never stopped doing QE for last 12 years

jon & Petunia

I think the low end FHA stuff will see a leveling or slight decrease in months / years to come, just due to the volume of inventory which could hit the market after forbearance ends. Even then, extend and pretend will not change the payment amounts, just the loan term, so the impact may be only a leveling since many of the defaulters are choosing not to pay even though they can pay.

I agree that never-ending QE, which will continue into the indefinite future, will likewise buoy home prices indefinitely. IMHO These charts reflect where house prices “should be” when considering the 12 year QE economy which will soon be the 16 year, then 20 year QE economy. In other words, the bubble will not burst but it might hit a soft ceiling for awhile as more inventory starts to creep into the market.

Exactly 50 years ago, in 1971, Nixon broke the Bretton Woods system and thus severed the link between the dollar and the gold standard.

Per “wtfhappenedin1971 dot com”…if you like economic charts about how the world financial system fell apart from 1971 forward, check out the web site as it is legit and used in various financial publications, including some hedge funds.

Here are some actual 1971 prices:

$25,7000 – New House

$10,622 – Average Income

$3,560 – New Car

$2,600 – Harvard Tuition

$150/month – Average Rent

I was not even born in 1971, yet I, along with everyone on this Earth, is paying a very steep price for Nixon breaking the gold standard in 1971, as 2021 pricing for houses, rent, Harvard tuition, etc have “run over” average incomes quite drastically versus 1971. Exactly 50 years ago is the keystone reasoning why the world financial system has gone scorched Earth in 2021, why housing has gone wild, why the Fed is delaying the somewhat inevitable (timing indeterminate) financial end game “reset” by any and all means possible, etc.

Just like gaining weight or getting old, it happens so slowly it is hard to figure out when it all started, yet study 1971 and see the patterns that lead us for 50 years to “WTF happened in 2021″…

Governments always are changing the definition of money to fleece the public. US government borrowing $30T at less than inflation means that capital allocation can be run out of DC. A few people have a few meetings and allocate more capital in a few days than Warren Buffet did over 50 years.

And in 1971 a single breadwinner could support a family and middle class lifestyle comfortably.

How we got from there to today’s economic nightmare without pitchforks and torches from commoners is perhaps best explained by the boiling frog analogy and normalcy bias.

Sales tax in my city was aound 3.5% in 1971 too. Now it is 10.25%.

I am guessing it will be 12% to 13% in 10 years.

Crook Cty?

Raising the tax rate is disgusting.

My understanding is that housing prices as well as many other things were somewhat stable before the gold standard was dropped. The fed and politicians have been messing with the free market for so long nobody remembers what a free market, with real money, even is anymore. What we’re seeing was and continues to be inevitable. I don’t know if now is the best time to buy but I can tell you this much…all of this printed money isn’t going to magically disappear and things will get more expensive as time marches on. Better figure out how to hedge it now or we’ll all be eating cat food for retirement.

Seattle homes cost more because they come with NonRemovable squatters,

use needles, heaps of garbage, massive utility bills, spent fire extinguishers,

graffiti, & broken: walls, windows, smoke alarms, light fixtures, appliances, etc.

Please be super, super cautious when you say “…a realtor says”….

They’re not all dishonest or terrible but many are.

I’ve sold several homes on my own…realtor not needed.

When a friend a few yrs ago said “My realtor said…”, I looked the guy up. He’d had a RE license for 18 months and said on his FB page he was “going to give a try”….since being a “chef and photographer” wasn’t working out

I told me friend: “For the love of God, man, do not make the biggest financial decision of your life based on this person’s “advice”!!!

Having deal with realtors over my lifetime to do routine real estate transactions for my own personal family, I have some personal experience with them as whole. My assessment is not favorable. Here it is in its raw from.

Most realtors, about 85%, or more are incompetent.

Most realtors, about 85% are dishonest, and unethical.

Most realtors, about 85% routinely lie and do not know they are.

The profession if you want to call it that is inhabited by people who have failed in other more demanding professions.

About 5% to 10% know what they are doing and are ethical.

Had one a while back who lost a deal because she told me not to buy on a busy street with heavy traffic, with small children in the household. She was one of the 5%.

Substitute “salespeople” more generally for “realtors” and you’re still correct.

“….based on homeowners’ estimates about how much their house would rent for. ”

Still marvel at this concept. In what other area is an estimate from a citizen involved in an index calculation? How would a person actually know what his house would rent for?

And, who knows the final inputs and the legitimacy of the calculation that is “25%” of the CPI?

Lots of room for number fudging, IMO.

As I mentioned in a comment on this topic in a previous article, the census folks aren’t too concerned about the absolute rent values estimated by folks. They are much more concerned about the change in those estimates year-over-year. The thinking is that if even if there is an inherent error in folks’ absolute rent amount estimates, the error itself would remain consistent from year to year, allowing the census to extract useful price change information from the data – which is all they care about.

Now note that I am not saying that I personally advocate keeping OER as the central component of housing CPI, I am just trying to explain the statistical logic behind how it’s computed.

So….the bureaucrats believe that the inaccuracies in their metric will be consistent. So that’s a good thing.

That sounds about right for the government bureaucrat.

Far be it from them to come up with accurate measures….that might mean extra work.

Again, I am not advocating for OER as the metric to use but from a pure statistical point of view, it is probably reasonable to assume that that error rate does stay consistent. Again, they don’t really care about the absolute amounts, what they care about are the changes to the amounts across time periods.

1) The glorious NFL overextended to 17 game to help the the owners of the empty stadiums.

2) Man.U owners, supported by City bank, empty Old Trafford stadium have 75,000 seats capacity, in the middle of a city slum.

3) Liverpool lost their thrust and slumped, because Anfield 54,000 singing and saluting fans were forced to evacuate their stadium. That didn’t stop few selected Liverpool’s superstars from kneeling and kissing the grass in front of the cameras, when they score. EPL rating plunged along with their empty stadiums RE. Those players don’t care. They have a different agenda and mission.

4) West Ham used to be near an Arab suk, that’s why they kneel.

5) NIKE made hairy Kaepernicht the man of the year. Xi punished macho

NKE, because they talk too much. NKE shared turned around in the last few weeks.

6) The $1B+ Giants stadium is vacant. No sausage and Buds. The Loews hotels are struggling. L, a lower high. Hilary Tisch, age 36, lost her life.

7) Mexico America kaisers don’t kneel. Two weeks ago they score a Borgetti header, showing their superiority.

Buy now or be priced out forever. There are many sites like this saying for many years that we have a bubble and prices are just speeding up.

Ok, in 2007 we had too much supply, it’s not the case currently.

I’m a happy buyer of a condo in 2015 and took a second house mortgage in 2017. My housing net worth increased from $200k in 2015 to $1.4kk right now. My stocks are up from $100k to $500k in just 5 years.

If I would wait I would be a forever renter like many of you people.

In the meantime I just live and work.

Just don’t wait, buy!

Adam,

Your IP address is in Tychy, a small-ish city in Poland. Did someone pay you to post this? If yes, I’d like to know who and how much these comments go for these days.

@Wolf,

I didn’t say I live in the US. In Europe house prices are even worse and Poland has the biggest increases y/y.

You just happened to leave out that crucial piece of information? Sounds pretty normal and not at all suspicious.

Either we’re really in a bubble and NAR is seeing storm on the horizon and hiring troll farm to post messages like this. If that’s the case, congrats Wolf, your site is famous enough to land on their radar

On the other hand, maybe he is using a VPN and hiding his IP. Just giving him a benefit of a doubt here.

Check and Checkmate.

In 2003 I bought a house for $275K with $100K down, by 2007 it was worth $430K, still had $100K too. By 2010 it was all gone.

The spread in your numbers scare the hell out of me, because they are not normal returns. Good Luck, I think you are going to need it, especially if you are in south FL.

@Petunia,

Europe here actually.

Petunia, what’s that house you lost worth in today’s Florida market? Just curious.

It sold in 2018 for 360K and the zillow estimate today is 419K. The current value is close to the value before the GFC crash.

Petunia, thanks…it seems like those property values have not gone off the map like other places (Ca, Seattle, etc). The home prices here in the part of Texas we are in are not going bonkers either.

Petunia, my primary home in the north central US is just about back to where it was in 2006. I do not expect it to stay this high.

I’m in South Fla and housing prices are insane. Lots of northerners/retirees flush with cash. Been waiting for the other shoe to drop with respect to housing prices. Want to sell my townhouse but not overpay on a bigger place. Paid $160k in 2004. Previous owners paid $87k three years before that. Definitely had FOMO and was afraid of being priced out of the market. Lived through the last crash. Can likely sell for $275-300k.

It’s comforting to see others on this site who are biding their time as well. I’d love to capitalize on the sale of my place but dread the thought of renting and moving multiple times. A couple years ago I thought the prices were too high. Now I question whether waiting was foolish or wise. I just can’t justify spending an obscene amount of money right now. It feels so similar to the last pre-crash even though you’ll read how different the situation is. Can’t shake that feeling in my bones that it isn’t a wise move to buy.

Adam,

Clearly ya don’t have a nickel to scratch ya but with, $1.4kk, yeah ok, it’s not a bubble, it’s a hyper bubble when measured against the economic situation, pending sales down today with an open economy, this is the top of a massive crash comming,

@Jack,

even if we have a bubble (which is not the case IMHO) the FED won’t let it collapse.

What is with people who think the FED (always in capital letters for some reason) has godlike power to prevent every bad thing in the world?

Please don’t stoke the FOMO (Fear of Missing Out) anxieties of potential home buyers sitting on sidelines. They need a clear, level head to figure out best course of action in Twilight Zone times we live in.

@Heinz,

I’m just sharing my opinion, we have a bubble on the stock market, crypto, but in RE it’s just natural supply-demand growth, not much speculation here.

What about government measures like forbearance and record low interest rates? Supply was low to begin with, yes, but there are several strong temporary artificial factors at play since COVID.

To me it seems pretty clear when looking at the mean trend line that there’s a massive residential real estate bubble. Wages are not increasing nearly as fast as real estate prices, especially in HCOL areas.

And what is it that they say? Supply is low, until it’s not. I’m endlessly curious about the impact of forbearance ending and how many will be forced to sell.

No bubbles anywhere. It’s just aggressive short term “investing.”

You sound like Tommy Woo… But you are probably too young to know who that was…

Is Tommy Woo the same as Tony Vu? The guy with the boat & girls and all those funny informercials? If that’s the same guy, I give him props for beating Dan Bilzerian to the punch by more than 3 decades

His commercials were hilarious. “You got guts to be rich like me”? That was just before everything went to heck….

I think supply will immediately appear once the top is there. Where I live, I observe the same pattern recently: a condo is put on sale, lots of traffic and it’s gone in a week or 2 – then it’s sitting empty after that. Not even rented out, so obviously purchased as an investment. Probably the same happens everywhere

Miami is sinking due to aquifer depletion and ground subsidence; plus there is sea level rise. Ocean view property is expensive. The Haitian immigrants moved inland to cheaper ground. Little Haiti was built is on the highest part of Miami. Real estate in the Little Haiti neighborhood is rising in value faster than other parts of Miami. Flood zone property is risky.

The outskirts of Miami have been moving since the city started to be developed. Back in the 1970s, the poor black areas were just over the bridge from Miami Beach. Now even Hialeah is being gentrified, the bars on the windows of homes are being removed.

The growth in Brickell, downtown, and Wynwood in the past few years has truly been remarkable.

Real house prices indexed for inflation in the Shiller 20 are back to 2005 levels, so yeah its a bubble. The ten year rates still look like they have room to run. So likely prices will stall and maybe go down a bit. The banks do have better lending practices than back in bubble 1 so most owners should be ok outside of the FHA mortgages no I think no crash just sustained sideways movement.

I concur. Flattening. No crash. Given how much investor cash is waiting for the low end FHA fallout, there may not be much of a correction there either.

I concur. Home prices would never fall. Worst it may concur and especially in san diego because we are special and this time is different

No, of course not. Never. Couldn’t happen. Just like in 2006!

What is more, the ratio of home price to income is off the charts. It has never been higher and is going parabolic. It never fails to amaze me just how short peoples memories are, and how little they learn from history.

I know, it’s like 10X in San Diego and probably worse in Los Angeles.