Now they’re wondering why.

By Wolf Richter for WOLF STREET.

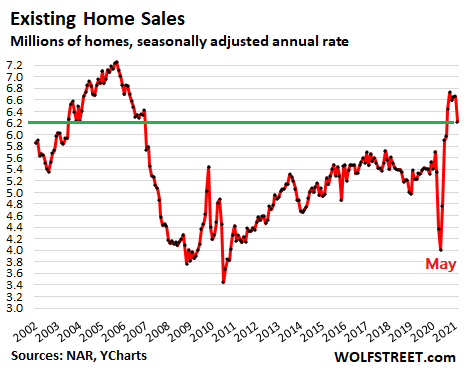

Home prices skyrocketed by the double digits starting last summer, despite the loss of 10 million jobs still, and with 2.5 million mortgages still in forbearance, as mortgage rates dropped from historic low to historic low. People bought homes without putting their old and now vacant home on the market because it’s profitable to hold it, amid surging home prices and low interest rates and the possibility of yanking cash out of the old house via a refi. As homes got grabbed and sales surged, other homes weren’t put on the market, inventory for sale plunged, and prices surged. But now, sales have turned from a preliminary dip late last year to a big drop in February. And everyone is wondering why.

In February, sales of existing homes – single-family houses, condos, and co-ops – dropped by 6.6% from January to a seasonally adjusted annual rate of 6.22 million homes, the National Association of Realtors reported today. On a year-over-year basis, sales in September through January had been up in a range from 19% to 24.4%. In February, the year-over-year increase was down to 9.1% (data via YCharts):

Now everyone is wondering why sales dropped.

Rising mortgage rates and the affordability issues that come from the dual impact of surging home prices and rising mortgage rates are on top of the list. But note that many of the home sales that closed in February went into contract before February, and that in January, mortgage rates had just started to rise from record lows at the end of the year. And we haven’t even seen the impact in the data of the jump in mortgage rates in late February and so far in March.

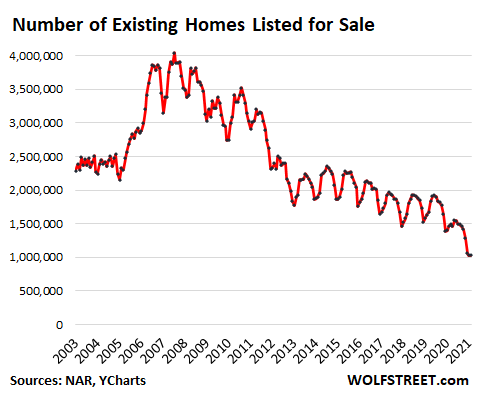

The inventory of homes for sale plunged to a record low in the data series in January of 1.03 million units, and stayed there in February, representing 2.0 months’ supply at the current rate of sales (up from 1.9 months in January).

Why the 12-year-long decline in inventory for sale? There has been a structural change: the business of selling homes has changed. It used to take months to sell a home, from the moment the home got listed in a paper publication to the day the sale closed, involving a lot of personal contact and paperwork. Now homes instantly appear in the listings and are marketed online; potential buyers can tour the home via video. Mortgage approvals are largely automated and lightning fast. So the period that homes sit on the market waiting for the processes to occur has shortened. This reduces the inventory for sale. During the Pandemic, technology has invaded home sales with a quantum leap and sped up the processes.

The shadow inventory: Empowered by low mortgage rates and surging home prices, people who buy a home feel no urge to sell the old home. They can just hold the vacant home and profit from the current price increases that far outrun the carrying costs. In addition, they can refinance the mortgage and take cash out of the vacant home, while speculating on further price increases. I personally know several people who have done this as part of their financial calculus.

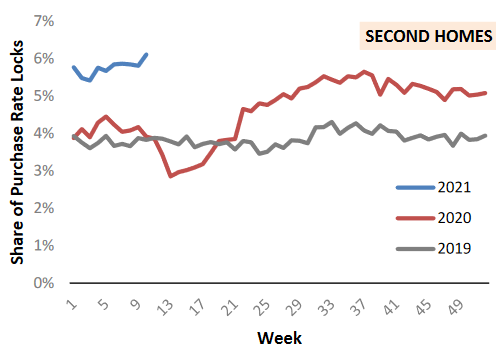

The share of second-home purchases as percent of total home purchases has soared to over 6%, a high in the data series by the AEI’s Housing Center, and far above the prior two years at this time. Some of these may be vacation homes, others may be part of the urban exit, with people simply not selling their old homes:

Mortgages in forbearance are still a big factor. According to the Mortgage Bankers’ Association, 2.5 million mortgages, or 5.1% of all mortgages, are still in forbearance, meaning that lenders have agreed not to execute their right to foreclose, thus allowing the borrower to skip mortgage payments. Many of these mortgages were already delinquent when they entered forbearance.

“Forbearance” doesn’t mean “forever,” though it may now appear that way, given the repeated extensions. The exit from forbearance can take various ways, including putting the home on the market and selling it to pay off the mortgage.

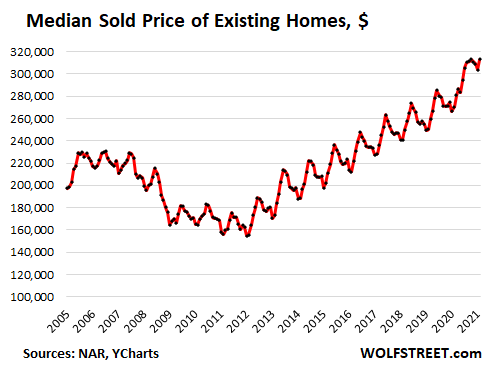

Prices upend historic seasonality.

The median price for all existing homes jumped by 15.8% year-over-year to $313,000, according to the NAR’s report. This was up 46.5% from five years ago. By home type: for a single-family house, the median price jumped by 16.2% year-over-year to $317,100; and for condos, it jumped by 12.3% to $280,500 (data via YCharts):

As in so many other economic indicators, the well-established seasonality of the median home price has been nixed during the Pandemic. It the past, it would peak in June or July (the high points in the chart above), and it did so even during the Housing Bust, and then it would drop and hit the seasonal low point in January or February. But in 2020, the median price hit a high in October, then dipped from November through January, and in February bounced back to the October level.

The Fed smiles upon rising long-term Treasury yields as sign of economic growth and rising inflation expectations. Read... First Signs that Surging Mortgage Rates Are Dialing Down the Heat under the Housing Market

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

FOMO

Because the 10-yr Treasury rate is below the inflation rate.

I bought my house in 2001. Its worth 4 times what I paid , which was 121k in w 2001 . Its getting 400k offers now in fly over country I’m selling. Dont care where I live , thinking a bout northern Minnesota where I can get twice the house on a lake. For a better house.

How much was it worth in 2009?

You might wanna get going while the going is good…

Rates have likely already passed their bottom (although Fed likely won’t allow 10 yr above 2% or – gasp – 3%…tack on 1% or 2% to get mtg rate, absolute key indicator for housing demand).

Rob, have you visited there? Northern Minnesota is a place you move from, not to. I know, I’m a former native of that area…

Cold, ticks, leech, mosquitos, humidity, tornadoes, besides all that it’s okay at best.

They have two seasons-Fourth Of July and Winter.

“Cold, ticks, leech, mosquitos, humidity, tornadoes”

All much preferred to urban/suburban liberal run areas.

A harsh climate does wonders to keep out people who don’t love weather and nature. It also keeps property prices low and simultaneously prevents California-style overcrowding.

The 6 seasons in the Northern Tier States (like Minnesota):

Spring Floods

Road Construction

Fall

Brown Winter

White Winter, and

I Can’t Believe It’s Still Winter!

Where I live in northern Maine there are three seasons:

Snow

Mud

Flies

Although some people insist that we have six months of winter and six months of damn poor sledding.

The north is a place you leave to go and make money elsewhere. Then once you have financial stability you can go back knowing you will have left the big city progressives behind.

Northern MN is a great place with fun-loving social people. Who cares about ticks, mosquitos, and a cold season. Anybody who wants to go home because of a mosquito bite is looking for excuses not to have fun. They call these people dead fish in northern MN.

Appreciate the beauty that is right in front of you, wherever you are.

Don’t listen to the naysayers. I live in Florida and it’s got one season. Summer. Even in January and February we usually have some days brushing 90. On top of that, it is rare that the humidity isn’t as thick as soup. The mosquitoes and sand gnats are awful year round with no strong freezing snaps to knock them back. And they are joined by numerous types of plant life that have their own attack vectors (rashes galore here). Anything not made of stone outside will rot (even hard plastics) or rust and stone will get covered in growth.

Having lived in climates ranging from those with yearly lows hitting -25 fahrenheit to Florida, I prefer the variety of the cold ones.

I wonder where Rhett lives because it isn’t Florida. One season?! Not. Here in Tampa Bay area, we have pleasant cold months (Dec, Jan, Feb) which is 40-60 degrees during day and sunny/low humidity. It can freeze rarely over night. March, April, May, Sept, Oct, Nov are likewise pleasant with temps from 50-80 and sunny/mid humidity. That’s why Florida is the 3rd populous state and growing quickly. Florida in June, July, August can be like living on the sun, which is apparently what Rhett is talking about. Thats why you spend month or two every summer up north to escape the heat/humidity.

With all RE being local, it would be interesting to hear from some of the agents about their local markets and recent trends.

We’re not seeing any drops on Vancouver Island in prices or construction activity. None. Mind you, this is also a destination for many Canadians on the move and for foreign buyers of RE. I have been wondering though? A friend of ours just listed her high end home as she has decided to move away due to the recent death of her husband. I have been surprised that her place did not sell in the first week compared to other listings at comparable prices. Early yet, though.

With Covid factors, weird weather everywhere, and divisive politics, I can see local markets slipping into volatility beyond simple interest rate changes and number crunching. RE agents are very aware of these issues because their clients tell them what they think and why.

The unfortunate fact of living in a desirable place has also seen a fantastic increase in local prices. Any house for sale sold, some within hours, always within days. Not now! Suddenly everything has come to a halt as over-reaching realtors and would-be sellers found the price ceiling. And they ain’t budging. Buyers must be going elsewhere…

We live in a world of hugely inflated housing prices where any mortgage rate above 3% or 3.5% makes the math impossible for a majority of potential buyers.

Inevitable result (as in 2008/2009) home prices have to decline off idiot, paint huffing highs.

Two basic emotions in every market– fear and greed.

Currently ugly expansive greed is everywhere we care to look, and of course it is so very evident in housing market. Fortunately all false ‘good’ things come to an end, and this fragile yet deceptively robust housing market has had a good run and now is on borrowed time.

Machinations and exhortations by Fed high priests will prove to have their limits.

In my average midsized Midwest city (an average midsized Midwest city is 20,000 to 100,000), the local housing market as well as all midsized cities within probably 50 miles at least, are doing “red hot” or at least good. From about 2010 the housing market really recovered and has been picking up momentum ever since that hasn’t seemed to ever slow.

The CCP-19 pandemic caused some weirdness early on, but has only seemed to accelerate the process. It did however cause the price of lumber to skyrocket meaning that new homes for part of the pandemic created no profit for the builders (profits for new homes are still lower), because of the time gap between planning a home, getting the loan approved, and actually ordering the building materials. Those same homebuilders still did well, because of selling existing homes

Here in the Midwest, the weather has had zero effect on anything. The Midwest is big though, maybe some south part of the Midwest was effected.

There was plenty of “”protests”” last year in the big cities of the Midwest, that had some impact (though not necessarily big), but most people won’t openly say it, because of being accused of social no no’s. The effects of the “”protests”” last year likely varied quite a bit by exact area.

The lockdowns were much smaller in the Midwest and didn’t really vary that much between midsized and large cities so that probably had little impact for moving reasons. Many small cities, but especially the very small cities, basically ignored most of pandemic rules. Many small offices in the Midwest simply closed their doors to the public or switched to a hybrid model, making moving harder than for those living on the coasts. Escaping taxes and cost of living rises, has also probably had little to do with most of Midwest. Though a small but growing number of those on the coasts and in the south have moved to Midwest midsized cities.

As it stands right now in my city, the typical newer 2,500 sqft house used went for 220,000ish pre pandemic and probably has gone up about 20k-ish to 30-kish since. Smaller and cheaper houses have gone up quite a bit over last 5 years, possibly as much as 25% to 50% for most without major problems, these houses vary alot more, so their prices also varied alot more. Almost anything under 300k has a very determined price and buyers already know max loan they can get, so house sales go very quickly. 500k and over houses have gone up quite a bit as well, proportionally, maybe even more than average houses (there’s a lot less of them, so hard to say), but there are less buyers and these houses can be more unique and can sit on market much much longer.

People will tell their RE agent extensively what they want the house itself to be like. They are not necessarily forthcoming in describing what kind of neighborhoods they are looking for, or why they moved (the real reasons).

Very thorough report TR, thank you for taking the time.

Brought to mind a friend in southern fly over area in 09-11 buying small houses on the courthouse steps for $3-5K, refurbing them as needed, usually minor repairs and a new paint job, then either selling them for $30-40K, or renting them and financing based on rents until they did sell; They did about a dozen IIRC, then stopped when the local economy picked up sufficiently to stop/slow way down the amount of houses available.

I thought the same thing was going to happen this time, but, clearly, it hasn’t YET.

Some friends still keeping their powder dry just in case…

Best time to buy a house in recent times was around 2012. It has been froth and fury in housing since them– it now rivals and exceeds housing bubble of 2006-ish.

When we are living through an aberration in economic activity such we witness today it is easy to get caught up in the ‘now’ and lose perspective. What is going on in housing is simply not normal or sustainable.

I think we are seeing first signs of rivets popping and water gushing into good ship SS HousingMarket.

As a middle class responsible saver with a sizable downpayment sitting in cash, who has planned for a few years to buy a starter home in the spring/summer of 2021 but is now priced out, I wish you were right. But here in the East Bay Area suburbs, I no longer believe this is an aberration. Affordability for the middle class (even the upper middle class!) may never be reality again. Not here. There are a ton of people in the Bay Area with ridiculous amounts of money and stock options. The wealth divide is enormous. Tech workers who are fleeing San Francisco and independently wealthy investors are snapping up almost everything in my historically blue collar city. Forget the middle class. They are now eternal renters. This part of the East Bay is well on its way to being predominantly a renter city. Most of us locals who have lived in this city for decades will never be able to own homes in our own city. The Fed deserves to die a slow and painful death for their intentional asset inflation.

Word, Rumple. In the same boat sitting on cash, having made around 15 offers, all over list, and landed nothing. (This is in L.A.)

Couple Captain Obvious moments from the last few days:

– CNN drops the hammer: https://www.google.com/amp/s/amp.cnn.com/cnn/2021/03/23/opinions/millennials-almost-impossible-to-afford-home-olson/index.html

– Tech boy genius Sam Altman figures it out: https://mobile.twitter.com/sama/status/1374078846664724482

I’m not sure it can go on like this forever; at some point, the bald faced scam of wealth transfer has to summon the guillotine, right?

Take a map of the US and divide it into quadrants then locate where you live. I can bet you live in the North East even though everyone from that region claims to be from the Midwest. They need to change that geographic distinction. The Midwest should be Colorado or Utah?

The Census Bureau’s definition of ‘Midwest’ is the 12 states in the north central United States: Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, and Wisconsin.

Thanks for shout out for the heartland.

Russell,

I definitely live in the Midwest. One of the reasons I never tell exact state is to preserve some anonymity. There’s alot of crazies online and so there is no reason to give full identity away.

My area is also very representative of the Midwest and so It could easily be a midsized city in Ohio, a Dakota, or anywhere elsewhere in the Midwest. There are of course distinctive types of midsized Midwest cities that are scattered throughout the Midwest. With multiple types in each state. I live in one of those.

You missed my point, Thomas. I wasn’t trying to guess at your locale; couldn’t care less. I was merely pointing out the misnomer of the “Midwest.”

Question – How many legs does a sheep have if you call a tail a leg?

Answer – Four. Calling a tail a leg doesn’t make it one.

The states mentioned by Heinz are all located in the north or northeast regardless of how the Census Bureau decides to define them. Their lack of geographical understanding is beyond me. The only thing they are mid-west of is the east coast.

Russell,

Who cares? There are countless examples of arbitrary names, definitions, and units of measurement. Eventually, America will annex Canada, after that, we can redraw the regional names.

Spoke with an experienced agent last week in Seattle. He said the last few months have been the worst market for buyers he’s seen in his 40 years of RE experience. People are bidding up properties 10% over list. Properties are listed on Thursday, then a dozen or so bids are reviewed on Tuesday. You have to buy the house with zero contingency at 10-20% over list. He also said something about a $50,000 nonrefundable deposit, which the seller keeps if you back out for any reason.

He’s a friend, so he tells it straight.

The nightly “burnings” in PDX, definitely have created a large exodus to Vancouver,WA The market is incredibly hot. People have lined up n signed up,waiting for their house to be built.

Rents in PDX down, while Vancouver have risen

Wow, Seattle must be full of fools being seperated from their money.

Thankyou Wolf for the information. When will the 2.5 million forbearances become a major factor in the real estate market? How many of these forbearances will become distressed, short sale, or foreclosures? Is there some sort of deadline for the forbearance program?

June 30 for Fannie/Freddie mortgages? Ymmv

https://www.fhfa.gov/mobile/Pages/public-affairs-detail.aspx?PageName=FHFA-Extends-COVID-19-Forbearance-Period-and-Foreclosure-and-REO-Eviction-Moratoriums.aspx

It would be interesting to know if these forbearance programs are a matter of only FHA backed loans or if private lenders are also making the decision to suspend billing. If so, why? What does a lender have to gain if it’s a just a private mortgage with no federal involvement?

Private lenders have to go along with the forbearance or fannie and freddie won’t buy their mortgages.

Cocomaan

I am a private lender and though none of my borrowers have requested forbearance or defaulted, you are correct, there is no incentive for a private lender to NOT foreclose, especially when the asset has been appreciating. One could argue you are doing the borrower a favor by taking over the asset, selling it, getting the loan and sssociated costs paid off and the residual goes to the borrower.

I have had borrowers in the past just offer up a deed-in-lieu of foreclosure (DILF) because they do not want to deal with it because life has gotten in the way. Most foreclosures or DILFs result in me losing $$$ though, as one would expect.

Thanks! Good to hear the perspective.

Given the rise in home prices, it’s natural to exit forbearance with a sale if the borrower cannot deal with a mortgage. So the mortgage principal would most likely get paid off in full.

But it adds supply to the market.

At the low end, represented perhaps most closely by FHA loans, the delinquency rate nationally is 17% of FHA mortgages, which is HUGE. But these mortgages are now in forbearance. In some markets, the FHA delinquency rate is over 20% of FHA mortgages. So if these delinquencies are cured by the sale of the home, it would add a LOT of supply to specific markets. That’s why forbearance keeps getting extended: no one wants these homes to show up on the market.

My understanding is that if a mortgage is in forbearance, the homeowner can not sell until they have the cash to repay what they owe. I have heard of people buying a home and then the deal falling through because the existing owner is in forbearance and does not have the money to pay back the lender. Has anyone else heard of this? The implications don’t seem good for lenders or distressed homeowners if this is true across the board. Selling a house once the can is done being kicked down the road doesn’t seem so simple if this is the case.

LD

Every state’s laws are different, of course. In a prior comment, I mentioned the common use of a deed-in-lieu of foreclosure (DILF).

As a lender, I would request a DILF in an appreciating market. The borrower walks away without a foreclosure and the lender has an asset that may very well be worth more than the amount of the outstanding loan.

The lender cannot stop a sale because the borrower is behind on payments, if the sale proceeds will cover the shortfall. If the sale proceeds don’t cover the shortfall, they can stop it. The borrower needs to have a lawyer involved in the sale to make the sale happen, because the lender has every incentive to foreclose if they can make money on the sale.

Sometimes the lender will approve a sale even if the proceeds fall short of the loan amount – this is called a “short sale” – if they think it’s the best deal they can get in the near term, and if they don’t want to own the place and have to carry it until prices recover.

Thanks for the explanation Beardawg!

Thank you once again Mr. Wolf.

Wolf,

Any chance we could get metro level FHA delinquency data? No full post necessary (though that would be cool) even a link would be valuable.

Signed,

GoogleImpaired

I might cover it again when the next batch of monthly data is released. I covered it a couple of times last year.

Wolf, How’s the delinquency rate for conventional and VA loans going? Any data for the 4th quarter, 2020? Most homes in the Swamp are purchased via conventional loans.

Those forbearances will be scooped up by investors IMHO. I have 2 rental homes I own. I get calls, text, and postcards several times during the week for cash offers.

I was a huge housing bear starting in 2007-2008. I knew there was a downdraft coming with the no-doc and subprime loans and adjustable mortgages. I knew when the combination of a plateau of home prices plus not being able to refinance, would cause things to crash.

This time a lot of the houses are being bought by Wall Street investors and private investors. They are locking in low rates. So lets say prices do drop some…so what, the investors cash flow is locked in with the low interest rates. Rent is stick and does not drop as much as a house…even if it does drop. I had a rental home go from a price of $52k to 80k in the 2007 bubble. Rent did not follow the trend of the house price so when the bubble popped, the house priced dropped to $40k but I never dropped my rent and thus my cash flow never really changed.

Also, last time there was a huge supply of homes built. At one time there was an excess of over 5 million home built which amounted to about 3 to 4 years of future supply. Now inventory is below 400k.

There are other reasons for house prices to stay elevated for awhile such as stimulus, new home buyers credits and low income buyer credits being proposed by Biden. Even an MTM payments.

But I think a lot of houses have been bought with such low rates, people will try to keep a house as a rental if they move?

I have a friend who locked in a 15 year 2% loan a month ago. Wow. How do you ever give that up?

ru82

Excellent recap of 2008-09 aftermath in rentals. I experienced the exact same thing. Values plummeted but rents about the same, so why sell ?

I very much agree the bubble this time has different variables for the reasons you cite. Price corrections, if at all, will be moderate when more inventory comes.

As long as the average RE investor understands (I’m guessing you do) but many just realized, the government can step in and change the rules in the middle of the game. If their tenant can’t pay the rent these days you can’t evict (covid). So, that “cash flow” don’t flo-no-mo. I don’t think anyone investing in RE ever thought that downside could/would happen. And at that point it really doesn’t matter what the rate or price of the property is.

If he bought it to flip it or rent it out, he’ll give it up the moment it stays vacant for a prolonged period of time.

Empty investment properties are white elephants, and people will want to get their cash out if they can’t do anything more productive with it.

Very little stimulus, IMO, will make its way to the housing market. The people who desperately needed the $10k for a family of 4 will either splurge on garbage (because they were improvident in the first place) or they’ll pay down debt. They still won’t be close to having the down payment.

Reading that folks not paying rent or mortgage saving their earnings and stimmy, and putting it down on buying a or another house rnyr.

Likely scenario for anyone getting ”free” money while still working, especially if now allowed to WFA, eh?

Vintage, I’m skeptical. I suspect it’s more “investors” looking to flip it, using their paper stock gains as collateral.

True with the mom and pop. I think the trend is wall street is becoming a landlord. They have found it very profitable with very little risk. They scooped up a lot of cheap home after the housing bubble. Then they got the SEC to allow them to bundle the mortgages into MBS and sell the mortgages. They even got the GSEs to back these MBS I think. So wall street now buys the houses, makes some money on selling the bundled MBS loans to investors, and then makes money on servicing the loans payments. They have very little risk in price depreciation.

Heck, if prices dropped, I bet they will buy up what ever they can? They seem to have a lot of political power to make laws in their favor?

If the dollar becomes worthless, then rents will not help you survive.

A house is a decent hedge against inflation I think. If the dollar becomes worthless, the house price will go up accordingly?

Rents are often but not always sticky – it depends on local employment base, wage stability and whether protests drive people out etc.

Also, in many jurisdictions the government can either rig the appraisal process or raise mil-rates, either way tax hikes on rentals can be a big issue for profitability.

The only reason I can think of is the incredible pain in the ass it is being a landlord.

Prospective tenants in the interview process are like people on first dates….very polite, considerate, sweetest folks ever.

You’ll meet your real tenants later. Like the guy who punches 100 holes in your walls because you won’t let him run an illegal food truck on the property.

Talk to somebody who has done airbnb, you’ll hear worse stories.

It’s been especially tough (documented here) on small time LLs with all of the rent/eviction moratoriums. The only saving grace (at least here in FL), is that you can evict folks on a month to month lease.

Being a LL can be a great source of income or can make you wish you’d never been born!

I have have rentals most of my life. I started back before the days of credit checks, so you learned to do your homework and to sharpen your judgement skills.

I have always liked the safety of real estate because as was told long ago, it is hard to steal, and if something does happen to it you are insured.

That being said, it is not always the best place to make money.

If you had your investment funds tied up in real estate back in the 80’s and 90’s when an average mutual fund was doing 20% a year, you were hating life.

“But I think a lot of houses have been bought with such low rates, people will try to keep a house as a rental if they move?”

That is why there are economic pundits in media now proclaiming that going into (housing) debt is a brilliant move and a great thing to have now because low mortgage rates on RE loans put buyers out ahead of inflation– they will be paying back cheaper and cheaper inflated money over life of loan.

Of course, that only works when status quo holds– imagine the consternation when buyer’s income is reduced or dries up (loses job).

It also assumes that inflation doesn’t get so bad that our leaders take drastic steps to rein it in.

As a landlord I now get 1-3 unsolicited calls per residential property per day from people offering to buy said properties.

This has now surpassed the regular number of spam calls I get about the “expiring warranty” on my brand new card or a chance to lower my credit card rate.

The spiel of the real estate calls is almost always “are you interested in receiving an offer on the property located at XXXX?”. In reality though they have no intention of actually making your an unsolicited offer. If you answer affirmatively to their question, rather than giving you an offer they will insist that you name a price (for fear that if they actually made you an offer it might be less than the one you were going to name).

Kramerica Industries would also like to know the answers to those good questions Art Vandalay.

?nice one

The film the big short helps the said 8%

I’m old enough to remember when people expected capitalism to make things cheaper and markets were supposed to work for society. Now taxpayers are supporting the stock market with trillions of dollars in QE, while scrambling to find affordable shelter.

At best, that’s before gangster capitalism we have now, at worst, what you described also really isn’t what capitalism’s intend. Capitalism sole function is accumulation of wealth through means of production. Wise men that wrote the book Consequences of Capitalism can provide some insight into that part and the whole making things cheaper and markets that work for society is really from control mechanism that keeps capitalism in check. We all know how well that works now from all the WTF articles from Wolf recently.

The trillions of dollars are also being used to support real estate prices. Neither the stock market nor the RE market can drop very much without pulling the other along.

All of which enriches those who are well off, and reduces opportunities for those less fortunate.

And so it comes to pass that the Millennials make up nearly half the workforce but own only 5% of the wealth.

For the average person accumulating wealth is a long 25 year slog of consistent employment, living 10 – 15% below your means and making a good purchase on a home once or twice in life.

It doesn’t require high intelligence. It’s more a discipline thing.

That’s so old school, Old school. but very true.

It was true 20 years ago. Not quite true in today’s environment of home price appreciation and wage stagnation. Its not discipline as much as its mathematics for most millennials. What I mean by that is, “slogging it” doesn’t make sense when you do that math and take into account the various factors at play.

For example: Lets say someone (person x) works at a job making 50k a year. Fairly average salary. And they decide to live 10% below their means, figuring that if they save an extra 5k a year, maybe in three years they can afford a home, or at least a down payment on a home.

However, what was a $300k home at the start of this “slog” and what was a $15k down payment at 5% with an FHA loan, is now in year three practically a $400k home. I’m using Phoenix, AZ as an example, because home prices there are easily appreciating (or inflating) at a rate of 10% a year.

Now, $15k in savings isn’t enough for the down payment, which now requires $20k. So now person X decides to “slog” it out for three more years. Because person X now will have $30k saved (assuming there is no need to dip into savings… had a newborn, medical issues, take care of an old family member, etc.).

However, in year 6 person X is now staring down a $530k house. That same down payment has now ballooned to $26k, which they could hypothetically afford as long as not a single life changing event requiring the use of their savings occurs. However, at this point the home is unaffordable. This house now has a $2,626 monthly payment at todays mortgage rates. This would equal over 60% of the persons yearly salary. Good luck finding a lender to finance that loan.

The point is, as long as the federal reserve and federal gov continuing propping up the housing market, many millennials are finding themselves in this position. No “slogging” is going to fix this systemic problem.

YES Old School. That is the way it is supposed to work, not by lottery. It worked for me, and my kids are doing it. I just tell them to enjoy the journey along the way when they can.

Self discipline might be more and more elusive for the gotta have what I deserve right now cohort, and that is not just an age definition. I know some oldsters who are screwed because they bought and did what they wanted a little to often along the way.

And you really don’t accumulate *that* much wealth (in today’s standards), but maybe just enough to get you to the grave with a little bit left over for the kids.

And this is not going to change, whatever people today say.

And timing is everything. Friends of mine bought a house in the mid-90s in a very nice neighborhood in St. Pete, FL for $40K +/-. They could probably sell it for $500K right now.

The folks who bought at the top of the last market, can finally unload those albatrosses for around what they paid.

I see in the property appraiser records of some homes currently for sale. Folks that bought at top of market and have been waiting 15 yrs to break even.

And not stumbling over job obsolescence in one’s 40s, divorce, business failure, serious illness….yup, it’s just about the discipline…

Sure, maybe that recipe worked in the past; for millennials in a major market, that first home purchase occurs at what, age 45? 50? And then the gutted remains of social security and an underfunded 401k (had to save up for that 100k down payment after all) should carry a 5k/month mortgage in your 70s and 80s, right? Or do you just write code until you die?

That ‘discipline’ line is such a crock! 99% of people in my generation who own a property did it via a gifted down payment from their family, not some pull-your-bootstraps fairy tale crap.

And the trophy goes to…. Joe in LA!

Bravo

Fed policies have created a veritable army of large and small investors marauding the housing market to procure every halfway-decent deal in sight. How is the little first-time homebuyer supposed to compete in this ruthless arena?

“How is the little first-time homebuyer…” That’s first-time INVESTOR, my friend. Stop complaining or were going to classify your food an investment and retro actively capital gains tax it since your first started eating it from the moment you were born.

Try to step back and get the big picture. We are in the biggest everything bubble in history. That includes debt and assets. In the past these usually end in asset collapses. I think the thing to do now is get your personal finances in order and do all the research on where you want to live and be ready to pull the trigger.

The big picture is that all of this runs like a drug operation with addicts and dealers. The problem is that the dealers have become addicts too and are eating up the profits in advance of selling the drugs. If you don’t believe it, how do you explain the existence of schemes like GameStop which is another pyramid based solely upon getting their hands on different supply lines for the ones waiting for the next fix to get their blood going? The entire economy including housing is part of this trap and only a clearheaded and ruthless dealer will get on under these conditions. The Fed is crack house central and will control availability through their registered dealer sytem.

The Fed is inflating home and equity prices while dumping a higher cost of living on those without assets. That is the big picture.

The other aspect is that no one is building because the material and labor costs are too high to build at the entry level. It’s only profitable to build luxury. High priced homes are not selling as quickly as starter homes in each market.

You wait for the big crash like I did in 2009 and then you pick up a nice property for 50% off.

From your keyboard to the SkyGod’s ears!!!!

As much as I would love that to happen, you could be waiting in vain (and getting even more priced out in the process). Bank standards are tighter than ever. People buying today have the money. They’re not making any more land or building fast enough.

I can see a 10% drop due to factors Wolf has articulated, but I’m sorry to say I think that 50% is pie on the sky, especially since the Government is now bailing out everyone for everything. Next they’ll be baling out people that can’t pay for their monster trucks.

I wonder what is happening with all the people who bought tons of property to use it as airbnb short term rental, they must be deep under by now.

If you rent an airbnb and decide to overstay your welcome, you are protected by the eviction moratorium. Lots of owners have squatters now.

“Lots of owners have squatters now.” We’ve equaled Brasil with a stroke of the pen. And some America is becoming/is a Third World county. Hah on them!

It’s scary how the Feds go on a legal power grab every time there is a crisis. It’s like the foundation of laws that you thought society was built on only applies in normal times. In a crisis it’s all thrown out the window so the Fed elephant can squeeze a little more into your tent.

“And when the last law was down, and the Devil turned ’round on you, where would you hide then, Roper, the laws all being flat? This country is planted thick with laws, from coast to coast, Man’s laws, not God’s! And when you cut them down, and you’re just the man to do it, do you really think you could stand upright in the winds that would blow then?

Yes, I’ll give the Devil himself the protection of law, for my own safety’s sake!”

The laws are going down, and the wind is starting to blow.

@ Lisa Hooker…Man for All Seasons! Best screenplay ever.

“But since in fact we see that avarice, anger, envy, pride, sloth, lust and stupidity commonly profit far beyond humility, chastity, fortitude, justice and thought, and have to choose, to be human at all… why then perhaps we /must/ stand fast a little –even at the risk of being heroes.”

I will not give in, because I oppose it. Not my pride, not my spleen, nor any other of my appetites, but I do, l. Is there, in the midst of all this muscle, no sinew that serves no appetite?

“Lots of owners have squatters now.”

Couldn’t happen to a more deserving bunch. Airbnb has destroyed the rental market.

Destroyed the rental market and nice neighborhoods. Nobody wants to live next to a circulating motel of neighbors…

What no one is talking about the gross abuse of the VA loan program. This insures mortgages for Vets who have served their country and risked their lives in overseas contingency operations. It was never intended to be a ticket to rampant real estate speculation via owning multiple homes. It was intended to help the Vet get a roof over their heads raise a family and pay them back for the time spend out of country. I used the program myself. Now the whole program is being corrupted by greed and unscrupulous real estate gangsters, lenders and brokers. I see empty homes being refinanced and leveraged to the hilt while the owner goes and buys another house. Gross zoning irregularities like renting out illegal basement apartments are commonplace violating fire insurance regulations. I tried to bring these issues up to the lenders and Real estate people who have the responsibility to police these matters and found out these people couldn’t care less. Just like in 2006/2007 all that matters is making a quick buck. Get the up front commissions, lender fees, funding fees, and cash in while you can. The hell with the Vet. When the whole thing collapses it will be someone else’s problem. The Vet will also be the one getting screwed, but they don’t know it yet.

In my area, and with this market, the VA loan has been largely on the sidelines. No supply, and a ton of cash buyers = no seller wanting to wait for the VA loan process.

Money supply is just sitting on idle in the banks/market waiting for supply.

Another supply chain disruption.

VA, FHA, Fannie Mae, Freddie Mac –

all horrible for families ……………….

do nothing but drive prices

great for packagers and promoters banks and wall street and certain real estate operators and private equity and other financial types

USDA loans seem to be going to investors too.

The median U.S. household income in Sept. 2019 was $68,703 (FRED).

When I was 15 I had a summer job. The minimum wage was $2.10/hr. Wages have risen. The price of a house went up.

I suppose if people will move in together, homes will become more affordable. My aunt had to move in with one of her daughters after her husband went into a long term coma and died leaving her the medical bills. He should have written a living will to avoid being kept on life support too long.

I think that is the trend to afford a house.

Yes. Multi-gen family households will/are starting to become ‘popular’ once more. What’s old is new again .. except these times ARE different – Behold the Murikin Favela!

This trends been happening in many metro areas for many years.Just moved out of suburban Cook County,IL.Been seeing That trend for decades,but accelerated during the last twenty years.The beighborhood was originally built in the fifties for vets/young families.Small homes unless owners enlarged them which most have done.Original s.ft=900/3 &1 basic home with crawlspace,not basement.Grew up in that neighborhood then moved to Chicago,then Vegas,then soliconvalley right around corner from Google.

Came back from CA fifteen years ago.Upon coming back to childhood home,I noticed immediately the change in numbers of residents and type.While growing up,I haf classmates and friends from several countries,but they spoke sufficient English and were polite.Parents made great efforts to learn the language and culture.Their properties and cars were always well-cared for.Basic family unit.More recently it was the fact that the newer immigrants from Many countries may or may not have made an effort to assimilate by learning proper behavior based on cultural context.Attitude change to the -,a sense of entitlement was pervasive.Fewer badic family, units per home and lots of cramming in.Illegal basement,crawlspace,attic,garage occupants more than likely,not legally here and a good cash source for owner.House next door had garage occupants who were loud,peed outside,drunk,and threw litter in our yard-which I promptly returned.8-10 people and a mess of polluting vehicles just at that house! 2 hour semireprieve from the vehiculat pollution from 1:40a.m.-4:00,or there abouts.Horrible change.

Pretty normal in SoCal these days. I’ve seen new construction starting at $1M marketed with multigenerational pictures. Grandma, kids and grandkids lovin’ their new home together.

I haven’t seen Lennar building homes with “NextGen” suites in Texas, but they sure are a thing in SoCal. It hasn’t made homes one bit more affordable. It just means you live with your parents or in-laws.

I am sooooo cynical at this point, as much as it hurts my brain and piss me off to no end, part of me feels like in another couple of months, this line will shoot straight back up and prove all the house humpers right all over again, hot streak for them last 10 yrs with some dips here and there, then back to moon again Alice logic seems to be on their side forever thanks to Uncle Jerome and his predecessors.

Housing is like a religion especially in SoCal, trying to convince anyone else the whole thing is cyclical might as well be like trying to convince them earth is flat. House always win and so far these people buying at the top or before the top are all house. F me and my family for trying to find a none piece of crap place without paying through the nose..

People definitely feelin’ special for the prestige of paying $1.2M for 2 beds and 1 bath “only two miles from the beach”. Draped in utility lines.

There will be a sobering thing eventually.

From a social perspective, rising prices in

the burb and falling prices in the cities could turn out to a really good thing. For too long once you left the city

you could not afford to get back which helped lead to

this polarization played out on capitol hill. Here is for hoping we can get

more city to burb interplay leading to a greater appreciation and understanding of each other

Time for Mr. Market to throw a hissy fit. Interest can’t go up. It’s unconstitutional and un American.

Everybody knows – all the way to top of the Fed – that markets are going up because vaccines. If housing goes down it means vaccines aren’t working. The Fed has to make the markets go up or our vaccines won’t work.

This makes medical sense!

LMFAO!!

We are vaccinated (both shots). Our home value went up 6.7% last year! Looking forward to a larger increase in 2021. America is great!

Swear I read this in a marketwatch article and on reddit. We’re all winners when what a walrus waltzed what? Wow!

Many buyers are payment sensitive. Not only is the P&I increasing with higher mortgage rates, property tax is increasing as well. Some of the adjusted rates on the higher home values on current sales in California are staggeringly high.

“Many buyers are payment sensitive.”

Seems to be true wherever consumers borrow, and their thought process is: “Forget final bloated costs of this freakin’ purchase over loan duration– all I care about is: can I make my monthly nut (payment)?”

I’ll tell you why Wolf. Because there’s more sellers than buyers ;)

Anyway, with 3 trillion new dollars coming down the line, interest rate will head down again.

Interest rates will never go down again.

“Interest rates will never go down again.”

From a historical perspective that statement is dead wrong.

Economics follows natural laws by reverting to mean eventually (nothing in existence grows endlessly to sky– human activity is not exempt from natural law).

The only things debatable about housing market faltering and reverting to its mean (with a nasty undershoot to boot) are the ‘when’ and ‘how’.

I wouldn’t give current clown car insanity much further life expectancy, despite herculean efforts of authorities to maintain this gravy train that is enriching so many opportunists of all stripes.

I think he is saying what you are saying. Reverting to the mean would imply interest rates can only go up, not down.

I checked my house worth on Zillow yesterday. My eyebrows flew up a bit

At the bump. Sure I am tempted to sell

But where would I go ? Can’t beat what I have here in the Olympics.

Bet –

In the Olympics, you have pleanty of fresh water, a moderate climate year around, relatively low population density, mountains, rivers, a Pacific coastline, etc.

Rest assured, the people are coming…

And someday soon, a huge megathrust earthquake.

EVERY region has it’s ‘down’sides. In the above example, I’d have a ringside seat on the ride of Subduction!

Tis what bottlenecks are made of.

And you think the Rockys are static? Guess again.

Polecat, no place on Earth is static, but the Rockies are safe compared to Cascadia. A great read on this is “Full Rip 9.0” – not sensational, just the geology. But the PNW is a beautiful place.

Hopefully for Bet’s sake, nobody in California will figure out where this magical place of “Olympics” is. Is there an income tax?

And plenty of junkies looking to rip off anything not bolted down. The worst place I ever stored my expensive RV was Sequim, WA. The thieves are as thick as flies. And did I mention the extremely low pay and limited employment opportunities? Oops, didn’t mean to harsh OutWest’s Kool-Aid buzz.

Are you trying to keep Sequim from becoming too crowded?

One of the best places to live in the USA IMHO.

Wish we never moved out.

“Are you trying to keep Sequim from becoming too crowded?

One of the best places to live in the USA IMHO.

Wish we never moved out.”

Perhaps you left in the Stone Age and it’s changed? Because you’re delusional.

My Chances of Becoming a Victim of a Property Crime

1 in 24

in Sequim

1 in 37

in Washington

Sequim crimes per square mile: 53

National median: 28

The fact of the matter is that Sequim, WA is a backwater town full of junkies with extremely limited economic opportunity. You’re not going to fool a native.

Here in WA (just south of Vancouver, BC) buyers are still biding up properties over the asking price. Do not see this slowing down anytime soon, as most properties selling within days with multiple offers.

Sounds like where I live in northern Idaho. But the problem is, a person can sell and make some money, but then can’t afford to buy locally (unless they downsize, but at an inflated price). This scenario is best for people who want to exit the area and move elsewhere.

And where can one go that would be any better? 15 years ago the Idaho land offerings were everywhere….I used to read the listings. Now, it’s a flee destination.

For the Minnesota comment up above I have one comment. If you like bugs and winter….. Good fishing, though. I used to work there and in NW Ontario. In fact, worked all over northern Canada. Bugs own all the RE; blackflies and mosquitos. You can’t walk through the grass without getting ticks. On the west coast, my last house didn’t even have window screens, didn’t need them. My newer place does have screens because the windows are new, but don’t need them. You can’t put a price on not being eaten alive when the sun shines.

My wife used to live in MN and says the state bird is Mosquito.

And some of the best people in America.

In central Ontario, North Bay, Algonquin Park, etc. the Blackflies are intolerable in May and the mosquitoes peak in June. After that, window screens and a little bug juice make things tolerable. After the first frost, the tree colours are beautiful and the bugs are gone, so Fall is my season.

Some people love winter, some don’t. What I hate is extreme dry heat because I grew up in northern Alberta where 80F was considered a heat wave. Each to his own, and I like living far enough outside Toronto that the population pressures are moderate.

The mosquitoes in MN have “N” numbers on them.

Spent some summers in Alberta visiting former neighbors who moved to Edmonton. First trick they taught me when going for a walk in the woods was to break off a tree branch and sweep it in front of your face, shoulder to shoulder, to keep the flies at bay.

Paulo – you forgot the worst part about constantly scratching the no-see-ums, inhaling vast quantities of them, and trying to blow them clear of your nose.

Forty years ago I said that in this buy-to-sell out, we would all end up in Moosejaw. Looks like even that won’t be possible.

That’s the case in SWFL too. I watch listing pretty closely and almost every decent home is ‘pending’ within a few days (sometimes the next day) of being listed.

There is nothing in the way of 50yr mortages. No one pays off a mortgage if it can be churned and flipped .This way a house that is selling for 300k is now 800k . This is one of the tools in the fiat tool kit. It will stop only when the rest of the world stops giving their production for our non-performing debt. The sky is the limit untill that happens. We should already be requiring a pre-invasion deposit from helpless countries we attack to bridge the cost until the rest of the world ponies up to pay for the attack by buying our debt.

What you need is a perpetual 0% mortgage. You just live there for free. And pay 3% property tax on your $10 million starter-shack :-]

Consol bond-age?

I believe in the Netherlands you have mortgages where a significant part of your mortgage is tied to a savings plan which – over the term of the plan – is designed to repay your mortgage with tax free money. So it is effectively close to 0%.

Interesting point, so if they (govt) implements no cost lending, can they raise property taxes? Shift funds from private banking to public coffers.

“You will rent everything/own nothing, and be happy” – C. Schwab

Labor force participation rate is currently at 61.4% It is simply not possible to have a booming economy capable of sustaining a house buying boom when only 6 out of 10 people are in the work force.

Americans since 2008 have developed a really serious case of normalcy bias. Even now with everything wrong with this economy, many people are convinced that going into debt and purchasing assets will pay off. They are gambling, not investing.

We are currently in an economic recession, with no or negative growth even if you do believe government massaged statistics.

Now there are three possibilities, and two of them are not good.

People are putting a lot of faith in the COVID vaccines, and believe that they will drastically cut the infection rate and the economy will improve.

That is the best case scenario.

Another possibility is that the vaccines will not be effective against the 5 new strains that are now spreading and we will continue, much as we have been, to still have wave after wave as the medical community tries to play catch up with the constant mutations and the now growing transmissions.

That would mean we stay where we are which is not good.

The last scenario is that the vaccines actually become detrimental to treating future strains due to ADE or viral escape. In this case the infection rate could possibly get much worse that anything we have yet seen. That would be catastrophic for the economy as we could expect event more draconian shut downs than we have seen in the past.

So basically we have 3 scenarios. Things get better, stay the same, or get worse. 2 of the 3 would be bad for the economy….

I think on average Americans are poor with financial decisions, maybe due to poor parenting, Feds encouraging poor behavior or poor education.

Last I read on average 401K investors do very poorly compared to an index over their lifetime. On average people take on the most debt to buy stocks and homes at the the top end of the market.

Fidelity did a study that found best stock pickers were dead people. Number two was people who forgot they have account. I have mba finance which deluded me out of index fund. The more time I spend researching, the worse the result. Recently, I just buy insane bullshit for short term including GameStop. Much better results. It’s either that or watch the money disappear to inflation

Buy gold.

Those who practice insider trading do better including those who know the secrets carefully buried due to our accounting systems loop holes. I also made money on gamestop but that was like rolling dice for fun. Insane pretty much describes our stock market as it did the one in 1928s.

The Little Book of Common Sense Investing by Bogle ought to be required reading in high school.

I took economics in high school. We were told to find a job and make a budget according to our income. I “figured out” how to drive a Corvette while working in a call center. Teacher gave me an A.

There will be a wave every fall/winter with or without the vaccine.

If you take a step back, turn off the news media for a minute, the pandemic is roughly on par with the 1957 flu pandemic.

In every scenario, it has to run its course, and interfering with nature just hurts future generations.

Turning shelter into a speculative orgy is the most heinous of acts. The last time I said what I really thought should happen to central bankers, Wolf deleted it. Think “French Revolution.” It’s what we desperately need. Society would be much better off. We’re past the point of playing nice. Drive around the homeless camps in every city to see what these greedheads have done to America.

Depth

You hit the nail on the head!

France never recovered from the Revolution. After the Great Terror where about 70,000 were executed with the guillotine ( aka: the Republican Window) including many of the original leaders, the Revolutionary Govt was being chased through Paris by a mob. They sent for help and a certain Captain Bonaparte arrived with cannon and administered the ‘whiff of grapeshot’. The Revolutionaries were so thankful they promoted him, eventually to general. Twenty years later a third of Frenchmen of military age were dead, 400K being lost in Russia alone.

Today if you ask someone, ‘which developed country do you associate with a class system? they will likely say the UK. In fact, the UK is far more egalitarian than France. One thousand people in France run the country and no one has risen from humble origins to the top job. Thatcher was raised above her parents’ grocery store and PM Major’s father was a trapeze artist, fathering Major. JR, in his fifties.

Evolution was better than revolution.

Moving to the problem of US inequality, wouldn’t the first step in evolution be to reverse the last admin’s tax cuts?

I second you and have mentioned this many times. But don’t expect any revolution of any kind. Why do you think Govt is sending $$ aka pittance to every Americans ?

Yep!!videos of Venice Beach,Santa Monica,elsewhere!Truly affordable housing is very doable.Convert empty office/warehouse/malls.Eventually it will happen unless certain entities Want the crumbling,urban blight so as to depress people and make them maleable,mmmmm????????????!

Great charts and data Wolf, as always. The median home price graph seems to be on a consistent rise post-GFC, continuing in the same trajectory this year. All of this is consistent with EZ QE $$$ and Fed rate suppression.

Median home price trajectory should arguably be higher considering lack of inventory. As shadow inventory + foreclosures hit the market, along with some interest rate increases, prices might flatten a little on the lower priced homes.

Yellen got to be head of the Federal Reserve and head of the Treasury after making some silly statement about there not being a housing bubble before the biggest housing bubble in history nearly took down the housing system.

Here is someone who couldn’t see or didn’t want to see the obvious. All DC wants is fiat debt and they will be around to print more when the next bubble bursts.

Who’s winning ?

— “Banks” who collect empty, unsupervised homes ? -or-

— The squatters occupying them ?

The banks always win because you bail them out when they don’t.

Invest in banks, then?

“House craziness cant last” technically you’re right but it can, I think, last a lot longer, US is a few trill deeper and currency is still ok, no reason to think the same wont be repeated several more times. I dont know what happens when the everything bubble goes bang but safe to assume it will make the present look great so enjoy it.

Everything is in price discovery mode which means the bubble popped and the remaining musical chairs are being identified. If the bobble was going to pop in the near future we would be looking for price discovery to take over which it has. Have fun everyone.

I hope you’re right but I’m not seeing much price discovery right now. I just see speculative excess.

Ricky Gervais:(while playing the guitar) Oh, yeah, can you feel it? Just over the credits, just riffing now. Words. And chords. Not the poetry in the…real thing, but not bad for an ad lib. Not good, but— (stops playing but the credits are still rolling) New car, caviar, four star daydream.

Think I’ll buy me a football team. And it’s not long enough, so I’ll just do a little bit more (plays a little) of this, nearly done—Money, well get back. I’m alright Jack, keep your hands off my stack. (strums) That’s the final credit, yeah, that’s the end. (clears throat)

Nice! I also love George Carlin’s “Advertising Lullaby”…

I live and work in the city. Many of my coworkers had been long term city renters. In the past year, from my team of about 30, six have bought houses outside the city. I think there’s a big renter to buyer shift driving at least part of this.

These are folks who can’t work from home, so they are trading city life for a commute.

I think a lot of the surge in housing, especially in warm climates, is the VRBO type renting. This has made renting properties much easier, and, with the low rates, many who are looking for SOME return on their money have bought and thrown it under a management and into the rental pool.

Second thought is ..What is all this mortgage paper going to be worth if the Fed gets their way with inflation? 2.5% inflation suggests that long rates would be up around 4%. All these mortgages written at 3% or less are then in a bad spot. These central bankers are leaping into their own you know what.

What’s the 10 year then? The central bankers are forcing everyone one way, then forcing them into losses the other way. How about “Get out of the Way” Mr. central banker?

“For every action, there is an equal and opposite reaction.”

Wouldnt some of this make good questioning for Mr. Powell.

VBRO’s are quickly replacing hotel rooms as vacationers first choice for a variety of reasons. First and foremost is that many of these homes and condo’s offer a superior level of luxury and amenities for basically the same cost. Also having a kitchen and outdoor grill gives vacationers the option to cook at home and avoid restaurants which are arguably the most risky environment.

This is definitely driving the housing market in vacation area’s but IMO will be a short lived phenomena as we will reach a point of market saturation making vacation rentals less profitable and therefore less attractive.

I would also expect the corporate owned hotel chains at some point to collectively lower hotel rates in a old fashion price war to eliminate at least a portion of the competition.

1) The Median Home price chart : a Lazer trending up.

2) Put a dot between every V shape open space.

3) The next dot might be inside an inverse V shape.

4) If correct, this dot will be a swing point. The following dots might aim lower. There will be a change of character in the housing market.

5) The line between the first dot and the swing point is the spinal cord.

6) Swing arches :

a) for an uptrend options.

b) for TR.

c) for several potential downtrend options.

7) Angela Merkel locked down Germany to fight cv19.

8) That might lead to European recession.

9) In combination with the vaccine, it might lead to ==> a successful victory in the next election.

7: Angela Merkel locked down Germany to quash the protests and keep them from voting in the upcoming national elections, where her already losing party will lose more seats.

9: The lock down will piss them off more. Expect more unrest => 1932.

Petunia,

#7 hilarious… no, Germans don’t have to leave the house to vote. And no, that’s not why she extended the lockdown. They have a massive surge in cases in Germany. And Mutti does care about the health of her underlings.

#8 correct. These protests (anti-lockdowners, anti-maskers, anti-vaxxers) bring together people that are at the opposite ends of the political spectrum and would normally fight each other tooth and nail, and now they’re all on the same side.

10) Mutti gets an impromptu ‘Ceausescu body lengthening’.

When did they start covdjabs,mmmmm?????

Ironic. Compared to Germany the US looks on the brink of civil war.

1) You cannot day trade houses.

2) If u could, by making only 1.5%/ per week, flipping will make

==> 1.015^52= 2.17.

3) Flip every two weeks : 1.015^25 = 1.45.

4) Those who had a huge unrealized gains in NYC and SF can pyramid in the flyover cities. They don’t have to put their apartments in the market.

5) They will wait for a rebound, because the WB 100Y trend is always up, since 1932.

6) The flyover don’t sell because there is nowhere else to go.

7) When the flyover trend will change it’s character, NYC + SF lead the downtrend.

Chinese home prices are up almost 17% over the past year. I used to think China housing was a bubble. It took so many years of a person’s income to buy a house. A billionaire said it was a bubble and sold his real estate holdings. Wages kept going up. Chinese home prices were down low single digits in 1999, but not this year.

An elderly couple in my community posted in the local community Facebook page they were low on funds and were selling their home and going to use the funds to rent. Medical expenses are a leading cause of personal bankruptcies. Good nutrition and good health are assets. A house has some equity that may be used in case of emergency.

Sure thing! By then, the backup plan is to embrace Cardboard Box Living .. under a freeway overpass …

What a Country!

Didnt the elitecabal suggest ikea sheds while they get pallacial mansions,yachts,helicopters,several homes,penthouses,several lux cars,limos,privatejets?But,But,climatechange n stuff!

Those charts support the notion of a Fed supported housing market. 2011 is when Fed stepped up to the plate; taper tantrum, OP Twist. They decided they were never going to back away. Absent forbearance they have pushed housing higher through a pandemic. Amazing. I thought they would nationalize oil before housing, (every other nation has a government owned energy industry).

Nationalize? The United Families of Makemerica Great Again thank you for your patronage. It is wonderful of you to be so willing to finance their gains and cover their losses without ever expecting any form of ownership stake. Please leave your donations in the tour-of-homes basket on your way out the door, which will be promptly locked before the next round of counting resumes. Don’t forget to vote..we have chosen your candidates to streamline the process.

I keep thinking Congress is going to call their marker with corporate America. So far not happening.

Fed owns roughly a third of housing (through MBS purchases) now and they continue buying housing debt out the wazoo.

Think about it: did they create that much and then buy $2 TRILLION worth of mortgage backed securities from the financiers for pleasure? While the supply shortage from the pandemic is decreasing the supply, when that supply goes up, if hyperinflation has not taken off yet, then the prices of many areas will drop like stones.

For example, I do not think that working from home is going to be the preferred way of working in future years. It just is not practical for most jobs. Thus, the people that moved away will eventually have to sell and move back.

One factor that may ameliorate the severity of the US dollar crisis is actually fear of communist China. Too many people around the world will not want the USA to lose its reserve currency status and go into a deep depression that disables its economy and cripples its military. Our allies may bite the bullet and keep taking US dollars out of fear, and the dollar collapse and hyperinflation may be delayed long after we have created them by the trillions for years. If I were president, I would see no choice but to pursue the same strategies that FDR tried and the US desperately needs infrastructure.

“The share of second-home purchases as percent of total home purchases has soared to over 6%, a high in the data series by the AEI’s Housing Center”

It seems like the real number is much higher than 6%. Nearly 50% of the houses we’ve gone in were vacant. Anyway the trend is up and that is not a good thing. Especially with the VA loan program. It was not intended to subsidize speculation, but that is just what is happening.

You fools houses haven’t increased money increased thus inflation of money causes this at some point 50% drop but don’t get in wait another 20 % after that most people buy more than they can afford also everyone bought second condos in Florida after reset going to collapse

Please use punctuation next time.

That is Ron’s “thing.” He is either a top secret quantum computer AI spying on and conversing with Wolf and his readers, or someone using voice to text.

I pick door no. 1.

Ron ==> James Joyce style.

Yeah, the old stream of consciousness. I’d do it too, but my primary school teacher may rise from the grave to haunt me.

Just a geography lesson…

Take a map of the US and divide it into quadrants then locate where you live. I can bet most people who claim to live in the Midwest actually live in the North East. They need to change that imaginary geographic distinction. The Midwest is really Colorado or Utah!

Nah. The mid-west is Northern California, halfway between Mexico and Canada. Just ask them.

Lol, I live there, a purple town in a sea of red. You are correct.

Somehow, we are not going to worry about The Real Estate market.

After all:

THE “FIRE” Sector reveals the greatest accumulation of wealth for the Super Rich is:

Finance

Insurance

Real Estate