In an investment environment where nothing matters anymore – until it suddenly does.

By Wolf Richter for WOLF STREET.

In the current craze that encompasses everything from sneakers and NFTs to stocks, where valuations don’t matter because of widespread certainty that valuations will be even greater in a few days, and where folks are chasing lottery-type returns, supported by the Fed’s interest rate repression and $3 trillion in asset purchases, and by the government’s trillions of dollars of handouts and bailouts – well, in this perfect world, there is a fly in the ointment: Vast amounts of leverage, including stock market leverage.

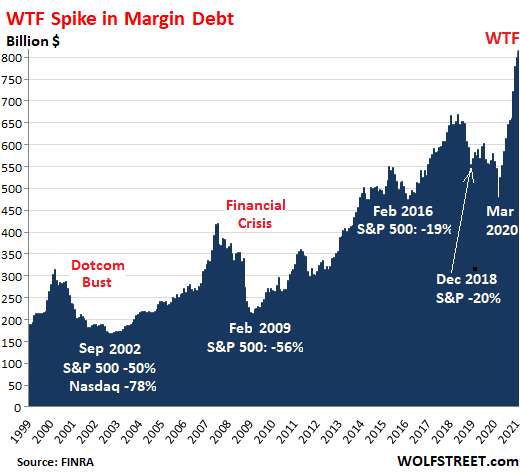

Margin debt – the amount that individuals and institutions borrow against their stock holdings as tracked by FINRA at its member brokerage firms – is just one indication of stock market leverage. But FINRA reports it monthly. Other types of stock market leverage are not reported at all, or are disclosed only piecemeal in SEC filings by brokers and banks that lend to their clients against their portfolios, such as Securities-Based Loans (SBLs). No one knows how much total stock market leverage there is. But margin debt shows the trend.

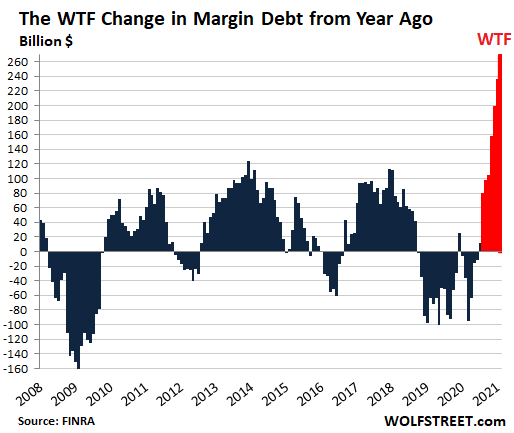

In February, margin debt jumped by another $15 billion to $813 billion, according to FINRA. Over the past four months, margin debt has soared by $154 billion, a historic surge to historic highs. Compared to February last year, margin debt has skyrocketed by $269 billion, or by nearly 50%, for another WTF sign that the zoo has gone nuts:

But margin debt is not cheap, especially smaller amounts. For example, Fidelity charges 8.325% on margin balances of less than $25,000 – in an environment where banks, money market accounts, and Treasury bills pay near 0%. Margin debt gets cheaper for larger balances, an encouragement to borrow more. For margin debt of $1 million or more, the interest rate at Fidelity drops to 4.0%

“Whether you need extra money for a short-term financing need or buying more securities, a margin loan may help you get the money you need,” Fidelity says on its website. In other words, take out a margin loan to buy a car or much needed bitcoin or NFTs.

Every broker has its own margin interest rate schedule. Morgan Stanley charges 7.75% for margin balances below $100,000, compared to Fidelity’s 6.875% for balances between $50,000 and $99,999. For margin balances over $50 million, Morgan Stanley charges 3.375%.

And it’s risky leverage for the borrower. It seems like risk-free leverage when stocks go up, but when your stocks do the unheard-of and tank below a certain level, your broker will ask you to put more cash into your account or sell stocks into the tanking market, whereby you then join the legions of forced sellers.

In the past, a big surge in margin balances tended to precede history-making stock market declines:

Over the two-decade period of the chart, the long-term changes in the dollar amounts are less important since the purchasing power of the dollar with regards to stocks has dropped.

But short-term, the changes show what is happening to margin debt in the run-up before the sell-off, and what is happening during the sell-off when margin requirements turn investors into legions of forced sellers.

Leverage is the great accelerator of stock prices, on the way up, and on the way down. Purchasing stocks with borrowed money creates buying pressure, and prices rise, and rising prices increase the margin balances a portfolio can support, and this encourages more stock-buying on margin.

On the other hand, selling stocks to deal with margin calls adds more selling pressure to an already declining market. The more prices fall, the more selling pressure there is from frazzled forced sellers trying to deal with margin requirements.

Then at some magic point, margin debt has been reduced enough, and its contribution to the selling pressure fades.

The historic surge in margin balances in recent months is another indicator of how hyper-speculative and blindly courageous the mega-bubble has become. All kinds of new theories are being proffered why fundamentals and valuations are meaningless, and why prices of all assets will shoot to the moon, no matter what.

These theories smacked into the bloodletting in Treasury bonds and high-grade corporate bonds with longer maturities, as long-term yields have been marching higher for months, which I discuss in my podcast…. THE WOLF STREET REPORT: Market Manias Galore, But Long-Term Interest Rates Smell a Rat

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Powell was one of Trump’s worst appointments. He was recommended by Mnuchin, the California liberal who donated to Gore, Kerry, Obama, Clinton & Harris. Powell’s economic philosophy is practically identical to Janet Yellen’s, a known liberal democrat. Powell himself was a former obama nominee (as a regular FOMC Governor, not chair)

Brian Taylor, known for the Taylor Rule, was Trump & Pence’s preferred candidate for FOMC chair until Mnuchin convinced him otherwise. Monetary policy is far too powerful & prone to abuse to not be bound by rules.

Powell should be trying to talk down this bubble and extinguish it. Instead, he dropped a zephyr full of gasoline onto an inferno. Reckless does not even begin to describe this financial terrorist. Diabolical is more like it.

Extinguish it will mean and end to his own personal wealth increase. Let’s see this summer how his personal assets managed by black rock has doubled once again?

Arguing the right thing is a waste of time by now. Or it has been for a long time.

I’ve had this discussion with professional ‘economists’. As soon as you bring up the term bubble and I’ve used it for five years, they assume that you’re predicting an imminent crash.

It should be clear to anyone by now that this is a managed bubble that requires frequent monitoring by authorities and calibration of monetary stimulus as needed. The chronology of events during the 2009 to 2021 period clearly shows periods where the central banks injected funds, directed pension funds and other large funds to swap out of treasuries and into equities, and used negative deposit rates to push more money into US assets.

Critics of the bubble scenario are also tripped up by the fact that the monetary authorities often give advance notice to allow large private investors to mark up assets before the purchases commence and that extended periods of zero interest rates and currency manipulation can work in similar way to QE.

The transition out of the Weimar Republic Hyperinflation and preceding the takeover by the National Socialists, might be instructive to recklessly printing money to inflate (mostly) paper assets.

I know you love your right wing media… But please Google what you are about to post.

Minchin has donated $400k+ to the GOP. You can call him a RINO… but he is a conservative.

You forget that like Biden… Obama appointed republican’s to try to be by partisan… Because they are fiscally conservative.

But this is why you don’t negotiate with terrorists… They are just going to deny reality and label everyone they disagree with a liberal or socialist.

Monetary policy is far too ‘blunt’ an instrument. Best that it be left to manage daily check clearing and very short term interest rates. What Yellen and Powell, and Mnuchin during the Trump administration, are trying is a very inept use of fiscal tools, primarily money (and debt) injections in an effort to fill a gap in spending caused by the pandemic infused recession. That gap was more than $5 trillion. There is another fiscal tool. It’s called taxes. Reversing the Trump tax giveaway should be done. That tax windfall is responsible for the asset inflation we are witnessing in the financial markets.

Stock up buy using cash and dividend – stock down use margin .

Stock drop 70% no need scared the whole world will be bankrupt but who the hell borrowed at 3%.. margin loans are at 1% with private banking.

the whole idea of central banks is that 1929 doesn’t repeat..

if the stock market crashed 70% the 401k would be gone… it will not happen however a 30% drop is possible in that case just buy more using margin whats the problem at 1% interest… ???continue to wait 6-8% devaluation of your money for sure..

I wonder what fraction of that debt is from large accounts, and what fraction is from small.

If I were to guess, its “all of the above.” I can see everyone from babyfaced Reddit traders to seasoned daytraders to big fish taking on tons of debt.

Every regular on this site *knows* a correction is coming, but I’m interested in who will be left holding the bag.

If you don’t know who the mark is, you know who the mark is.

They have been talking about a market crash for many, many years. As long as the Fed is in control it’s not happening. Just print up some mooore is all they have to do and they will. jmo

john,

We had a HISTORIC crash in February/March. Did you already forget? Oh my, how time flies.

“We had a HISTORIC crash in February/March. Did you already forget? Oh my, how time flies.”

Wolf – if you blinked it was over with. We didn’t even get back to any reasonable valuations. DOW 10,000 would be a good start.

Depth Charge,

Look, I made money on that crash. It was real. Don’t say it didn’t exist.

In addition, we had a 20% sell-off in late 2018. There was a 20% sell-off into early 2016. This is when junk bonds blew up big time. People keep forgetting all this stuff that happened what we have described in these pages here.

A crash doesn’t mean markets are going to stay rock bottom for 100 years.

I don’t deny there were minor corrections, but I just don’t call them a crash. They were too brief and the rebounds all too fake. This entire market is a rigged sham.

I certainly do not doubt, however, that you made a lot of money. You’re a very smart man and I love reading your content. I’m just a free market capitalist, and what we’ve had my entire life has been crony capitalism and rigged markets by a corrupt banker cabal. I’m not one of the beneficiaries, I’m one of the losers.

DC has a point, Wolf.

Lots of people, including analysts at Goldman Sachs, etc, were predicting a further epic decline of the stock market to historic lows, a halving of the Dow, SP 500, etc.

I thought so too, and completely missed what I will now call the “Wendy Buy Signal” (to give her full credit for having posted about this here a couple years ago), which is that when the market has crashed, the VIX skyrockets to over 30, and the Fed suddenly drops the Fed Fund rate to zero or close to it, that you should buy, buy, buy stocks.

Yeah, I even watched, agog with disbelief, on “60 Minutes” the Neel Kashkari interview where he said, Don’t worry! We will make sure there is enough money! We will do whatever to pump things up! Or words to that effect.

Shoulda coulda. I wonder if Wendy made out like a bandit again in that one.

Gandalf,

“Lots of people, including analysts at Goldman Sachs, etc, were predicting a further epic decline of the stock market to historic lows, a halving of the Dow, SP 500, etc.”

I didn’t think so. That’s why I covered my short. This was a huge crash, with gigantic volatility, and declines in single days going up to 12%. Here is one of the charts I published about the time I covered my short:

Everyone in the stock market except maybe some lucky value investors will suffer real losses but rising inflation may cover them. This is like 1920s to 1929s’ over use of leverage in the stock market that led to that crash.

I predict a huge crash made less visible by rising inflation due to hyper QE by the banksters’ (not government owned but deceptively named) “Federal” Reserve to protect its banksters and their cronies.

If we have 50% plus stock market crash it will temporarily take down more than 495 of 500 of the stocks, but the best will survive if you can hold through it.

when u sell your money devalue by 6-8% a year… when u hold your stocks goes up if drop dividend and money come in just buy more…

The people that are not vested are left with holding onto eroded cash.. yearly.

infinite amounts of money chasing a finite amount of good stocks..

So what happens if you can’t pay your margin debt?

Does Fidelity send Guido over to collect? Is it all unsecured debt?

The broker sells shares until you’re paid up, for whatever the market offers.

Harrold,

The absolute beauty of margin debt (from the broker-lender’s perspective) is that it is 1) fully secured by the stock it is used to buy and 2) the broker-lender can immediately and easily liquidate that stock if you fail to maintain margin/ignore margin call to add new money.

In other words, the broker is fully collateralized and has control over the collateral (the stock).

Most people don’t get how banks/lenders really protect themselves when lending – they do it by getting collateral/putting the borrower in the “first loss” position.

For margin loans,

1) With $50 down, you can borrow another $50 to put a total of $100 into a stock (this amt of leverage may be high but simplifies the math).

2) But…if the stock falls to $80, *all* of the $20 in losses is charged against your original $50 in equity…netting it down to $30.

4) But since 50% margin loan coverage is always required and your now $30 in equity is against $80 in stock…you gotta cough up another $10 on a margin call to raise your equity to $40 or,

5) The broker-lender will cash out enough stock (which it holds and fully controls) to restore the 50% required margin (the ratio between your equity and the current value of the stock/collateral).

The key step is #2 – any interim losses in the market value of the collateral are immediately and fully charged against the equity of the borrower – thus providing the lender with a “cushion” of collateral value loss that can occur before the broker-lender is out a single penny.

The exact same dynamic applies with mortgages, 20% down payments, and home equity (albeit slower and with less precision).

Borrowers need to understand that they are always in the “first loss” position if the value of their loan collateral declines – their equity takes 100% of the hit before the lender could be out a penny.

This is how lenders protect themselves and get rich – they lend against things/collateral that are unlikely to lose 20%+ or 50%+ before the lenders can take them over and liquidate.

The poor schmo borrowers get fully annihilated (their equity zeroed out) before the lender might lose a penny.

(This dynamic is crystal clear in CLOs where the paint huffing owners of the bottom “equity tranche” absorb 100% of CLO losses before the next lowliest tranche loses a dime. The cheerleaders at the bottom of the human pyramid drown, before the next tier even gets its hands wet)

I don’t like to borrow money, so I know nearly nothing about leverage. How long do the margin lenders give you to make good on the margin call before foreclosing on the collateral (the forced sale of the equities)?

I don’t like to borrow money either, so I don’t follow broker level specifics.

But my guess is that broker-lenders won’t wait long because the market values can move so fast with stocks.

And broker-lenders never want to be in a position where a fast 50% loss zeroes out borrower equity entirely and endangers a dime of the broker-lender’s share of the collateral.

In practice, the highest volatility/most dubious stocks are denied margin loans by brokers.

Those stocks are known/thought to have prices/values that move too far, fast, and unpredictably for even the risk-insulated broker-lenders to mess with.

Brokers and banks get rich by charging interest for appearing to take on more risk than they actually do.

(Always gotta read those loan documents)

I believe accounts have to settle at close of business day.

If all investments of a borrower go down rapidly, its/his/her securities account may not be enough to cover margin. Remember 1929.

It really depends upon how stupidly overvalued stocks get…and if a broker-lender would actually margin lend against the worst of them.

With 1 for 1 leverage ($50 in gets you a $50 loan to buy $100 in stock) the first-loss-to-borrower dynamic means that the $100 stock would have to fall to $50 very, very quickly (like minutes…before the continuously monitoring broker could sell off the stock collateral) before the broker-lender would be at risk of losing a dime.

Since that is extremely rare (except with the absolute crappiest of stocks – which brokers won’t lend against) it is very rare for broker-lenders to take an actual loss.

Lenders *love* decent stock collateral for these reasons,

1) The high level of required collateral is very easy to almost always reliably value and,

2) The stock collateral is very easy to almost always quickly and reliably liquidate.

Now, compare that to home mortgages, with just 20% down payments/equity cushions (or 5%…or 3%…or 0%…).

And, in a housing implosion, the home/collateral might take *years* to liquidate.

Now that I think about it…8% for a margin loan is *insanely high* when home mortgages are less than 4%…

Lest we forget – when a stock bought on 50% margin falls through $5 (last I recall) the margin goes away and you will get a call to ante-up (24 hrs) to 100% of the current stock price. Cost me big $$ of profit on a short.

Oh, c’mon everybody. It’s time to margin out on some Tesla and Amazon stock. It’s been a sure thing. Never work again.

As a percentage of GDP (very roughly):

’99 – 1.6% (pre-derivatives)

’20 – 2.3%

’21 – 3.7%

yeah?

This seems to be doing more than tracking the market.

Wiltshire 500 / GDP

Peak in

2000 1.41

2007 1.05

2021 1.91

Holy S77t!

Fed announces no rate hikes THRU 2023.

Is Powell psychic? How the hell does he know what will happen in the next 33 months? Is he saying if inflation reaches 4% there will be no change in rates?

Why not just say: ‘steady as she goes and we’ll see how things play out’?

Guess that is no longer enough.

Someone has asked WR: ‘what would you ask Powell?’

How about this: ‘Chairman Powell: if you were unable to hear any news about stock markets for 10 days, could you still your job?’

Typo: ‘still do your job’

Well the mid terms are November 2022. Can’t let anything unwind until then.

Don’t you know that the Fed will keep reporting inflation at 2% until after next presidential election? I mean….it’s pretty simple.

Called my congressman to insist that since everyone knows that 2% inflation is necessary any minimum wage bill ($15?) must include a 2% per annum automatic increase. Kind of like the COLAs in 1970’s union contracts that helped get us some really great inflation.

Anthony,

The Fed does not report inflation, the BLS does.

CNN headline: ‘Powell says no hikes until at least next year’

CNBC headline: ‘No rate hikes through 2023’

Am I misunderstanding American English? I thought not happening ‘through 2023’ means not in happening IN 2023. Or does it mean not until 2023 ? Or is this just CNBC going overboard in their usual job of making things rosy?

Within limits that’s free speech, but are they misquoting such an important announcement?

Sorry to persist but Just noticed CNN headline ‘no hikes until at least next year’ allows possible hike in next year, 2022. So one of these news sites has it wrong.

It is only important if it were honest.

Fed/G “promises” are literally meaningless…only intended to shape/condition/brainwash public actions *today*.

If the Fed “needs” to raise rates because inflation of 15% in 2021 can’t be hidden…it will do so. And the reverse is also true.

Monetary Macroeconomic textbooks talk about the central role of “surprise” inflation/deflation upon mkt outcomes.

What they don’t like to talk about is how often those “surprises” are the result of conscious Fed/G deceit.

The Fed/G doesn’t have a contract with us…they will do what they think serves their (“our”) interest best at any given moment.

That’s not “free” speech nick, it’s really expensive speech. CNN charges a lot to lie like that.

nick kelly,

You’re misunderstanding the Fed’s statement. What the Fed “announced” was no rate hike at THIS meeting.

But the dot plot shows the projections of each committee member, and the median of that dot plot shows the median projections of rate hike expectations by the committee members.

There was no “announcement” of rate hikes, neither in 2022 nor in 2023. There is no schedule for rate hikes.

But Powell said what would and would not trigger rate hikes: metrics of unemployment and inflation.

Also the sequence is:

1. taper asset purchases to zero.

2. wait and see.

3. raise rates.

Even that statement from him is nonsense. They’re basically trapped, and playing it by ear. They will raise ahead of time if they can see the dollar weakening too much, as that’s the source of their power, or if inflation is becoming unbearable.

CNN headline: ‘Powell says no hikes until at least next year’

‘There is no schedule for rate hikes.’

Not having a schedule for rate hikes does not exclude one. Saying no hikes until at least next year does exclude one.

@RightNYer

Not with the amount of debt they are piling on.

Say whatever you like but that last stimulus was not only largely unneeded, but mostly misdirected.

But no big deal, 1.9T, another 2 to 3 on deck with infrastructure, although this one will be done through taxes. If they manage to reduce Gate and Buffet to less than $10B when all of their assets, foundations, “charities” (AKA tax shelters) are drained of assets, then we can talk about how fair taxes was this time.

The future sequence is:

1) feed more to unicorns

2) watch unicorns get fatter

3) go to step 1

He wants you to believe that they are not going to raise rates so that you will make decisions based on that believe. They don’t want the wealth affect to disappear until he gets the bathtub full. Never take personal finance advice from a central banker unless he is retired and can tell the truth.

Even better, the margin debt (leverage) is being used on leveraged products (options, 2X & 3X ETFs) creating [leverage]^2.

What could possibly go wrong? To the moon!

And though not a big percentage, I’m sure there are plenty buying options ON leveraged ETFs with margin leverage.

[leverage]^3

With all this gambling on growth, perhaps it’s time to introduce the “swab-o-meter”? Paper-stick single-ended cost what for a regular pack in the 1960’s? Now plateau at 300 of the double-headed fish swimming all the way from China to eat a measely buck for several years going. And taking up a cargo space that could be held by an item with at least $20 of profit potential. Can this really persist much longer, or will we see someone realize they can cut that to two packs of 150? If the bottom suddenly changes, won’t this entire pyramid start to shake on wobbly sands? You can’t improve the swab and you can’t alter it’s base components anymore than they already have. Something’s gonna give. Just when?

If I remember correctly there was net no margin but positive cash in accounts when sp500 bottomed at 666. It’s what humans do. leverage up at the top and panic at the bottom. Makes for some easy money if you are patient.

The first step is two packs of 120.

Counterparty risk is going to be a major theme again very soon

YuShan

As long as Fed is pouring Trillions each year, there will ne no counter party risk! Wonder why 20% of S&P which are zombies still surviving?

Fed could keep the rate low, until Economy catches with the Economy on the ground!? They have no moral compass just more QEs!?

Is this the same type of margin trading that would create the huge demand for treasuries that resulted in the -4.5% repo rate you discussed? Like, would these numbers also include hedge funds doing a “basis trade”? It’s certainly something to try and wrap my head around this amount of borrowing on top of borrowing in many cases to buy options contracts. With no pandemic it’s hard to justify a bigger and bigger bazooka.

Excellent charts as always.

Is it possible to post a chart with margin debt as a percentage of S&P?

Good thought/suggestion A!

And this old guy would really like to see such a percentage chart going back to the era right before the crash of 1929,,, as well as an extension of the first chart in this article by Wolf showing the current WTF situation.

That first chart alone, not to be seen anywhere else very likely, is worth the price of admission,,, or at least the price of another mug!!! ASAP

Thanks Wolf,,, mainly for all the ”straight dope” continuing to keep me away from the SM, for now.

IIRC, it was old JP Morgan his own self, who said, ”buy on the way down, but only if you are sure you can keep it until ANY bottom,,, and sell on the way up because you can never know in advance the exact timing of either the top or the bottom.”

I was thinking, and wrote on here, around this time last year, that the bottom this time would be about 1800 for the S&P, and that I might jump back in at or near that point. Now even that point seems to be on very shaky ground…

And it was Jesse Livermore that said something like – “the price of corn was falling precipitously. What else could I do but sell more.”

VVN

I would think that we are so far into uncharted territory that we can’t use any of the old maps. Almost like being put on Mars and comparing it to discovering a new continent. The FED/Treasury are trying to save the economy and doing a decent job of keeping the market from going to zero. So I think we just need to watch and carefully navigate this new landscape after some reflection because they too don’t know what they are doing

No, they’re not trying to save the economy. The economy is toast, and they know it. They know we’ll never have the level of growth needed to catch up with valuations or with our debt load. What they’re trying to do is create the illusion of there being a productive economy so it doesn’t collapse on their watch.

When this whole dog and pony collapses, I wonder how long it’ll take them to start it up again? Fifty years? Twenty-five? Never? Who knows? Certainly we seem headed for some kind of widespread upheaval the likes of which will make everything so far seem like a streetcorner sideshow.

The Greatest Generation knew there was no such thing as a free lunch because their own parents tried to get just that and shafted them in the bargain. I wonder how many millennials and Gen Z-ers will die cursing their forebears as the wildfires, resource wars and whackjobs shrieking about gay frogs wash over them like like a tsunami of unpaid loans.

We just need a few big countries willing to dump the US dollar. Here is a make-up scenario:

The Chinese government announces that the Chinese Yuan (Renminbi) will be pegged with gold, effective immediately. The Chinese Yuan will definitely collapse, but I believe the US dollar will fall even further.

Yep, but…

1) The Fed would print any amount necessary to buy the share of US’ Treasuries that China dumps and

2) The resultant, inevitable US inflation would be immediately blamed on US asset holders (blood thirsty landlords, hoarding commodity speculators, corrupt businessmen/domestic terrorists/white supremacists/invaders from Mars) it will a 7/24/6 month CNN circle jerk orgy.

3) The White Knight of DC will then introduce a wealth tax to slay the Domestic Terrorists of Inflation (offsetting some of the inflationary madness DC itself set off).

The US economy, as architected by DC, is a series of interlocking gerbil wheels/guillotines for private income/savings.

If China ‘dumps’ Treasuries, what does it end up holding? Dollars.

Sells Treasuries, converts dollars to euros, buys German Bunds.

China’s money printing would make any central banker blush. It’s off the charts, but they lie so bad you have no idea what’s going on. China is one GIANT LIE.

@Depth Charge

Sorry, but sooner people will trust China more than the US. This is because Chinese Yuan is NOT yet the most common global reserve currency.

Perhaps China is one GIANT LIE, but the US is definitely the biggest scam we’ve ever had!

Those who own all of their assets in US dollar will be dead meat.

Have to disagree with you there. China is the world’s largest counterfeiter and overall fraud by far. It’s not even close.

Depth C,

Almost all fiat nations have shown themselves unworthy of trust and genuinely lacking in ability.

We have already entered into a Dark Age of Fiat and the question is how do the savers of the world exit it.

Over thirty years in the Asian financial industry, supplier of investment opportunities – now CHINA the Syndrome Of fake everything except the claim for now population. But I got out once I realized the CCP’s leadership had no ideal of what they where Doing – Kid’s wiht a credit card – sad that Wall Sreet was selling CCP’s junk bond ( starting to default) but I’m sure that that xI will bail the Wall Street investors out NOT But these day it nice to watch the CCP being challenged by the rest of the world government.

Life is Good On The Glod Coast. Cheers

Who Cares? The stuff that China manufactures is real enough!

This is what you get when a central bank makes you believe that they will never let the market crash again, while at the same time they are debasing the currency. Of course people will then go all-in with maximum margin debt.

Central banks today are reckless beyond believe.

Why would the party end when bs j Powell stands in front of camera says no inflation and no one brings up housing lumber cars probably not allowed three ring circus bigger than China,s propaganda machine

You’re not allowed to ask those questions period. As Danielle DiMartino-Booth, who used to work at the FED, said, you ask something like that and you will never be allowed at another press conference. Only softball questions allowed.

NFT’s take the cake.

Only Wall Street can make fungible something non-fungible. RFL

You need a margin account, if you want to sell a stock short. Selling short involves borrowing on margin.

You need a margin account, if you want to borrow to buy more stock with existing securities as collateral.

Not at all. You use margin for leverage. Selling a stock short that is priced at $5 or less requires 100%.

The rules on margin debt have changed, thanks in large part to the Fed bridging the gap in every selloff. My (FS) broker tells me confidentially that my PLOC will not be marked to market if stocks selloff. Brokers know when they start making phone calls that they are undercutting their own position. No individuals will be allowed to go down without the ship. Makes sense if you think about it, the brokers have full institutional backing, (did you see the market go up while JP said nothing?) The rules for online brokers are different. My house is doing a deal for one of these online brokers with full intent to steer their clients. They no longer are trying to gouge on commissions. They won’t need to firewall off the online broker, while FS has the Fed backup. Most FS clients only risk a small percentage of their holdings, which is already rehypthecated at about 1/2 to 2/3s of value. Yes there are unvetted speculators playing with stimulus check money, who will be margin called, but the majority of spec is being done out of Portfolio loans, backed by the Fed at a FS brokerage against a stock market event.

“Real” traders eventually get margin calls. Hopefully investors don’t. ;-)

Petunia, I love u.

Of course, who wouldn’t.

Ahh, just do a 2.5% cash-out refinance of your home and go all in on TSLA!

Wolf,

“Compared to February last year, margin debt has skyrocketed by $269 billion, or by nearly 50%,”

But the SP 500 is only up about 25% over the same period.

So here in Weimar/Arkham America, things aren’t as utterly insane as they might be.

The Diminishing Marginal Impact of Madness.

(Proceeds to laugh manically, uncontrollably)

the things happening around us are not sane and sadly we can’t change it.

Personally I believe only revolution would bring some changes but sheeple are made to sleep with hand outs

Over time, I see us becoming a rentier society..

how can we make money of it ?

I am big into stocks and BTC although I have no faith in these but where can I put my money into ?

I totally believe in WR’s thesis but the problem arises when you put reason to madness

I had ample opportunity and knowledge to gamble in Bitcoin. I chose not to. This is way back in the summer of 2012. It was like $10 a coin or something. Nobody wanted to buy it, and it didn’t make any sense to me so I passed. Do I wish I would have bought a bunch and held onto it? Duh. Who doesn’t like to retire a hundred millionaire?

But let’s be honest here. First, I would never have held onto it until now. Like Wolf said, I would have sold long, long ago. In fact, I can’t imagine holding on after it appreciated 5 to 1 from that point, so I may have sold at $50. The bottom line is I would not still have owned it at today’s price, because I know myself. I always sell way too early.

But moving on to reality, if I was transported back in time without the knowledge of today’s price, I would make the exact same decision, NOT buying it. I don’t believe in it. Any crypto can be made up, and infinitely. As such, it’s valueless.

If I could go back I wouldn’t buy it either. The latest crypto scam is leasing tokens instead of owning them outright. The speed of the scamming is exponential now.

I am thankful there are people like you out there, in this world of reckless gamblers. The situation is really disgusting, in my opinion. Everything is speculation and greed. It’s off the charts.

William Gibson got that part right: We might get Magick-level technology, but, it will mainly be used by people to screw each other over faster and harder.

You and Wolf are right. I bought low and sold at 4X. I should check my old Bitcoin wallets for dust. Might not be dust anymore.

Maybe some can HODL, but no point holding until you are dead.

I would have sold the Bitcoin I didn’t buy at $100.

Hmm… The .1% control over 50% of global wealth… When will you be happy? When they control 99%

If you don’t want hand outs… Why not be direct, pick your favorite billionaire and sell yourself into indentured servitude! Do your part to not take hand outs amd increase the wealth of the .1% !

Already there. The FIRE sector runs America and all its markets. Banks don’t invest, they loan off collateral. Eighty percent of bank loans is for property.

(Just venting out)

Apart from ZH, Wolf and others are predicting a correction, bear market or even a crash for a long time. Such predictions are often sound grounded on economic theories and the real world happenings. Somehow, the markets, Feds and the government are able to kick the can down the road. Since like 2003 or so, the debt of US gov is increasing. There are inefficient zombie like companies and products like crypto or NFT and so on. The world goes on. Common people or even scholars have no interest on them. There may be a correction or crash but I think the whole system will be in place, same drama and a predictable plot. I hope we will be right…

Common people have no interest, this is true. But this all impacts common people in a big way. Common people have no interest and they have no clue as well.

Common people are now living in tents. Barbed wire around the capital, closed schools and businesses, and government handouts and shiny new financial/gambling games. The consequences happen slowly but surely.

Old guy here who has seen a lot going back to the late 1960’s when I was in a war. And have seen everything since then (recessions, stock market crashes, 18% mortgages (I had one), 12% CD’s, and on and on).

When this fiasco bites the dust, we will be well on our way to 3rd world nation status. The two “parties” will be one, like now really, and lawlessness will be everywhere. Homeless people….lots more. Prisons full….like now, but more prisons.

And by then, our freedom of speech will be withdrawn and Twitter will be a distant memory. Wonder why China doesn’t allow Facebook, Google, et al?

@Anthony -we’re headed here:

“You run one time, you got yourself a set of chains. You run twice, you got yourself two sets. You ain’t gonna need no third set ’cause you’re gonna get your mind right. And I mean RIGHT”

“What we’ve got here is…failure to communicate.”

– the Cap’n

Yeah, although each new “injection” is less and less effective. The P/E of the S&P is now above 40, and the Schiller P/E almost 36. It won’t take a lot to cause a massive drop, and we won’t know the cause until after.

That is the only reassuring fact. No amount of liquidity injection can make a bad business model to run profit. But again, the purpose is not efficiency

Someone said that phd economists should spend less time studying math and theory and more time studying economic history. I would have liked someone to have asked Powell doesn’t he think financial paper leveraged at 6.5 times gdp is enough and why he thinks more than that is better.

Powell is either a Russian or Chinese agent ;)

I posted this in the last Wolf posting. But for those who missed it:

My BNY Mellon fund sent me an annual report a month or two ago and they reported this same “no rate hike till 2023” bull s$it. How did they know this if the Fed just released this information yesterday? Sounds like some people are more connected than others. Someone knew this information and could have traded on the inside baseball and made a killing. I would say this leaked inside information should be investigated by the SEC. We have crooks and leakers right inside the Federal Reserve.

Or it could be that the Fed looks at the same data the banks use, runs similar models to them and has similar projections for the future. So if BNY or Goldman project interest rates increases far out into the future the Fed also projects the same based on the same data, similar assumptions, probabilities about growth inflation and financial conditions.

Sir.PiratePapirus & Wolf

To make my point clear, the wording in my fund’s annual report concerning future interest rate policy of the Fed wasn’t paraphrased based on models or projections. It was word for word the same as the Fed’s announcement yesterday. “Interest rates will stay at zero through 2023”. This could NOT be just a coincidence. The fund managers accidently let the cat out of the bottle. They obviously knew, probably via leaks, way ahead of time what the Fed was going to say and do. How many other mutual fund managers and hedge funds were tipped off in advance to the Fed’s announcement? This should concern every investor who puts money into the casino. The whole game is rigged against the small investor. That’s one reason I have no money in the stock market and don’t plan to put any in there any time soon, or ever for that matter.

@Swamp Creature

I too knew that the narrative of hikes further into the future 2023 etc would be the case and i don’t have contact with the Fed. As Wolf said it was telegraphed ahead of time, and there is only so many ways to describe the same thing in finance so BNY’s choice of words don’t matter. The Fed has stopped surprising anyone for years now so pretty much you know what they will say and do ahead of time what you can’t know though is how the market reacts, so such events end up being not tradable except during times when the Fed surprises the market with easing or tightening, this is true for everyone including BNY.

Your concerns about the unfairness of the market is of course justified there are plenty of examples of corruption of intentional leaks and backroom deals but i am afraid this is not it. If you are looking for cases of how the little guy is screwed every time take a look at credit markets and the giant elephant that is the Fed in these markets, or the 2008 episodes, or GME and so on and so forth.

Swamp Creature,

“It was word for word the same as the Fed’s announcement yesterday. “Interest rates will stay at zero through 2023”. ”

I don’t know where you get that.

Here is the FOMC statement from Wed. And it says no such thing:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20210317a.htm

Here are the FOMC Implementation Notes from Wed, and it says no such thing:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20210317a1.htm

Here are the FOMC Projection Materials from Wed, and it says no such thing:

https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20210317.htm

Here is the transcript of Powell’s statement at the beginning of the presser, and it says no such thing:

https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20210317.pdf

The projections of rate hikes have been largely the same. There was no big change today from the last meeting, in that respect. The rate hikes have moved a little bit closer in the projections (a few FOMC members moving them closer). We’re talking months, not years :-]

These projections show what each committee member sees in the future in terms of rate hikes. The median of these projections is often put into headlines as if it were an “announcement.” But that’s not the case. The Fed did not announce a “schedule of rate hikes.”

The Fed divorced policy from dot point projections, and linked to hard data on employment, taken from a “variety of sources”. Bernanke walked back the employment benchmark on his watch, wink wink. They also promised to signal any QE taper “well ahead”… No projections on rate hikes, plenty of signals on QE. Most disingenuous Fed speak ever. A fit of apoplexy at mention of yield curve, but some truth leaked out, “we are buying all over the place already…” Enough money is brought to bear “during” the meeting that no one can attribute the selling to their guidance. Bond vigilantes were pedal to the metal throughout.

Wolf & Sir.PiratePapirus

I stand corrected.

I read Wolf’s links and I agree they do not say word for word that rate hikes will not take place until 2023 even though they do imply that. Someone in the media must have taken what Powell said and extrapolated it into the same narrative that was reported in the BNY Mellon report. This is why I read the Wolf Street report. To get the raw financial data and information that I can use to make investment decisions. The comments section is also well worth ready.

Swamp Creature,

A lot of times the media are terrible about reporting on the Fed, especially in the headlines. They can make a grown weep in despair ?

Part of the reason is that everything the Fed says is so complicated that, if you try to explain it, you’d lose your average readers. So they simplify everything.

Wolf

Thanks for posting the Fed text. I don’t have the time, nor do most of your readers to listen to the speeches live. I printed out the text from the links and will compare it to what transpires in the next few months. It will be interesting to see if they stick to their guns if interest rates and inflation go through the roof. Or mayby they get lucky and everything turns out rosy.

Its obvious and that the progressives don’t understand economics.

If they did they would realize that the largest transfer of wealth in history is occurring right now……from the middle class to the rich.

Those zero rates are stripping the middle class while the rich reap trillions from the stock and bond markets, their incompetently run businesses which are highly profitable due to low rates and kept from collapsing by the fed, our slanted anti middle class immigration and trade policies and low tax rates.

The only question is where the wealth will end up…..here or the Cayman’s.

Yep, Biden is going to raise taxes a point or two. LOL.

Progressives have zero to do with what is going on now. Progressives still believe in taxes. Progressives are not monetarists.

I don’t remember. Were the banks doing QE during the tulip mania? Or is it really different this time?

Yep. They were printing Mississippi stock certificates and convincing rubes they were as good as collateral as gold more or less. All it took was some enterprising Germans to go to Mississippi and say we have been sold a sack of poop.

The way things are going, I get the feeling I will be seeing every Wolf’s article starts with WTF in the title. Truly a WTF time, sure do feel like a never ending episode of Twilight zone.

We clearly need a WTF Derivative.

WTF ETF

It’s called ARKK. And it is doing very well, thank you. ?

WTF CLOs, covenant light version.

Should be WTH, “What The Heck”, to match the mug.

Bubble watch. I realize this isn’t the same as the margin trading discussed in this post, but a close relative took out a half million dollar mortgage and put it all in the stock market last year. I have been encouraged to do the same by my bank.

The bubble of everything continues

if the slow grinding devaluation of the US buck

goes on.

Not sure if anyone here other than me reads Orlov? He has a brilliant new post up on his website on the topic of hyperinflation. It’s partly satirical like this:

“And then will come a brave new world in which the government issues money, hands it out, it circulates for a bit before losing of its value, and then the government issues more money. Obviously, the government, no longer being good for much, would do well to let the tech giants—Apple, Google, Microsoft, Facebook and, last but not least, Twitter—take over the money-issuing function. New smartphone-based banking and payment systems will not only make it possible to take these changes in stride but will make hyperinflation fun for everyone.”

USAA isn’t doing conventional home loans right now. Haha. They know.

When did they stop doing conventional loans?

Don’t know when but within the past year. Conventional loans aren’t federally backed so they don’t want any part of the boom/crash. USAA is old school. They went after people who didn’t pay back their home equity loans last time.

A game of hot potato plunder: When the music stops they get our chairs, and we get the floor, if we’re lucky.

When former Governor of the Bank of Canada, Mark Carney moved on to head the Bank of England, he hadn’t been there long, when, in Brit- speak, he was told ‘we would be looking for a good deal more decorum’, or in Yank-speak, STFU.

The Brits were not used to weekly ‘fire side chats’ from the BOE and found them unsettling.

Every time the Fed yaps it uses up its gravitas. We know ‘forward guidance’ is BS, so why not just STFU and give at least the impression of an institution that does not react to every market tantrum.

Exactly. The FED gets off on their own power, and is more than happy to show up and bloviate on the regular. They need to disappear.

Bernanke set the post-Greenspan policy of being more “open.” Didn’t help.

XOM and Boeing has been called Zombie Companies just 6 month ago. Now they back to live. They have been crushed by pandemic big time, but there was nothing wrong with their business model. If pandemic is temporary, plenty of those Zombies wil be back to live.

If not we are all f…cked.

But still, historic high corporate debt is major concern, for FED at least.

I’d keep an eye on those new members of a Junk Club.

Nope. A corporation should be structured so it can survive a severe recession. Covid was a tell- tell sign of how over leveraged the system is that corporations were going under without government handouts.

bitcoin most likely will reach 100k this year. They located Binladin but not Satoshi? Ever wonder who’s really behind it?

The stock market will melt up to even higher all time highs.

Followed by every other asset class trailing behind on the way further up.

The cost of goods will continue to rise.

And although you thought it was over

The streets will cry with civil unrest this summer once again.

And that WTF chart will ever expand higher. With a WTF WTF double whammy chart.

Not sooner but later in a few years this will all cause the worst collapse, bitcoin will collapse because thats its ultimate goal was to create wealth out of nothing, many banks will fail, anything over the FDIC protection will be wiped out Janet will directly purchase ETFs the pensions, along with government assistance programs will go bust and even if you can collect a pension or social security what will $1000 actually purchase at that point?

Major depression not today not tomorrow but soon.

Wonder if our head honcho in charge Wolf could vision the aftermath in an article of what awaits us on the other side of that WTF chart?

“bitcoin most likely will reach 100k this year.”

What is the $100k number based on? Why not $200k? Or how about a cool million?

The further something gets from a bond paying a fixed amount of interest the harder it gets to value. A blue chip with long dividend history you might get pretty close to true value.

Some people with ideas about bitcoin’s future might could make a theoretical case for it’s value, but as an investor I think you only invest in what you can reasonably value and leave the rest for somebody else. Money in retirement is a serious thing and you need somewhat predictable asset values to plan your income.

I bought more miners today, the insanity could continue but I would say were close to another correction before next earning season…

Gold and silver are just becoming more important with the world of debt spinning faster…..time to fish more and batten down…

I have used margin successfully and disastorously. I learned, the hard way, you have to get out of your position before things get really messy. This comes with experience and of course some pain.

I heard today that the stimulus that many the younger generation will receive will go into speculation in the stock market.

My brain is bursting with dopamine enjoying this circus!

JK

Jim Cramer on CNBC just recommended just that to his audience of lemmings.

At a glance, it looks like the prior three periods of YOY increases lasted approximately 2 years (duration subject to drilling the detail). Ignoring the magnitude of the current run, the next big correction could be deduced as beyond 2021. Simplistically speaking :)

Investing in SPACs, buying stocks on Margin, buying cryptocurrency, going on a consumer spending binge, taking flyers on short squeezes you heard about on internet blogs… this has become NORMAL for Americans???

I thought the smart move in a recession was to hunker down and ride it out. Clearly I am doing this wrong.

Working hard and creating something of value is for suckers.

Instead, to make money you better go deep into debt to speculate on already exiting assets (even virtual ones) and see them appreciate in price while the central bank has your back and debases the currency right in front of your eyes.

It’s beyond ridiculous that policymakers are actively stimulating such behaviour.

We really deserve something better guys/girls!

Simply stated, the Federal Reserve Board is abusing its mandate by disregarding long-term employment and price stability. By optimizing everything in the short-term, the Fed damages the long-term health of our economy and also creates huge generational wealth disparities.

This is a clear abuse of its mandate.

“In an investment environment where nothing matters anymore – until it suddenly does.”

Seems to me that’s the way it’s always been. Just a bit more extreme these days.

Might be a good time for another short position? Just a thot…

I notice too on the WTF graphic that the margin debt seems to plateau a bit before the next crash so maybe next month or so on the short… ;-)

I like Charlie Munger’s style which is try to buy a great company’s stock when it pencils out to a very high return (usually in a recession) and unless a CEO tanks the company you can hold forever. You got to buy them at a good price, you can sell when they get expensive, but you don’t have to.

Plan A is to have a plan. :) Sounds like a good one but I probably need better pencils. Will stick with my business for now and see what happens. Hate chasing parabolas…get burned too much.

I wouldn’t mind some inflation. It would inflate away my 5 mortgages into what seems like easier payments.

My rental properties rents would go up.

I own a service business, so I will just raise prices!

What a wonderful life

(for the record I wish things wouldn’t be this way, and a family of 4 could easily afford housing)

@Jack, lead-off post above:

I actually took an International Econ course taught by Janet Yellen at Bezerkely, during the days of the Japanese economic engine ascendance. In order to keep my student loan debt as small as possible, I worked various part time gigs, including at an economic think tank, where I encountered the very fetching Laura Tyson, who would go onto become an economic advisor to Bill Clinton, and later, dean of the UC Bezerkely business school. Coming from a science background, I was struck by the impreciseness and subjectivity of the social sciences, and also, the detestable reality that to get along, you had to go along. Sadly for my initial career advancement, I rejected this reality, clinging to the belief in the primacy of absolute truth, but that is another story.

Anyway, the prevailing go along dogma at the time was that the US had to exit manufacturing, for example, surrender the auto industry to the Japanese behemoth, and focus on future, high tech fields, where the US would have a lead by dint of its superior academic institutions, and flexible capitalistic system of financing new industries. The folly of this thinking is illustrated in the Charlie Rose interview of the lovely Laura Tyson, where Sir James Goldsmith completely eviscerates the haughty, talking down to you Tyson, and history has shown Goldsmith to be absolutely spot on. But if the by then fabulously wealthy Goldsmith were trying to build a career as an economist at that time, his anti-dogma position, whilst ultimately correct, would have been career suicide.

And why the momentum to this go along point of view? Well, the economic institute that I was working at part time authored ostensibly independent academic papers that served to provide cover to industry, and industry wanted to make higher profits by moving manufacturing to low cost labor and less regulated markets, including less regulated regarding protecting the environment (think Chy-Nah). And the profs had side consulting gigs with industry, and the financial industry also favored this move, and of course, the financial industry is a big employer of economists, and a source of substantial income to folks like Yellen, for example. And so that is how the wind blew.

Parasites, not patriots, infest the bureaucracy. And money talks.

That sounds like one of the ‘squid arms’ of corporate fascism to me… buy the politicians, own the intellectuals and run the money into your pocket at the expense of the plebes.

Bitcoin. I know that word drives you mad and you need to pop another Lisinopril to keep your BP down, but just relax. This debt is completely uncontrollable, the Dollar is fading FAST, and yet the market is up. Why? Because WHERE ELSE do investors put their money?! The Dollar is flat out dead, and Bitcoin (Cryptos, Theta is my favorite), Gold, Silver, and Food will be the ABSOLUTE kings of commerce. You need only look to the past to understand that civilizations that adopt to technology quickest get ahead and live. You would be wise to do the same.