San Francisco Bay Area condo prices are the glaring exception. House Price Inflation in all its glory.

By Wolf Richter for WOLF STREET.

We’re not talking about miracles, such as the same house getting bigger somehow or fancier, but about how many dollars it takes to buy the same house. According to the National Case-Shiller Home Price Index for October, released today, it takes 9.5% more dollars than it took a year ago to buy the same house, meaning that the US dollar has lost purchasing power by that much with regards to houses. This watering down of the dollar is the purposeful result of the Fed’s interest rate repression and the $3 trillion it printed and handed to the markets, which triggered, among all kinds of other peculiar phenomena, a land rush.

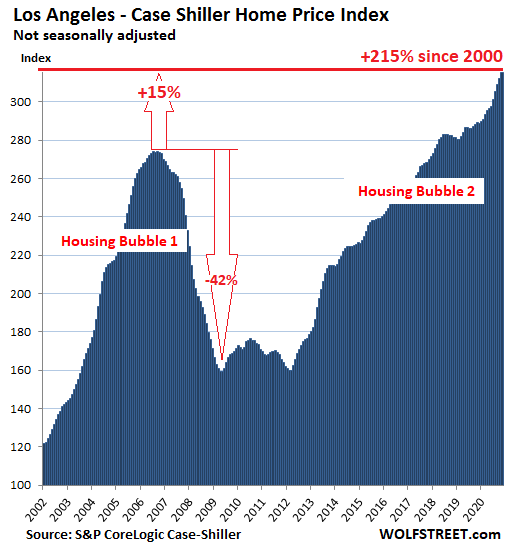

Los Angeles – the #1 most splendid housing bubble:

The Case-Shiller Index for house prices in the Los Angeles metro rose by 0.9% in November from October and by 9.1% year-over-year, with prices now exceeding the peak of the insane Housing Bubble 1 by 15.1%. The index was set at 100 for January 2000 across the 20 cities it covers. So the index value for Los Angeles of 315 indicates house prices in the metro have surged by 215% since January 2000 – meaning they more than tripled in 20 years – thereby making Los Angeles the most splendid housing bubble on this list.

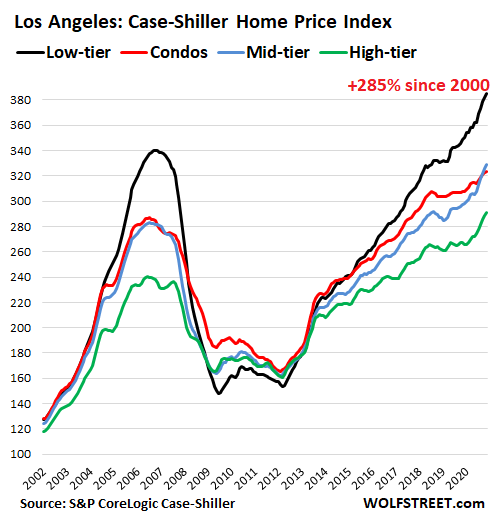

For Los Angeles, along with a few other cities, the Case-Shiller Index provides not only an index for house prices, but also separate indices for prices of condos, and high-, mid-, and low-tier houses. In Los Angeles, they have diverged, with prices of houses in the low tier (black line in the chart below) nearly quadrupling since 2000 (up 285%), and with houses in the high tier (green) surging the least. Condos (red line) are in the middle.

Compared to November last year, prices of mid- and high-tier houses have surged the most (+10.4% and +10.7%), while condos have surged the least (+5.2%). During the Housing Bust, prices in the low tier also collapsed by the most (-56%):

Today’s release of the Case-Shiller Index, “November,” is a rolling three-month average of closings that were entered into public records in August, September, and October.

This is “House-Price Inflation.”

By comparing the sales price of a house in the current month to the price of the same house when it sold previously, the Case-Shiller Index tracks the amount of dollars it takes to buy the same house going back decades, thereby measuring the purchasing power of the dollar with regards to houses. This “sales pairs” method (here is the methodology) makes the Case-Shiller Index a measure of “house-price inflation.”

So, consumer price inflation across the US as measured by CPI (which does not include house prices but includes rents) amounted to 55% since 2000, while house price inflation in the Los Angeles metro amounted to 215%, and house price inflation with regards to houses in the low tier, house price inflation since 2000 amounted to 285%!

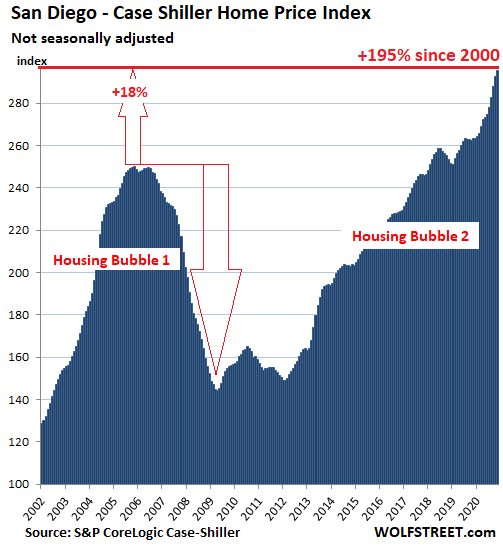

San Diego:

The Case-Shiller index for the San Diego metro rose by 0.9% in November from October and by 12.3% from a year ago. Prices have nearly tripled (+196%) since 2000:

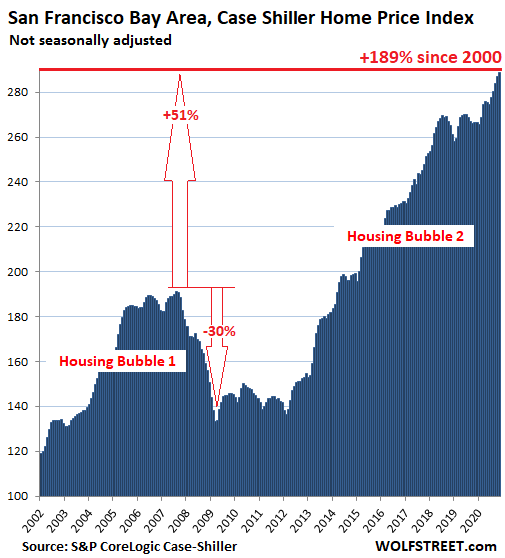

San Francisco Bay Area:

The Case-Shiller Index for “San Francisco” covers the Bay Area counties of San Francisco, San Mateo (northern part of Silicon Valley), Alameda and Contra Costa (East Bay), and Marin (North Bay). House prices rose 0.6% in November from October and were up 8.3% from a year ago. The index has nearly tripled since 2000 and is up 51% from the crazy peak of Housing Bubble 1:

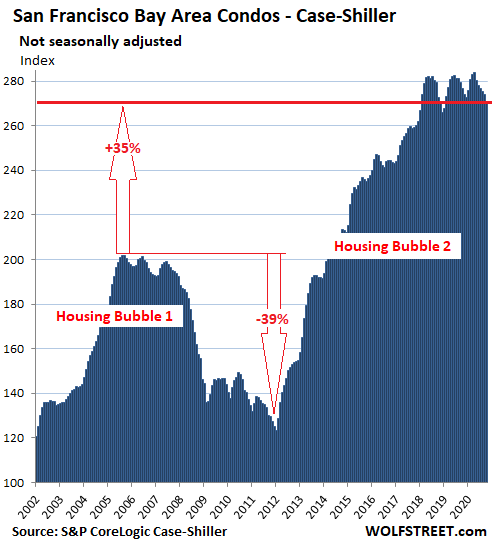

San Francisco Bay Area Condos:

Condo prices in the five-county Bay Area are another story – and the only exception on this list of the Great American Land Rush: they fell 1.1% in November from October, the sixth month in a row of declines, having fallen 4.5% since last May, and 2.1% from a year ago. They’re below where they’d first been in March 2018:

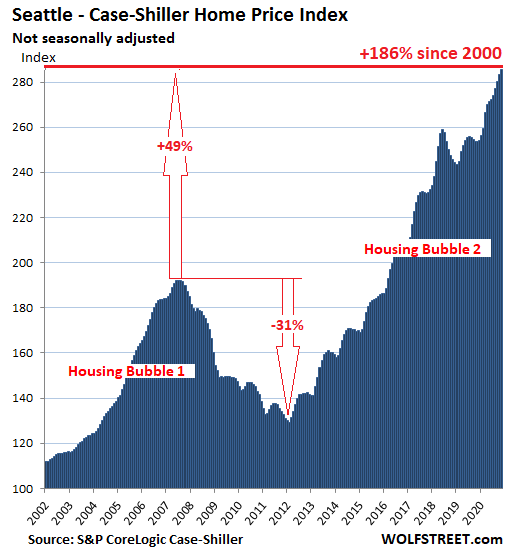

Seattle:

House prices in the Seattle metro rose by 0.9% in November from October and by 12.7% year-over-year. This makes Seattle the market with the second hottest annual house price inflation among the Splendid Housing Bubbles here, behind Phoenix (13.8%):

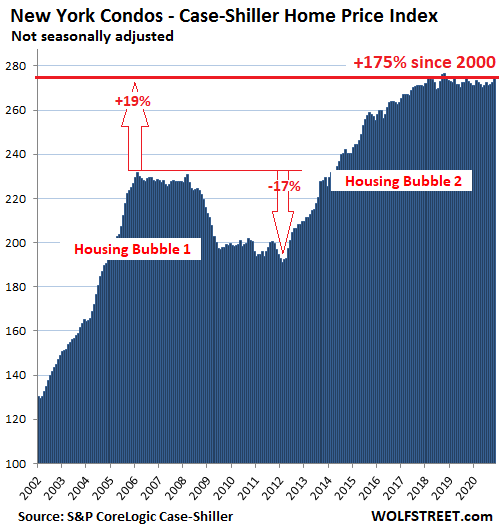

New York metro condos:

The Case-Shiller Index for New York City covers the vast and diverse market of New York City and numerous counties in the states of New York, New Jersey, and Connecticut. Condo prices in the area rose by 1.0% in November from October, having been essentially flat since late 2017:

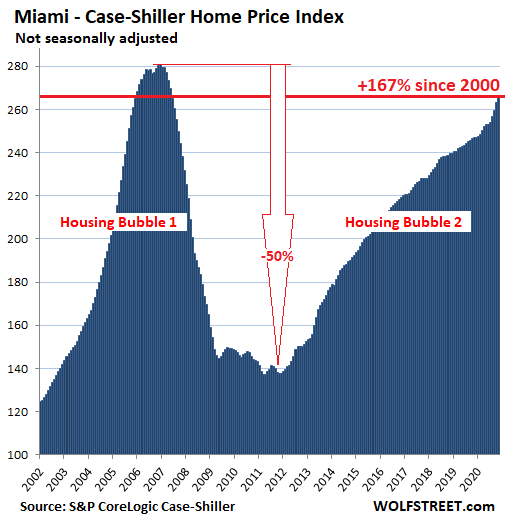

Miami:

House prices in the Miami metro jumped by 1.3% in November from October and by 7.9% year-over-year, and are now just 4.9% below the super-nutty peak of Housing Bubble 1:

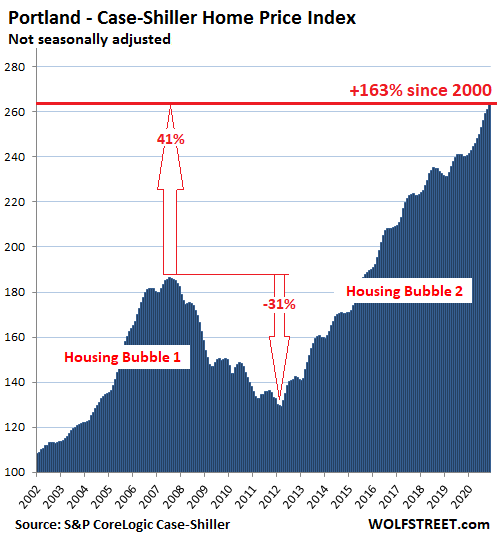

Portland:

House prices in the Portland metro rose 0.7% in October from September and 8.9% from a year earlier:

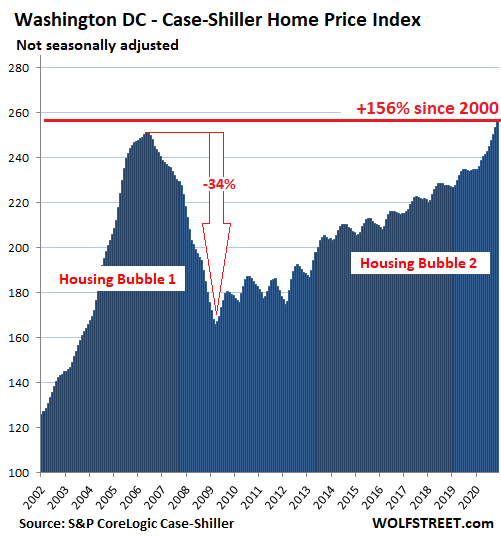

Washington D.C.:

House prices in the Washington D.C. metro rose 1.1% in November from October and were up 9.1% year-over-year and now have surpassed the insane peak of Housing Bubble 1 by 2.0%:

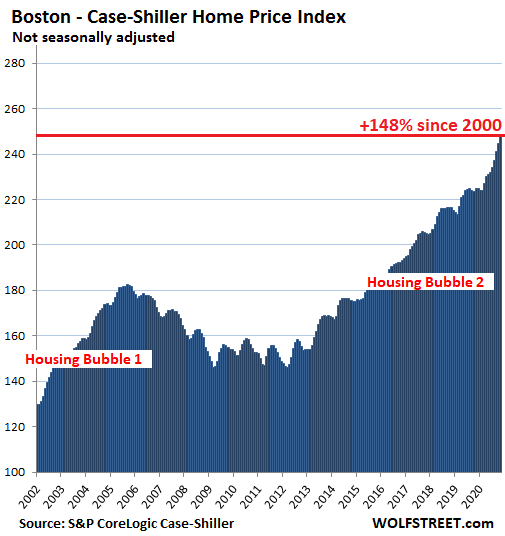

Boston:

House prices in the Boston metro rose 1.4% in November from October and by 10.4% year-over-year:

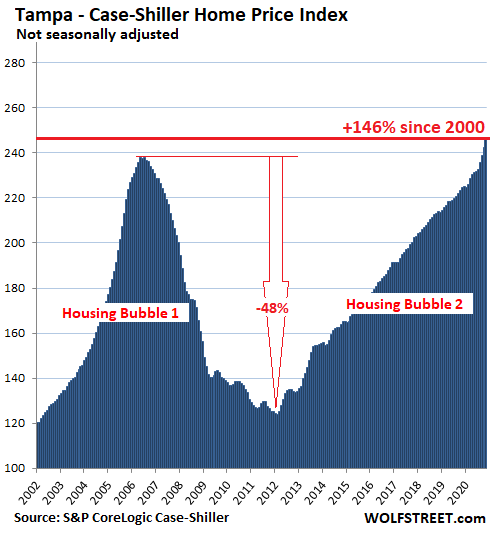

Tampa:

The Case Shiller Index for the Tampa metro jumped 1.4% in November from October and by 9.5% year-over-year, and thereby surpassed the crazy peak of Housing Bubble 1 by 3.3%:

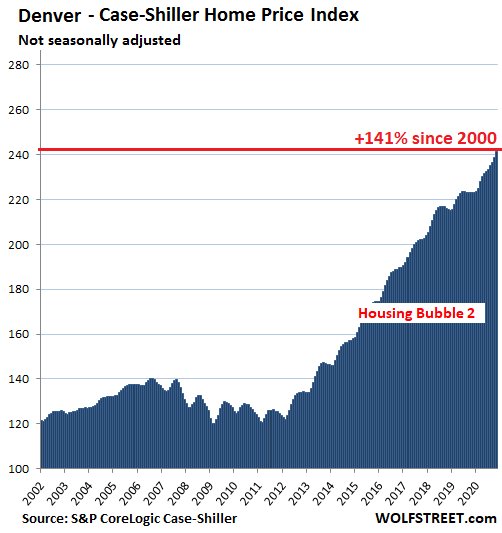

Denver:

House prices in the Denver metro rose 1.0% in November from October and by 8.0% year-over-year:

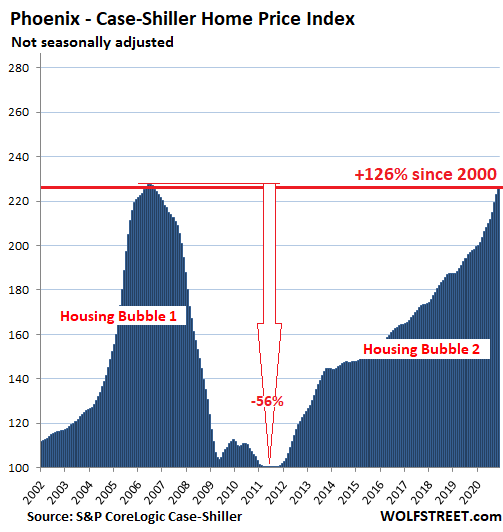

Phoenix:

House prices in the Phoenix metro jumped by 1.3% in November from October and by 13.8% year-over-year. This made Phoenix the market with the hottest annual house price inflation among the Splendid Housing Bubbles here, ahead of Seattle (12.7%) and San Diego (12.3%). And prices are now just about even with those at the peak of the crazy Housing Bubble 1:

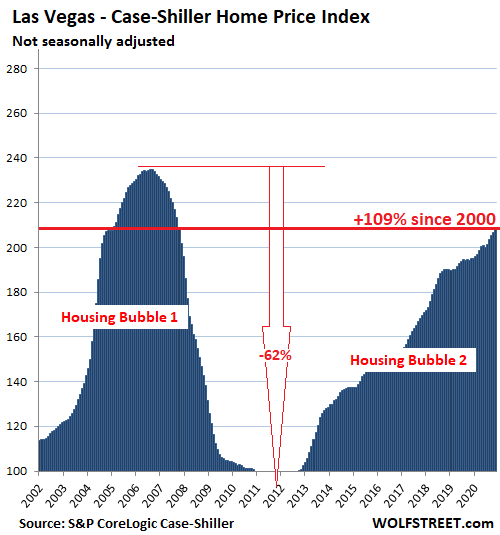

Las Vegas:

House prices in the Las Vegas metro rose 0.7% in November from October and 6.8% year-over-year:

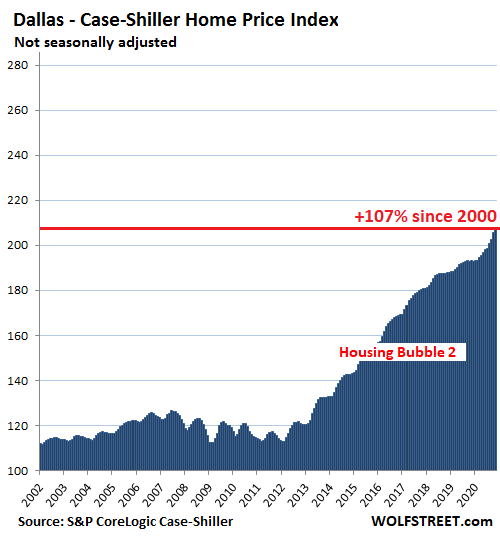

Dallas:

The Case Shiller Index for the Dallas metro – counties of Collin, Dallas, Delta, Denton, Ellis, Hunt, Johnson, Kaufman, Parker, Rockwall, Tarrant, and Wise – rose 0.8% in November from October and by 7.2% year-over-year, and is up 107% from 2000.

In other words, in the Dallas metro, you have to pay over twice the dollars today that you had to pay 20 years ago to buy the same house. House price inflation since the year 2000 in the remaining cities on the 20-city Case Shiller Index has not yet ascended to this level, which makes Dallas the last entry on this list:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Love the charts, but if possible, could we have these inflation adjusted? It’s difficult to figure out how much of the rise is just dollar devaluation (the everything bubble) and how much is part of ‘housing bubble v2’. Another nice bubble indicator would be rent/buy ratio.

Yaun,

PLEASE READ THE ARTICLE — including the entire section under the heading “This is House-Price Inflation” — and don’t just look at the pictures. This IS a measure of inflation. HOUSE PRICE INFLATION. It doesn’t make conceptual sense to adjust one measure of inflation by another measure of inflation, such as House Price Inflation by CPI consumer price inflation, or CPI inflation by PCE inflation, or PPI inflation by wage inflation… or whatever.

It’s the same 2X4 in a $200,000 house as in a $2,000,000 house.

The value is always in the land.

Maybe some are the same, s1, but mostly not in most places that I have worked, coast to coast in USA in the last 60 years or so.

Most of the studs in lower cost construction/housing are the very cheapest and lowest grade permitted by the local code, and sometimes less than code if the mordida/baksheesh is in.

Most of the studs in expensive housing will meet the code AND meet the requirements of the inspecting licensed design professional, architect or engineer who is usually on the hook to confirm the quality of every component meets the specifications they have prescribed.

Similar delta usually prevails throughout, from quality of concrete right on through quality of all other structural components and especially fenestrations, final finishes, fixtures and appliances, etc.

Found out years ago that municipal building inspectors were required to inspect ONLY for code compliance, and were not allowed to even comment about quality…

But the land price is different.

Are we still talking about this? It’s not a bubble. Bubbles pop.

The article does say that CPI inflation was 55% since 2000.

Some of that CPI inflation is also “owner’s equivalent rent” (OER) on those houses. I think the weighting is about 20% for rent and OER.

I agree with Wolf’s point that inflation isn’t a single monolithic thing. It’s more like a balloon held in your hand, being inflated from an air compressor: some parts will inflate more and squeeze through the gaps in your grip. Housing inflation, and financial asset inflation generally, is where most of the expansion takes place. Consumer prices haven’t budged nearly as much but wealth inequality is off the historical charts.

The Fed has a lot of injustice to answer for.

You might want to review some of your personal pricing from 2000 with today ws if you don’t think ”consumer prices haven’t budged much.”

New pickup, basic no frills reg cab 8′ bed ”work truck” type full size pick up around $20K to around $40K.

Decent full meal w moderate wine for 2 in a good but not ”stellar” sit down restaurant $50-60 then, $100-150 now.

Dozen eggs, free range organic XL around $2-3 then, $5-7 now.

Whole chicken $0.39/# then,,, crazy now, other meats and dairy similar.

Busch 12 pack $5 then,,, last I heard it was $12, haven’t looked recently due to preferences delta,,, (-last few years.)

Red Cedar shingles, Blues, $100/square then, $400 a couple years ago.

Local ”handyman” $25/hr in 2015, $50 now and long wait.

Basic 10-10-10 fertilizer $4/40# then, $20 last summer.

Decent area basic housing in Saint Pete almost double since 2014, per the graph above for entire TPA bay metro.

Surely some things that are adaptable to productivity cost effective process engineering are down or level, but every thing else is up and upper…

Somehow, WE the PEEDONs must cajole the fed guv mint to focus any kind of ”official” inflation reporting on the real needs of the vast majority and stop all the various and sundry manipulations, especially those that keep pushing the old folks into poverty.

Basic restaurant lunch 7 bucks then. 15$ now.

Vintage, please read more carefully – I’m on your side. Note that I said “nearly as much”.

House prices per Wolf’s graphs are up 107-250% in many metro areas, while CPI overall is up “only” 55%.

55% is not nearly as much as 100% or 200%, is it?

Meanwhile, like houses and other financial assets, the stock market is up about 200% as well. Those are only owned by the wealthy – hence the wealth inequality.

Watch “Why Grantham Says the Next Crash Will Rival 1929, 2000” on Bloomberg in which Jeremy Grantham discusses what I believe is coming. I could not agree more with what he says except as to precious metals (which the government can confiscate by calling all Americans who hold such “hoarders” and taking it at a very low price as in the 1930s) or precious metals ETFs (which usually are NOT required in the contract you sign with them to ACTUALLY HOLD any REAL precious metal but just GLEEFULY charge you “storage” charges on metals that they do not actually hold), a huge number of which will just go bankrupt when asked to cough up the fictitious holdings of precious metals.

Removing the “Federal” Reserve from the banksters’ control will remove their greatest asset without which their fortunes will evaporate like heroin addicts’ stashes, because the banksters gamble recklessly and compulsively. Since the deceptively named “Federal” Reserve has caused the gigantic loss of Americans’ purchasing power (and wealth) since its founding in December 23, 1913, a mechanism to end its corruption should be enacted: such as requiring that any future bailouts, via its repeated, trillion-dollar gifts to its bankers’ (now) legally insolvent banks, be in exchange for “Fed” ownership of most of the shares of those banks, so the “Fed” will slowly slip from the power of those banksters.

One can’t help but notice in charts, that the most radical “twin peaks” occur in the Sun Belt.

I can only speak for AZ, since I was in down in Phoenix/Tucson off and on ’07 to ’14, full time ’09-’10, mostly in Tucson, but I imagine it’s the same story elsewhere that one sees radical twin peaks in this article. Vegas for sure.

They expected 10-15 Million people in the Phoenix-Tucson corridor, (from good source who previously worked as civil engr for City Of Tucson), and also “somehow” met a law proving there would be plenty water for them all. They were expected to be refugees from the snow belt, and also a lot of “snowbirds”, expected to maintain dual residences.

Tens of thousands of “illegals” were hired for the massive housing and support services construction, low pay, miserable working conditions, and often just outright stiffed on pay. All the developers and contractors (even subs) got rich.

Now they want all the “illegals” OUT, GONE !!!…..except for their gardeners, housekeepers, restaurant kitchen workers, etc, of course….

Point: Who is really responsible for “invading Mexicans” and should there be some really HEAVY claw back on all these folks to pay for our “border control problems”.

Hell, I even heard dairy farmers in way up in Maine concerned about their cheap illegal labor. And of course the chief pot stirrer of this faux “brown peril” employs them at some fancy resort in Fla…forgot name.

Condo prices have only paused their upward “dollar” price rise.

Once more money is printed, condos will probably resume going up in dollars too.

As important as the quantity of money injected into the economy, is the distribution of that money. Who got it? We have a huge unemployment problem and an even larger under-employment problem. Why didn’t we put people to work and fund full employment? Who is pushing property prices up, anyway. The millions of renters and the millions of underemployed people? It’s not hard to figure it out. Same problem applied to stock and bond prices. The Feds could impose a 3% interest rate almost over night. That should ‘rationalize’ prices pretty fast. The money should be going to produce full employment. All the rest of it’s a waste.

Thanks for the good info, Wolf.

As someone who’s looking to buy a house in a small market around this fall/winter (moving for work), part of me is selfishly hoping that this entire thing deflates in the next few months. Of course, that’d have pretty bad financial consequences for a whole bunch of stuff.

But at this point, maybe it wouldn’t be worse than letting the bubble build more?

You’re not the only one.

Every time housing prices go up the homeless population increases. It’s been held at bay a little by stimulus and rent eviction moratoriums, but as soon as that stops it will increase again. This is out of control.

The more homelessness and near homelessness increases I’d expect more civil unrest.

A stock market crash might do the majority of people some good right now.

What do I know .. right.

I have been looking to relocate for the last 8 years.

Today I am looking for a 2-3 bedroom unit with a garage.

For how long have I been looking ??

What I figure is that everyone is overextended & juggling for dear life.

Everyone wants maximum bucks for their bang ..

They themselves want it dirt cheap “Give me a break” cheap.

I am talking about .. from the top of the market down & yes it matters what interest rates are but many thing are also spinning the ball.

No one wants to go from riches to rags & I think that, that is the fear.

There are 1 bdrm 1 bthrm units .. seriously overpriced .. but I would have to throw all my stuff away .. it hurts a bit to have to unload loved stuff .. I won’t know who I am.

Big Government and institutions like the Federal Reserve are Organized Crime, plain and simple.

Big anything is organized crime.

Power corrupts.

Hard to believe there were single family homes sold for under $100k in Florida during 2011-2012. House flipping is decreasing the availability of affordable homes.

My brother in law says he’s selling property to those fleeing Los Angeles, so odd LA is A Numero Uno. In another note since Melissa said Redfin is better than Zillow, the internets say my house jump in value 15%. The internets are smart.

Redfin actually has an algorithm. Zillow just does a drawing in the neighborhood with no regard for house type. Even the Zillow CEO sold his house for 40% less than the estimate. The entire industry laughed :)

I wonder how many property sellers and their agents in this crazy foaming housing bubble start at the outlandishly concocted (high) Zillow Zestimate number in their asking price.

And many buyers foolishly take the bait for FOMO– fear of missing out.

These are historic times and I hope historians are taking it all down for posterity to study in amazement.

Nationally, the Zillow Zestimate median error is 1.9%

Not bad for a free tool.

On the Zillow site, click on the Zestimate tab where the median error is broken down by metropolitan area, state, etc.

Where is your bro-in-law located?

Are we getting a Gamestop WTF chart anytime soon? Will be easy to draw the X-axis. Think it hit 240.

Don’t you just wish someone would ask Janet Jerome Powell Yellin about Gamestop and equity bubbles and how building a nation of day gamblers err I met traders is part of the Fed dual mandate and how it helps us beat China in world competition?

I recall Greenspan once talking about irrational exuberance. That guy really had a command of the English language. The way he could speak in riddles makes me believe he must’ve been a reincarnation of Nostradamus.

Yellen reminds me of a toad.

Greenspeak (Fedspeak) was the epitome of talk with little substance.

Yellen is just yellin’ nonsense.

“Yellen reminds me of a toad.”

When I see her in photos, she brings to mind the witch from ‘Hansel and Gretel’. Act benovolently and generous as the hapless victims are fattened up to be consumed.

She’s reminds me of a school mom

Jay gets only soft ball answers, look at his press conferences, they look more and more like Soviet nomenklatura these days. Have you ever seen some mainstream media outlet criticizing the Fed? All they do is venerate the chairman Powell.

No one will ask him to explain and insist on demonstrating how their actions have inflated asset prices that are owned by 10% of the population to the detriment of the majority of the working class , creating unheard of wealth inequalities that are tearing our society apart.

Maybe someday those Vikings that rearranged furniture at out Capital buildings will show up at a Fed conference with full media coverage and cut Powell and Yellin down of notches off their pedestals with some incisive questions.

China spends trillions to remake global trade with Belt and Road.

We spend trillions to move pieces of paper around.

Yes, and our biggest global export is the Dollar.

As many have warned, some day those increasingly worthless dollars will be sent back to their origin (US) and provoke a currency crisis.

Alibaba’s Webull is a Robinhood competitor. I wonder if Chinese investors are in on the party. The Chinese do like to gamble.

Somehow more than 100% of all GME stock (and 140% of the float) was shorted. (We’ve been assured that naked shorts aren’t possible, but obviously they are.) Now those shorts are being squeezed.

Naturally, the focus is on retail investors doing the squeezing, not the fools who shorted a stock when it was already heavily shorted (and therefore ripe for a short squeeze). This is not the first time this kind of thing has happened, so chalk it up to lack of training among the hedgies.

It’s possible to short >100%, non-naked….as long as shares sold short keep dropping into accounts that can lend their shares out. In theory, if all shares were lendable, you could have an infinite cumulative outstanding short. But some accounts aren’t lendable, or are held by institutions that don’t want to lend them. So a natural limit kicks in somewhere.

Rogers:

Gamestop: 9:30AM Wed. 1-27-21 approx $329!

(Yahoo Finance)

gotta put your time zone on that kind of dated and timed post s7,,,

your post was actually put up at 1217 EST today,,, a long time from the opening of the SMs…

startled me for a sec, until seeing the time of post above…

thanks,

GME 420 easy… to da moon!

Nevermind. Somehow I missed it. But it gets more rediculous as time goes by.

Yep, the chart for Washington DC Metro confirms what I’m seeing on the ground. There are virtually no houses for sale. When one pops up is is usually gone within a few days. Its sort of like 2005/2006 at the blow-off stage of the last bubble. The people buying these houses are overextending themselves. Low down payments and huge leverage. Many of the homes in the close in suburbs are so big and such energy hogs, and built with the cheapest construction materials. The cost of ownership which includes property taxes, insurance, utilities, and maintenance must be huge. Last summer during the drought, I noticed hardly anyone even watering their lawns, probably due to the high water bills which they couldn’t afford.

How do we know people buying homes are over extended? There are a lot a cash buyers, and I haven’t really seen any evidence that those who borrow do overextend. I’m open to it, just haven’t noticed any suggestion that it’s happening.

Few cash buyers right now in DC. Lots of parents helping with down payments as well. The parents have the liquidity and the belief in the market in DC. I think it will be okay here. I’m just worried about the rest of the country.

The year over year average price for some of the neighborhoods in Maryland are mind blowing. I just researched zip 20905 for a client. Prices are up 20% year over year. I’m not seeing as much lunacy in the higher price points.

If a person needs to buy or rent and easily has the money to do either, what is the best move. That is my position.

Didn’t you have like a million national guard troops in your city about a week ago?

You can tell people are overextended when they move into an expensive house and do little or no landscaping, don’t water their lawn, don’t pay their bills (I run a small business and have trouble collecting), leave a lot of the house empty, do no home improvements, and many other signals.

Lots of Boomers in the DC suburbs are buying homes in the Active Adult communities with cash. A few months ago many of them were getting mortgages due to the low rates, but now it’s all cash in order to be competitive.

We had so many troops and barbed wire here last week, it looked like the German trenches on July 1st just before the British launch the Battle of the Somme. This was a national disgrace, initiated by a bunch of s$ithead local and national politicians.

I wonder what the end will look like. Housing bubble #1 seems to be relatively symmetrical in shape despite the name implying that the down was steeper than the up. Roughly applying the same shape to Bubble #2….10 years until bottom? Assuming the popping starts now.

In 2008, most people still had confidence in the govt’s ability to correct the economy, no matter how misplaced. Now, no one has any confidence. This time, I expect the slide to be even faster and more severe.

How do you figure that? I keep hearing people talking about the Fed and massive government “stimulus” as though government can cure all ills.

I think they are misguided, but they truly believe it.

The dems are lying like they always do(former dem and NYer).

Besides, dem infrastructure spending means they will study the issue for a decade, with half the money spent on dem consultants who don’t know $$it about anything, and the other half going to plug holes in dem area’s mismanaged budgets.

Much of the public today (especially recent grads of public school system and higher ed) has been led to believe gubvarmint is the ‘solution’.

Hence, those who count on a gubvarmint backstop for moral hazard, and those who rely on welfare, entitlements, and other handouts from it think (if they think at all) of gubvarmint as a combination of Santa Clause, Tooth Fairy, and a rich uncle that will always be there for them.

this for pet and mr57:

Both right on the money and wonderful wonderful responses to this very challenging times that besides what us old folks know from experience,,, we know a lot more about the formerly mostly hidden stuff due to the reporting by Wolf and the commentariat on WolfStreet.com, and I thank you all for helping this old boy’s modern financial education.

Old ”joke”,,, ” How can you tell when a politician is lying? When his lips are moving.”

Hoping that will change with all the wonderful well qualified young women coming along these days.

Thanks for the gubvarmint H,,, may have to adopt is as a more appropriate/accurate description instead of the ”guv mint” I have been using for decades…

Maybe we will see 40,50, 60+ year mortgages before this is all over. There are many parts of Florida that are still much less than 2006-2007 period, especially in lower priced markets because those (lower priced) properties were probably bid up with so called “liar loans,” which are no longer allowed. However coastal cities and towns in Florida are likely higher than the peak in the previous bubble.

I think the biggest difference between this bubble and the previous one is that lending standards are better now. However there might be other equal or worse perverse circumstances that will cause problems that could be worse than before.

The article by wolf street and the comments followed above are of intense interest. Who would have predicted that the financial markets and real estate would go up so much after the pandemic started.

Yeah, better standards , 2% down payments.

I paid $275K, in 2003, for a house in West Palm Beach, FL. By 2006, a similar model had sold for over $500K. Now, the house is worth $360K.

My colleague bought a house in Wellington in 2010 for around $125k. People laughed at him at the time. It’s probably at least doubled or tripled since then.

Lending standards arguably are quite loose now.

FHA in particular, but including to some extent other GSEs like Fannie Mae, is loose as a goose if you look at relaxed standards like low FICO scores, cartoonishly low down payment requirements, and even down payment ‘assistance’ for those having trouble with those low down payments. In other words, dodgy borrowers with very little skin in game.

Hence, FHA mortgage delinquency rates were high even before COVID and today they are shockingly high in many cities.

In looking at the broader housing market (both in cyclical and even linear markets), one thing for sure is that historically low mortgage interest rates (thanks to Fed) are main enabler of our monumental bubble (although there are of course numerous other factors at work like foreclosure forbearance).

The biggest housing bubble in the entire United States is Reno, Nevada. The median house price is $500,000. This is up 23.5% year over year. Median HOUSEHOLD income is $58,790, and it’s an area where $15 per hour warehouse jobs are considered “good.” This is beyond outrageous – it’s criminal. You’ve got people paying nearly $1,000 per month to live in RV parks.

I forgot to add that Reno, NV house prices are up 350% since 2000.

I was definitely not expecting to see this as Reno doesn’t show up in most of the big reports. Your comment matches exactly what I have been observing here for several years. My parents recently visited and asked “What are all the high paying jobs here that support this?” Shrug…dunno..cant think of many or any high paying jobs that support industry outside the area. Feels like most of the high paying jobs are local lawyers, local engineering, local etc. Feels like a tinderbox waiting to go.

Wolf, wanna bite and add Reno to the next bubble report? :)

It’s 100% speculation. Last bust, Reno crashed worse than almost every market in the country, save for maybe Bend, Oregon – another area with shiddy jobs which don’t even begin to support house prices.

Did the RE sell for lower prices after the crash, or did the banks hold on to them?

RE Bend, Oregon

Isn’t that a haven for distance runners?

Tesla! But the wages he pays don’t support that kind of home price appreciation.

Right l,

This coming as result of CA folks wanting to be out of CA taxes and SO much controlling of freedoms, while still wanting to be near enough to enjoy SF Bay area wonders, some really world class wonders such as walking across the Golden Gate, but also many other world class ‘stuff’ etc., etc.

Not to forget the totality of the skiing and other outdoor opportunities in the nearby Lake Tahoe and the many other lakes and mountains.

Nothing supports the prices, and the city is an absolute dump.

My friend has parents who bought in Reno 2 years ago. Apparently, it’s a hotspot for blue collar California state pensioners who don’t want to pay california income tax. This couple makes will $400K / year for life from Cali taxpayers courtesy of the Dept of Corrections but don’t want to contribute back in. lol

Idaho is the same.

I may add, the 2017 tax bill completely distorted the free market for recycling homes to new families. When you sell your highly leveraged home, you could lose a lot of the tax advantages of a large Mortgage Interest deduction if you have one. People are staying put to keep the tax advantages. If you have paid off your home and want to move then the asset is also a great investment as a rental asset. Rents are going through the roof in the Swamp, for single family homes due to the pandemic WFH effect. Where can you get this rate of return compared with a bond market at less than 1% average risk free returns. This combination of distortions, the 2017 tax bill, and lack of decent competing returns on capital because of the Feds interest rate repression has depressed available homes for sale, resulting a supply and demand imbalance and inflated home prices. I don’t see this changing anytime soon, unless the interest rates start to rise substantially on the 10 year Treasury rate. When and if that happens, the bottom will fall out of this housing market worse than it did in 2008/2009.

California’s Prop 13 has caused a similar effect of people not moving for the tax advantage for decades now.

That’s me. I inherited my place in Napa Valley, and the property taxes are so low that it keeps me here. I know it’s completely unfair, but since I am a retiree, that tax saving is enough to keep me from selling and going elsewhere.

“I know it’s completely unfair…”

It is not unfair. Just fortunate.

Yeah, I think California’s biggest mistake was not instituting “portability” the way Florida has. For example, in Florida, if you have a $500k house with a $250k tax basis because of the cap on tax appreciation, and you buy a $700k house, you get to transfer the $250k in “savings” to the new one, so the new house is taxed as though it’s a $450k house.

“It is not unfair. Just fortunate.”

Of course it’s unfair. Charging the young couple 3x the taxes on the same product as an old person is discrimination.

What was Prop 13?

It limits property tax increases to 2% a year, so you have situations where a person pays $5k in property taxes, but the new buyer will pay $30k when they sell it, as the basis “resets” when sold. That might be an extreme example, but it’s not uncommon.

You can take prop 13 with you anywhere in the state.

But you can’t avoid the huge capital gains tax on a home purchased decades ago if you sell it. The hit is especially hard if you are taxed as single.

RightNYer

The couple paying $5,000 a year in property taxes has been paying them for 30 or more years, and the dollars they paid with were worth 25 to 50% more then before inflation.

There is no top for house prices. However, there is a bottom for the dollar, and it is a very, very small number.

“So the index value for Los Angeles of 315 indicates house prices in the metro have surged by 215% since January 2000 – meaning they more than tripled in 20 years – thereby making Los Angeles the most splendid housing bubble on this list.”

When it last 20+ years, can it even be call a bubble anymore? More like this is the new F up paradigm created by the FED. I am about as bearish as they get seeing all the insanity in housing & stock but even I struggle to picture how anything would bring a sharp reversal to this insanity, especially with FED on ever trigger happy to pump more liquidity, mix that with Reddit “investors” or Instagram real estate “experts” hyping up the market to infinity.

If the California PUA Fraud alone is $20bln, add on the rest of the country, then add on the rest of unemployment fraud PLUS fraud in PPP loans. How much is that? My head is spinning..

Now, how much of that, what percentage of that, was re-invested in single and multifamily housing in the US? Straight up or through hidden LLCs or straw buyers? Because I’m sure some percentage was.

Wells Fargo just fired 100 employees for defrauding the PPP loan program.

All 5 major Banks are criminal syndicates. They’ve milked the Covid-19 to boost their bottom line.

Yep, LA looks bubbly, allright.

Vegas and Dallas average 5% a year since 2000.

What can possibly justify 10% a year increase, I wonder… Foreign Investors, GDP growth or Inflation of Assets? Fed

started heavy printing in March, not that long ago. When LA was running hot last 8 years in a row.

What’s next, collapse or correction? And when, more importantly?

Even SF and NY condos are essentially holding the line. With no inventory available and lenders with nothing to do, I am guessing they are approving more loans since there are so few applications.

Do condo HOA fees tend to go up when the values of the condos go up?

Every now and then I get an unnatural urge to look into moving into a condo, then I hear horror stories about rampant HOA fee increases, and it stops me in my tracks. It seems that it’s cheaper to own your own home and pay some service to do the lawn/snow, etc. HOA fees appear to be a kind of racket in the area I’m in.

I couldn’t help but notice prices are rising the fastest in LA, San Fran, San Diego, Seattle, Phoenix, and Portland, which are all in non-recourse mortgage states. People will pay just about anything for a house if they have the ability to walk away from the mortgage and only lose the down payment, if and when prices start dropping. Especially if they get an FHA mortgage with only 3.5% down.

The federal government should not be subsidizing this risk taking.

+1. The government overreached on this.

They overreached….AGAIN !!!!

At some point, you have to believe bailouts are intentional and planned by corrupt individuals in leadership positions.

They’re all speculating in real estate. Surprise, surprise!

Public Private partnership at its best!!!

I mean you have to have two hands to clap no?

Which overreach are you referring to here, specifically?

The Government should not be in the business of guaranteeing loans. Freddie, Frannie, all that garbage.

Oh, okay, yeah I agree. I thought you were referring to something specific that happened post COVID.

I’m thinking the bubble is more about proximity to the Pacific Rim. Check out the real estate bubble in Vietnam; it’ll make most of the US look tame.

All that money that used to go to American Labor, now gets funneled back into the real economy as high asset prices by our Wall Street and Chinese overlords

On the BBC news website a few weeks ago, they were talking about “house price GROWTH” instead of house price inflation!

That is the disgusting thing about it. Government, central banks and MSM all promote this as “wealth creation” and nobody in the MSM ever calls them out on this.

don’t believe it!! For once australia leads America in insane house price inflation!!

Australia, New Zealand, and Canada have beat us on house price “appreciation” for many years.

Murdoch’s media especially keeps promoting real-estate as a no-loose proposition. It has become so expensive in Australia that almost no business can survive because the land costs are so high. The Australian dollar has been fiendishly losing purchasing power. Down about 33% in the past year measured against commodities (real things).

Yes, “inflation” is often called “growth” in prices. Sounds much much better than “decline in purchasing power” of the currency.

“QE” (quantitative easing) also sounds a lot better than “printing fiat money”.

The problem is inventory.. no one is moving. Sales in my country dropped 60% from 2019. So you have the same people looking in a market with 69% less supply.

Until COVID and government policies stop gumming up the works, this trend will continue.

Fewer immigrants and declining birth rates, signals excess supply. The problem is speculators, at the bottom, buyers take a second home and put it through an extended remodel, which is no problem as long as prices keep rising. House next door to me has been off the market for over a year. The contractors went on a three month vacation. No rent coming in, mortgage payment due, (or in forebearance?) it’s all good. You are adding value to the property which is gaining value every day regardless.

Once the price appreciation goes into reverse, you will never see people working so hard to get a property to market. Everybody’s a genius on the way up. On the way down, they all get religion.

Yes I agree supply should be increasing (eventually). However under the current conditions there is no reason for it to. Let’s see how long extend and pretend goes.

It’s been going for almost 15 years. At this point I will probably die before I buy a house. In fact, I don’t even really need one at this point.

I can’t even buy a house in ridiculously high taxed cook county. I can’t even see a house because multiple offers. Wtf is happening here? Just past year it was dead. What’s worse? Higher prices and low rates or vice versa?

A disagreement:

I do wish to respectfully disagree with Wolf’s up above comment about not comparing inflation with inflation. Certainly, today’s virtual 0% has added to the buying rush, and the devaluation of the dollar is also reflected in rising prices. However, none of this would be a problem if wages/incomes had kept up with REAL inflation, and they have been suppressed for decades. Of course this assumes that house buyers are working and not on declining or fixed incomes.

You can’t build a modest home these days for under $200 per sq foot. The actual price by a decent builder constructing to accepted standard is $300. For a 1500 sq foot rancher this is 300-450K. Add on land purchase, fees and permits, hookups etc and you are in the realm of $600K. Obviously, in vibrant cities everything would be more.

Insurance companies require a $300 per sq foot valuation for replacement costs, at least where I live and this ain’t California.

And I haven’t been through Reno for a long long time, but I wouldn’t put it on the attraction list with what I remember about it.

I am a retired carpenter. I am approached frequently to do work for people, folks hoping for a cashie job to save a few bucks. There is one reason why I never take the work on. I can’t bring myself to actually charge the prices needed to do the jobs. I’m presently doing a reno for myself and going to town for materials today. 1 gallon of good paint will be $60. A sheet of plywood $60. Luckily I plane up and machine my own trim and casement materials where we are talking dollars per lineal foot from the building store. My clear yellow cedar trim is free….to me. I know the supplier costs in town…..they apologise but that is what they have to charge to survive.

A qualified and competent tradesman requires $35 per hour at a minimum if he/she is also to own their own modest house and feed their kids. The contractor has to charge out at $50 to $60 per hour to pay for the tools, trucks, operating loans, and their time. A minimum callout has to start at $100 to make picking up the phone even worth the effort and time. It is like the old school math of time and distance problems. Punch in the numbers and it has to add up or you run out of gas or never arrive. :-)

The point of this comment is that NEW construction and replacement costs set the market floor whatever the locale. If it costs X to build new, then this particular used house can fetch Y. When the lines cross because of demand, then more stuff gets built. As long as rates are low the financing will continue. If people in other countries stop using the dollar and the value drops further, it’s all over. If wages continue to stagnate, it’s all over too. And just look at the bitching about a $15 minimum wage (by 2024 for God’s sake). That’s 30K per year if someone works full time and no one can make it on that.

Get used to the homeless camps because the pie is shrinking for the bottom 90%. The voting population has been bullshitted so long about unions and socialism they’ll believe the memes until they move into their own underpass or tent. This might be the last generation with a bunch of cash to actually buy homes. And if someone falls off the straight and narrow path wagon of getting ahead, good luck starting over and regrouping. Pandemic, anyone?

Paulo,

All the items you mentioned whose prices have surged and therefore drive up costs for builders are different parts of “inflation.” Loss of purchasing power. Takes more money to buy the same thing.

Depends on where and when you are p,

Started paid employment as helper/apprentice in Naples, FL building the finest homes for $12.50/SF; they now sell in the low $K range, with the dirt.

At the time, basic new homes were selling around $10/sf including dirt, utility hook ups, everything. they now $200-300/SF

Good neighbor is building 10-20 homes per year, said it was now $120/sf for 3/2 CBS, all included for average 1400-1800 SF.

Otherwise, as usual, as another retired carpenter/analyst, I agree with the rest of your post, and thank you for continuing to post on here.

With Wolf’s great reporting and especially his great graphs and the long term experience of the commentariat, there is a lot to learn here.

50 to 60 an hour?

I’ll flip burgers.

Salary, taxes, insurance..liability, health, disability, retirement, business expenses.

No thank you.

Those are the contractors who do cash

So their union, and govt, does not know about it. I’m surrounded by it.

Front page headline in today’s Minneapolis StarTribune:

‘Twin Cities home prices jump 9%’

“The global pandemic also reshaped the market. … a surge of interest in larger houses with home offices and big yards in the outlying suburbs.”

“And with sales outpacing listings in parts of the metro, the total number of properties for sale at the end of 2020 was down nearly 40% compared with the previous year.”

As I’ve commented a couple times since March 2020, the century-old Craftsman bungalows in my 55406 neighborhood are selling quickly and at prices above listing. For the Twin Cities metro, the median sales price has doubled in the last eight years.

And are those Craftsmen homes recently remodeled or are they endless money pits. I like the ones like on the sitcom the neighborhood (are they Craftsmen?) But I’ll bet it would cost $200,000 to get them that nice.

Scotty,

These are pretty well maintained homes. Most have been updated. Mine is a Sears home, and in my immediate area about one third were build-it-yourself from Sears.

A nine foot tall ceiling, a brick fire place, glass & dark oak French doors from the living room through dining room on the south side and nice woodwork is what one sees when entering my home. Classic and comfortable is how I would describe the style.

My neighbor’s homes across the street and to my side that sold this summer are similar. They looked great at their showings, and had professional inspection checks from the buyers.

thanks for the continuing boots on the local dirt reporting dr,,,

kinda sorta similar here in the west part of the tpa bay metro,,,

not so many century old ones here, mostly in my hood that goes from mansions to basic ’50s winter homes for two people, almost double in the last 5 years, and many of the smaller old houses going down to make way for modern 2 story homes with double garage double SF overall, and same price per SF, approx $200.

In spite of all the very clearly ”prices” going there, in fact, the houses and the underlying value of a home have not changed one bit in the last 60 years…

Gotta be the degradation of the USD as Wolf posits and supports lots of clear supporting data for with re us RE.

Plans are afoot to new build single family homes for rent. Rents will be market rate but no down payment needed. I bet government subsidies will also be available. Also, current home owners will also be eligible for a reverse like mortgage scheme without the final transfer of home. I read that a person could receive a lump sum payment, stay in the house and pay rent. This is a Wall Street critter and supposedly new companies are being formed to execute this. I wish I could produce footnotes to the report I saw several months ago. Anyone see them also?

The mega landlords are contracting with developers to build rentals for the last couple of years. Be careful where you buy new construction because an entire section may be rental homes.

The worst part of the rent to buy scheme is that many renters will participate in these scams which basically transfer the responsibility to maintain the home to them. So if something breaks, even though the renter doesn’t own the home, they are responsible for all repairs, while still paying rent. And in the end the renter will never own the home anyway.

Post GFC you had to watch how many in the neighorhood were on section 8. They had either lost the home and were squatting, or they had been bussed in. You were buying into a homeless camp with McMansions all around. The problems were worse in exurbia. Now you can buy and sell without an RE agent and cash buyers. The banks never foreclosed on properties in that crisis, now it seems they are and they have Chinese names.

I expect that reverse mortgages are going to be a big thing in the coming years, because pensions will be much lower than most people were expecting. People will have to eat their house!

In addition to that, also the government needs to find a source to fund the increasing expenses in the coming years. The obvious source for that is of course housing, because that is where most of the wealth is concentrated. But people won’t have the cash to pay the increasing taxes, so also for that reason they will be forced to take a reverse mortgage on their house in order to pay their taxes.

So, it’s a no-brainer. There will be wide political support from the growing zoomer and millennial demographics, because they are fed up with paying for babyboomers after they have been denied affordable housing themselves, and have been denied opportunities to save for their own pensions because of ZIRP and inflated stock prices. The financial industry will also lobby for it, because of massive profit opportunities.

Does this mean that there is actual inflation in the USA..ha ha ha

You have to laugh when Govts say inflation is very low but don’t worry, they will claim lower inflation when the bubble pops..(if ever, who knows?)

We are at the end of a 40 year bond bull market. The wind has been to our backs in both housing and stocks. We are now looking at a 40 year bond bear market. Both housing and stocks will be crushed. Welcome to the decade of “Fear and Loathing”!

Heard the same thing in 2012, 2013, 2014, 2015, 2016, 2017, 2018, 2019 and 2020. Maybe you’ll be right this time!

According to the Chief Economist for the Bank of Montreal, in Canada, the price of houses (which are est. 47% higher than in the U.S.) are at the current level because people want to pay that much!!!! –

In most of the commonwealth countries, mortgages are 5 year zero interest loans. Every 5 years you have to reapply for the loan and never have to pay principle. The whole real estate game there is price appreciation, selling at a much higher price than what you owe the bank.

Sorry, I meant to say interest only loans, not zero interest loans.

Well, that’s almost the same nowadays! :)

Two different chart patterns up there – places where today’s prices surpass the previous peak and places where prices haven’t got back to that level yet or have only recently got there.

Motrgage forebearance and foreclosure moratoriums affect over 10, maybe as high as 20 percent of the mortgage market

Why wouldnt you reach for a house when you dont have to pay off the loan.

5.4% of all mortgages are in forbearance at the moment.

Don’t worry, I bet new mortgages will be issued to replace old ones.

Fannie and Freddie will pay the old ones in FULL, because of …. inclusiveness or some such.

So what is the take-away? I never been in a better financial position in my life, at the same time it feels hopeless out there, just as in 2005.

If you think the market is topping out….sell and make out like a bandit. You can brag about it later while you’re sipping daiquiris on the beach.

I’m not sure about the current mania. To give money with low interest rates is a different game than the game played in 2007. It seems like 2007 was about greed, 2020-2021 is about survival.

I am playing by the rules of 2007, which were then changed in 2008. So, now the rules have changed again, with accelerant. I can get an 800000 (loan amount from a major) mortgage right now for 4300+ tax insurance all included- I can get 3500-4000 on that house in rent.

The Dallas chart shows yet again that a high property tax is anathema to bubbles. No 2008 at all there.

I do wonder, however, how much of the growth these days is the 1% buying better houses and/or moving as opposed to regular folk.

if your state switched gears and raised property taxes like Texas (even while lowing taxes elsewhere) everyone who bought in the last few years will get clobbered. High purchase price and mortgage combined with high taxes while housing prices are dropping due to higher taxes forcing prices lower. I like the Texas tax policy as higher property taxes mean money stays localized while low property taxes enable bigger mortgages and interest sent to Wall Street and banks.

Agreed but raising taxes isn’t the only way to shift the policy.

The recently defeated ballot proposition in California which proposed separating large businesses with the rest of the real estate ownership base was one example.

Of course, that progressive state defeated both the Prop 13 reform and the gig worker reform.

Good to reaffirm that limousine liberals only case about causes that don’t hurt their own lifestyles or pockets.

Leads to an analogy….

Long mortgages with no recourse are the housing equivalent of the gig economy. You’re paying rent to the bank, and you’re also taking all the responsibility for repairs and insurance and taxes. With a gig, you’re receiving piecework wages, and you’re also taking all the responsibility for health care and insurance and taxes.

Both systems break the former arrangement of two-way responsibility and two-way constraints.

Now the responsibility and constraints are solely on the individual. The bank or employer has no expenses and no constraints.

Inventory at its lowest point, price at its highest and existing home sales climbing to a decade long high!

In times past I would have been in wait and see mode. I’m re-adjusting my beliefs these days. This is a different world run by people with an agenda that doesn’t include rational markets.

Respectfully, this is not a bubble. Not Equities, not housing and certainly not securities! We will have corrections like last February in equities, we will have periods of softer prices and higher inventory in housing and securities will never again be allowed to price on the open market.

We are in a new world and this is a hard pill to swallow for this Libertarian minded individual.

C

“Respectfully, this is not a bubble.”

Then please, please tell us wise one what you think current insane and unsustainable economic conditions really are.

A socialist dream. Government intervention everywhere! As I stated prices will soften but uncle sugar is always coming to save this party! Some areas outside of city centers are going to go fully insane! Some city centers maybe abandoned but don’t be fooled by local differences in price this party is never going die!

We’re living in a new world old school economics is out the door!

C

Agree C,

Most of the time, it takes a long long time for those in the power that corrupts, not to mention the absolute power that corrupts absolutely to even start to realize any kind of event/change.

While to some of us, for sure, the only constant is change,,,

most of the time every day change…

Change can be challenging or worse for those stuck in any world view/or and other kind of belief system, so we who pray can only hope and pray for all of our species to get beyond all ”believe systems” and be able to focus on the here and now.

So the stock market bubble is a socialist dream too, huh?

Copy that. This can go on for many more years, and don’t think for a minute that wealthy, powerful people in the world don’t have an exit plan. If history is any guide, we will get a currency reset, and you will want to be in front of it.

I thought the same in 2008-2009.

It’s not a bubble unless and until it burst.

The above data points are far less interesting than median income vs. median house price.

I certainly agree the printing has no end in sight, but affordability is always an issue.

In Seattle, I see home prices rising but I do not see rents rising. Today’s buyers are going out on a limb. People go through a rent v. buy analysis. If the difference is too great, things will revert. Either rents go up, or prices go down. In this economy, I don’t see rents going up. Landlords are very lucky to keep the renters they have at current rental prices.

I sold my 1m+ house in an affluent NJ suburb 3 years ago. THe buyer ( a developer)expanded on the house and placed it on the market after about a year. It is still on the market . Our friends in NJ have told us that the market is dead

Everyone has been calling this a bubble for many many years now. So what would these curves look like if we weren’t in a bubble? Pretty flat? Only with the rate of the rest of the economy’s other measures of inflation? What curves would the housing index graphs need to look like to make the claim that we’re not in a bubble?

Why on earth is the taxpayer still buying MBS ?????

Good question. Who’s making the those purchase decisions – Beevis or Butthead?

They’re MBS the taxpayers are already on the hook for, unfortunately.

QE continues. “The Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage-backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee’s maximum employment and price stability goals.”

Price stability guys? ROFL

I can’t for the life of me understand why people venerate this man. It’s like giving accolades to the parents who give in to their bratty teenage children because it’s “easier.” Sometimes the right thing to do isn’t popular, and that’s what makes someone courageous. Powell is a coward.

The right thing for whom? For Powell, Pelosi, etc then yeah he’s doing it.

This is always the question for me.In five years will the money be able

to buy more of what you want or will the value of your house be

able to buy more of what you want.Subtract normal living costs for

a more accurate picture.

This is just getting started. Just wait for Janet and Jerome to put their heads together. The shenanigans will be unheard of. It’s getting scary.

Notice how Dallas avoided the 00s housing bubble, but then joined all the rest post bubble pop. Halfway down a long tunnel, and a train is coming.

Median house prices in my zip code went up a little over 25% year over year, per county generated statistics.

Imagine how much quicker house prices could go up if we had 0.9% mortgage rates, which is the current cost of debt for Tesla via today’s TSLA earnings report.

“Price Stability”?? The Fed is in bed with wealthy home owners, not so much those who are forced to rent, making minimum wage. And when Team Blue reverses the $10,000 SALT limits later this year, everyone will know the housing system is rigged for wealthy homeowners who own huge houses, in expensive locations, with higher incomes, which will further increase wealth inequality.

“…not even thinking about of thinking about…”

Fed Powell: “We’re not even thinking about thinking about… (raising rates)”

Fed seems to apply this mantra to their policy unintended consequences…yet are they “unintended”at this point???

“And when Team Blue reverses the $10,000 SALT limits later this year, everyone will know the housing system is rigged for wealthy homeowners who own huge houses, in expensive locations, with higher incomes, which will further increase wealth inequality.”

Which just goes to show how foolish and naive the average Democrat voter is. They are voting against their own economic interests.

Wolf, this is interesting is there a way to plot this nationwide? I’d be curious to see a national heatmap of home prices t see how much this effect has spread to the exurbs and “newer” hubs like Charlotte, Atlanta, and Austin.

I dunno, I’m starting to see some cracks. The high priests at the fed have seen a doubling of the ten year since August of last year after ‘Mississippi’ Jay purchased $400B of US Treasury notes and bonds. Imagine that! He expands his balance sheet from $6.9T to $7.4T and gets a half of one percent yield boost despite that massive amount of propping up the market. So all those billions of dollars of Treasuries that the Fed bought at lower yields are now trading at losses.

Despite everyone pulling out their hair wondering how they are going to fit into a system well on the road to hyperville, maybe we should ask how sustainable is a Fed who in the last thirteen years has multiplied it balance sheet by more than eight times? What is so comforting about a Fed who is imagined to have ‘your back’ while basically destroying their own balance sheet to the tune of $906B in 2008 to $7.4T in 2021?

Twenty years ago, the LA American dream was owning a 3BD home in a upper middle class suburb.

No more.

Today, the LA American dream is renting a 3BD home in an area without gang activity.

Any guess what the LA American dream will be in 2030?

Tiny houses on someone else’s lot.

.

Has income risen by equivalent sums?

If so, then it is supply and demand.

If income has not risen, then cheap money to borrow also equates to supply and demand.

However, in the first case, if interest rates rise house prices will be stable. In the second case house prices will fall.

Watch those rates.

.

“However, in the first case, if interest rates rise house prices will be stable. In the second case house prices will fall.”

You’re sorely mistaken. As interest rates rise, house prices fall. This has been proven by history, because it’s all about the monthly payment for borrowers. Higher interest rates mean higher payments, so house prices fall for them to qualify.

Depth Charge, I think his point is that if income has risen by equivalent sums, then an increase in interest rates likely will mean an increase in wages, so house prices stay stable. If it’s debt based, then, as you said, prices will drop.

Charts on Longtermtrends illustrate how US house prices are tracking above their historical relationship to incomes (wages).

That long term historical relationship was that a house cost around 3 times the median annual income. That ratio climbed to 4.5 during bubble of mid-2000s, dropped during the crash, and stayed above 3 since then (now at about 4).

Interest rates are a prime influence behind this ratio of house prices to income. Lower interest rates make higher house prices more affordable, so naturally house prices go up accordingly. This interest rate impact on housing costs correlates with interest rates trending down since 1981 (also known as our long term bond bubble).

Depends on the reason interest rates are rising.

1. If interest rates are rising because the economy is doing great and people are getting higher incomes then prices will keep going up.

2. If interest rates are rising in a bad economy with the Fed printing massive amounts of money, bond vigilantees going wild, then prices will start to fall.

3. If they are rising because the Fed tightens up like in the Paul Volcker Days then prices will fall.

With clowns like Powell and Yellen in there the probability of ‘3’ is zero.

With the new administration screwing everything up the first week the likelihood of ‘1’ is also zero.

So we are left with ‘2’ .

Enjoy

We’re also starting to see fraud in the VA loan program. This used to be the last place for dishonest practices. But the lenders are getting so greedy they are looking the other way again, just like back in 2007. Now, you see a lot of VA borrowers abusing the loan by not moving into the property and just renting it out immediately which is not the way it is suppose to work. Others are turning basements into rental units, violating the local housing ordinances. They are using the income from the rental unit to pay the mortgage, which they could not afford otherwise. Of course the homeowners insurance company is never notified of this. The lenders also look the other way. With Covid-19 the appraisers can’t even do a proper job of appraising the property. Exterior appraisals just don’t cut it. The loan officers just want to make their commissions. The Realtors and their broker make a fat commission. The lender usually sells the loan as soon as they make it and pocket the lender fees. The VA funding fee is a big ripoff to the Veteran. The taxpayer gets screwed if the loan forecloses. It will all come crashing down just like it did in 2007/2008. This time there will be no appetite for a taxpayer bailout.