National sales volumes have been sliding for a few years, but this is like nothing seen in a long time.

By Kaitlin Last, for Better Dwelling:

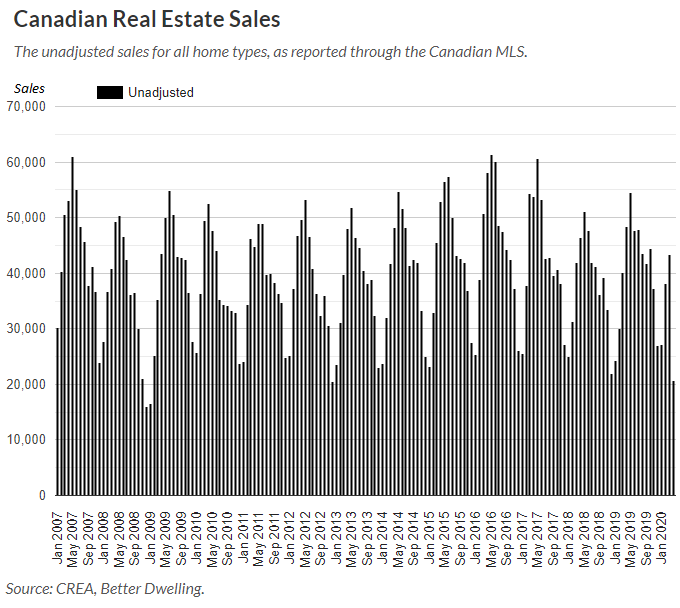

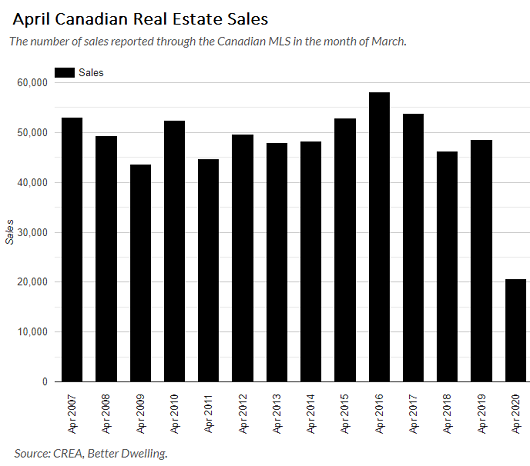

Canadian real estate sales have dropped to the lowest level in a generation. Canadian Real Estate Association (CREA) data shows sales fell in April. Slower growth was expected going into this month, however not this slow. The volume for the month was the lowest since 1984 – when the population was a third smaller.

Canadian Real Estate Sales

Canadian real estate sales slipped to a generational low. There were 16,612 seasonally adjusted sales across CREA in April, down 56.8% from the previous month. Unadjusted sales came in at 20,630 for April, down 57.6% from a year before. Most of the slowdown was obviously due to the pandemic, however not all of it.

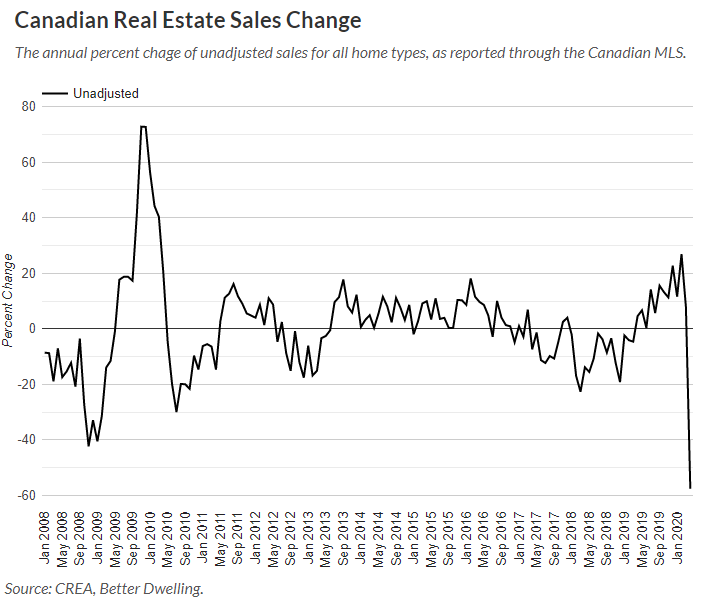

Slower growth was expected before the pandemic, due to the comparison period. The months in the first quarter of this year were being compared to negative growth last year. Comparing it to negative numbers last year, makes the acceleration seem more impressive than it is. Due to the pandemic, the numbers are obviously worse than they would have been under normal circumstances.

National sales volumes have been sliding for a few years, but this is like nothing seen in a long time. April sales peaked in 2016, and have had trouble challenging that high. Last month was the worst April since 1984. This is easily explainable by the pandemic, but the lack of sales volume still has broader macro market consequences – regardless of the reason.

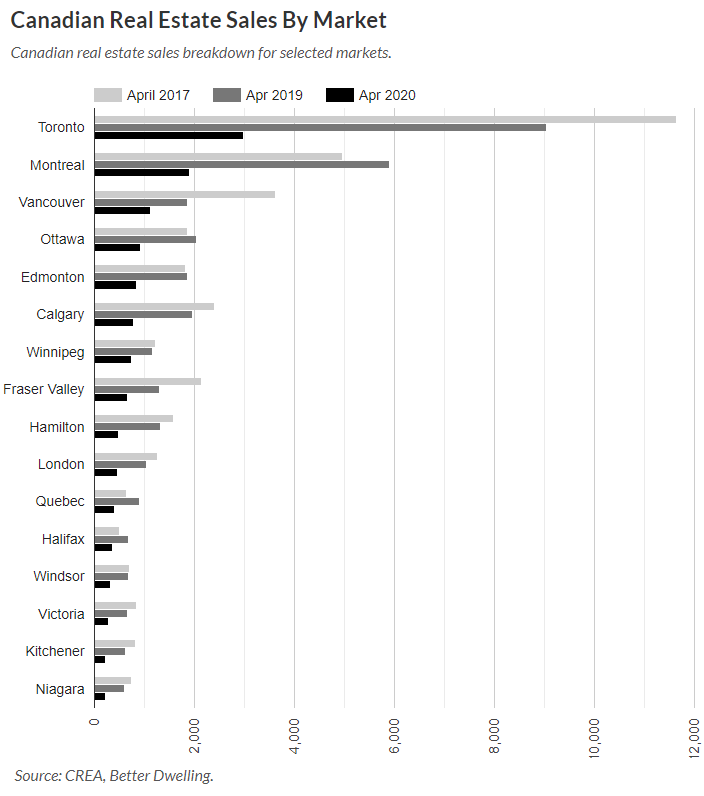

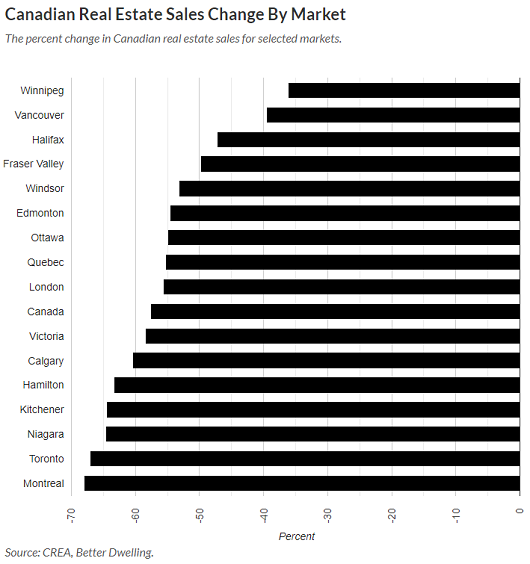

Vancouver Real Estate Was One Of The Least Impacted

All markets have seen an impact, but some markets saw declines of less than half. Winnipeg saw the smallest drop with 739 sales in April, down 36.2% from last year. Vancouver follows with 1,119 sales, down 39.5% from last year. Halifax came in third with 354 sales, down 47.2% from last year. Winnipeg and Vancouver have both slipped for two consecutive years.

The largest drops were in Eastern Canada, with Montreal and Toronto taking big hits. Montreal reported 1,890 sales in April, down 67.1% from last year. Toronto followed with 2,975 sales, down 67.1% from last year. The Niagara region came in third with 213 sales, down 64.6% from last year. Both Niagara and Toronto are in the same economic region, and both slipped for a second April in a row.

The insights in this month’s numbers aren’t as clear as most analysts claim. Sales are predictably down, due to pandemic measures – that’s obvious. Sales will rise as the pandemic measures are lifted, that’s also obvious. What isn’t clear, is whether the volume can be made up without driving prices lower. The Bank of Canada is forecasting mortgages in arrears will triple over the next few months. They don’t see the arrears rate peak until next year – and this a conservative, anti-fear mongering forecast. If that happens, some buying volume may be delayed as people wait for the air to clear in the market. By Kaitlin Last, for Better Dwelling

“The next big shoe to drop will be when appraisers call a declining market in early August.” Read… “Pent-up Supply” is Building up in the Housing Market: Example of San Francisco Bay Area’s North Bay

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The last report I read on Toronto real estate said everything was roses!

Everybody was adapting to virtual tours and closing deals virtually too!

I guess those were just virtual sales!

I am very sorry… what you do not understand…”It is always a GOOD time to Buy!!” – Now, get your sorry butt in line and get with the program…

Only those making profit In the real estate biz will tell you its great. They can’t afford to have the public know the truth. It turns business away

Canada has the craziest RE market I’ve ever heard of, crap shacks for C$1.2M on median salaries of C$80K.

Just the other day, I listened to a podcast out of Canada, a woman was relating her current experience trying to buy a house. She has been looking for a couple of years and feels totally priced out. She happens to work in banking and says the houses going into foreclosure usually have a primary and second mortgage from a B lender.

The B lenders, in a foreclosure, are buying the homes from the banks to keep the second mortgages from being wiped out in the foreclosure. If they weren’t doing this they would be going into bankruptcy themselves.

If one is priced out in Canada there is always Alaska, Greenland. Iceland is nice this time of year. But, but.. free healthcare. Siberia has free healthcare for free, I think.

Where is SoCal Jim when you need him.

Iceland is very expensive and a great place to live if you don’t mind the cold , the dark and the overall isolation

Sounds like a cold version of Hell!

Second that. Amazing in summer. And the health care is almost free, as well :)

The publication is from groups of realtors…

Nuff said, everything is always good.

This is why the prices are so far from reality as they have colluded together. Many scams are going on behind the scenes.

Actual pricing is collapsing.

Gaming the system has made actual costs are 5 times lower in big cities.

Hi Petunia.

Are the residential foreclosures in Canada, per the scenario you described, “recourse” or ‘non-recourse” with respects to the borrower?

Are the big Canadian banks usually the lenders or are smaller institutions for residential?

Thank you.

I believe almost all residential real estate loans in Canada are recourse.

They are all recourse in Canada. Most financing is done by the big banks and local credit unions. CMHC requires a hefty down payment. And once again in the WS comment section, stats are taken from a few markets and extrapolated to a country bigger than the US.

So, are houses sold in Tennessee the same as Boston or the Bay Area? Of course not. Are crap shacks 1.2 million across Canada? (The answer is, “No”.)

Vancouver Island anecdote: I am presently involved researching RE market in prep for an estate sale. This is a house located on east Vancouver Island, in a small city of approx 40K. The house; 1 block from the beach, quality 3 bedroom, nice cabinets (cherry), hardwood floors, sunroom, 2.5 baths, new roof, etc should fetch around 540K. This is with the 3% drop in selling price since Covid and lockdown began.

Houses are selling around here, at least those that are still listed. Many sellers took their houses off the market because they did not want buyers looking through their houses during the pandemic. That is one big reason why sales are down. Fewer listings are available. The house we will be selling is empty, so it doesn’t matter. There is one interested private buyer, and if that doesn’t pan out we will be listing with an agent. Our goal is to have it sold by the end of July. Since our favourite RE agent just retired, we have been researching others and will make a decision, soon.

Tomorrow is a cleanup and boxing day, and getting ready to disperse stuff. The decks need pressure washing, and so do the gutters. We have a grounds maint company doing the lawns weekly.

I suppose if this house was in Vancouver it would be 5X as expensive, well over 2M. But it isn’t, so it is 20% of that. Will prices drop on Vancouver Island? The answer is, “It depends”. There is a greater interest in smaller cities these days, and this is a time for evaluation. Certainly, retirees and other cash buyers are still moving to the Island for the weather and lifestyle. There are still entire subdivisions under construction as well as spec homes by smaller builders. My buddy runs the local main const material wholesaler and they are still quite busy filling orders. My carpenter brother in law has 1 year work lined up in the Courtenay/Comox area. They haven’t missed a days work this year.

regards

Shiloh,

I’ve been listening to this podcast out of Canada for a couple of years now. They mostly concentrate on real estate in the major cities of Canada.

The general consensus is that real estate is funded with Chinese money, laundered money, or through non-conventional means even for conventional borrowers. There’s the bank of mom and dad for down payments or many private investors funding down payments. There are also many B lenders funding down payments or cash out second mortgages. But the bulk of primary mortgages are still with the big Canadian banks.

Well.

Your Chinese comment would chime in time with the other articles for 18 May about Hong Kong real estate. I guess chinese investment has found its way into housing and commercial real estate.

To what extent will that apply to the European housing and commercial real estate picture?

Anecdotally I have heard that Chinese investment is significant in London. Maybe it is elsewhere in the UK also?

Petunia, your comment is too general. Vancouver is the place with crap shacks for 1.2million. Most of of Canada is not like that. Housing is too expensive in most of the large cities compared to income.

Toronto has way to many condos. I have had the opportunity to travel to many countries and many major cities in the U.S. and I have never seen a city building as many condos like Toronto. This has has been going on for at least 15 years.

In one small section along the lake front I can count at least 20 cranes building new condos. Yikes.

Toronto Mayor will whine to Trudeau and get big bucks to add more immigration to the city. Seems how this system works.

That’s true Joe.

Most of the immigrants can’t afford a million dollar crap shack..

The ‘B’ lender in Canada, i.e. 2nd mortgage lender, has the ‘equity of redemption’, first dibs on taking over the property. Some people do this as an investment strategy: besides receiving the premium interest for a 2nd mortgage they effectively have an option to acquire the property by assuming or paying out the 1st mortgage.

BTW, ‘power of sale’ is the preferred method of default; foreclosure takes much longer and power of sale actually benefits the defaulting party; any surplus equity over mortgage and expenses goes to the unfortunate previous home ‘owner’.

My local Paper, the “Santa Rosa Press Democrat”‘s headline on their latest Real Estate article asked “Is it a good time to buy?”.

They mentioned the significant drop in listings and sales and then quoted several Broker’s and sgents, one of whom mentioned that it is now a “Buyers Market”.

If you see the property you want, You can afford it without stretching and the resale price doesn’t matter due to your circumstances it is always a good time to buy.

If that is not the case, be prudent.

It’s been a long up cycle and this looks and feels like a long over due correction to me.

Prices are usually sticky on the way down and the best advice I can give is to buy when it makes sense to you.

Please do not bet on any real (Above inflation) price appreciation happening any time soon, unless it is a bet you can afford to lose.

A correction is an understatement, try a CRASH.Most people are in jeopardy of losing their jobs or are taking salary reduction in pay and benefits. The new requirements for a housing loan are a 700 credit score and 20% down, most Americans barely have 200.00 in savings. A great depression is coming, real estate will soon be the least of your worries.

Well, I do hope no one overpaid in this environment.

At 40:1 leverage.

All for that sweet equity.

And they didn’t throw that silly money away on rent.

The equity is inflated by the realtors and not real.

Check with the bank/lender and it could be quite a different story to what they will allow you to borrow.

Banks are being more diligent now in risk with the new high unemployment.

Hasn’t there been some complaint made to the SEC today/yesterday about real estate valuations being artificially inflated by some larger financial institutions? Artificially high valuations that high led to overblown loans and then fed into the face value of MBS subsequently packaged up and sold on?

Not sure, saw something in passing.

I know it’s taboo to discuss, but I’m waiting for the bank mortgage deferrals to wear off. Hopefully job losses in Vancouver continue to climb too.

If I’m lucky, I will be able to buy a place for the balance of the mortgage. (Assuming the seller didn’t buy at the top)

Unfortunately, the Canadian government treats the RE market as too big to fail and will let dirty Chinese money flood back in.

So if housing prices don’t drop like a rock in 6-12months, I don’t think anything will cause them to drop.

The Chinese money never stopped flowing in Canada. It was sidelined to other cities when Vancouver passed the foreign buyer’s tax. Also many HK Chinese hold Canadian passports, so the demand will only keep increasing as HK keeps being squeezed.

It only takes about C$500K to buy yourself Canadian citizenship by buying property. Then you can educate all your children on the govt dime, use the healthcare, bring in your entire family. It’s a bargain, you get all that for the price of a one bedroom condo.

Hoping for job losses?!!

Not sure what is more depressing, you, or the lack of comments.

Here’s to hoping your not “lucky”.

The local Chinese are still bidding up home prices in all the Chinese areas except in Vancouver. Check Markham, Richmond Hill, Unionville and Stouffville. Prices have already risen about 10 percent in all 4 cities this year. All four cities with the exception of Stouffville are basically all Chinese. The Chinese from Markham are moving up to Stouffville. With zero interest rates the stupid local non-Chinese will once again bid against the Chinese and drive home prices to the moon. Long Genworth Canada.

Canada does not have the mortgage interest tax deduction like the US. But I bet there will be more people from China putting money into Canadian RE, and avoiding the US, given our new US Cold War with China.

Many years ago, in the 90’s, I felt that some buildings in Vancouver resembled Hong Kong. I think Chinese interest has been strong for years. I follow Greater Vancouver real estate as I’m looking myself, but prices are very high still. As long as you got Chinese money purchasing, you will not see a sell off.

Why on earth would you buy in Vancouver, now? The time to have bought there was in the late ’60s and 70s. Every aspect of the city is unaffordable.

Chinese interest in Canadian real estate started shortly before the British handover of Hong Kong to China in 1997. Rich Chinese thought of Canadian real estate as a hedge against possible future troubles in China. China became an economic superpower after it was admitted into the World Trade Organization a few years later and created many multi-millionaires. Canada was quite interested in attracting rich immigrants while the US was still focused on family reunification. My guess is that Chinese money will continue to prop up the Toronto and Vancouver markets for a while longer.

I agree, Chinese money will never stop. Chinese money supply has increase by 11.1 percent over the last year, fastest in 3 years, it’s holding at $29 trillion. This is money printing on steroids. And interests rates at 3.85%, a new low. Even if just a fraction of this is laundered in global real estate it will affect markets in a big way. So Canadian property owners have nothing to worry about, pretty soon they’ll be back up to 1.2M crap shacks again.

Question #1: how are all those Chinese millionaires going to be able to travel to Australia or Canada to buy a house, let alone live there?

Question #2: since the Chinese economy seems to have met some poetic justice (their plan to ride this crisis to the top of the world has backfired spectacularly), how are all those new millionaires going to be created?

Question #3: how are the Australian and Canadian governments going to manage the mounting anger at China and at the OMS/WHO? A few damning leaks to the newspapers, like the German government has been doing, are not going to be enough this time around.

Our whole relationship with China will have to be throughly re-evaluated after this crisis. This includes how to handle capital flows, meaning the cash needed to buy those houses in Toronto and Vancouver.

The Canadian government’s long-standing attitude to turn the other way in the name of goosing local real estate prices won’t get them anywhere this time around.

Time for a big marketing push. Add a garden rake to that maple leaf symbol. And a catchy slogan like “Canada, where yards look better”. Then as they used to say…KB and SRE (kick back and sell real estate) ’til the beavers come home.

1) The first chart : volume have peaked in 2016.

2) Since 2016 : lower highs and lower lows. The trend is down.

3) Prices are beyond peak. Prices didn’t collapse.

4) Look at RE when there will be blood in the street.

5) Don’t expect a V shape recovery, because inflation will reduce

RE real value further down, for many years, probably for a decade, or two.

6) When there is “no more hope” because rent is for free ==> move in.

7) If u are in your 60’s, stay away from RE.

It’s all about location, location, location in Canada. You got your hot cities, your cool cities, bedroom suburbs, your seasonal ocean side homes, your premium vacation/weekend lake/mountain homes. And everything in between. Canada is the second largest country on Earth after all. There’s something for everyone.

It’s all about location, location, location everywhere No?

Resale apartments and resale townhouses in Edmonton, Alberta have fallen on average sixty percent the past thirteen years non-inflation adjusted. Calgary is almost as bad and Fort McMurray is a complete write-off.

What will be interesting over the next few months is what happens to the condo market in Toronto. There are tons of AirBnB condos in TO. People/Investors own multiple AirBnB condos and now they aren’t getting any revenue but have hefty mortgages. Sime people use LOCs for their down payments. Some tske equity out of their primary homes for the down payment.

Also, some people have been carrying condos with negative cash flow because the value of the condos have been going up year over year. Its been a sure bet for a long time. Even through 2008/2009. Lots of people have been putting down payments on pre-construction condos and then assigning them before closing.

There’s alot more I can say (like debt load of individuals) but I think you are getting the picture.

The housing market in Toronto has been resilient for about 20 years. There is a limit. Is this it? Stay tuned….

No because the Canadian government will take a larger stake in new and resale home sales. Presently its ten percent. They’ll increase it to 20 or 25 percent and prices will mainline with zero interest rates.

Good article. It provides a different perspective from MSM and Realestate Agents.

Hi Wolf,

Can you cover south California housing market, and price indexs, too please. Thanks.

Canadian real estate prices make no sense to me.

I’ve been looking to move back to my hometown in Windsor, Ontario, which should be among the cheaper Canadian cities. But looking at wages and looking at home prices, it doesn’t square.