Availability of Jumbo Mortgages Plunges.

By Wolf Richter for WOLF STREET.

That mortgage lending standards have suddenly tightened in just a few weeks – and in some areas drastically, such as jumbo mortgages – has been reported in bits and pieces by boots-on-the-ground mortgage brokers and mortgage bankers. But how loose were those lending standards to begin with, and how did they compare to the lending standards in mid-2006 right before the Housing Bust and Mortgage Crisis, and by how much have those lending standards now tightened?

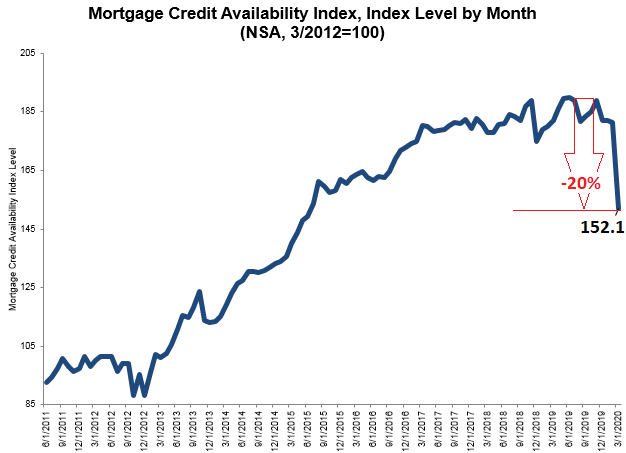

There’s an index for that. The Mortgage Bankers Association’s “Mortgage Credit Availability Index” (MCAI) tracks various aspects of lending standards with an overall index, and with several sub-indices for different types of mortgages. When the MCAI rises, it means lending standards loosen and there is more “mortgage credit availability”; and when it falls, it means lending standards tighten and there is less “mortgage credit availability.” In March, the MCAI plunged by 16.1 points, after having already dropped 21 points over the prior three pre-Covid-19 months:

Chart via Mortgage Bankers Association; powered by Ellie Mae’s AllRegs Market Clarity. Red marks added.

When lending standards tighten, it means that there are fewer mortgages available for certain borrowers and certain types of mortgages. In terms of where the lending standards were tightening, the report pointed specifically at:

- Borrowers with lower credit scores

- Mortgages with higher loan-to-value (LTV) ratios

- Jumbo mortgages – loans with balances over $510,400 in most markets; and in the most expensive markets, with balances over $765,600

- LIBOR-indexed Adjustable Rate Mortgages (ARM), after Fannie Mae and Freddie Mac announced that they would halt purchases of those loans.

- Non-qualified mortgages (non-QM)

For a mortgage to be a QM, the lender has to follow requirements based on the borrower’s Ability-to-Repay (ATR), centered around income, expenses, assets, and debts. These rules came out of the subprime mortgage crisis. In turn, a QM provides the lender some legal protection; and they can more easily sell a QM to Fannie Mae, Freddie Mac, and government entities. But non-QMs are more difficult for lenders to offload, and so lenders are becoming more careful with them.

Key MCAI’s sub-indices.

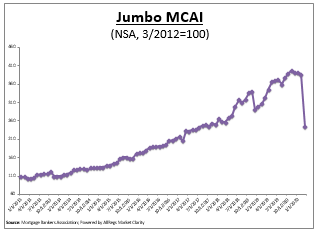

The “Jumbo MCAI,” which covers mortgages with balances that exceed the loan limits from $510,400 to $765,600 depending on the county, and that therefore cannot be sold to the Government Sponsored Enterprises Fannie Mae and Freddie Mac, and that lenders have to deal with on their own, plunged by 36.9% from February to March (all charts below via Mortgage Bankers Association; powered by Ellie Mae’s AllRegs Market Clarity):

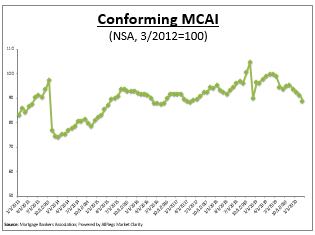

The “Conforming MCAI” covers mortgages that conform to the loan limits ($510,400 to $765,600 depending on the county) and that can therefore be sold to Fannie and Freddie. This index dipped by only 2.7% from February to March but has been declining for months:

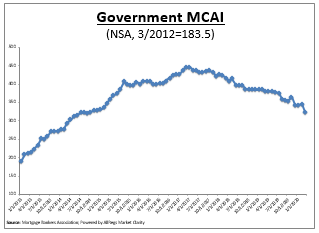

The “Government MCAI,” which tracks mortgages that are backed or insured by government agencies – the FHA, the VA, and the USDA – fell by 6.6% from February to March, the latest step in a process of tightening lending standards that began over two years ago:

The plunging availability of jumbo loans is not a big problem in less expensive housing markets; but it’s a mega-problem in the most expensive markets, such as those on the West Coast and some parts of the East Coast.

It’s going to get much tougher to finance the purchase of a home in many parts of the San Francisco Bay Area, in some sub-markets of Southern California and in the Pacific North West, and in some large markets on the East Coast, such as New York, Boston, and the Washington DC area. Buyers of expensive homes, even if they accept higher interest rates, might have a hard time getting a mortgage. And sellers will have a hard time selling those homes at the price they envision.

But lending standards weren’t that loose to begin with

“To provide historical context” to the current status of lending standards, and how they have loosened in recent years, and then tightened since December, the MBA provides the “expanded historical series” of its MCAI, which covers the housing boom and housing bust that led to the mortgage crisis during the years 2004 through 2010. This stretch of the MCAI is based on six-month intervals (chart via Mortgage Bankers Association; powered by Ellie Mae’s AllRegs Market Clarity):

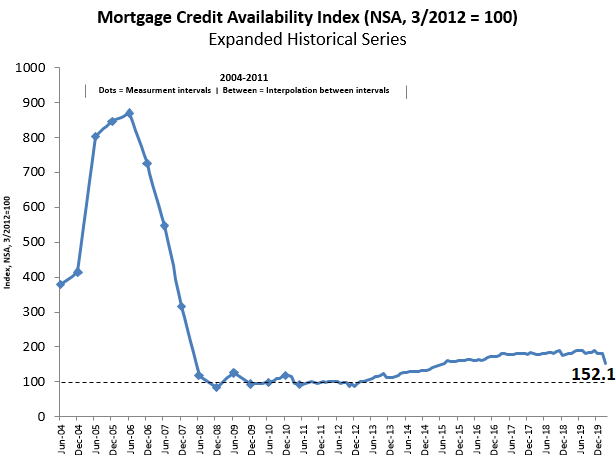

And it shows just how crazy lending standards were in the run-up to the housing bust that started in 2006 – there really weren’t any lending standards as anything would fly. But lending standards were drastically tightened from 2006 through 2008 as mortgage lenders collapsed, and even big banks threatened to collapse, leading to enormous waves of bailouts. Then, from 2009 through 2012, the MCAI remained around the same level for three years of prudent mortgage lending, before it began rising again in 2013.

But in comparison to the pre-2006 years, the loosening of lending standards since 2013 was relatively mild; and in comparison to 2006-2009, the tightening of standards wasn’t nearly that drastic.

This historic perspective shows two things: Just how totally nuts things in the mortgage market were before it began to collapse in mid-2006; and that despite the loosening of lending standards since 2013, lending standards never returned to the craziness of 2005.

But mortgages rarely get in trouble when home prices rise because the borrower who cannot make the payments (due to job loss for example) can often sell the home and pay off the mortgage with the proceeds.

The trouble in mortgage land arises when home prices are falling, as they did during the housing bust. When home prices fall far enough, and a larger portion of mortgages are under water, just as people are losing their jobs and cannot make the payments, that’s when the pain for lenders and investors – and the government entities and quasi-government entities that back them – commences. And the biggest risk in the mortgage market today are the immensely inflated home prices in many markets that face a major reckoning.

“The mortgage market has more risk than previously acknowledged.” Read… “Mortgage Forbearance” is Suddenly Hot, Hits Shadow Banks, which Clamor for Bailout from Taxpayers and the Fed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Conventional mortgage up to $510,000 – there’s a bubble seeking a pin right there.

What would happen to housing market if 15 or 30 year term interest rates went to > 5.5% ? There’s a bubble seeking a pin right there.

What would happen to housing market when property taxes stay same or even rise (e.g. Illinois) in this economy? There’s a bubble right there.

5.5% + is low by historical standards. My first home in 1999 was 8.5% with very high credit score and a decent down payment. We may just be returning to some sane credit standards!

We could not afford to buy a house during the Volker days. Right after he left, we bought our first house. I remember the interest rate fell to above 10%.

volker said that we have to accept a reduction in their living standards, if inflation is to be reduced. they jammed the cpi with the boskin commision thereby fucking old people and future old people, they passed the garn-st.germain bill which set the stage for texas to spread it’s unique brand of corurption and gave us the S&L scandal, which set the stage for repeal of GS.

Their goals have been achieved, finalization of all life is near complete.

Everything is dictated by eps and quarterly earnings and executive compensation. Everything.

GDP grows as profit grows but all profits go to banks/wall street first; they concentrate there and starve the rest.

I have a question: Are there any 2A people on this board? (I dont own a gun)

my question is: what would it take for there to be mass insurrection in this country?

my question is: why are people not out in the streets burning banks down? burning luxry buildings down to the ground? why arent people shitting on beemers and benzes and lambos?

this is the most surprising thing: the fact that for the past 40 years normal people in this country doing it the right way, just trying to live quiet lives, the so called silent majority (no such thing, which is the problem because they have effectively balkanised us via the internet), have been tottaly screwed, killed in wars for the rich, stolen from, dreams, years, lives all transferred to a relatively small group of ratfucking elites,

why are there no riots given that we have now seen 2 major bailouts of the rich in just 10 years while everyone else gets shafted?

there is too much hand-wringing and navel gazing.

is the hesitation or lack of will a function of:

“we got a good thing here (America) let’s not throw out the baby with the bath water and reset the entire thing”?

my question is: when if at all, will there be blood?

does math matter? does mean regression matter?

how much pain will = mass violence

Super-car discounts begin: the most discounted car in the U.S. in April was the Lambo Huracan Evo, with $16,269 OFF the sticker price. Avg sale price was $248k.

any discounts on toyota camary or honda civic?

IamJ,

Ain’t gonna happen in any major way, if for no other reason than reason able people know who has the fire power, and it ”ain’t” We the People…

Look carefully at the videos of the fire power just in the black SUVs following the pres tank,,, a serious ‘curtain’ of lead, they fire something like several thousand rounds a minute…

No way Jose used to me a common reply to absurdity,, etc., etc.

The other, and main reason IMO, is that violence begats more violence, and nobody actually wins anything in the long run.

America has persisted on the basis of rule of law, and that is what must change: there are several legal and doable methods of serious change imbedded in our constitution for that very reason, and yes, it is time for serious change, and yes, the oligarchs and the other rich folks need to step up and make that change happen soon,,,ASAP.

I am John’s Trigger Finger,

No dice. Although some projectiles will be useful for the odd assailant. An armed uprising against drones and Apache gunships is a silly as it sounds.

The time to buy is when interest rates peak. I bought two homes for cash back in December 1982. That rule has never changed over the years.

But the prices of the houses were not comparable to today’s housing market, correct?

Also, back in the early ’80’s rates were in the teens and everyone had to pay 3 points to get that rate. I agree with Stephen, things are gtting closer to normal lending standards and not what we have seen the last 20 years.

@Shiloh1

Why would rates stop at 5.5%? That’s still a shockingly low rate of interest.

People are in deep denial of the corruption of the currency and rate markets. USD Rates could be anything in the future. This means home market values could go to zero or even negative.

How about.

20% down.

The taxpayers don’t guarantee any mortgages. None.

Banks eat their bad loans.

Enforcement of GAAP and fraud loans.

Bankers go to jail for not following GAAP and fraud laws.

I know, I know, hard to buy votes that way.

that’s crazy talk!

It’s worse than that, it’s downright UnAmerican!

C

He’s a communist.

A blood hungry communist, I tell you.

Chase just announced that they will not lend to you unless you have a 700 score and 20% down.

I like it You got my vote banana

The issue is that, particularly for the low or moderate-income community, 20% down is not achievable in a market in which the cost of housing, whether to rent or to own, rises faster than wages. Between 2010 and 2020, the average cost of a home in most of the US doubled or more. Rents went up 25-50% on average. During that same time, income rose a total of about 10%. It was still cheaper to pay a mortgage, including taxes, insurance and mortgage insurance, than it was to pay rent though, at least in most markets. If the availability of home loans were restricted to only those who put 20% or more down, you would have a large number of renters and very few owners. Owning a home, by the way, is one of the few ways that a moderate-income person can actually build wealth, both in the reduction of their loan balance over time and in the appreciation of the property itself.

Fewer buyers –> lower demand –> lower prices –> more buyers who pay a lower price.

In reality 20% down would lead to much lower prices, lower rents and more people who owned their own home. But banks would make less profit.

Banks still lend aggressively to low to moderate income since they are supported by the government through community reinvestment. Also, owning a home is not a right, but rather a privilege.

@Mike S

“Owning a home, by the way, is one of the few ways that a moderate-income person can actually build wealth, both in the reduction of their loan balance over time and in the appreciation of the property itself.”

Here’s the correction:

“Owning a home is one of the fastest ways a moderate income person can impoverish themselves, by excessive mortgage payments and perpetual bank friendly refinancing that leaves nothing to replenish the depreciating elements of the structure, leaving them in their old age with a dilapidated, moldy house to suffer in until they die”

I don’t think you understand what that would do to the market nor do I think you want to endure what it would do…. 20% down? why? I currently own 22 houses and have never put that much down, even the investment/rental homes. It is a bad idea. Risk on the lending side can be mitigated w/o funds like that being put down. I will save the rest.

You are right. It would be bad. 20% down would lead to house prices of 3x income instead of 5x income. A 40% drop. Assuming that you have a 80% mortgage on the 22 homes you own you would end up with owning 22 homes and having a mortgage for 27 1/3 homes. That would be really bad.But capitalism and such would say suck it up.

Why are you a part of this conversation…. to brag about your 22 homes or to brag about how you secured them with less money down….

You are an investor!!! This conversation is about the ability/inability of HOME ownership; as in primary residence….

Couldn’t agree with you more. Very well said.

Bankers are not going to bribe their pet congress critter to get that kind of a world!

5.5% is only likely to happen if inflation also goes up. First few years it depresses prices but than inflation will catch up and prices will rise. In reality prices probably wont drop housing prices are really sticky

Unless people with margin calls sell their bonds.

Or if the low price of oil reduces the petrodollars returning to the Fed to buy bonds.

5.5% with 0% inflation is not durable.

People told me the same thing in 2008 2009 that this time is different and

Southern California is special

I agree real estate prices cant go down and this time is indeed different

Down versus what Federal Reserve Notes I might agree but in gold terms I believe it will go down quite a bit

Good, can’t wait to see this hopefully will put downward pressure on some insane market like SoCal and SF. When you’re asking for $600k for a crappy condo in Culver City or $1M for a craphole in Venice Beach you know this is just insanity fueled by FOMO.

Real estate is a slow turning ship but jury is still out if price will tank in a long run, my hope is if these market can adjust down 20% maybe that’s the best one can hope for.

Sticky Uhh not really from what I’m seeing o sites such as Zillow Serious sellers are starting to get real nervous I think

I am seeing that on Zillow as well. Also, turnover rate in markets are slowing, inventory on hand increasing. Housing prices can and do fall significantly. Everything got way out of hand. Spec builders lost their minds building gilded shit homes and asking 300-400 per ft. Virus or no virus, excessive debt leads to deflation. I will be looking to buy a mcmansion when they hit $50/ft soon and sellers are crying in the streets begging people to take them off their hands.

“What would happen to housing market when property taxes stay same or even rise (e.g. Illinois) in this economy?

either property taxes go up or pensions fail. it’s that simple.

@yossarian – Sadly, some places will have both rising taxes and failing pensions. Politicians forget that people can move to avoid paying outrageous tax rates, and property values will fall as well if tax payments rise. The actual tax collected suffers from the usual Laffer Curve effects.

Move where ? There is a depression on. Laffer curve completely discredited. USA style Capitalism in death throes. Witness Trump-and Republicans- out maneuvering Democrats from the left. General strike and massive civil disobedience inevitable.

Well Stuart some are actually moving south across the border as there’s nothing there to stop them YET

@stuart

Laffer curve NOT completely discredited, top marginal tax rates fell from near 90% to near 30% from 1960 to 1980s and federal tax collections as a percentage of GDP declined only slightly. There is an optimal point on that curve for tax collection and economic growth. That’s not to say tax cuts “pay for themselves”, that is clearly propaganda, but some taxes clearly don’t pay for themselves because they cause economic growth to lag, or cause massive tax evasion. See the underground economy in Italy as an example.

And relative to IL, NJ, NY, and CT, there are many lower tax states from both income and property tax standpoints, there is very clear migration from those states to low tax states. This is a solid strategy for anyone living in high tax states and those migration paths are well paved by millions.

From 90% to 80% maybe not but the Laffer curve is completely discredited from 60% to 30%. And 90% was never the effective tax rate. There is also the question if you do want to have high incomes. More equal societies seem to function much better. Even for the top*.

*outside hereditary effects.

You think rising property taxes in IL and NJ will keep pensions solvent in those states? They will do nothing of the sort. People are moving to lower tax states. IL and NJ will eventually default on pension obligations. This is an inevitability, especially in IL.

I agree to building wealth but 20% down is becoming difficult for middle-modern income when your income is taken up in health care and the price of a homes has reached at Million dollars in California for the size of hotel room. Can we say “Capitalism”!

These financial conditions were inevitable. They were going to affect the most expensive real estate first. The expensive homes of the baby boomers were not going to be able to continue appreciating when the later generations were suffering so much.

The bubbles have not all popped yet. They will. Brace yourselves. This virus cannot be easily eliminated. It was predicable and foreseen.

Many states were late in closing or are not closed down or have major exceptions to lock downs, such as religious gatherings. Therefore, sadly, many will get infected while seeking to pray.

Reportedly, the CDC does not have enough staff. It and other agencies cannot do the necessary contact tracing even in states with few infections, as could the well funded single payer health care agencies in other countries. Testing is also not sufficient.

Negative feelings toward others in the US have made many oppose efforts to provide them with health care for too long. Thus, we were not prepared.

Countries with fewer minority populations have ensured proper health care and other assistance to their less wealthy. Our country’s unfortunate traditions of discrimination and disdain for the poor will keep this virus feeding on our population for a long time.

I predict that our economy will slowly collapse more and more. If attempts are made to open it up in May 1 or June 1, without measures to address the reservoirs of virus infections among the unfortunates, the virus infections will only explode again and even force more lock downs.

This reminds me of President Lincoln’s second inaugural speech: that God may will that the war continue “until every drop of blood drawn with the lash shall be paid by another drawn with the sword”, and that the war was the country’s “woe due”.

My heart is heavy for my country. While I studied science and drifted away from what I learned in childhood, I know that you can guess whose just wrath I believe in my heart we have incurred.

A few questions:

Are the changing standards simply a reaction to the falling price trend, or are there new directives which lending companies must now be in compliance?

Plus, who changes the standards? Is there a ‘rule of thumb ratio’ that loans officers now look at? In short, who decides, the mortgage company boss, or those writing them up?

The prices have not fallen but there is an unbelievable amount of uncertainty. For the mortgage companies it is also not important if prices fall but if the houses still sell. The mortgage company makes the biggest losses when the owner can’t sell the homes themself, not when the market drops the most. If a mortgage company is forced to sell a house than extra costs are something like 20% of the market price, or more.

Mortgage companies fear that the housing market locks up because of Covid. I doubt that there are many who claim that they are wrong

Jumbo loans are decided by individual lenders, and those lenders on average are tightening up their lending standards on jumbo loans.

Thanks, Char and Wolf.

Rates will stay low for the next 2 years because when the economy sucks rates go down. When a recession comes rates go down. There is so much demand for housing this will weed out many buyers who can’t pay the higher prices. With mellenials now getting married and having kids it’s irresp9nsible to rent for the next 30 years. The new buyers are coming and there is no way to stop it.

Yeah, next month we’re going to have 25% unemployment. Great time to buy a home for the unemployed.

But the economy wasn’t all that fantastic in the late 70s because of inflation and yet Volcker raised rates very significantly

In a recession rates go up*)**)

*) They go up for those that really need the money. The rates for AAA goes down, The rates for BBB goes up and the rates for BB’s that where single A’s a year ago are really going up. And this is especially true in a very low interest environment.

**) nominal, in inflation corrected it is even worse.

I’ll bet that rates; maybe not the “friends of the FED”-rates, but the rates available for everyone else, will in fact go up. Significantly.

Because default risks / risks of never seeing the money are going up in circumstances where both borrowers / lenders (investors) can die or be in quarantine.

On top of that, lenders will force the borrowers to take out loss-of-income and life insurances on a mortgage.

This will be quite a show: Dow goes to 150000 while everyone goes bankrupt!

But most people will in the end be ok because nobody will be in a hurry to collect the collateral: Lenders will not want a lot of price-discovery on their books.

For some property they will even recruit the “owners” as caretakers.

People don’t buy homes in a depression.

People do buy homes in a depression… they just don’t use mortgages to do so.

In 2008, condos in the Bay Area could be picked up for $40K or less.

A friend of mine bought a condo in Sacramento (near Arden Arcade) for $7,500. As in seven thousand, five hundred dollars.

He lived in it for four years and now rents it put for $1,200 a month.

Plenty of houses will sell. For pennies on the dollar to savers who can shell out cash to buy them.

Yes yes yes, this article is spot on and exactly what I’ve been saying for months (years actually).

Loan quality/Underwriting standards of today are of no comparison to what they used to be circa 2004-2006.

Case in point:

A refinance client referral I picked up a couple days ago. We will be consolidating a 1st and 2nd, both of which were modified. Nice monthly savings for the client.

After investigation I realize this person bought in 2005, with an 80/20 loan (0 down), 1st mortgage was a neg am (negative amortization) and 2nd adjustable. Stated income (no income verification).

So, after modification and 15yrs, these people have pretty much not paid off any of the original principal. Think about the loan program they went with compared to today….. Ya, no comparison whatsoever.

Broker Dan,

So this person has made mortgage payments for 15 years, and has no equity built up?

That hurts my brain to think of being in their shoes. They basically rented with a bit of a tax break from the mortgage deduction the IRS gives.

If the Fed prints enough money maybe this “owner” can catch a future wave. Optionality.

@Romig,

Yes. Neg Am loans were popular bc once could get a property and have a payment LESS than the interest only payment. The difference monthly would tack on the balance and therefore the principal would INCREASE every month.

Anyways, just one example of how ridiculous it is to compare FHA and Conventional guidelines today to the early 2000s.

The problem today is not fraudulent loans, it is overvalued real estate. Prices are simply too high for incomes. We are in for some serious price adjustments..

Actually this is great. It’s about time we go back to Financial Soundness.

It starts at home.

Yeah I think there are too many people milking the thing, the system was never meant to function as an ATM or provide a tax breaks. ( I guess some people have kids for the same reason.) They should cap mortgage “benefits” at twenty years or something.

Iamafan.

Amen brotha! A Return to Thrift. But, just look at those conforming mortgage limits. That is (or was) a lot of money!

Debt destruction and capital destruction enable new credit creation. For want of a better analogy, the market collapse and the impending credit crisis create a hole that can be filled with new government and Fed largess. It’s creative destruction aka a reset.

Deflation is a beneficial outcome for money printers. It props up a currency when it otherwise would have devalued. It also provides great asset buying opportunities.

There are so, so many speculative apartment buildings out there. Good deals have got to be on the horizon.

We are at an inflection point in history. We are going from Highway Suburbia to Renewable Amazonia. Positive market survive such a switch relatively well. Parts of the Market that are down can be killed in such a situation. You need good knowledge and luck in this market, unlike previous markets were almost everything was successfull.

This effectively acts like a tightening of the money supply. Any time the credit markets dry up everything contracts, because credit is what ballooned demand in the first place. Above sustainable amount? Exactly, hence a bubble looking for a pin. We got a pin, and now there will be deflation.

The Fed’s blowout won’t change that in the short-term. If you can get a mortgage in the next couple years though and then the fed’s tidal wave comes roaring through as credit re-expands (step in step with labor market), heck you might end up with a cheap mortgage payment as your bank watches shrinking dollars fall through their hands. This is all highly subject to speculation though of course.

Gammon and Schiff agree. So would any oldsters who had 15 year fixed rate mortgages written in mid 60s to early 70s before inflation started roaring.

That’s what I’m thinking. Wait for cash to be coronated as king. There are always business cycles, especially in real estate. They are just splayed out and extended now with financial engineering.

The end game is some type of flation, Stag or hyper. I’m on the side of eventual stagflation though I can’t say when.

I think it will be sudden. The stock financial markets are the canary in the coal mine. Therein lies the signal for stagflation… but where is the green light to buy at all costs?

Gold is King and everybody knows that No fiat currency will ever hold a candle to Gold That much is for sure

Gold is king so long as the government neglects to confiscate it.

I agree completely. Cash will be king. Those with cash will be able to buy homes for pennies on (today’s) dollar.

Question: Are techies still going to be able to monetize those otherwise illiquid employee stock options? That script was a great way to come up with the down payment…

Over-compensates tech employee here.

I saw this coming a mile away and left an employee-stock-option job to take a 100% cas job in 2017. I can confirm I’m the only person in my entire network that thinks this way and everyone else is blinded by unicorn fairydust that their ESOs make them a millionaire already.

It’s a huge “wealth effect” bubble that’s going to pop when lots of people in their late 30s to mid 40s wake up to the fact they aren’t as rich as they thought they were, they can’t afford to pay that house with their evaporates ESOs, and they’re a lot further away from a safe&secure retirement than they thought with less time on the clock to save for it.

You don’t have to take a 100% cash job to manage that risk. Another way is to simply sell all of your stock options as they vest. The RSU’s are nothing but an additional yearly bonus anyway. The prevailing wisdom on those says sell them as they vest because they’ve already been taxed by the time you receive them, unlike ESPP’s.

But your point is taken. If you’ve been sitting on AAPL stock or TSLA stock because it was going to a bazillion soon (because stock market always goes up!), you’re in for a surprise.

Options that are under water are worthless. Options in a defunct company are also worthless. There’s some of that going on.

Let me tell ya, every.single.homeowner in SF believes the startup millionaire pipeline will always be there to pay top dollar. That’s how you justify 7 turns of leverage.

When they lose faith in that illusion, watch out! Rapidly falling prices on highly leveraged assets is a hell of an inducement to sell.

Wife works for WeWork

Soon to be worthless options

uhhhh…how are they worth anything now?

Setting startups aside, in established tech companies stock compensation is widely given as RSUs [restricted stock units], which are grants, not options.

Indeed, and I think it’s because there’s some law; when you’re offered stock at one of these companies, they ask you to select whether you want them as options or RSUs. Of course, the correct answer is, RSU, since your money without having to worry about a strike price. Of course, if the stock tanks you get less money, but that’s a lot better than zero for an underwater option.

I saw a rumor Wells Fargo wants 20% down and a credit score of 700 for a new mortgage.

Unemployed workers maxing out credit cards and missing payments does not qualify them for the most favorable terms.

Real estate is overpriced. Some people hoarded homes and lots trying to corner the market.

JPM is doing so

“From Tuesday, customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value.”

https://www.cnbc.com/amp/2020/04/11/jpmorgan-chase-to-raise-mortgage-borrowing-standards-as-economic-outlook-darkens.html

Why anyone would get a mortgage with one of the big banks is beyond me. Wells Fargo, Chase, Citi, Bank of America… After the financial crisis, anyone who is dumb enough do business with them will get exactly what they deserve.

Oh the horror! Lending to people who can actually repay their loans.

House flippers, speculators, greater fools, etc: This is how capitalism really works. I used to think lenders and bond buyers were the smart money but they caved to greed and oh happy day the Fed is buying up their garbage.

Lenders who were not cautious about loan requirements, this is what you get. You don’t deserve to survive but the Fed will backstop your greed-driven foolishness by buying your crap.

My advice if you’re underwater and can’t pay your monthly tithe to the bank: short sale.

Let the weak and the imprudent suffer the consequences.

Like a forest fire you have to let the dead wood burn and the Fed hasn’t done that. Hello Japan and zombie companies.

Google “The depression you’ve never heard of”. Yes, huge crater in 1920-21 resolved quickly by letting the chips fall where they may.

OMG I’m starting to sound like an Old Testament prophet. “And their yachts will sink and all their kine (whatever that is) shall perish. And the land will be covered in sackcloth and ashes and Many Other Bad Things Will Happen”. So saith whatever higher power you believe in.

Wise advise. Problem is nothing moves

If you compensate for wage inflation and lower interest rates on the actual monthly cost of a mortgage, houses only appear to be overvalued in some heavily bought up markets by 20% or so over long-run trends (not the most extreme cases mind you). Of course prices can also dip below the long-run wage inflation trend. A lot of hot markets could drop 30-40% over the next few years. However, that depends on a lot of things, not least of all govt policies. However, for the time being, these bank policies on top of skyrocketing unemployment should drop housing markets quite a bit.

Wolf,

As an owner of one of your beer mugs, there is something that goes to Heck in a Straight Line, —– the Chinese Virus!!

Nick Walker

Its amusing in a “dark humor way” that right after Wolf got one of his soundest short insights into society and the economy widely printed, the economy responded with a “Oh Yah? I’ll show you, I can do strait lines if I want!”

LOL.

If it just weren’t so terribly serious. Those straight lines to heck are truly scary.

According to sifma, till the end of 2019, here is the US bond market outstanding:

(in billions)

Total: 45,129.9

Treasury 16,673.3

Mortgage Related* 10,333.6

Corporate Debt 9,597.8

Municipal 3,854.5

Federal Agency Securities 1,825.9

Asset-Backed* 1,799.6

Money Markets 1,045.2

Tell me we’re not going to default after the coronavirus.

I believe we haven’t even seen the start of the debt crisis.

oh and please don’t give me the cleanest dirty shirt argument.

Ok, so what currency does the dollar holder go to?

This is a US bond market (not included is the US Loan market).

Obviously, its in our local currency, US Dollars.

The problem is that there is a creditor and a debtor (even if the currency is the same).

Simply stated, when the borrower cannot pay (despite the low interest), S**t happens.

Because the main street economy shut down, then we can expect problems.

I am not recommending an American living in the USA save in another currency other than the USD. I am recommending, though, everyone stays LIQUID.

Sooner or later, the smoke and mirrors will turn into hot air and broken windows.

Dealing in any other currency is a speculation.

Whether lending or borrowing, you could be ruined by exchange rates, even if the interest rate is attractive.

If you do do well, you’ve been lucky!

Other than that, some percentage in gold bullion coins of low denomination like US Eagles with no collector premium, just the small bid-ask spread. ‘Junk’ silver pre-1966 coins, at today’s prices also good. And store it where you can touch it, not under someone else’s lock and key – if they even have it. Even allocated storage is suspect, and unallocated storage just means you’re an unsecured creditor, even if it’s a bank.

Collector coins, while attractive, are speculative and not fungible. Like art. Also like art, beware of fakes!

Gold bullion is speculation and meant only for your great grandchildren should things go badly. Dollars are speculation as no one knows what the purchasing power will be in the future. Best invest in fishhooks and tools that can keep a sharp edge. Perhaps metal containers with a screw-on cover. Implements for hand farming. OMG what have we come to.

Gold seems like a good idea

That’s a nice housing bubble you’ve got there.

It’d be a shame if someone popped it.

Have you *looked* at the coronavirus man? It’s got an outer shell that’s very prickly! You know what happens when prickly things get close to bubbles…

CA home sales volume has been about 60% of peak bubble volume in the decade plus since the bubble.

https://journal.firsttuesday.us/home-sales-volume-and-price-peaks/692/

(Chart 3)

To me, that made for brittle peak pricing today – even before C19 has shut everything down.

Current peak prices were propped up by a small sub-population of price insensitive buyers.

First guess – First Tuesday will show a huge sales volume collapse for March. That rpt will be out in about 3.5 weeks.

Next guess, following 2 or 3 months after volume collapse, CA median prices will start a long rapid decline.

CA has been a home valuation/affordability basket case for as long as ZIRP has enabled it to be (and, actually, well before that).

Hey if things get really bad there’s always Slab City

Who needs or wants a McMansion now? Got a feeling times are a changing.

We’re all frugal now.

Amen to that and I got a witness. My 1400 sq ft(full basement) hovel , paid for decades ago. There’s a whole lot of 3500 sq ft mc mansions between me and the nightly news hero pensions that government has awarded themselves . Collapse this debt ridden bitch.

I sure would. Makes lockdown much more comfortable to wander around in an oversized home in a nice neighborhood! Always assuming your job sticks around, of course.

Depends on your personality I suppose but in this environment I would prefer a little two bedroom cottage near the sea with a nice acre or so of tillable land for a veggie patch and some chickens instead

I have one For Sale in Small Town North Central Florida USA LOL!

They can repurpose those things, if city planners amend zoning laws, turn them into rooming houses. We already have in place zoning laws which allow the owner to repurpose into six bed healthcare facilities. Post 2008 when a McM went into foreclosure they referred it to section 8, and moved in HUD people – and yes it was used for the dubious purpose of racially integrating wealthy white suburbs – We are lots poorer now. You would be amazed at the size of the room to rent market in SoCa. Sq foot wise there is plenty of supply, albeit a lot of it is in exurbia, but without a job, the commute is not a concern.

I’m of two minds on these big houses.

I’ve always thought that during a time of global climate change, nobody will want to heat or cool a 3,000 square foot house.

During this pandemic, rather once its over, I believe we will see more telecommuting, which will encourage people to go further out and get that big house in the burbs.

And the 2700 plus square foot place will seem less decadent as houses literally become classrooms, and multiple offices for two different business as well as dwelling for a family of 4 with two incomes… hypothetically.

Time will tell.

Did wealthy property owners slip thru a crack the Fed missed in it’s 24/7 scrabble to bailout every rich person on Earth? Granted anyone who has to borrow money it’s truly worthy of limitless Fed bailouts, but really how careless. Fed better fix this.

Unfortunately real estate markets depend on people actually buying… real estate. And right now the market for real estate worldwide outside prime areas of China simply doesn’t exist anymore.

Americans are still in the early phases of the lockdown and their spirits are still high, so they are still thinking ahead and about the future. But give them a few more weeks and no hope of ever leaving the house again and they’ll become like the Italians: broken, disheartened and hopeless.

If by accident the US ever allows people out of the house expect a repetition of what we are seeing right now in Wuhan. People will just have two priorities: getting back to work as quickly as possible and getting out of Dodge, quite literally.

Since the airport and the train stations have been reopened people are scrambling to leave Wuhan, most likely for good. All attempts to stem the flood have so far been useless and people are terrified a couple new cases (perfectly possible) is all it will take for Chinese authorities to shut down the city once again. They’d rather take their chances elsewhere.

In spite of China’s near-legendary love of real estate there have been zero RE deals signed in Wuhan (a city of 11 million) since the city was shut down in January. That’s the future we are looking forward to.

I’ve been following the market in Palo Alto, CA for 2 years and I’ve seen very few listings the last few weeks. So I am not sure the mortgage availability is the issue right now but rather that people aren’t listing their houses. We still can’t have open houses in CA so it does make sense to hold off from that perspective. I think the question is going to be are people going to hold off on listing their houses or will there be a rush to get them listed and then a dearth of buyers (in part due to job losses, ipo losses, general uncertainty and the mortgage tightened from this article) which will cause prices to final drop (they have been dropping a little but are still far inflated from 2008).

Yeah, I have been following the peninsula real estate market as well. Especially Palo Alto. My husband and I make a lot of money, but we really can’t afford to buy something for much more than $2.3 million. We are still pretty secure in our jobs, and I in fact got a new job offer, but we certainly do not have a 20% down for that kind of a mortgage, plus most things here require quite a bit of work. And we would really like to have 4+ bedrooms for our decently large family. I don’t yet see any kind of movement in that price range.

Good luck, but PA has to be one of the more expensive places to buy a house… unless you are talking East PA, which is not viable. I would suggest further up the peninsula if possible.

Even at 20%, a mortgage on a $2M is going to be challenging.

We are a family of four feeling guilty with schadenfreude as we look to break into the SF Bay Area market. The all-cash overseas buyer may not gamble on catching the falling real estate knife here, but other desperate buyers are betting the post C19 housing recovery is swift. Not me, we are on the sidelines until at least fall 2020.

Home sellers have massively pulled their homes off the market. There is no reason to have them listed. Right now, everything is hung up. That’s why inventories are low. But there are also very few buyers. And in Palo Alto, nearly all mortgages would be jumbo. And lenders are leery of those now. So even if there is a buyer and a seller and a meeting of the minds, the buyer might not find a lender willing to lend.

I’m in the East Bay (just outside of San Francisco), and within just a few weeks, I’ve noticed 1/2 a dozen homes that are “back on the market”. I’ve been following this market for the last 5 years, and I rarely come across this status. One can speculate why – one partner loses a job, the down payment (in stocks) has fallen in value, and perhaps the buyer no longer qualifies for the loan.

Same thing in much more affordable ($200/SF for livable houses) neighborhood in tpa bay area that i ride my bike around as often as I can manage,,, All homes for sale were gone by late fall 19, with new owners mostly moved in, a few with new ”build to suit” signs in front.

New signs popping up the last several weeks, now about a dozen new ones; looked one up with bil Sat evening, it was already reduced in asking price after on the market for 6 or 7 days!!

Remembering last time, some properties went to half within months, some went to pre-bubble prices within a year,,, but most good ones jumped right back up very quickly, especially the ocean front condos, shells or finished, in SRQ area.

If in the market, ya really gotta pay very close attention, that’s for sure!!

The Chinese buyer paying all cash gone? Buying a vastly overpriced home in Palo Alto a bad bad move. $2-3k Per MONTH Property tax in a city with a massively underfunded Pension obligation to the tune of $455,000,000 as of Sept ‘19. Midtown homes doubled in price since ‘10. Area with original ‘mid fifties 1500 sqft tract houses mixed with McMansions covering every inch of the lot. Likely increasing risk of flooding depending on accuracy of sea level rise forecasts. I would not want to be the greater fool.

Great comment about Palo Alto’s pension obligations. Owning a house costs you, mortgage payments, property taxes, proper management services, repairs etc. And a lot of people in the SF bay area don’t just have one of these, they have several. We are only 4 weeks into the US side of this pandemic, prices will fall as a results. I wonder what the playbook says when people can no longer pay for anything of things I mentioned above.

Mr. Richter, it sounds like there may be some third party price discovery happening now.

Would it be a bad time to look into a streamline option on an FHA mortgage

I agree, Josh!

Real Estate has always been a tough bus.Those that tend

to survive are not highly leveraged and rent nice apts. to lower middle

class tenants.

Today those owners will be able to help their

tenants though this and longer term will be rewarded.They will sell

their units close to retirement and live the dream.

I suppose jumbo loans are constrained because all the huge lenders are going to be skittish about discretionary lending since they’re going through the wringer themselves. They have had their liquidity sucked dry by corporations draining revolvers for crisis survival cash. They are also potentially doomed themselves depending on how the bond market bailout Calvinball plays out.

The easy fix is for the Fannie/Freddie limits to be increased a bit on a temporary basis. But in the meantime it’ll be tricky.

Note also that the Asian capital-flight cash buyers can’t easily come over to shop this spring.

This is part of the reason but not the main one.

Homes are an expensive investment for everybody except Bill Gates. During periods of uncertainty people stop investing in things that they don’t need to buy. Jumbo mortgage homes are by definition things people don’t need because they could also buy a medium mortgage home to provide a roof over their head. The Market for expensive homes seizure up and selling a jumbo home becomes impossible. Now some persons will claim that you could lower the price and sell it but that is not how markets work. If you sell something significant below market price* than you are calling out a lemon and buyers who look at property with “Is this a lemon” will find in their eyes the proof that it is indeed a lemon and as such not a bargain.

*some people will claim that the price something sells at is the market price. This is wrong. Short, but not totally correct answer is that market price is the price the sellers makes the most profit. In the case of homes this includes the costs of carrying a home, the expected future price and the probability of selling a house at each price point.

Banks lend you money they do not have but expect you to have it. Nice.

Well CtP, I can remember fall of 66, when I went to get my first ever bank loan, short term to pay my college tuition temporarily until not liquid enough assets were cashed in; not only did I have to prove how I was going to repay the loan, I also had to prove that I absolutely did not need the loan in the first place…

Cuz had to co-sign eventually, which he did laughing because I was so naive as to think banks loan money cause you need it!

My oldest CA friend, 92, has one savings account, no credit cards, does biz only in cash, and a lot of it. I wish I could duplicate that, but I eventually found out she does use her daughter’s card when cash does not work, as is more and more common these days.

So, like the old Diodude going around with the lantern looking for an honest person, I keep looking for an honest bank,,, maybe someday, like over the rainbow or something like that.

Pay by phone linked to bank debit card is not bad for food shopping in a decent store. My ATM card (does debit) and has that RF thing so I can just pay without touching.

It is not a good idea to use a debit card online!

In case of card fraud, getting reimbursed is a complex process and relies on the mercy of the card issuer. With a credit card, one can just refuse the fraudulent charges and get a new card.

There are no penalties for paying off credit cards in full every month, rather the opposite.

@fajensen

It is not a good idea to use a debit card online in a country that is third world online

The only honest banks charge exorbitantly high interest and are subject to RICO investigation.

1) Jumbo MCAI plunge is the largest on the chart.

2) Mortgage Credit Availability Index : there are x5 dots on the chart

between the 2006 top and 2008 bottom.

3) The widest plunge is in the middle, between #2 and #3. The space between #3 to #4 is already shorter.

4) At the bottom, between #4 and #5, there is shortening of the thrust.

5) For 12Y this chart pulse is hardly alive. It might be saved by gov ventilator.

6) Its resting in accumulation. It need a springboard. Thereafter it will jump, perhaps > 900.

7) Feb/ Mar Nasdaq plunge is the largest on the chart.

8) The Nasdaq Mar 2020 low @ 6631.42 was higher than Dec 2018(L) @ 6190.17 and Feb 2018(L) @ 6630.67 support line. Its positive.

9) A positive option : the Nasdaq will jump to 12K // and SPX > 3,600.

10) A negative option : volatility is still on. The markets must relax. There was a huge down thrust that must fade first

11) Wave C lower, including 3/of 3/of C , will shorten the thrust, because C is equal to : (0.8 to 1.25) of A.

12) That bottom will be a springboard. Things will jump including

jumbo loan.

13) There are more options…

How the Treasury is Financing the Coronavirus Stimulus

The Fed can QE all it wants but the Treasury has to raise NEW MONEY to spend.

The money is mainly coming from Cash Management Bills.

Since March 19th (up to April 14th) about $745 billion will already be auctioned.

Cash Management Bills have durations from 39 days to 154 days.

This means that they will mature anywhere from May to Sept.

In other words, they will have to be paid back soon.

In addition, T bill auction (sold weekly) sizes have dramatically increased.

From the week of March 19th to the latest week;

4 week bill increased from $50b to $90b.

8 week bill increased from $40b to $70b.

13 week bill increased from $42b to $57b.

26 week bill increased from $37b to $48b.

These short-term T bills have a maturity problem – they have to be redeemed shortly.

In order to get new money from T bills auctions, the size has to grow above the amount being redeemed. Therefore, the auction amounts tend to grow geometrically.

If you don’t think debt will kill us, think again.

And once yield goes negative, the mob will.

Jumbo mortgages have been difficult to get for more than 10 years. Making them a little more difficult to get changes nothing.

Central banks stepped up and purchased securities just to avoid impared assets on bank balance sheets. As long as the bank balance sheets do not land up with impaired assets, then there is no credit crunch, and no major problem.

>> As long as the bank balance sheets do not land up with impaired assets<<

Banks and credit unions always lie about impaired assets unless their regulators come along and force them to tell the truth. But the regulators function was compromised long ago. So I go forward believing any bank's balance sheet is just a work of fiction.

Difficult for people without a down payment. I has zero problem getting such a mortgage in 2010. But I had cash.

How could bank balance sheets not end up with impaired assets when we are about to see the biggest default rate since 1929?

Well, that escalated up the wealth chain quickly!

The jumbo applicants or re-fi applicants are going to find the new ATR and terms quite hard to swallow, shocking even, not that they’re going to get the pitchforks and torches out, but as the old Bagehot dictum says “When a man has to plead for his creditworthiness, it is already gone”.

The banks are in this case a leading indicator of the real economy. They are telling the jumbo end of the market “you think you’re sound, employed, solidly valued, and have a range of hedges. But you ain’t. You’re a NINJA in waiting, an OptionARM to be, a candidate for FICO collapse, so close to jingle mail you have UPS on speeddial. And you ain’t gettin our money.”

There is (now) no pressing problem at the wholesale or funding end of the mortgage market, bank liquidity is fine, solvency is a problem but one for another day. This is about retail banking and the signal is ominous.

I’m just disappointed we can’t watch Bank-Implode to track this like last time. It’s far more distributed, insidious, and ultimately damaging.

C

In the Gotham city, no body can figure out Bruce Wayne is Batman. Majority of the people do not know whats going on. We think there will be no one to buy the houses and prices will fall. Poor us!

Big wall street companies will come and purchase the homes. They have freshly printed money and zero interest rates. They will hold these houses, make it look like there is acute shortages of homes, build more, sell among themselves, create fake price increase and be the last one standing. Even if the next generation become all renters or worse homeless, they will sell to Uncle Sam and finally, then the wealth will trickle down.

That’s what I fear may happen, is part of the plan. I’m calling it the second phase of this Covid crisis. Wall Street got is bailouts and this time a administratively forever basis….next phase is turning the vast majority of home owners into renters.

REIT have zero interest in “hoarding” properties to drive prices up: in fact they have every interest in leasing them out as quickly and expensively as possible to maximize their cashflow.

They have zero need to artificially drive prices up (and hence their own asset value) because the media and retail investors will do the job for them and for free: remember that as Robert Shiller said the real estate market is sentiment, not fundamentals, driven.

Right now there’s no sentiment in the real estate market, for the simple reason people right now there’s no real estate market, like there is no car or travel market.

Nobody has a clue on what the real estate market will look like in the near future, but the West has to look more to Wuhan than to China as a whole for the damages caused by the lockdown. And if that’s the case it isn’t pretty: real estate is as far removed from people’s minds as possible.

The two top priorities right now seem to be getting back to work (most factories and offices started re-opening in increasing shifts and will be back to full speed this week or the next) and, much more critical, getting out of Wuhan. China Railway and domestic airlines are struggling to cope with the flow of people trying to get out of Wuhan in spite of the frantic, and ultimately unsuccessful, attempts to somehow limit movements after promises to the contrary: many won’t come back.

It’s well possible the West will look similar: people may consider moving to places where lockdowns are perceived as having been handled better by local authorities. Countries (and US States) were lockdowns were extended time and time again are likely to see a steady flow of people trying to get as far away as they can.

But this is still far in the future, of course if we are allowed out.

Ya, the Fed and the oligarchs and plutocrats that it protects own every aspect of the US economy. This is the latest chapter towards a fundamental shift away from capitalism and free markets.

Wolf, the next leg down is so obvious I’m not even sure it happens. But it will.

Another 1K loss on S&P 5 is like money in the bank, if you get timimg right.

Short Bezos, Zukerberg, Ma, Pichai, Nadella, all of them.

Tech is next. NDX has not been taken to the woodshed…. yet. Earnings this month may change that. The SOX index is breathtaking in its nosebleederness heights. I learned in the last two swoons 2000 2008. Chips crumble and when they do. When the love is gone They don’t bounce. They are a commodity

andy,

I was so itching to short this market on Thursday — the end of the best week in decades, with exuberance out the wazoo even as we’re looking at 25% unemployment next month. A prime short point. But I was able to restrain myself. This market is totally nuts, and I don’t want to get run over :-]

Don’t have any itch to enter “investment” casinos, but I realize do need to know what’s happening in them, because they indirectly affect my life, fortune but not my sacred honor.

Thanks, Wolf.

So happy I’m not in the home “asset” market!!

I purchased way, way back when my 1st home cost was perfectly affordable on my wages back then, 1956.

Owned three homes since, never ever putting more than 50% of realized profits into next property. Always retained the other 50% in cash/cd’s etc.

Last home (present) in mountains just sold to oldest daughter and husband planning retirement in couple years. Gave them a good deal and am mortgage free after all these years!

I feel nothing but sorry for those young who expect to be able to purchase homes today unless they are wealthy to begin. The commitments they will have to make on average will put a noose around their necks for decades.

The country has been finally plundered by the oligarchs (the Chicago Boys) and it will take a virtual revolt before major changes are made to restore some semblance of financial normality.

We can’t have maniacal consumerism as a social goal for the masses.

You can’t have just “kill them all and let God sort them out” as a policy.

“Survival of the fittest” is not a long term policy.

All that jus leads to serfdom.

Here in SEquim I am seeing the first of forclosures. RE has been very hot up here and houses are still moving. Probably flee sales. But this town is going to get hammered. So much is dependent on tourism, summer visitors to big festivals likely to not happen. Foreigners visiting the olympics. Prolly not. Lots of service industry. The rest are over 55 retired in big houses most likely dependent on pensions and investment portfolios.

75percent of the town closed and the local sporting goods store just went under

Bad juju headed this way

As for Seattle. Tourism dollars are pretty big There and so are the techie stock options. Might be fewer new Tesla’s in six months.

Sequim may prove to be one of the more resilient places – R.E. wise. With the likely dispersal of office employees it may well turn into something of a haven for ex-Seatlleites.

One of our abiding regrets was the move from there to assumed pastures greener.

Chin up!! You will probably ride out the coming storm just fine.

People who work from home still want to be within reasonable proximity the office, as they need to attend periodic meetings, etc.

Sequim is nice, but I doubt it will attract tech workers. The Techies would rather pay $800/sq ft. to live in Kirkland.

Plus, a lot of tech workers are recent immigrants. They don’t like the red zones, and the red zones don’t like them.

China’s ghost cities and is the US soon to follow?

In the past, economic realities determined where people lived.

SF during the gold rush, Texas during the oil rush, Detroit during the auto buildout.

Can local economies survive on simple home building?

Build it and they will come.

China’s government manufactured vast cities not based on economic demand but with the expectation that demand would soon follow as the population filled in the gaps.

The US approach is different but similar.

In Utah, the demand for housing is definitely there but from what I have seen the underlying economy is sketchy at best.

Take out home building and all its associated economic activities( Realtors, mortgage brokers, bankers, title insurance etc ) and what economic activities do you have left to support these communities?

The housing market can never be allowed to dry up or economic chaos will soon follow.

Sidebar, One reason I think that Utah has been hit so hard Covid wise, is large Mormon families, which leads to lots of in home contagion, and thus more cases. Same with Hispanic areas where large families predominate.

I see little risk for single residential, market was tight with inventory before and sales were strong , at least in the San Diego county that I follow.

Apartment buildings are a different animal, about 30% of our tenants didn’t pay April rent, I can only guess that May will be worse.

The government has put a 6 month moratorium on evictions and one year for the delinquent tenants to pay. Every landlord knows they will never collect. But government gives tenants incentive to stay without paying even if they can and most tenants will exploit the opportunity . I know most of the tenants who didn’t pay for April it was out of choice not necessity . There is nothing the owner can do about it right now.

Why doesn’t government mandate so people can buy food at any retail outlet and not pay for 6 months as well?

I think apartment buildings are going to suffer, 6 months without rent income is a long time and we might see some owners with no choice but try to sell them. Unless the Fed comes up with a program for them, this could get ugly.

I am now seeing price reductions in San Diego

Although its anecdotal but still

Most of the decent homes in san Diego needs jumbo loans

Its gonna be interesting

We have endless brand new empty apartments here in the DFW area. I think they were overbuilt. Everywhere you look apts were going up, I’ve never seen anything like this. Now they are everywhere and many are empty.

Many are still under construction. It won’t end well.

But on the other hand, many families were priced out of the absurd housing market, maybe, if prices drop to a reasonable level they will be able to buy a house, Specially if they are essential workers and didn’t lose their job.

Apartments might get converted to condos like last time?

When we have high “low inflation” and anemic wage growth pushing people to spend more than they can afford on rent, and damn near everything else, this type of situation happens.

That vast precariat have no savings to cushion the blow from this type of event. The owners of capital might just have to take it in the seat. The horror!

When this is all over the owners of capital can continue to squeeze the precariat until they bleed.

A little poetry for Sunday.

So I walk up on high

And I step to the edge

To see my world below

And I laugh at myself

While the tears roll down

‘Cause it’s the world I know

Oh it’s the world I know

Collective Soul

A little poetry for Monday.

Sunday’s done, workday’s here

But work is gone, perhaps all year

nice RD…

Velocity is the drug that I need

The wind in my face riding at speed

Swiftly I glide, singing my song

While high overhead, a hawk soars along

He floats without effort, smooth and free

As I spin at a pace almost effortlessly

Though gravity binds me down to the road

My spirit flies as the world I behold

Oh well, 15 cm of snow fell yesterday. I’ll stay off my bike(s) today.

Wolf, do you still get your exercise fix in by swimming in the bay these days?

Dan Romig,

Yes, but it’s more complicated now. My swim club is closed, so there is no sauna afterwards to warm up. The water temp now is a nice 58 degrees, but when you get out of the water, the air may be 50 degrees and windy. You’re on the beach with until then well-managed early-stage hypothermia (we swim without wetsuits, and I don’t have the natural insulation on my body that would come in very handy in moments like these). So warming up afterwards is a three-step procedure that includes running up Russian Hill a couple of times, then taking a hot shower until the hot water runs out, and finishing off the warmup with a big mug of steaming sweet red-bean soup (oshiruko in Japanese). And afterward I’m on a high for couple of hours.

Since there are not many morons out there doing this, “physical distancing,” as it’s now called in California, is easy to do. Just stay away from the sea lions.

It keeps me sane (OK, I know… but give me break)

1) Wuhan-19 will lift BK. BK will increase empty spaces.

2) Those who survive will need larger RE for social spacing.

3) Buttressed economy will send RE prices up. The cubicles are dead.

4) Yesterday fads will never sell today. Its hard to predict today tomorrow fads.

5) Today fad can be ugly, low quality and stupid, but they sell.

6) When supplier meet a customer, the customer will evaluate stuff.

7) We don’t create fads. We follow them after they are born. When they fizzle we have to cleanse their leftovers.

8) sku #1000 will never sell today.

9) Our customers can buy sku #1001 at a certain price, but we can’t make profit.

10) We like sku #1007, it have potential. We can sell it to our customers, but your price is too high.

If u give us a 20% discount for quantity, we can put it online, have high turnover and give u a large repeated orders.

11) SF RE next to tent city prices are too high. When SF RE “animal spirit”

is back, the surviving co will need larger spaces, at a discount, for social

distancing.

a comment on 2A. I think the trouble will start soon if the economy stays locked down. Wait for the shortages to develop which they will in time. When local authorities take advantage of this lockdown to issue fines when no one has any money that could be the tipping point. All I know is it’s coming and when it comes it will be a hurricane!

To support RE cities/ states will write spacing laws.

Have you read Ralph Nader’s letter to Powell?

It’s good. Read it.

Just read it. Thanks –

Is the stock market a rent-to-own racket?

Just read it, thanks. Yes, compared to last year the new interest rates will cost me all my living expenses, expenses that were paid out of cash flows in 2019. I was taught to be careful and prudent. It appears I was taught wrong. Prediction is very difficult, especially about the future.

More evidence that the great depression isn’t happening.

Bookings for cruises are UP. Yes you read that right, up. Bookings for 2021, made in 2020 are higher than bookings for 2020 made through the first quarter of 2019. This is for cruises, the one area of travel where you’d think nobody would be touching for years to come. And yet, everyone’s shrugging their shoulders.

The masses realize this is all nonsense. And those same masses will go back to their lives once the nonsense ends.

Just Some Random Guy,

I hope you do your part in this cruise ship boom and go on a cruise ASAP :-]

Think of how much fun you will have if just one infected person on board turns the whole ship into a pariah ship that cannot dock anywhere, and where people infect each other as the ship sails from country to country, begging to be allowed to dock. Think of all the adventures you’ll have on board. Send me pics!

Wolf: Any truth to the rumor that the old style Roman galleys are making a come back to replace the “Everything Included” Petri dish experience ??

Reminds me of the ads for those hotels where you have to make your own bed and they hand you a hammer and nails at check in. ;)

WT Frogg,

That would be kind of fun, actually. Get some real exercise while on a cruise :-]

I have a feeling that the cruise booking increase for 2021 is fueled by all of the 2020 cruise cancellations. The cruise lines are offering either a full refund on 2020 cruises or 120% credit toward a future cruise. I can’t imagine anyone looking forward to being contained on a floating Petri dish at this point, but I’ve long been out of step with the general populace…

Good Idea HD; I for one will never again get on one of the behemoths AKA cruise ships floating around the world, some for eva from what we are seeing, and feel very fortunate not to have done so since Uncle Sam’s tin can put me back on shore in Long Beach long long ago…

A 40-50 foot private sailboat on the other hand, would be of great interest, more so than the CAL 36 last time,,, so if anyone is ready to sell their sloop, or, preferably, a ketch, please LMK, especially if it’s on the CA coast, $0.10 or so on the dollar,, and ”fully found and ready for sailing to HI” so I can go see the grands,,,

(IOW, not getting on another petri tube from Heck either…)

A sloop can be a good ketch, if it’s cheap enough.

Pun (genuine, not generic for “joke”), intended.

RD, yawl have a penchant for puns.

Spot on HD. Bookings are being made with future cruise credits. This is not “new” business.

Your post piqued my curiosity, so I had a quick check on AIS Marine Traffic: by “quick” I mean I only had a look at the Mediterranean, Red Sea, Persian Gulf and Northern Indian Ocean.

Right now there are a grand total of four (4) cruise ships under way: two belong to German travel giant TUI (you know, the one whose bonds a high EU official just pitched to German savers), one to Costa Crociere (the Italian division of Carnival Cruises) and the last one to Seaborn Cruise Lines of Seattle. All four are heading to offshore anchorage points, where they’ll join a huge fleet of oil tankers and LNG carriers idled by lack of demand.

That’s it.

Tankers and LNG carriers in Eastern Asia are being pulled out of storage as China and Korea get back to work, but cruise ships are another matter completely: while it’s likely there will be some recovery sooner than anybody expects it will take 2-3 years to get back at pre-epidemic level. The sector will be ravaged, so I propose a new game: which cruise line will be the first to get a bailout? The winner gets the smug satisfaction of being right.

Why would a cruise ship be pulled out in April 2020 for 2021 cruises? I realize it takes some time to get a ship ready, but probably not 8 months. Would be interesting to see what’s happening in Oct or Nov, that would be a good indication of how many cruises will be taking place next year.

The idea posted here earlier MCO1 was to use those cruise ships as floating hospitals/containment facilities.

I thought it a good start, but looking like most of we ‘murricans’ are doing a heck of a lot better at taking this virus seriously, so now thinking we may not need that many ‘confined’ beds, etc.,,,

though I must admit, out just now to replenish the wine futures for the first time in 2 weeks, with my gloves and mask, saw some folks with neither, including elders who should really know better,,,,

wine store clerk, a good younger guy, had on both gloves and mask,, and his usual cheery disposition

Cruise ships will make most of their money this year as storage tanks for oil products.

JS Random,

I don’t agree. I think people expect to go back to their regular lives, but actually have no clue. Even our Cdn leader (Trudeau) has said there is no possibility of normalcy until there is a vaccine, and went on to say it would be 12 months to 18 months duration.

Cruises? Not likely. Victory gardens instead of front lawns, likely.

Trump is floating the idea of firing Faucci as of last night and is trying to lay the groundwork for blaming the individual states for the test and response failings. Now, he is pushing the idea he has the power to force reopening the economy which even the Heritage Foundation disputes.

Mass layoffs coming in state and city support services as people stop paying taxes and cities forced to cut back.

Cruises and future credit card freewheeling? No, there will be some kind of reset and we’ll be lucky to see financial institutions remain functioning without drastic changes going forward.

Lol, those cruise liners are probably selling those cruises for never before heard of discounts and fully refundable. I am sure they will do whatever possible to inflate their bottom lines and paint a rosy picture. This is nothing but people trying to take advantage of the situation, it has nothing to do with the economic health of the country or whether people think the mobile morgues and impromptu graves are “nonsense,”

Wolf – thoughts on GNMAs in this new mortgage environment? Thanks for the great site!

I have one For Sale in Small Town North Central Florida USA LOL!

gleaned this off stocktwits: “As a former real estate banker, I have told my friends on their primary residence, either you leverage it to the sky or have no leverage at all. A loan to value of 50% is very dangerous because if you can’t service debt for whatever reason, your equity can be wiped out because of foreclosure, especially during a house market collapse where values are all over the place. IMHO, real estate is a demonstrated high-low game where a middle hand can become worthless.”

Seattle Times has a piece about flippers aggressively soliciting for homes in the area. Like with the stock market “crash” of last month, this is an awesome buying opportunity for those with cash. The profits will be very nice once the V shape recovery starts.

Of course this being ST, the angle of the story was of the “oh my god how can anyone possibly think of making money in a time like this”. Always good for an early morning laugh from that rag.

Why don’t you go and flip some houses and make some money with your V-shaped recovery, no?

Wolf,

I am becoming more and more convinced with each comment of his that he’s a paid shill you’ve put here for our entertainment and clicks.

I kid, I kid!

I think you’re sentiment fits better in docotorhousingbubble site. You and New Age would have something in common being a house humping cheerleaders ;)

I think this means the top tier is headed toward some fairly quick and significant price declines. The top tier is dominated by small specialty builders that have to keep selling in order to stay afloat.

I’ve saw this in action at the start of the last crisis. In Sept 2007, just as things were getting shaky, I looked at high priced custom homes from various builders in a new development area. They all panicked as the transactions started drying up. The builders were so worried they were taking time to show the homes themselves, to provide that extra personal attention and speak knowledgeably about the features. One guy, who had already built and sold about 6 quality homes in the development over the previous few years, called me up and offered a 20% priced decline if I bought the following week. I said how about a 30% price decline? Sold.

He was a smart guy who saw what was coming. He confided that he was worried about paying his contractors and somewhat of a team together. He also said I was the only serious prospect he had seen for a long time.

The other homes I looked at, which I did not buy, languished on the market for years. The builders’ family members wound up living in some of them, as prices kept dropping.

In the high end builder market, you aren’t dealing with Toll Brothers or Polte Homes. You are often dealing with small family-owned businesses that can’t afford to wait things out.

I’m seeing a lot of memes & comments on twitter from my millennial friends sarcastically observing “Well now that millennials have given up on their avocado toast & lattes does this mean we can finally buy houses now?” And “Millenials just waiting for Housing Market crash to swoop in!”

So should I link this article about lending difficulties? *insert crying AND laughing emoji, because it’s so incredibly tragic- the state of housing- that ya just gotta laugh*

Someone mentioned it upthread but very few renters are able to save 20% for a downpayment with sky high rents, even if prices come down moderately. My parents, without a college degree, have been able to buy 3 houses. We both have degrees & haven’t been able to buy 1.

Yup and you have article like below that blames Millennial for being entitled to think this way which I find it utterly BS. While I don’t think it’s a good idea to rejoice at someone else’s misery, but saying they are entitled to think this way is completely missing the point. I have a lot of sympathy for the millennial, they got the double whammy, one from GFC and now this. Perhaps it’s this hugely flawed system that helped so many boomers creating wealth from homeownship that completely left millennial and Gen Z behind and this is the only form of expression at this level of inequality they have left.

As a Gen Xer myself, I definitely see the hypocrisy on display from boomers and my generation alike. Easy to blame an entire generation when you’re the benefactor of the positive while leaving everyone else to clean up after your destruction.

https://www.ccn.com/these-entitled-millennials-are-cheering-for-a-housing-market-crash/