The Fed is going nuts trying to contain this.

By Wolf Richter for WOLF STREET.

Thursday early afternoon, during the chaos when the S&P 500 was down nearly 9%, what would turn into the worst single-day stock market sell-off since the 1987 crash, the Fed rolled out its fastest mega money-printer yet, after its smaller money-printers malfunctioned. It’s not going to be a long-drawn-out QE – though there is a component that is just that – but it’s going to be trillions of dollars, essentially all at once, front-loaded, starting today, though today fizzled already.

This is the Fed’s latest effort to bail out Wall Street, the cherished asset holders that are so essential to the Fed’s “wealth effect,” all repo market participants, the banks, and the Treasury market that suddenly has gone haywire. Lots of things have gone haywire as the Everything Bubble unwinds messily.

Last week, the 10-year Treasury yield had plunged toward zero during the stock market sell-off, which was crazy but in line with the logic that investors were all piling into safe assets, and early Monday morning it fell to an unthinkable all-time low of 0.38%.

But then, the 10-year yield more than doubled from 0.38% at the low on Monday to 0.88% at the highpoint on Thursday. That the 10-year yield spikes during a stock market crash is somewhat of a scary thought. It means that both stocks and long-dated Treasury securities are selling off at the same time. And that probably made the Fed very nervous.

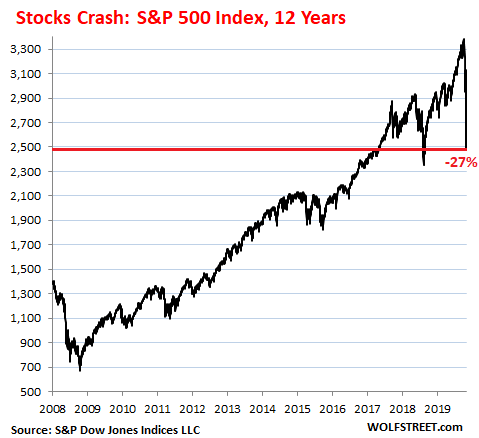

For stocks, Thursday was the 16th trading day since the S&P 500 peak, and in those 16 trading days, the index has crashed nearly 27%.

The smaller money-printers fizzle.

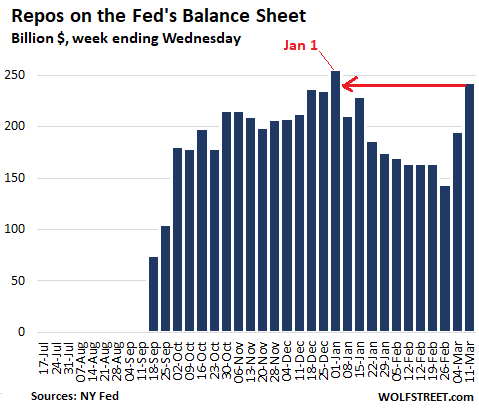

Late last week, demand for repos had increased. And earlier this week, as markets came further unglued, the Fed shoveled more cash into the repo market.

- Monday morning, the Fed raised the maximum of the overnight repo from $100 billion to $150 billion.

- Tuesday morning, it raised the maximum for the twice-weekly 14-day term repo from $20 billion to $45 billion.

- Wednesday, it sat on its hands and watched its handiwork, which was a continued crash

These increases are reflected on the Fed’s weekly balance sheet released today. Repos soared from $143 billion two weeks ago to $242 billion, nearly back where they’d been on January 1 ($256 billion). Note how the repo balances had been declining from the beginning of the year, dropping by 44%, until the stock market began to crash and the Fed opened the vault:

And it didn’t work. So Thursday morning, the Fed threw more cash at the market:

- It again raised the maximum of the overnight repo, this time from $150 billion to $175 billion.

- It added a $50 billion 25-day repo to the mix.

And stocks just continued to crash.

So the Fed rolls out its fastest mega-money-printer ever.

Thursday early afternoon, the Fed announced in a surprise shock-and-awe move that it will use the repo market in a big way to try to prop up and inflate whatever needs propping up and inflating. It will offer a series of $500-billion term repos at least through April 13, amounting to $4.0 trillion in new money over the four-week period.

On Thursday at 1:30 p.m., it offered $500 billion in three-month repos, to settle on Friday. But it fizzled: Of this offered amount, only $78.4 billion were accepted, perhaps because market participants weren’t able to come up with that much collateral that quickly or because they didn’t want that much cash.

This surprise announcement of the $500-billion offer caused the S&P 500 index to spike 6% in 15 minutes. But when it emerged that only $78.4 billion had been taken, it succumbed again.

On Friday, the Fed will offer $1 trillion in repos: $500 billion in three-month repos and $500 billion in one-month repos. That’s a heck of a lot of bucks to print in just one day. But no problem for the new mega-money printer. If anyone wants this much, it can print it.

Next week (the week of March 16), the Fed will offer another $1 trillion: next Monday, $500 billion in one-month repos; and next Friday, $500 billion in three-month repos.

This will continue in each week, the same procedure of $1 trillion a week plus all the other repos, through Monday, April 13.

If all these $500-billion repos starting Friday are accepted during the period, minus this Friday’s one-month $500-billion repo that will unwind on April 13, they would amount to $4.0 trillion.

These repos would come on top of the other repos and on top of the $60 billion a month in purchases of Treasury securities, that the Fed said it will broaden to include Treasury securities of all types and maturities, not just T-Bills.

In total, this would amount to nearly $4.5 trillion through April 13 that the Fed is offering to create to bail out Wall Street, repo market participants, the asset holders, the banks, and Corporate America. It would more than double the already re-ballooned balance sheet (currently $4.3 trillion). It could push the balance sheet to nearly $9 trillion by April 13.

This is apparently the price of trying to maintain the insane Everything Bubble that the Fed has created since 2009.

But maybe not.

It may well be that there is neither enough collateral nor enough demand for cash to come anywhere near those amounts. Repos works differently than QE. Under these repurchase agreements, the Fed offers to buy securities, and if there is not enough demand for cash, or not enough collateral to cover this much cash, then the repo auction will be undersubscribed.

This was the case on Thursday, when the first $500-billion repo was way undersubscribed, with only $78.4 billion being accepted. The rest of the cash the Fed offered found no takers.

So that total amount of cash that will actually get poured into the system may only be a small fraction of the theoretical $4.5 trillion offered over the next four weeks. It may turn out to be just a guarantee by the Fed that there will be enough if there is enough demand for it, and enough collateral to cover it.

But when you think about it, it’s really nuts what the Fed has done since 2009 to create the Everything Bubble. And what it is trying to do now to contain the implosion of the Everything Bubble is even nuttier.

Holy moly, that’s fast. Too fast. Desperate Fed rolls out biggest bazooka yet. Read... Stocks Crashed. I Covered My Short Positions (SPY, QQQ) Because “Nothing Goes to Heck in a Straight Line.” Out of Spite, Bought Some Crap for a Bear-Market Bounce

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

How do repos work in the real world?

Could I (if I was a banker) give the FED my airline shares for cash, and like a pawn shop just not pay the fed back if the airline stocks fall in price and just let them have the worthless shares?

Can I give the fed Bitcoin for repos?

The Fed only accepts Treasury securities, MBS that are guaranteed/issued by Ginnie Mae (government agency) and the GSEs Fannie Mae and Freddie Mac, and “agency” securities. The Fed does not yet take bitcoin or old bicycles, though someday it might, the way it is going :-]

Wolf,

What if the Fed take the opposite move next week and raise rates by 50 basis points. Would that shore up treasuries?

I know it’ll tank the stock market, but at some point, someone will figure out that there are other priorities relative to equities. It will draw a lot of overseas money over into the treasuries right?

May be the Fed needs to go contrarian here. Toss a big middle finger to the market, and see what happens. It’ll mean blood letting, but that’s going to happen anyway when next quarter’s earning start to show up. And when Apple reports it sold 5000 iphones during all of March, well, that’ll tank all of tech and crater the market anyway.

Bloodletting is long overdue. Cull the herd. Darwin would approve.

The Fed has been an overindulgent sugar daddy for far too long. As a result, the market has become a spoiled trust-fund brat, bailed out at every turn. Those trust fund kids never are able to function independently.

Please say no to the printer, Jerome. Just walk away. Time for some tough love at the repo window.

Yes, I’m with you. I’ve suggested before that the Fed should actually sell long-dated Treasuries to bring up the long end of the yield curve, and raising short-term rates would then raise the whole curve. In terms of the economy, those higher rates would still be very low, and those increases would have no impact. But it would show that the Fed has confidence in the market and the economy and isn’t panicking. But that’s never going to happen.

Wolf,

Wouldn’t it be necessary for the FED to Buy long dated treasuries in order to bring up the long end of the yield curve?

I would be very happy to go to Saudi Arabia and give the Fed MBS for cash. Just don’t step into one of his Embassies, especially the one in Turkey.

What happens with the illiquid assets?

Those are stuck and the cry babies need ‘help’.

Wolf,

Thanks for the analysis, as always.

Indeed the big banks cannot possibly take down multiple hundreds of billions in repo’s as it would trigger non-compliance issues with banking regulators (Tier 1 capital ratios).

The smaller players, as you mentioned, don’t have that much collateral sitting around.

Found it amusing that reverse repo’s had their largest volume day in months Thursday afternoon, draining liquidity.

Fed is clueless. They’ll confirm it again when they cut Fed Funds this week while median CPI is starting to accelerate. Cutting rates didn’t work. Maybe they should try raising them?

Way too funny.But I finally understand Repos .Thanks for the

Question A

Wolf, I have two old bicycles in great shape. I can use them and they’re worth something. I wouldn’t exchange them for Fed $$ that are worth ??? next year, or month, or week.

Hold on to them. There’s a rusty old bicycle bubble coming.

The private repo market has been populated by hedge funds. What if the collateral is subject to more than one claim?

Cailtlin Long in Forbes:

“For every US Treasury security outstanding, roughly three parties believe they own it. That’s right. Multiple parties report that they own the very same asset, when only one of them truly does. To wit, the IMF has estimated that the same collateral was reused 2.2 times in 2018, which means both the original owner plus 2.2 subsequent re-users believe they own the same collateral (often a US Treasury security).

This is why US Treasuries aren’t risk-free—they’re the most rehypothecated asset in financial markets, and the big banks know this. Auditors can’t catch this because GAAP accounting standards obfuscate it, as I’ll explain later. What it all means is that, while each bank’s financial statements show the bank is solvent, the financial system as a whole isn’t. And no one really knows how much double-, triple-, quadruple-, etc. counting of US Treasuries takes place. US Treasuries are the core asset used by every financial institution to satisfy its capital and liquidity requirements—which means that no one really knows how big the hole is at a system-wide level.

This is the real reason why the repo market periodically seizes up. It’s akin to musical chairs—no one knows how many players will be without a chair until the music stops.”

https://www.forbes.com/sites/caitlinlong/2019/09/25/the-real-story-of-the-repo-market-meltdown-and-what-it-means-for-bitcoin/#17166d8a7caa

They can’t all be collecting the interest income.

8O (That’s an emoji, BTW)

This is not going to be pretty.

She is a bitcoin nut.

If you want to read about collateral re-use or velocity you are better off getting it from the source:

Manmohan Singh of the IMF

His thinking:

Transactions on wholesale capital markets are often secured by marketable collateral. However, collateral needs balance sheet space to move within the financial system. Certain new regulations that constrain private sector bank balance sheets may have the effect of impeding collateral flows. This may have important consequences for monetary policy transmission, for short term money market functioning, and for market liquidity. In this context (and in contrast to the literature, which has focused mainly on the repo market), this paper analyzes securities-lending, derivatives, and prime-brokerage markets as suppliers of collateral. It highlights the incentives created by new regulations for different suppliers of collateral. Moreover, it argues that the central banks should be mindful of the effect of their actions on the ability of markets to intermediate collateral.

Sample work:

https://www.imf.org/external/pubs/ft/wp/2013/wp13186.pdf

Argument: The securities at the Fed are dead and hoarded. They should be freed and used for collateral -:)

@Iamafan,

I am well-acquainted with Dr. Singh and his work. She may be a Bitcoin nut, but she is essentialy saying the same thing.

Caitlin Long of Forbes said:

“Last week the financial system ran out of cash.”

and

“Here’s what the books of three parties show when a transferee (Party A) sells pledged collateral to a third party (Party C):

Party A owns a particular US Treasury Bond, showing an asset of $100.

Party B borrows it, showing a liability of $100 ($100 of securities sold, not yet purchased).

Party C shows an asset of $100.

If you add up the positions of all parties, economically there’s no problem because the net of the two longs and one short position add up to $100. The problem arises when you aggregate the three US GAAP financial statements. Both Party A and Party C report that they own the same asset (!) The balance sheets balance because Party B records a liability, so auditors don’t catch the problem. When that same bond is reused again and again and again in similar transactions, the magnitude of double counting within the financial system builds in a manner that no one can accurately measure.”

1. The financial system does not and did not run out of cash.

2. The contents of the second quote are very unclear, and I suspect, in error. ie “Party B borrows it” …… borrows what?

the whole blurb makes no sense ……………..

you can’t still own something that you sell …………..

um… anyone remember mf global? it’s called re-hypothication.

screw this repo dance what happens if Fed just quit? There are approximately 129,000,000 households in US. Divide that into $4.5 trillion you get approx $38,000 per family. I know $4.5 trillion not repo but my Calculus is bad and I cann’t find area under curve for repo BS. Maybe you could do that math for me. And what would households do with extra $38,000? SPEND!!!

What black swan necessary for biggest bubble to pop? BONDS!

That will be more than a cold when that happens.

Repos are to provide overnight or short-term temporary liquidity for 13 listed participants who are unable or unwilling to lend to each other but who have good paper, Treasuries etc to offer as collateral to a lender. This is done every day on a normal basis. The Fed becomes the lender of last resort, if regular players are unable/unwilling to participate, unfreezing the repo market should there be temporary liquidity issues for any or many participants.

QE4 would be the purchase by the Fed of less-than-stellar paper from financial institutions.

Thank you Robt for providing needed clarity.

How are about my gold bars I bet they are slobbering to get their hands on those.

Good luck, wife guards those like a rabid dog!

@ Wolf

“The Fed only accepts Treasury securities, MBS. . .”

How can you possibly know that? Have you seen the Fed’s books? Has anyone? How do you know they don’t do all kinds of secret deals for their cousins and buddies of the Fed’s owners?

End the Fed and fractional banking forever

Raging Texan,

Every single one of those securities has a CUSIP number, and the issuer knows who holds them by CUSIP number, because the issuer has to pay interest to those who hold them. Just like stocks. Everyone who holds stocks is known so they can receive dividend payments. So EVEN IF the Fed wanted to lie about what it holds, everyone else would know what it holds anyway. The Fed is not that stupid to try to lie about its holdings.

@A

No, what you are referring to is TALF.

The Fed did TALF and the Treasury did TARP.

This is when they did Cash for Trash.

Minerd is waiting for TALF because his hedge funds customers need to lever up.

That’s next, if this repo doesn’t work.

REPOs provide trading cash for the investment banks, the most recent parabolic rise in the stock market coincides neatly with the start of REPO in Sept, and ends with the pullback in REPO a few weeks ago. The Fed cannot jumpstart a market, they can only add fuel to the uptrend. The REPO announcement yesterday fell on its face. They probably feel a bottom is near, and certainly the PPT was in the market buying the overnight futures. The Yellen Fed asked for authority to buy a broader range of assets. That requires Congressional authority. In a REPO the banks offer securities, treasuries, for cash, so bitcoin for REPO would be a Reverse REPO, cash for the security. If you do both concurrently you are directly monetizing the Treasury.

Fed can also issue payment in kind for distressed assets. If you own shares of an airline, and the FED takes the shares, and liquidates, you might get a 737 in payment:)

you could find a third party that has treasuries, offer them your shitty collateral and they will ask for a fee and give you some of their better repo. Then you can take it to the fed and get the money.

Welcome to the world of sponsored repo and repo rehypothication.

But that requires the sponsors to want to trade with you, and they might not want to give you their pristine collateral and be caught holding the shit like in the case of bear stearns.

so the 3 month repo being so under suscribed is i believe the term is too long and lack of quality collateral in the system, no one is willing to offer collateral for that long to companies that might go bust with it on their books, they wont get it back. hedge funds probably have a lot of complete junk in their hands and no one trusts it either.

I had never heard of the Repo market before last September. Prior to YouTube, I always thought the Fed was part of the US Government. Then, during the ‘08 banking crisis, I learned all kinds of new vocabulary words: CDO, MBS, QE, ZIRP. Still not quite sure I know what all those acronyms really mean.

We all read the book The Big Short and later saw the movie and then we thought we understood what caused the ‘08 crash.

My question is, before the internet existed, how did the Repo market work? Was there an open cry trading floor somewhere? Did the bankers just get on the phone at 5 O’Clock and start cold calling other bankers seeing if they could borrow dollars in exchange for collateral? How did the Repo market work before the internet?

The Fed has run out of dry powder

And I see the US response to COVID-19 going down the same path as AIDS in the early 1980s. Once the disease was identified, the transmission pathways identified, and a test to identify infection was made, EVERYBODY should have been tested, contact tracing pursued vigorously, and quarantines imposed

Standard infectious disease control

But that didn’t happen. AIDS exploded world wide and killed millions of people and is still with us, now become a favorite of Big Pharma to make Big Bucks selling patent drugs to infected people who will need the drugs for life.

COVID-19 is less lethal but far far more infectious – it will explode and then be with us for a very long time

If you think the stock market has gone nuts, just imagine what it will do if a certain person in the White House who’s still in denial about the disease gets it

Matt Hancock, the UK Secretary of State for Health, said yesterday that testing everyone is not going to help and would not be done in the U.K. “Because the test is not reliable for people who are not symptomatic. It’s not effective,” he said. He gave a lot of reasons, such as too many false negatives and false positives, which made testing without symptoms “counterproductive.”

“Because the test is not reliable for people who are not symptomatic. It’s not effective”

In many U.S. states, there are no test kits for those who ARE symptomatic.

Exactly the base foundation of the very worst case now very likely in USA IP.

Thanks for pointing that out, but IMO, just the very early beginning of the discovery of the spread here…

At this point, with one of the really great WC Fields characters in charge here, we are about to go through the scene where he, Fields, went through what “must have been a plowed field.”

The US is shamefully late the CDC botched testing roll out and FDA has held up the private market. This was so predictable seeing what happened in South Korea and Italy that is a scandal we were not more prepared.

But every state has COVID19 testing capability as of several days ago, there is no state in the US where symptomatic people have no access to testing. And Roche now has the capacity for 500,000 tests at 100 facilities all over the US (emergency FDA approval), look for a huge spike in presumptive cases in the next week as testing capacity grows exponentially. It is far too late for containment in the US, and we are on a path to be more like Italy now than Japan. But now that a real response with an emphasis on social isolation is starting to permeate all states, the curve will probably start to turn in a month or so.

Let us hope anyway.

Reports from China are that it depends on where in/on the patient the samples are being obtained. The tests right now are specifically for the virus. Asymptomatic patients might not be shedding from the oral region which is most commonly the place to swab for a test as it is super easy to do. Blood tests or swabs from the throat or elsewhere on/in the body might be better. We’ll know soon

The UK’s policy is absolutely nuts. I’ve been following it closely since it’s my country. Expect the number of cases to explode there. They have done less than the USA.

I was thinking he just might have it based on his appearance Wednesday night.

Trump does not ignore it. He is a notorious germophobe.

They are politicizing it all because they hate Trump and Orange didn’t come up with an inoculation in the basement of the White House with his chemistry set.

Put the blame where it belongs with the bureaucracy at the CDC. Their funding went up a lot since Trump has been in office yet didn’t get moving at all when it was known last November that there is a novel virus circulating around the Level 4 lab in Wuhan.

Even the lefty governor of California was complimentary on the adminstration’s efforts in getting it going nearly two months ago when solid information was coming out with the analysis of the virus. Try to be objective.

“in the basement of the White House with his chemistry set”

Why does a person who can move hurricanes with Sharpies need a chemistry set?

You made a funny, but the hurricane paths predicted on that incident included just that same sharpie track from the weather bureaucracy. It happened to be on the more southerly set of computer modeled tracks.

I do blame him for not using his laptop to calculate the path from his vast knowledge of high altitude steering patterns of hurricanes.

Erle, this post is not only too politicized, its full of false information. You are fake news Erle.

You make unwarranted assumptions on my politics. I hate them all, some more than others. The administration had to nullify several bureaucratic rules in order to get CDC to use private providers to get off of the dime. Since the Department of Homeland Security department was foisted upon us by a bi-partisan group of doltish thieves in congress and shrubco they have consumed a Trillion and have only succeeded in transmission of foot fungus in airport inspection waiting lines.

I always have my special TSA socks for that problem. Go barefoot or re-use the same socks in an airport? No thanks

Trump has not been helpful and his leadership on coronavirus has been shamefully late and far short of what is needed. CDC botched the testing roll out and FDA held the private sector out of testing. This will probably sink Trump in the next election and it should. He should have been leading.

Just announced: Trump was in proximity with Brazilian ambassador (?) who met with mayor of Miami, who tested positive. LoL.

Regardless, CV19 has been in the wild for MONTHS. It’s already here and underwhelming, aside from the reaction to and capitalization on it.

Yeah, I actually do remember the AIDS thing in the early ’80s. It suddenly appeared, the media and some organizations criticised Reagan for not having an instant cure and not caring if there was one anyway because that’s the way he was. Scientists were deemed racist because the entry path of the virus was via Haiti from Africa.

However it was quickly determined that by not engaging in certain behavior chances of being infected were greatly or even totally reduced to negligible cases. For that analysis, charges of homophobia were tossed at politicians, scientists, and clinicians.

Cures, or rather palliative remedies, were developed reasonably quickly and improved over time by ‘Big Pharma’, for which they are chastised because it involves making money for their investment, and everyone knows all drugs should be free because they would be developed by somebody, anybody, who does it for no reason and there is no cost to do so.

Sound familiar?

Anyway, AIDS didn’t affect the stock market in the manner of these times because today’s panic is the result of a triple-witch attack: Coronavirus mania, historic multimarket market bubbles (of which only the stock market is the first indicator), and the overnight collapse of the oil market.

The current president is not in denial; he has been in pro-active and response mode since mid-January, for which he was predictably ridiculed by the same people and organizations that now say he ‘did nothing’, and should have had the cure developed, a cure for which nobody even really knew what the threat was in December.

To see all the media talking heads and politicians licking their chops over the possibility that, having failed at all their other strategies to destroy the presidency, this could be the one that ‘brings Trump down’. They’ve been hoping for a recession, hoping the market will collapse, organizing hoaxes, and wishing bad things on the citizens for the last 3 years; now they are hoping for an epidemic to fulfill their dreams, completely missing the point that in doing so they offer nothing constructive and are actually hoping for misery of the population in order to further their self-centered hate fest in the pursuit of power.

I do criticize one action though; in restricting inbound travelers from Europe, the UK should have been included. Not only has the UK had limited or no screening of inbound travelers, it would be a natural stepping stone for Europeans to reach the US. As is noted elsewhere, the first reaction of people in an infected area is to flee, so as not to be infected or affected by quarantine measures. China and Italy are example of this.

It’s quite something that the organization in America that most controls the money, knows what the real priorities are.

“If your outgo exceeds your income, your upkeep will be your downfall”

What a great line!

Gonna nail that line underneath the WOLF STREET logo :-]

That’s Yogi-Berra-worthy, Tony. :) A genuine Yogiism which could also well fit Wolf’s site:

“Predictions are hard, especially about the future.”

The Swiss National Bank has set the precedent for a central bank to directly purchase stocks. The Swiss did this to keep their currency, the franc, from appreciating too much. A strongly valued franc would depress exports and increase imports, which the Swiss did not want to happen. They cleverly decided to use the strong franc to their advantage. They traded a strong franc for weaker foreign currencies, then bought foreign stocks to recycle the foreign currencies. The SNB had almost $100 billion in US stocks at the end of 2019. About 20% of its total foreign holdings, or about $158 billion, was in stocks at the end of 2019.

https://www.bloomberg.com/news/articles/2020-02-06/snb-s-u-s-equity-portfolio-hits-record-97-5-billion

Direct purchases of stocks would be politically risky for the Fed, but it might try an indirect approach.

I wonder if the Fed is going to quietly accept stocks as “collateral” for its repos, and then accumulate a stock portfolio if the value of the stocks then declines. The party that holds the repo might decide that they will keep the cash and dump the less valuable stocks into the hands of the Fed.

“Cash for trash”, once again, with stocks rather than mortgages this time.

That’s similar in principle to the Fed accumulating over a trillion dollars in bad mortgage debts after the last financial crisis (the 2008 one, not this week’s). The mechanism is different as they would be doing this on the sly, through the back door rather than the front door, but the result could be about the same. The Fed could, in the end, own a trillion or more in stocks that are worth far less in reality than their nominal “book” value.

Few Americans have any idea of what a “repo” is or how it works, so this would be a very confusing thing to explain to them in a sound bite, or a sixty second political attack commercial on TV. It would have the same end result as direct stock purchases, but would be far less transparent to the general public.

The BNS is a major stock market player worldwide not because they “manipulate” stocks but because due to its structure and mandate they are effectively the Cantons’ hedge fund: they trade financial products to turn a profit which is then passed on to the Cantons… and the rest of the BNS shareholders which include some pretty shady outfits based in Germany. Move along US Federal Reserve.

The BNS only discloses stock holdings when they are forced to do so, such as under SEC rules in the US. Domestically and in the EU their policy can be summed up with “mind your own business”: this is not merely because the BNS manipulates stock prices of domestic and foreign (chiefly German) companies for political reasons but because as one of the world’s largest hedge funds they like to keep their cards as close to their chest as they can.

One last thing: the BNS has always hated the strong franc and has long fought a losing battle to trash it. Why? The Swiss economy, like the German and Swedish ones, is very manufacturing heavy and very export oriented. Swiss exporters are always (always) lamenting how “the franc is too strong” and “the strong franc is wrecking our business”, often mere days after boasting how good things are for them.

The infamous attempt to peg the ChF 1,20 to the euro was one of the most stupid monetary ideas I’ve seen in my life, which says it all. The big and now semi-deserted shopping malls built near the border are an Ozymandian reminder of this idiotic policy.

The laughable “soft peg” came unglued last year and we are already at 1.05. Marching to parity?

I wish that I could write like that. The jumble is in my head but I sound like a politician trying to explain it to the eyes glazed over crowd. You make it so clear.

With that, I will not post anymore as I am about to be banned bu Wolf.

Last for certain, I was watching a few guys on BBG TV and one CBOT fellow was asked about the friction in Thursday trading in usually liquid assets. He was asked if the gusher of FED oil would make the bearings stop seizing up but offered that there was bearing damage that might be OK in a week or two. He didn’t say that quite the same a my relating of the segment, but I am a car guy.

Only weak producers hope for weak currency to help them. Strong currency countries have a history of strong exports of desired products. Maybe it compels them to produce quality goods efficiently.

And maybe the unpegging of the ChF was to help the patsies in Europe and Eastern Europe who took out franc denominated mortgages and loans because the interest rate was so good.

If the Fed took stocks as collateral, allowing hedge funds would go nuts buying stocks with everything they prescribed, they would certainly rush to do it. The first one in would gain the most and the buying pressure would be beyond any realm of fundamental sanity.

I think they would be very careful with such a tool. Powell tends to like methods that have been tried before, giving him a model to point to and thus beaurocratic cover.

Smoking MACRO marking for a flash crash.

Never before : Copa libertadores plunged into chaos : x8 red cards.

Notice how stocks always want to bounce back in low volume after hours trading. They don’t trade sideways for a few days, they want to constantly rebound. I see this as evidence that the dip buyers are alive and well.

It’s amazing what a decade+ of operant conditioning can do.

High-frequency exchange-traded algo-derivative dream:

Markets halted limit-up and limit-down in the same day!

(where can i bet on this??)

Wolf,

Equity re-inflation (but can’t push on a string – look at undersubscription) or bridge to recapitalization of TBTF banks with pending hits to internal loan books (which is causing them to stop lending into repo mkt)?

Either way, short term nature of repos makes for an odd tool…maybe goal is simply wholesale substitution of panicked/distressed TBTF repo lenders exiting repo mkt to massive extent.

The Fed try to prevent prevent an anti parabola underwater US yield curve.

A moribund system of debt-based consumption and speculation, thrashing about in its death throes…

Lazy, complacent economists brainwashed into thinking ‘there’s no alternative, this is the way things are’ and lazy politicians allowing the debts to balloon in order to garner votes via the false impression of prosperity that burgeoning debt imbues.

Stock buybacks are the perfect paradigm of this – legalized fraud, but HEY we mustn’t regulate because that’s ‘communism’!

All coming to an end now. Tides and naked swimmers…

Maybe, but I despair that the honest price discover and buying opportunity in reasonably-valued stocks and bonds will never be allowed. How else the everything bubble ends if not in deflation of the bubble is hard to fathom at this point, but as I said, I despair that the rational conclusion is not going to be allowed.

Remember when they said that they would never monetize the debt? That was back when a retiree could have fixed income.

Isn’t fed repo basically the same thing as a stock buyback?

I guess it would be more accurate if every stock buyback was accompanied by a subsequent re-issue on a pre-determined schedule.

“Stock buybacks are the perfect paradigm of this – legalized fraud”

Not exactly fraud (real money is being paid out to shareholders) but it does make companies riskier (fewer internal resources reserved) and pricing more “brittle” (because a greater source of share demand comes from corporation itself, which will be less able to buy own shares in a recession…just as non-corporate share demand also falls).

In and of itself, share repurchasing is just another way to distribute corporate earnings (like dividends), but it has now grown to such a large pct of share demand that it has likely introduced share pricing pathologies and made valuations less stable.

But so has 20 yrs of Fed ZIRP.

“In and of itself, share repurchasing is just another way to distribute corporate earnings” — Not if you’re using new corporate debt issuance to fund the repurchases, which happens to have become the most popular game on Wall Street in the past decade as a result of Fed perma-ZIRP policies. See Wolf’s post yesterday on Boeing and the $43 Bln it blew on such share-price manipulation over recent years.

True, but corps can do debt financed dividends too – so it isn’t buybacks per se that cause the problem…it is excessive risk/leverage appetite by boards and condoned/endured/sown/reaped by shareholders.

And, as you say, heavily fueled by ZIRP – which purchases the illusion of stability today at the cost of inflation tomorrow.

Wolf – Would love to hear your opinion on how this stock market volatility would change real estate market, if any.

I 2nd that emotion !!

The housing market is in another fat bubble.

It will also implode. Taking with it municipalities that have gorged themselves on ever higher property taxes.

Old school math:

The average house should sell 2.5-3 times average yearly income. America is now at 5-7x.

The average house should sell 100-120x the average rent for the same house. America is now at least double that.

Bay Area housing prices have been joined at the hip to the Nasdaq, with a lag of a few months.

And home mortgages are levered, amplifying consequences of price declines.

Florida real estate is at risk. Hotels, Airbnb condos and Airbnb single family homes might be less attractive destinations. The airlines are seeing cancellations. Disney is closed. Layoffs seem inevitable. Restaurants in Wuhan and Milan closed. What will happen in Orlando, Miami and Key West if the virus spread is exponential? An assisted living facility is on lock down. No visitors allowed in and residents are not allowed to leave. COVID-19 test coverage is inadequate. There is no toilet paper or hand sanitizer in local stores. Some northerners own winter homes in Florida. Will they continue to own two, or choose one?

Canadians have been advised to avoid travel to the US. Both countries have urged citizens to avoid crowded places, and unnecessary air travel. Sports are done for this season as are all large venues. Then, supply chain issues have yet to unfold, at least publicly and noticed. Point: all the liquidity in the world won’t add up to much if business as normal crashes. And restoring market optimism doesn’t put bread on the table of furloughed and laid off workers.

Here is just one example. I have a friend who is an extremely high level helicopter pilot. Every spring he picks and chooses his contracts due to his ATR in both US and Canada, heavy time, multi-engine, and wide range of experience. He isn’t getting replies because, “I don’t think the companies know what they are going to do this year”. This even includes fire fighting commitments.Why? If industry is in the tank every dog and his brother will be chasing fire contracts with the obvious result of no one making a dime.

Stretch this to all industries and who is going to actually borrow money and expand? Makers of face masks, nitrile gloves, and hand sanitizers?

And food, and home entertainment (e.g. Netflix) suppliers…

David Hall,

Good point re AirBnBs. I know they are getting hit with less people travelling. If you own a few AirBnBs and you have a few mortgages to pay, uh oh! How long can you last with much lower income?

Now extrapolate that to all other debtors who won’t be able to meet their obligations because of impaired income. How many trillions would that be?

Still, that one humonguous band-aid the Fed’s got there, no doubt about it. Is there anything mountain ranges of unpayable debt can’t do?

Doesn’t solve any actual problems though. Just kicks the can down the road a bit.

Next up: more cash for trash. That band-aid won’t last long, but it might last the day, and the Fed’s got more trillions of toxic financial waste to take up. They can have all they want – the damaged economy will ooze more. And more. And still more.

“unpayable debt can’t do?”

It is payable, in inflation…as trillions in newly invented money represent an unchanged number of real world assets.

But the G will then just invent distanced villains (speculators! Hoarders! Free Masons!) in order to offload responsibility for the inevitable consequences of its own decisions.

I would surmise there is a high amount of refinancing where I live. Any price action on the stock market will impact those refinancing , Nifty trick a refinancing mortgage here is not communicated to US banks, so a lot of homes here are doubly refinanced! First refinancing fuel a stock portfolio , the second one a bond portfolio with corporate debt. The listings are exploding in size meaning more than a few people are feeling the heat of that tiny weensie manipulation. The locally issued refinancings are mostly cov-lite, meaning upon default, the full loan and interests gets called in full. Banks have started to recall as early as last week , so that gives a pretty good idea of the stom clouds gathering.

Please explain. You are saying that a bank would issue a refinance on a mortgage without actually being able to verify that the mortgage isn’t already refinanced?

That seems impossible to believe. Can anyone corroborate this?

I doubt there is any corroboration to be had. Institutional lenders are not stupid about securing collateral.

I don’t do repos so I am a laymen on the intricacies of them but when the Fed got into this market late last year it explained the problem as being one of insufficient reserves being held by banks at the Fed so it set out to boost them.

Now they say they had to intervene again, not because reserves were insufficient but because the bid/ask spread was too wide but isn’t repo about ‘collateral’. I lend you cash and you give me collateral. For me to lend you cash your collateral must be good. Well, when the Government debt you are offering me for my cash is fluctuating wildly in price over the course of a single trading day how good is it and why should I want it ?

Imagine trying to find your way with a compass where NORTH swings wildly between NW and NE depending on what time of the day you look at it. You can’t trust it.

I like your compass analogy. What if you are a staggering drunk making alternating 45 degree swings while averaging headed north. Eventually you will get to the north magnetic pole and find Jerome Powell in a Santa Claus suit.

Well, so nothing goes to the North Pole in a straight line, either.

Would dressing Jerome Powell in a Santa Claus suit have a calming or upsetting effect on the markets?

It bears discussion. After all, conventional means of economic stimulus are not working.

Santa Claus suit = calming.

Hazmat Suit = upsetting.

Law Suit (ZIRP and Takings Clause) = long since justified.

Unit472:

Ah! That word, “Trust”!

Where have I heard that word before?

Somewhere in my past way, way back in my youth…..when in small business and doing business with my local bank…….

Today that word is mud!

It became mud during the contemplation of what the financial wizards were going to do about the GFC in ’08-’09.

The FED can opt to put into operation any kind of plan it wants to sop up the “overturned spaghetti sauce” of this crash but the olive oil will make it all skid to the ground.

Bottom line:

If we don’t pay the piper we will not be able to play “another” game of “capitalism”.

Too many ordinary folk don’t understand twat about how our economic system/casino works. They only know that when they have no money they and their families can go hungry.

Someone mentioned AirBnb. I live in an area that has gone fairly heavily into that scheme. I can’t imagine what the owners of those properties if not fully paid will do and what it will do to the local and regional economies.

We continue to look for some magical formula (algorithm?) that will make 1+1=3.

That’s the problem.

That leaves no trust left in the system by the regular (global) citizen.

After all, they were (are) just, “Doing God’s Work”.

> Lots of things have gone haywire as the Everything Bubble unwinds messily.

My new favorite quote.

> It may well be that there is neither enough collateral

Wrongo, bongo. The alleged “collateral” is government debt, which can be spent into existence by the legislature. And spend they shall. Congress is still in session, after all — they’ve cancelled their recess.

Bring on the spendulus! Debt in the wazoo, out the wazoo, and up the wazoo!

Indeed – but what happens to USD (and other fiats) when they do this?

When the USD drops versus other currencies, does that make U.S. real estate more attractive to foreign investors? Because it must become cheaper for them to buy.

I really wish our country did not allow foreign parties to buy U.S. real estate. I can’t really understand why we allow it.

Z,

We argue…but there may be a pt of agreement here.

1) Perpetual trade deficits require G policies that depreciate dollar

2) Depreciated dollar makes US real estate cheaper…but only for foreign fiat holding foreigners

3) Who can now outbid US citizens for US real estate, driving US real estate prices up (sound familiar?)

4) So, in essence, 50 years of habitual US trade deficits – transiently paid for with depreciated dollar IOUs – are ultimately actually paid for via the sale of US RE to foreigners.

5) The trade deficit balances…over decades…by selling accumulated assets (US RE) to cover annual trade deficits.

I am waiting for the “Fallen Angels”; credit rating agencies must have the coronavirus. They are asleep and watching tv at home.

What people need:

1. If there is a quarantine/lockdown, families should be paid, not fired from the jobs. Like a paid vacation.

2. Insurance coverage, good testing kits, assurance of goods like toilet paper.

What the .gov offers

1. bailout to stock market

2. liquidity to the big giants

Exactly, the government is beyond stupid. When some 70% of the population lives from paycheck to paycheck, without sick leave compensation and complete bill coverage for COVID of course they will be forced to work and infect others all over the place.

Socialism for the rich, “fuck you, you are your own” capitalism for the masses.

Aw, come on, you know how well ‘Trickle Down’ works, right?

What people need:

1) authorization for everyone to print legal currency at home on their inkjet.

2) see #1

That is just overwhelmingly awesome!

Kudos.

“Pay usa workers for not going to their jobs.” That’s cute.

Well, we’ve been paying the political class for decades not to do their’s…

Well, the only thing the G really has the capability to manufacture is…phony baloney money (toilet paper of another sort).

Wolf, Fed said that it realized 500 billion dolars repo auction but it realized only 78,4 billion auction (in 12.03.2020)

Yes, that’s what I said in the article.

Wolf,

Would like to get your take on the big shortfall on repo uptake.

Suggestive of pushing on string (ie, low true demand among Repo borrowers)?

In turn, suggestive of fact that Repo spikes not coming from demand/borrower side but from supply/lender side (TBTF banks exiting repo mkts, because…)

Coming in a little while. With something hilarious inserted into it for your amusement. Be prepared to laugh in dire times :-]

Remember when the Fed had an emergency meeting in the weekend and dropped the Fed Funds rate by 50 basis points?

Well the way it gets to make that a more permanent reality is to increase money supply. Or else, it’s just “forward signalling”.

Well, this dreamed-of 4 trillion of monthly term repos is their way of increasing liquidity (or the supply of money). But note two things.

Repo is temporary. It expires and must be paid back at the end of a month or 3 months.

Repo needs ‘good’ collateral i.e. government securities. It does not address the bad loans out there that are in trouble.

How ‘good’ money will help ‘bad’ money will need magic. That’s wall street’s craft.

I agree with you. Repo is temporary – but, it must be rolled over every night, or 14 days, or 30 days, or whatever, for as long as it takes to…

Agreed, Fed repo lending (by its nature short term) looks like a bridging technique…not a long term intervention/solution.

Essentially designed to meet short term liquidity needs of US financial intermediaries, corporates, and…hedgies (borrowing short to lend levered long – no risk there…).

So if traditional lenders into repo (TBTF banks) exit en masse, then Fed has to intervene so that lack of daily liquidity does not cause the economy to seize up.

But why are TBTF bank screaming for the exits of Repo mkt?

Well, TBTF can’t quickly exit their internal loan books if they are going bad…corps don’t allow their loans to be called at will by TBTF.

But…repo loans are constantly maturing, so if TBTF want to conserve capital (because their own internal loan books are turning to mush) TBTF simply stop perpetually re-lending into repo mkt.

In a way, repo mkts are a way for TBTF to monetize their excess reserves…but now TBTF need those excess reserves to cover pending loan losses.

Just a theory…

Fed: it’s a small plumbing problem.

Banks: I don’t care to lend more. I can’t take more junk.

Friday the 13th.

Tomorrow, the Desk will further offer $500 billion in a three-month repo operation and $500 billion in a one-month repo operation for same day settlement.

Offer is not equal to submitted.

Let’s see.

Your first graph (S&P 500) should be done on a log scale. As is, less meaningful.

Log scale charts are garbage for financial purposes.

Wolf,

Not entirely clear on your statement (although log charts do take an effort to interpret correctly).

The problem with non-log charts is that they give a very misleading impression in percentage change terms (which is what investors care about…annual pct returns).

A good example…all the thousands and thousands of losses in indices lately…really only unwind the mkts way, way back to the misty, antediluvian days of…what, Oct 2017?

The huge point losses are only properly understood in the context of percentage changes, both current and historical.

Log charts reflect that (although most people are not used to interpreting them).

I’m not really lobbying for their specific use (people don’t “get” them) but periodic tips on the hat to percentage changes are useful.

“The problem with non-log charts is that they give a very misleading impression in percentage change terms (which is what investors care about…annual pct returns).”

Yes, you got what I was saying. Log charts, for investors, are simply a massive distortion of reality.

If, as an investor, you want to know what you money did on an annual basis, you use a %-change chart. That will tell you without distortion. And you use a regular chart for trends and total amounts.

I use %-change figures and charts a lot for that reason. For example, in my next article on the market, which will be out later today, you will see my standard daily %-change chart of the S&P 500. I also indicated the %-drop in the chart above.

So let me be first and say that we are heading into a “Plague Economy “, or Pandemic Economy. Not quite yet a Zombie Apocalypse but potentially headed there in the worst case scenario.

With the awful delays in ramping up test kit production, White House blinders full on, it is certain that COVID-19 will explode in this country.

The US service and consumer economies are already taking huge hits as entire major sports seasons and tournaments get canceled or postponed, schools closed, major movie releases postponed, travel plans are canceled and social isolation becomes the new way of life.

Workers are getting furloughed and laid off. They will soon become bankrupt

Throw in the Saudi Russia war on oil prices and the US shale fracking industry is fracked. There’s a long list of banks with excess exposure to loans from the shale industry, Bank of Oklahoma at the top of the list. Most of these are smaller banks, and unregulated by Dodd Franks capital requirements. Banks be failing soon

The list of industries that the White House wants to bail out grows every day. This is the white House MMT at work here, socialism for corporations, having already given Corporate America a huge tax cut most of which got blown on stock buybacks.

Democrats want to bail the American people directly with their versionnif MMT.

Either way, or both, it’s gonna be Debt Out The Wazoo at hyperspeed.

The Fed, ad usual wants to solve it all be printing more money. What good is all that money when the underlying service and consumer economy is shrinking and nobody can use it?

Exactly wrong, James.

Also all graphs should start with 0 on y axis. Always. Otherwise it’s an arbitrarily scaled representation of the data that can only serve to mislead.

Totally agree with you on the ”’all graphs should start with zero on the Y axis,” and, with the advent of today’s very superior digital representations, IMHO it should be fairly easy to make the X axis and others also, Z, etc., at least available from zero, though I ”get” what Wolf says about if some graphs do so it would reduce the information to size needing microscope…

So, the answer, for now, is to have at least some of the graphs do so, and then refer back to them.

And, to be sure, this from someone who has watched carefully every ”crash” since 1956, and would like to see that in proper perspective.

Hi Nice report Wolf.

The main lesson here chaps is that you cannot taper a PONZI scheme, Period.

Ah, the most relevant comment I have read here so far. No one wants to admit that it’s just fraud and the ‘system’ needs to be corrected not saved.

That’s the difference between a recession and a depression. A recession can be handled with monetary and fiscal policy. A depression requires structural changes.

The only thing holding the global economy together is the fact that the worker drones keep getting up in the morning and going to work so they can pay their bills. Or at least they used to, before everything started getting locked down.

You can limit withdrawals. Otherwise great comment.

Well, you can taper gvt Ponzi…but it is usually in a bunker, with a small caliber handgun pressed against the temple…

Very Smart Wolf (with a little contagion luck). Heartiest Congrats…PJS

Did you notice. This is essentially operation twist all over again.

As a part of its $60 billion reserve management purchases for the monthly period beginning March 13, 2020 and continuing through April 13, 2020, the Desk will conduct purchases across a range of maturities to roughly match the maturity composition of Treasury securities outstanding. Specifically, the Desk plans to distribute reserve management purchases across eleven sectors, including nominal coupons, bills, Treasury Inflation-Protected Securities, and Floating Rate Notes. The distribution of purchases across sectors will be the same distribution as the Desk uses to reinvest principal payments from the Federal Reserve’s holdings of agency debt and agency MBS in Treasury securities. The first such purchases will begin tomorrow, March 13, 2020.

I told you so weeks ago.

I told you so weeks ago.

And you’ll be reminding us again when the opportunity presents itself next week.

Has anybody noticed that the European banking system is about to detonate? They’ll be lining up at the repo window next. Going to need a bigger waiting room.

No need for a waiting room. We all just work from home now. But I get your point.

England premier league suspended.

Warren Buffett suspended the buffet.

2020, year of the total death of small business. Government-Backed corporations and banks take total control of every aspect of American enterprise.

Liquidity is not a vaccine or anti-viral.

Privileged debt junkies only. You’re too responsible.

Wow.

84 day repo only 17 billion

31 day repo only 24.1 billion

Where’s the beef?

A trillion dollar fiasco.

There is a massive liquidation going on. The next crash will be the bond market, I think the 10-year yields will explode to 2% then 3% in a couple of months. This will happen in parallel with HYG yields exploding even higher. I doubt the feds can fix this.

Also, what happens if someone at the Fed ends up with the Corona?

Yes, no demand for cash. As I suspected in the section above, titled, “But maybe not.”

Liquidation of equities seems to indicate a demand for cash or cash equivalents. Lack of repo demand indicates lack of acceptable collateral? Congress will ask the treasury to fix that. Shazam! Magic bonds/notes/bills.

Lack of repo demand suggests that cause of repo rate spikes is maybe not on the borrower/demand side…maybe the TBTF lender/supply side has exited the repo mkt. Fed just stepped into their shoes to prevent liquidity seize up.

The repo rate is 0.29 pct for 3 months.

That suggests were going to zero (technically 0.125) in the next Fed meeting.

Disaster.

What does everybody think will happen when earnings get revised down?

I think that some commenters suggest the worst is yet to come when companies post grizzly earnings updates over course of 2-3 months.

What’s your view Wolf in terms of that? Would this operation lead to sustained rise in markets today, Monday Tuesday? Or will people realise that the Feds action isn’t really sufficient?

I am in the “earnings going to sink all boats camp but would welcome all views

The corporate news is going to be horrible for months, if not for the rest of the year. There are going to be dividend cuts. Share buybacks are going to get slashed. So far, there have been no mass layoffs at big companies, and that’s a good thing. But people have been asked to take paid and unpaid vacations, etc. This is going to get messy on the corporate end.

I doubt the Fed will be able to drive stock prices higher in this environment. The euphoria is gone. Investors are now trying to protect their wealth. This is a different environment.

Wolf,

In 2009 or so, didn’t MBS’s (or their precursors) get reclassified as “toxic assets”? Are we seeing a pre-buy on the part of the Fed in their allowing these securities to be used as Repo collateral?

I thought the Repo was only to be secured with treasuries?

Yeah, well, “private label” MBS essentially disappeared. Now nearly all MBS are government guaranteed or are actually issued by the government itself (Ginnie Mae), so for holders, they’re about as good as Treasuries in terms of credit risk. That’s why the Fed doesn’t accept private label MBS.

re: “What does everybody think will happen when earnings get revised down?”

At this point, I think downward earnings are baked-in; any upward surprises will trigger price spikes.

Largely agree, the mkt tends to be hair trigger, acting far in advance of definitive earnings changes (especially when mkt has been ZIRP inflated for nearly two decades).

But…it is very, very hard to time a bottom…even with all the losses, index PEs are still only halfway back to non-ZIRP normal…and that is before any earnings have been accurately slashed.

Thanks Wolf – see this is my view, I can’t imagine that they have a sober view of earnings. Even Yardeni , who I follow, currently has earnings in 2020 flat year on year and returning to growth in 2021. Surely we are going to get negative earnings year on year at the very least, perhaps 10-15% ?

California Bob – that’s interesting – what do you base that assumption on, meaning do you think 10-15% drop is baked into prices now?

Maybe the issue is a “emotional” one – we are going to overshoot the way down, and that’s the opportunity for those of us in cash over the coming months

The horse bolted and headed south.

The door was locked by the swirling wind.

The horse stumbled and broke its leg.

We know how this ends.

When algo’s started to dominate the market, many wise folk said just wait until they get told to sell-the drop will be epic.

They weren’t wrong!

It has not been widely circulated, but in the 1929 collapse the president of the NY Fed George Harrison loaned liberally.

Indeed, he exceeded his authority by a factor of six times.

And it did not work.

Mister margin had the real power.

As he does now.

Another severe post-bubble contraction is underway.

In 1929, the leverage was at the retail level, now the leverage is in the corporate and shadow banking system. A totally different power dynamic.

On my chart of the curve back to 1857, the rule is that every inversion has been followed by a recession.

There are some examples where the curve inverted twice.

2007, 1929 and 1873.

And over the past year.

All were great bubbles with much in common including the consequent crash.

The curve seems to see through the details of each bubble.

So do spreads.

And the record has been that at the end of a financial mania, the Fed has no control over the curve or spreads.

Mister Market and Mister Margin do have the power.

It was at the corporate level, not retail in 1929. When the bubble burst, it lead to a wave of corporate defaults in the summer of 1930 which then moved to banking by 1931.

1873 was more like 2008.

The bank failures led to the business defaults. Loans were called in, layoffs, no buyers. The speculation was wide among the middle and working class. Stocks were a spectator sport with buying parlors and investment clubs all over America.

If one takes the companies listed on the exchanges and looked at their assets and liabilities to determine what they were worth and took away the intangibles, how far above the market are stocks currently. In other words, remove speculation inflation.

“Goodwill” listed on the balance sheet – priceless.

Well, if massively overpaying in M and A did not result in some sort of “asset” a lot of CEOs and invt bankers would be in trouble…

The really scary thing is that governments keep much shittier books. No mergers for them, but three guesses if public pension liabilities are accurately funded/projected…

The fed still has the same problem they had in September, repo rates want to rise and the fed can’t afford to let it happen. They need to keep the national debt from getting even worse.

The reason the new facility has not been highly subscribed is probably because, while the fed has captured the “quality” collateral in its repo operation, the not so great collateral(like maybe BBBs) is still on offer and finding a home in the money markets. To stop this the fed will need to change the rules or buy the not so great collateral too. Stay tuned.

To stop this the fed will need to change the rules or buy the not so great collateral too.

Collateral? Who needs collateral? This is an emergency.

Are you sober enough to remember TALF ?

Be patient, it’s coming…

Since when is consumer debt ‘temporary’?

“not so great collateral…” Used bicycles?

Or maybe there is little demand on the repo borrower side, maybe the TBTF repo lenders have all just exited the mkt to deal with their own internal loan book issues…

My understanding is that the same assets can be used as collateral for different loans. So… what could go wrong? They’ll find a way to get the money…

Why do you think the Fed Repo is finished by 8-9AM?

The Wuhan virus is a wrecking ball, and it will be pounding literally everything for some 12 to 18 months – minimum.

So everyone should start reasoning and projecting from there.

Or better, just have a damn strong drink.

Have an idea.All that really matters financially is we spend money.

So instead of the games they are playing give all Americans with

a mortgage 2% for 30 yrs. Will create plenty of cash flow

A rising tide of debt drowns all leaky boats, and there is a tsunami on the horizon.

Has any central bank in history ever built a money-press that includes an off-switch?

Has any central bank in history ever built a money-press that includes an off-switch?

Who needs an off-switch? Just keep cranking it faster and faster until it explodes. That’ll turn it off.

This calls for a Luddite revival.

Historically, the money printing off switch is when the emperor gets decapitated or a shot rings out in the bunker.

1) Yesterday DOW was a bloodbath in hell.

2) People who do what the are told, don’t care.

3) The never fly to San Siro, or visit Rome colosseum,

because it was built 2,000 by slaves.

4) The never heard about the ECB, or $1/4T Fed repo waves.

5) Don’t bother with things beyond control.

6) Yesterday was a very nice sunny day.

7) After work they went to the lake.

8) Down bellow, deep in the lake, Pottesville bank is manna from heaven.

We all need some good news:

Atlanta Fed latest GDPNow growth estimate: +3.1 percent.

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2020 is 3.1 percent on March 6, up from 2.7 percent on March 2. Following data releases by the Institute for Supply Management, the U.S. Bureau of Economic Analysis, the U.S. Bureau of Labor Statistics, and the U.S. Census Bureau, the nowcasts of first-quarter real gross private domestic investment growth and first-quarter real personal consumption expenditures growth increased from 5.2 percent and 2.2 percent, respectively, to 6.1 percent and 2.4 percent, respectively, while the nowcast of first-quarter real government spending growth increased from 1.7 percent to 2.1 percent.”

Unfortunately that was on 6 March.

The next GDPNow update is Tuesday, March 17.

I’m beginning to panic as I can’t remember where I put my rose-coloured reading glasses.

It’s possible that the Fed may have first used the 50 basis point reduction to aide the margin carry rate. When the market tanked on Thursday Bloomberg stated that the selling was caused by “investors” not being able to meet their margin calls. Is it possible that third party repos ie. JP Morgan etc. were loaning hedge funds cash by putting up their own treasuries etc. for the cash? If so, what kind of collateral were they taking in? Would they even take that kind of risk?

Look at weekly transaction of dealers below.

The “Others” are the funds they trade with.

USMCA : Wuhan 19 suspended Canada parliament and US congress.

Political campaigns are suspended for candidates > 70Y old.

Nov election delayed.

Nov election delayed.

Elections? Who needs elections? You’ve got a Stable Genius who has everything “totally under control”. Best ever. Just get out of his way and he’ll get everything fixed. So to speak.

Uh… whaddabout the PEOPLE, the huddled masses, tempest-tost cowering in self-quarantine? Where, what is their relief? Cash stimulus in their hands immediately refloats the economy, maybe staving off even deeper, predictable disasters.

whaddabout the PEOPLE, the huddled masses, tempest-tost cowering in self-quarantine?

Those are non-performing assets. What do you think they do with non-performing assets?

Unfortunately the helicopters have been grounded until at least 1 May. Sorry.

Hey Wolf, I can’t help but recall Cougar_W on Zerohedge in “12 with the Feds latest actions. I know some here have read his comment, for those who have not here you go…

“These XXX are going to print hard enough to wake the dead. They’ll print like XXX, print like mad men, print like fly pimps. Print until their eyes bleed.

They will print via the swaps, via bank bailouts and mergers, via fixed Treasury yields, via real honest-to-God negative interest rates, via loans to banks on no collateral, via payroll tax reductions, and in the end via actual fiat paper instruments which they might very well drop in bails from actual XXX helicopters.

They will not give two figs what anyone thinks.

Here is why.

Because this is the Goddamned end of it my friend. There is no accounting beyond this point. There will be no history of it. No one to take notes of rates of exchange, or of the graft and violence, nobody to worry about the deficit or the GDP or the national debt of any nation large or small under the blazing XXX sun.

End. Of. It. Does anyone bitch about how Rome totally debased their coinage at the end? Hell no. But whoever did it had enough to hand and grabbed some land with a nice vineyard and sat back and waited for the Middle Ages to start 700 years further on.

And that’s what a singularity is about. Anything that passes through is striped of all meaning. Nothing we think is important now will remain so beyond the event horizon. Nobody will remember, nobody will write about it, nobody will be held to any standard. Ever for evar.

So yeah, they’ll print like the mad XXX. Because they have nothing to lose, and maybe something to gain. Maybe a dollar. Maybe a day. Maybe a slim chance to escape with some of the loot. Whatever XXX advantage they see in it, for themselves and their elite crap wanking buddies, they will full-on-full-time-XXX do it to advantage.

Watch for it, Dawg. It’s totally on this time, on like Donkey Kong. And when the dust is settled in a generation hence it’s going to have become another unbelievable episode among the ages of men.” (Cougar_W, Zero Hedge, 2012)

I replaced the language that is inappropriate here with “XXX.”

Also, though I can understand the anger, many of the important parts of this comment are just plain garbage, including most of the things classified as “printing” that are in fact not “printing.”

I don’t think he meant every point to be taken literally, but he does convey with a colorful turn of phrase, pretty much exactly the situation we find ourselves in with the Fed’s relentless expansionary monetary policy.

Thanks for all the insights I get from this page.

Just think. Jerry holds down his computer’s zero key for only an extra second — $4000000000000 — and then a US (or foreign) bank, or a corporation or a nation can “buy” 4 trillion “dollars” worth of real, Real, REAL, REAL! goods, services, gold, land, etc. etc. etc.! “The Fed” could LITERALLY buy the world!!

As long as the US military is used, as it has been for literally decades, to literally force the rest of the world to accept these trillions or quadrillions of US “dollars” in payment for their REAL everything, the US’s Big Steal can, and will, go on literally forever!

Hey, this economy thing is so, so simple!

Just in case you have not noticed.

Weekly Primary Dealer reports for 3/4 (that’s the latest out there, ok)

Transactions As of Date 3/4/2020

Inter-Dealer Brokers 384,644

Others 640,814

Total in millions 1,025,458

This was for 3/4 and it’s the largest (at least since 2019 when I started recording it.) It’s already above a trillion even before the Fed bazooka.

Can you imagine what it is now 3/13. I will keep track of this.

Must comment on how poorly the FED has conducted policy. After rate normalization failed, balance sheet reduction failed, REPO was applied in excess, and when they pulled back the market topped. In a world where Fed policy was appropriate, or consistent, the virus would have been a sidebar. The US is the least well prepared to handle Covid, because our financial system is in disarray. Powell Fed has no policy on the dollar, or fiscal spending. It seems obvious he only cuts rates to confirm the mantra that high asset valuations are a reasonable goal while traditional policy tools are not needed. At this moment in time someone needs to be brought in from outside, someone with credibility. Other than that happening wait for the inauguration.

At this moment in time someone needs to be brought in from outside, someone with credibility.

That’s been done. He took a good look and walked away, giggling hysterically.

Unamused:

Not good! I’m starting to like you!

Ha-Ha!

ROCHE from Switzerland.

Ahh follow the money …

The markets can tank but guess who is paying a LOT LESS in Interest?

Looks like a good time to launch the 20 year bond.

The smoke will clear one day.

With Treasury/HY spreads widening, who is going to buy T bonds?? After the Fed REPO flop they are going to reach deeper and reset the dollar. That would boost stocks and gold. Foreign money seems to be where this market is bleeding. Fed controls the NYSE during trading hours. After a dollar reset the US economy will gain new export markets and rates would rise. Such a move would be disruptive, but when markets are pushing slowly in that direction it’s often better to jump ahead to the end game.

The Fed will buy T’s. Q.E. special.

What are the objectives of this QE? Lower interest rates? Already there. Monetize government bond auctions? What is the money going for? Swap MBS for Treasuries? The problem this time around is not mortgage paper, its the ability of consumers to pay their debts. Direct fiscal consumer aid will address that. The political lines are drawn, we aren’t going to throw endless money at the banks. This is one reason Powell is using triple REPO, he knows QE is a hard sell. After abdicating on fiscal policy, he would have to eat a lot of crow.

Yep, holding the fiat dollar is a lot like playing Monopoly with a sociopath.

4.5T with a capital T…I guess that’s why we don’t have money for anything else the regular joe might want…Medicare for all, free or lower tuition, proper pay leaves…etc.

4.5T?

That is a paltry $13,846 for every man, woman and baby in the Un-ited States.

Or, since “There were 152,186,000 jobs in the US in January 2020 according to the CES survey of employers.”, that’s $29,569 per job.

There seems to be something wrong with this picture.

1) The Fed was born in 1913 with “Real Goods” 90 days consignment promissory notes, as assets.

2) After WWI president Wilson cleansed “Real Goods” assets

and rotated Fed assets with illegal UST.

3) NY Fed Strong signed a secret handkerchief pact with BOE

Montagu Norman to put mighty Germany in a leash.

4) Ben Strong got his virus in 1916.

5) He died from tuberculosis in Oct 1918, a year before his

created bubble crashed.

6) Killing “Real Goods” killed US industries in the 1930’s.

7) Mfg have lost their mean to pay workers.

8) US mfg had to borrow from the banks.

9) Gov have no limits to their borrowing, but mfg have. There isn’t

a fair competition between mfg and gov borrowing. When US mfg got x8 red cards, the 1930’s depression had no end..

10) Source : Antal Fekete who escaped Nazi Germany.

$4.5T would pay off a whole lot of debt, rent, mortgage payments and other expenses for the common folk who are going to be suffering as result of the economic shutting-down caused by the Covid-19 pandemic. @Fed: Where’s our bailout, assholes?

The Fed and Treasury has forgot us.

When Congress authorized IOER, they stipulated that the Fed can pay bank reserves interest but not above what Treasuries will pay PEOPLE.

Today IOER is 1.1%.

But the 28 day T Bill (last auction) non-compete rate is only about 0.4%

Term: 4-Week

High Rate: 0.395%

Investment Rate*: 0.401%

Price: $99.969278

CUSIP: 9127962B4

Every T bill auction yield has dropped by more than 1% from the last 2 weeks. You can see the amounts invested in Treasury Direct DROPPED. Meaning the ordinary people bought LESS (I guess they put the money in toilet paper instead).

Hey Powell, we also have to eat!

You can eat cake. It’s a tradition.

A more likely reason that ordinary people bought less .4% t-bills is beacuse they prefer an FDIC insured rate if 1.5%+ at online banks (capital one, CIT, Ally).

“Capitalism” at is finest!

Wake me up when this whole corrupt system has collapsed (6 months?)

“Capitalism” ain’t the one printing money and defrauding savers for two decades.

That’s the G – which has been purchasing political status quo careerism at the cost of every citizen’s accumulated (post tax) savings.

DC could have confronted the US’ productive inferiority vis a vis China two decades ago…but it was easier, cheaper, and sneakier just to continually hit the big green print button and paper over the cancer.

Wall Street got it’s welfare Ka-Ching from the Fed. Are corporate bailouts on the way?

“WASHINGTON (Reuters) – United Airlines confirmed Friday it is in talks with U.S. government officials about possible financial assistance in the middle of a dramatic falloff in travel demand due to the coronavirus outbreak.”

3: 22PM and still no Trump. Must not have good news to tell otherwise you’d think he’d want to get it out while markets are open

apparently you are in the wrong time zone…

in spite of my dislike of djt, imho he did a good job on his presser that i just turned away from

the experts, including private company CEO types as well as MDs, etc appear to have developed a good program for We the People…

as always,,, time will tell

Maybe entrusting our money issuance to a criminal private banking cartel wasn’t such a hot idea.

All the “sophisticated” demented program plans implemented by the FED/Treasury/Gov won’t be worth a fig when families can’t feed their children.

That’s when the blood begins to flow in the streets!

This is not a game for Keerisakes!

Millions of lives are at stake….both economic and health wise now.

We’ve had a bunch of sequential clowns running our government(s) and since it felt so nice we didn’t pay attention (not all but too many).

What we see today is a result of greed, apathy, corruption, a cult of “individualism”, and just plain bunch of crooks running this country.

This is no game.