Low Tier Skyrockets. Super-Luxury in Trouble. Condo, High-Tier House Prices Stall Since mid-2018.

By Wolf Richter for WOLF STREET.

The Los Angeles metro housing market has some of the most expensive properties in the US. They’re listed at aspirational prices, and they sell for a lot less, years after having been first listed. The most expensive home on the market, according to Redfin, is this 20-bedroom 19-bath on 67 Beverly Park Ct in Beverly Hills that took years to build. It lists for $165 million, and the developer apparently hasn’t sold it yet:

Then there’s the reality of the deals that are actually being made, for example, as pointed out by Curbed Los Angeles:

It’s been a rough year for luxury properties. The Bel Air mansion that was once the nation’s priciest listing at $250 million sold in October for a mere $94 million, and a vast hilltop property once listed for $1 billion sold at auction for $100,000 in August.

Deals are eventually made, including a sale that broke the price record in California last December, when Rupert Murdoch’s son Lachlan Murdoch forked over about $150 million for the Chartwell Estate, which had originally been listed for $350 million.

But the housing market is not dominated by the super-hyper-stratospheric-end. It’s dominated by the bulge around the middle and below the middle. And there is now a discrepancy forming in how demand and lack of affordability are carving up the Los Angeles market.

Yesterday, I reported on The Most Splendid Housing Bubbles in America, based on the Case-Shiller Home Price Index data. It included the index for the Los Angeles metro, the market in the 20-City Case-Shiller Index that has experienced the most house-price inflation since the year 2000, with prices having inflated by 190% over the 20-year period.

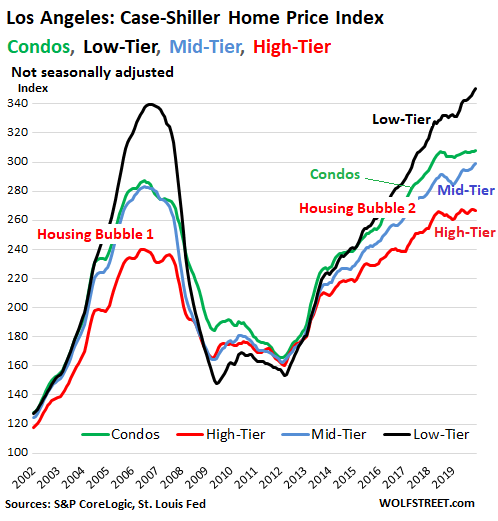

Today we’re diving into the price layers of the index, and into the condo price index, which the Case-Shiller Index also provides for Los Angeles (data via St. Louis Fed’s FRED database): Turns out, at the “low tier,” meaning the bottom third, prices have surged ginormously and continue to surge, but the “high tier,” meaning the top third, and the condo market have hit rough waters.

The 18-year chart below shows Housing Bubble 1 and Housing Bubble 2, with the three price tiers for houses, and with condos. The index value at the top of 350 means that at this point, prices increased 250% since 2000.

- Black line: low-tier house price index (bottom third of sales prices) skyrocketed 240% in six years from 2000 to 2006, then plunged 56%, then skyrocketed again, now up 250% from 2000. Home-price inflation at its grandest.

- Red line: high-tier house price index (top third of prices) surged 140% over the six years from 2000 to 2006, then dropped 31%, and then resurged and is currently up 166% since 2000.

- Green line: condo index (all condo prices combined) surged 183% from 2000 to 2006, then plunged 42%, and re-surged, and is now up 207% from 2000.

In other words, the low-tier prices do the most skyrocketing and the most plunging.

Now the details.

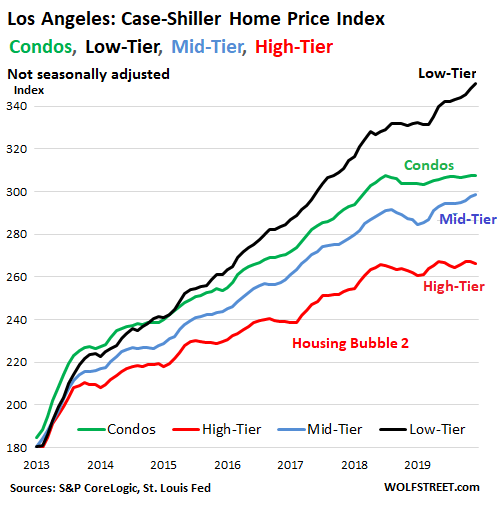

The chart below shows the price movements of the same four indices since January 2013, when they all had an index value of around 180, meaning that prices have risen about 80% since 2000 across the board.

But since July 2018, prices in the low-tier (black) have surged nearly 7% while prices at the high-tier (red) and condo prices (green) have stalled, wobbling but going nowhere, with no change in price since July 2018:

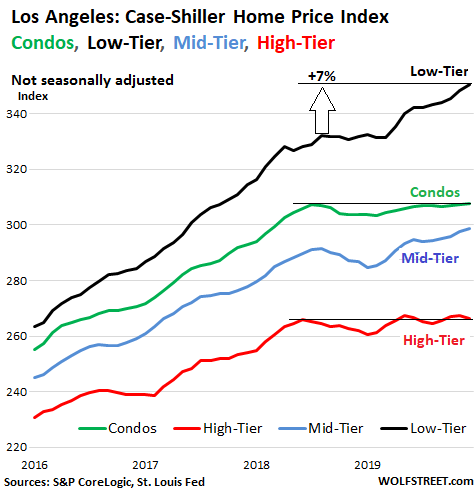

This divergence is even clearer in the chart below, going back to 2016. Note the dip in prices after July 2018 of condos, mid-tier houses, and high-tier houses, but there was no discernible dip in the low tier:

Obviously, this “low tier” that is currently so hot in the Los Angeles metro is not the playground for “low-income” households. Those houses are still expensive, and their prices have outrun wages for years by a big margin. They’re just in the lower third of the spectrum, and the whole spectrum has moved up.

What is happening is that as incomes cannot keep up with this type of blistering house-price inflation, buyers are stepping down the ladder, based on what they can (barely) afford. And this creates massive demand at the low tier, which drives up prices further, while demand has fizzled at the high tier.

And condos face another dynamic: An onslaught of supply, the result of a construction boom, including new condo towers in central Los Angeles. Nearly all of this new supply is high-end, because that’s where the money is, given the expense of new construction in Los Angeles. But that’s not where the market is, and prices run into resistance.

So in aggregate, house prices in the Los Angeles metro look to be on an upward trajectory. But by layer, it’s the bottom third where prices are skyrocketing, and it’s at the top third where prices are stalling. And prices are also stalling in the condo market.

Prices in San Francisco Bay Area, Seattle, Chicago, New York at early-2018 levels. But Phoenix, Tampa, Charlotte show surging house-price inflation. Read… The Most Splendid Housing Bubbles in America, Feb. Update

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The spread between high and low shows that speculation is still in operation and flippers are still working on new kitchens.

I’m not buying it. But I may eventually buy someplace at a discount with a new kitchen just like I may buy an old car that’s already been fixed up.

I’ll wait.

A friend was talking about selling her house and the realtors claim they have “investors lined up ready to buy” which is the opposite of what home ownership was supposed to be.

Houses were supposed to be where families grew up and now it’s just another financial asset for the rich to bid up to nose bleed levels……and force everyone else into renting…….with 4 other roommates

“a vast hilltop property once listed for $1 billion sold at auction for $100,000 in August”

You need to post a warning sign before sentences such as these.

As Theoden (King of Rohan) said….”how did it come to this”…rhetorical question in this case.

It was purchased by its lender for $100k, but it had $200 million in debt associated with it.

It’s a fascinating story, Merv Griffin once owned it was also owned by the sister of the Shah of Iran.

Would property tax see it as a 100k house or a 200 million + 100k house?

Anybody wanna imagine what a LA median household income chart would look like overlaid on these charts.

cas127,

I don’t have what you’re asking for, but something similar, from a prior article some time ago: this is the percentage increase in median house price in LA (adjusted for inflation) v. percentage increase in median household income in LA (adjusted for inflation)

https://wolfstreet.com/2019/07/12/changes-in-house-prices-rents-and-household-incomes-since-1960-in-the-us-by-region-and-major-metro/

Wolf,

Thank you.

That seems about right…and sustainable…

The scary thing is that the Fed/DC have to know all this…and likely knew it half way through bubble 1.0.

But apparently (it has been 17 yrs) they have no other cards to play (beyond ZIRP/NIRP) and are shit out of ideas.

Interesting to note that the madness started right about when US left gold std.

Could make a case that US RE became the oblique backing of the fiat dollar…USD might be continually diluted, subject to ZIRP, and there is much less to buy from de-industrialized US, but you can always use your export generated Disney Dollars to buy US RE (major exporting nations frequently being land starved).

But apparently (it has been 17 yrs) they have no other cards to play (beyond ZIRP/NIRP) and are shit out of ideas.

My kingdom for an edit button.

Cas127:

It appears to me anyway that the C. virus is/has saved the FED from itself……..

Oops, that’s nasty from Sam Sixpack’s point of view. I have understood that property taxation is quite nasty when you buy a property in the big cities over there in CA, too.

This chart is a good start Wolf, but does not explain why the apt I rented in Berkeley for $50 in 68-70 is now $2500 or 50x, nor why the apt building I estimated in West L.A. in late 17 was being built on the assumption that rents for 300 SF studios would be $5-6K depending on the ”view.”

And, BTW, that one and another in a lower rent district were both canceled by Chinese owner/developers.

At this point, IMO, these increases are most dependent on the devaluation of the USD as suggested, but what about the similar points brought up by the comments from Netherlands? Does this imply that ALL currencies have been similarly debased?

Socaljim: No bubble here!!!! Keep buying please

The median price of a home in LA is between $600,000 and $650,000 according to two reports. There may be discrepancies between asking prices and sales prices.

The median price of a home in Arkansas is close to $130,000. Oklahoma is also cheap.

But the cullllllture.

Actually, post interest, the total amount paid on a mortgage might be 2 or 2.5 times the original amount borrowed.

Ignoring DP (which is a major problem in itself), the AR/OK/40 other states…house will cost 260k, the LA one…1.25 mil.

And yet the Fed will slaughter every saver in existence to prop up NY/DC/CA delusions.

LA County prices differ from LA City prices..

Some Californians seemed to think everyone is rich. Far from Hollywood Hills is Pine Bluff, AR.

Check out home prices there.

California has the highest poverty rate of any state in the nation, they don’t need to look at Arkansas

California has the highest poverty rate in the nation. With census data. Post govt transfers

I said I would like to see an analysis of housing affordability, and by golly, I got it. Thanks.

And boy is it ugly. Angelenos are screwed, and it’s not even the worst. It’s way down the list on wallethub.

Nearly all of this new supply is high-end, because that’s where the money is, given the expense of new construction in Los Angeles. But that’s not where the market is, and prices run into resistance.

Which just goes to show that no matter how bad things may be, they can always get worse. Maybe the builders will stay solvent. Maybe not.

Still to come: viral pandemic and water shortages.

The good news is that the DJIA dropped only 123 today. And to think that some people insist that there is no such thing as progress.

Don’t forget earthquakes that can take out hundreds of thousands of homes in one go.

Helluva sunshine tax.

Earthquakes cause less damage on an annual basis than floods in the mid-west, hurricanes on the east and gulf coasts, tornadoes anywhere, and other weather related “disasters” around the States. My family has been in Southern California for over 60 years, been thru all the major quakes in that time and, other than broken glass, the only major damage has been loss of a brick chimney. I’ll gladly pay that sunshine tax, and I’ve been through all of the above named disasters in the other States and countries I’ve lived in. California is still a fantastic place to live if you can afford it.

“if you can afford it”

So is Manhattan…but if you make the median income…it means living in a broom closet with two roommates.

If you bought into CA RE decades ago, by definition you are not confronting the same financial equation that today’s buyers are…in fact, you are on the exact opposite of the trade. What is very lucrative for you is extremely expensive for a putative buyer.

And as for earthquakes plenty of CA residents have been unaffected…but hundreds of thousands have not been unaffected.

Do you go naked on earthquake insurance?

Does CA *allow* Commercial RE to go naked on earthquake insurance…I know the building codes are mandatory…

You need to add “ if you can afford it “and if you don’t have a awful commute

That wasn’t a drop That was the “ Deadcat bounce” every buy the dipper was waiting for

And what about those HGTV home buying shows. Are these plainly just entertainment, or is there any ‘truth’ the seemingly unlimited ‘madness’ presented to the viewers?

As a long time investment RE investor (not in CA, but did live there 18 years), all the Flipper shows leave out the commissions that have to be paid and they get lots of remodel materials donated or super cheap. Flipping, by definition, is a short term play. High risk and high reward, but like VC investments, less than 25% actually make money.

If it’s on the boob tube I very much doubt that there’s much truth to any of it

Ours for a long time was a B&W console. The old man called it “The Mahogany Shrine”. Tube tester days.

I believe the 2017 tax law limiting the deduction of state income and property taxes to $10k and only allowing interest on a mortgage of up to $750k is a big reason for the higher end stall in price appreciation and the reduced spread between high and low end.

Excellent point.

DJT – anti-RE speculator crusader…

Meant to write “…only allowing interest on a mortgage of up to $750 to be deducted…”

Super-luxury in trouble? I wonder how much (in percentage) of the net worth of the super rich is stuck in houses. I am not sure they care that much. Maybe the builder or developer are the ones in trouble.

Eskimos Quinn here. I am a young Inuit, trying to get ahead, who lives in the capital city of Iqaluit in Nunavut.

We too have sky high igloo prices due to a shortage of land. Besides high property taxes, the city even taxes the snow we use to build our igloos with!

I thought about moving to a cheaper Hamlet like Igloolik or Kugluktuk, but they aren’t any cheaper. Besides there are no jobs there for young Inuit like me who only know how to code. Internet connections are frozen most of the time, up here, due to the cold.

Igloos up here have become so unaffordable, I have become homeless and have been forced to just dig a hole in a snow bank and hope the city doesn’t find and evict me. I also worry polar bears will find me too.

I was thinking maybe I should move to SF since I am homeless too. I can code. I hear SF even has good internet too.

SF seems to like homeless people, unlike up here where they pass laws against homelessness. It would be really nice to have some warm company, as it is pretty lonely and cold up here.

Do you think they would let me build an igloo in SF?

Does a (polar) bear poop on a SF thoroughfare?

Cas127:. Polar bears only poop where it is legal to do so in SF, on the sidewalks!

WES,

The City of San Francisco, seeing the problem of attracting homeless people from up north, made snow illegal and banished it. This happened quite a while ago. It was fairly successful. Since then, snow has essentially disappeared from the City, though there is a black market for it, and occasionally people try to grow their own in their freezers, but not enough quantity to build an igloo with. So most homeless people here use tents or just blankets and cardboard, or similar. It also works pretty well. But homeless tents can be legally confiscated by the City, in which case the city is legally obligated to offer the now tentless person a bed in a shelter, such as in an igloo, but since igloos have disappeared because snow has been made illegal, the whole thing has turned into kind of a convoluted mess.

I really love this site.

Bravo!

Wolf: Does Case Shiller cover the entire LA county or just the City boundaries?

City Boundary lines:

http://www.arcgis.com/home/webmap/viewer.html?url=https://services1.arcgis.com/p84PN4WZvOWzi2j2/ArcGIS/rest/services/CityBoundary/FeatureServer/0&source=sd

County boundary lines:

Fairly sure that Case Shiller tries to use the MSA multi-county borders but I might be wrong.

Ron,

It covers the entire counties of Los Angeles and Orange.

https://controllerdata.lacity.org/dataset/City-Boundaries-for-Los-Angeles-County/sttr-9nxz

Excellent Post Ron. Most people cannot comprehend just how large the City of L.A. actually is.

The thing I’m seeing is the sale of houses by folks at retirement age, who take the money and move to a less expensive neighborhood. In many cases that house is their retirement plan.

People who have been in one place in CA rarely move if they’ve managed to stay in one place more than 6 years. And that’s due to the property taxes set by Prop 13. If you bought 20 years ago, sold and used the money to pay cash for a new place of the same value, your tax bill would be more than your old mortgage payment was. There’s no incentive for people to “move up” when wages don’t even keep up with with the taxes. Better to just stay. Heck, even a loan to add a second (or third) story on an existing place is cheaper than moving as the Prop 13 tax restriction can’t keep up with the cost of housing.

Compare that to Seattle (for example) where every year your property tax raises 10-30%. In that town the retirees are selling because they can’t afford the taxes, so they too take the money and run.

If all the sudden you’re neighborhoods getting expensive and grayer it’s just those folks from the coast looking for a place to park for their last 20 years.

At the elevated prices of today, the SFH exit bandwidth is limited…since the bust, only about 400k to 450k homes are sold ea yr in CA as a whole (population 40 million…).

During Bubble 1, the annual volume was about 750k.

People *do* learn…

Adds ons to prop 13 allow passing the tax valuation to children and even grandchildren, and in some instances, they are not living in the homes but renting them. And in SF, there is very onerous zoning that precludes the kind of density in most of the city that demand would dictate. There is no more messed up RE market in the country than SF.

We live in the middle of this. Our area has become a caste system: those in place before 2014 and those that came after.

Density has skyrocketed. We all laughed when developers built tall buildings on our street with two bedrooms at $6,500 to $9,500. Then they all rented. Now there are condos going up behind us that are $3 to $30 million. Units will have their own lap pools and terraces.

Yet we know a neighbor who bought his one-bedroom condo for $120,000 in 2001.

According to Wolf’s chart, anything from 2001 or so and earlier, cost about one-fourth of today’s prices.

What ZIRP hath wrought.

But I’m sure it is safe to assume that 20 yrs from now homes will fetch 16 times 2001 prices…

Of course, you can only ZIRP once if you don’t ever allow rates to rise…and if you allow rates to rise…sales volumes collapse.

aunt paid $18k @5.25 in ‘63, gma similar. I don’t remember the price of my brothers in 70’s but 19%+/- w/ cal vet loan.

thx for serving.

Does anyone pay over %100 of their income for housing.?That is the obvious conclusion if you extrapolate out from the provided graphs. While the answer to this question is obvious, what happens if I change %100 to 50%. There are numerous households paying over %50 of their income for housing , and that is pre tax. And if housing prices continue to rise faster than incomes ,that 50% becomes %60 and more and becomes untenable for many households.

My point is simple . Housing prices can not rise faster than incomes from current prices. And when the inevitable recession happens incomes will stall or fall and housing will move lower

House prices may or may not drop in the future, but a lot of homes in California, especially LA and San Francisco Bay Area are bought with cash (20% maybe?). Income does not matter in this case. People looking to park their money here for safety and security.

Recent price drops and or stabilizing has partially been due to China clampdown on cash leaving the country.

The price inflation in the lower reaches of this housing bubble is reminiscent of Mark Baum’s remarks to the audience at DeutscheBank in the movie version of “The Big Short:”

“…I just know that at the end of the day, average people are the ones that are gonna have to pay for all this, because they always, always do.”

Wondering how much will coronavirus help when it comes to making housing affordable again. The only option when NIMBYs restrict supply is either lower demand or a recession that brings incomes down significantly.

We’ll see how it plays.