Something funny’s happening in NIRP land: long-term yields are rising, negative yields are turning positive, and investors are getting punished for having handed their brains to central banks.

By Wolf Richter for WOLF STREET.

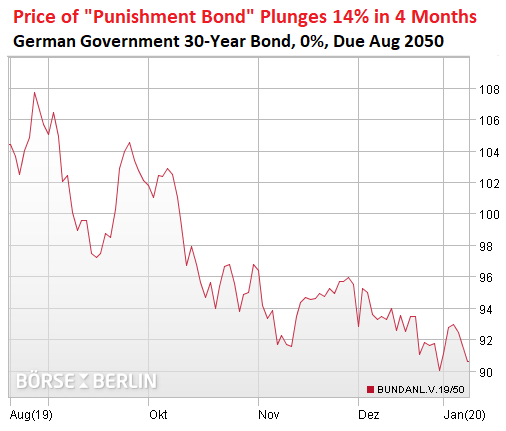

So how much can you lose in a little over four months buying one of the most conservative investments, the German government 30-year bond, during peak-hype of the negative-interest-rate era?

At peak-hype of the negative-interest-rate era, in mid-August 2019, the German government was able to squeak by selling €869 million of 30-year bonds (ISIN DE0001102481) that it had the temerity offer with a 0% coupon, meaning no interest payments ever, and that it was able to sell above face value, giving the bond a negative yield of -0.11% at issuance.

So, as yields fall – become more negative – bond prices rise. That’s the bet for buyers of these things. And this is what happened for a few days in August. The bond started trading up, going over 107 cents on the euro at the peak, giving it a negative yield of around -0.20%.

But as yields rise – become less negative or become more positive – prices fall. And this is what happened next. At the end of August, this bond traded at 105.62 cents on the euro, giving it a negative yield of -0.18%. So far so good.

Then a funny thing happened in NIRP land, as well as the US: Despite ECB and Fed rate cuts, long-term yields began to zigzag higher, and bond prices fell.

Now let’s say this upfront with bonds: If this 30-year German government bond, issued in August 2019, goes south in your portfolio, you can always hold it to maturity, because at maturity – in August 2050 – the German government will pay you face value for it.

So, if you bought this bond in August last year, say, at 106 cents on the euro, and you hold it to maturity, you will receive zero interest income over those 30 years; and then in August 2050, the German government will redeem it by paying you face value, namely 100 cents on the euro. You will book a 6% capital loss and zero interest income for 30 years.

In addition, you will experience the loss of purchasing power of the money that was tied up in the bond for 30 years. When the German government credits you this money in the amount of face value of the bond, you will discover that over the span of 30 years, this money has lost much of its purchasing power due to inflation. If inflation over those 30 years averages around the ECB’s target of just under 2%, the loss of purchasing power would amount to about 50%.

But today, we won’t think about inflation. We’ll just focus on the capital loss so far.

Say, you bought the bond at the end of August at 106 cents on the euro. So today, a little over four months later, it closed at 90.592, for a loss of 14.5%.

This bond’s yield is now positive +0.32%. In other words, on this bond, the yield rose a still minuscule 50 basis points, and this translates into a 14.5% capital loss. This is when duration meets negative yields that are ticking up in tiny baby steps into the positive (chart via Börse Berlin):

With positive-yielding bonds, when they’re headed south, holding them to maturity means that you get at least some interest income to help you defray the scourge of inflation. With negative-yielding bonds, it’s a guaranteed loss unless yields go even more negative, say, over the long term, to a negative -100%. And that’s unlikely to happen. That’s why I call these long-duration negative yielding bonds the ultimate “punishment bonds.” They punish you for having surrendered your brain to the central bank.

Every German government bond with a remaining maturity of over 13 years has left NIRP land. There are still plenty German bonds around with negative yields, but medium and longer-term yields are rising as well, with the 10-year yield now at negative -0.216%, up 50 basis points from negative -0.712% on August 28.

And this is happening around the NIRP world:

- The French 10-year yield has turned positive, now at +0.063%, up from negative -0.438% at the end of August.

- The Italian 10-year yield never made it into the negative. It bottomed out at +0.82% at the end of August and has now risen 56 basis points to 1.38%.

- The Spanish 10-year yield almost made it into the negative, to 0.02% at the end of August, and has since risen to 0.45%. Spanish debt with a remaining maturity of slightly longer than 5 years has left NIRP land.

- Japan’s 10-year yield has turned positive at 0.007%, up from a negative -0.284% on August 29.

But it was fun while it lasted – the idea that you could eventually earn a regular income stream by taking out the biggest possible 30-year mortgage with a negative interest rate, or that you could pile up student loans to the max whose negative interest rates would pay for your early retirement! Just imagine the possibilities! So we watch with sadness in our hearts as this era of impossible possibilities is fading.

Folks who hoped the Renminbi would break the dollar hegemony have to be very patient. Read… Status of US Dollar as Global Reserve Currency v. Euro, Yen, Chinese Renminbi, & Others

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Negative bonds make the Argentine 100 year look like a solid investment.

Negative yielding bonds are kinda like a negative carry short trade on the global economy that is forced upon the institutions that are supposed to be the most risk adverse:

But where are The helikopter money Bernanke promised? “The helicopter money are channeled ONLY to The rich

There was the Economic Stimulus Act of 2008. It wasn’t administered by the Fed but the IRS. Most taxpayers got a $600 ‘rebate’ ( couples $1200) from out of the blue) as the Congress realized the bottom was falling out of the economy. Even Social Security recipients got a windfall one time payment.

Interesting to speculate what if, instead of the $163 billion in this stimulus program, it had been supersized to the $700 billion TARP bill passed that fall or the $900 billion plus ARRAS stimulus bill passed in early 2009 it might have prevented the worst of the recession. $600 per taxpayer just wasn’t big enough to matter but sending $2000 or $3000 to each taxpayer might have boosted demand.

NIRP has already managed to bankrupt the European banking system. You can describe it anyway you want, but it’s a suicide trade.

But no Normal person buys bonds at this levels only Not NORMAL and that is centralbanks mainly ECB and some banks for some reason. Buy silver much cheaper than gold.

Cannot understand why people do not buy more silver,,, it has been around for 6000 years compare with fiatmoney 40 years

They don’t accept it as payment at the grocery store. Conducts good though.

Don’t worry, declining ore grades along with inflation ensure a rising price on a long enough timeline, but anyone trying to do things legally would realize they are getting screwed buying precious metals due to the government’s specific capital gains taxes on bullion. Most people don’t want to bother dealing with that.

It’s impossible for cost basis to be determined on cash precious metals transactions.

Then what would you suggest one does, trying to preserve some of his/her hard earned capital?

Do they take Certificates for Tesla or AMazon stock at the grocery? Or Treasury bond coupons? Do u bring the deed of ur mortgage for credit at the grocery? No!? Hmmm. Strange! Then why do people buy such things?

Pity on all the folks who couldn’t be bothered with picking up all the shiny stuff lying on the ground around in 2000 when it was $300 or so, and the went to $1900ish.

Or was it the other way around? U now needed $1900 to by the same shiny rock that cost $300 in 2000.

But, yeah, I can see the hassle. Where are you going to put all that worthless paper when you sell the stupid yellow rock?

Now that is funny!

Sorry for my financial ignorance, but why would ANYONE want to buy a negative yielding Bond? In my less than informed financial paradigm, I could only think of one scenario. Person ‘A’ buys the negative yielding bond for say $100. Then person ‘A’ know there is a greater fool out there (person ‘B’) in TV Land that will buy the negative yielding bond for say $105.

Is this the gist or is there a bit of Voodoo that I am not getting? I suppose this scenario would also make sense if the German Bundesbank or ECB agreed to buy the bond back at over $100? Thoughts?

Banks are required to hold government bonds as part of their safe asset ratios set in Basel III. Just cost of doing business.

ABC,

It really is remarkable how long governments were able to obscure just how much theoretically independent banks are really just extensions of the state – central to economic command and control.

But what with TBTF, huge rqd holdings of gvt bonds printed like TP, and habitual QE – the mask has really come off.

It is going to make it harder and harder to argue against nationalization during the next looming bailout – because, the truth is, the whole damn shebang isn’t so far from being gvt run already – at least at the more macro levels.

It is almost like the TBTF banks are more or less actors paid to provide a front.

Even more obvious that it is all politics now that ECB will make “fighting climate change” one of their prime mandates (FED will follow once they have a Democrat president?). Just like the Dutch climate / energy policy it will probably mean shoveling even more easy money to the biggest polluters and some other well-connected entities, and making life a lot more expensive for ordinary people irrespective of their environmental footprint.

Of course previous ECB policies were also all about politics and not about economics, but more difficult to understand for the general public that misunderstands who is really profiting.

Per my understanding, you are right. A person A buys negative yield bond for say $100 and after some time, the yield becomes more negative then price of the bond you are holding would climb up and thus are able to sell it for say $105.

Jon, still doesn’t make sense: why would I give somebody more than the bond’s face value? I’m getting zero benefit until maturity in the meantime, right?

If the coupon rate of newly issued bond is less than what you are holding, then the bond you are holding goes up in value as it’s original yield ( coupon rate ) is more than what is currently available.

If you have a bond with coupon rate of 5% at face value of $100.

After few months, the govt issue another bond at coupon rate of say 2% then you can sell your bond for say $102 since your bond pays more than what is currently being issued.

Yield/interest-rate/coupon-rate goes down, the existing bond in your hand increases in value.

It’s a suicide trade. You are hoping the bonds hold up better than the bank where you keep your cash. Either way your risk is enormous but you don’t know who will fail first.

It’s like buying a gold eagle coin. Face value is $50 but you pay 30 times that to get one. It doesn’t matter so lang as somebody, some day will pay you more than you paid for it. It’s all about the trade, not the face value of the ‘asset’.

Capital gains my friend. The central banks have all but promised they will buy these bonds from you later at a higher price to fund government spending. Getting paid dividends is for suckers these days – everything going up, up, up, capital gains! Why would anyone care about earning a miserly 1.5% bond yield? You should instead expect 20% bond capital gains.

Central banks are the greater fool and they have an endless supply of currency to make you rich so climb aboard the capital gain train.

Subtract out inflation and financial engineering and the S&P 500 also has a negative yield, but that doesn’t mean it’s not a bargain today, because the price just goes higher every single day. Clarida blabbing again today about continued money printing- says Fed will not relent.

The best economy in history calls for a giant liquidity celebration and the Fed knows how to party. CAPITAL GAINS!!!!!!!!!!!

“says Fed will not relent”

America’s financial Vietnam – the Fed has to destroy the dollar to save the economy.

Three guesses as to how well this is going to work out.

in order to save the financial system it became necessary to destroy the financial system

Just throwing this out there – because I don’t know. But if I thought the Euro would rise 10 percent with respect to the dollar next year – say from 1.15 to 1.27 – then I wouldn’t care about a .05 loss. (This I am sure is true in the reverse – foreign money pouring into our equities and real estate – over inflated as they are)

if you are sure about that you should do a currency trade, not a bond trade …

I wouldn’t be so sure though about euro appreciation. If there is one thing the ECB is extremely good at it is trashing the euro. It has lost over 85% of its value within 20 years of introduction (compared to gold), quite a feat for a new currency from one of the biggest economic areas on the planet.

If I was a gambler, I would bet that the Euro will fall agianst the USA Dollar and the GB Pound over the next few years.

I actually beleiv the GB Pound will rise against the Euro and US Dollar over the next three years.

That’s the gist. But the key to the joke is gold.

Why would anyone buy a “conservative” zero / negative yielding “asset”’ in An attempt to preserve wealth, when they could Instead buy wealth incarnate: Gold?

Especially when the zero / negative interest rates on the bonds are themselves a screaming indicator that things are not well in the financial system?

Everything is being done to head fake the price of gold down, because once gold lets loose, its game over for the manufacturers of fiat currency.

The mAin Achilles heel for the central bankers is that they constantly have to manipulate down the price of gold – the price of which everyone can see has hasn’t moved up with the inflation –

And hope hope hope no one notices that they are forced Daily to put on a fire Sale of precious metals.

The name is Bonds. James Bonds.

Bondage. The name is James Bondage.

Naive question, but is there anything stopping the bond issuer from buying the bonds at market (lower price) and thus lock in their “profit” by not having to pay the face value at the end of the term? Seems like a good way to make money: issue NIR bonds, wait for ’em to go down and buy back to pocket the price differential at some opportunistic time in the future.

William Smith,

Yes, there is something that stops the bond issuer from buying these bonds back at market value: The issuer is not allowed to under the terms of the bond contract and the under the law where the bond was issued.

However, there are some bonds that are “callable,” but that’s written into the contract. Callable bonds usually have higher yields and specified call dates.

And then there is the negotiated (distressed) debt exchange, for example as part of a debt restructuring outside of bankruptcy court. Greece did this to its private sector bondholders in 2012. This amounted to a haircut for the bondholders of around 60% if I remember right.

Wolf, didn’t you mean to say that the issuer MAY not be allowed to buy back its own bonds on the open market under the terms of the bond indenture or under the law where the bond was issued? Quite frankly I never heard of such restrictions. When I managed bond funds years ago, I was always a willing seller to anyone who wanted to overpay me for bonds in my funds. I never asked the sales person covering my account why their buyer was willing to overpay me.

It’s not your responsibility as seller to figure out who the buyer is. So you don’t need to worry about it. It’s the issuer that is not allowed to buy back bonds.

Seems like “don’t buy back your own bonds” leaves a lot of wiggle room. How many issuers have “affiliates” (or simply good friends) who are able to buy up the bonds when they’re cheap? Possibly with wink-and-nod back-channel “considerations” to balance things out?

Considering the Byzantine financial structures used by many large conglomerates, with cross-ownership and cross-listing in multiple markets, can one really be sure it’s not happening already? It wouldn’t be so different from the stock market games described by Jesse Livermore.

Say Joe Bankster owns large stakes in both European and US banks, and persuades the European bank to issue bonds to buy up the US bank’s bonds when they’re at a discount. Meanwhile the US bank then uses the proceeds of its own bond issue to buy up the Euro bonds at a discount! Then they make a horse trade on the side with a mutual friend and everyone profits (except for the original bond investors). Regulators in the individual countries might not notice the overlap, or might be persuaded to ignore it in exchange for future lucrative employment…

Technically, there ARE some scenarios in which even a negative yield is attractive as a long-term investment – because one expects everything else to perform worse. Such as a major market crash with monetary deflation. Especially if you deal in size and don’t want the hassle of zero-yielding cash-stuffed mattresses!

30 years is a long time. Within 30 years one could imagine, say, an acrimonious Eurozone breakup leaving German investors with a ginormous pile of nonperforming southern-European debt, in a political environment where the central banks’ follies have been discredited.

Surely just drawing out your money in cash and holding cash is safer as a starter than negative interest bank accounts and negative yielding bonds.

I think some of these “financial experts” think too much and confuse themselves.

Physical Cash is awfully risky if you’re a retiree who needs $300,000 in the bond portfolio, and tough to arrange for retirement accounts like IRAs and 401Ks in the USA. And it’s flat-out nonstarter for an institution or fund who buys bonds in $Billions.

For everyday use, yes, cash still has plenty of use, and the more the banks push ZIRP/NIRP the more cash will slip out of their grasp…

Cutting rates and bond prices falling, and yields rising. I remember stocks and bonds being bought or correlated with higher prices. Could that happen with stocks? Probably IMO.

If you’re a pension fund and you need to hold $10 billion liquid you’re going to need a really big mattress. You could put it in a bank but you would be better served to find a tall building and dump sacks of cash over the side of the building – counter party risk.

With all the crazy shenanigans and financial opacity in today’s world these guys are too concerned with return of capital to worry about return on capital.

van_down_byriver,

“If you’re a pension fund and you need to hold $10 billion you need to put in a bond ”

That tells you that you would be a mug to put money into a pension fund.

That’s because you’re thinking about individual small retail investors. Think large institutional investors, fund, brokers, banks and add in regulatory requirements.

Technically the only reasons to buy this stuff is to use it as a loan collateral or for a repo operation (especially in the interbank market) or to sell it at a profit down the road to the proverbial greater fool.

Bond markets are starting to escape the ECB control: the ECB focused too much on equities and as a result bond yields have started going everywhere bar where the ECB wants them to go. As a proof while ultra-prime government bond yields were escaping negative zone, euro junk bond yields were sinking lower and are now averaging 2.6% or some similarly silly figure. This means the spread between those 30 years German bonds and euro junk bonds as a whole is now below 230bps. Spread between 10-year Italian and German sovereign bonds is in the 150-160bps range. Typical symptoms of a bond market that’s going out of control due to excessive manipulation.

Bond buyers (I buy to speculate, rarely to hold) such as myself are raking their brains over what the ECB will do next.

Normalization right now is completely off the table, but at the same time the same old doesn’t cut it anymore. With politics all over the Continent sliding into uncertainty if not downright chaos the ECB cannot afford even one quarter of official recession to justify flooding the markets with extra stimulus China-style. In short the female version of Hulk Hogan (one is a terrible pro-wrestler, the other a terrible central banker; both sport the same grotesque orange suntan because they spent far too much time in the spotlight) is trapped: either we get a recession, which will be blamed on her, or the European economy will grow more dysfunctional by the week, which will be blamed on She-Hulk as well.

I expect the jawboning to start very very soon, as usual to be followed by disappointment when whatever the ECB does turns out to be not enough for the crybullies. Now it’s just time to understand when to be greedy while everybody else is fearful… and be quick enough to sell before everybody hits the same button.

Oh boy,….. I just can’t convince myself to somehow rely upon a “fool”, greater or otherwise, to bail me out of a really bad investment.

I equate this to a lot of drunks actually do get home every Sunday morning without killing themselves or someone else, but I’m not gonna even try it.

ZIRP really stands for “Zero Intelligence Regulatory Platitudes”

More seriously… if a central bank really believes it’s home economy will stagnate (10yr note yielding zero) or shrink (10yr yielding negative), they are really saying the tax base of host government (aka their ability to repay debt) is going to stagnate or shrink.

When the government and central bank tell you they cannot repay debts, it’s absurd to call that debt “risk free”. The central bank is telling investors that the debt are junk bonds that “pay in kind” (pay with more debt, not cash).

Who would bet their retirement, or anything important, on junk bonds with PIK (pay in kind) coupons? Someone actually tried to argue speculators are paying **politicians** to keep their money safe.

Holding NIRP bonds is like holding cash. FED shortening duration on its balance sheet is the same thing. Rates may rise when collateral (currency) is downgraded. In countries where yield is double digits the currency is crap. Holding cash during inflationary markets is a losing proposition, you rehypothecate those NIRP bonds, your collateral value is more sound than newer higher yielding bonds, esp UST. It’s all predicated on the value of the Euro vs the dollar, and the outlook for Treasuries vs Corporates. The problem for bonds is the collateralization process, if the Euro keeps it value, you are better off there. Treasuries are toxic.

“Holding NIRP bonds is like holding cash”

Are you serious?

Cash means you have access to it immediately and it is not tied up for 5, 10 or 30 years.

Cash has no risk of loss of capital as a bond has ( think Argentina ).

The Cash will be the same amount as opposed to less with a NIRP of the bond.

The only government bond you might consider to buy would be an inflation linked bond; but even that would be dubious as the government fiddle their CPI and RPI figures.

Assume you have 5bn dollars.. How would you hold that in cash?

You do the same as US and Japanese corporations do: you put them in US Treasuries and to a lesser extent in dollar-denominated investment grade corporate bonds and hold them in a “favorable jurisdiction” such as Belgium, Ireland, Singapore or Malta.

US Treasuries won’t turn negative any time soon and are probably the most liquid asset around.

Then you wait for your home government to give you a tax cut to bring them home. ;-)

Bernanke called T bonds for BIS payments to China to be held as reserves, was “sterilizing” that money, meaning those dollars would NOT feedback into the US economy and cause inflation. The Fed never offloaded its balance sheet, it merely shifted the duration to short term paper, which is more like cash. Treasuries are cash is US financial propaganda boilerplate.

The Greater Fool (GF) method of investment only works when you have more greater fools tomorrow than you have today.

“This bond’s yield is now positive +0.32%. In other words, on this bond, the yield rose a still minuscule 50 basis points, and this translates into a 14.5% capital loss.”

Bear market rally.

The media is just as much to blame for fanning this farce as the CBs. The headlines last year were ridiculous.

Ida, take that thought a step further. The media aren’t just followers. They are paid by their advertisers (and other sponsors!) who WANT to create popular fads, exploiting popular delusions for profit. The article-writers might just be tools but the headline-writers are shills.

So when you see the media all lined up to shill the same dodgy story, you can bet the opposite and profit (or at least avoid loss).

Did you hear about taco bell mangers making 100k?

It takes one guy to earn that income in high CoL area to ensure that everyone else feels shame for being a low income loser. Its magic how mass media works.

Back in the early 80s, I worked as an assistant manager at a very busy Taco Bueno with lots of (part-time) employees. We maangers worked 80-hour weeks, late into the night. It was a tough job. Every dime of that income was earned.

No one is as culpable as the central banks, not even the media. Not even close. It was the central banks that eliminated investment yields, making it impossible to earn real investment income, the media did not do that – Bernanke did that.

Bernanke is now the poster child for the entire destruction of the European banking system.t

Yes, Bernanke was the worst, but had a predecessor. Greenspan cut the rate to 1.52% in December 2001 from 5.74% in January 2001. By December 2003 Greenspan had cut the rate to 0.94%. December 2009 it hit 0.05% by Yellen’s hand. Subsequently little help from Powell. We are all doomed, I say, doomed.

Wolf, beer and wine are now totally inadequate. We require Wolf Street shot glasses. I could be induced to help subsidize the production of same.

I just did not understand at the time the reason that anyone would want to tie up their cash for even 5 years with zero return, let alone negative return.

Not only was there no return on investment (can’t call it an investment really) but there was a chance (maybe little chance with German Bonds) that you lose your capital totally.

I even mentioned on here that with negative interest rates in banks in Switzerland and capital on tax of 0.2% (including bank savings), one was better off, to draw out the cash (in one thousand Swiss Franc Notes = US$1,000) from your bank account and put them in a safe depsoit box that costs $60 dollars a year.

Thank you for this article that makes me feel a bit more sane.

Negative yielding bonds makes under one circumstances: If you there the rates would go even lower or even more negative.

I don’t think anyone keeps the bond for 30 years .

If you think the rates are going to go down in the coming time, buy the bonds now say for $100, sit tight and may be able to sell for $110 or more for example..

You make a good point.

Negative yielding bonds can make a very good investment under only ONE scenarios

a. Long term deflation of prices.

Unfortunately, I have never seen a country with a fiat currency backed by nothing that has had long term deflation.

Moreover If the EU breaks apart ,each country would replace the EURO with their own currency. That would mean that Germany would replace the Euro with the “new “Deutschmark and Italy would replace the Euro with the “new “LIRA .Any bonds currently issued by each country would be backed by that individual country and not by the larger Eurozone. German bonds currently issued in Euros would be converted to bonds issued in “new “Deutschmarks ,which would be backed by the German economy with has relatively little to no fiscal deficits and a relatively large trade surplus.

On the hand if Italy were forced to replace the EURO with the “new”LIRA”, Italian bonds issued in EUROs would be converted to

to bonds issued in “new “LIRAs, which would be backed by the completely irresponsible and dysfunctional Italian government.

In this example negative yielding German bonds would go down slightly, while those bonds issued by Italy would tube.

” You make a good point.

Negative yielding bonds can make a very good investment under only ONE scenarios

a. Long term deflation of prices. ”

Surely you are still better off with real “cash” in a metal box burried in the garden?

As I said above, not if you’re an investment fund with $2,000,000,000, or even Grandma with $200,000 in “cash” in an IRA.

P.S. If I was going to stash valuables in a garden, I wouldn’t use a metal box, either. Metal detectors give thieves a sixth sense… Wouldn’t stash PMs outdoors either except maybe underwater?

Better with gold coins in a box hidden away

The IRS will give you a good sound reaming when you go to sell your gold to get cash to buy food. The government says gold is a collectible, like beanie babies or commemorative plates, they tax gains at 30% and if gold goes up significantly you had better bet there will be a punitive windfall profit tax as well.

The government is basically making wealth/savings preservation illegal – unless you are ultra wealthy and can afford lobbyists to write laws that exclude you from their clutches (start a hedge fund and lower your tax bill to 15% – carried interest!).

@van_down_by_river:

The same applies for withdrawing cash and using it at a later time to buy more than simple food. In much of Europe buying big ticket items with cash is already impossible now (cash transaction limit 300 to 3000 euros), and it won’t be long before a simple 50 Euro banknote will start alarm bells ringing.

Taking money out of the banking system is relatively easy, but putting it to use again in larger amounts without getting nailed for tax fraud or something similar is very difficult, unless indeed you are ultra wealthy and different rules apply.

What happens to Germany’s outstanding Target 2 balances of €830+ billion?

Everybody should be able to see that this balance can never be repaid and will likely keep growing until it evaporates in thin air; authorities just pretend the money is there. In reality this is a huge tax on North-European savers who will pay for it all by devaluation of their savings.

yes, and in case of Euro breakup the current negative yielding Dutch government bonds would be backed by their epic mountain of mortgage debt, for homes that might be under water by the time the 30-year bond matures ;)

1) NR all over the world, in a shakeout of the weak hands

investors, before the downtrend resume and bonds

value will rise again.

2) The US10Y – German10Y = 2.08%. Its shrinking, but still

large enough in a world of low rates or NR. Both are

trending up.

The German 10Y is rising in the last 6M, from (-) 0.743% to

(-) 0.161%, but retreated after reaching from below the

Jan 2016(L) @ (-) 0.204%.

3) All German rates up to 15Y, including 15Y, are underwater.

4) The German 2Y weekly had a selling tail bar last week,

giving us a warning. The 2Y high was still (-) 0.571%.

5) The German 3M had a huge volatile bar last week, the 2020

opening, with even more impressive selling tail bar.

It opened @ (-) 0.801%, hit (-) 0.5% and turned down, half

way.

BCE buy 95 PROCENT of this bond. Not only germans,french too in last 4 years. 5 PROCENT are Banks. Its free digital debt. GAMES WITH NUMBER ZERO.

Amazing article. Thanks. My head is sore from scratching…or thinking about neg bonds, not sure which?

Maybe this is old fashion, but paper purchases are not real to me. land, tools, skills, and health all have value. Neg bonds? Like I said, how could anyone think this is a good idea? Ever. Don’t see it, never will. As for talking my wife into it or explaining why this would be a good investment for my kids, impossible.

Neg bonds? Like I said, how could anyone think this is a good idea?

I explained that in an earlier comment several days ago. Probably not very well. I’ve been busy, and in a hurry.

Maintaining the present BS bull market and preventing a crash requires that interest rates must not only be low but must continue to decrease. Equity speculators are in over their heads and depend on that, for one thing. Aggregate debt must also increase, climate activism must be repressed, and economic reforms must be repressed, all to maintain overconsumption and keep the system moving. These provide cover for the continued bleeding of the real economy by the financial economy. The financial economy must continue to bleed the real economy or crash, which is to say, they must extract more wealth from the real economy than it can actually produce. This will ultimately damage the real economy so it cannot service its debt and will result in a crash anyway.

The article I linked to earlier, above, explains how CBs have painted themselves into a corner. GMTA, I suppose. Since rates cannot go lower you’re now in the end game. I’m sorry I don’t have more time to explain it in a more compelling fashion using tables and charts and graphs: I was going to offer WR such an article to post on this web site, but I don’t have time to summarise several hundred pages of evidence into a compelling argument. But there’s nothing you can do about it anyway except to acquire productive assets ahead of time – as you say, tools and skills and land. Hope for the best, prepare for worst, and maybe that way you can buy yourself some time.

The article I linked to earlier, above, explains how CBs have painted themselves into a corner.

Deleted. Oh well. Good night.

A one-line tease with a link almost always get deleted. Summarize what you want to showcase from the article in two or three paragraphs and then add the link at the bottom.

Okay, good idea for the Govt systems trying to say afloat…Not for individual personal investment.

I have a small rental. My friend/tenant pays me cash and I charge him about 50% of the going local rent rate. We have adopted him into our family as he is alone. His cash pays our taxes on primary residence and taxes on property. It also pays for all liability and replacement insurance. The rental has increased the value of the property at the same time. This ‘value’ is better than ‘interest earned’ on bonds. The property is worth more every year because I bought it long ago in a poor market. This increase is also earning value beyond inflation.

The transaction is all ‘off the books’. It is a hidden investment just like a mattress or box of cash buried in the garden. The rental is something I understand, much more than ones and zeros controlled across the Country by someone else. If I needed more income I would put another small house on the property and do it again, renting only to someone I know. I have hydro in our name and every two months I go and collect for the bill which would allow a bit of a home and health inspection for the elderly tenant, although we usually have a visit weekly because we are friends. If a future tenant turns into a problem, the electricity is in my name so it gets disconnected and we make a visit with some logger friends to move things along.

So, what’re going to do when the banksters and CB shenanigans destroy your money stream or value, thereof?

I have visited accountants. They have assured me that on paper we will never make a profit. Is that any different than what I do? I have paid income taxes deducted at source, with no deductions, for 45 working years. Lots and lots of taxes. I also pay income taxes on my pensions, and other investments while retired. I have done this, as a workingman, while watching ‘operators’ play the deduction game and write-off strategies orchestrated by accountants. Screw it. My way works.

Paulo,

You are OK with this for a while.

However the following is/going to implemented:

There will be a tax on ownership of second homes. A capital Tax.

Landlords/Owners will have to register occupants of houses to local government offices. Failure to do so will be a fine.

Landlords will have to register as landlords with local government offices (obviously a registration fee will be chargeable) and failure to do so will incure fines.

Landlords will then have to have certificates for electrical compliance, gas compliance, smoke alarm compliance etc.

And the biggest crunch; the Tax Office will have access to all this information from the local government office (think databases) and know you have tenants and therefore rent and therefore want the tax on the rental income.

The government is still running after the “little person” as opposed to the corporations and super rich.

That may well be when house prices start to fall as Landlords off load property because they can’t be bothered with the hassle especially as there is no benefit to them as their government state pension will be reduced as a result of rental income.

It all depends on one’s frame of reference. British consols (perpetual bonds) were in existence from 1751 until 2015. You can read about them on Wikipedia, if you are interested. Over the past 30+ years, I have done very well with my bond investments, although I have been in run off mode since 2011. The Fed ruined the bond market for average investors. It doesn’t make sense for investors to buy very low yielding (or negative yielding) bonds unless they want to gamble on a greater fool coming along.

I read somewhere that Fed Brainerd said that Fed should communicate that next time the Fed is going to stay at zero until inflation hits 2% no matter how long that takes. I don’t know about you, but I have a little trouble with that statement.

I guess the greatest fool was found.

Negative interest rate bonds aren’t just bad,

they’re the best option, at times.

If shadow banks are “too large to fail”,

then Congress should ban them altogether,

instead of bailing out the richest among us,

“heads you win, tails we lose” fashion.

The old mantra “Neither a lender nor a borrower be” applies nicely to this insanity.

According to Gundlach, watch double line current presentation, most common people accounts are not yet negative. Only accounts larger than 200,000 euros in Germany are charged and pay negative rates.

I cannot get my mind around negative rates. Gives me a headache.

Tip: watch the double line conference. It’s super.

Are negative yielding bonds any more ridiculous than the vast number of zombie stocks with a negative book value and negative free cash flow , but a super high stock price?

There’s always a sucker born yesterday …

Some other EU countries are getting ready for negative yields on savings accounts, usually above 100.000 euro. But this is irrelevant in the big picture: that 0.1% or so punishment (initially, they may try how low they can go before the guillotines start chopping) is nothing compared to the yearly loss from inflation (Netherlands 2019: 2.6%) and wealth taxes (Netherlands 2019: 1.2-1.7%) on savings accounts.

I have significant savings because I see no safe alternatives at the moment and negative rates would be a headache, but I’m certainly not going to quickly withdraw my money as cash (as a majority of savers says they are going to do according to some polls, when rates go negative). With cash you still have the inflation punishment, plus lots of extra cost because it is getting increasingly difficult in EU to pay cash especially for big ticket items.

There are some other issues too that usually not mentioned but should be considered too, e.g. companies who need to hold significant cash for payments or individuals who hold cash in an incorporated company might cause significant extra cost (less income) for the tax office. There are a lot of unpredictable side effects.

I think that the purpose of negative interest rates is really the start of tax on capital and a way of bailing out the banks.

In the UK and EU Zone, a lot of people are losing their jobs but able to find work but on minimum wage.

This low wage means little or no income tax is payable on it. On top of this, the government is paying out state benefits (housing benefit, income support) in order for the person/family to be able to live.

This results in a government deficit (most western government have had accumulating deficits for years).

I therefore see that the governments in the future will have no option but to charge Tax on Capital like in Switzerland that is generally about 0.3% per annum.

Just about all bonds now have negative real interest rates, after reduction for inflation. When will central banks realize they don’t have the right tools to transfer wealth in an effective productive fashion. Giving money to rich people does nothing for the real economy.

when will people realize that central banks are not interested at all in improving the real economy, but only in maximizing wealth transfer from productive people to the elites?

I just wonder how Wolfie is hangin right now shorting the whole market.

Those margin calls are brutal.

Look, if something moves 0.74% one way or the other, it’s a nothing burger. This is not a leveraged bet. Index goes up 0.74%, I lose 0.74% on my position. Index goes down 0.74% I make 0.74% on my position. What’s the big deal?

Too bad there is no way to collect , but I will be glad to bet anyone that sometime before July4th, the market closes at least %3 lower than on Dec 30,2019

This isn’t negative rates yet but take a look at the recent 30 year Treasury auction (actually 29 years and 10 month reopen).

The high yield was 2.341%. But the low yield was 0.880%.

Who the heck needed the bond badly enough that more than 800 million was bid at such a way out high price?

Something strange is going on.

Negative interest rates do not spur the little people to spend more and save less as the central banker’s supposedly expected!

Negative interest rates tell the little people that something is seriously wrong and they had better spend less and save more because of the increased uncertainty their future holds!

Clearly central bankers are trying to save their system at the expense of the little people producing real wealth.

Central banker’s are clearly the enemy of the little people.

They have always been so.

Yes, and in Europe this is painfully obvious. People are saving MORE despite NIRP/ZIRP and it makes perfect sense, except for bankers and e-con-omists … They will never admit they were wrong and more likely double down by driving rates even lower.

Of course this isn’t about saving the economy at all, it is about extracting the last blood from the middle class and maximizing profits for the global elites.

WES,

From what I can see “The Little People” are not actually able to save anything so negative interst rates will not effect them.

Most are living on a month to month basis in debt in reality.

In the older times (plus 20 years), you might have had little savings but also no debt but had the prospects of knowing one day you would own your house with no mortgage and more than likely have a private pension as well as your state pension.

Prospects of owning your house are diminishing, private pensions will be worth little (if anything) and will probably be taken into consideration by the government in paying you a state pension.

It does affect some of the little people because it allows them to go deep into debt and live way beyond their means, especially with housing. In my country renting can be 2-5x more expensive than “owning” and anyone with income can get a zero-down mortgage at 1.0% or so (fully deductible from income taxes, so effectively more like 0.5%). With no savings available the choice for these little people is easy: take on more housing debt and hope that current political/central banking policies continue to infinity, and all debts will be erased by inflation. And even if inflation fails to wipe out the mortgage debt, if you have no savings what is the risk 30 years from now?

On the other side, if you have savings and no or very little income (like many older people) you are in a terrible situation over here because there is no way to leverage the low rates, but you get taxed from all sides (inflation especially for shelter, wealth taxes, no subsidies or other entitlements).

Also with pensions it varies very much depending on the situation: my private pensions have already proven worthless, but government workers in my country still have gold-plated pensions and there haven’t been any benefit cuts yet thanks to the surging stockmarket. Government can borrow money for less than nothing and so they are giving large groups of government workers (e.g. teachers, healthcare, many more to come) huge pay increases like +10% in 1-2 years. And despite this extremely favorable situation government is raising taxes and cutting certain expenses. If this continues for a bit longer they will own the whole economy – together with a few remaining multinational companies – and the middle class will be completely eliminated.

In Europe there never was a better time to be a government worker, many of them are paper millionaires if you consider just the cash value of their state pensions (and on top of that, many have homes valued at half a million euro’s at least at a very low monthly cost). Even a “refugee” can start over here with a free home that others had to work their whole life for, plus the government will royally cover their other living expenses forever.

Government knows that a lot of little people are profiting along and will keep them in power as long as they can keep the Ponzi going; and so rates will never be allowed to to up.

Negative yielding student loans to empower the scholars?

I’m waiting for other innovations like negative incomes for bankers and politicians; more likely to improve the economy than the current craze of negative rates :)

In some industries, there are negative incomes for Millennials. Many interns work for free to gain experience so they can eventually make a wage.

It is negative, because they have to pay for coffee while working for free. As they say: “Coffee is for closers”

“But it was fun while it lasted – the idea that you could eventually earn a regular income stream by taking out the biggest possible 30-year mortgage with a negative interest rate, or that you could pile up student loans to the max whose negative interest rates would pay for your early retirement! Just imagine the possibilities! So we watch with sadness in our hearts as this era of impossible possibilities is fading.”

Alas, there goes my retirement plan. :-)

I am actually still hoping interest rates skyrocket. ie 6% would be good.

When CDs are making 5% and my mortgage is at 3%, I still may be able to make this retirement scheme work. It did work in the late 70’s and 80’s when FDIC insured CD’s were paying 10-12% and mortgages from the 60’s and early 70’s were at 6%. Why pay off your house when even the safest investments were making more than you were paying on your mortgage.

Dutch students are still lending huge amounts of money at 0.4% for their first home that will automatically appreciate by at least 8% yoy (30-year track record); why bother studying when you can party for a few years, travel the world and retire financially at 25 thanks to the ECB madness?

Of course these students cannot be blamed because it is their only hope to get on the housing ladder; when you officially mention your student debt after getting a degree even in Netherlands it might be impossible to get a mortgage high enough for a decent home ;(

President Bernie means health insurance for all. So retire and let the employed pay the bill.

All money is created out of thin air when banks issue loans. The primary lenders who “buy” bonds don’t lose anything at negative interest rates because the “money” they use to buy the bonds was created out of thin air.