Vancouver has tiny uptick after 14 declines. Toronto dips below July 2017 peak. Victoria ekes out new high. Calgary, Edmonton stuck below oil-boom peaks years ago. Quebec City flat for 6 years. Montreal ticks down from high. Ottawa ekes out new high but remains low.

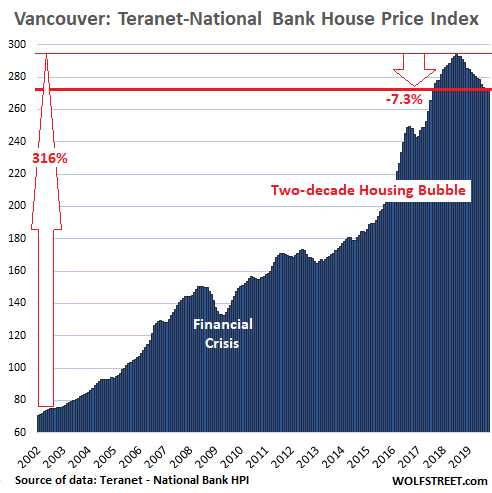

House prices in Greater Vancouver ticked up 0.2% in October from September, the first monthly increase after 14 month-to-month declines in a row. Prices were down 7.3% from the peak last July, and down 6.2% from October last year, and are about where they’d first been in August 2017, according to the Teranet-National Bank National House Price Index.

How big was the bubble that was considered one of the world’s hottest housing bubbles? Over the 16-year boom from January 2002 through the peak in July 2018, house prices in the Vancouver metro had more than quadrupled:

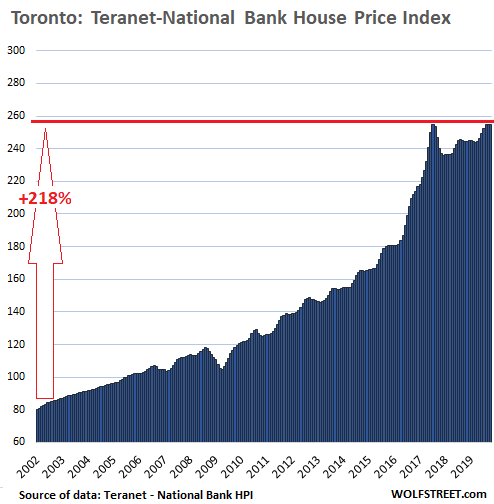

Toronto:

Unlike Vancouver, which had its first month-to-month up-tick after 14 months of declines, house prices in the Greater Toronto Area had their first month-to-month down-tick after six monthly increases in a row. In October, house prices ticked down 0.2% from September and thereby slipped 0.1% below the prior peak in July 2017.

In the GTA, house prices had more than tripled (+218%) since 2002, but that was practically lame compared to Vancouver’s more than quadrupling over the period (+316%). Toronto’s chart and the charts of the other markets below are on the same scale as Vancouver’s chart. This shows the house price changes in each metro in proportion to each other, and you see more white space as we go down the list. It also shows just how diverse Canadian housing markets are.

The Teranet-National Bank House Price Index tracks price changes of single-family houses via “sales pairs”: The price of a house that sold in the current month is compared to the price of the same house when it sold previously, often years ago (methodology). This method eliminates the issues with median prices where changes in the “mix” can skew the index; and it eliminates the issues with average prices, where a few big outliers can skew the index.

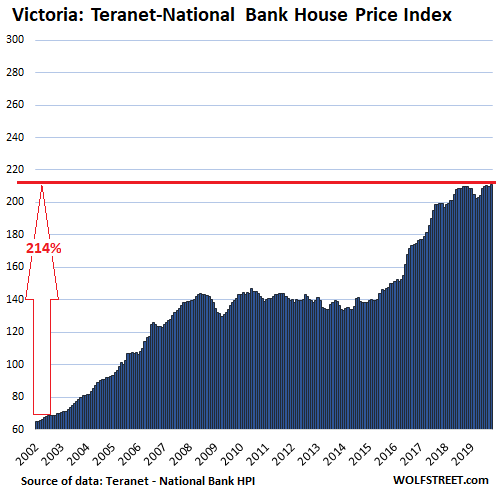

Victoria:

In Victoria, house prices, which have more than tripled since January 2002 (+224%), rose 0.7% in October from September, and reached a new record, but only 0.7% from a year ago, with the index being essentially flat for 13 months with a dip in the middle:

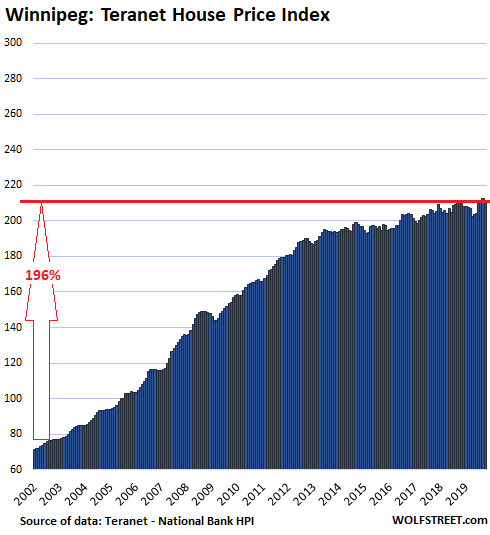

Winnipeg:

House prices in the Winnipeg metro declined 0.4% in October from September and are up just 0.3% from October last year. The index had nearly tripled between 2002 and September 2014, as if Winnipeg was going to run out of land or something. Since 2014, after it was inadvertently discovered that the metro wouldn’t run out of land, the curve has flattened out:

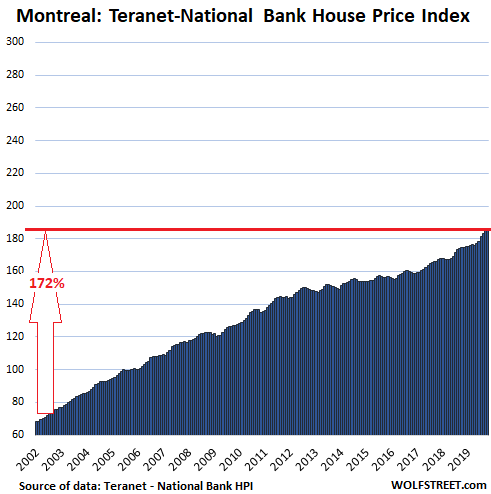

Montreal:

House prices in Montreal inched down 1.0% in October from September, which had been a record, and were up 6.0% year-over-year. The index has risen 172% since 2002, at a steady pace that not even the Financial Crisis could trip up. But the sharper pace of increases earlier this year has now come to a halt:

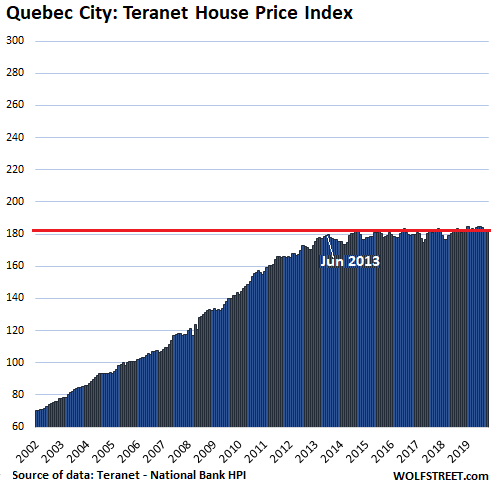

Quebec City:

House prices in the Quebec City metro ticked up 0.1% in October from September but were down 1.1% from the peak in July, and have been essentially flat since June 2013, after a mind-bending jump of 160% in the prior 12 years:

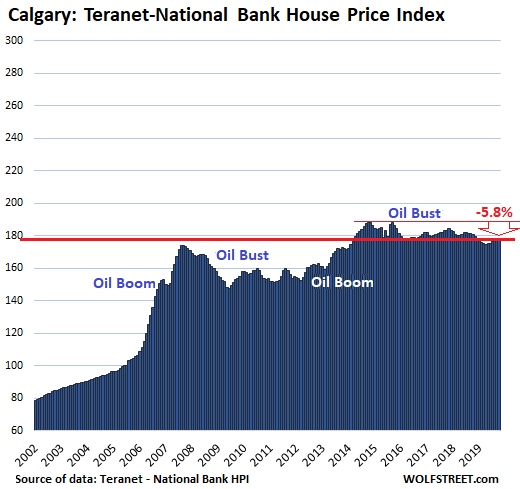

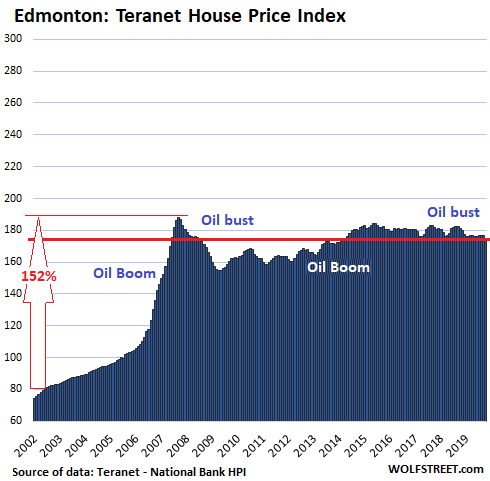

Oil Boom-and-Bust Towns Calgary and Edmonton:

In these two cities, oil booms and busts determine house prices. During oil booms, the housing market goes into party mode, but then the hangovers last many years. Over the two years during the oil boom before the Financial Crisis, the index for Calgary skyrocketed 78% and for Edmonton 87%. Then came the oil bust, which then cycled into a boom, after which came the next bust, namely now.

In Calgary, house prices ticked down 0.1% in October from September, and are down 1.7% from a year ago, and down 5.8% from the peak in October 2014:

In Edmonton, house prices fell 1.0% in October from September and were down 3.4% year-over-year and down 6.9% from the mind-blowing peak in October 2007, which was exactly 12 years ago:

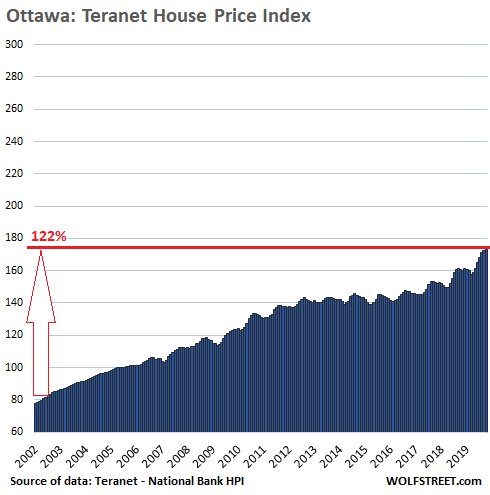

Ottawa:

The house price index for Ottawa ticked up 0.2% in October from September to a new record, and are up 7.7% year-over-year. Since January 2002, the House Price Index has risen 120%, which is a substantial increase by any measure, but compared to Canada’s other housing markets, Ottawa ranks in last place on this list in terms of price gains since 2002:

It’s just house-price inflation

The Teranet-National Bank National House Price Index tracks how many more Canadian dollars it takes to buy the same house over time via its “sales pair” method. When the price of the same house doubles over the years, it’s not because the house doubles in size, or become twice as opulent, but because the purchasing power of the Canadian dollar has declined, and it takes twice as many dollars to buy the same house. This “sales pair” method makes the index, and indices such as CoreLogic Case-Shiller Home Price Index for the US, a measure of local house price inflation, which is what is pictured in the charts above.

Despite startup millionaires, house and condo prices in the San Francisco Bay Area and condo prices in New York City fall from a year ago. Seattle house prices fell again. Los Angeles, Las Vegas lost steam. Phoenix, others ran hot. Read… The Most Splendid Housing Bubbles in America, October Update

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Is it a wonder that the personal bankruptcies have skyrocketed.

Everyone is broke and yet government and workers still want more.

Hence the strikes taking place and adds being bought for more…

Is it just me or does it seem like the Everything Bubble will just. not. go. down… (much). WTF?

It will probably need a major stressor such as major fuel or oil shortage, massive computer and hack freezing some key computer functions or satellites crashing with debris in space or EMP pulse in some area vital to hit electricity or computer servers…

This other way is just adding more paper cuts.

How about the food chain collapsing.

Or watching 10 million climate change refugees die from starvation live in technicolor?

Nah.

The trigger is going to be all in our heads. The chattle are overrun with technology that is triggering more and more destructive delusions. Stuck in a positive feedback loop until everyone just freaks out.

If you think about it in times of war governments have always been able to get the resources they need by either borrowing money or printing money. The next step is citizens paying for it through taxes, financial repression or inflation.

The US has spent a lot on the warfare and welfare state. We all know it’s getting papered over causing a lot of distortion. It’s not so complicated really. Look at Europe. So much leverage added to boost the economy but now that debt service is so high rates must be suppressed so debt payments can be made.

There are certain rules of thumb to investing. One is over performance in an asset class will usually be followed by a period of under performance. Another is the sawtooth pattern of asset valuation which is a long period of increase in asset price followed by rapid decline.

Personally I benefited so far from the bubble in terms of asset prices, but if you estimate future cash flows based on interest and dividends it is probably more of an illusion than real wealth.

Check out VANCITY VANLIFE on YouTube. He (Cruise) and many like him gave up the insane high cost of apartments in Vancouver, BC and other parts of Canada to remodel a large van to live in. He has made a channel out of showing others how to make it happen so they can save money and have a way of building financial freedom as well. It’s worth checking out.

Just what you would expect from central bank money printing.

In 1949 my Grandfather bought a 100 acre farm for $5,500 Cdn.

The original owners had paid $5,500 Cdn in 1899, 50 years earlier!

So land prices didn’t always used to go up!

Perhaps the currency was more stable back then. I am not a currency historian but there was a gold / silver backing back in the day. Price of land does not go up. Our purchasing power does. And then there is cheap money and bubbles.

In central Toronto, the houses on our street sold for about 5000 in about 1913; in 1950 they sold for … about 5000 (in inflated dollars!).

CN Rail reported a slowing Canadian economy. Jobs increased YOY. Jobs decreased in October.

Freezing weather might have slowed some sectors.

Without foreign, mainly Chinese money, prices in Vancouver and Toronto would be less than 1/2 of where they are. Canadian incomes, after payroll taxes, cannot sustain the paper price of the houses in those 2 cities.

Kam,

It isn’t just YVR and TO that feel the impact. It is everywhere when the established cash out, relocate and buy 2-3X the house for 50% of what they just sold for. They pay cash for a new place, and then put the balance in the bank or invest somewhere else; maybe work part time for shits and giggles. And so the bump goes, all the way down the line to even the boonies, where I live. On Vancouver Island we get lots and lots of boomers settling here for retirement, or just relocating from the Prarries or from back east. If you go to Comox airport and watch Westjet or Air Canada deplane, the crowds are oilfield workers coming home for days off. Or, folks just returning home after a visit somewhere cold or buggy.

The Housing Market in Canada is mainly held up by a booming US economy whose benefits crosses our borders and low interest rates. Either of those go, and Canada goes down, along with the US. Also, I don’t think people realize how many young people only buy because of the financial support of their boomer parents. When the Stock Market goes, and it will at some point, those boomer’s won’t be able to help out their kids as much, and that will hurt the housing market, a lot.

First off, boomers are in their 60s and 70s. Not many “young people” have parents that old. Most likely “young people”‘s parents are GenX and even a few Millenials. There are kids in college as I type this who have millenial parents. WHOA!! Mind blown right?

Second, I hate to break the news Augusto, but despite what millenials think, history did not start the day you were born. Parents have been helping kids buy houses forever. My parents got money from my grandparents when they bought their first house in the 80s. I got help (as did my sister) to buy in the 2000s. And I will help my kids when they buy their first house, probably some time in the late 2020s or early 2030s.

What people also don’t realize is the trillions of dollars those evil boomers have in assets. When they start passing on – and since the oldest boomers are 74, it’s already happening and about to accelerate – all that money will be passed on to their kids. The richest generation ever is about to make their kids the richest generation ever. Your dreams of a collapse are not coming true, sorry to tell you.

Just Some Random Guy,

“The richest generation ever is about to make their kids the richest generation ever.”

In theory, yes. In practice, from what I’m seeing, boomers will pass much of their wealth on to the health care industry during the last few years of their lives.

That’s the plan, but nobody ever talks about it

In fact the entire scam, pharma requiring prescriptions, and out of this world health-care-costs, and AMA and limiting doctors; It’s all part of the Rockefeller ‘health plan’ from 1920’s to 1950’s, and now its pretty much NWO.

Funny in CUBA any kid smart enough can be a doctor, and anybody can walk into a drug store on every corner and buy a bag of pills no prescription, cuz pharmacists are trained to know what you need,

In the meantime say the USA, people die because they can’t afford to go to the doctor for the flu, which always leads to pnemonia, which means $100k/day blow-out of any savings one may have had.

Like WOLF always harps on here, the USA is a kleptocracy, and edooocation and health are perfect examples.

Hell yes, by the time the old-farts go to hospital, and stay in ‘retirement’ home there ain’t no money left on table.

People will return to what ASIA does, kids live with parents, and grand-parents die, everybody moves up a floor.

In the States, the majority of Boomers don’t have the money to finance a decent retirement – I have a friend who worked for thirty years in publishing, got whacked in his early fifties, spent his IRA trying tom maintain his lifestyle and is now homeless – and those that do will get the treatment Wolf describes.

That’s the business model: if you have money, private equity-owned health care will take it all; if, not, they’ll leave you in a ditch.

But seniors have Medicare. And I have been assured by Bernie and Lizzie that Medicare means freeeeee health care. So either Bernie/Lizzie are lying or boomers will have no health care expenses post 65. Can’t be both.

Just Some Random Guy,

Does it make you feel better to politicize every issue? So maybe you don’t have to think about the real issues?

I’m talking about fairly well-to-do people who are now in their 80s and 90s with paid-for homes in California and Texas, with portfolios stuffed with bonds and stocks, and with rental property, people I know personally, and who are NOW getting cleaned out by all the things that are happening at the end of life.

I know that one of them pleaded to just let her die and let her join her husband and eldest son, and they’re keeping her alive against her will. She is too limited in her capabilities now to do anything about it. Medicare, even with the alphabet soup of “Parts” you might have, doesn’t pay for a lot of this stuff. You can easily rack up a few million bucks that way before you finally die.

The health care industry has this worked out to perfection. Boomers, once they get there — and eventually even you — will face an even more sophisticated health care industry whose sole purpose at this stage in life is to take as much away from them (and also from the government) as possible.

I know that many boomers have laid out plans to dodge this sort of abuse, vowing for example that their plan is “one gun, one bullet” or a less messy approach with pharma products. But once you get there, suddenly you might not be ABLE to follow through on your plan, and you become the conduit over the next two years of a phenomenal wealth transfer, from you and your heirs to the health care industry.

If any one doubts Wolf’s comments just take a look at UnitedHealthCare stock over the past ten years to see who benefited from Obamacare (which was originally Mitt Romney Care BTW).

Thank you Wolf for admitting gov run health care, ie Medicare does nothing for the population. We agree on this.

Just Some Random Guy,

Ha, that’s funny. Putting your words in my mouth. Medicare works great for people who have it. It just doesn’t cover all the expenses you incur when you need to be taken care of 24/7 because you’re wasting away.

I’m going on Medicare in the not too distant future, and I’m looking forward to it. Everyone I know who is Medicare is glad they’re on it. Private-sector health care in the US has become a racket of endless greed.

Two years ago I inherited a house in California from my parents, free and clear with no mortgage or medical bills. It just took 10 months to get the squatters (previously ‘caregivers’) out of the house that were looking after my stepmom before she passed. After reading these comments I guess the squatters were the lesser of the two evils, imagine if I would have had to deal with the American health care system. They would have taken the house all for the privilege of letting my Step Mom die in bed just the same.

I hate to “preach” but…..

In the US if you are “healthy” you are already “wealthy”!

This is especially true if you are elderly.

Sorry. All that “wealth” is paper wealth. After a crash, nothing to pass down. Stocks, Bonds, Real Estate will all collapse.

Canada is one of the richest country on the planet… there may be a recession at some point…But no collapse.

Canada is rich in resources (oil, trees, minerals), owned by the GOV, not the people. In fact Canada is just like Austrailia, another place rich in resources ( minerals )

Well what your saying here is ASIANS ain’t buying anymore,

What about little princess MENG with the leg bracelet waiting to occupy Trump’s prison in USSA – HUAWEI

First off, old timers like me call men and women such as yourself, “silver spooners.” My apologies if you were not born with a silver spoon in your mouth, but, you certainly talk like one. WHOA!! Mind blown, right?

Second off, I hate to break the news JSRG but despite what silver spooners think, this whole financial system that they have been enjoying, is built on a mountain of lies that would make Satan jealous.

What people such as yourself also don’t realize, is that Boomers stuff is getting repossessed and the pace is picking up, quite sadly, very fast. I would love for you to sit with myself and the regional bank manager in a closed meeting. I will allow you to educate him with the great wealth transfer that is about to begin. I can see him now, looking over at me, trying not to laugh his butt off.

There is nothing more embarrassed, undignified, and, oftentimes violent, than when a silver spooners dream implodes. That is what scares me the most concerning what is coming. Because I have already seen it many times on a smaller scale; and that is no dream.

Indeed, there was an article in Macleans magazine in the early 1990s talking about the “inheritance windfall” boomers were about to realize as their parents expired. This money was expected to have a material impact on the economy, and a massive impact on boomer wealth. Years later, Macleans ran a mea culpa referencing the earlier article, in which they quoted various financial advisors and estate lawyers to explain why the expected wealth transfer amounted to less than half what it should have.

Parents helping their kids is nothing new. Parents borrowing against their home equity to help their kids is definitely new. That didn’t happen 20 years ago. It’s called Ponzi borrowing, i.e. borrowing against an asset to purchase more of the same asset in anticipation of further price increases. And it’s been a big part of the run-up in prices from 2009 to present.

Negative interest rates will wipe the boomers out in the next 20 years. There will be no wealth transfer of any type to the next generation.

The good times will keep rolling then.

New home construction keeps heading up in the US.

So home buyers in Edmonton have not made a cent in appreciation since 2007, 13 years. Plus lots of expenses. Rough go. Our debt loads are the highest in the western world on a debt to income basis which means a recession will be uggggly. Houses are really just Taxation Units in some ways. I think owning some Gold Bullion makes some sense right now. 1 oz Canadian Maple Leafs

My sister owns rentals in Edmonton, happy tenants pay a reasonable rent, low interest rate mortgage… the properties pays for themselves with a bit of profit as a bonus, no complaints.

No complaints until tenant-law is FREE

No complaints until rent-control

Then watch out fast she wants out,

I know it happened to me.

….

They can drag you into court as a land-lord no cause, the tenant gets free legal representation, and your not allowed to have a lawyer present. They call it fair, and of course its a loaded game. If they show up, they auto-win, if they fail to appear you win.

The only way to win, is NOT to play.

I don’t care, sold out and now very rich, and don’t have to feed the system.

In Edmonton they need rent control to save the owners not save the renters.

nicko2,

Yep. That’s how it works. I have one rental myself. All my profit is invested back into the house, ie accelerated mortgage payoff. This house is my kids’ college fund. The house will be fully paid off when the oldest starts college. Even if it doesn’t appreciate another dime from today – and in the next 10 years that’s highly unlikely, but worst case scenario – it will be enough to cover college for both of them at a top tier private school.

Last time I had my car in for service, I went out with the service manager to show him an issue I was having. We got chatting and he’s got the exact same plan. He bought a rental house about 5 years ago, should be paid off just in time for his kid’s first year of college.

Both of us are nobody special, just some random guys (see what I did there) that you see on the street every day. Despite how the media demonizes EVIL LANDLORDS, truth it, most landlords are just normal people making a few bucks on the side. And anyone can do it as long as you stop believing in all this never ending doom and gloom. You’ll never make any money living in fear your entire life.

There’s no renters in Edmonton. I still own some townhouses there. I paid cash for all of them. No mortgages and all negative cash flows at the end of each year. Laidley Property Management manages all of them. I live in Ontario in the GTA. Resale condo prices today in Edmonton are 50 percent or less than they were way back in October 2007 non-inflation adjusted. Rents never go up but condo fees go up each year.

All these charts tell me one thing: long term real estate in Canada has been an excellent investment opportunity. Even the “crashes” were short term blips in a long term boom.

You need to look further down the list — Quebec City, Calgary, Edmonton, and the like.

Assuming owning a home in those city is at rental parity, even with no appreciation, one is better off owning vs renting. Quebec City died when the Nordiques moved to Denver :)

Long term… looking back at 2000 and then applying blinders isn’t long term. Look back at the high interest days of the 80s, see how much money you can profit if we see interest rates hit 10% – only half of what the 80s mortgages were. If that 10% scares you then you should be concerned. If not, then keep whistlin’ dixie.

Canada is a resource selling nation that is pumping the brakes on selling resources. That leaves them with only tax payers to ask for funds.

Has been. Definitely. Tense is important here.

Do Canadians cash out all that “free” equity like Americans have been recently?

https://ei.marketwatch.com/Multimedia/2019/11/07/Photos/NS/MW-HU875_cash_o_20191107131001_NS.jpg?uuid=d12aa7d6-0189-11ea-a927-9c8e992d421e

It seemed bizzare to see three of my neighbors all buy new vehicles, boats, vacations, etc this past year as the previous year all three told me they had money issues. All three refinanced their homes in 2019, and I am guessing all three also cashed out some of that “free” money. Why do I guess that is how they solved their money issues? I came across the chart above that shows 81% of Americans are refianancing, and “cashing out” in 2019. Just like in 2007, house “ATMs” are extending this credit cycle. Who knows how long it will last, as NIRP could extend it indefinately as I just had one neighbor, just today, tell me he might get a negative home loan, as he read the “Swiss” are getting paid to borrow. I think the Pres tweeting about NIRP recently is going mainstream. People really believe they are going to get paid to borrow, and believe it or not, my neighbors have college degrees (not saying much to be honest)…

To me housing is one of the things that ‘policy makers’ in a lot of countries like to mess around with the most. It’s relatively easy to pull demand forward by lowering lending requirements. Poof you have pulled forward a $500,000 of economic activity and created an asset for the bank. If it’s a 3% down loan then you are leveraged 33:1 and if things go south the losses are going to be socialized to the taxpayer in many cases.

I think housing prices relative to income also show the relative health of the economy. If the average middle income person can’t obtain decent shelter with about 1/3 of his income then the economy isn’t working in that area. It’s up to you to figure out a solution.

Another thing to consider is the reaction of people to gov/central banker’s long term repression of interest rates.

This repression of interest rates minus inflation has made real interest rates negative.

Negative interest rates encourages people to borrow and put it into something real like real estate, that they hope will retain it’s value.

Even if the real rate of return is as low as zero, people perceive this as winning,

In a negative interest environment, this is the logical thing to do.

Negative interest rates reward people for borrrowing and investing in something real and then doing nothing! Ex empty condos/houses.

This is how to game the current system especially if one believes central banker’s must continually lower interest rates or the current banking system will collapse.

Owning a vacant house in Vancouver,

— thus quadrupling your money in 10 years —

is a lot better than any savings account.

I’m surprised none of the presidential candidates

are advocating a vacancy tax; they should be

focused on housing undesirables, not relative poverty.

By the way out of curiosity I researched the Javelin missle and launcher that’s in the news lately. It’s pretty impressive. But since this is a money site it’s about $250,000 for missle and launcher. Developed by a US company that ended up being owned by Lockheed Martin.

If you used all my federal taxes in my lifetime I might have purchased 1 of them. As corrupt as Ukraine is said to be I would not be surprised if these things don’t get sold on the black market.

Obeying the law is so last century.

I’m surprised anyone pays their mortgage anymore;

so many have gone 5+ years without making a payment,

Fannie Mae doesn’t even keep track of them anymore.

Commonwealth countries, Canada and Australia,

have benefited from a flight to safety, out of China;

laws to prevent it are circumvented, of course.

Letting the guppies out…The big fish are either well contained or being tracked. The bigger countries tend to have squads for catch the biggest fishes.

A bit off topic as this applies to the U.S. real estate:

Given that we are now into QE4 and rate reductions, logic dictates we will likely see real estate price increases.

The declines in the U.S. we’ve seen might be mostly due China exit. That took air out of the bubble, but Fed policy is once again pro-bubble and real estate should respond to this.

Tell that to LOWES, they just closing a bunch more under performing stores. Shopped at many of the ones that are closing and they are huge and in great areas when urban sprawl caught up.

Probably the taxes would be getting huge as well.

The bigger box change love the outskirts do to lower taxes.

Lot of house-broke residents can’t afford never-ending home renos anymore. Although Canada was so over-saturated with home reno stores these closures were inevitable, regardless of economic trends. Lowes + Home Depot + Rona was always one big box home reno store too many, and we always knew when Lowes took over Rona there would be massive consolidation.

Ok so looking at the graphs, with the exception of Vancouver, would it be more appropriate to call it the Most Splendid Housing Price Plateau rather than the Most Splendid housing bubble? Because bubbles eventually pop, balloons like the inner tube in my bike, deflate; neither of which is happening.