US-China trade war, falling business confidence, slowdown in China, German exports, and new: the temporary shutdown of Hong Kong’s airport, the largest cargo hub in the world.

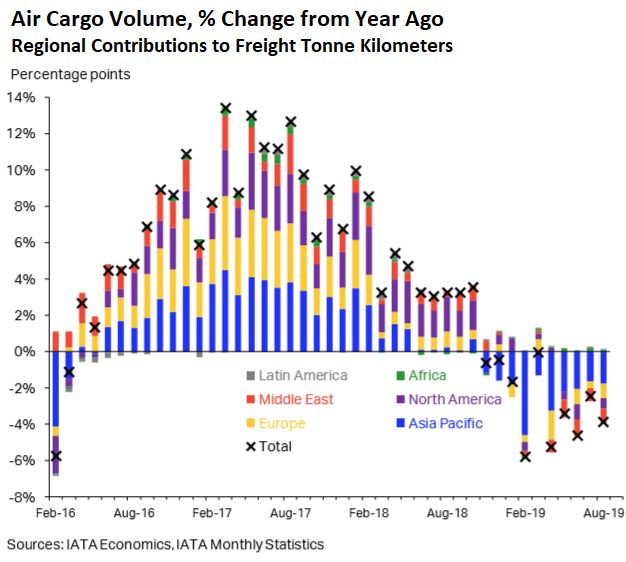

Demand for global air freight, domestic and international, as measured in freight tonne kilometers (FTKs), fell by 3.9% in August compared to August last year, the 10th month in a row of year-over-year declines, the longest such period of declines since 2008 during the Global Financial Crisis, according to the International Air Transport Association (IATA). But there have been steeper year-over-year drops more recently, including in February 2016, when air freight demand fell by nearly 7%.

In the largest region, Asia Pacific, which accounts for 35% of total air freight, demand fell by 5.0%, accounting for just under half the global decline (blue). In North America (purple) and Europe (yellow), each accounting for just under 24% of global air freight, demand fell respectively by 2.4% and 3.3% (chart: © International Air Transport Association, 2019. Air Freight Market Analysis August 2019. All Rights Reserved. Available on IATA Economics page).

“Shrinking global trade, political uncertainties, and weakness in some of the key macroeconomic indicators – particularly the new export orders component of the manufacturing PMI – continue to weigh on this month’s outcome,” the IATA report said.

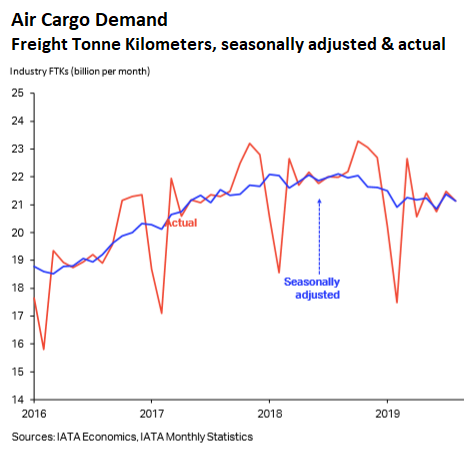

Demand in August ticked down a little from July, after having ticked up a little in July from June, thus continuing the sideways movement since April, but at a level that was 4.4% lower than in mid-2018.

The chart below (© International Air Transport Association, 2019. Air Freight Market Analysis August 2019. All Rights Reserved. Available on IATA Economics page) shows billion freight tonne kilometers per month, not seasonally adjusted (red line) and seasonally adjusted (blue line):

Capacity across the industry increased by 2% in August, compared to a year ago. With declining demand and rising capacity, the industry-wide freight load factor fell 2.7%, and is now at 44.6%. This means that 44.6% of the available freight tonne kilometers were used. This is a sign of “overcapacity, the structural challenge” of the industry, as the IATA has been pointing out, including in a report last year.

During the freight recession in 2016, the freight load factor (FLF) fell as low as 41%. Then it began climbing steadily, powered by rising demand, and despite increases in capacity reached 46% in 2018 and looked to be heading higher. But recently, under declining demand and still rising capacity, the FLF has been falling again.

| Region | Market share | Change in Demand | Change in Capacity |

| Total Market | 100.0% | -3.9% | 2.0% |

| Asia Pacific | 35.3% | -5.0% | 2.3% |

| North America | 23.7% | -2.4% | 1.3% |

| Europe | 23.4% | -3.3% | 3.3% |

| Middle East | 13.3% | -6.7% | 0.8% |

| Latin America | 2.7% | 0.1% | -2.9% |

| Africa | 1.7% | 8.0% | 17.1% |

International demand

Demand for just international air cargo – the above is for combined domestic and international air cargo – fell more steeply, with freight tonne kilometers down 4.6% in August, compared to a year ago.

For Asia Pacific, international FTKs fell 5.8%, the 10th month in a row of year-over-year declines. The IATA pointed out:

Mounting trade tensions along with the slowdown in the Chinese economy continue to be the main drivers behind the contraction.

Additional pressure this month came from the temporary shutdown of Hong Kong International Airport – the largest cargo hub in the world – which affected both passengers and belly cargo.

Demand in North America for international air cargo has also come under pressure, particularly the Asia-North America routes, where volume dropped 5%, as “carriers continue to face headwinds from the US-China trade war and falling business confidence.”

In Europe, the decline in demand for international air cargo “has reflected softer regional economic outcomes and weaker support from new export orders in some of the key countries, notably Germany.”

In recent months, demand has stabilized on the largest international trade lanes for North America and Europe, the IATA said – but “well below” the levels a year ago.

“Fleets are nervous. The latest manufacturing and construction numbers are concerning. The trade issue with China looms.” Read… Orders of Heavy Trucks Collapse, Layoffs Start

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

And of course the Trade War doesn’t help.

OT, but Wolf said to address comments here.

The Fed says now it will add $60 billion a month to balance sheet. This on top of about $200 billion in recent weeks.

This is not QE. So they say.

You can’t go wrong, Africa is the final frontier.

Wolf,

Our politicians in the west have created an impossible situation where the whole system has to fail.

Imposing massive amounts of laws and regulations to innovation in a financial structure that is only concerned for money and max profits.

The manufactures then have sacrificed quality and safety for profits.

This then has come back to bite them in the butt with structural failures and design flaws that bring massive lawsuits.

There are some wonderful technology that could be created but…

The search for max profits has shelved them forever.

Our politicians in the west have created an impossible situation where the whole system has to fail.

Corporatists have coerced your politicians in the west to create an impossible situation where the whole system has to fail.

FIFY

Which isn’t to say that many corporatists aren’t also politicians or that many politicians aren’t also corporatists. Nominally, politicians are only out to get elected and will do and say whatever to get elected, but many are out to get elected so they accelerate their accumulations, so as to cut out the middle man and/or the middle woman.

I think it is, well, strange, that some commenters like to blame the puppets while ignoring those who are pulling their strings. But let’s not get into motivations just yet, shall we?

Most politicians, Left and Right, still believe that infinite, ‘sustainable’, growth is possible on a finite planet. Hell, they are now promising ‘Clean, Green’ growth!

It doesn’t help that most are mere lawyers and arts/social sciences graduates, and therefore intellectually incapable of dealing with problems of late-stage global civilization, which are essentially about physics……

Not that I’m letting the corrupt and short-sighted corporate types off the hook, of course.

What I was taught in school, always left me with questions that I couldn’t find the answers to. After all, these are our trusted experts and have vastly more resources than me…

When computers came along, I was able to do a lot more research and found our experts were wrong. Our politicians hate any type of change or even look at anything that does not fit their following the US at all costs. Our education system too was compromised to follow a political agenda now for funding.

Would it not make sense to understand how our planet actually mechanically works in order to create a perfect mechanism to harness its abundant energies?

I thought it would…but our educators and politicians never admit a mistake.

So all this fantastic research is shelved until our brainwashed society changes.

Amazon is building more fulfillment centers in an effort to reduce dependence on air freight.

US rail shipping volume declined. Trucking volumes receded. ISM manufacturing contracted. The service sector grew.

US housing starts spiked to a multi-year high.

Inflation is in the low single digits.

Global growth slowed, but no global recession has been seen.

Germany/India/China/Turkey and many others are skirting on the edge of recession…..perhaps BREXIT will be what pushes them over the cliff.

Germany could afford a recession. Not happily but running a 2.5 % budget surplus as well as the overall balance sheet leaves it room.

However the already tense budget discussions with other euro zone members like Italy would not improve.

If China were to have what we define as a recession: two consecutive quarters of negative growth, a lot of people are going to be very upset. Possible it’s not survivable for the CCP.

My understanding is that the average German is actually poorer than many in other parts of Europe.

Germans as Wessies & Ossies or only Wessies. If you include Ossies than that is absolutely true. Only Wessies, it is still true for Scandinavia and Luxembourg. Other places the difference is so small that it depends on PPP.

Global growth slowed, but no global recession has been seen.

Presently there are recessions in numerous sectors in numerous locations. There are always recessions going on somewhere. But it isn’t called a Recession unless the decline involves the Financial Industrial Complex, and it doesn’t, so it isn’t. So long as the wealth of the Right People is maintained and enhanced they could care less when whole populations are going to hell. And everybody gets a turn.

Don’t blame me. I don’t make the rules.

I’ve been looking for that cartoon, the one where the man in the tattered suit explains to some children, huddled around a fire in a cave, that “Yes, the planet got destroyed, but for a beautiful moment in time we created a lot of value for shareholders.” Has anybody seen it? I know it’s around here somewhere.

You also need to find the Goya print from ‘The Disasters of War’: two or three well-fed people are looking past a mass of starving, skeletal and tattered commoners.

It think the title is ‘They might as well be different kinds’.

Something like that.

One of the greatest books on the human condition ever made, together with ‘Los Caprichos’.

( The moronic Chapman Brothers will surely go to Hell for drawing their childish scribbles over it, as ‘an improvement.’)

You just have to google the entire phrase to find that cartoon, originally from the New Yorker

One month signs of optimism, like housing starts last month, happened quite a bit in 2005-2006, and we all know what followed. Many of these indicators have been on downward trends for 12+ months.

Morning…. Some of the the comments bring to mind the script, characters, situations and numbness of the HBO series “Succession”… IMHO

Why are planes said to be a losing business yet so much money is invested on it?

This isn’t like the “Great Unicon Massacre”, everyone actually believes things won’t get better.

Be it commencial flights or cargo, it seems the system is rigged to lose money.

Why?

The problem is very simple: the capacity that is coming online right now was ordered in 2017 and 2018, when the sky was the limit for all kinds of growth, albeit in Q3 demand started to hiss out a whole lot of air already.

If you can secure funding quickly, it doesn’t take much for a freighter airline to enter service: a freighter conversion takes about four months once a used aircraft is delivered to Bedek, Precision Aircraft, AEI etc and unless you are clinically insane once work starts you cannot say “We don’t need that thing anymore” because penalties are crushing and it’s just cheaper to take delivery and lease the aircraft out to start recouping costs as soon as possible.

Ironically enough the Boeing 737 MAX fiasco is helping out keeping overcapacity at bay because due to the dozens of grounded and undelivered aircraft a lot of conversion feedstock is still carrying passengers around: earlier this year Boeing (well, actually AEI: Boeing and Airbus have no capacity to spare and hence contract the conversions they design to specialist firms) finally delivered the first 737-800SF freighter conversions and the Airbus A320/321P2F finally solved its mind-boggling technical problems.

Freighter operators are ready to order a lot of these conversions as soon as feedstock becomes available, and this feedstock will become available in adequate quantities once the 737 MAX will resume service (educated guess: late Q1/early Q2 2020).

People are still very sanguine about freighter growth, albeit their justifications sound downright laughabale sometimes: a piece I read a few weeks back tried to push demand of fresh exotic fruit from China as the “next big thing”, perhaps forgetting China is already a mature market when it comes to exotic fruit. Does anyone remember the 2015 picture of that greengrocer playing stocks on his laptop next toa mountain of bananas and pineapples? ;-)

– Boeing seems to be sliding deeper and deeper into problems.

https://www.moonofalabama.org/2019/10/boeings-problems-reach-beyond-the-737-max.html

– Then more and more of Boeing’s production capacity can be used for coverting their planes to freighter planes.

The transfer of wealth continues. From middle class savers who receive nothing or negative real rates for their savings to the business owners or owners of equity.

With a large leakage of funds to overseas to preclude inflation and keep everything calm.

Government helping by taxing wealth very little and hitting middle class with payroll taxes, sales taxes and property taxes.

Its a valid way to run an economy that has zero demand. The half that has nothing receive their bribe to stay happy under both parties.

Unfortunately……if you discount national wealth to reasonable levels……15 pe for the market, a 10 year yield of 4% and real estate by 20% to reflect real market interest rates……the US is just about broke. The 338 trillion in assets melts to 230 trillion…… less liabilities of about the same……zip. No real wealth creation going on…..just paper moving based on the fed and ECB and Japanese central bank……and a transfer of wealth to the rich.

One of these days gold is going to explode. $20,000 an ounce. The wealthy will jet off to Switzerland. Any large stress to this mess and it all falls apart. The wealthy were in the same position in the 1920’s but at that time the country was accumulating wealth. Trade surplus.

I am starting to change my mind on savings. If there is no real return on savings then I am faced with a choice: 1. Be patient and wait for a better time to invest 2. With a real hurdle rate of zero maybe I can dig around and find something to do with my savings to at least get a small positive return that is worth a slight risk. If you have a mortgage might mean paying it off early. Could mean investing in new energy efficient HVAC or more efficient automobile. Might get you a 4 or 5% return.

“..One of these days gold is going to explode. $20,000 an ounce. The wealthy will jet off to Switzerland. ..”

And the nouveau riche will be with them, up at the pointy end. (I’ve ordered a brand new collapsible walking frame that fits nicely in the over-head lockers, in anticipation..)

Gold is a good long term investment because every time there is a huge crisis people rushes to buy gold and the price goes up and that more or less happens once every ten years.

Can you afford to wait a decade or a bit more?

And usually the price hike doesn’t last long unless the crisis goes from huge to “real”

Physical gold is priced in paper gold which remains manipulated by vested interests. look at the volatility in GLD stuck between $1450 and $1560/ounce!

Every one knows that fiat currency is getting devalued all over but the GLD is stuck! So are the GLD miners. There is disconnect some where! Libor manipulation is nothing compared to GLD futures!

Should we say “gold going to $20000 per ounce”? Or should we say “$ going to 20000 per ounce of gold”?

The difference is, first statement suggests that dollar holds constant value against real “things” and gold’s value is set to rise.

In reality, gold holds constant value while $ is set to decline by 14 times approx.

February 2016. Has that to do with Chinese new year?