Ending the repo market blowout and un-inverting the yield curve.

Since Fed Chair Jerome Powell’s initial explanation of the Fed’s new plan, and with a big push this morning from the Fed’s announcement of the actual details of the plan, the 10-year Treasury yield has jumped 23 basis points, from 1.52% when he was speaking on Tuesday to 1.75% at the moment. And the yield curve has steepened and is getting close to un-inverting. Here is what happened.

The New York Fed released a statement this morning that formalizes and details what Jerome Powell had said on Tuesday and what the FOMC minutes, released on Wednesday, had indicated the Fed would do: Buy short-term Treasury bills with maturities of one year or less, of at a pace of “approximately $60 billion per month,” starting in mid-October and “at least into the second quarter of next year,” in order to replenish the “excess reserves,” whose dropping levels have been blamed for banks’ refusing to lend to the repo market, thus triggering the recent repo blowout.

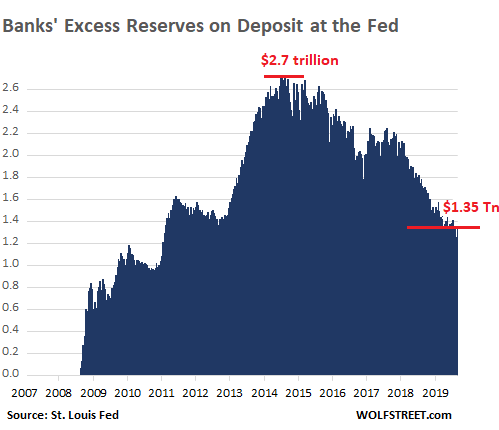

Excess reserves came into being as a result of QE during the Financial Crisis. They represent the amount of cash the banks have on deposit at the Fed beyond the required reserves. They’re liabilities on the Fed’s balance sheet, not assets, and the Fed pays the banks interest on those reserves currently at a rate of 1.8%. These excess reserves have fallen by half since their peak at the end of QE.

The new-new-new plan.

Banks would rationally lend these reserves to the repo market if rates make this profitable (if repo rates are higher than 1.8% currently). But that system broke down when repo rates spiked and banks weren’t lending, despite high repo rates that would have allowed banks to make a bigger profit.

Exactly why banks, or why one or two of the biggest banks, refused to lend to the repo market or lend to a few players in the repo market remains subject to speculation.

But the Fed’s new plan is supposed to resolve that problem. The Fed thinks these excess reserves dropped too much and went below the level where they’re sufficient to prevent repo market blowouts. In its announcement this morning, it said it would push up those reserves back to where they’re “at or above the level that prevailed in early September 2019.”

Leading up to the repo blowout, the excess reserves had dropped by $160 billion in four weeks, from $1.42 trillion in mid-August to a low point of $1.26 trillion in mid-September, when the repo market blew out. And the Fed thinks that this level was below where the system can function.

The Fed’s purchases for this purpose will be exclusively T-bills – Treasury securities with a maturity of less than one year. This will reduce the overall average maturity of the Fed’s balance sheet. The Fed will absorb T-bills and the market will have to absorb Treasury securities with longer maturities.

On top of the new-new plan.

And the Fed will continue “at least through January” with its new-new plan, first implemented in mid-September in response to the repo market blowout. These are its repo operations – overnight repos that unwind the next morning, and term repos that unwind when they mature, such as in 6 days or 14 days.

The Fed said today that the pace will remain the same, daily overnight repos of “at least $75 billion” and term repos about twice a week for “at least $35 billion” per operation.

These term repos were 14-day maturities at first but now vary and have shortened. For example, today’s term repo, instead of 14 days, was for 6 days (3 business days, as the bond market is closed on Columbus Day).

These operations have all been undersubscribed every day in October. On the Fed’s balance sheet yesterday, the total assets from its repo operations fell by $2.5 billion from the balance a weak earlier, to $178 billion.

I assume the T-bill purchases under the new-new-new plan to raise the excess reserves will take further pressure off the repo market, and that the Fed’s repo operations – the new-new plan – will be further undersubscribed.

Diving deeper into the ocean of assumptions about the Fed: I assume when there is very low demand or no demand for the Fed’s repo operations that the Fed figures excess reserves have risen enough, and that it will then end these new-new-new plan purchases of T-bills.

The Fed’s repo operations are set to continue “at least through January,” the Fed said in today’s announcement, which would get the repo market through the expected turmoil at year-end, which was quite a spectacle last year, and promised to be a much bigger spectacle this year.

On top of the new plan.

The new plan from earlier this year remains in effect, the Fed said today. Under this plan, the Fed ended the reduction in the balance sheet assets, by reinvesting the balance of MBS that rolls off with Treasury securities with a mix of maturities, including short-term T-bills; and to reinvest all Treasury securities that mature with Treasury securities of all maturities, including short-term T-bills.

Effect on the yield curve.

From the end of Operation Twist until a few months ago, the Fed has not held any meaningful amounts of T-bills on its balance sheet, having instead focused on long-term securities and MBS to push down long-term interest rates, such as mortgage rates, as a stimulus measure.

But these new plans have a special effect on the Fed’s balance sheet: They will reduce the amount of long-dated securities and MBS the Fed holds; and they will proportionately and in absolute terms increase the amounts of T-bills the Fed holds. In other words, the market will have to absorb more longer-dated securities and more MBS, meaning upward pressure on long-dated yields, and the Fed absorbs more T-bills.

Since Fed Chair Jerome Powell’s initial explanation on Tuesday of the new-new-new plan of only buying T-bills, the 10-year Treasury yield has risen from 1.52% when he was speaking to 1.75% at the moment. And the yield curve has steepened. The Fed hasn’t said this, but clearly, this system is designed also to un-invert the yield curve, and it has taken a step into that direction already.

The repo blow-out — whoever instigated it — comes in real handy. Read… How the Crybabies on Wall Street Try to Force the Fed into QE-4

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In simplistic terms isn’t this another arrow to suggest we are closing in on a recession and downturn in stocks? I heard Jeff Gundlach rightly pointing this out when he said the yield curve inverting isn’t the issue: it’s when it uninverts that tends to be followed by a recession. What do you think Wolf?

The Fed believes in the wealth affect

Last S&P bottom was 0.8 × sales. It’s now at 2.18 × sales which implies about 1100 on S&P if we were to go back to 0.8. Fed doesn’t want that to happen.

It’s kind of funny how the Fed’s create special powers for the creature to survive. Can’t lie to FBI but they can lie to you. Can’t disclose truth about govt breaking the law to spy on you. Can’t print your own money as that is stealing, OK for FED to do though because Congress said that’s OK.

Dear Readers and Commenters,

The beer mug for a relaxing moment away from the chaos of this world has arrived. “Nothing Goes to Heck in a Straight line,” it says on one side, with a funny wolf doing the talking on the other side of the wrap-around design. Have a laugh at my expense, and enjoy.

The art is by artist and long-time commenter Kitten Lopez in San Francisco. Long-time reader and commenter “Ripp” and the company he works for in Arizona are doing the heavy lifting of getting the mugs to you.

The mug with free shipping in the US will set you back $25, *beer not included. You can order them from our store:

https://www.wolfstreetstore.com/

Thanks, Wolf!

My HeckenStein/WolfenStein just arrived and has a splash of a certain Belgian Ale remaining.

I could have used it reading through the Sticker Shock comments:)

Thanks for the explanation on today’s FED statement. Still many questions…

How much if shipped to Canada, very closed to the US border?

Em,

The store should give you a postal rate to Canada once you put your address in at checkout. If you prefer, you can send an email to [email protected] with your address and I can get you a rate.

Technically, I would just need the postal code.

This article says that the FED is fighting the behavior of the crybaby’s you describe in.

https://wolfstreet.com/2019/10/10/are-the-crybabies-on-wall-street-trying-to-force-the-fed-into-qe-4-you-bet/

Or do i have it wrong?

Also you mention FED will buy 60 B per month bills, which sound’s like oh QE, but is not, as FED will not buy the 60 B of long dates available (unless of course nobody takes them) it would normally buy to maintain its sheet size. leaving them to the market.

So unless purchases exceed roll offs T sheet will stay basically neutral only end dates will change, and MBS should still be creeping down.

Be interesting to see how the whole FED sheet looks, in your end Nov report.

My theory is banks don’t want to lend because the Fed is suppressing rates thus inflating assets which banks find more attractive, add the fact this (QE) has been going on for so very very very long the banks are learning and adapting and thinking “to heck” with this peanuts overnight rate let’s buy FX’s or something. Reminder: we are still at this very moment in FULL stimulus mode interest rate wise and have never ever ever ever not been in it for 11 years. Add to that – Powell’s transparently silly statement that his his QE isn’t QE if we call it “organic” or “not QE” when it is QE. QE is QE by any other name…a rose is a rose by any other name.

I still can figure out from his statements, exactly what he is doing.

Wait till end Nov wolfs sheet review.

I think we will end up with sideways, or close to it, in total, the way Powell has expressed it, but I wouldn’t bet on that.

Maybe there are enough people like me that it has affected demand. Decided to get out of corporate life completely by 50. I will do without any luxury not to have to go back in that toxic mess.

Got food, shelter, transportation and health insurance. Don’t really ‘need’ anything else. My main focus everyday is to stay healthy and have good relationships. Lived about 13 years on $15,000 per year and gave some of that away. Now I can spend about $40,000 after taxes but it will be tough as I am not a thing person. Trying to convince myself to spend it before I croak instead of leaving it to kids to spend.

d,

Good questions – and the first two are somewhat tricky. But I’ll give them a shot.

1. “…the FED is fighting the behavior of the crybaby’s you describe in….”

I think this is the reverse of what I tried to describe. I attempted to say that the Crybabies are trying to force the Fed’s hand. In other words, they’re trying to push the Fed around. I would not go as far as saying that the Fed is fighting them. Often, the Crybabies get what they want. If they don’t, then the market crashes or locks up or something implodes, and then the Fed steps in to save the butts of the Crybabies, and gives them what they wanted in the first place, only more.

2. “sounds like QE”

I’m not hung up on what to call it. It sure as heck looks like QE to me. BUT there is a difference in purpose and effect, the way this one is laid out and is being communicated, so that it doesn’t actually have the effect of QE. It’s designed not to do what QE did. So I think we can call it whatever we want to, but the effects look to be different.

3. Yes, the Fed has decided to get rid of its MBS, and they will continue to creep down. Most of the MBS mature in over 10 years, so this is really long-term debt that is coming off the balance sheet here. It is being replaced by Treasuries of a mix of maturities, including T-bills. There has been no visible opposition to the Fed’s efforts to get rid of its MBS. The market seems to have accepted that – until something implodes :-]

Thank you.

Your end NOV sheet review, will tell us much, me thinks.

Before then, we are really just making noise.

So at the bottom of this is the realization that tax cuts weren’t enough and the rich required yet more money, correct?

When is QE not QE? When Jerome says so, damn you!

—Mainstream Media

Also, the beatings will continue until infinite growth occurs. Thank you.

—The Management

/sighs

“I assume the T-bill purchases under the new-new-new plan to raise the excess reserves will take further pressure off the repo market, and that the Fed’s repo operations – the new-new plan – will be further undersubscribed.”

Can someone explain to me what is undersubscribed or oversubcribed? What does subscribe mean in this context? Thanks

qt,

When the Fed offers to buy $75 billion in securities, for $75 billion in cash, and sellers only sell $35 billion to the Fed to get $35 billion in cash, it means the operation was “undersubscribed” — meaning there was less demand for the Fed’s cash than the Fed offered.

Oversubscribed means that there was more demand for the Fed’s cash than the Fed offered. This has not happened so far this month, but it happened in September.

Fed places bonds (or bills) in bank reserves and the banks go to Repo and turn them into cash, which is borrowed, and the collateral is borrowed, nobody owns anything. When reserves disappear there is no cash. The cash equivalent spread between short term Treasuries and cash is much closer than say 10 year bonds and cash. With rates rising the cash value of the bond goes down, (and nobody trusts the collateral value not even for overnight) so if you want rates to rise in the middle of the curve you do the opposite, you put short term bills in reserve, these are more liquid and it takes pressure off the middle, which pegged those bonds to cash value, so it can rise as well. Now it all begs the question why put T bills in reserve, why not hand the cash to banks, and skip this arcane sideshow. Yields could rise on mortgages, and longer Treasuries may reset higher, the dollar is off the charts, foreign buyers continue to buy our worthless paper, with one eye on the currency exchange exit, the cost of derivatives to insure the transaction goes down, and the Chinese don’t have to drop the Yuan. So everybody is happy.

Strangely appropriate, I think. In any case, I ordered one. I’ll raise a toast to the insanity of today’s “markets” with everyone else here…

Darnit, that was supposed to go under the picture of the mug. I blame my fingers.

I am glad that was fixed . It’s All good .

What a difference a day makes. Long Term Yields spiked violently today causing prices to fall. The volatility in bond prices are not good for Repo borrowers, Expect margin calls on Monday. Today’s a real crazy day.

Dow up by more than 450, it’s only normal for the yield to go up a bit, I don’t buy Wolfs theory that because Fed is buying the short term of the curve the long term yields will go up. Fed is the market right now in the bond market and will do whatever it likes, but given the amount of QE in the pipeline, I expect the yields to go lower and Dow to hit 30k before the election.

Yes, but it dropped 200 points in the final 20 minutes of trading.

Monday will be interesting

So people took profits from the surge.

So what?

Any rise in yields should be offset by new buying interest. In other words bonds cannot go down. BUT, the Fed is throwing billions of taxpayer money at bank reserves, which is ludicrous, and which could fuel a real crisis considering the delicate situation with governments bottom line. Would China sell their bonds and slap a downgrade on the US credit rating (after they get a trade deal)? What does it matter what Moody’s thinks, the only party that matters is the party taking our paper in BIS. This is like the prologue to W2, when the Japanese delegate sat in the WH and said everything was fine. Only this time it’s financial war.

If the Fed is buying less long-term securities (i.e. MBS) and has a strong desire to purchase short-term treasuries, wouldn’t it make sense that yields go up on long-term securities? Just my thoughts.

I am new here. I have enjoyed reading Wolf’s blogs and listening to his podcasts.

He said, She said, They said…… an economy/market based on assumptions, remarks, and innuendoes. Hot air, the perfect fuel for a balloon economy!

\\\

…remarks, innuendos, he said, she said…sound like a great plot for a Telenovela

“Lo Dinero del Pueblo”,

staring in lead Roles,

The Banks as evil dude with all the money and the mustache,

The government as the old sick corrupt landowner,

The FED as the manipulative, charming and misterious business man,

The young people as Juanita, the girl that needs to pay back her sick father’s debt,

The elder people as the sick father who kind of messed up things but is aware of his mistakes and it’s too late to do anything about it,

The MainstreamMedia as manipulative twin sister who is in love with the business man and seccretly works for the man with the mustache,

The readers of Wolfstreet, that masked hero who is trying to save Juanita.

Tune in next week for another series of … “Lo Dinero del Pueblo”.

\\\

Your plot sounds more convoluted than a Gordian Knot but more entertaining,does every body keep their cloths on?

\\\

Nope, but just like in GoT it’s always the favorite most noble characters that get killed of. And there is some nudity, but only every 4 years…Juanita seems unable to learn from here mistakes…

\\\

Bullish !

I’ll put on my tin foil hat for a moment. the Fed will do all it can to get long rates up, up,up until it busts the wheels off asset prices so it’s buddies in private equity can buy for 10 to 40 cents on the dollar just like before. Ain’t it Wonderfull!! Love my Wolf Street mug by the way!

Something Stinks with the Repo.

The latest H.4.1 Statistical Release (in millions) for Oct 9, 2019 indicates:

Repurchase agreements – 178,650

There are two kinds of repo ops:

Overnight – which ends the next business day

Term – which ends about 14 days (or whenever) later

For October 9th only 3 repos should still be active:

1) Overnight started 10/9 for 30.8b

2) Term started 9/26 to end 10/10 for 60.0b

3) Term started 9/27 to end 10/11 for 49.0b

Together, all three total only $139.8b

But the balance sheet says repo was still $178.65 billion

That means that about $38.85b for PREVIOUS OLDER repo operations have NOT been repurchased (or paid).

The borrowers cannot even buy back (repurchase) all their collateral. That bad. No wonder the Fed is very concerned.

Good analysis, sometimes it’s not that simple to turn questionable paper into cash.

His analysis was wrong. See below. He forgot one $60 billion term repo that matured one day after the close of the balance sheet, and he then came to a hasty conclusion that “something stinks.”

Thanks for the clarification Mr. Richter.

Iamafan, it looks to me as though you missed the Term Repo that opened on 10/8 and closes on 10/22. No cause for panic here.

https://www.newyorkfed.org/markets/opolicy/operating_policy_191004

Yes, you are right. Thank you for correcting me.

Iamafan,

You forgot to add a term repo that matured on Oct 10 of $60 billion:

Balance sheet as of afternoon Oct 9 included:

$30.8 billion overnight, Oct 9, matured Oct 10.

$38.85 billion term 14 days, Oct 8, matures Oct 22

$49.00 billion term 14 days, Sep 27, matures Oct 11

$60.00 billion term 14 days, Sep 26, matured Oct 10 (Thursday, day after balance sheet close)

Ok I’ll check it. Dates are hard to match. Sorry if I caused alarm.

No problem. Happens to us all :-]

Ok, found it. I added it to the next week. Shucks. Sorry. My mistake

Total for Oct 9 should be 178.650b

Nope I forgot to add the 38.850b. I moved it to the next week by mistake.

I seem to be way behind — I put some comments at the end of the previous thread that have quite a bit to do with the subject matter of this new thread.

Jeffrey Snider in Today’s Real Clear Markets makes a persuasive case that increasing bank reserves has nothing to do with the issue.

https://www.realclearmarkets.com/articles/2019/10/11/chairman_powell_is_absolutely_right_that_this_sure_isnt_stimulus_103944.html

He points out that buying up T-bills in excnange for cash reduces the collateral available in the repo market and that its counterparty risk that is clogging the repo system.

I’ve never understood Snider and this article is no different.

(1) If a shortage of T-bills was really the problem with the repo markets, why did the Fed’s overnight and term repo operations fix the problem? The Fed wasn’t supplying T-bills, it was absorbing them.

(2) Why is there suddenly a shortage of T-bills? The monthly Treasury accounting shows that the most recent low point for T-bills outstanding was in July, and there were $171B more T-bills outstanding on September 30 than July 31. But there were also more T-bills outstanding in March than in September.

Why was there no repo panic in June or July, when there were fewer T-bills available? Or, if the problem is a glut of T-bills, why no panic in March?

Let me say this, if there is anybody that knows how that repo market works, it should be FED, right? And FED had NO idea. If they have had any idea, they would have made sure when they “commincate/threat/force” the repo guys to use rate at 1.5%, they should obey! Turned out, they did NOT obey and FED had to get their hands dirty and step into the market themselves. This means even the FED do NOT know/control the repo market enough to shape the behavior in a certain/predicable fashion. Now you think anybody can answer your questions?

I do NOT think you need to know the answer. All you need to know is that when there is money to be made, the banks did NOT lend. We all should raise our cash.

The purported “shortage” of t-bills will not be a shortage of t-bills for those who actually OWN t-bills and want to repo them (or sell them to the Fed). It will be a shortage only for those that want to *borrow* t-bills for a “collateral quality transformation” scheme (described in Snider’s article). I have to admit, breaking the market for “collateral quality transformation” sounds like a GOOD thing to me, not a bad thing. The scheme of “collateral quality transformation” *is* the cause and reason for elevated counterparty risk in the private repo market.

I get the concept Snider is trying to explain, I just don’t see it supported by the actual data on T-bill availability.

Why would there be a sudden outbreak of T-bill hoarding when inventory is high and heading higher, and not before? And especially in September when a whole bunch of T-bills were issued?

Why did the Fed’s absorbing more T-bills via repos lead to less hoarding and not more?

The article by Scott Skyrm makes far more sense in terms of the mechanics of what happened and how the Fed’s fix worked.

https://www.zerohedge.com/markets/panic-repo-one-worlds-top-repo-experts-explains-what-really-happened

WS, my comment was a response to unit472, not you :). I hadn’t even seen your comment before I posted mine. I think we are in agreement.

PS: Scott Skyrm article s the one I talked about a few threads ago, but not by name. I’m often afraid of posting links because of the moderation delay.

If asset purchase isn’t stimulus then what is it. Liquidity lubrication?

For Jeffrey and M. Singh of the IMF, Treasuries are meant to be repo collateral especially for Eurodollars.

Not sure what a saver like me is supposed to do.

I am too small to repo I don’t want to lend my Treasuries either. I guess I am a hoarder. Yuck.

Nice supplemental read. Everything has become a derivative of what it used to be. What is liquidity? Only something you can use in a trade for something else to make a derivative.

Implicit:

Bingo!

+1000

Pretty soon all humans will be “derivatives” of derivatives! LOL!!

(We are DOOMED!)

Doug Noland does a nice job of pointing out that the trillion$ of leveraged daily trade (carry trade) turns into a huge mess when rates start to go up even a little bit. FX, derivatives, you name it. All a big powder keg. And it is the FED’s job to bail itself out whenever needed.

Stock market: Is it up today because of Trump Trade Tweets, rather than because the Fed actions today are “good for stocks”? Also notable is that stock prices took a steep dive just because closing today, but still up overall. Will Monday be a big down day for stocks?

In my book, Fed’s choice of actions today signal that Fed is NOT going to support another bout of asset inflation? Am I right or wrong?

I have a slightly different view of why banks quit lending in repo.

Banks lend bonds to raise cash in repo. If the interest rate spikes, the expected cash raised is less, and the buyback is expensive and requires additional funds which need to be raised in repo putting more bonds on the market.

Once additional risk is perceived by other banks, the repo rate has a tendency to rise ahead of itself creating a panic to be the first out the door if there is an overhang of near future cash needs. It is the same sort of mentality in a bank run, and in the fright raised by a bank going the Fed discount window.

For example, if a bank goes out to repo and the last repo went for 1.5%, and bank B goes to repo and gets only 3%, the perception is that there is big risk and that bank B is desperate thereby rapidly raising their next repo costs, or if bank C perceives the need to raise cash and is looking for a better deal, bank C will rush to get the next bite of the repo apple driving rates up, fast, and so on. This is especially so if the other banks perceive themselves riskier than the last repo bond lender or they perceive rates rising.

Repo is a fundamentally unstable market and requires the Fed to cap rates. It is a phantom discount window.

Repos are unwound each morning.

Collateral is marked to market or repriced.

If your repo is “open” or “fixed”, then it needs to be reinvested again. The price of your collateral might already be smaller so either you need to put more collateral or post cash. So having a buffer works.

I just read a report that outlined the fact that excess reserves are part of the implementation of sterilization implemented during the GFC brought in to control interest rates. A brilliant case of hide the sausage.

That is why price discovery when let out of the cage spiked up the repo rates. Price discovery for treasuries must be suppressed at all costs. All of this makes the repo market unstable.

Stock market is closed on Monday

I can see stock trading sideways for few days and now the new earning season is there..

it may go up a bit till the mini trade deal euphoria wears off

Fed would do everything and anything to keep the asset bubble inflated.

A year back they were increasing rates but now for the last 6 months, they have decreased rates 2 more time.

F

Forward guidance for S&P 500 Q3 earnings is negative. Companies have been beating their earnings estimates, thus actual earnings might be close to flat. It is not a time of high corporate earnings growth.

An Iranian tanker was hit by Saudi missiles in the Red Sea. The price of oil bounced. The world is dependent on Persian Gulf oil exports. New fields don’t get developed overnight.

Stock markets are open on Monday but Bond markets are closed. No one knows how far this insanity will go ? went short midday today but may get my face ripped off Monday… LOL

My mistake.

Market open on Monday..

I guess the market stays sideways for sometime

Fed won’t let it plunge :-)

I did learn something useful from the Snider link: he quotes former Fed Governor Jeremy Stein as saying in 2013:

“Collateral transformation is best explained with an example. […]

… use the junk bonds as collateral to borrow Treasury securities from the [investment] fund. And why would the [investment] fund see this transaction as beneficial? Tying back to the theme of reaching for yield, perhaps it is looking to goose its reported returns with the securities-lending income without changing the holdings it reports on its balance sheet.”

I’ve repeatedly seen mutual fund descriptions which mention that a given fund may be “lending securities to earn income”. (Hello, Fidelity!) But it means that nearly any investor may be in the repo markets unwittingly (unless they read their prospectus with great care). Oh, and they don’t necessarily say who’s keeping that income.

Isn’t it nice to know that your fund is goosing returns for the managers (and maybe a slice for you) by lending out the very securities you thought you were investing in, so someone else can partake of them as well?

I do agree with you, Snider has perhaps the most dense prose of any financial writer I have read. Right up there with Alan Greenspan. Still he is very erudite so I read him ever Friday even if I have no idea what he is talking about.

In the USA, SEC Rule 15c3-3 limits rehypothecation to 140% of your margin account. The margin account also must be segregated. In London, there is no limit to rehypothecation. See what happened to Lehman and MF Global.

This isn’t margin accounts, these are mutual funds I’m talking about. The “lending securities” is done by mutual funds.

Wisdom Seeker,

Good to know! Another reason to dislike Fidelity, which I’ve generally avoided like the plague

What about Schwab or Vanguard mutula funds?

If in doubt, use Treasury Direct.

I don’t think it is even a broker.

I moved a chunk of my portfolio because of this fear.

Gandalf,

If you’re entertaining to invest in bond mutual funds, make sure you google something like this:

schwab bond fund class action yield plus

A series of Schwab’s big in-house bond funds collapsed during the Financial Crisis, with investors losing something like 60% of their principal. These were conservative yield investors that got cleaned out as if they were trading binary options.

Other brokers also had bond funds that collapsed.

Bond funds that exclusively hold US government-backed securities (Treasury, Agency, GSE-backed MBS, and the like) are OK because there is no credit risk and because these securities are very liquid.

But for everything else…. Open-end bond mutual funds are the most falsely advertised and mis-priced instruments out there. You are not being paid for the risk of a “run on the fund” which can wipe out your investment.

The problem they have is a “liquidity mismatch,” where investors can take their money out on a daily basis, but the underlying assets are illiquid and cannot be sold during tough times, except for cents on the dollar. And if you’re not among the first out the door – “first mover advantage” – you get your face ripped off during a run on the fund.

It’s OK to knowingly take risks if the potential gains are high. But in an open-end bond mutual fund, the potential gains are small, and the risks are high.

If you’re OK with small gains and want security, Iamafan has it right. Treasurydirect.gov allows you to set up an account managed by the Treasury Dept. It’s hassle free, fee-free, and pays the yield that Treasuries pay. It’s not spectacular, but it works, it’s easy, and you get your money back.

Thanks Wolf,

I’ve generally avoided bond mutual funds, period.

ETF’s are another bad investment strategy where liquidity mismatch can cause a collapse of the fund whenever things are going south in a hurry.

Corporate bond ETF’s, now that’s a double lethal combination.

WR:

Some of your finest advice EVER!

Yeah, what do people think of the Vanguard VMFXX fund? That’s the designated Vanguard settlement fund, and is supposed to be the safest of the safe, but still yielding better than t-bills. F stands for Federal, which means not-just-Treasury, but also GA debt and GSE MBS, and some unspecified but hopefully Treasury-only repo stuff as of this week. The content of VMFXX does seem to change over time (wish there was a history function), but overall my impression is that Vanguard is very conservative about risk management relative to most of those Wall St sleazefucks.

That’s my cash buffer. At least it makes interest. The only weird thing is how Vanguard computes interest. Something to do with beginning and ending month balances which I can’t figure out.

The average gap between an inverted yield curve and the onset of a US GDP recession is about 2 years (some say 21 months).

So, a US recession should not begin until about 2021.

My theory is banks don’t want to lend because the Fed is suppressing rates thus inflating assets which banks find more attractive, add the fact this (QE) has been going on for so very very very long the banks are learning and adapting and thinking “to heck” with this peanuts overnight rate let’s buy FX’s or something. Reminder: we are still at this very moment in FULL stimulus mode interest rate wise and have never ever ever ever not been in it for 11 years. Add to that – Powell’s transparently silly statement that his his QE isn’t QE if we call it “organic” or “not QE” when it is QE. QE is QE by any other name…a rose is a rose by any other name.

Why does a cash short enterprise need to do a repo if it can simply sell treasuries? They obviously have treasuries because they offer them as collateral under the repo arrangement.

Well, first of all there is plenty of private repo that is not Treasury-based.

Then there is the additional factor that repo is being used as a funding mechanism. As Wolf mentioned in a previous thread, companies like American Capital Agency Corp. (ticker: AGNC) will repo GSE MBS bonds every day of the year and pocket the interest rate differential. As Wolf said,, it works great as long as some bank will accept your repo at some lower rate.

I looked into AGNC. As of 2019-06-30 they had a portfolio of nearly 105B in MBS, of which they financed 85B with repos that cost 2.64% and have a duration from 0-3 years. Scary stuff if you ask me.

It’s cases like this that make me lose faith on the Fed. Why support liquidity for these companies at all? Should not be the Fed’s mission.

If companies like AGNC are using the repo facility as a way to speculate further, the Fed would be directly encouraging speculation in a manner more risky than the original QE programs. I doubt the Fed would go there, but who knows. They have already gone where no rational responsible monetary official has gone before.

Theory #1: There exists a very vulnerable investment bank in Frankfurt, er I mean Wall Street, that is very long on 10+ year treasuries in a very leveraged manner. In September, yields started rising. All the other banks see this because these funds are being pledged overnight to fund operations. The other banks realized they don’t really want to lend to this one struggling bank with such a huge leveraged treasury position. The repo market locks up. Along the way, a shrewd trading desk (or two) takes out short derivatives on this struggling bank. Without overnight funding, the bank is forced to sell their leveraged long term treasuries at a large loss to fund their daily operations. Boom, banking crisis 2.0.

Then Powell arrived to “save” the repo market. I didn’t hear any wall street banks singing his praises. Likely because he screwed up the trade that everyone was in on.

“Since Fed Chair Jerome Powell’s initial explanation on Tuesday of the new-new-new plan of only buying T-bills, the 10-year Treasury yield has risen from 1.52% when he was speaking to 1.75% at the moment. And the yield curve has steepened. The Fed hasn’t said this, but clearly, this system is designed also to un-invert the yield curve, and it has taken a step into that direction already.”

I just happened to be listening to a video about Stuxnet when I was reading this article, and I couldn’t help but compare and contrast the effects of this deliberately deceptive and destructive computer virus with the policies of the Federal Reserve.

The Stuxnet virus (actually more of a worm) would infect the controllers of the Iranian centrifuges used to separate U-235 and destroy them by increasing the speed of the centrifuges, and then suddenly decreasing them, over and over until the mechanical strain of over-speeding and then suddenly stopping tore the machines apart. Stuxnet also hid this behavior from scrutiny by sending fake messages to the central computer stating that everything was just fine, and the centrifuges were spinning at the normal rates for the entire time.

All of the warning lights were green, right until the machinery self-destructed.

Now I read that the machinery that regulates the flow of capital in our economy was about to rip itself apart, but the Fed has stepped in and is now fixing the problem by keeping the flow of money nice and steady. Oh, by the way, the yield curve has now been restored to normal from its inverted condition, and the signal that is used to indicate future recessions is now showing green instead of red.

False alarm, everyone, there’s no problem here, stop looking this way, resume your normal activities, go back to sleep, all of you sheep …

Correct me if I am wrong.

With rates higher than %1.8%, banks should find it profitable to lend in the overnight market. But there is a reason why they are not doing so. Either they have already borrowed to the hilt against the Treasury securities that they have on their books or because the credit quality of the banks borrowing the money is highly questionable.It has been rumored that Deutschland, Commerzbank and Barclays have been in trouble for a protracted period of time.

The Fed supplying money in the overnight market does alleviate the problem over the very near term, but does nothing to change the basic problem

There’s another “suspect”, JPMorgan:

“Although Deutsche Bank’s plunging stock price has many believing it’s in serious financial trouble — and the main cause of the repo market crisis — Reuters has public data that shows JPMorgan reduced its cash deposits at the Fed by $158 billion in the year through June — that’s a 57% decline. In fact, JPMorgan’s draw down on its cash accounted for about a third of the drop in all banking reserves at the Fed during the period.”

https://lenpenzo.com/blog/id57200-black-coffee-12-oct-2019.html

What we need is a reincarnation of Andrew Jackson.

What if you see the FED for what it is: a consortium of private banks. And combine that with the first rule of survival: “protect yourself before helping others”. What can we deduct then?

Long term debt has too much risk for too little return, compared to short term debt?

To me it looks like the FED is getting rid of long term risk (let the rest deal with that) and replaces it with someting (or anything) that is more predictable.

With coming negative interest rates, it is harder and harder to predict what the (long term) risks will be. Allegedly it is mathmatically impossible to calculate it. I’m not so good on integral calculations, but i do remember that you end up with a variable that is not defined. Something undefined is a risk you can’t measure.

For example: Einsteins E=mc2 is the result of such an integral equasion and actually should be E= mc2 + D, with D being the unknown variable. Einstein didn’t want to philosophise about what D could be and left it out. Maybe some day we will find out what it is.

To make this story short: i think the FED doesn’t want to be part of that equasion when we find out it is something desastrous. Therefore it has kicked into self-protection mode.

1) The 2Y, 3Y, 5Y..10Y are useless for repo. Sharply up this week.

2) But the weekly short duration 3M, 6M,1Y, are still down.

3) When the Fed buy short duration available inventory

is down.

4) The Fed constricting oxygen from the repo market.

5) Markets are up sharply on Fri. on Fed news and trading deal hope.

6) The DOW closed above the Jan 2018 high, the Buying Climax.

7) Since June 2019, for 4M, the DOW backup on Jan 2018 peak.

8) For 3Y the media Impeach, but markets are up.

9) For almost 2Y the market are in TR.

10) Someones dump inventory. Have a lot.

It take time. When ready the useful idiots from the media will

send markets down.

It is also possible that SPX next stop is 3,200.

stellar financial reporting . you have pulled together bits and pieces of articles from other sources and presented them in context. The How,why,when and where all addressed . Beer mug on the way !

Thanks. But I actually relied on the original sources: the data and info released by the New York Fed, various statements by the Fed, and the data base at the St. Louis Fed. For a few less important things, I relied on my own memory (Operation Twist, QE-3). I ignored articles in other publications.

The “Federal” Reserve’s banksters are always treating (covering up) the symptoms and not the disease. The economy is full of over leveraged companies and as to the major banks, the term “over leveraged” is generous. They are actually reckless in gambling with derivatives, because they have purchased enough politicians that they are sure that they will get bail outs.

The worries over all of these problems among investors and knowledgeable economists will not go away with this simplistic manipulation of short term rates to make the yield curb appear normal. The real job market is so bad that many have withdrawn from it: because too many jobs do not pay a living wage.

The ultra low interest rates have not just transferred the savings of millions of pensioners to the banksters. They have caused thousands of companies and others to be so over leveraged that the raising of interest rates to normal levels would trigger a chain of bankruptcies.

This cannot be easily undone with mere manipulation of short term treasuries. Thus, it may be motivated by short term, political considerations: i.e., to get cronies reelected. Nevertheless, there will inevitably be gigantic problems rolling over the enormous debts that the “Federal” Reserve bankster cartel have caused to be created. See the comments of Bob Prince, the co-chief investment officer at Bridgewater Associates at https://www.youtube.com/watch?v=DuTm1WA09uk

Soon, the banks will be demanding another bailout, when the economy has more problems. Even if the banks are essential to our nation, the crooks that have run our banks into the ground so many times (the control group of rich shareholders and crooked officers), who have gambled with derivatives, etc., do not have to still own those banks.

If any other business, e.g., a florist or plumber, becomes insolvent, the creditors take over its assets. If there is a chapter 11 bankruptcy, the creditors become the new shareholders and the prior shareholders lose everything. If the banks have to be bailed out, again, and if the Wall Streeters again try to panic the congress to bail out the insolvent banks due to Dow declines as in 2008, congress should require that in exchange for government aid all shares in the banks be transferred to the social security administration or some other government agency. (IF the banks need a bailout, they are legally insolvent, so their shares truly have a fair market value of zero.)

According to Forbes, the US has so many liabilities that it cannot ever meet them: $124-219 trillion. See https://www.forbes.com/sites/johnmauldin/2017/10/10/your-pension-is-a-lie-theres-210-trillion-of-liabilities-our-government-cant-fulfill/#763d5efb65b1

If the “Federal” Reserve bank cartel must again give aid to the insolvent banks, let the bottom 95% of Americans benefit, for once. Otherwise, I foresee that the social security payments of future retirees may just be enough to buy coffee as in Russia during its collapse in the 1990s. See https://www.washingtonpost.com/archive/politics/1990/05/20/millions-of-soviet-lives-pervaded-by-poverty/01fa67ab-7d05-483c-958c-21fc1db4e970/

The ultra low interest rates that the “Federal” Reserve bank cartel has established for about a decade have already resulted in zero growth even for private pensions, which have had to invest in risky businesses or else accepted returns below the real rate of inflation. Meanwhile, the “Federal” Reserve has used the US government’s credit to create wealth that it has transferred to the banks through ultra low interest rates on funds which it makes available only to the banks.

After receiving funds at ultra low, below fair market value interest rates, the banks turn around and charge average Americans 26 to 33% interest on credit card loans and all fees that they can invent. This incredible transfer of wealth to insolvent banks and later to banks engaged in risky derivatives and other gambling to give huge dividends to their corrupt shareholders for a decade must not be repeated without the banksters suffering any consequences. (A way that taxable dividends are avoided but banks transfer wealth to their shareholders is by stock purchases of their own bank’s stock. Then the stock prices go up and by selling shares the bank shareholders can get profits and pay only a low capital gains rate of 0%, 15% and 20%, depending on income of recipient, which are typically much lower than the ordinary income tax rate.)

Wolf,

When investors deploy capital to T-bills, this indicates a defensive or bearish posture.

So the Fed states loud and clear that it will be buying T-bills hand over fist for months to come. So what type of message is that supposed to send?

Also we learn today that this decision to launch the latest round of POMO’s was conducted via video-conference or in other words, via an emergency meeting.

Yah, all is well…

Seems the algos are confused or this observer is.

Awfully convenient that bond markets are closed on Monday. Will be curious to see how this unfolds the rest of the week.

Investors and companies routinely buy T-bills for cash management purposes (instead of putting the money into a bank account) — in other words, to have a safe place to store liquidity until it’s needed.

@HR01, your first sentence illustrates a common investing myth:

“When investors deploy capital to T-bills…”

The T-Bills already existed and were being held by other investors, so no new “capital” is being “deployed”. Existing T-bills are simply changing hands. T-bills are only added to (or removed from) the outstanding stock by the Treasury and the Federal Reserve.

Also, investors do not actually “deploy capital”. Investors trade bank credits (aka “liquidity”) for securities. With T-bill purchases there is no capital involved, merely credit and debt, which remain unchanged but in opposite hands.

The production of capital can be enabled by financial activities, but it’s a separate activity.

P.S. Bank credit is obviously not actual capital for the fundamental reason that the Federal Reserve creates and destroys it at will. Just because other people call bank credit “capital” does not make it so.