Vancouver sags. Calgary, Edmonton down from many years ago. Toronto rises but below 2017 peak. Montreal, Ottawa at new highs.

July is seasonally a strong month in the Canadian housing market, as tracked by the Teranet–National Bank National House Price Index. Over the past 21 years, the composite index for the metros has risen on average 1% from June to July due to seasonal pressures. This year it only rose 0.7%. On a seasonally adjusted basis, the composite index declined in July by 0.1%, after having declined 0.5% in June, and 0.4% in May – “pulled down by the three largest markets of Western Canada,” the report points out, particularly by Vancouver.

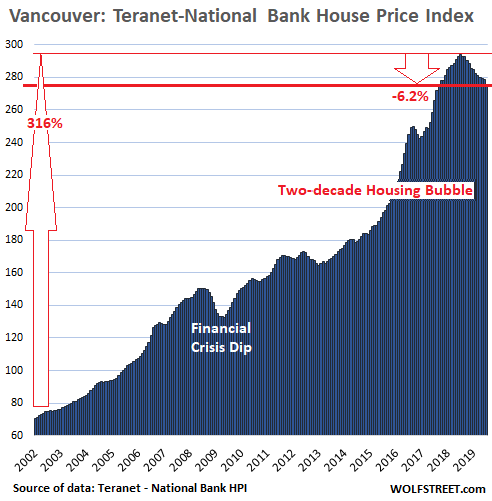

Vancouver:

Normally, July is red-hot for Vancouver house prices. In July 2017, for example, the Teranet–National Bank National House Price Index for Greater Vancouver surged 2.8% from June. But not this year. This July, house prices fell 1%, the 12th month-to-month decline in a row. Vancouver was once one of the most splendid housing bubbles in the world, with house prices having more than quadrupled in 16 years. But the Vancouver housing bubble is deflating. The July drop left the index down 6.2% from July last year, the steepest year-over-year decline since July 2009:

The Teranet-National Bank House Price Index tracks single-family house prices, based on “sales pairs,” comparing the price of a house that sold in the current month to the price of the same house when it sold previously, often years earlier.

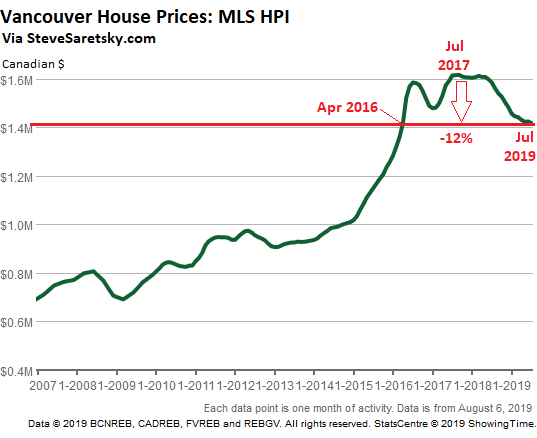

This produces a kinder-gentler and delayed version of the already kind-and-gentle official MLS House Price Index, which is based on a “typical” house with a “benchmark” price. This MLS HPI benchmark price for Vancouver fell to C$1.417 million in July, down 12% from July 2017, and is back where it had first been in April 2016 (chart via stevesaretsky.com):

Toronto:

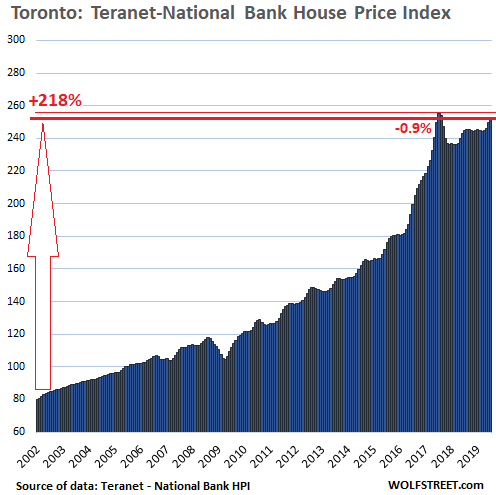

House prices had more than tripled in the Greater Toronto Area (GTA) from January 2002 through the peak in July 2017, with the index skyrocketing 218% — a huge increase in 15 years but just a pale imitation of Vancouver’s 316% increase.

In July, house prices in the GTA rose 1.3% from June, according to the Teranet-National Bank House Price Index, and were up 3.2% from July last year. This leaves the index down 0.9% from the peak in July 2017.

The charts on this list are on the same scale as Vancouver’s chart to show in relative terms how big the house price increases were in each metro. So, Toronto’s chart shows quite a bit more white-space than Vancouver’s:

The house price changes, as tracked by “sales pairs,” is based on how the price of the same house changes over time. The index tracks how many more Canadian dollars it takes to buy the same house over time. A price increase of the same house is a measure of how much purchasing power the currency has lost with regards to houses. If the price of a house doubles over a number of years, it means the currency has lost half its purchasing power with regards to houses. This makes this index (and similar indices, such as CoreLogic Case-Shiller Home Price Index in the US) a measure of house price inflation.

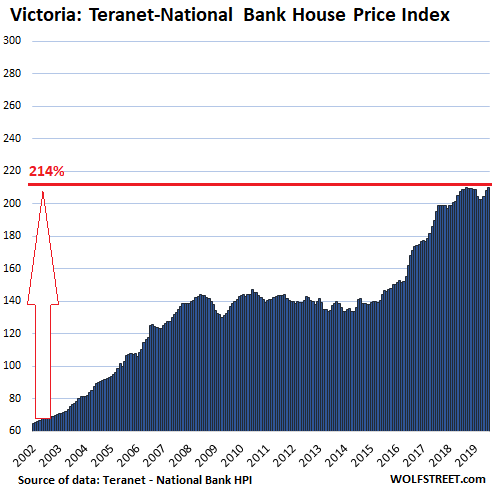

Victoria:

House prices in Victoria – having more than tripled between January 2002 and September 2018 – ticked up 0.6% in July from June, and was also 0.6% ahead of where it had been in July last year. The index and is about flat with the peak in September 2018 (chart is on the same scale as Vancouver’s):

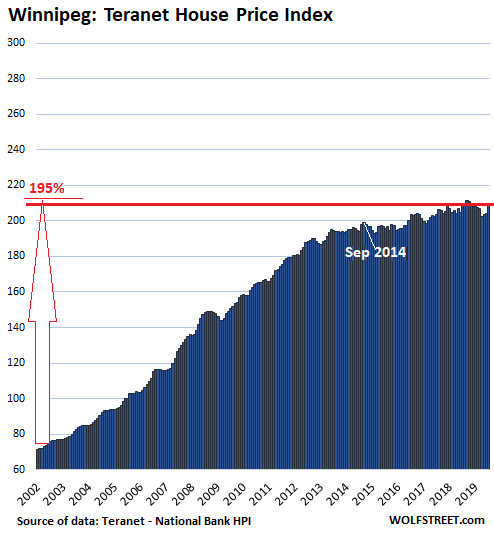

Winnipeg:

House prices in the Winnipeg metro jumped 2.9% in July from June. But on a year-over-year basis, the index inched up only 0.5%, and remained down 0.8% from the peak in September 2018. The index had nearly tripled between January 2002 and September 2014. But then prices stalled. In July, even after that 2.9% one-month jump, the index was only 5.5% higher than it had been in September 2014:

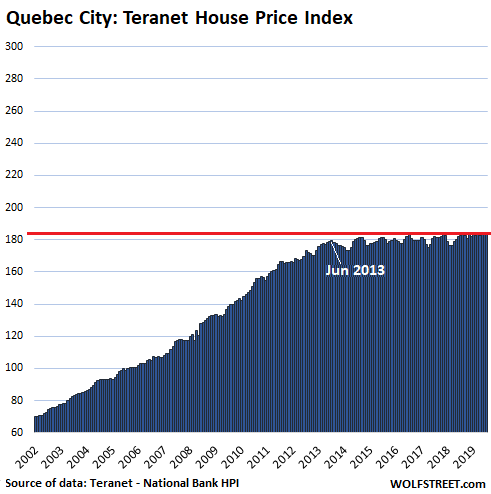

Quebec City:

In the Quebec City metro, house prices were flat in July compared to June and were up 1.0% from July last year, having been flat for the past seven months. Since July 2013, the index has ticked up 2.8% — essentially flat for six years, a sort of a hangover following the blistering 160% gain in the prior 12 years:

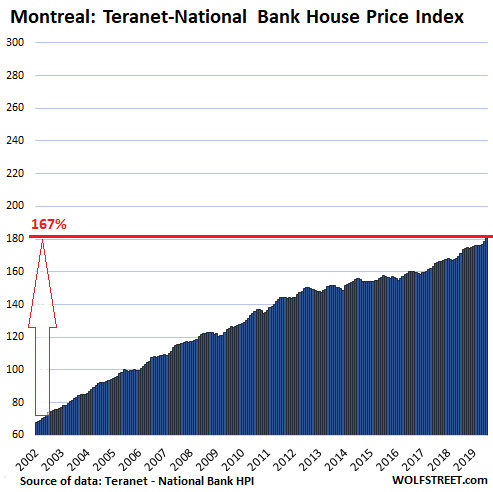

Montreal:

House prices in Montreal jumped 1.7% in July from June to a new record. The index has risen 167% over the past 16 years, blowing right past the Financial Crisis. But that was only about half of Vancouver’s crazy 316% price gain over the same period (chart on same scale as Vancouver’s):

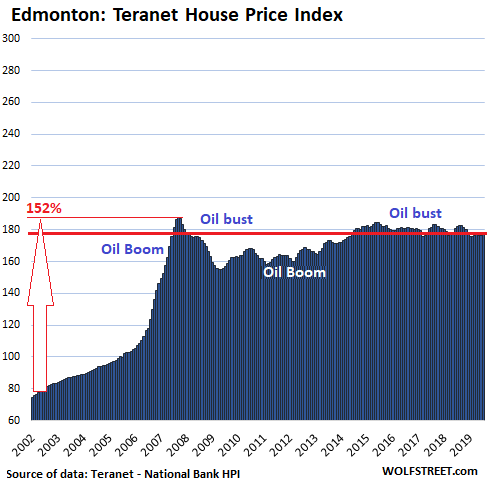

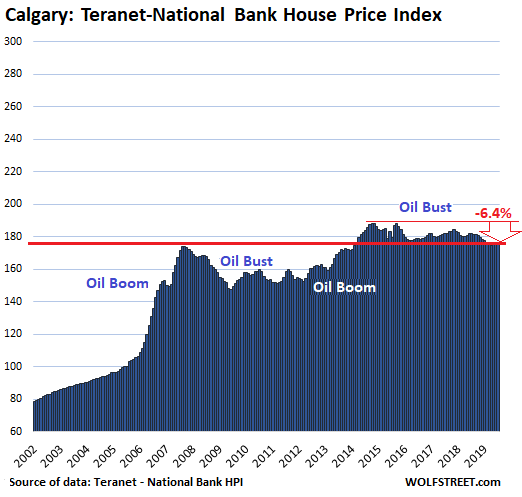

Oil Boom-and-Bust Towns:

Calgary and Edmonton, at the center of Canada’s oil patch, are dominated by oil booms and busts. In two years during the oil boom before the Financial Crisis, house prices in Edmonton soared by 87% through October 2007; and in Calgary, by 78%. But following the subsequent oil bust, these house price bubbles in Calgary and Edmonton deflated.

In Edmonton, house prices ticked up a smidgen in July but were down 2.8% from July last year and were down 5.8% from October 2007:

In Calgary, house prices rose 0.7% in July from June but remain down 3.1% from a year ago, and 6.4% from their peak in October 2014. The index is where it had first been in July 2007:

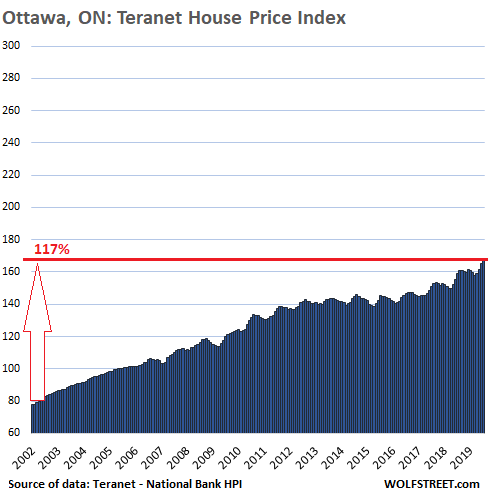

Ottawa:

House prices in Ottawa rose 2.0% in July from June to a new record, and are up 6.0% from July last year. Since January 2002, the House Price Index has risen 116%, meaning that it has doubled in 17 years, but given the splendid nature of the other housing bubbles in Canada, Ottawa occupies the lowest place in terms of price gains since 2002:

House prices in the San Francisco Bay Area dropped again – and ironically, they dropped the most in San Francisco and Silicon Valley. Read… Housing Bubble 2 in San Francisco Bay Area & Silicon Valley Pops Despite Startup Millionaires & Low Mortgage Rates

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

We’re still waiting for the glut of condos under construction to be completed.

The end of 2020 should give better insights as to what is really happening up North.

Stay tuned.

I think the reason Ottawa’s housing prices grew the least is because everyone knows their roads are paved with gold and central bankers have been busy suppressing the value of gold!

Do these stats take into effect the change in currency depreciation and on/or inflation?

The Canadian dollar was par to the US dollar a decade or two ago. Now the Canadian dollar has lost 30% to US.

The Canadian dollar was at par for a very brief period when oil was above $100. Anything is possible, but it’s highly unlikely to go back to par

Ottawa is consistently ranked one of the best cities in North America….could be that too. ;)

Based on who’s interpretation of “best cities”? It is a small town full of boring civil servants, end of story. Good for raising a family but outside of that there is nothing going on there.

All the government jobs are in Ottawa. Cutbacks probably had something to do with it.

Governments pushing people to drink the “Cool Aid” to tie the to the massive taxes that are tied with owning a house that doesn’t depreciate as they fall apart.

I remember when the cost of a house was strictly tied to their condition and not as an investment.

If my read is correct, the entire neoliberal project, embraced by both Republicans and Democrats here in the States and likely Liberals and Conservatives up in Canada, was very much to convince people, through home ownership and the 401(k), to think like and act like petty speculators and identify with “the market.” The falling rate of profit in the 1970s and the fears we see quite openly expressed in the Powell Memo of 1973 (plus the proliferation at that time of so-called “think tanks”) meant that the post-war consensus came under attack, and the entire heavy artillery of monied interests was aimed at undermining faith in unions and government and pushing “free market solutions” and “public-private partnerships” where the public took the losses and the private players garnered the gains. So the idea of a home as a place to live in, raise and family, and then die in and pass along to a future generation was dismissed as utterly quaint (kind of like drawing on a pension or having a good job that paid the bills and let your wife stay home and raise those kids).

The age of speculation and financialization and maximizing shareholder equity (a concept that entered law in 1979) had come.

The real beauty of neoliberalism was to make the asset appreciation that you noted above so mainstream, that the robber barons of old were now “legendary investors”.

@ Joe,

It depends on where you live, and how you live, so it is impossible to make all encompassing statements about taxes and home ownership. Our local Regional District rep fights very hard for us in order to keep costs down and reduce interference from outside Govt oversight to a bare minimum.

It is a major reason why we live here.

Our primary residence has increased in value 500% over 15 years, however there has also been much sweat equity invested in renovation. The raw land has increased 150% in 8 years with no development expenses other than some fencing. Taxes have only marginally increased over the same time frame. Our investment in a home has been far more effective than stocks or equities this past decade.

Add to this, we would have had to spend money living somewhere/anywhere, so any expenses we have incurred has been moot, and lower than if we lived elsewhere. In fact, by buying a fixer/upper home and renovating without a mortgage or finance charges is one reason why I retired early. If I were to do it again I would not have changed a thing. My kids have followed the same route by buying low, renovating, and retiring debt and mortgage commitments asap instead of trading up. Daughter will be mortgage free by age 44, son by age 40. Daughter is a public school music teacher and son is an industrial electrician. Their US cousins, with far more education and flashier job titles and salaries, carry 3X their debt and live on the edge of worry should work slow down.

It’s all about debt, imho. Plus, people need to be discerning in the choices they make, including where to live if at all possible.

Let’s just face it — there is a lot of luck involved. Looking back, you and your children were fortunate to get in prior to a major run up in prices. That’s great. I don’t know if the “buying low” is an option right now in many desirable places.

Leverage can work great when prices go up, but can also be devastating if prices go down. It least it used to be devastating. These days many people just declare bankruptcy or strategic default and pass the damage onto the general society. I don’t want to live in an economic system where speculators are made whole upon failure.

Amen

Where I live (Australia) the fixer uppers usually cost more than brand new houses. Land is expensive and taxed. Those options available to your children are no longer available for those younger if they are on a lower to medium income. Often the fixer uppers are bought by cashed up retirees in rural/ outer suburban locations, so moving to the outer suburbs is out of reach.

I hate to be the one to burst your bubble, but housing is just plain too expensive whether it’s land, old houses, new small units. The prices are out of reach with reality and that’s not the fault of first home buyers.

From an old fashioned perspective, housing costs should be a function of population increase (which could make current stock inadequate and therefore push up prices as homes become scarce), plus labor and material costs of building. When people talk about homes as a market, they seem to forget about these old fashioned material facts, and dive, unthinking, into the mentality of speculators. Are housing prices rising because of speculation, or are they rising because there are more Canadians around purchasing bigger new homes that cost a lot to build? How you look at this, and what you can do to address the issue, are fundamentally tied to the answer to that question.

“Canadians around purchasing bigger new homes that cost a lot to build?”

Canadians? In reality in Canada there is 60,000 empty houses, which owned by people not residing in Canada. Canadians in turn hunting for rental properties because the majority of them cannot afford to buy anything – neither apartment nor a house. So, who is buying as you say bigger new homes we do not know. But everybody say that young people (graduates from Universities) can not afford buying homes and often consequently they stay with their parents.

Or because the government is printing too much money?

That doesn’t ring true for me because Central Banks have, since 2008, been “printing money” to the tune of trillions yet inflation is not rampaging through most economies at a 1970s pace. The money is largely “sterilized” because it is being horded by a relatively small number of people with a low marginal propensity to spend. They can jack up certain asset markets, but they don’t induce systemic inflation. Perhaps they are jacking up Canadian real estate, but that just answers my question: this is all about speculation, and is not an organic process.

Canadian immigration rates are nearly 1% of total population, which is 2.6 times greater than the US, for comparison. That constant flow of the world’s best and brightest will fuel an unending housing boom for decades.

Very few new immigrants to Canada come with a boatload of money to afford this outrageous price

It’s a matter of time when chicken would come home to roost

When my family came to NA they migrated to areas where land was available. My wife’s family lived in a soddy north of Edmonton. Think of it, a home made out of a hole in the ground. They built up and onwards from there. Nowadays, new arrivals complain about the high costs of living in cities where everyone else spent generations becoming established. Millenials decry the lack of affordable housing, in some of the most expensive cities in the World.

Just saying……

Getting ahead with a home isn’t about just luck or timing. It’s about going where others aren’t, and getting established, before the rush. My best friend arrived,(where I now live), in 1940. He was 6 years old when he landed on the Kelsey Bay wharf, courtesy BC Steamship Company. He dropped out of schoo and made good wages his whole life and spent a lot of money in the pub and on fast cars. He still spends a great deal of his pension on his truck. I rent him a cottage for $350/month because he never bought a home, and there was always one reason or another not to buy. I can list 50 aquaintances in the same boat. People that did buy in the early phases were set for life.

If a person has skills people need to pay for, opportunities abound in the hinterlands. Plumbing, electrical, carpentry, hd tech (heavy duty equipment mechanic), equipment operators, are all trades that pay 100K and up, provided people move to where the work is. Coincidentally enough, land and housing is available where this work is at a far lower price than what drives these stats. If you want to set up in a city or subburb? Guess what? Unaffordable, and always has been for the most part.

Uh no, housing costs should be a function of INCOME. Localized housing prices need to be supported by local incomes UNLESS of course the government allows foreign money to flow into an area to skew the normal market mechanism. Governments love to see housing prices go through the roof as they are more worried about their own bottom line than the actual citizens they pretend to represent.

Based on my quick read, it appears the Canadian housing market is holding up pretty well relative to the US housing market in the financial crisis.

The FC unfolded slowly, things stagnated and started slight declines before they really started accelerating losses.

Too early to make that call, IMO.

I read if you earn $120k a yr in Vancouver, you can not afford a house. Maybe Canadian dollars, not sure. Some Chinese invested in Canada for dual citizenship. I presume some of these were fearing mainland Chinese repression. An acquaintance from Toronto told me there is a large Chinese immigrant community in Toronto.

You are right. 120K in Vancouver for someone not already a homeowner is chump change. Move 150 miles away and you are royalty and living a good life. You have to have skills to suit, though. Or, work away. Managers, MBAs, lawyers…you are stuck. Engineering and design often contracted out, overseas. Trades and tech skills? Willing to work away? Great wages, lifestyle, and respect. Your job is protected by foreign worker restrictions and wages are supported by union collective agreements.

Never been a better time to buy! Ask any realtor, they will back me up on this one.

Ask socaljim, if you don’t buy now, you’ll be priced out forever!!!

I get these mailers that pretty much say just that! I feel like asking one of these local realtors “Is it a buyer’s market or seller’s?”, and I expect the answer to start with.. “hmm.. are you looking to buyer or sell?”

If you’re buying Canadian RE in $USD….this probably is the best time ever, as the USD is currently at 20 year highs. ;)

That’s about 8% return per year. You guys must be getting big raises up north.

The average Canadian household wealth is about double compared to the Average American household. Canadians are indeed richer, on average.

I should have said 8% appreciation. Read somewhere that real estate bubbles are the most dangerous. They involve high leverage and banks.

Stocks down 50% you still have equity. Real Estate down 50% with 10% equity in it there is a big problem.

10% equity is not home ownership. It is a renting to own agreement with property taxes thrown in on top. All in the hopes of RE appreciation.

If I was 20 and starting out I would buy a rural property and put a used fifth wheel on it. Pay the land off then build a home. A friend of my son-in-laws is doing just that. He bought 7 acres in the Cowichan Valley, did the trailer thing, built the smaller house, then will build a larger home as his family grows. The pan is to rent the first out for extra income. He is a ten minute drive from downtown Duncan and 30-40 minutes from Victoria.

He builds furniture for a living and is now in his late thirties. In 20 years people will drive buy his home and wonder how he got so lucky? Was it timing? Or was it a savvy plan and hard work?

When the housing bubble bursts is anyone going to be able to afford to buy his furniture?

Can someone tell me what caused Toronto and Vancouver prices to climb so rapidly starting in late 2016? I don’t think Canada had any Quantitative Easing going on. Was it the bank of Canada’s surprise cut? Was it more rapid capital flight from China? Was it animal spirits of market participants? It really boggles my mind. Starting to wonder whether prices will ever return to traditional “fundamentals” relative to income and rent.

In addition to being immigrant friendly, Canada is also a safe haven for HNW individuals. —- in case you haven’t noticed, the world is pretty messed up at the moment, and will be for the foreseeable future.

In YVR, money laundering with a complicit Govt raking in the 1% RE tax had a lot to do with it….all urged on by connected and influential right wing RE developers. Seriously…this is not just cynicism. Investigations ongoing.

Amen,brother.The previous provincial govt turned a blind eye to the money laundering and off shore buyers parking their often ill-gotten money in Vancouver real estate as the real estate industry was lining the politicians pockets and the revenue from the BC property purchase tax was making the governments bottom line look good.

Thankfully our new govt has taken steps to curb the insanity but for young people looking to get into the market,it’s probably a lost cause if they want to ever buy a house in greater Vancouver or Victoria.

The two rate cuts by the Bank of Canada in 2015 (the U.S. did not cut) and the influx of Chinese did it. The two cuts were because of the slumping price of oil. The two cuts did nothing for the oil market but fueled the speculative housing bubble.

Just read a saying by Jeff Gunlach that might apply to Canada housing and to many countries: You can’t save your economy by destroying your financial system.

When is everyone going to figure out that these aren’t bubbles. This is inflation and it’s permanent. As in the purchasing power of your fiat dollars have permanently declined and not coming back. Or do you think that these house prices or any asset prices are going to revert to 2015, 2010, or 2000 prices. These are not bubbles. It’s called inflation, and more is coming.

If house price inflation is not associated with similar wage inflation, after a while you will run out of buyers who can afford to buy. Then the hype brakes, and everything goes into reverse. Just check how it went in the past. Even Canada had huge housing busts, but just not in 2008.

BTW, check the charts of Calgary and Edmonton.

I reviewed the Edmonton and Calgary graphs again. I didn’t see a significant retrace of prices in the previous 15 years. Are you suggesting that prices will revert to year 2000 prices when this “Bubble” bursts? They won’t. Prices will fall but inflation has set in and will back stop any reversion to historic prices. And just like the Fed Balance Sheet will never go back to year 2000 levels, neither will asset prices. Look at housing prices in the US. The first “Bubble” burst, prices kept rising. The second “Bubble” will burst and prices will keep rising after a temporary fall. It’s called inflation. Do you expect healthcare costs to fall back to year 2000 prices. Of course not because you recognize the inflation effect. Bread costs $5 a loaf not because of bread products are in a bubble, but because of inflation. If everything is in a bubble, then there is no bubble. It’s inflation. Pure and Simple. Prices are not going back.

I’ve posted a similar idea previously – that one might make the argument it’s not a bubble as the price of most everything non-perishable has gone up in lockstep. But I conclude that the deciding factor in whether prices retrace is simply sustainability of current prices, which I think really just means price to income for debtors, since leverage causes fragility and unsustainability.

So, I’ll go out on a limb and say that we’re in a bubble and change my mind only when wages start increasing rapidly. A lot of malinvestment is occurring, causing fragility and reinforcing the bubble scenario. At least I can look forward to a subsidized dorm-style room from We Company.

The resale market in both Edmonton and Calgary are where all the damage was done. Prices for resale townhouses and resale apartments today are down 50 (fifty) percent from the October 2007 peak in Edmonton. The same is true in Calgary.

Is Toronto real estate market in a bubble and how long will it take for it to burst. Or the market has room to grow further as it has not reached heights of Vancouver real estate growth, meanwhile, the immigrants keep pouring in and most choose to make Toronto as their home

Here is a data point for everyone to chew on:

” According to ATTOM Data Solutions, a leading real estate data provider, only twice in the last five recessions—in 1990 and 2008—did home prices come down. In 1990, prices decreased by less than a percent. During the other three, prices actually went up.”

My expectation is prices will hold up in the next slowdown for reasons I have stated many times.

That’s a ridiculously biased source, as it only focused on the impact to values during the actual recession, which is a small period of time. In 1990, prices fell further after the recession ended, and stagnated for nearly a decade. In 2008, prices slid all the way to 2012. We were out of the “recession” in 2009. I can’t tell you how many realtors I have seen post graphics citing that study as they get increasingly nervous.

You are also discounting that up until the past 25 years, housing wasn’t subjected such boom and bust credit cycles as we have now.

Looked at the FRED graph that starts in 1963. The home price graph is at the national level, and it has recessionary areas shaded. The graph seems to match what AATOM concludes. Take a look …

In my opinion, during a recession, there are always deals to be had. It is just in some recessions, there is very little deflation or even a little inflation, and prices hold up just fine.

sc7 says:

“You are also discounting that up until the past 25 years, housing wasn’t subjected such boom and bust credit cycles as we have now.”

Just after college in the 90s, I was looking at beach close fixers that were priced around 300K. People were telling me I should rent and wait because it was a bubble. They said 15 years before that ( i.e. late 70s ), those same homes were selling for 50K so it was a bubble and it would crash. The mistake they made is they did not understand the central banks rig the system with a small amount of inflation … Bottom line is if you believe the central banks will keep the economy on the tracks over the long term, then a small amount of inflation is a must, and a long term investment in quality real estate is the slow but steady way to build wealth … the inflation compounds yearly .. the trick is you have to live long enough to benefit, and you have to start young.

LMAO. As a Canadian living north of Toronto I personally saw prices drop between 30 to 50% in the early 90s. New lake front condos in Barrie sold for $50k, less than half their original price.

Once upon a time houses were homes not investment opportunities. The goverments should have intervened with rent controls, tax on foreign investment, help increase land availability, invested in social and rental housing through tax incentives and increased capital gains tax on real estate. Unfortunately they must have seen the uncontrollable rise in prices and flipping as job creation and a cash cow with support from banks, corporate interests, and the top 10%. Unfortunately it has been at the expense of the vulnerable, working middle class, young families as well as those who saved their money for a downpayment that keeps 2 steps ahead.

Canada definitely needs more social housing /rent control complexes…there are some, but not nearly enough.

You must be joking? I grew up In Toronto next to a public housing project. Once they entered they never left. It might as well have been a graveyard. The last thing this country needs are economic dead zones and poverty traps. As to Rent Control, yeah let’s keep the rents and by default their portion of property taxes down so everyone else can pay more. Of course, there are government Coops, however I never met a Co-op resident who wasn’t a union member, generally public sector, and somehow I imagine they weren’t there for society’s benefit.

Teranet…chuckle.

Social media is awash with real people posting dozens, even hundreds of examples of Vancouver houses selling for 25-50% below peak, yet Teranet’s data still doesn’t show it, despite the fact it’s been going on for almost a year now.

The charade is wearing very, very thin, and even the unwashed masses are starting to see through the BS data game.

The teranet index is backwards looking in time and is not a good indicator.

Can anyone provide a “cost of replacement” graph. Surely the measure of a bubble can be seen by looking at the replacement cost of a property. If developers are building for $300,000 and selling for $700,000 then there is a bubble, no doubt. If they are selling for $350,000, not so much.

At the rate that crap houses are going up around here (tiny lots, crap construction materials, lousy workmanship), I’d bet that they are making a pretty penny. I pity anyone buying a new place these days.

A lot of Canada’s housing is being driven by immigration. More particularly, many hi-tech firms are expanding operations especially in Toronto and Montreal, bringing in qualified people from around the world, as the US is restricting green cards/visas, plus Canada is cheaper to operate in, but integrated with US economy. The explosion of condos in Toronto, Montreal is to a large extent housing these type of hi-tech singles.

What puzzles me, is if your reasoning is house appreciation is due to real inflation (not a bubble), then why are bonds going up so much and bond yeilds almost negative? It’s a bubble because there is too much cheap money in the system. Hopefully the Fed doesn’t cut rates again which will inflate the bubble even more.

Meant as a comment to Reality above..

There is no reason why the Canadian housing market should perform any differently than the US housing market. Yet, there remains substantial differences between both markets. Canada seems to be such a back box when it come to RE info. It would be interesting to compare Teranet–National Bank National House Price Index methodology with that of Case-Shiller Home Price Indices.

Rates of immigration to Canada are nearly 3x higher than the US. Combine with the fact the vast majority of Canadians live in just a handful of cities, there will always be insatiable demand for RE.

After reading many comment above, actually, everyone are correct, property valuation (medium price/medium income) will fall, but the nominal CAD dollar value will not fall as much.

When price starts to fall sharply, then Bank of Canada will immediately debase the currency by 20-30%, as such, everyone just loss currency purchasing power. All you need to look at is what’s happening in Australia now, and what happened to US in 2009-2010.

However, the after effect of the debase the currency will have profound impact on the Canadian society for many years to come. Canada may even have Trump like PM in the future…

Home prices will rise sharply in Canada as mortgage rates fall. The only place that will continue to fall in price will be Vancouver. If Trudeau gets re-elected this October home prices will rise double digits in the GTA and golden horseshoe year over year. I live in Canada I can guarantee this 100 percent.

I’m late to the party here but this is a phenomenon I only see in Canada- a complete and total refusal to acknowledge that houses are detached from incomes and therefore susceptible to a correction or crash. I lived in NYC during the GFC. Watched friends get laid off and lose jobs from Lehman, law firms, legal recruiting shops, etc. landlord lowered my rent so I wouldn’t leave because others were having a hard time getting tenants (despite nyc having high immigration, high paying jobs, shortage of apts, etc). Here in Toronto there is like extreme defensiveness from people if you mention “bubble” and they recite the same talking points seen here about how things will only go up. I cannot understand why all this hubris. Bottom line, my friends got jobs again, my rent went up eventually, etc. life goes on. Let’s live in the real, friends.