The bifurcation among consumers.

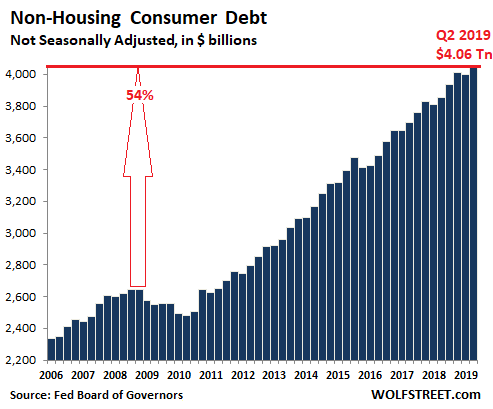

Consumer credit – auto loans, student loans, and revolving credit such as credit card balances and personal loans, but not housing-related debt such as mortgages and HELOCs – grew 5.4%, or by $208 billion, in the second quarter compared to a year ago, to a new record of $4.06 trillion (not seasonally adjusted), according to the Federal Reserve this afternoon.

This 5.4% year-over-year gain was the strongest such gain in two years. The quarterly gain from Q1 to Q2 of $60 billion was the strongest such gain since Q2 2016. In other words, American consumers are not slackers. They are doing their collective job, propping up the US economy, and by extension the global economy, with money they don’t have:

Every dime of that additional $60 billion that consumers borrowed in Q2 – and of the additional $208 billion they borrowed over the past 12 months – was spent and became part of the $14.5 trillion in annualized consumer spending, nudging it up by about 1.4%. Consumer spending accounts for nearly 70% of the economy, as measured by GDP. Everyone and everything depend on these consumers to consume, which is their function. That’s why they’re called “consumers,” and not “people.”

In the chart above, note the sharp and relentless increase since the bottom of the Financial Crisis. Since 2010, consumer credit balances have surged 60%. And since the peak before the Financial crisis in 2008, they have surged 54%. So how did this happen and what does this mean for the American debt slaves?

Revolving credit

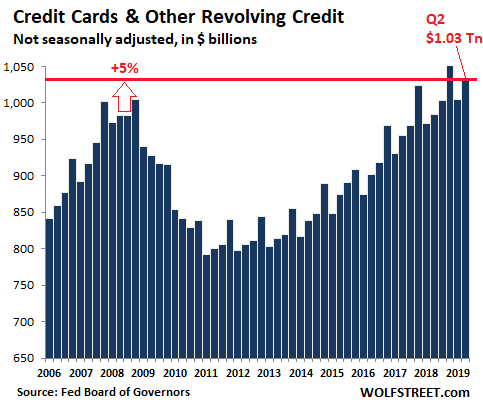

Outstanding balances on credit cards and other revolving credit, such as personal lines of credit, rose 4.8% in Q2 compared to Q2 last year, to $1.03 trillion (not seasonally adjusted). This was a record for a second quarter, and was below only the holiday shop-and-borrow season, Q4 2018:

As laudatory as these efforts may seem on first sight, consumers have actually been fairly lackadaisical with their credit cards. Since the prior peak just before the Financial Crisis in Q2 2008, so in 11 years, credit card balances have edged up only 5%.

Over the same period, the Consumer Price Index rose 17% and the US population rose about 8%. So adjusted for inflation and per-capita, American consumers have shed credit card debt.

In terms of GDP, in 2008, credit card balances amounted to 6.6% of nominal GDP. In Q2 2019, credit card balances amounted to 4.8% of nominal GDP. So clearly, in terms of credit cards, consumers have learned their lessons. Or so it seems.

In reality, there is a bifurcation.

Many consumers pay off their credit cards on a monthly basis without sweat and use them only as a payment device and to gain loyalty awards. They don’t carry balances on their credit cards, and they don’t pay credit card interest. Their credit-card activities are not reflected here.

Then there are the tapped-out consumers with multiple maxed-out credit cards, or with credit cards with large balances, and consumers with personal loans, payday loans, etc. And they’re paying a fortune in interest at double-digit rates because they don’t have the money to pay off those loans. They can barely make the minimum payments and get to the next paycheck.

These are the folks who owe that $1.03 trillion. And this is why credit card debt curdles so quickly during a downturn. People with credit card debt have little wiggle room.

Auto loans and leases

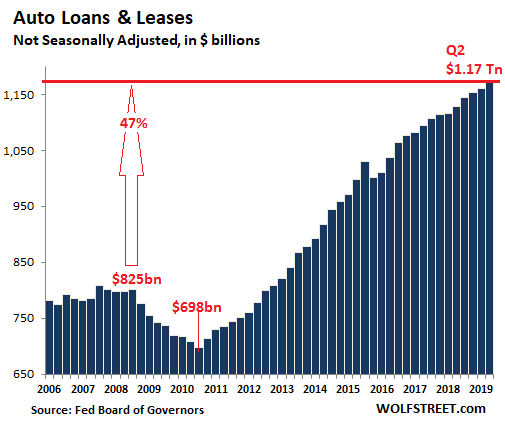

Total auto loans and leases outstanding for new and used vehicles in Q2 rose by 4.0% from a year ago, or by $45.6 billion, to a record of $1.17 trillion, despite new-vehicle sales that declined by 1.5% in the same quarter, and despite lackluster used-vehicles sales. This 4.0% increase in auto loans is the consequence of higher transaction prices of new and used vehicles, an average loan-to-value ratio that continues to tick up, and the lengthening average duration of loans:

Since 2008, auto loan balances have surged 47%, compared to the increase in the Consumer Price Index of 17% and population growth of 8%. So, on an inflation-adjusted per-capita basis, the burden of these loans has increased. But in terms of the size of the overall economy, auto-loan balances have remained at about 5.5% of GDP.

The bifurcation of consumers is not so straightforward with auto loans. Auto loans here include leases. Many people, including wealthy people, lease a vehicle not because they lack the moolah to pay cash for it but because leasing brings real and perceived advantages. Even buying a new vehicle with a subsidized loan can be an advantage for people with cash to burn.

But there too is a bifurcation of consumers – the subprime end.

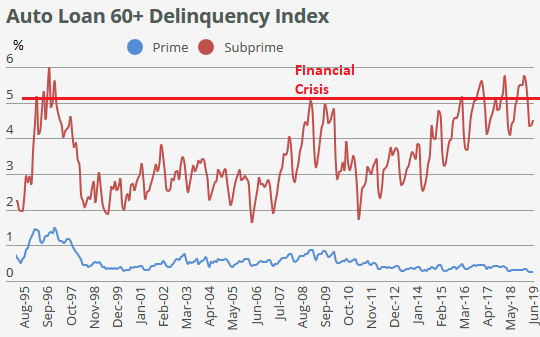

Subprime auto loans account for about 21% of total auto-loan originations this year. Delinquencies started ballooning in 2015. By 2018, subprime auto-loan delinquencies — as measured by Fitch Ratings, which tracks subprime-auto-loan-backed securities — were exceeding the levels during the peak of the Financial Crisis and were back where they’d been in the mid-1990s during the subprime auto-loan bust. Some smaller lenders specializing in subprime auto loans collapsed last year. Lenders have started to tighten up their standards. And delinquency rates have stabilized over the past year at very high levels. The low and falling delinquency rate for “prime” borrowers (blue line) illustrates the bifurcation:

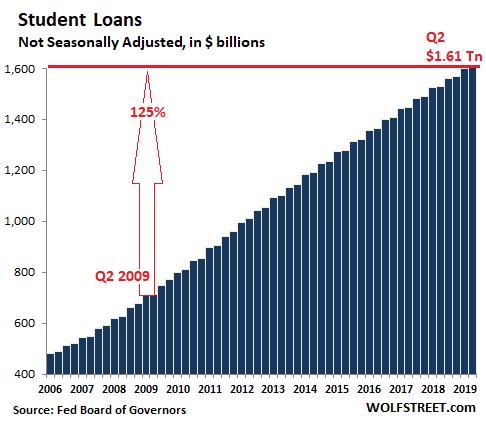

The University-Corporate-Financial Complex

Student loans rose by 4.9% in Q2 compared to Q2 last year, or by $75 billion, to a new horrifying record of $1.605 trillion (not seasonally adjusted), having skyrocketed by 125% in the 10 years since Q2 2009.

But that surge in student loan balances is not because there are more students enrolled. On the contrary: According to the latest data available from the National Center for Education Statistics, enrollment fell by 7% between 2010 and 2017, from 18.1 million students to 16.8 million students.

So who got this $1.6 trillion that students now owe and that the taxpayer guarantees? Students are just the conduit for this money. Who ends up with it? Universities; Apple and other companies, such as textbook publishers, that focus on selling their goods and services to students; other participants in the economy such as grocery stores and concert venues; and importantly, investors in a booming asset class called “student housing.” They are the recipients of these taxpayer guaranteed funds. And every dime of this debt contributes to the economy as measured by GDP – on the time-honored principle of Apocalypse not now.

In the most expensive US markets, apartment rents hit a ceiling, in some cases years ago, and have dropped since. That this wasn’t a brief fluke is increasingly apparent. But rents in 10 other cities surged by 10% to 15%. Here’s how rents have changed in the top 100 markets. Read… Hottest, Most Expensive Rental Markets Unwind

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

I think you mean propping up China’s economy. Cause most of our trade goods come from China. :)

pure tongue and cheek here. I know in reality, we’re all consuming a lot more Starbucks and Netflix, and it’s a service oriented economy that is winning out.

Doh, hit send too fast, we shouldn’t call them consumers… that’s not reflective of what they are. But I have a new phrase, let’s call them what they are. (By they, I include me too). Con-Shee-ple.

Hey, that’s a good one, let me trademark that phrase. But I’m happy to assign Wolfstreet that particular trademark. Con-Shee-ple… or just plain old consheeple.

I wonder if we can get that into the dictionary with a picture of your typical American consumer in it.

By their insistence on maintaining a lifestyle they cannot afford, the consheeple enthusiastically pad the profits of everybody else.

But Wolf’s description is even more apt imho: debt serfs, selling out their future. And in doing so, competing in the marketplace with money they don’t have, they drive up the prices on everything (houses, rents, vehicles, …).

I think the Fed should start referring to them as debt serfs, the saviors of our economy (and particularly the rentiers also beloved of the Fed).

As I’ve said before regarding the dollar, I always go with the coin of the realm, it’s our history. But in this context, you are always free to start your own country.

Denny’s bull run of debt, but investors love DENN.

Went to Denny’s restaurant today.

DENN was in a 3Y slump, between Oct 2000 to Aug 2003,

but on Feb 2004 DENN made a jump.

In 2009 it fell on top of 2000 the highs. Since then DENN enjoy a nonstop bull run.

Denny’s lead the stock market higher & higher, on a sugar high.

Its relative strength vs the SPX is up.

DENN is even stronger than the restaurants & bars sector and stronger than consumer staples sector XLP.

DENN bull run fueled with debt.

Total current liabilities 98.73 is higher than total current assets of 57.42.

Total liabilities 581.31 is higher than total assets of 438.74.

Equities = (-) 142.57

Retained earnings = (-) 257.08.

Many Denny’s customers are hooked to a walker.

Shocking. I mean usually when a company takes on excessive debt, degrades its products and services, and jacks up its prices (all things I have observed with Denny’s), private equity is involved.

So I looked it up. Yes, private equity.

Who could have guessed?

I don’t think I understand how this is done and the implications of this. Is the private equity essentially transferring money from the investors (via debt, which destroys the stock later on) to their own books, and hollowing out the company (Denny’s) in the process?

Isn’t that somehow fraudulent?

Dale, I’m sure they are within $50 million (legal fees) or so of being legal, and all big business has been working on “business/financial” laws since a big spurt in these efforts around 1970.

My other and bigger concern is loss of public companies.

4,775 in ’75

7,322 in ’96.

3,700 in ’15

No wonder market goes up as this trend goes on.

Just like anything else rare.

Then it’s bye-bye pesky gov’t controls.

Already about 85% of world’s food supply by sales is in private hands.

Disturbs me, anyway.

Should have addressed Richard, sorry.

In my town, Denny’s does well because everything else closes at 9. There’s Denny’s and IHOP and it took well over a year to get the IHOP open again when it closed.

But in the end, hookers and drug dealers and their clientele gotta eat!

My boss and I used to go to Denny’s then tried the IHOP once, and I dunno, just haven’t been going to either any more. It’s just too expensive.

I think the good news is that the Non-Housing Consumer Debt chart still looks (just eyeballing the chart) linear. That is, the rate of growth doesn’t appear to have increased perceptibly. I worry most about an increase in the rate of growth that gives an exponential chart. But I guess flattening out isn’t great, and a negative rate of growth isn’t good either. But the last two cases mean consumers are handling their debt load, the first one means a lot of people are heading down the tubes faster, and a crisis is in store.

it’s a new plateau. ya just gotta believe!

Putting interest rates at or near 0% means you can borrow whatever you want since the bucks have become worthless ( for savers ).

And that is where we are : fiat currency is worthless. Unless one is poor and needs credit cards to buy food and other essentials. Or if needs a mortgage for buying a house. THEN you are really fucked, THEN you pay your butts off for the glory of the banksters.

In regard to credit card debt it should be noted that cash is being used less and debit and/or credit cards are growing both individually and corporately.

We live in an E world!

Credit card balances (debt) in this article are only amounts that have become interest generating for the lender — so not amounts that people run through their cards just to make payments and pay off every month.

And a debit card by definition is not credit (and not debt) but a way to draw your own existing money out of your bank account directly, sort of like an instant check.

A lot of places in my town, those card readers do. not. work. So while I’ll use some places with the few readers that generally work as ATMs, doing my purchases and getting cash back, I use cash a lot.

When I am putting around the house I like.to listen to Dave Ramsey on radio. He has turned the debt lemon into lemonade. It’s funny that he works so hard to get people out of debt while central bankers work so hard to make sure debt expands. Anyway he has turned debt reduction into an enterprise that I am pretty sure is worth more than $100,000,000. Maybe several times that.

Listening to people call in you can see that the typical person has substantial college debt, a big car payment, a house and then they have the wake up moment that if they don’t take drastic action they are going to be debt slaves the rest of their lives.

One thing that I have noticed is that a lot of females have fallen in the trap of getting multiple degrees in a poor paying field and have college debt multiples of their income sometimes as high as 5X. Very sad.

Dave Ramsey also tells people that they can rely on 12% annual return from stocks. Maybe he is right, as the Fed has proven incontrovertibly over the last 30 years that they work for Mr Market and not for the United States.

That bothers me as well and I think he will regret saying that. It’s interesting that his mutual funds have averaged 12% over last 30 years of debt expansion. If market drops by 2/3 that 12% becomes 4%.

Don’t think TPTB will allow “the dow” to drop.

I personally revile the entire financial system, but that revulsion and purposeful effort to live outside of it have gotten me nowhere.

If we see a 2/3 retrenchment, it is t s h t f scenario and no one will be immune , unaffected, , or floating high .

I wonder how much higher HELOC balances are today than they were from their initial draw and/or median balance? I suspect the balances owed have inched upwards.

No one, especially the parents nowadays, ever asks little Suzee what she plans to do for a job after receiving her underwater basket weaving degree. The parents just keep writing the checks so Suzee stays happy and doesnt end up selling herself at truck stops.

Funny thing is, I remember a big hollywood producer (boyfriend of girlfriends’ Mom) ask me what the hell I was going to do with my life by learning computer programming in college back ~1991. Parents didnt feel I was going down a good path either (No joke, my Mom thought I should focus on writing since I was good at that as well, lol), but I could see the future in that everything engineering related (I started out studying applied math) would be done on computers and that I better get good at using them.

Of course there was no easy money for starving students back then so I ran out of money (recession sucked in the early 90s, tuition tripled in a few years) but had enough credits to get the sheepskin. Started working, dot com boom hit and the rest as they say is history.

Well I sure as hell wish I’d gotten a degree in basket-weaving!

First, instead of working 20 hours a week, commuting 10, and trying for an EE degree, I’d be doing that for my basket weaving degree. Which means I’d have finished just fine.

Next it means I’d be able to weave some mean baskets, which if sold by the side of the road, pays better than any of the non-existent ‘tronics tech jobs that theoretically exist around here.

Then, with a 4-year degree in hand, since the gatekeepers only want “a” degree, I’d be able to get certified to teach English as a 2nd language and get paid to do what I did an awful lot of when I worked as a tech anyway.

In looking at my relatives kids vs. ancient history (when I was in school) I’m exceedingly depressed by the inability of our very expensive education system to produce individuals who, at 18 years of age, are capable of being on their own. No idea as to what jobs they are fit for (let alone prepared to take on those jobs), no ability to house, feed, or care for themselves, and worse, not much incentive to correct that.

And now we have politicians trying to buy votes by forcing taxpayers to assume the student loan debt. And those debt slaves, thinking this is great, fail to realize that a) that means they’ll still be paying for it only at a higher rate of interest, and b) that this sets a horrible precedent for the Federal gov’t’s transferal of private debt to the working individual who has no say in what was bought or how it’s use could possibly benefit those now responsible for paying it off.

It’s no wonder the two newest generations fall for the lies pushed by some of our politicians. They have never been forced to face the reality that everything has a cost, and mom and dad (or the grandparents) won’t assume those costs forever.

When did school become a job training center?

They used to be about education.

Too many expect too much from the education system. What about the family helping to get those youngsters ready for a “job”?

We expect our teachers to be mother, father, baby-sitter, counselors, and so much more.

Having more than the first 7 of my 15 grandchildren graduating from high school, almost all either in college or finished and getting decent jobs I would argue….What more can we expect from our schools?

Parents have to step up to the plate also.

That is their role.

Not the education system.

When I did my university degree in the UK in the 80’s tuition was free. Only 65 of people use to do university degrees and the subjects were relevant.

I studied mechanical engineering and remember that psychology degrees had just be added. In our engineering department toilet, we had a sign above the toilet roll holder saying “psychology degree – take one”.

I was amazed that they would be worth anyting but they all got good jobs in HR departments which was a new company position.

University in my day gave you the ability to think logically and analyse problems and make decisions as a result.

A university degree now seems to be about google search, copy and paste, print and hand in.

Most university students now lack the ability to do anything practicle. As aresult they are pretty useless in a small company.

I actually think the German education system is better where you learn how to do the job while working, i.e. as a mechanical engineer, you might start by learning how to use a simple bench drill at 16 years old.

Too many boomers forget COMPLETELY that they had a stay at home mom, and a dad who wasn’t a bit worried about losing his little butcher, truck driver, or soft water maint job. And schools WERE better. Private schools were mostly religious, not “charter”. Corps, Banks, Financials, Insurance, Utilities, etc, etc, were more tightly regulated. Tax schedule reached into the higher levels of income, & estate tax,. Unions strong. (BTW: just wtf is the diff between a corrupt Union and a corrupt Corp? Labor wins or share holders win, if they get away with….something “bad”?……those at top of either ALWAYS win, anyway.

I envisage the return of the Liberal Arts Degree. Going with the fashionable degree is like chasing the stock market higher. You may win but what have you won? Consumers ingest vast amounts of popular culture, and know almost nothing about it. That film Yesterday deals with this self reflexively. Doug Noland once measured the “media” bubble, and the levels of debt (NFLX – a content provider) entails. The turn around at FB is remarkable, Libra?? These guys went from agents of, to Deep State busters?

I’ve noticed the advice of a lot of parents ends up being poor or flat out wrong. People get cemented in their view of the world and they can’t keep up or generally understand the speed of technological progress. My parents and grandparents never could understand the trickiness of the job market these days, couldn’t fathom how for me, my brother, cousins, friends etc. it was taking almost everyone who went to college, regardless of major, so long to get job offers in most cases and in positions that seemed only slightly relevant to their education. Many jobs are software related these days and I swear every large company is currently looking for people who can do cyber security. I don’t personally know of anyone being educated or trained in this area and instead for instance I have met vast quantities of biology related majors working in insurance or sales or random administration type positions for $20 an hour (in a high cost of living city), and the same goes for the swaths of liberal arts majors now in cutthroat competition for modest pay marketing positions. Their linkedin profiles crack me up with the amount of churn that’s evident in the industry. One of the biggest problems I notice after having perused many job postings, is that unless the employer goes lax on even their “minimum basic qualifications,” good but still relatively modest paying jobs ($50-70k again in high cost of living city) that would be considered extremely high skill 30 years ago, basically would take 2 or 3 different careers and a number of years along with a degree to gain the right experience mixture, and basically you would have to have been strategically planning to get these jobs by thirty from day one with a plan to hop jobs every few years, provided the opportunities actually presented themselves. Almost nobody is pulling this off from what I can see and you end up with a bunch of mad employers going on about a skills mismatch. It’s not apparent how people are supposed to acquire these skills in any kind of timely fashion though, and it’s not as if universities or technical schools are necessarily even teaching this stuff half the time if even that. We really need a different system if we’re going to have a modernized workforce that can keep up with how fast things are changing, otherwise pay will keep lagging in lower skill positions and people will irresponsibly try to rely on debt to keep living the lifestyle they’ve come to expect because it used to be possible.

My uncle is a 65 year old electrician in New Mexico. The company he works for cannot find any young people with the right skills to replace him when he retires. He’s making good pay for his location, and lives a comfortable life.

Young people assume a degree is required to make a living these days. This idea is perpetuated by businesses that require a degree to even get your application submitted. A degree does not equate to actual skill or the ability to learn, adapt, and succeed.

These people need to quit trying to be part of the rat-race, and find an industry that is lacking specialized workers. You can make a very good living as an electrician, plumber, carpenter, or similar trade. Someone has to fix all of the crap we surround ourselves with. I look at the invoices we pay to have our machines serviced/repaired, and I can see those guys are definitely not hurting for cash. Unfortunately, these jobs aren’t as “cool” or “prestigious” as being a wage slave for Corporation X, so young people aren’t interested.

Not that this advice is for everyone, but I see so many people doing the exact same thing when there are plenty of alternatives.

Ripp – Do you know anyone trying to go out and get into an apprenticeship? It’s hard as hell to get in. Companies used to take on apprentices and train people.

Here in Phoenix the carpenters union has a training program and and job placement fund. I don’t think many companies take on apprenticeships directly, but get them from the union training or community college trade programs.

It’s hard as hell getting into anything when it comes to the workforce. There’s going to be a lot of competition because the barrier to entry is so much lower. Like everything else in life, it requires a lot of effort. The difference is you aren’t spending 4+ years burying yourself in debt before you even begin to try.

You want to make a decent living? Be an HVAC tech in Arizona, the community college has a training program. They are begging for them on the radio daily. There are certifications for all kinds of technician roles that don’t require a 4 year degree.

All I’m saying is there are other options. Nothing is going to be easy, that’s just life.

Right there with you, except my math phobia and low self-worth kept me out of studying CS. I had a scholarship so graduating in 1992 left me with no debt, though I couldn’t find a job. Kept mowing lawns with a friend of mine until I went to grad school, which was a different kind of dumb, but I found some writers I wouldn’t have known about otherwise.

Remembering those 1991-3 days of applying to jobs looking through the classifieds and just finding garbage.

Amazing what interesting things/people you run across taking “garbage” jobs. Especially good for one who wants to write. Don’t regret my pre homeless “garbage” job period at all.

Alex, and don’t forget ALL that SCUBA training!

I think that someone should offer a “Stupidity Hot Line”, a place where profoundly stupid people can call-in for advice on how to not be as stupid as they currently are.

But I also think that some stupid people should be excluded from any call-in help. Graduates from Trump University… well, I just wouldn’t hold out much hope for any of them, for example.

if only we could promote more rhodes scholars to positions of power and influence. that would fix the stupid in short order. smh

The smartest people make the biggest messes.

LOL

Not sure that that would work, at least not for the most stupid as they are too stupid to know they are stupid thus will assume the “Stupidity Hot Line” is not for them.

Except that if someone thinks they’re stupid then they aren’t stupid, HowNow, so the people who phoned in would probably be pretty insightful.

Better to call it the Sveriges Riksbank’s Prize Winning Economist Phone-In. Get people like Krugman and Nordhaus to phone in with their world destroying theories, and you’ve covered all the stupid you could ever hope for.

Must have hit a raw nerve. Anti-intellectualism has a long history in America.

And by suggesting that Trump U. grads are a little on the short side of intelligent because the whole operation was a scam, you’re ready to trash MIT grads and all of academia as equivalent. Populist logic. May keep the hot line ringin’ off the hook.

HowNow, if the economic academics didn’t ignore things like limits and diminishing returns, and actually espoused both the inevitability and the merits of contraction, they would be far more worthy of respect.

Instead they use simplistic models based on obviously false assumptions to fit a desired ‘reality’. And even e.g. Nordhaus, who actually recognises the reality of climate change, thinks it’s something that should be weighed up against the costs of limiting our accelerating consumption of the planet, when we’re talking about an existentials threats…

All Right! Now just add the Bio-Med prize to that list and you are set to address the main “Nobel” beef, e.g. “no one person should have that kind of verbal power”, in academia or elsewhere. It can be bought. Any science that is totally immune to profiteering still seems safe; Physics. (the big or the small sectors) Everyone in all academic disciplines still keeps an eye on most all of those guys, and always have, anyway. Concept inventors.

Sounds like perfect biz for you to start. Takes “animal spirits”, though, I’m told to start a biz.

Almost unique to the US, the insane inflation in higher education and healthcare. On in American can someone go bankrupt for getting a degree or going to the doctor. There will be a reckoning.

The pharmacist I got some medicine from recently mentioned he’s $300k in debt for his degree – and I’m not sure if he was a pharmacist or a pharmacy tech.

Guarentee ya he’s a Pharmacist. Gives me an inflation comparison, though. First professional year of Pharmacy, tuition and room and board, cost me $8K out of state at OSU (Beavers). But did stay in double occupant 150 sq ft room at International House (West Hall) and ate in cheapo cafeteria. (Did go up with a fair amount of savings for back then). 78-79.

Still have a hunch he lived a LOT better than I did.

Wait, sorry. Was thinking of Pharmacy School only. I had way more than enough units for BA, when I applied as Grad at OSU, maybe 160+, at zero loan cost as I worked full or at least 20hr, the whole time. (except 3 sem on GI bill, which pissed wife off) Took 10 years, was 31, but then I just dug college scene and learning, and the JC and State College I went to.

And it was MUCH MUCH easier to find better paying low wage jobs back then.

They don’t teach critical thinking in schools anymore. The teachers oftentime are bad examples for the students in terms of how they deal with debt, life planning, etc.

Instant gratification has become the new normal when in reality is the slipery slope…

Might as well blame schools and teachers. It really couldn’t have anything to do with families and values, could it? Schools already teach bus safety, dog bite safety, sex ed, internet safety, etc etc, (but no politics/values or the parents phone the boss and complain)…and now they are responsible for common sense? Oh, forgot to add….there is talk about arming teachers to prevent shootings. Obviously, these wonders of fixing everything must be grossly underpaid. Now they’re supposed to take over from parents who didn’t learn enough life lessons.

Where are the parents? They must be too busy buying stuff.

Paulo,

I totally agree; it is the parents that are to blame.

Children are mollycoddled by their parents.

Parents don’t seem to ask children to do anything and buy them everything so they have no sense of value and believe they are entitled.

There will be a shock in the future (with data bases, IT and Robots and AI) that there will be only jobs on minimum wage.

There parents will also be shocked to find out that their pensions will be worthless so their kids won’t be able to get handouts anymore.

WTF is “critical thinking”? Hear it mentioned on Fox a lot, as ref to people only watching MSM, and not them. Implies look at both sides, and is stupid the way they use it, e.g.,”watch us more”.

Null Hypothesis has been around FOREVER.

Met a kid at regular old friends (and friends of friends) coffee waiting to apply for job. Last owner owned coffee shop in large area, mostly employs State College students. Anyway, he was debating getting $9-10/hr job vs going to grad school. I told him I would go for the degree, if it were me at his age, because they can never take what you get there from you, and picking up enough bucks to totally enjoy one’s youth is IMPOSSIBLE now, but it sure was for me. So I did. Screw the boomers who pissed away their best years planning for the future, and “SAY” they had “fun”..(that only applies to those from wealth, otherwise it’s a fn lie) Sure, ya’ll are living much better “$$$ lifestyles” than me now. So fn what? I hate golf, anyway, and big houses, and “luxury” cars are just good for a laugh.

My “life changing adventures ran from 17-34, where I started going homeless, which took 3-4 years, unable to find interesting, newish, or start-up 40 hr job (LOTS of bit jobs didn’t hurt growing skill set, though, and I relearned Haight St. cheap living) for first time ever in 80’s recession, when I was saved by work and school and Army experiences and passed USPS tech test. Then I was worried about future, and did something. No complaints now.

In some ways it’s sad that mortgage debt has decreased in the last 10 years and consumer debt has increased. You could make the case you should never borrow for consumption even education. If you are going to borrow for anything it should probably be for housing because it is a long lived, generally appreciating asset that is an inflation hedge and the government basically ensures the mortgage rate is cheap compared to other loans.

If you do the maths you find a mortgage is an incredible bargain so long as there’s normal inflation of about 5% (it’s still a bargain for any +ve rate) . By normal inflation I mean wages are keeping up with rising prices.

An interesting question is, do you end up with a house (asset) worth far more than what you effectively paid for it? I think you do, in general. It certainly seems likely you’ll be better of than someone with similar job etc who rents instead of buying. At least that’d be the case when house prices are above their ‘true’ value, which tends to be always.

Old-school,

I was brought up never to borrow except to purchase your house as and individual.

It paid off.

I recommend this to my accountancy clients all the time.

I can see that people are too busy chasing the American Dream:

Buying trash they don’t need

With money they don’t have (debt)

To impress people they don’t like.

Bifurcation is right. The CPI adjusted wage of the 70% of emplyed Americans classified as production / nonsupervisory has been flat for 60 years. Yet real PCE expenditures per capita have quadrupled.

Bi FUC ated, again.

Actually it has not been flat. If fell about 20% from ~1973 to the mid 90’s. Since then it has slowly worked its way back and is close to 73 again. Interestingly the LFPR is now back to where it was in the early 70’s, I have always wondered if there is a connection there.

investors in a booming asset class called “student housing.”

Purely anecdotal, but lots of friends and colleagues are taking their high school kids on the college tours and they informed me most colleges they look at insist students must live on campus for their freshman year. Even if the school has traditionally been a commuter school like Marquette Univ in Milwaukee.

What a racket.

I visited a church founded school in the middle of no where because a friends grandson attended. They had just built a multimillion dollar student activity center with top of the line pool and workout center. It looked so out of place with the modest legacy buildings on campus.

It became pretty clear that the game to stay viable is that you have to compete for the students by offering luxury ammenities. If the student loan bubble bursts a lot of these small schools will close.

It gets worse – It turns out the money’s not in in-state local students, but in out-of-state students and even more so, in out-of-country students. The world’s 1%. Lots of rich but really stupid kids whose parents are willing to pay what’s not a lot for them, to get their kid a degree at an American college.

Colleges actively court students like this. They’ve got money to burn. The brilliant kid from a farm 5 miles up the road probably doesn’t.

When I went to a state university in Illinois back in the 70’s, students were required to live on campus their freshman year. I don’t think that’s anything new.

Of course, our campus housing was similar to a jail cell. Furniture bolted to the concrete block wall, a small closet, gang showers, and vinyl tile flooring. Now they have “suites” with private baths and the costs reflect it.

With you 100% ElKatz. I went to U of I in Champaign in the late 90s, stayed in a dorm the mandatory first year. Cinder block bunker from the 50s or 60s, I’d guess. I lived in a triple smaller than most doubles these days. Bathroom was at the other end of the hall. No in-room kitchenette. And I thought *that* housing plan (and meal plan) was expensive. These newer dorms are more like moderately upscale hotels, with, as you say, the cost to reflect it.

And add to that the mind boggling increase in tuition. When I was at U of I, the tuition was ~$3,500….*for the year*!! Now it’s over $8 grand per semester, so $16k+ per year.

Yeah. When first went to USPS Tech Training Center, they used a whole 50-60’s era 12 story dorm and other old buildings around OU campus.

Joke was beds were so “canoed out” that ya couldn’t roll out even dead drunk. But they had to pay per diem for food, so they finally moved the whole show out HWY 7 to the middle of nowhere. I liked good VB and other action on campus, so I fought to stay in Couch tower as long as I could, with bad knee needing exercise excuse at Huffman Rec center. Walked to school. Other guys thought I was nuts.

Parents these days want their child in a more controlled environment. They prefer student housing.

Been seeing a lot of ads on TV of late for web sites that promise to boost your credit score. I guess this must be an all out effort to keep the debt serfs spending at a slightly higher rate.

As for me I pay off the credit card each month. Both cars and the house are paid for. It’s nice not being a debt serf.

I have always tried not to borrow anything that I could not pay cash for if necessary. I will admit it took me 31/2 yrs. to pay for my home. It 08 i bought a new pickup and carried a balance on in order to get a 1500. allowance from FMCC. I paid it off in 6 mos. Yes, I have credit card debt. If I hit a special interest rate and know where I can turn it into more income than outgo. I am in. I always have enough Gold, Silver, or cash to take care of it if necessary.

It’s almost to the point where having kids is a curse financially.

Brant, you nailed it. Millennials have opted for the ‘dog’ option to children. It’s a shame and in the long run I believe a serious mistake for many reasons.

Kipling saw it coming. This quote from The Gods if the Copy Book Heading:

* Till our women had no more children and the men lost reason and faith,

* And the Gods of the Copybook Headings said: “The Wages of Sin is Death.”

A/C in SD – I had to look that poem up, it’s a pretty decent one.

And yes, indeed, the “dog option” am I getting sick and tired of people dragging their damn dogs along with them, everywhere. But, I tell myself, better the damn dogs than a bunch of little yuplets who’d be noisier and do even more damage.

“The Wages of Sin is Death.”

OTOH, the salaries of sin are excellent, not to mention the executive bonuses.

Meanwhile, debt continues to increase faster than income. How easily slaves are taught to love their fetters.

Yeah, Welcome to the charge of the light brigade, the last one.

If couples wait to have children when they can “afford” them they will be in their ’90’s and certainly infertile! LOL!

We (my ex and I) had 7 un- planned children; She a stay at home mother; me a workaholic working two jobs for twelve years almost ruining my health. Today they are all in mid to late ’50s…not all married but all very hard workers and their children of those married also very hard workers. And, certainly not the, “Brady Family”. Many normal problems from health to all the other pre and teen problems that most normal families have. Would i do it over again?

If I was a millionaire and knew then what I know now? I’d a had a dozen!

I don’t know where my husband and I sit on this? We are 60 and 62, he has a pension and is collecting SS so $30,000 a year no debt and recently sold our house we had for 20 years. And someone paid us a shit ton of money for our house and I’m in Boise. I’m still working making 65,000 and my employer pays 17% into my 401k. I was getting a lot of money a month in my 401K until last week.

I’m thinking of buying an RV and traveling?

“I was getting a lot of money a month in my 401K until last week.”

Your 401k is probably worth 3% less today than it was last week. After doubling in the last 3-4 years.

You need to take a breath, stop freaking out and put things into perspective.

You’re in the right spot for buying an RV; I just visited Boise and there must be a half-dozen RV sellers along Hwy 84, each having a couple hundred units on their lots. A cousin informed me they are all owned by a mega-corporation named ‘Thor.’ I’ll bet a C-note the corp is private equity backed:

https://www.thorindustries.com/

Almost all RVs are made by 2 companies. Post 2008/9 there was yuuuge consolidation in the industry. Those 2 companies all sell RVs under a bunch of different names, but they’re all basically the same RVs with different badges. Think GM with Chevy, Pontiac, Olds. Same cars different badges. Now extrapolate that to include GM and Toyota selling the same cars under 30 different brand names and that’s basically what the RV industry is. 15 versions of the Camry and 15 versions of the Impala.

Selling out and traveling is what I’d do in your situation. If you’re in good health, have no other obligations? Go for it. Never wear shoes for the rest of your life.

Norma, an R.V. is an incinerator on wheels that burns money. Other than that they’re pretty fun.

You definitely should buy an RV. We do not yet have enough of them clogging up our scenic roads or our national parks. And be sure to buy one of those really huge ones that are approximately as big as a house. Why travel with a sense of adventure when you can just drive all of your creature comforts around with you?

The way I see it, most ordinary people (the 99%) are getting into more debt to survive or get a life. This used to be called the American Dream. Talking to my kids today, I don’t hear much enthusiasm. They definitely know there’s a problem but they don’t know what the fix is.

The fix? Self discipline..

Convert from consumer to be a preserver…

Learn to discern need from want and cover the need.

Don’t watch TV – it fools you..

Debt-free since 1971,

I haven’t had a penny of debt since 2005. Money in the bank fixes almost all of life’s problems. In fact, it keeps them away.

Roddy nailed it. Don’t buy anything if you don’t have the money…… unless it is absoutely necessary.

Debt bad. Life good. Be the ant, not the grasshopper.

I did buy that truck today. Cash…4K cdn/or 3K US dollar. My neighbours thought I bought a new truck off the lot. Hilarious…it’s a 2002.

Paulo – it’s a fable well worth studying, in all its forms.

https://en.wikipedia.org/wiki/The_Ant_and_the_Grasshopper#Fable_and_counter-fable

I actually remember reading a version of it where indeed the grasshopper lives for the moment, but the ant works himself near to death, and when winter is finally fully there and it’s freezing, he considers finally taking a single bite of his saved-up hoard, perhaps a slice of “a juicy moth ham” and dies right there of exhaustion and self-imposed hunger.

That version may have been by James Thurber, who was a snarkmaster of the first order and who’d be right at home with today’s “lost generation” kids.

In this last version, got the the message that it’s good to take a middle path, enjoy life but save for the future, too.

Crow and Fox made more lasting impression on me, if we’re talking same book.

Ever read Pete and Penny Pendleton Books? No? You are VERY LUCKY, all too many were not.

We replaced two household appliances (paid cash via CC, 30 day float, + 1.5 % cashback, that way).

A dishwasher that sometimes managed to apparently rinse dishes and a clothes washing machine that never could get clothes reasonably wrung out, and died after 4 years.

We bought German-made machines, Miele, which are performing relatively excellently for us and lasting twenty years in Europe. About 30% higher priced than the usual U.S. brands.

We avoid U.S. (Chines manufactured) brands, when we can.

I bought a Bosch dishwasher about 8 years ago. So quiet you can barely hear it run and has always worked perfectly. It was about $200 over other Chinese/American brands and worth every penny.

Dishwasher? Not very Spartan. Anyway I do have REAL beef with them. Folks on top two floors use too much or wrong soap and I get bubbles coming up my sink. Not too often, maint guy says he yells at them, because other first floor folks complain. Fire alarm goes off a lot, too.

Tip: slip on pencil erasers make perfect earplugs and so cheap you can have them laying all over. Of course round end first, sheesh.

Debt doesn’t matter and obviously trump deficits don’t matter (just like back in 2009, when people realized The Great Recession was no big deal). It also doesn’t matter that trump is yelling at The Fed to lower rates — while pushing Treasury to head the other direction. Classic strategy from Bankruptcy Man, pitting two entities against each other while he plays rabid barking rabies dog in the middle.

See: The large increase in debt issuance has the potential to partially offset the monetary easing just announced by the Fed. As the Treasury floods the market with new debt to rebuild its cash reserves, the new supply could have the effect of driving down prices and driving up yields of Treasurys and other market-determined interest rates.

Also see old read from 2009 about velocity of money, debt and deficits:

“We will explore all the deflation-fighting options and what the results might be in future letters, but remember that there will come a time when the Fed will have to “take back” some of the liquidity they are going to provide. That means we could be in for a multi-year period of slow growth after we pull out of this recession. And this recession

could easily last through 2009.”

https://ritholtz.com/2008/12/the-velocity-factor/

The Debt Slaves can’t be trusted and nether can the Debt Masters. Check out this snip from 6 months ago, we’ve gone from debt doesn’t matter much, to a full blown ZIRP Panic. It’s somewhat amusing and alarming that nobody has a clue and in the big picture, I think this chaos and instability will result in fewer investors playing games in casinos that are filled with smoke and mirrors.

International Monetary Fund director Olivier Blanchard has recently said that higher debt levels might not cost us as much as we thought. And the Federal Reserve has admitted that the trade-off between lower unemployment and higher inflation is so small right now that it can afford to raise rates at a much more measured pace than it had assumed.

https://www.washingtonpost.com/business/2019/01/25/everything-you-need-know-about-theory-that-deficits-dont-matter/?noredirect=on

Seems to me that the idea deflation must be avoided at all costs is barmy. Deflation is neither worse nor better then inflation. It’s argued that in a deflationary economy firms won’t invest as returns will be lower and so profits lower too. That is true but what is also true is, by the time those profits roll in, prices will be lower too, thus the lower profit buys you pretty much the same goods as if there was zero deflation or even -ve deflation (= inflation).

The problem with deflation is debt payments don’t go down. Any business with relatively long-term debt is doomed in a deflationary scenario, along with the banks holding the debt. From a bankers point of view, deflation is a disaster.

What’s so good about debt payments going down? Yes, fine for the borrower but not so fine for the lender, plus their capital is losing value too. But businesses aren’t daft, they can see what you and I can see and will adjust rates accordingly.

In a deflationary economy borrowing rates would have to be lower, otherwise borrowers wouldn’t borrow so much and would be keen to repay early. So lenders get smaller repayments but they grow in real value with time. Firms that do borrow long term a rates that are too high will, as you incline, go bust and so they should, as should those that lend to them.

All in all 0% inflation is fairest, as if favours neither borrower nor lender.

I find the auto loan delinquency rates a source of amazement.

The way I see them is that automakers haven’t merely tapped into very marginal market segments but have exploited them to their very limits: since subprime has mostly become the preserve of the shadow banking sector (not just in the US) risk has been shifted elsewhere so automakers just don’t care. Nobody is going to miss a few shadow banking concerns… apart from the private equity, wealth “management” and pension funds which lent them money. Not me: I’ve learnt my lesson the hard way. :-(

However that stabilization at such high levels spells troubles for automakers: it means to avoid the full-blown recession they so richly deserve they are doubling down on tapping into marginal market segments, all the while doubling down on leasing, which means a rapidily growing supply of used vehicles between 6 and 24 months old that need to be sold as well. Just ask JLR how well leasing is working out for them.

As Pyrrhus is rumored to have said after defeating the Romans at Asculum in a particularly bloody battle “If this is victory, I dread to think what defeat must look like”.

The role of non-bank lending is now today’s norm. My nephew recently quit his bank job because his bank had constantly embarrassed him. After working hard to get his client base, nearly all of them were refused loans. It’s easier for non-banks to lend to business. I think the funds have learned well. Why provide money to the banks when they can be lending directly to the banks’ customer. I think it’s called Disintermediation. Not sure where the added protection or value is if the loans were all going to be securitized anyway.

I think this might be the problem this time around. The banking system is safer and the losses will be in bond ETFs and pension fund alternative assets where middle class will eat the losses and go what happened.

It’s ironic that a lot of poor people drive new autos because they can’t afford to drive an old auto. In other words they don’t have the cash to buy even a $2000 beater, so they go the no money down new car route.

A $2000 car will cost $3000 in repairs within the first few months of ownership.

This isn’t 1975.

Japanese built cars go 250,000 miles these days.

If you do your due diligence when buying a car, and learn some basic mechanical skills, not even close. I’ve been driving a $4000 car for the last 4 years every day , 40K miles, and only changed the spark plugs and alternator, along with regular oil changes. Itll need tire soon but every car needs tires.

Problem is no one wants to drive an older early 2000s car because its not fashionable or doesn’t have bluetooth.

I own 4 vehicles, paid cash for all of them, and the newest one is a 2007. If you combine what I paid for all my vehicles, its less than the cheapest brand new car on the lot, plus no interest, plus no insurance, plus i have different vehicles for different things (4×4, fast car, motorcycle, daily driver).

And cars, no matter how good they are, come with parts that wear out and need to be replaced. Sure an engine will run for 500K if it’s well maintained. But not tires brakes, starters, fuel pumps, shocks, struts, timing belts/chains or the 1000 other parts in a car that wear out. I always find it funny when people think oh I have a Camry, it can go 300K miles without me spending any money on it. Uhm no. The ones that go 300K miles are ones that have had a ton of money spent starting around 100K miles. Which is why, even though it’s counter intuitive a car with 200K miles is often a better buy than one with 100K miles. By 200K everything has been replaced already.

A true recession causes you to correct some bad things that are going on because there isn’t enough wealth to fund it anymore.

Might be time that education gets restructured. It’s not been a good steward for quiet a while.

Leasing – done properly – is a benefit to the manufacturer. However, when the balance between retail and leasing exceeds a certain threshold, it becomes very dangerous – especially when they “juice” the residuals to make the numbers work.

The residual values – if not based in reality – can cause the captive to lose twice. The rates are usually subsidized with incentive dollars or “lease cash” (expense 1) and then they eat a loss at the auction because dealers refuse to buy them at residual value (expense 2).

There is a penetration level where the luxuries and the mass produced vehicles can thrive in leasing. It helps the manufacturer because they have a known number of customers returning to the market at predetermined intervals. It helps with planning production and helps with survival during downturns – again if done properly. It also helps a manufacturer market new technologies (hydrogen for example) because they lease them at 100% and then take them all back before they become a PR nightmare.

The problem is when the “sales guys” push the “bean counters” too hard to make sales objectives. They start playing with the lease structures to overdrive the leasing penetration – which looks good on paper at bonus time but comes home to roost 36 months later when they’re forced to eat their own cooking.

JLR counted on all those customers who had leased the Evoque SUV to be back at them in 24 months. Nobody did because the impossible happened: the car went out of fashion and merely rebranding it as a Jaguar didn’t help. Now everything is breaking down as JLR is still planning for 2017 levels of sales/leases while dealerships are swamped in used inventory with very high book values (aspirational residual value as I call it) they cannot sell at a discount and that nobody wants anyway…

Next up VAG (Volkswagen AG to normal people), which took leasing excesses to the next level.

I have already been offered 12 month leases on company cars and on some markets 6 month leases (which once qualified as long term rentals) have started. In 18 months at very most VAG dealerships will be in the same position JLR dealerships are right now if not worse because the master strategists at Wolfsburg have started to lease small cars to private individuals as well… things surely went downhill really fast.

Hopefully our “leaders” figure that out in time. “winners” = “losers” ignored for far to long, in context of this big ball of ours.

David Stockman has a way of taking the extremely complex and making it simple. He says debt bubble was one time sugar high for the world as leverage went from one times GDP to three times GDP.

Other concept I like of his is that the Fed creates dishonest money because it’s conjured and not earned.

Here’s a little salt for some US credit card holder debt wounds.

‘It’s crazy’: Chase Bank forgiving all debt owed by its Canadian credit card customers

“Finally, a good news story about credit card debt.

U.S.-based Chase Bank is forgiving all outstanding debt owed by users of its two Canadian credit cards: the Amazon.ca Rewards Visa and the Marriott Rewards Premier Visa. The bank retired both cards last year and said it’s wiping out cardholders’ debt to complete its exit from the Canadian credit card market.”

https://www.cbc.ca/news/business/chase-bank-amazon-visa-marriott-credit-card-debt-1.5239411

Just think I missed out!

Could have moved to Canada and got the Canadian Amazon card, instead of the U.S. one.

I have the wrong Visa, damn.

That’s hilarious!

There is another category of consumer debt that is even more burdensome than bank debt yet I have never seen it tabulated in any economic data. It is court imposed fines for minor offenses and traffic fines. Fail to pay it and your drivers license will be suspended which puts the offender on a legal treadmill.

It is astonishing how many traffic violations some people can accumulate particularly those who imagine they have a right to drive late at night when the police are on the prowl. A $250 speeding ticket or red light camera violation can be devastating for a debt serf. A DWLS leads to arrest and a day spent in jail more fines and possible job loss.

Maybe traffic fines should be ‘progressive’. If high income people had to pay, say, half their weekly salary for speeding as do low income people local police might find their enforcement activity curtailed.

Yes, and these small fines are very discriminatory: people with $500 in the bank or some room on a credit card pay them without sweat. Others who don’t have that $500 available can lose their DL, for example, which means that they might also not be able to go work legally, so they either lose their jobs or drive without DL, which can land them in jail. And the downward spiral goes from there.

There are some reforms being discussed in various states and municipalities.

Wolf: Granted that driving fines can be onerous for many people.

Here is a revolutionary thought : DON’T rack up driving offenses in

the first place !!!

I’ve been licensed to drive for 50 years, have driven in all conditions from desert to high Arctic to high density cities approx 50,000 miles per year.

My tally to date : 1) Last moving violation was in 1984 for over the limit speeding on a section they had just re-posted lower.

2) NO at Fault accidents………I have been rear ended 4 times, had one idiot kid with no license, insurance or paperwork for his car running from the cops T- bone me, and another driver pull out of a side street on a snowy day that I couldn’t avoid.

If I can do it so can just about anyone else. Be aware of your surroundings when driving is all it takes + a modicum of driving skill.

Sorry, no sympathy here with all the lousy driving I see daily.

WT Frogg,

We’re talking parking tickets here, or a broken tail light, and the guy doesn’t have the money, and late fees explode, and the spiral starts.

In San Francisco, sooner or later, you fail to read the bewildering forest of signs posted half a block away explaining in cryptic language when you can and cannot park here, and for how long, and on what days, and when the free parking turns into a tow-away zone (at 4PM sharp in front of my place).

If you park in free parking on my street, the tow trucks start lining up just before 4 PM, and at 4PM they start towing. This will cost you over $600 because you didn’t read the sign half a block away. You lose your car if you don’t have $500 to get the car back. And you might lose your license if don’t have $100 to pay the parking ticket.

That’s where discrimination is: a guy with $600 gets this resolved without problems; a guy without $600 is in deep trouble.

Yes, I understand, a lot of people are perfectly comfortable with the fact that in our society money buys these kinds of privileges, that, for example, a rich person gets away with murder because he/she can hire the most expensive legal team to induce “reasonable doubt” in the jury’s mind, while a poor person ends up on death row.

Wolf, my favorite quote that encapsulates what you’ve expressed is from Bryan Stevenson. He wrote a great book called “Just Mercy” that changed the way I think about justice and it explains the fallacy of being “tough on crime”.

“We have a system of justice that treats you better if you’re rich and guilty than if you’re poor and innocent. Wealth–not culpability–shapes outcomes.”

The 30 yr fixed mortgage was over 6% in early 2007. Since interest rates dropped, the debt servicing cost (interest portion of monthly payment) as a percentage of disposable income dropped. This means the cost of being in debt dropped for those with good credit ratings.

This allowed people to go deeper into debt. If their investments are wise, it is not as bad as when their investments are foolish. The nationwide price/rent ratio has risen since the Great Recession; as if a new housing bubble was forming. Can lowering rates ever be considered a Ponzi scheme? In all my 60 yrs I had not heard of negative rates until recently. Has this ever happened before?

“In all my 60 yrs I had not heard of negative rates until recently. Has this ever happened before?”

Switzerland had negative rates in the 70s. It’s nothing new, despite the way some in the media want you to think it’s some sort of unprecedented event.

re: student loans

This week my kid is at a camp on a college campus. So instead of driving back and forth twice, to drop off and pick up daily, I’m hanging on campus and working from the student union building. Things have changed since my days in college. Restaurants serving GMO free this, organic that, locally sourced this and that. The building itself is amazing architecture, leather chairs and couches throughout the place. It’s like walking into an upscale resort.

In the 90s my student union building was a 50 year old place that needed a paint job, with crappy pizza and chicken wings available.

It’s things like this that make me roll my eyes when I read about the “student debt crisis”.

Wait a dang minute — you had chicken wings at your student union? Man, in the 80’s we had some chairs and I think a pool room where you could play by the hour. Maybe a couple of pinball machines, IIRC.

Lemme guess you had to walk in 2 feet of snow, uphill both ways to get to it? :)

On that table “Auto Loan 60+ Delinquency Index,” what is the vertical scale?

Oooops! Percent. That got clipped somehow. Fixed now. Thanks!

I appreciate the qualifier ‘debt’ in this series, i suppose for the culturally depraved identified at fault, them, they, students, mills, women. that just leaves a few of us shiny turds posting from the porch and still searching for wmds.

1) Denny’s customers are heading to some big troubles, if they are not already in. They are hooked, keep coming back in, repetitions.

2) Today Denny signal a positive setup, to serve DENN

wealthy owners to dump, to cash in. Denny’s went from $1.15 on Mar 2009 to 23.55 on July 2019, x20 times within a decade.

3) Warren Buffett $125B cash liquidity to serve WB from troubles.

BRK is the US economy. Its covering the whole spectrum : from insurance, to consumers, banking, RR, industrial, retail, RE….

BRK weekly chart have a nice rounded cup over its head, the inverse of the 1960’s/ 70’s DOW chart.

Personal debt is nothing but slavery by salami slice. For a little bit of money, you become a little bit of a slave.

There are those in the economy who want everyone enslaved. Some despise savings, and that is in evidence by negative interest rates available to those who would save. Scandalous.

I am often amazed at how we are able to keep this country together. Crime statistics indicate 13M people were arrested in the US last year. Almost 7M people currently in prison or on parole. 40M lawsuits were filed as well. One more unanticipated crash and this time, perhaps ,the whole house of cards will come tumbling down in earnest. So many decent, responsible, hard working Americans have had enough. Unhappy with their jobs, their communities and the mood of the country in general. I will save my thoughts on the inner city public education catastrophe for another post, however keep in mind that millions upon millions of US high school students graduate every year with no marketable skills and are unable to pass even the most basic proficiency examinations in Reading, Math ,Science, Social Studies and

Language. Keep praying for America because she desperately needs it.

Excuuuuuse me, to quote Steve Martin, IF the “consumer” is losing half his money to inflation, and about another quarter to taxes, why begrudge him, and call him greedy and wasteful for trying to make lemonade out of the pittance he has left–from one who lives on SS and still loses half of my below poverty stipend to inflation???????

CANADIAN CREDIT CARD DEBT JUBILEE !!!

Quote:

“‘It’s crazy’: Chase Bank forgiving all debt owed by its Canadian credit card customers”

https://www.cbc.ca/news/business/chase-bank-amazon-visa-marriott-credit-card-debt-1.5239411

And the creator of this website stated that a “Debt Jubilee” was nonsense and that the person who had even suggested such a thing should stop posting such stupidity .

I responded by saying that he should allow people to post their thoughts and beliefs freely without dictating what they can and cannot say as long as it doesn’t offend anyone . Then I stated that I wouldn’t post on this sight any longer due to his close minded dictating mentality …………

However , there’s always an exception . And in defense towards that particular commenter who spoke about a potential “debt jubilee” , well there you go my friend , IT HAPPENED on a smaller scale but still happened none the less !

Wolf Richter , this goes to show you , you should always keep an open mind no matter how “ridiculous” someone’s belief may appear to you ………

No hard feelings . However, I hope you learned something from this “confirmation” …….. Anything and everything is possible !

Best of luck !

Noble1,

READ THE FRIGGIN’ ARTICLE IN ITS ENTIRETY BEFORE you post the link!!!! You have now proven that your attention span is only good for a headline. Congrats!

So I’ll tell you what’s in the article: There is no Debt Jubilee in Canada, not even on a small scale. This was a basic business decision by JPM. JPM shut down its credit card operations in Canada because it was too small and didn’t matter, and it was probably losing money on it, and rather than waste its resources trying to collect the remaining balances (likely negligible amounts given the size of JPM), it walked away from them. JPM looked at how much in balances were outstanding, and how much in personnel costs, office costs, and other costs it would incur by keeping its credit card operations in Canada, and it added 2+2 and decided it was cheaper just to walk away. Businesses make this type of decisions ALL THE TIME. It’s one of the most basic business decisions – when to walk away from an investment that didn’t pan out.

If you people watch, none of this should suprise you.