Chicago struggles, Dallas-Fort Worth, Atlanta, Minneapolis, Charlotte reach new highs. Drum-roll for Detroit and Cleveland!

This is the other side: Not every metro in the US has experienced the kind of blistering housing bubbles occurring in Miami or the San Francisco Bay Area, as illustrated in The Most Splendid Housing Bubbles in America: Year-Over-Year Declines Spread to Seattle. This is about the others among the 20 metros in the CoreLogic Case-Shiller Home Price Index, the metros that range from crushed markets — that are trying to dig themselves out — to blooming bubbles that haven’t quite yet qualified for the list of the Most Splendid ones.

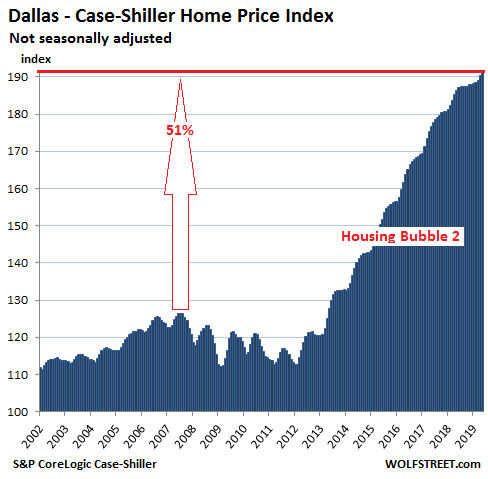

Dallas-Fort Worth House Prices:

To the aggravation of homeowners and speculators at the time, the Dallas-Fort Worth metro skipped Housing Bubble 1, so called because it was the first housing bubble in this millennium. Consequently, they were spared Housing Bust 1. Now the metro is in a housing bubble of historic proportion: The Case-Shiller index for the Dallas-Fort Worth metro rose 0.5% in May from April, to a new record, and is up 70% over the past seven years! But as in many other bubble markets, the heat is fading: The index in May was up just 2.6% from a year ago, the weakest year-over-year gain since March 2012:

The Case-Shiller Index is a three-month average; the current release represents closings that were entered into public records in March, April, and May.

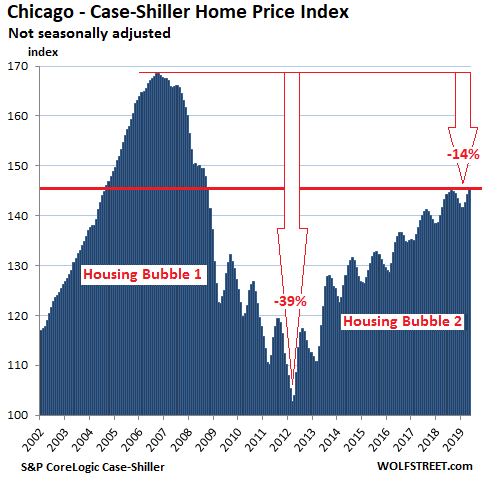

Chicago Home Prices:

Prices of single-family houses in the vast and diverse Chicago metro rose 0.8% in May from April, slightly less than last year’s seasonal uptick at this time. This whittled down the year-over-year gain further, to just 1.6%, according to the Core-Logic Case-Shiller Home Price Index. The index is still 14% below the crazy high of September 2006 at the peak of Housing Bubble 1:

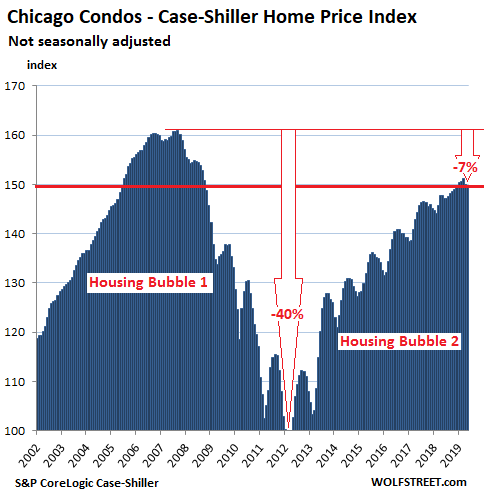

Prices of condos in the Chicago metro dropped 0.2% in May from April, the second month in a row of drops, which whittled down the year-over-year gain to 1.4%:

All charts here – except for the Dallas-Fort Worth metro above – are on the same scale. On the Chicago charts above and on the charts for the other metros below, the vertical axis ranges from 100 to 175 to fit Chicago’s Housing Bubble 1. The Case-Shiller Index was set at 100 for January 2000. A value of 175 means that prices have risen 75% since January 2000. The Dallas-Fort Worth metro blew past that scale, however; so it has its own scale. For the remaining metros below, the left scale is that of Chicago, topping out at 175, with some chilling effects for Detroit and Cleveland.

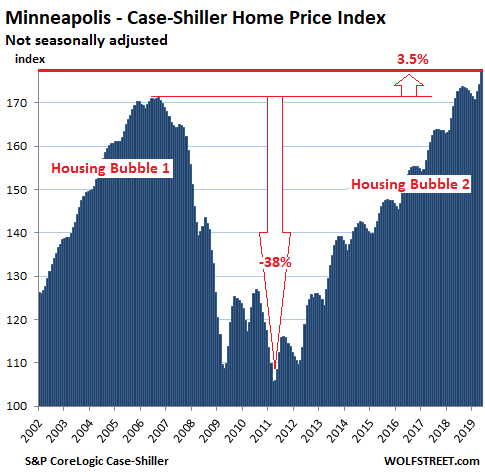

Minneapolis house prices:

House prices in the Minneapolis metro jumped 1.7% in May from April. On a year-over-year basis, prices rose 3.6%. The index is now 3.5% above the peak of Housing Bubble 1. The chart, which is on the same scale as Chicago’s chart, shows that the price changes during Housing Bubble 1 and Housing Bust 1 were similar in both metros, but during Housing Bubble 2, Minneapolis has pulled ahead of Chicago:

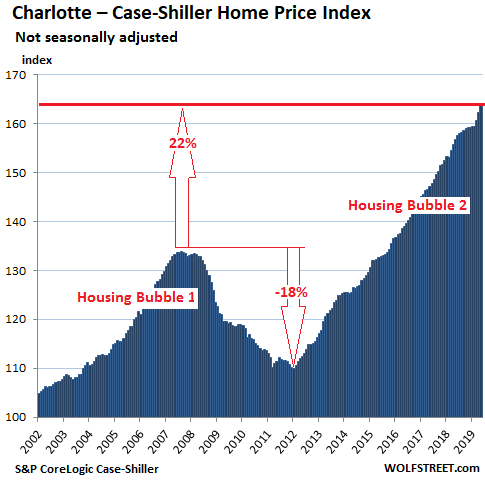

Charlotte house prices:

House prices in the Charlotte metro rose 1.0% in May from April, to another record, pushing the index up 4.5% from May last year, and 22% from the peak of Housing Bubble 1:

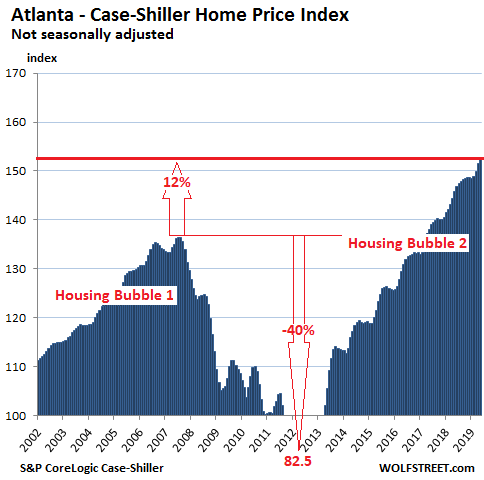

Atlanta house prices:

The Case-Shiller Index for the Atlanta metro ticked up 0.7% in May from April to a record, and is up 4.7% from May last year. This leaves the index 11.9% above its peak during Housing Bubble 1. During Housing Bust 1, the index plunged to 82.5, where it had first been in 1996. Note that the chart is also on the same scale as the charts for Chicago and the white space is beginning to grow:

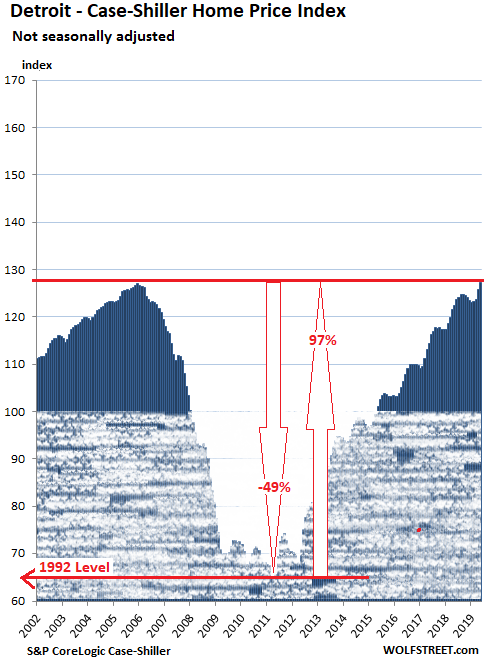

Detroit house prices:

House prices in the Detroit metro rose 1.2% in May from April to – drum-roll – its first new record since the peak of Housing Bubble 1 in December 2005, which hadn’t been much of a housing bubble in Detroit. From the bottom of this market just before the city’s bankruptcy, house prices have surged 97%. On a year-over-year basis, the index rose 4.0%.

To show the drama of this market, and just how far prices plunged from not very high levels to begin with, and to what extent they have surged since then, I have extended the scale downward. The shaded area shows the underwater part that the above charts don’t show. The 100-line on the left scale was set for Detroit’s house prices in January 2000. During Housing Bust 1, house prices fell to 1992 levels. They have now recovered to December 2005 levels:

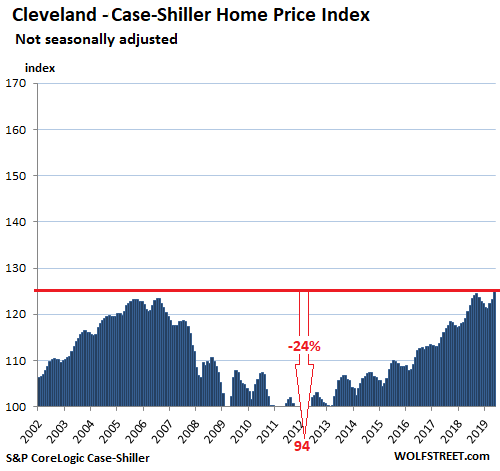

Cleveland house prices:

The Case-Shiller Index for the Cleveland metro jumped 1.4% in May from April and is up 3.6% from May 2018. With this move – another drum-roll – the index has finally edged past its record during Housing Bubble 1 of 2006. Since January 2000, the index has risen 25%, which would be about right in a normal non-bubble housing market, but in our bubble-and-bust-crazed times, it was the smallest increase of the 20 metros in the Case-Shiller Index:

Seattle House prices fell year-over-year, as did New York & San Francisco Bay Area condo prices. Los Angeles and San Diego house prices tick up. Denver and Boston jump to new highs. Las Vegas, Miami, Tampa, and Phoenix aspire to the crazy peaks of Housing Bubble 1. Read… The Most Splendid Housing Bubbles in America, July Update: Year-Over-Year Declines Spread to Seattle

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

People waiting for prices to come down as a strategy will be renters for ever.

If prices tomorrow crashed 50% they will still be waiting for them to go down more.

It’s always a good time to buy a house if you are renting and plan to live in the house for a long time. Right now prices seem high but interest rates are so low. If prices crashed tomorrow, you won’t be able to get a mortgage unless you are a cash buyer. So waiting for better prices is not as straightforward as it seems.

There is no precedent of the scale of QE and other inflation generating experiments that the Fed has engaged in right now and no one knows how it will end. Real estate is the only reasonable asset out there that can provide some reasonable protection to normal people without having to go into crazy speculative investments right now. It will be probably so for the foreseeable future and its hard to accept it.

For the middle class there is no better way to build long term wealth than buying a house and paying off the mortgage over a few decades. This is as true today as it was 10, 20, 50 years ago. Obviously short term nobody knows what happens. Long term, there is no better bet than real estate.

True comments 20 years ago. Not so today. Very location dependent.

Property taxes, especially in the NE but really in any long term democrat controlled area with powerful public unions, will eat you alive.

And will more than negate any appreciation in price.

For example. I have friends in northern NJ that own very modest houses, in nice areas, on small lots. Property taxes increase every year and are approaching $20k a year.

I highly doubt in the next five years their housing equity will increase over $100k.

And don’t forget insurance. Here in Florida our insurance is as much as our property taxes……

The other big bug is maintenance. For example a roof that would of cost me 15K 10 years ago is going to cost me 25k today, on, and on and on…..

In my area I don’t know how landlords are making a decent buck, and if there is an HOA, well, they are now just treading water, if not losing at these prices.

There has still been investor activity tho….so…..

A mortgage has never been a wealth builder for the average American. Unless you get really lucky you’ll just about keep up with inflation. Throw in the maintenance and taxes and you’re pushing a ten ton boulder up a mountain.

Maintenance is generally 1% of purchase price. Compare that to an average 3% increase in rent yearly. I get it some people don’t want to own and are happy renting. Have at it. But you’re doing some serious mental jujitsu to convince yourself renting for 40 or 50 years is better than paying down a mortgage fo 30 years.

This does not really make sense in boom and bust market…

Everything is about timing..

Americans move a lot. Nobody stays in a house for a long time.

There *has* been.

Whether there *is*, remains to be seen.

90% of the population never recovered from the last crash, and the “betterment” of the economy (really only for the top 10%) we’ve seen over the last decade may be the last hurrah.

I’m reminded of 2007, when things went all to hell for me and many others; but the early part of that year was actually pretty good, after things sagging all through 2006 and hearing tons of people telling me they’d lost $50k by not selling their house sooner. But Feb. and March looked pretty good … the tailspin wasn’t obvious until June or July of 07.

If you have the money, sure, get into a place. Prices are so high, it’s good to buy, right Socal Jim?

I have heard that the average mortgage lasts 7-8 years. Only about half a real estate cycle. Add in the potential to lose your job at any time (unless you are a government employee) and renting might make more sense. Everyone has a life that is different.

Buy now or be priced out forever.

Just ask the last 3 bubble buyers. It just works. ;)

“It seems we’ve reached a permanently high plateau”

Where have we heard that before!?

Like James Altrucher says “home ownership is the true American religion”.

Putting all of your resources in pretty much one subset of an asset class might not actually end well for the proles.

Not just America. If it’s a religion in America, it’s a moonie cult in Australia.

It probably is a feature of English-speaking cultures. Anywhere they speak English, the language of a rather soggy set of smallish islands, until they set up a worldwide Empire. Keep in mind all that great English literature, from Dickens to Austen to, well, everyone else, is almost all about having or not having land and wealth, where land *was* wealth.

As long as you can guarantee your income to match the term of your mortgage this logic is sound. Not many people in the “gig” economy have that security, a mortgage can’t just pick up and move during a downturn. A mortgage can’t be re-mortgaged for upgrades in the future during a downturn.

So it is a sound investment, if your income stream is sound. Like everything else in life, it is NOT guaranteed.

I’m part of the “gig” economy. Last time I had a real job was during W’s first term. Then one day it dawned on me that I can make a ton more money doing exactly the same job but cutting out the middle man, ie my employer, and going directly to the end client. Also much more advantageous tax situation working as a 1099 consultant than a W2 employee.

I took a risk leaving a very well paying relatively stable job to go strike out on my own. I could have fallen flat on my face. But I did it anyway. Close to 20 years later, my financial situation and general happiness is exponentially better because of it. Not having a boss is worth $1M a year alone :)

And I also LOL when I hear people talk about job security as if being a W2 cube dweller is some guarantee of a job. There is no job on earth that is safe or guaranteed. Anyone reading this could be laid off tomorrow with zero notice. The days of 40 years on the job with a gold watch at the end are ancient history.

Your attitude is a self defeating attitude. Oh no what if something happens sometime in the future???? Yeah things can happen. It’s called life. There are risks in life. Living life always worried about what may happen is not the way I want to live. It’s also not the way people get ahead in life. Anyone who has ever started a succesful business was told my people like you they could fail and shouldn’t take the risk.

I disagree. My job is as close to guaranteed as it gets and I have advanced notice if I were to be laid off. Many work 10-40 years without missing a paycheck. One of the benefits of working for the state of CA. If I lose my job, this round of civilization is practically over.

Back to the topic, I’m looking at buying a house sometime but I don’t know if I’ll still be in this location 5 years from now. A few have told me to wait until after the next election as CA is near the end of this current real estate cycle.

If I’m detailing cars, yeah, I’d rather work on my own. Go to the customer, have control over the quality of cleaners and waxes, build up clientele, as opposed to being paid min. wage to work very hard at a car wash.

But for a lot of applications, people are not in the gig economy because they want to be but because they have to be.

This comment contains a fundamental flaw in residential real estate investment. The big question you must ask yourself before purchasing a home is:

If I decide to move somewhere else, in the long term, will this home be a good rental home investment? If the answer is no, do not buy it.

I never live in a home more than a handful of years. I have a string of rental homes and I have lived in most of them. Everyone of them was carefully picked as a long term rental investment before I moved in.

+1

Absolutely. Can it rent and also can it sell it a down market. You want the cheapest house in the most expensive area, never the other way around. A $500K house surrounded by $600K houses will be much easier to sell in a down market than a $500K house surrounded by $400K houses.

I think in the distant past I might would have said that owning the s&p500 was riskier than buying a home, but now I think that overall that putting 20% down on a home (4:1 leverage) has more risk. It’s a reasonable assumption that stock market can go down 50% from time to time, but seems like in hot real estate markets that is a possibility and with leverage – yikes.

Will you continue this method, or will you at some time also be a renter while continuing to rent out your properties?

Most of these are old homes that are near the beach. They were not built very well when new. Now that I am retired, I am working on getting my rents higher. So, I move from house to house and do the work myself. Each one takes me about 2 years of effort. The only downside is I am unable to write off the repairs and I have to add the upgrades to the basis since I am occupying the home as a principal residence. I have my hands full. However, if I decide move to an area where owning a rental home does not make sense in the long term, I will rent.

Socal Jim, (and other above comments)

Respectfully, I read your comment and came to just one conclusion. You have never bought a ‘home’. You have bought houses and investments. There is a big difference.

When one is lucky enough to buy/build a home where one truly wants to live, the idea of actually selling it is repugnant. In fact, my wife and I have many many times said we will be removed from our home feet first, dead. The fact that where we live is exactly what we are is quite likely the main reason.

I am curious about the nightmare property tax taxation stories down ‘south’? Some of you might know I live in what many US citizens would describe as a Socialist Country, (Canada). Our Provincial Govt is left of centre. We have terrific public schools and teachers are paid a very liveable wage. We have single payer universal medical coverage. (I have never had to pay a medical bill for numerous injuries requiring surgeries). Nurses are paid well, and it is against the law for Cities, Regional Districts, and Municipalities to run and operate in defecit. (They can carry long term debt for capital projects, but NOT for operations, wages, benefits, pensions, etc). School Districts must also have balanced budgets. Everything is audited by acceptable accounting standards/practices (No Enron Scams). My house, while priceless to me, is most likely 500K at market value in the rural area where I live. My property taxes are $900 per year. We pay an additional $130 per year for weekly garbage service. I have a well and septic system, but if I were to move my home and it’s benefits (riverfront, views, etc) to a nearby city with municipal water, and sewer, fire, street lighting etc, my taxes would be approx 5K per year. definitely NOT 20K.

This begs the question. Why on earth are your property taxes so high? You have fewer services, worse schools, high cost medical and pharma, poorer infrastructure, and lower municipal wages on average, etc….then why on earth are people so gouged? I don’t get it?

I would hazard a guess that it is a result of lower to non-existent taxes elsewhere; income, alcohol, fuel, etc. Surely, it balances out? Property owners are either getting hosed, or just whining as they forget they aren’t paying elsewhere.

If homeowners here were taxed at those rates we would revolt and ‘retire’ some poiticians, for sure. There must be more to the story.

You have a valid point … my wife always asks me if she will ever get her dream home. I penciled out her dream home, and it would be a loser.

Paulo:

While reading your post it dawned on me to describe how I feel about “living” in the USA vs/vs Canada.

In Canada, it seems to me (all my previous knowledge about) that “living” there is like a true sports fight….according to “the rules”.

In the US of A however, everyday living is like, “Cage Fighting”!

And, I’m afraid it’s going to get worse.

I bought my first house in the mid 1950’s because I got married and it fit my income ok……1250 sq ft home; $5,000 down and balance of $10,000…pymts of $50 month! But, I was only making $1.00 (one dollar) hour.

One more home and a condo later I end up in Paradise…the Sierra foothills with a modest home, kids all grown with decent jobs in the “flatlands”.

It’s so different today. I don’t understand most of the $$$$ numbers.

A home should not be an “asset”.

But, in the USof A economy it is the only platform for the lowest of the low to achieve any future value.

It’s a “Cage Fight”!

Socal:

Your dream home should be a loser, you don’t want to feel the need to sell and you may even find less neighbours crowding the location.

Check out Credit Suisse Wealth Management latest report on number of USA households with net wealth over $50M. Don’t know if they still put it out, but I have one from around 2010-13 which sure surprised me. Appx 70K in several marked big # increments up to Gates/Buffet levels, as I recall back then. Then think about Sierra 7 comment on “rules” and “cage fight”. Or that 0.1% have net wealth equal to bottom 92% (went up 2% since 2016) Should help answer many questions.

Might also reflect on founding father Tom Paine’s lack of statues or his many unmentioned writings. His Common Sense did more to motivate troops than Gen. Washington did. All time per capita best seller here to this day, I think.

As you know, taxes are assessed differently throughout the U.S. I reside in Texas where property taxes are higher than a lot of other states as we do not have a state income tax. We do have a state sales tax of 8.25%. A high portion of property tax is designated for public schools, then first responder services, then infrastructure, etc. Depending on where you live in a city within Texas, there are fluctuations in property tax rates – I pay 2.7% assessed value on a 3,700 sq. ft., 2010 built home that is currently valued by the county assessor at $366K, so about $9,800 per year. HOA fees are just $600 a year. Insurance purchased through the builder is relatively low at just $1,400 per year. You can protest any new tax assessment, which usually occurs every 1-2 years. With our higher than average household income, we know we are still way ahead as we would pay tens of thousands more if we lived and worked in a high income tax state such as California. We could afford a more expensive home here based on income, but property taxes are a concern and I would rather invest extra income. The trick here is to find the most affordable home in the best school district within a reasonable distance of work, which we feel we have done (two sons went on to good colleges and graduated). The major downside of property taxes here is that assessments gradually climb, and/or supply and location drives prices higher, and some folks sell to downsize or relocate to the country to save on property taxes. Seniors ages 65 get a partial property tax exemption, which is fair. So, instead of revolting, I quietly complain and remind myself that I chose my home, and with it the tax rate that I must pay.

Paulo if I had the million or so dollars it costs, I’d hie me up to your neck of the woods and pledge my obeisance to the Queen in a heartbeat.

Sadly, it doesn’t balance out. There is an enormous amount of public funds wasted with no true oversight, and often frank fraud. The public pensions are a nightmare when you look deeper into them and are almost never audited. When they blow up, you will hear the screaming from Canada. My property taxes are about the same as yours would be for a similar amount of house in the city, but I get very little for them. Yes, our gas is cheaper, but I think the difference per month would be a maximum of $20. No one in the private sector has pensions anymore, and so all of us must (but so few do adequately) save for retirement. Social security won’t cover rent alone in most places. Politicians and “public workers” are legally insulated from being held personally liable for their actions on the job. There’s almost no way to actually hold them accountable.

Sorry, but for those of us who want a house, it is not a good time to buy. The mortgage is far too high. How are we supposed to pay it when outsourcing from corporations and asset stripping by private equity funds don’t give us the salary to pay for things?

The only way the middle class can own a home is by waiting for the price to fall.

I’m with you. I *want* to buy a house. But the prices right now are so ridiculous. And I’d settle for 2016 prices… I’m not waiting for some gigantic crash and 2012 prices.

Memento Mori,

I think you are right in everything you said above. If people want to create wealth for themselves their best chance of doing this is to invest early in their adult lives and to invest often. It worked for me.

I am from Ireland (but live in the US) and i remember the Celtic Tiger years. I grew a little concerned ( from 2005-07) about that bubble from because my parents and siblings own homes in Dublin.

My dad bought his home in Dublin 15 in October 1977 for 23000 (Irish Punts) which converted in 2000 to approximately 28,000 Euro.

In 2007 almost identical houses on his road were selling for 800,000 Euro and today they are worth about 700,000 Euro.

Interestingly, my dear ol’ dad never even considered the purchase as an investment at the time. He was just looking for more space for his growing family.

Moral of the story : Get started early and do not worry about panics, bubbles and crashes.

Unfortunately, just investing only works if there is no massive financial manipulation occurring. If all accessible investments are inflated or put at risk by derivatives gambling, as a stocks and real estate are now with enormous bubbles, you can invest but (since I would presume that you would use leverage, e.g., to buy real estate) a later collapse in RE/stock prices could wipe out your equity and leave you under water. The same applies if you have a restaurant or other business and an economic downturn results in no customers.

The “Federal” Reserve came to its bankster sponsors’ aid by blowing another RE bubble, in which we are now living. Remember that the banksters were holding enormous sums of uncollectible, bad real estate loans in 2008-2010. Thus, the RE owned by the banksters could be disposed of at high enough prices that their banks would not be recognizably insolvent.

However, as I mention above, aside from the fraudulent gambling in high risk auto loans that are securitized and sold to the gullible like mortgage backed securities were sold to the gullible in 2000-2008, the banksters are gambling in derivatives. Since central counter party clearinghouses (CCPs) will fail if one of the larger gamblers fails and the other CCP members will then have to cover the loss, they will fail.

Those banks other CCPs may then also fail when those banks are unable to meet their derivatives bets. This may cause other CCP members to fail. This will go on like a nuclear reaction, if a large enough CCP member fails.

This situation is like the FDIC, which has only limited funds to cover the losses of the banksters’ banks when they fail. The other funds must come from other (innocent) FDIC members (which non-bankster banks and credit unions will then fail) or due to the corrupt, Dodd Frank Act depositors and other creditors. Then, of course the U.S. government will again bail out the banksters’ banks and ensure that they do not go through bankruptcy, so the banksters will remain in control of the banks. However, since the banks now are gambling with over $200 TRILLION of derivatives the US government may itself become OBVIOUSLY insolvent and not be able to roll over its debts.

Would it not be nice if you could own a restaurant, take all of the profits out of it for years, then when it failed, the government stepped in and bailed that “essential” restaurant out without requiring any transfer of stock ownership (as the US government did in 2008 to the present with the banksters’ banks), let you keep your “bonuses” from that insolvent restaurant, and made sure that you kept your ownership of that restaurant intact. The banksters have a cushy life. That is the treatment that banksters received and will receive: they own the current judges and politicians.

They are the corporate welfare queens of the world. Do not be deceived it is not the politically powerless poor that receive most welfare it is the banksters and other crooks that are the control groups of the banks (which have and will later receive the greatest amount of welfare in the form of bail outs) and the military industrial complex entities (e.g., defense and intelligence contractors) that are the true “welfare” queens that parasitize the U.S. government.

Mike:

+1000!!

Talk about welfare queens.

Why is mortgage interest deductible and rent not?

They threw fairness out the window.

this is why we can’t have nice things. and also why i am thankful i never had children.

at least my parents still had the illusion that things would be better for the next generation, if only they educate themselves more.

what a fiasco life has turned out to be.

P. Coyle – it’s been poorer every generation in my family, going back to the 1920s if not earlier. No way in hell would any of the 5 of us have kids, not after what we went through growing up. The next generation would be digging through piles of garbage at the town dump to get something to eat, and none of us could bear the thought of that.

The better idea is to buy real estate for investment (literally anywhere), and then rent where you live. You get the best of both worlds.

I rented a house for a year when I relocated to where I live now. I kept my old house as a rental as well. I knew if I held onto it for a couple of years I could get a lot more for it. And I was right as the market exploded right after I moved. Made another $100K waiting those 2 years and still qualified for the tax free exemption.

So I’m a renting and I own a rental property. And MY landlord was also renting a house. His son had some medical issues and they moved to Dallas for a year to be close to a team of specialists in that medical field. But they didn’t want to give up their house so they rented to me. It was a perfect storm for everyone. And it was this 3 level of renter/landlord hierarchy that we used to joke about. We were both simultaneously greedy evil landlords oppressing poor renters, and we were also oppressed poor renters ourselves.

well at least you were able to joke about the new “sustainability.” many others don’t have that luxury. they gather on most of the major intersections on my way to and from work, holding cardboard hand-written signs asking for help. so it goes, as vonnegut so aptly put it…

I’m currently a renter, and will continue to rent as long as renting is a cheaper way to put a roof over my head than buying. I re-run the numbers periodically, but for the last 20 years, it has NEVER come up in favor of buying. Even if I had bought a house 20 years ago, the price appreciation today it less than the extra I would have paid to “own” the house.

When you do your numbers, do you account for principal pay down? My hunch is no. And that’s the great fallacy when doing a rent vs buy calculation. Everyone focuses on the monthly payment, forgetting that a % of a mortgage payment is your money, transferred from a checking account to home equity. Over the past 20 years you could have paid off a house and be free and clear today.

Where I live it’s about $1000/month more to buy the same place. Immigrants are willing to pay whatever, then rent out rooms via AirBNB or pack other families in one floor to make the nut.

My rent has gone up about 6% or so over 5 years.

I would buy if I could find something decent, but landlording has it’s challenges as well. My landlord thinks of himself as some sort of proper mogul, but is pretty dumb mentally. I can tell there is stress too, like other tenants always having excuses for not being able to pay. I pay on time, rent stays low. shrug.

The people I know that do great in Real Estate (other than Realtors) have inside connections to get properties before they’re listed on the MLS and all that. A retail shopper isn’t going to win.

Meanwhile my bank account grows. Shrug.

‘good time to buy a house if you are renting and plan to live in the house for a long time’

NOT if one has to look forward to have careers in more than one field, in the near future. Not with the student loans, marriage postponed!

All together a different picture emerging there for the young!

hey wait,

I’m reading this, and I waited, and I bought near the bottom in 2013 in CLT.

But, but, but…

Anyway,

And I don’t believe this real estate nonsense.

Rent as affordably as possible (roommates??), bank your savings….,

eye your target, and wait.

And better yet, do the opposite of what everyone is doing, and lever up on physical gold / silver.

DON’T lever up on housing / real estate at the end of 30 – 40 year boom, even after dip. That ship has sailed.

Lever up on the one thing they (govt ) has desperately needed to depress to in order keep the illusion alive.

Gold / silver are on sale at bargain prices. Come get some. Why not take a loan and lever up on it.

One ounce of silver = 3 Starbucks coffees, etc. etc.

Not long ago, silver was defacto 1/15 the price of gold.

Such disrespect.

SSHHHH….. I am not done buying silver at these historically low rates, and I need more time to get to a ton…

House prices are local but UN- AFFORDABILITY is national (or global).

That’s what the beautiful graphs tell me. In my extended family, almost all of the next generation is RENTING. That’s what really matters.

Just wondering of everyone in your extended family that is renting…

How many of them have a $1000 phone? How many had destination weddings that cost $50K+? How many of them go to Starbucks every day? How many of them eat out more than once a week? How many of them go on weekend trips to wine country or on craft beer tours?

I bought my first house in my late 20s. But if I spent money they way today’s typical 20-something spends money, I wouldn’t have been able to afford to buy either. When I was in my 20s I did this weird thing called – wait for it – saving money for a house. WHOA!! I had fun, too, I went, I enjoyed life. But nowhere near at the spending level today’s yuuutes. I’m nobody special, and what I did, anyone can do. But it’s easier to whine about how unfair life is, than being responsible I suppose.

Median family income in San Francisco is the highest in the country at ~$120,000.

But real estate prices are BY FAR the most expensive at around 1.375m or almost 12 times median family income. The major reason why real estate prices are so high is due to foreign monies, specifically the Chinese. When these monies evaporate WATCH OUT

but the $1000 phone will still be a good investment once the foreign money runs out…right? i would go on, but i have to pay for my $6 latte. priorities, and whatnot.

When I was young they were super picky about getting loans. I had such a hard time qualifying for a credit card, with no debt and 5 figures in the bank I never though I would qualify for a home loan. By the time I “got there” career wise the USA had gone Flipper nation . It’s not just in housing, look at TV. Be it American Pickers or HGTV drivel or… it’s the same in collectibles as well.

Household debt levels are lower than in 2006.

Ocean view property is priced higher. Miami is close to the Gulf Stream and is frost free. People grew coconuts and bananas. There is a Latin community that attracted investors from Latin America looking to store wealth outside of shaky autocratic regimes. As the city depletes its freshwater aquifer the ground subsides. Flooding is becoming more frequent. Some coastal cities have to cope with saltwater infiltration of their aquifers.

In parts of Arkansas land is cheap and the short term cost of a home might not rise much higher than building costs. Inflation is low. One might not get immediately rich owning a home. 2011 prices are long gone. If I buy land that is not good for growing crops, I can not rent it out. It is taxed anyway. Taxes might be raised as govt. worker healthcare costs rise.

Worker participation rates were higher in 1998. The median age of a US citizen is rising. The get up and go got up and went. China will face issues with its own demographics as they had a long term one child policy. Japan is using guest workers as they are lean and lived long. Some US couples with college debts can not afford the hospital costs of having babies. Government rate cuts cannot cure what ails you.

But..but…but…global warming. Rising oceans. The earth has a fever. We only have 12 years before the end. Florida will be under water in 20 years (predicted 20 years ago)…

“Ocean view property is priced higher”

Yeah, and the expensive re-enforced concrete pillars are getting higher at the best viewpoints where the red state “coastal elites” are. (sorry, I know I’m using the “coastal elite” insult entirely wrong…obviously not one who “gets it”).

But I think presently “cheap” fossil fuel is gonna cause some other problems, likely bigger. Especially when it isn’t as cheap anymore. And the best proven eco-friendly battery is called a dam, and they won’t fit in most vehicles, or structures.

And the Mojave is so, so close to the Sierras, and is just begging us…sigh. If only I could take over some brains for a while, like T.Boone, etc, etc.

Re: Household debt levels are lower than in 2006.

What does this mean?

Interest Rates dropped and home prices increased a lot.

So, mathematically, you are right.

The 30Y Mortgage rate is very low now. But houses are very expensive.

Can people afford?

Household debt levels in the US are in fact at record highs, surpassing the heady days of 2006.

Household Debt Service Payments as a Percent of Disposable Personal Income (TDSP).

This is the measure of lower household debt payments relative to disposable household income prepared by the US Govt. FRED. In 2006 debt payments were higher relative to disposable income.

Think back to 2000. Same deal.

Almost everyone is head faked into the stock market because of the tech / internet boom.

What did that mean? It meant that coal, oil, gold, etc. were on sale cheap.

Gold / silver are cheap now because they HAVE to be. When they pop / get expensive, it will signify the end of the paper money bubble.

Stop complaining about what is expensive, and start taking advantage what is cheap.

ragnar, as far as i can tell gold ain’t cheap. the time to buy it was a few years ago when it was below $1100.

not that you can’t make some short term profits if, say, you bought the dip yesterday morning…

@pcoyle

Gold hit $800 in 1980. It’s $1400 now.

What’s changed in the 40 years since?

USSR? Red China? Where is oil demand? USA Debt? Global debt? Global population. Aggregate global wealth?

Money printing?

And how much has the supply of above grown gold grown? And at what rate? And at what rate will it likely grow in the future?

What else is less than double its 1980 cost?

What else is a better indicator of inflation?

What else does the govt need to manipulate down / disparage more than gold to keep the facade going?

Considering the average family income I agree affordability is a major problem. The top 10% of wage earners nationwide could probably afford to buy a house but the rest?

After my recent experience in Florida which is a non income tax state with high insurance rates I am not convinced home owning is a wise investment unless you’re going to be in that one location for 20+ years. Though I sold a house I lived in for 8 years for 25% more than I paid for it I didn’t come out that great. Property tax and homeowners insurance equaled over $10000/yr. I could have rented a perfectly suitable house in the same area for about what my principle and interest rate was and invested the rest. That $1000/mo would have built my portfolio nicely. Sure my rent may have gone up in time but my insurance rate went up each year too. Renting is not all that bad, many people in other countries pay rent their entire lives. Home ownership is something that has been pushed as an investment by mortgage companies and renters until in the USA you are considered to be a lessor mortal to rent and many times that financially makes no sense. It is a high price to pay in order to be allowed to put a nail in a wall and cut your own grass.

Greg answered my above question re: taxation and property taxes. How does a State pay bills with no income taxes? Just put the full burden on property owners, I guess.

They have a high sales tax to take advantage of tourist spending money there, I’m sure they get alot of tax money from out of state people.

Sales taxes are highly regressive, affecting the poorest much more than the middle-class and even less, the rich.

This is probably why in Red states I’ve been in, the sales tax has been well over 10%, more like 12% up to about 14% in some areas.

Meanwhile Hawaii, a blue state, has a “general excise” tax, a sales tax really, of 4% and no, they won’t tax your banana, like they will in Red states. It’s not applied to food.

Jeff and Paulo: that’s exactly how it works in Florida and Texas. Plus in Florida we have pretty stout gas, hotel, and rental car taxes, since the tourists have to spend those dollars wherever they are.

@Greg

Couple of points I would make….

* Your math is on the assumption of the 30 year mortgage – justifiably, considering the modern market. But we as a people *really* should be only buying houses with <= 20 year mortgages.

* Folks are are buying the most house they can afford – keeping up with Jone's. Rather, if folks said, "I will only buy a place I can afford to buy with a decent disposable income cushion left over", they would end up with a lot more equity at lot sooner.

Granted, this is hard to do in many housing markets, but IMO a LOT of the housing trouble folks – at least in the middle to upper middle income range get into is due to their assumption that they must have 2,500 sq ft when they could get by fine with 1,500 sq ft.

They could get by with 1500 Sq feet, but when they purchase that 2500 Sq foot home they need to justify having that extra space by buying more furnishings and other “stuff ” they think they need but don’t. The other thing not really taken into consideration is the added cost of maintaining that 2500 Sq foot house, whether it’s the extra electricity costs of cooling all that space during increasingly hot and broiling summers, or the added heating costs during the winter. That same homeowner could save anywhere from $500 to $1,000 a year by living in a smaller space, which would also address the issue of not having enough money to cover sudden emergencies or inconveniences.

yep, and one of the ironies is that as our families have gotten significantly smaller our houses have gotten significantly bigger.

Also, people don’t appreciate how transitory are the various stages of their lives.

You will NOT have a house full of teenagers for more than a handful of years. The house you buy doesn’t need accommodate everyone in regal comfort at maximum family size. Its OK!!! to have a “few suck it up years”.

1. Look at the houses our parents / grandparents grew up in – and had normal healthy lives.

2. Look at the size of the spaces the rest of the world lives in.

Glancing at those charts, the stand out that pops in my eyes is the rather abrupt increase in prices since around end of 2018.

That’s when Powell did his U-Turn and flooded assets with $$$.

The Fed is now openly endorsing cutting rates for insurance.

They don’t have much left to cut in terms of rates, but if insurance is all it takes to get the Fed to cut rates, predictions become easier to make:

The Fed will cut rates again soon, for more and different reasons.

well the 4-week auction wasn’t that bad today

Term: 4-Week

High Rate: 2.080%

Investment Rate*: 2.118%

Its good bye. Not a good buy.

There is the slight chance that per capita wages and income will impact this housing game at some point – and that’s the reason some markets are cooling down. Between low performance pension interest yields and low wage part time jobs, there will be a point in time when a higher percent of people will have to either eat less or consume less in order to pay higher cost for housing; that’s already happening. Lower and slower consumption in retail, as an example will eventually cause GDP to fall and in-general jobs will be less plentiful and fewer people will have the income to support bubblemania. If anything, there will be greater caution and hesitation by most people, but as usual, thee will always be really stupid people pushing the edges until they explode. It’s hard to understand how things have not fallen apart lately!

One of the greatest threats to the US economic system is the proles waking up to be able to distinguish between a, “lifestyle” and a, “quality of life”. When that happens all hell will break loose!

if, and it’s a big if, the proles in the US wake up to the fact that they have to take on unrepayable debt to either maintain a lifestyle or quality of life, all the while being charged what in olden tymes were called usurious interest rates, the pitchforks and torches may have a resurgence in the popular culture.

but, sadly, they will most likely argue about more superficial things.

That won’t happen as long as there are other disadvantaged groups to demonize. Gotta keep those people fighting amongst each other so the rich people aren’t discovered screwing the proles.

BTW, people are already cutting back. Even Walmart is getting too expensive, so they have been hitting up the local Salvation Army and Goodwill thrift stores for clothes. Maybe they’ll make vintage clothing cool again.

One can only hope. But advertising is not going to give up it’s death grip on us, and allow any of that ugly and money losing “waking up”.

Unlike with the Ancient Greeks, “What is the good life” is no longer up for debate.

Although the fossil fuel of those times was called a slave, allowing them the time to think.

But we still did drop the above from the foundations of European thought.

Many thanks for charts and info. Is interesting what the future holds. Looks like Midwest is not in such high risk as coastal areas.

I am 88 years old…..I purchased my first house 50 years ago for $ 29,000 and sold it for $49,000…..My second house was purchased for $44,000 and I sold it for $333,000……My third house costs $119,000 and it sold for $ 189,000……My 4th house was purchased in Florida for $120,000 and one year later it sold for $ 190,000…..I live in my 5th house for 5 years now I paid $100,000 and the current value is about $120,000….If you can afford the down payment then buy a house, don’t worry if the price goes up or down, just enjoy it.

It’s all about timing, and these are long term time frames that tend to be generational.

I was first settled, ready and able to buy a house in 2007. Fortunately I didn’t, but I had plenty of friends get burned.

After going back for a master’s degree and getting settled again (took a while after a failed business start up and such), I’m seeing prices higher than 2007 while my earnings are about the same. Stretching for a small $300k place with a long commute doesn’t sound like a good idea. I tend to think stretching to spend 60% or more of your take home pay on any property is a bad idea – you need that wiggle room for inevitable emergencies.

All I’m saying is each generation’s got its own set of challenges and the same answers don’t fit all. Us 40-year-old kids aren’t all crazy :-)

Take the underlying issues with the Dallas market with a BIG does of salt.

The primary reason why Dallas didn’t bust in 2007 was due to the vast amount of new construction tamping down the prices of existing homes. I have personal experience with the real estate markets in both Chicago and Dallas suburbs. The problem this time around is due to folks who purchased the new construction in outlying areas such as Anna, McKinney and Prosper etc. learning that those commutes are horrendous. Dallas has very little north-south travel corridors and what they have was overwhelmed back around 2007. Therefore, home prices in areas closer in have skyrocketed.

As background:

I Sold my house in the Chicago suburbs in 2004

Purchased a home in the Dallas Metroplex in 2004

In 2007, I was transferred back to Chicago.

Sold my home in Dallas in 2007

Purchased in the Chicago suburbs in 2007

Sold my home in Chicago in 2012

I wonder how DFW was able to escape Housing Bubble 1? The only area I know of that has escaped Housing Bubble 2 is CT, where values seem to be dropping, for a variety of reasons.

They had price increases, just not huge, compared to what has been going on over the past few years.

Wow. Did we just have a flash crash minutes ago in Specialty Retailers ?

Probably, Akiddy.

From CNN Money: “But Trump said on Twitter that the United States would be “putting a small additional tariff of 10% on the remaining 300 billion dollars of goods and products coming from China into our country.”

Maybe the SEC should be investigating the purchases and sales by friends and family members with every tweet and resulting Market swing. Nothing would surprise me about this. It is either full ignorance on display, or crafty malfeasance hiding in plain view.

1) Make America great again :

In the last 60Y inner cities LT project was to produce babies.

What happen to them, who cares.

Sixty years, since the sixties, entitlements in ==> babies out.

– Can they buy a house ? Can they live in your house ?

– Is a new S. Bronx demise waiting for us ?

Politicians talking from their nose, with a sweet smile, promise

their core voters whatever it takes.

2) Egypt great S curve : population growing to 100M //

average age < 25Y.

Does everybody in Egypt have a house ?

3) Extrapolation of LT trends, without evaluating a potential

future change, can cause asset destruction.

4) Who expected abandoned houses in Japan, starting in the rural areas, spreading to the outskirts of major cities.

5) RE investors believe that a tenant in your $2 million

house is a safe, producing dividends and capital gains.

How about future leaders telling tenants that your house is

tenant house, for free, as part of reparation for slave owners crimes.

Great red day SPY.

SPY trying to close the gap above, failed.

“I am falling and I cannot get up”, after shaking out investors,

Forever up.

If SPY will make a new all time high, its likely to be another bearish divergence.

Time for impeachment yet? Maybe if we let disinflation take hold, home prices will drop like rocks? Too bad that there is no one in DC to stop this madness — maybe Marianne Deborah Williamson will save us?

benchmark 10-year yield slid to 1.89%, hitting its lowest level since November 2016. The 2-year rate dell to trade at 1.726%.

Fed and CBers are fighting against ‘disinflation’ for over 10 yrs. BOJ for over 2 decades!

DEBTs of all or any kind are at record levels, unlike any time, all over the world!

CBers will keep fighting but nasty de-leveraging DEFLATION is heading our way. more or less.

Any DEBT has to be paid or written by the lender or the borrower goes bankrupt. One can prolong the public debt by printing digital money out of thin air. But what about the private debt?

sunny129,

Read Mike’s comment above at 12:22 pm.

The Central Banksters are not fighting for anything except to further enrich the oligarchs at everyone else’s expense.

Anyone who thinks you cannot make money in real estate has never invested in real estate. Whether flipping, renting or purchasing your own home, there is nothing like this tangible asset. If you do lose money in RE, you sold in a down market because you were ill prepared to weather the storm. Once again, most of the prognosticators here see doom and gloom while we investors are salivating over the “next” downturn.

This time is different lol

Interesting charts. Thanks Wolf.

Charts are probably not available, but I wonder how rural America is doing in this area? It’s my general understanding that the jobs are in the cities, (mostly big cities), so I would expect property values sliding in rural Alabama or Nebraska, for example. Is there any hard data other than anecdotal? I would not expect rural property values to be doing terribly well right now either.

More tariffs on China announced today.Hong Kong represents a major example of how poorly they treat their own people, let alone other countries . Chinese monies toward foreign real estate purchases will no longer exist by the end of the year.Given that that Chinese are the major reason for real estate price rises in Aus, NZ, Western Canada , Toronto, SF , Sea, NYC and Mia, look for prices to fall precipitously.

Many oil exploration companies are not far from 2016 lows. Look for real estate prices in Dallas – Fort Worth to follow

Both the stock market and the real estate markets have made high for this cycle.

There will be blood in the equity and real estate markets before this is over .

Home buying is an extremely complex financial decision mainly because of the financing involved. The best rent vs buy calculator I have found is the on-line one by Michael Bluejay. I usually assume a rent and desired breakeven date say 10 years and then play with the major factors of how much down and assumed appreciation and assumed returns on the opportunity cost. After a while you get a feel for the range of outcomes. If you buy you have to determine how much leverage to use and if you rent you have determine your risk in the investment portfolio. Its probably not possible to be absutely certain which is best if you use leverage on the house or 100% equities in the investment portfolio. I have come to believe that if you are a good equity investor you are probably better off renting and if you are a good real estate investor you are better off buying but there is nothing wrong with being diversified and doing both. I did both but I have rented the last 12 years or so and I did better mainly because I live in small town where real estate appreciation is modest and I worked in business so I have some understanding of equities.

With new construction not being enough to satisfy demands, and low interest rates seemingly for the near future, will this big price drop ever happen? I can see high prices playing out a bit longer than anticipated when you add these factors up.

USA taxes make the UK look like a paradise.

A cage fight is a perfect analogy.

A great way to keep the proles focussed on the essentials of life, rather than the governing wasters… until it’s too much to bear.

It can’t be too much longer until something gives.

I can see hyperinflation on the horizon.

Buy low, sell high. Wait for correction. Can you afford mortgage, taxes, insurance and maintenance when we have a recession? Figure at least 1% of market value for yearly maintenance.

One sad thing about the CoreLogic Case-Shiller Home Price Index is that its operators refuse to carry data for Houston – one of the country’s biggest housing markets and Texas’ largest. It’s not like the data isn’t available, either. What’s up with that?

Hank Lloyd,

Here is the story on why Houston is not included:

“Unlike most states, Texas doesn’t allow public access to deeds, which is one of the easiest ways to populate an index with sales data, in order to derive prices. So Blitzer and his team struck a deal with a Dallas-based Realtor association to get data from their multiple listing service.

“And when it was all put together, the decision was that was a bit of a hassle, so we’d stick with one city,” he said. Also, “we had Boston, New York and Washington so we decided that was enough for the Northeast, with apologies to Philadelphia.”

Houston wasn’t a hot RE market in the late 1990s when this index was developed and people around the country weren’t that interested in it – so it wasn’t worth the trouble at the time. Today, he said they would do it differently and include Houston along with other cities.

https://www.marketwatch.com/story/the-man-behind-case-shiller-on-why-the-housing-index-has-no-houston-and-why-thats-no-problem-2018-10-30

@pcoyle

Gold hit $800 in 1980. It’s $1400 now.

What’s changed in the 40 years since?

USSR? Red China? Where is oil demand? USA Debt? Global debt? Global population. Aggregate global wealth?

Money printing?

And how much has the supply of above grown gold grown? And at what rate? And at what rate will it likely grow in the future?

What else is less than double its 1980 cost?

What else is a better indicator of inflation?

What else does the govt need to manipulate down / disparage more than gold to keep the facade going?

Lending Update:

Conventional: income limits reduced for “low income” programs, less buyers to qualify here and underwriting tightened up.

FHA: 09/01 they are reducing the loan to value maximum from 85% to 80% for cash out borrowers

VA:. 10/01 they are reducing the cash out loan to value maximum from 100% to 90%.

Also, VA is removing the max loan amount limits which were capped by counties.

Non-QM: more programs coming online everyday and loosening up.

All in all, it’s hard to say what going on. Certain agencies are tightening up while other programs are loosening so it’s interesting to see this dichotomy.

Since 2002, the start of your graphs inflation has increase 42% so just to stay even home prices should have risen equally. Supply and demand, there has been a tremendous demand in the Dallas/Ft-Worth area due to the booming population. No one wants housing prices to get out of control so a cooling off of the market is good, but no reason to bust the bubble when there isn’t much of one above inflation. The only concern in DFW is that the wages haven’t kept up with the home prices, making affordable housing harder to find, but that too isn’t a large disparity over the wider DFW area. You just may need to commute further to find affordable housing.