Beatings Will Continue Until Morale Improves, or Something.

The media and the Fed make it sound like inflation is inherently good. That’s how the media pitch it to regular folks — that the Fed is heroically trying to make sure everyone gets enough of it. (10 minutes)

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The one thing we can be sure of, not ours.

Sad really… Central Banks and economists when from studying the economy to thinking they can control it

Put on a puppet show here and there, have the media clowns act like it’s really complicated stuff, to add credibility to the bs they talk about… Wolf is right to talk about this low Inflation nonsense narrative. The more money that gets created into the world, the more it loses purchasing power. It doesn’t matter if credit is flooded in Japan or Paris, it can drive the Inflation of any given society, money moves without borders… Purchasing power always adjusts to the amount of money in circulation in any given society. Once it adjusts, you have to maintain it or a decrease in money supply causes deflation, like a dog chasing it’s tail these Central Banks have become, never ending circle… You can flood new money, but the moment you stop and purchasing power adjusted, deflation happens, so you gotta redo more stimulus but they don’t work as well, since 09 you see every 2-3 years massive stimulus, then fades, stimulus, fades… At every stimulus, it has much less juice and growth, yet they double down ?

They want inflation, just not wage inflation.

Workers be damned.

I think a critical factor is that today the debts of those workers and their college-age kids are among the most lucrative assets of the people at the top. It would be interesting to find out if corporate America makes more off of profits from goods or interest on debts.

They want CPI and they cannot get it in a sustained way if total wages don’t rise. Probably this is just why, or one of the reasons why, they fail.

That’s the big game. The 50’s/early 60’s are never coming back. But the gilded age sure will.

I am in my 40s, and I am retired. I invested heavily in single family homes in top end zip codes … I hope this protects me from inflation because I have many decades to go.

Tomorrow is not promised

Every day you wake up is a gift … at any age … even if you are in debt.

Amen

+1

If you can manage to avoid floods, fires, earthquakes and the pissed off 99%, you should do fine.

Just as good as an ex-friend of mine who likely still owns a boat business in Newport Beach. We used to all spend beach nite (Thurs) around a campfire at Corona Del Mar and watch the yachts come in in the mid 80’s.

I did some numbers …

The nominal median income in the US rose from 41K to 59K since 2000. That is an increase of 44%.

At the same time, the average home price rose ( national ) from 170K to 320K. That is an increase of 88%.

However, if you calculate the payment on a 170K home in 2000 at 8% for a 30 year fixed, which was the prevailing rate, the payment is close to a payment on a 320K home today at 4% is only a few hundred dollars more than it was in 2000. The price rise was more than offset by the interest rate drop.

There is nothing to see here ….

For the top 5% maybe. Everyone else’s income has been falling, for decades.

Until interest rates go up, then asset values are going one way… down.

The fed simply protected the bubble from retracting as much as it should have in 2008.

Well i guess it is just too bad for those that didn’t invest in the stock from 2009 onward but decide instead to waste money buying stuff on credit cards that charge 18% APR.

NickL,

Please think for a moment: in most cases, a person who uses a credit card to buy stuff and pays 18% interest on the card has no money saved up to invest in the stock market, or else they would pay off their 18% credit-card debt first. That person is most likely living paycheck to paycheck and has trouble making ends meet. Life — including rent or mortgage payments and healthcare — is very expensive for many people in many places in the US.

And from 2009??? By 2010, 12 million of these people were out of work, and many more were afraid they’d be out of work. So are they going to invest in the stock market to catch the rally, when they have no idea how they’re going to make the mortgage payment or pay rent next month?

SocalJim,

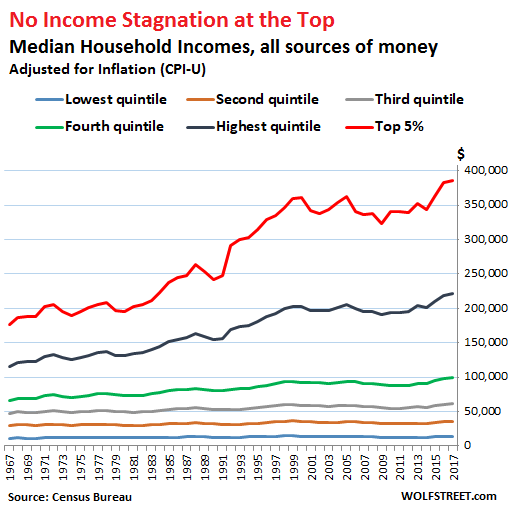

Here is the median real household income data by income level and by gender, going back to the 1960s:

https://wolfstreet.com/2018/09/12/real-earnings-of-men-women-income-distribution/

It includes this chart:

320K wont buy much in most areas where the jobs pay a median of 60K. Try 500K starting, 700K median.

Typo …

I did some numbers …

The nominal median income in the US rose from 41K to 59K since 2000. That is an increase of 44%.

At the same time, the average home price rose ( national ) from 170K to 320K. That is an increase of 88%.

However, if you calculate the payment on a 170K home in 2000 at 8% for a 30 year fixed, which was the prevailing rate, the payment is close to a payment on a 320K home today at 4%. The payment is only a few hundred dollars more than it was in 2000. The price rise was more than offset by the interest rate drop. The wage increase ( nominal ) covered the payment change.

There is nothing to see here ….

Your missing the real story… rise in healthcare/education/daycare/food/fuel ect….

@SocalJim:

“The price rise was more than offset by the interest rate drop.”

Spoken like a true realtor…. Price doesn’t matter…. it’s the payment.

Hogwash.

You pay what it’s worth. Period. The interest rate is meaningless as you can’t refinance a price paid… but you can refinance a usurious note.

When you go to sell, it’s the price paid that comes home to roost… not the interest rate. Smart people know that you make your money when you buy… not when you sell.

Why include interest rates in the value of real estate? Total BS!

Wolf, maybe I didn’t pick up on it earlier, but it seems your recent articles exhibit more cynicism of the Fed than earlier ones. Are you catering to the readership or just opening up a little? Also, I bet readers would love more articles on investment strategies to mitigate the various risks that you bring attention to – it seems you intentionally avoid making predictions though.

I bet readers would love more articles on investment strategies to mitigate the various risks

The biggest risks are outside the scope of this blog, and they will ultimately make financial risk irrelevant. You have no control over those and mitigation would be futile, anyway.

Don’t look now, but your life support system is being converted into capital just as fast as it can be managed. That’s a bad thing.

Sorry.

ZeroBrain,

Ha, you should have read my earlier articles about the Fed, the corruption at the Fed, and all kinds of other things. I despise that institution, and my early articles conveyed that. But anger is not helpful when it comes to understanding things.

The Fed is what we’ve got, and we have to live with it, and so these days, I try to understand it in unemotional factual terms to see where this is going.

I think raising rates and unloading assets on its balance sheet were good moves, and I was not shy about saying that. I think holding rates at this level for a while is OK. I think cutting rates with this economy is nonsense.

I’m trying to keep a clear head about the Fed. It’s hard to do. I’m trying to keep a clear head about inflation too, and I’m trying to convey different aspects of it, how it works, what it does, etc., to dispel some of the nonsense being plastered all over the mainstream media.

The Fed is an unsupervised federally charged entity like the CPFB which was overwhelmed with cronyism, corruption, and self dealing. Mick Mulvaney took it down.

Trump has not been happy with the Fed and has made noises that it should follow public policy and not go off protecting banks. Banks should fail. They key to bank failure is regionalization, not federation.

The original concept of the Fed and its regions was to assist in limiting bank panics and supporting small, regional banks What is now happened is that almost all banks are national, and the failure of Citi, JPMChase, BofA, or WellsFargo, or even USBank would likely be catastrophic and require nationalization.

It is with supreme irony that Minnesota who until the last few years required all banks to have a local charter and prohibited most forms of branch banking, is the original home of WF and USB. The conservative banking left the predecessors in some of the strongest financial position.

Much as I think political control is bad, it should be outside the supervision of Washington and abandoning the Fed is in order. Franking the treasury could take over all modern banking transactions, and should as it already does with treasury direct for bonds, bills and notes. Adding currency accounts and directed cash payments would be trivial. It is the local banks that we lost, that should supervise debt and debt creation and notions like checking where there can be overdrafts. Checking should simply go away unless part of a debt account.

The fed should either be under direct political control for accountability, or abandoned.

The Fed is no better than Fannie or Freddie which attempted to transfer privately vetted debt to the federal treasury, and was a cesspool of corruption and cronyism.

The Federal government should be in the private debt business. We either offer direct subsidies to people and corporations, but not debt. This holds for student loans and business development loans. Either pay up or shut up.

Government guaranteed private debt becomes to hard to track, and much of it goes to benefit multinational corporations and foreign investors, which our government has no business subsidizing.

Hmmmm….one need only look at a country like China or Turkey to see how such an arrangement would be disastrous.

>CPFB which was overwhelmed with cronyism, corruption, and self dealing.

Number on, it is the CFPB. Two, the idea of an agency that tries to reign the abuses of Wall Street seems like a pretty good idea to me. The idea that the fiduciary rule by the CFPB to have financial advisers work in their clients best interests being removed by the current administration is insane.

> Trump has not been happy with the Fed and has made noises that it should follow public policy and not go off protecting banks. Banks should fail. They key to bank failure is regionalization, not federation.

I agree that banks should be allowed to fail and shouldn’t be too big to be allowed to fail, but those noises were before he was elected. Recently Trump’s noises have been that the Fed should lower interest rates, even when the economy is humming along very well and is almost at full employment.

His reason is no doubt because he wants a booming/overheating economy to guarantee him another 4 years in office. Politicians will always end up going for the short-term and lower rates beyond what is best long-term and this is why direct political control of a central bank is a very bad idea.

I’m not sure there is a stable system without a central bank, but personally I think them lowering their *inflation target* to 0-1% would be long-term positive for most people.

Makes sense. I should do better at detaching emotionally from my disillusionment with humanity/gov/world. It’s good to hear that someone older and wiser thinks that’s a good route, plus my peers don’t want to hear what the Fed is or does anyway.

Wolf : “The Fed is what we’ve got, and we have to live with it”.

Surely if the government shut down the Fed and wrote off the debt owed to it we would not have to live with the Fed?

I was under the impression that Trump’s plan is to shut the Fed if he gets re-elected. Trump probably hates the Fed and banks more than Wolf.

One needs to look at the history of central banks in the USA. The common thread to these was that they were set up by Congress to have twenty-year charters.

In 1791, the First Bank of the United States began, and it did so with Alexander Hamilton leading the way to convince Congress that the new nation needed a unified currency. By the way, Hamilton and Isaac Roosevelt had founded the Bank of New York in 1784, and this became the first corporate stock traded on the New York Stock Exchange in 1792.

When the twenty-year charter expired in 1811, Congress did not renew it. Although the Colonies had gained independence from England, as a result of the First Bank, the issuance of the dollar had been indirectly controlled by the banks in the City of London. A year later, the War of 1812 began. Nathan Mayer Rothschild’s comment prior to this war, “Teach those impudent Americans a lesson. Bring them back to colonial status!”

In 1816, Congress authorized the Second Bank of the United States; again with a twenty-year charter. In 1836, under President Andrew Jackson, Congress does not renew the charter. Jackson’s feelings towards the Second Bank and the Rothschild banking cartel was summed up in 1833 when he made this statement, “You are a den of thieves vipers, and I intend to rout you out, and by the Eternal God, I will rout you out.”

That’s a bit stronger than Wolf’s, “I despise that institution, …”

Finally, on 23 December 1913, the Federal Reserve Act is signed into law, but again, the Fed begins with a twenty-year charter. However, on 25 February 1927, Congress passes the McFadden Act. This gave the Fed an override of the twenty-year charter, “To have succession after the approval of this Act until dissolved by Act of Congress or until forfeiture of franchise for violation of law.”

Congress alone controls the fate of the Fed. Our Senators and members of the House are bought and paid for by Wall Street and K Street; therefore, the Fed will continue on as long as I and most of WolfStreet’s readers are alive.

“Anger is not helpful when it comes to understanding things.”

Mandated inflation makes me angry. But there’s not a damn thing I can do about it, eh?

Why didnt the Fed chose to combat the Great Recession by implementing a negative interest rate policy like other central banks?

NIRP is destructive to the banks, and the Fed figured it out since it represents the banks, and since the 12 regional FRBs are owned by the banks. The Fed doesn’t mind wiping out savers, pension funds, the SS Trust Fund, people on fixed incomes, etc. But when it comes to the banks, it gets very protective. And that’s a good thing. NIRP is an insidious policy.

The ECB and the BOJ have no such compunction, and Eurozone and Japanese banks are struggling, and they’re chasing yield, and piling on risk in order to deal with NIRP.

No Wolf!

The Fed is an institution that you and the American people don’t have to live with.

It was never “ PART” of the constitution of the US, that and other stuff that have leeched itself like parasites onto the American Psyche, parasites and entities that are beyond the scope of this Forum.

Big Government and the Fed should be the Target of all decent citizens of the US.

That is the role that the outcome of next Election should be fought on.

Return America to its citizens, and build friendship with other countries, advocate for Future that your sons and daughters aspire to , living free and dignified life.

Go, Jack!

Ya got backbone.

It’s the $2.5 billion per day you give to the Pentagon you need to concern yourself with, and getting that redirected into constructing democratic infrastructure in all its forms rather than being frittered away in perpetual pointless wars in dusty places.

Ike Eisenhower did warn y’all a long, long time ago. At least – he tried.

“Common sense is a collection of prejudices usually acquired by about age 18”

– Albert Einstein

Regarding Wolf’s statement: “I think cutting rates with this economy is nonsense. ”

Respectfully, to me this pre-supposes the economy is actually in good shape, and I don’t agree that it is. Yes, the ‘so-called’ stats indicate that it is, but imho those stats are just ‘fog’, fog created by the inflation Socal Jim does not accept even exists.

My argument about the economy is a much simpler one and I just look at my childhood for a couple of examples, not statistically significant, but so universal it doesn’t have to be. When I was a kid, early years in Bay Area and after age 12 on Vancouver Island, I knew just one set of parents whose spouse worked. In every other case the breadwinner was the husband and the wife ran the show. Were these upper echelon types? Absolutely not! My good friend’s Dad in Walnut Creek was a German immigrant sheet metal fabricator, (not the company owner…but an employee). They owned 20-30 acres of walnut orchards, had a grandparent cottage next to the main farm house, a small in-ground swimming pool, and a cabin in the Sierras. The kids went to catholic school. This was a solid basic hardworking family. The couple that both worked were Pan Am employees, the Dad a flight steward and the wife in the office. They owned outright a very nice rancher. On Vancouver Island I knew only a few two income families. People that worked in department stores owned homes and had cars. Loggers owned homes. Mill workers made excellent wages and had homes….no one relied on two incomes to get by.

So, not only does Pan Am no longer exist, flight attendents are now paid piece work as opposed to salary, paid only for flight time with a small add on for ramp duties. Sheet metal work is now mostly non-union, with many parts pre-fabbed through automation. Loggers, are back to piece work, the mills closed, and department store workers are now minimum wage gas bar attendents or Dollar Store shelf stockers.

Meanwhile, housing is now unaffordable for almost everyone, post secondary requires financing for God’s sake, (there were no student loans for my older brothers), and yesterday WS commentors were choosing between health care and/or housing.

So if there’s no inflation….then pray tell what the hell happened? Sure, de-unionization and off shoring, but if the Market was truly free prices would have actually declined to relect the buying ability of citizens.

I agree wholeheartedly with Mr. Richter that lowering rates is insanity in this economy, but not because the economy is strong, but simply because it will continue to goose housing “assets” even further with a renewed buying spurt, and goose the stock market and other holdings of the connected, (who, quite frankly have enough already). Meanwhile, no matter how affordable loans and payments end up being, and how much savers will be further punished into buying ‘other’ assets, opportunies for the lower 80-90% will be further eroded.

This isn’t economics, it’s class warfare and the byproduct is an increase of anger, racism, and reactionary politics. I suspect the end result will not work out well; for everyone.

Paulo, In the Detroit that was (1950s), family economics were the same as Vancouver’s, except it was the automobile industry that sustained the city and its inhabitants.

A strong, honest union, the UAW under Walter Reuther, contributed to workers getting good wages.

That was a generation that had just gone through the Great Depression and WWII, and it enjoyed and appreciated good times.

Flight attendants are only paid for the hours they work?

They should form a union and negotiate a better deal.

Paulo – My father worked for a bank, programming their computers or something (he’d been hired as a teller) in the 1960s and kept the 5 of us kids and my Mom comfortable in a ranch house in Costa Mesa.

My boss’s father served in the Navy in WWII and came back and worked for the posts office, eventually ending up being the postmaster or something of his post office. He raised 5 kids, put them all through Catholic schools, and they had little problems going to college.

All of that is gone, because the US would rather have guns than butter, imperialism than public health, etc. Well, the Czars didn’t get their way either, did they?

The right (including the poor right) down here prefer no mentioning at all of “class warfare”, Paulo. It is usually rolled up into such terms as “winners”, along with a strong moral caution against “envy”. Note our president’s supreme insults….”loser”, “failing”, etc, etc.

And yeah, it is not real likely to work out well for all.

Thank you.

I think your insightful in-depth data-based analyses have caused your blog to take off. it’s very helpful to me. Thank you.

And I know I trouble you sometimes with my odd-ball posts about my life outside the money envelope. So, my apologies, also.

Mad Max Beyond Money-Sphere

Don’t think your notion holds much water. The heading used to be “Howling” (about the Fed and other economic problems like private equity, Wall Street, Banks, and financial engineering games in general.

As for giving advice, maybe it’s best to let me quote Indiana Jones. “Here we seek facts, if you want to seek truth, the Philosophy class is just down the hall”.

Economics is not a science, just opinions (usually with strong agendas, unfortunately), and therefore there is no such thing as the Nobel prize for Economics, even though most really believe that nonsense.

Also, I never try to speak for anyone, it’s merely my take, nothing more.

And sure, he wants to make a buck for his efforts to create something worth reading, but who wouldn’t? Kinda like a never finished book.

And my own opinion regarding the Fed, this likely 25-50 bps cut is just more can kicking, so those still in the Pullman cars can get off at better stations before the wreck. I’m back in the boxcars along with most of us, and will just have to continue riding.

To Dan-

Don’t forget that at first (c1800) NO Corporations were trusted, as they had too much power and were feared. If a canal had to be built, they were chartered, watched like a hawk, and disbanded when the project was done.

“Borers” (now lobbyists) immediately began infiltrating government (State, usually) and had put an end to that by, say 1850.

Abe Lincoln spoke to this issue as much as he dared.

Now they are People or Corporations, (whichever is most convenient), but I look at them as sovereign dictatorships, with all the privileges of same. And still quite scary, although private equity seems to be replacing them fast.

Ha! It’s maybe even likely a good reason to invest in them, as they are getting rare as….gold?

Great piece Wolf,

Question: You talked about Consumer Price inflation and Wage inflation. But you didn’t (explicitly, at least) mention Asset Price inflation. Where do you see that fitting in?

Thanks. This is all about asset price inflation:

https://wolfstreet.com/2019/07/11/with-all-this-money-printing-where-is-the-huge-inflation-asset-price-inflation/

Inflation is very real at my house. My grocery bill is up 17% in the last year. My electric bill is up.

But food and energy do not count. In the meantime the SS increases run around 2-3% . But! My supplemental ins. goes up and I wind up with a negative. At 76 I have been drawing it for a while and my net check is now $200.00 less than when it started. If they were honest and figured the inflation on real life figures it would be a totally different picture.

Someone has to teach the Feds to count.

I spent the weekend in the hospital.

The hospital ER was filled with elderly people and drunk Hispanic gardeners and old aged convicts in handcuffs. Thanks to supplemental Medicare insurance, I wasn’t charged before I got discharged. Just waiting what’s in the mail.

For something like the bottom 50%, the only access to the health care system at all is the ER. You just wait for the bills (which might as well be millions; you won’t be able to pay them) and write back telling them it’s a rare day you have more than $200 in the bank and you can’t pay. Period.

in the US, about 14% of the population is uninsured. I understand that you’re in a tough spot, Alex, but don’t extrapolate from you personally to 50% of the population. That produces misleading results.

A few points that Wolf might have forgotten to mention.

In the older days; pre 2005, interest rates used to increase and decrease with inflation. That was the way that savers/pensions retained the buying power of their savings.

When there was a shortage of labour to jobs available, you had wage inflation. That has gone now because, in reality, there are more available people than PROPER paid jobs.

Corporations are in effect subsidised by governments in benefits paid to employees to live on that don’t earn enough from corporate wages.

If you have inflation, but wages don’t go up, people will have less money to buy non essential goods and services (essential being food and rent). In the longer term, corporations would be making less sales.

If you have inflation, then the CPI and RPI (Consumer Price Index and Retail Price Index) would rise meaning that governments would have to pay more state pension and benefits to people. That would create a larger government deficit.

And if interest rates went up in direct proportion to inflation (as used to be the norm), that would result in the cost of government debt going up and people’s loans would cost more to pay back once a again creating the situation where people would have even less money to buy non essentials from corporations.

So inflation surely does not help corporations in the long term?

“Who’re the victims of inflation”?

They sure do. (Remove the apostrophe from who’re)

Real estate investors want house price inflation, but they do not want medical procedure inflation, food inflation and home repair bills going up. They will try to raise the rent.

Debtors want lower interest rates in order to refinance at lower rates. Lenders want higher interest rates and loan origination fees.

brilliant thinking and articulation.

Dow Jones William Hamilton : A turn in the tide, 1929.

The subway is packed, but the storefronts are shuttered.

Frappuccino, but the tenants of the tent city use the bathroom.

Senior coffee in MCD next to empty Sears dept store.

Rising rent, but landlords fate in the hands of the bank.

Where the deer population exceed people, there is little change.

On Oct 20 1969 Nixon put a man on the moon, but he was doomed.

Kennedy put man on the moon.

Nixon would have gladly had the rocket “accidentally” fall on a student demonstration or something.

After I listened to both Congress and Senate grill Powell, I don’t think anyone really cared to know WHY inflation was important especially at the 2% level. Powell cannot explain this well to the American people.

I think Volker had the best comment recently. He said ANY inflation was bad for the common people. There’s nothing in law or sound central banking or economics that rules the 2% target. Any inflation debases people’s incomes and savings.

We need Volker back before he dies.

Inflation is important to the fed because they need to inflate away the national debt, whose limit is about to be raised, yet again.

The 2% inflation target is probably because the traditional/normal/average interest rate historically is 3%. If they can normalize the long term rate to 3% with a 2% rate of inflation, that gives you a 1% real rate over time. This real rate is rather low considering that historically there was little to no inflation, except in times of panics over limited resources.

Inflation has a heavy psychological component. If the populace believes that money is losing value they will rush to dump it regardless of what the actual situation is, causing a surge in inflation. Alas, the average American is strapped for cash anyway except for in items where credit is readily available like housing.

Who’re.

Yeah, well, URLs eliminate apostrophes and other punctuation. You write “the Fed’s” and it becomes the “the-feds” in the URL. You write “the U.S.” and it becomes “the-us” in the URL. Sometimes I remember to not use phrases with apostrophes, and sometimes I don’t. This time I didn’t :-]

Geez with the miss-spellings, malapropisms, and poor grammar on here, we’re giving Wolf a hard time over an apostrophe?

Your best one yet. Nice job Wolf

– Inflation will metastasize from FANG to RE to energy,

basic material and food. It will spread.

– The first scars are the shuttered storefronts and the tenants in tent cities. Their numbers is growing.

– The face of map will change, countries will be ruled under new mandates, don’t get heart attack.

– Stay on the left hand side of the bubble, when it come, because the left side is winning.

Don’t lose your grip, don’t let go, until it pop.

– The US yield curve will fool the Fed.

In order to have hyperinflation people have to have money to spend. The people with the cash already have everything they need. The rest of us save up for months to buy necessities.

I see deflation in the discretionary economy and inflation in the non-discretionary economy. We had the two nicest furniture stores close in our town, one after 132 years in business. People are still buying houses but can’t afford to put anything in them. This is not a hyperinflation scenario.

I fear the same, too. I have no idea how people can deal with more inflation. They’ll shop less I think and substitute stuff to remedy the price hikes. Vegetable gardens to the rescue. Buy cheaper.

Hope you’re not in a part of the US where they seize your house and clap you off into jail for having a garden instead of a lawn!

Excellent report Wolf.

Another way of looking at it is to track the $1 buying power over the years. The dollar experienced an average inflation rate of 3.75% per year during this period. As a result the real value of a dollar decreased. In terms of purchasing power, $1 in 1940 is equivalent in purchasing power to of about $18.30 in 2019. Year to year it was hardly noticeable especially through 1970 when it was mostly offset by wage inflation.

But the current inflation rate (2018 to 2019) is now “ONLY” 1.65%. I hope the Fed does not have 3.75% as its goal.

Many of my friends have kids that are just about to start college. They, and their children can see inflation up close.

In-state tuition at the University of Minnesota when I began in fall 1980 was $1,150.50 ($383.50 per trimester). Minnesotans who’re (couldn’t resist) about to begin at the U of MN this fall will pay $15,236.

In 39 years, that is more that 13 times as expensive

https://admissions.tc.umn.edu/costsaid/tuition.html

When I started school in the early 80’s, the tuition was $300/trimester=$900/year and minimum wage was $3.25/hr.

$3.25/hr*40hrs per week *4 weeks per month = $520/month

Working 2-3 months at minimum wage per summer paid the entire tuition bill.

Try that now.

I hate when older people who went to college in the 1980’s start railing that Millennials can’t pay for college due to their Starbucks and avocado toast habits.

Oddball look at inflation from outside the money envelope: If not much money is needed, it’s cost if needed is relatively unimportant.

Living in a remote area where much of the essential stuff of sustenance is generated on the land is one such situation.

Another is having a lot of money and greedily acquiring more to “keep up” with inflation at the expense of the losers (so to speak) in our society.

This blog deals mostly with the latter, although it doesn’t usually offer much in ethical judgements (e.g. about greed). This time, it does: the perverse bias of fed policy against the working class.

But note: The remote resident is relatively unaffected, no matter where fiat money shenanigans go.

Reminds me of a pal living on 93 hilly rural acres. Said, “I really don’t give a damn if the value of this place goes to zero.” He is a 100% disabled vet, though, still fairly sacred “entitlements”

NBay, Do you think the vet meant “price” when he said value? The fact that he doesn’t care about the price tells me that he values it independently of its price.

Obviously.

The old boilerplate on inflation (70s) was that price increases came first and wages came second, the consumer was always behind the curve. However on matters of mortgage rates inflation makes the payment a lot easier. Pre 2007 consumers were consolidating credit card debt, or using home refis to pay off the CC. That might have worked, along with the current form of home equity extraction Tom Selleck is pushing, if only.

Perhaps, in the larger theoretical context of re-writing the inflation narrative — there is a policy goal to do-away with paper currency and thus use NIRP as a framework to support lower inflation. Hence, you apparently get a win-win solution to stimulate the economy without causing inflation. Everyone gets a free (tasty) lunch … and stocks can scream higher and yields can be a thing of the past and no more bubbles and pets will live ever and nursing homes will be cheaper and the American Dream will in fact be super cool.

Wolf,

On the lighter side, I had a maritime oriented tee shirt that said….”The beatings will continue until morale improves…” I think I’m going to go on line and buy a new one. Thanks!!

WR is the messenger and is on task as stated by the fed.If the fed cuts rates it will signal to the world that we will pay back our debt only in ever decreasing de-based currency. If the fed launches QE3 the road to ruin and to serfdom for we the people will be complete.The productive economies of the world will be forced to protect themselves with a gold backed trade note for nation debt settlements. The fed is warning we the people that we will be fortunate to suffer inflation and not deflation. The fed and its vassal banks can game inflation to keep the connected and powerful whole, we the people are screwed. The ONLY product of the fed is DEBT. Deflation is the destruction of DEBT, we the people are screwed again with one BIG difference , Debt free assets cannot be manipulated by the fed and debt free transactions without credit belong to we the people . Our job is to be We the people. So as our Anglican brothers like to say, carry on.

Debt is not only a product of the fed, it is the fuel that runs the markets. The best collateral is not the underlying asset, but the paper that represents the debt on the asset. It’s the Twilight Zone of investments.

If the fuel of the market is weighted to silver or gold based debt then that fuel is elevated to the status of money and is secure in its value.Everything else is debt and is not secure in its value and is open to the devious manipulation of others . History holds no example of lost of trust in gold or silver backed fuel , this is not true however of credit based fiat. Imagine the chaos that would be imposed if an agency of a political system could change the boiling point of water. The natural consraint imposed by immutable properties on humans deliver a fair field of play .

QE3? Where have you been!?

You mean if they launch QE4!

The Fed is middleman in this, neither creating nor destroying debt, but simply offering the Treasury an intermediary who holds that debt, and then passes it on to the primary dealers who do likewise. How it is collateralized, into real capital expenditures, or into stocks, matters little to them. (Though it should) Their purpose is to fund government spending, so when JP draws a blank on fiscal policy and the dollar I am agasp.

There are a lot of things you can do to reduce your own personal inflation rate. A few examples are to primarily buy meats, produce and other raw ingredients when grocery shopping and avoid boxed and prepared food items. Cook for yourself and avoid eating out. Also buy quality clothing and footwear the first time to avoid replacing worn out items or to keep up with “fashion.” Do most of your own home and automobile repairs and maintenance. Get a gym membership and stay healthy to reduce extortionary health care costs. Corporate America hates healthy and self-sufficient “consumers” with little debt and money in the bank.

For me, this is the best of Wolf so far. Excellent.

To understand certain aspects of inflation and its effects, here’s a pretty good link with an excellent in-depth analysis of inflation and corporate bond spreads. Most of the MSM articles really do NOT approach explaining the real dynamics of cycle of the inflationary trend, interest change effects, and market direction at all. This analysis from Seeking Alpha is a good step to reveal the real crucial indicators and effects of inflation trend that we are in right now. Victimization is due to a lot of not explaining any of the real facts that economic activity really can’t be read in the stock market charts.

https://seekingalpha.com/article/4274110-cycle-matters-seeing-credit?

1) A clogged vein constrict normal blood flow.

In 2000 bubble the tech sector was above 30%, choking the rest.

Today its around 22%, constricting the flow of other sectors like finance & energy and commodities.

Another correction will further rectify XLK and enable the rise of XLF, XLB, and XLE. At the bottom of the next correction, before inflation rise, get commodities, and commodities users.

2) The income chart above shows that only one quintile make it above 100K.

The other x4 quintiles, the lower 80% of wage workers, are under 100K.

The majority of the population live near the coast lines, not in the flyover. When rent is too high, unsustainable, tenants enter a bear market and leave.

– The top quintile, the top 20%, contain the top 5%, top 1%, top 0.1%….0.0001

==> the top of Pareto chart.

When Gauss become Pareto, the snake head will be cut. The ultra rich donate & fake. They tell the lowest quintiles that they are guilty, hate money and capitalism, in order to survive.

3) The Fed clueless, but not the gov.

US yield curve gravity with Germany pull them together, indicate low future inflation.

That is blessing to US Treasury.

US fragile seniors and those on snap will be oppressed when inflation takeoff, above the smoke screen of the yield curve.