Five companies blow $55 billion in Q1 to prop up their own shares.

Apple was once again the biggest share buyback queen of them all: In the first quarter of 2019, it spent a new all-time record of $23.8 billion on buying its own shares, apparently because everyone else was selling them, and someone had to buy.

Over the past four quarters through March 31, Apple spend $75.1 billion on share buybacks to prop up its own shares, according to the latest report by S&P Dow Jones Indices. But Apple’s shares remain 16% below their peak last October. Over the past five years, Apple spent $284 billion on share buybacks.

When a company buys back its own shares, the shares get canceled and disappear, the cash used to buy them gets handed to sellers and is gone, and “stockholder equity” on the balance sheet drops by that amount.

Buybacks are at the core of financial engineering: They lower the share count, and so earnings are divided by a smaller number of shares, which generates a larger earnings-per-share figure, and a lower price-earnings ratio, to bamboozle people who still bother to look at these metrics after 10 years of being told that fundamentals don’t matter.

Share buybacks also cover up the dilutive effects of stock-based compensation plans and stock-based acquisitions of companies that have no earnings, such as startups, that Apple and others constantly gobble up.

Apple still has a rock-solid balance sheet and can afford to blow this kind of money. Other companies are not so lucky; nevertheless, they did blow a ton of money on share buybacks.

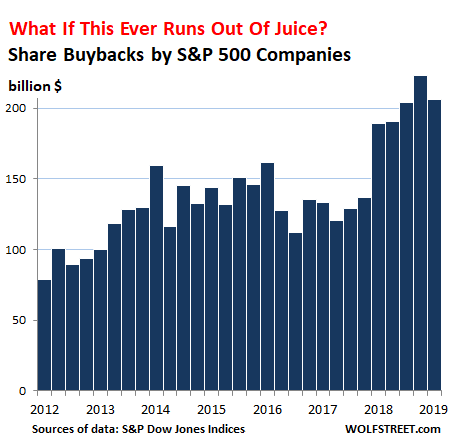

In total, companies in the S&P 500 index spent $205.8 billion in Q1, the biggest first quarter ever, the second biggest of any quarter ever, and up 8.9% from Q1 2018, but down 7.7% from the all-time dizzying record in Q4 2018:

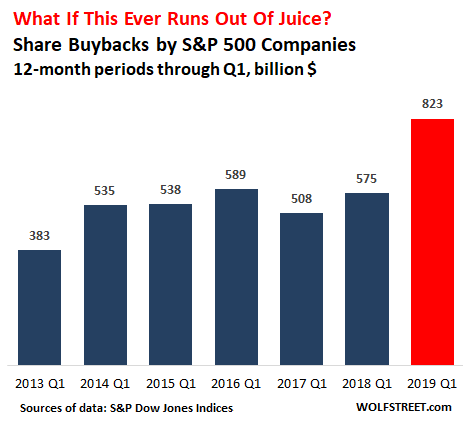

Over the past 12 months through March 31, share buybacks jumped 43% from the prior 12-month period, to a record $823 billion. And it’s adding up: Since 2012, share buybacks have totaled $4.03 trillion, which is about the magnitude of Germany’s annual GDP. The chart shows share buybacks for each 12-month period through Q1:

Higher share prices in Q1 than in Q4 – less bang for the buck – and the 7.7% decline in share repurchases in Q1 from Q4 resulted in 20% fewer shares being repurchased in Q1 than in Q4. The share count dropped in aggregate by 0.94% down from a 1.18% drop in Q4.

The buybacks are “top heavy,” with only five companies accounting for $55 billion, or 27%, of total buybacks in the quarter:

- Apple [AAPL]: $23.8 billion in Q1; $75.1 billion over the 12 months.

- Oracle [ORCL]: $10.0 billion in Q1; $35.3 billion over the 12 months.

- Pfizer [PFE]: $8.9 billion in Q1; $15 billion over the 12 months.

- Bank of America [BAC]: $6.3 billion in Q1; $21.5 billion over the 12 months.

- Cisco Systems [CSCO]: $6.1 billion in Q1; $22.8 billion over the 12 months.

And it’s getting increasingly top heavy: The top 20 share buyback queens – of the 389 companies that reported share buybacks in Q1 – accounted for 51% of total share buybacks in Q1, up from 41% during the 12-month period, and up from 36% in the prior 12-month period.

The tax cut did it. Obviously, everyone knew what would happen: Passed under the pretext of encouraging US corporations to “repatriate” their previously untaxed overseas profits and invest them in the US to produce more in the US and to hire more people in the US and to move the US economy forward, these provisions of the corporate tax cut have instead led to a tsunami of share buybacks.

Everyone knew in advance it would happen, despite rhetoric to the contrary, and so share prices surged first in anticipation of a tsunami of share buybacks and then as a result of it. And when the selling went wild last year, shares plunged less because there were buyers out there, buying back their own shares, at the highest possible prices with relentless bids whose sole purpose was to drive up the price of the shares they were buying.

But these profits registered in overseas mailbox entities that are being “repatriated” for share buybacks are not endless, and they’re being drawn down. And borrowed money that is also used for part of these share buybacks requires loosey-goosey credit markets, which we have now, but credit cycles turn, and when investors in bonds and leveraged loans get burned, they tighten the screws, and borrowing money to blow on share buybacks gets tough.

The Fed has already accomplished more with its verbiage this year than it had last time when it cut rates all the way to zero and did trillions of dollars of QE. My podcast.… THE WOLF STREET REPORT: Stealth Stimulus Has Arrived

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Creating a Smaller P/E ratio keeps the valuation from looking to high, when in reality it is.

Qué? That’s the opposite of what happens.

As I mentioned in a previous comment, share buybacks are a form of liquidation of a company. Same thing with overly generous dividend payments. As long the companies are profitable, you can prolong the game, but when the buybacks, dividends, and cost of borrowing outstrip the revenue, the end is in sight.

And the buybacks also indicate the company has no better use of capital. Remember when Gary Cohn was speaking to a room full of execs when he worked in the White House. He asked how many of them were going to use the money from their tax cuts / repatriation for CapEx and literally a couple of people clapped but the silence was deafening and it even caught Cohn off guard for a moment.

Demand for shares other than for buybacks has dried up. My dartboard says it hits the fan between 2nd week of Sept to Mid-Oct.

I don’t think this can be timed, so your dartboard analogy is apt.

I’m going to use the conventional logic of the textbooks here, rather than my own more jaundiced opinion, but here goes: investors invest in plant, equipment, research, development, and inventories because they think there is demand out there for what they would be selling. Demand is made up of income and credit. Income is radically skewed, so somewhere between 70% and 85% of the population is dependent on credit to increase demand, as their incomes are flat or falling (when you disaggregate the income numbers, it turns out that almost all income gains over the last four years are among managers, professionals, and those who work in states that raised their minimum wage). People are reaching the limits of credit they can service. Therefore, you have little to no reason to invest in plant, equipment, research, development, or inventories. So you buy back your stock, boost dividends, and hope that someone, somewhere, is going to increase wages significantly so that you can keep selling the things you are now, and perhaps down the line make old-fashioned “real economy” investments.

What candidate will have yo raise minimum wages in their campaign?

Is all tax cuts, that really tax redirection, that means some taxes get cut and other gets raised and maybe new taxes appear.

Companies hate to raise the minimum wage despite the fact they are making a lot more dough than the last time it was raised.

The idiots don’t understand that highter wages means people has more money and if people has more money they tend to waste more money and that means they buy more.

But who you hear saying to the public that raising wages would be good for the economy?

Some specifics:

– Real wages for 70% of employed Americans (production / nonsupervisory workers) have been flat for 60 years.

– In the meantime, real per capita PCE costs have increased to 4x what they were.

And the savings rate is very low. There was a huge adjustment in 2018, but it was based on unreported income (proprietorships, LLCs, other flow-through business income), virtually none of which obtained by the 70%, whose collective savings rate can be generously estimated at near-zero.

On the other hand, businesses feel they can’t raise wages, because they need to remain competitive. The wage repression has resulted in the highest profit margins ever, such that US corporate profits / GDP is 70% higher than Warren Buffett has said is sustainable. In any case, corporations as a whole are rolling those unprecedented profits into buybacks– further enriching those with capital at the direct expense of the 70%.

This house of cards cannot stand. It is far too unstable. Trump is just the first warning shot.

You make some very appropriate points. It is why I think the push to put tariffs on foreign made products is probably doomed to make the situation only worse. To successfully bring some of those products onshore would require a shift in paradigm to investing in manufacturing rather than just buying back shares and counting on the FED to push interest rates down. And it would have to happen quickly. But I question whether the U.S. has the know how, both financial and technical to do that. And I question whether the corporations have the mindset to do it. It is much less risky to just buy back your stock. A point you make clearly.

A few years ago Bill Gross had commented that once upon a time $1 in credit nearly increased GDPby the same amount. At the time he made the comment, he said $1 in credit increased GDP by $0.05 so I guess as long as interest rates are below 5%, there will be demand for credit.

A manipulated EPS number (via massive buybacks) generates the illusion of earnings stability, which drives the P/E ratio higher.

Regarding: “Buybacks are at the core of financial engineering: They lower the share count, and so earnings are divided by a smaller number of shares, which generates a larger earnings-per-share figure”

This trend (and others), is covered quite well in a new Chris Hedges book, called, “America, The Farewell Tour”. The title is a big hint where this financial malfeasance is taking America (and Canada), and what it is doing to citizens who are not in the rarified 1%.

snippet from Amazon review: “Hedges–who was unsurprised by Trump’s victory–shows how neither the left nor the right are addressing the systemic problems. Until the corporate coup d’état is reversed, these diseases will grow and ravage the country. A humane cry for a decent future, this remarkable book is our wake-up call to reality.”

America, Canada…and a large part of the western world that’s bought into the ‘no alternative/debt is wealth//end-of-history we’ve found the perfect solution’ narrative that’s held sway for a time now. Backed up by the phenomenon of perpetual war against nebulous and ever-changing enemies, as predicted by Orwell in ‘1984’.

We truly are through the looking glass – but we do still seem mostly to aspire to be like Bobby Axelrod rather than Mahatma Gandhi, so maybe we get the system and the leaders we deserve in the end analysis.

When corporations stop buying back stocks Fed will. JP has said he wants the “authority to buy a broader range of assets” in the next QE. There is also the possibility that in a market meltup (a hyperinflation of assets) companies will start issuing new stock, and do stock splits. What investors are willing to pay for stocks in terms of earnings, is a function of what the currency is worth, and the bond market. Corporate debt is firewalled off, so there.

Central Banks buying publicly traded stocks: effectively this is turning the stocks into “fiat” stocks, like fiat currency. Ultimately it should end badly. But in the meantime, it will serve as a safety net and draw more money into the whirlpool.

The monetization of stocks (like using bonds for BIS payments) is obvious, buying stocks would make the obvious tangible. Whirlpool or squirrel cage? Fed designates stocks held on its balance sheet as closely held, (available for shorting), and corporate America prints more. The purpose of the Feds divesting bond holdings from it’s balance sheet is to make room for (stocks) at some later date. The notion that the Fed is selling bonds to make room for bonds is ludicrous.

That’s why the Fed is now indispensable. Without it, the whole racket would collapse and living standards would fall back to the beginning of the 19th century. Not that it can’t happen, but probably not as long as the petrodollar is alive.

sorry, but I am shocked and coming to this late! Ambrose, could you say again (or provide a link to the news) that Fed is BUYING EQUITY SHARES ON IT’S Balance Sheet?!!!!

Kiers,

I have read Ambrose Bierce’s paragraph three times, and I don’t understand what it is saying. Its occasional future tense and conditional structures make me think this is about a potential future development, rather than what is going on right now.

“Sell to expand, buy to contract.”

Companies buying back shares or paying dividends out of profits is fine. That is return of income to the shareholders. When they borrow money to buy back shares or pay dividends, it is a potential problem, especially if they are frequently cash flow negative.

“…when investors in bonds and leveraged loans get burned, they tighten the screws, and borrowing money to blow on share buybacks gets tough.”

I guess that the next step will be for companies to start divesting themselves from their assets. For example, when Mark Hurd was HP’s CEO, he sold dozens of assets (while renting some of them back) to perform cosmetic surgery on the balance sheet. That was standard practice in the 00s. IBM sold plenty of assets too but Hurd was probably the most aggressive seller. He was caught falsifying his expense account (a minor sin compared to what he did to the company) and got embroiled in a sex scandal. He was fired with a ~$50 million severance package. HP shareholders were taken to the cleaners to the tune of $10B.

I believe the same will happen again as credit becomes more expensive. The art of performing magic tricks is to ensure the public looks everywhere where except where they should be looking at.

hey don’t let carly fiorina off the hook. makes me cry what she did to hp.

HP was a derelict husk long before Carly Fiorina was called in to bust out the joint.

Mark Hurd was immediately hired by Oracle, which apparently doesn’t care about financial or personal improprieties, or running companies into the ground. (But notably ORCL is up 30% since he was hired.)

It took me a while to realise that “flexible morals” is a thing for ones CV, but, I finally did when I experienced the career trajectory of two people up close:

One was a manager who hired friends and family as consultants for millions per head per year, for years. The other was the controller who signed off on it all. Both of them got nailed eventually, then ceremoniously fired and prosecuted for fraud. There were several stories with names and pictures in the serious papers that business people read. According to my LinkedIn-feed both of those jokers got similar high-level jobs within 6 months.

There is, I.O.W., an active Job Market also for the alternative skills that these people have!

Intriguingly enough selling off the family silver, laying off people and closing down R&D centers is exactly what GE has been doing since 2017 after it came to light Jeff Immelt’s “stock price magic” came with a terrible price attached. And that “stock price magic” had come among other things at the price of selling off more family silver. See GE Plastics.

After the layoffs started earlier this year, the Wall Street hype machine went back in sanguine mode: buy GE, buy it now, buy it without thinking.

But I am thinking, in the specific about the R&D cuts. In five months GE competitors, ranging from Rolls-Royce to Shenyang, had already hired all the people fired from the overseas R&D centers and put them to good use. GE will pay for this dearly down the road.

On top of this GE is looking for a buyer for GECAS, the aircraft leasing arm. It has long been one of the company’s best cash generators and has always placed big orders for GE Aviation engines. GECAS has been stripped of assets over the last couple of years (read: aircraft sold to raise cash and not replaced) and if not for the present cooling of Sino-American relationships it would have already started to speak Mandarin as the Bank of China has expressed “strong interest” in at least two occasions and they have the cash to be serious about it.

Sacrifices must be made for a reason, a good reason. The cash raised by selling off parts of a group must be put to good use, not merely used for financial wizardry or frittered away to prop up unproductive divisions and pet projects.

So far the GE leadership still seems to live in Immeltland, where the only thing that matters is the stock price. They probably plan to be long gone by the time painful decisions, such as stopping buybacks and slashing executive compensation will have to be made.

They may or may not be so lucky.

I would argue that GE’s issues didn’t begin with Immelt ( not a fan). The guy before him, old Jack Welch was an early leader in ” financial engineering”. He was able to get out with guru status long before things hit the fan.

there is nothing inherently wrong with buybacks. the issue is that companies are borrowing money to do it. because interest rates are artificially low, due to the financial engineering of the fed, we have this distortion.

apple is a troubling case because it signals that they are past there growth stage and have become a mature company. since jobs died they have lost all their vision for new products. they have nothing better to do with their money yhan buybacks. pitiful. they have become microsoft.

It’s not as if these corporations are FORCED to buy back their own stock just because the IRs are low – the reason they do it is because it’s an easy way of hitting growth targets (and getting better option strike prices, fast)- much easier than innovation, for example.

Blame it on a system that requires perpetual growth at all and any costs, and demands it instantly. That’s what leads to the manipulation.

“A system that requires perpetual growth at any and all costs, and demands it instantly”

I think we’re gonna need a bigger .. Planet Ferengi ! ……..

Problem is, there ain’t one close by, so it looks like we’ll totally trash the only one we’ve got, all for the “THIS IS YOUR GOD !” Dollar. What a world, what a world ..soon to be What a waste, what a wasteland !

I’m just surprised there arn’t more financial services companies on this list, like insurance companies!

I can understand tech being up there as some have a lot of cash on their balance sheets.

GE is the same as GM a globalised vampire corporate ,sucking America and western “investors” dry, that is today, as American, as squid and seaweed won-ton’s

Stock buy backs and naked short selling and creating fiat backed gold were illegal in the less insane past. Planet Ponzi with almost free money has to continue its march toward a fiat calamity of unknown result. As long as their is a perception that debt does not matter and the natural enemy of fiat , gold, is being created by paper the fiat will continue and will have to increase at a geometric rate. It will not take much to panic the herd due to the media and goverment constant fear message, you must be afraid of everything and be terrified until giving the all clear . The question is this , Will you have command of Your emotions to see that you must step aside before the herd goes over the cliff. Greed will take you over the cliff.

Buybacks were considered illegal until 1982, because they are a form of stock market manipulation. SEC Rule 10b-18 provided corporations a ‘safe harbor’ to buy back their own stock under certain conditions.

Notably, the SEC never has audited to ensure that corporations meet those safe harbor conditions. Because corruption.

Indeed, buybacks are Gilded Age shit.

I wouldn’t worry about companies that use their profits to buy back shares- I would only worry about companies that borrow to do so.

In addition, I would be more interested in net share repurchases since, as Wolf describes, these repurchases can mask how much the management is extracting in compensation.

Boeing is the poster child for buybacks. They cannot invest in aircraft design, so passengers die. Instead, they borrow money to plow into buybacks (along with all their profits). That is why they have a negative book value.

NOT.

HP BY far.

After over a decade and billions of shareholders money, spent on buybacks, there were more hp shares, than there ever had been.

Due to Management share compensation/bonus schemes.

HP then in that incarnation, effectively died.

The insane thing is that this level of blatant corporate administrator fraud, is still legal in America, making America the land of legalised corporate fraud.

If Boeing partnered with Google, they could use the accelerometers in the passengers Android smartphones to detect a problem with the aircraft and then have robots buy life insurance policies on everyone with Boeing CEO’s as beneficiaries while the plane is going down.

Hiding In Plain Sight

Using loans and leveraged loans to buy back shares.

The question being, how much of this credit has made it’s way into the derivative sphere? In the form of Credit Default Swaps, Securitized Loan Obligations, Collateralized Debt Obligations, Credit-Linked Notes, etc. To name just a few.

Without even looking at the junk bond market, which many corporations have used to raise the capital needed for their share buy back programs.

These derivatives and junk bonds have been sold to everybody and their cousin!

Some think that purchasing a credit-linked note, keeps their investment protected from derivatives. Well, guess what? These notes have at their core an embedded derivative of some type. Out of sight? Out of mind. Caveat Emptor. Buyer beware.

These twisted, intertwined, complex, and complicated, debt instruments and vehicles, have a common denominator. Think of those very large, complex domino settings. It takes just one domino to start the entire display toppling over. Just waiting for that first domino to fall. Won’t be long now.

This is a great report!

If you are still buying stocks or ETFs after knowing that buybacks increase equity prices, I’m not sure what you are smoking.

I have a feeling this will end badly and with a lot of sobbing and tears.

There is a parallel story in Treasuries. For the rates to go down (without the Fed not changing Fed Funds Rate targets), someone has to BUY a lot in both auctions and resale markets. Buying a lot makes the price go up and the yield go down. Other than the SOMA Reinvestments (which can act like another Operation Twist if the Fed allocates the reinvestment in LONGER term Notes and Bonds), the culprit here can be tracked to the Primary Dealers. If you look at the NY Fed reports, the primary dealer inventory of Treasuries was the highest on record, about $280 billion. I wonder how they will offload those as the foreigners are in a diet.

IAMAFAN : Ditto on your comment, let’s have a single malt and watch for activity at the edge of the cliff.

I am giving up the quaint notion that we ever return to “normal” markets

that time has passed. There will be more QE, maybe like Japan. There are no free markets, America is and has been for some time A corprocacy

Are Bank of America buybacks “normal”, or are they the preferred Treasury shares from TARP?

The CEO has said it is buying up the dilution from the financial crisis….

I miss the old days when companies bought back shares because management thought they were undervalued. I used to view buybacks as a positive sign. Peter Lynch discussed it in his book One Up on Wall Street. How quaint that book seems now. Value investing? That’s so 20th century.

Buying back shares when shares are at or near all highs can only be interpreted as management shenanigans.

What are the “boards of directors” doing??? What a farce.

” Passed under the pretext of encouraging US corporations to “repatriate” their previously untaxed overseas profits and invest them in the US to produce more in the US and to hire more people in the US and to move the US economy forward, these provisions of the corporate tax cut have instead led to a tsunami of share buybacks.”

The money did not disappear into thin air. Someone received it, and the only thing that someone can do with it is either invest it or spend it, both of which will boost the economy. It may even be propping up the low interest rates we see now.

“The money did not disappear into thin air. Someone received it, and the only thing that someone can do with it is either invest it or spend it, both of which will boost the economy.”

Or it can simply lead to inflation and not really boost the economy at all. GDP may rise but inflation adjusted it stays the same.

The buyback money gets reinvested in other passive assets like stocks and bonds. This does not help the economy. It just increases the price of passive assets. What helps the economy are investments in wages, equipment, buildings, etc.

Just a bit of historical Perspective,Buy Backs went parabolic into 2007 just before ….. well you know the Story https://static.businessinsider.com/image/53402a696bb3f7fa2a030178/image.jpg

All part of the ongoing theme of the stock being the product. This has been discussed in prior articles and continues to be the case in many of the leaders of the buyback process.

Wolf : thank you very much for giving us this information. It is an excellent article. And you explain clearly the sheer level of manipulation that is ongoing when it comes to company valuations based on “share prices”

Perhaps I am a fossil – but I remember a time when share valuations were based upon a company’s commercial and financial performance.

This sort of buy back chicanery should not be permitted in my opinion.

It is robbing peter to pay paul, while trying to dupe potential investors.

Wolf, you are doing a great service to the readers of this site. Please keep up the good work! And thank you.

Was QE a giant bond buyback to make the economy appear better to boost confidence? The government “investing” in its own treasuries and Fed back mortgages?

Interesting thought about what happens when profits drop and these mail box entities draw down their cash and the money for buybacks dries up. Maybe disaster or maybe by then we will be in negative interest rates so you can borrow cheaper than your declining profits and keep the nonsense going. My guess if you plotted out cash burn, you could find potential pain points….who knows might be a good predictor of rate cuts. The Fed is owned by the markets.

“Running out of juice” if of course the description to all collapsing Ponzi schemes.

The money was repatriated unless an investor spent it on foreign products or investments. The companies doing the buy-backs lose control of that money. Federal reserve notes (spendable $USD) can be controlled in many more ways than overseas profits. Senator Romney (via Speaker Ryan) had more input in how the tax cuts were structured than President Trump. And Senator Romney wasn’t even a Senator yet.

The notion that buybacks are OK unless companies borrow to finance them is a bit hopeful.

Companies always borrow. Buybacks in the retail space are particularly suspect since open-to-buy is the perfect measure of growth and prospects.

Buyback operations always conceal their true source of funding.

In order to create transparency, the names of the shareholders and the names of their owners and their owners and their owners etc. would have to be public. At that point, buybacks wouldn’t make any sense. Of course, that is not going to happen. The few powerful financial entities easily control and manipulate the market. The rest is just morons, pansies, and victims.

This used to be considered a form of stock manipulation and was illegal. Now it’s a good idea? GE bought stock back at a high price and then watched their share price collapse. This kind of financial gambling should be restricted to a casino.

Radio shack bought more than $3 billion in stock buybacks before the bankruptcy…

The worst crime is BANKS burning “Tier 1” capital to buyback their stoopid shares!

The market as a whole: $500bn margin debt; $200 billion+ buybacks. This is what makes a “roaring economy”?

sorry, that’s $800bn+ buybacks and $500bn plus margin = $1.3Trn on a total market cap of 15Trn = 6% return.

A slew of stories and articles have hit the news about how companies buying back their own stock are driving the market higher. Trump’s tax law which lowers corporate taxes and encourages repatriation of cash that has been stored overseas has fed fuel into the share buyback frenzy.

To be perfectly clear, buybacks are a tool corporate boards and CEOs use to manipulate the prices of their own shares higher. This means insiders can get out or hedge their positions before reality sets in and prices fall back to earth. Call it a well constructed exit strategy if you like.