Madrid, Barcelona, other markets are well on their way. But some markets are still crushed.

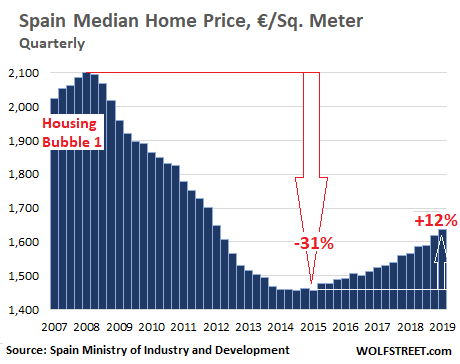

Spain’s last epic housing bubble, one of the biggest in living memory, propelled median home prices to €2,100 per square meter, at which point the bubble began to burst. The national median price eventually plunged 31%, according to government data, as Spain’s financial system began to collapse only to get bailed out by an international aid package. The long-drawn-out event wreaked all kinds of mayhem on the economy, workers, and the people. So where is the housing market now?

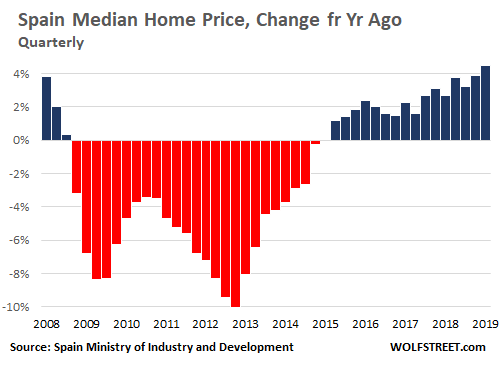

The median home price in Spain increased by 4.4% year-on-year in the first quarter of 2019, compared to the same period last year, to €1,636 per square meter (to convert € per square meter to $ per square foot, divide by 9.6), according to new data by Spain’s Ministry of Industry and Development. This pushed the national median price to its highest level since 2012, but it remains 22% below the crazy bubble peak:

Averaged out across the nation, across hot and cold housing markets, the current upswing in house prices has a ways to go before it comes even close to emulating the mind-watering dimensions of the last bubble. But in some markets, prices have been surging for four years, while in other markets, prices are now below where they’d been in Q1 2015, during the national low point. In these markets, prices have remained crushed (we’ll get to those in a moment). But the national median price throws all of them into the same bucket.

The first-quarter surge of the national median price was the biggest year-over-year gain since the first quarter of 2008 and the 16th year-over-year rise in a row. The year-over-year declines started in Q4 2008 and lasted through Q1 2015 — seven-and-a-half years of Housing Bust 1!

The current price resurgence pales compared to Housing Bubble 1. Between 1996 and 2003, the median price in Spain rose by 176% — meaning prices nearly tripled over the span of seven years. Since 2015, so over the last four years, the median price in Spain has risen 13.5%.

But real estate is local. And in some cities and regions, the boom has been reignited. The biggest year-over-year price gains occurred where prices are already heating up again:

- Madrid: +8.3%

- Seville: +8.1%

- Barcelona: +7.4%

- Navarre: +7.0%

- Balearic Islands: +5.1%

- Canary Islands: +5.0%

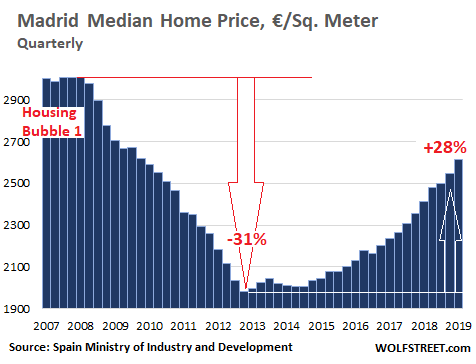

In Madrid, Spain’s largest real estate market, prices plunged 31% from the peak of Housing Bubble 1. From the trough in Q1 2015, they have now surged 28%, including the 8.3% year-over-year gain in Q1, to €2,613 per square meter, and at this pace are well on their way to Housing Bubble 2 — merely 12.9% below the crazy peak of 2008:

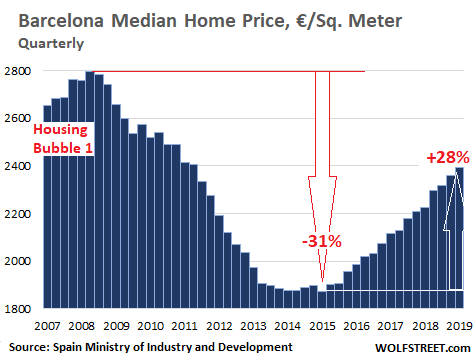

In Barcelona, Spain’s second largest housing market, home prices have tracked those of Madrid, but at a slightly lower level. The median home price plunged 31% from the peak of Housing Bubble 1 to the trough in Q1 2015. Then they surged 28%, including 8.3% year-over-year in Q1, to €2,392, also well on its way to Housing Bubble 2 — merely 14.5% below the crazy peak of 2008:

Aggregated home price data are somewhat in the eye of the beholder. The above quarterly data, released by the Spanish government, was dug up by WOLF STREET editor Don Quijones. He also dug up other data that show a similar trajectory of home prices, but on different scales, with much deeper plunges and much bigger surges.

For example, according to real estate appraiser Tinsa, house prices in Madrid plunged about 50% from around €4,000 per square meter at the peak in 2007 to around €2,000 at the low point in 2015. And by this measure, prices have since skyrocketed 62% to their current level of €3,240, which is about 19% below the crazy peak.

Something very similar has happened in Barcelona, where the median price plunged 50% from €4,400 per square meter in 2007 to $2,200 per square meter in 2015. Since then, the median price has surged 54% to €3,380 per square meter, according to Tinsa, but is still 23% below the 2015 peak.

Residential building activity is picking up for the first time since the crisis, with much of it focused on already heavily built-up coastal areas where demand for real estate, particularly among foreign investors, is strongest.

From Catalonia to the Balearic Islands, numerous building projects that fell through during Spain’s economic crisis have been restarted as growth returns. On the Costa Brava, a nearly 100-mile stretch of rugged coastline in northeastern Catalonia, some 20 projects are in the works, according to Don Quijones’ research, citing environmental group SOS Costa Brava.

The current mini-construction boom still pales compared to the boom before 2008, at the peak of which around 600,000 new homes were being finished each year. One year, the number reached a staggering 800,000, which meant that more homes were being built in Spain than in France, Germany and Italy combined, with an aggregate population four times greater than Spain’s.

Today, despite the best efforts of the last government to reanimate the construction and real estate sectors, including offering subsidies to first-time buyers and construction companies, fewer than 100,000 new homes are being built per year. Roughly 1.2 million people now work in Spain’s construction industry. While the number is growing, it’s still less than half as many as in 2008.

Does this mean that Spain is once again on the cusp of a high-octane housing bubble? The Bank of Spain and the Spanish government don’t appear to think so, arguing instead that real estate prices have merely reached a point of equilibrium. A few months ago, the IMF warned that although there is still no sign of a new bubble, there are indications of “a slight overvaluation” in the market.

While there may not be glaring signs of a national bubble, there are glaring signs in some markets, such as in Madrid, Barcelona, and some of the coastal and island markets.

But in other markets, home price have barely risen, and in in some markets, home prices are now below where they had been in Q1 2015, when the national low point occurred, according to the data by Spain’s Ministry of Industry and Development. And those markets remain crushed.

The table below shows all of Spain’s markets per the Ministry of Industry and Development: percentage change from the peak in Q1 2008 to the bottom in Q1, 2015; percentage change from the bottom in Q1 2015 to Q1 2019; and the median price in Q1 2019 in € per square meter. I highlighted the prices that are still below where they’d been during the national low point in Q1 2015 (if your smartphone clips the right columns, hold it in landscape position — there are 4 columns):

| From Q1 2008 | From Q1 2015 | Price in € | |

| to Q1 2015 | to Q1 2019 | Q1 2019 | |

| Spain, aggregate | -30.6% | 12.2% | 1,636

|

| Andalucía | -32.9% | 7.9% | 1,304 |

| Almería | -35.9% | 3.7% | 1,117 |

| Cádiz | -31.6% | 3.5% | 1,354 |

| Córdoba | -25.9% | 0.5% | 1,155 |

| Granada | -30.0% | 5.1% | 1,120 |

| Huelva | -40.7% | 2.3% | 1,083 |

| Jaén | -27.3% | 0.1% | 810 |

| Málaga | -36.7% | 18.9% | 1,769 |

| Sevilla | -29.2% | 5.1% | 1,333 |

| 0 | |||

| Aragón | -39.3% | 1.3% | 1,206 |

| Huesca | -31.9% | -1.5% | 1,140 |

| Teruel | -22.9% | -3.2% | 784 |

| Zaragoza | -41.1% | 3.4% | 1,295 |

| Asturias (Principado de ) | -28.8% | 0.8% | 1,275 |

| Balears (Illes) | -22.1% | 23.8% | 2,321 |

| Canarias | -28.9% | 16.1% | 1,513 |

| Palmas (Las) | -28.6% | 17.8% | 1,608 |

| Santa Cruz de Tenerife | -28.9% | 14.3% | 1,418 |

| Cantabria | -27.7% | -1.1% | 1,456 |

| Castilla y León | -31.5% | 0.6% | 1,050 |

| Ávila | -43.2% | 2.1% | 841 |

| Burgos | -36.2% | -0.4% | 1,143 |

| León | -30.2% | 4.7% | 886 |

| Palencia | -20.4% | -4.8% | 1,002 |

| Salamanca | -25.0% | -4.2% | 1,173 |

| Segovia | -39.1% | -3.6% | 964 |

| Soria | -23.8% | -3.5% | 990 |

| Valladolid | -33.2% | 9.9% | 1,233 |

| Zamora | -30.9% | 2.9% | 865 |

| Castilla-La Mancha | -39.0% | 0.3% | 886 |

| Albacete | -28.6% | -3.8% | 923 |

| Ciudad Real | -29.3% | -3.4% | 753 |

| Cuenca | -27.5% | -0.9% | 776 |

| Guadalajara | -47.4% | 9.3% | 1,111 |

| Toledo | -45.8% | 2.5% | 832 |

| Cataluña | -32.7% | 22.0% | 2,019 |

| Barcelona | -32.1% | 27.6% | 2,392 |

| Girona | -34.9% | 7.8% | 1,533 |

| Lleida | -29.2% | 1.5% | 1,024 |

| Tarragona | -37.8% | 5.4% | 1,279 |

| Comunidad Valenciana | -33.4% | 9.2% | 1,226 |

| Alicante/Alacant | -30.1% | 7.9% | 1,312 |

| Castellón/Castelló | -40.7% | 6.5% | 1,088 |

| Valencia/València | -35.2% | 11.3% | 1,178 |

| Extremadura | -16.9% | -0.7% | 848 |

| Badajoz | -15.4% | -3.3% | 854 |

| Cáceres | -20.0% | 4.3% | 838 |

| Galicia | -25.7% | 2.0% | 1,190 |

| Coruña (A) | -25.3% | 3.7% | 1,224 |

| Lugo | -29.0% | 2.0% | 833 |

| Ourense | -15.6% | -0.4% | 957 |

| Pontevedra | -31.1% | 3.6% | 1,253 |

| Madrid (Comunidad de) | -32.0% | 27.8% | 2,613 |

| Murcia (Región de) | -39.3% | 2.3% | 1,003 |

| Navarra (Com. Foral de) | -25.4% | 8.4% | 1,417 |

| País Vasco | -20.8% | 0.0% | 2,406 |

| Araba/Alava | -22.7% | 2.8% | 1,993 |

| Gipuzkoa | -12.9% | 0.1% | 2,670 |

| Bizkaia | -23.5% | -0.6% | 2,367 |

| Rioja (La) | -33.4% | 3.0% | 1,129 |

| Ceuta y Melilla | -6.2% | 7.8% | 1,687 |

| Ceuta | -7.7% | 1.5% | 1,729 |

| Melilla | -1.5% | 12.1% | 1,688 |

Where are the foreign investors in this phenomenon that is playing out in the US? Read… US Home Sales Drop, Drop, Drop Despite Lower Mortgage Rates. But Mortgage Applications Jump. What Gives?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf and DQ, thanks for the magnificent report.

I lived in Catalonia several years (like DQ) and speak Catalan. Whenever I have a chance I read “La Vanguardia”, Catalonia’s largest paper. From what I have read it appears that foreign money is again buying properties, often sight-unseen, and immediately turned into Airbnb-like apartments. For Chinese and Russian nationals it’s a shortcut to obtaining residence. If I’m not mistaken, a 250k euro investment will do the trick. It’s also an opportunity to launder anything that needs to be laundered.

Yesterday Spain had three elections: municipal, European and regional. One of the biggest issues in Barcelona’s municipal elections was the overwhelming influx of tourists: 9 million in 2017, versus a local population of 1.6 million. Locals complain that they are being kicked out of their neighborhoods because of the short-term rentals. Barcelona, like Venice and other European cities have become nothing more than giant tourist traps… ooops, I meant wonderful tourism destinations.

You probably remember this angle already played out pre-2011: in some places “Russian oligarchs” were to blame, in others wealthy German retirees, in others still Dutch speculators. Seemingly everybody in Spain had a theory which involved foreigners buying properties “sight unseen”.

When the dust settled it was discovered what had fueled the bubble were the over 100,000/month mortgage approvals in the 2005-2009 period, with peaks of over 129,000/month in 2006-7.

Why would a “Russian oligarch” or a “wealthy German retiree” need to take out a mortgage in Spain to buy a horrible house in the middle of nowhere I was not told, and the issue quickly became so embarrassing it was quietly swept under the rug.

I’d like to say we are back to square one but this time is different. While prices go up up and up, sales go down down down. Existing home sales are down to an average of 34,000/month per Q1 2019 (they were over 36,000/month in 2018) and new home sales have hit the skids, with the latest data at a crummy 8,000/month. Construction output reversed route in January after a frenzied 2018 and has been going down since. We are down 5.5% year on year. Even mortgage approvals are down.

But prices tell a different story.

This is no new wave of foreign speculators: this is good old c. 2005 Spain back at her GDP goosing and vote buying tricks again, no doubt with full complicity of various European institutions. Again, just like last time.

Trust me on this: I am part Italian and part French and saw this kind of stuff firsthand since I care to remember.

Regarding European cities… as ye sow, so shall ye reap. Our administrators have been performing true feats of acrobatics to “incentivate tourism” and this is just reality presenting the bill.

There’s no money to be made in mass budget tourism and it leaves behind a mass of bills that still need to be paid, from the money-losing airports (cough… Girona Costa Brava… cough) that fuel it to cleaning after the average lager lout.

If my body holds up and I don’t kill one of my vendors over a defective batch of parts I’ll see you all in Spain this Fall. Riding is really really really good in the interior. ;-)

Funny how the so-called centrist politicians see rent gouging and price gouging in homes as something that will get them more votes.

There’s one of many reasons people are abandoning these parties.

Political radicalization one reason we probably are heading towards interesting and wholly unpredictable times.

The 12-month Euribor rate is -1.48% and the 10 yr Spanish bond is 0.8!%. I bet interest only home loans are very popular, especially for British remainers looking for a house on the mainland.

I understand that Spanish Mortgages are tied to your remaining economic life. My neighbor bought a house in Spain and only his younger wife qualified for the mortgage. It was not that long either. Not like the 30 years we are used to here.

I don’t really see 2600 Euro per m² as a high price for a city like Madrid. In Munich, Germany, nowadays prices north of 8000 Euro per m² for new buildings are paid. That is ~740 Euro per square foot. The Madrid prices would be about 240 Euro per square foot. What is the price in SF?

1. Compare household incomes in Madrid and Munich.

2. Munich is idiotically high priced. It’s not a good reference point for housing sanity :-]

Munich has a serious supply and demand issue.

Plainly put the city government has been handing out building permits with the utmost care if not downright stinginess, partly because residents of areas like Ober-Föhring have successfully resisted large development projects, partly because the present city government favors commercial over residential real estate (see the maxi CRE developments near the Hirschgarten) and partly through sheer political calculus. The CSU doesn’t really need to give people more reasons to vote for the Green Party. ;-)

This has resulted in a host of residential developments in the towns and villages within commuting distance of Munich, as far away as Holzkirchen and Erding. Good luck during rush hour on those roads and railroads. ;-)

The City of Madrid on the other side has been handing out building permits with what I can only call complete abandon for almost two decades now.

Madrid is not exactly an economic powerhouse like Munich is and according to my fashionable/cool/hip/etc acquaintances it has lost “a lot of glamour” over the last few years. I trust their judgement because I am the least hip person in the room.

This is another matter of supply and demand, but the problem is the opposite as in Munich.

It’s funny to watch how the learning curve for humans is actually flat and coincides with the (0,0) reference!

Speaking of housing bubbles, the re-elected Liberal Party of Australia have just lit a fuse to the bursting Australian housing bubble.

First home buyers will now receive up to $100k from the Newly elected government towards their first home. APRA, the financial regulator are re-introducing sub-prime lending and the Reserve Bank of Australia is about to cut interest rates by 75bp.

Thats not a fuse, Thats a life jacket.

A life jacket to try to ride out a tsunami with hungry sharks waiting after that and …

China may be a worse housing bubble:

https://www.scmp.com/economy/china-economy/article/3011960/china-showing-signs-similar-japanese-housing-bubble-led-its

Australia has gone from housing boom to housing bust.

Seattle housing speculators may have moved south to Tacoma:

https://q13fox.com/2019/05/25/report-says-tacoma-has-hottest-housing-market-in-the-country/

Vancouver home prices have given way. Speculation in other Canadian cities continued to inflate prices.

Political radicalization one reason we probably are heading towards interesting and wholly unpredictable times.

For example, in Windsor Ontario,an industrial city near Detroit there is an accelerated housing bubble.

Rates in the Latin Eurozone have been moderating. Could it be that the front in the war on Brexit has preoccupied the EU monetary troops and left their flank open. It might be a fleeting moment if the EU takes a page from the Trump playbook, if you can’t make a deal with NK, punish Iran.

And….in 2012 Spanish tax authorities introduced declaration of worlwide assets on hard asset beneficisl owners (model 720).

The cycling is however, primo

Be surprised if property prices declined in San Sebastian (Pais Vasco) which is generally considered to be one of (if not the) most sought after destinations in Spain.

Income and wage growth has been largely absent from Spanish recovery as well and Commercial real estate has been keep afloat by US real estate thought this too looks overcooked – El Cortes Ingles in the process of selling its real estate portfolio to US Private Equity – Apollo Global Management.

“Spain’s last epic housing bubble, one of the biggest in living memory, propelled median home prices to €2,100 per square meter, at which point the bubble began to burst. ”

In Israel you need to go to really remote locations to find anything near this price. In Tel Aviv it costs 4 times as much. I wonder if this is a bubble and how long will it last.

Just come back from Camino walking in Galicia. Stopped in a town called Saria looking around the amount of property up for sale, the amount of property falling down through disrepair was staggering. Also noticed in Santiago for a town of 90k the amount of bank branches was enormous-crazy, Santander, BBVA, Caizabank etc etc far too many.

The problem is the stagnating wages of the younger generation since 2008: these prices may not seem so very high on the global scale, but in local, comparative, terms they are.

Demand in our (rich) province is mostly for apartment rentals, as the younger employed professionals with children cannot possibly afford the houses they would like.

Youth unemployment is still high – and still disastrous in some provinces.

Lots of young adults hanging around at home; even in my well-off family this is the case, as my siblings are not very bright or well-qualified and so can’t rent. It’s cheap to keep them in the large family house built decades ago.

Of course, all the brightest and best move to Madrid, Barcelona, or abroad, leaving the rest to fester.

An awful lot of people are going to have to swallow the reality that grandad’s lovely 4/5-bed country house built in the 90’s is not going to find a buyer at the price they want, I see them sitting on the market for many months…….

I live in Barcelona. What I have seen here is a perfect storm of factors pushing up prices. 1) Tourism boom. The number of tourists has at least doubled in last 10 years. Some apartment buildings have been converted to hotels to meet the demand. 2). Related to point 1, Airbnb, which has taken a lot of supply of the market. 3) ECB. Interest rates at practically zero has pushed demand for yield, and buying and renting a flat can get you around 5%. 4) Demand from international investors/speculators. 5) increasing number of foreigners and even companies moving here for the good weather and food. The international community here continues to grow, and many of these people have a lot of money (relative to locals) and earn much higher salaries than locals. 6) Companies like Blackstone that have been buying up rental properties all over the country, thus concentrating ownership. 6) The growing interest in city living. Most good jobs are concentrated in Barcelona and Madrid.

The problem for normal people is that salaries have not kept pace, so you end up with very high prices (rent or buy) compared to the local salaries. That said, this phenomenon in Spain is mostly in the big cities. My wife is from a small city near Alicante (pop. 75000) and the prices are super cheap. Why? 1) Salaries are low and 2) No jobs, no housing demand.

totally agree, I live in Malaga, and we face the same problems you mention.

Has the incidence of bed bugs increased in Barcelona? In Malaga it is now rife. My gf rents out an apartment to AiRbnb, unknown to her she moved one of the mattresses in the rental apartment back to her place and weeks later she is waking up with what she thinks is. strange rash,. turns out she has a next of bedbugs in the mattress. These bedbugs arrived apparently through suitcases which they sometimes can hitch a ride on.

Visited a ferreteria which sold the rather toxic pesticide for bed bugs and he told us that for 20 years he hardly sold one pack per month, now he says he sells many cases of the packs per week.

Airbnb is one of the causes behind this. Spain is seen as a tourist hotspot nowadays.

AS I mentioned on the Rigged Economy blog re this story. The real estate bubble in Spain is nothing compare to the rental bubble, caused almost entirely by AirBnB and other similar so-called sharing economy type businesses. I live in Malaga city and the rentals have gone up at least 40-50% since 2012. It has caused really bad feeling amongst usually friendly and generous Spanish people. They are being gentrified outside of the city centre as they cannot afford the rents.

And on top of that there is now a new explosion of bed bug plagues in central Malaga, a vermin more or less extinct for last 2 decades has come back with a vengeance due to a massive increase in short term tourists. The hotels have strict regulations about treating matrreses etc….no such regs for AiRbNb.

I now call them AirBed&Bug :-)

Probably same story in most of EU/Europe.

In my small Dutch city rents outside the social housing sector have increased around 100% in the last five years (average rent is now over 50% of average income). I don’t doubt that Airbnb is the major factor behind this, it went from non-existent to all over the place in just a few years and our local government is strongly encouraging this. It also helps that there is massive speculation by “investors” who buy homes to park their money because rates on savings accounts are zero in Europe (or even worse) and will probably never go back to normal if the ECB has their way, so why not buy a home and cash an easy 10% ROI every year. Most of these homes stay empty for years because why bother to rent out a home if you can get massive returns doing nothing? If enough people does this you get an epic shortsqueeze in the housing market …

Some of these investors are foreign investment companies and pension funds, but also many older people from all over Europe with significant savings. In the better areas of my town (in a remote corner of the country) you can find owners from almost every EU country nowadays – some of them visit the home for the summer vacation, but many of them never visit and just park their money there. Many of these people probably use the yearly appreciation to get a higher mortgage and buy even more homes in their own country and abroad. Until about 10 years ago foreign howeowners were only found in the tourist hotspots near the coast, speculation has now spread all over the country courtesy of the ECB.

Unlike the situation in Spain, Dutch housing prices are now (much) higher than the previous top in 2008; prices bottomed around 2013 at ~30% down from the previous top and the banks are expecting at least another 1-2 years of 5-10% yearly price gains. In major cities like Amsterdam prices have increased 60-70% in just a few years and only in a few remote areas prices are still below the previous top (but not for long I guess). In my city prices of single homes are now around 20x higher than around 1990 when the Dutch housing bubble started. I’m talking about “repeat sales” so the same home without significant improvements, both very small and old worker homes in the inner city (from 8-15K in 1990 to 200-275K now) and large monumental homes for wealthy owners (from 75-150K in 1990 to 1.5-2 million euros now). Only for apartments the appreciation was lower, more like 5-10x (which is still a ridiculous increase if you ask me). Over the same period, incomes have at best doubled or maybe tripled in rare cases.

But what can you expect when 10-year fixed rate mortgages are around 1.5%, everybody with a pulse can get a zero-down mortgage (officially 102% is the max now instead of 120-200% ten years ago, closing costs are around 2-3%), full deduction of mortgage from income tax (= government pays half the mortgage) and with a free government provided put option for any mortgage below ~300K euro (= it is assumed no owner can lose money when selling a Dutch home). Result is that nowadays basically any home below 300K is POS, a small new home with very small garden will cost 400-500K and anything a bit fancy will cost at least 750-1000K depending on location. Most Dutch homeowners are virtual millionaires, at least when measured in the original Dutch guilders. For sure it is one of the most epic housing bubbles on the planet and of course our politicians and much of the public loves it; the Dutch have decided to double down on tulip mania.

BTW, my brother lives in Spain (in the center, not in the tourist areas near the coast) and has been trying to sell his old home for two years now. The RE market seems to be close to dead over there with no sign of price gains…

Air Bed & Bug – troubling but also amusing.