Here’s Where Americans Suffer Hot Inflation, But There Are Cool Spots Too

This is something the people in the San Francisco Bay Area have figured out a long time ago: The national inflation numbers don’t quite measure up to local realities.

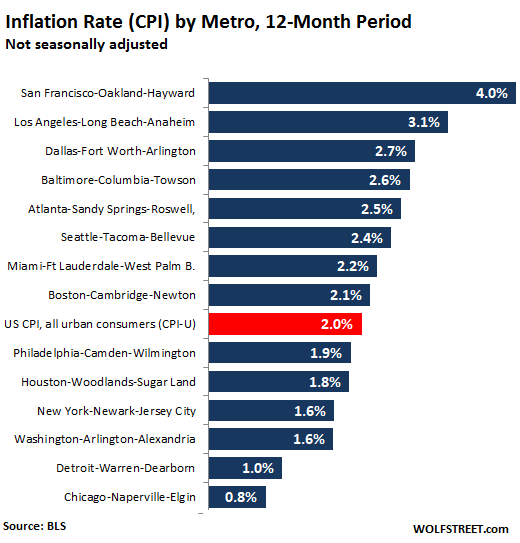

The Bureau of Labor Statistics reported today that the national Consumer Price Index for all urban consumers (CPI-U) rose 2.0% in April compared to April last year, the highest rate since November. The BLS also releases CPIs for the 14 largest Metropolitan Statistical Areas (MSAs) And there are large differences, from hot inflation of 4.0% in the San Francisco-Oakland-Hayward metro to much cooler 0.8% inflation in the Chicago-Naperville-Elgin metro. The red bar indicates the national average for April:

The two metros with the highest inflation rate are both in California. But note that the Dallas metro is in third place. At this rate, inflation rose five times faster in the San Francisco metro than in the Chicago metro.

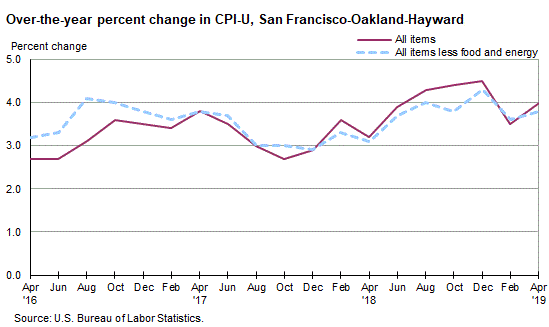

In the San Francisco metro, the CPI category of “food away from home,” such as at restaurants, jumped 7.6% from a year ago and tuition jumped 10.6%. Motor fuels jumped 9.5% and the people were getting restless to where Governor Newsom, blaming potential “inappropriate industry practices,” asked the California Energy Commission for an analysis of gasoline prices by May 15. There are no oil pipelines across the Rockies, so gasoline prices in California depend on other dynamics than those in Texas, and there have always been rumors of “inappropriate industry practices.”

But the biggie in terms of inflation because that’s where consumers spend most of their money is the index for services, which rose 4.3% in the San Francisco metro.

No matter how you look at it, the rate of inflation in the San Francisco metro is way above the Fed’s target, reaching to 4.5% late last year, and forceful monetary tightening would be highly appropriate for the metro (chart via BLS):

The CPI for the Chicago metro, for much of the past two years, has been wobbling around 2%. But in October last year, it started zigzagging down. The CPI without food and energy (blue dotted line) in the Chicago metro rose only 0.4%. A big factor is the index for services, particularly the sub-index for services without health care, which dropped 1.7% from a year ago helped pull down the overall index. The index for motor fuel rose 5.4% (chart via BLS):

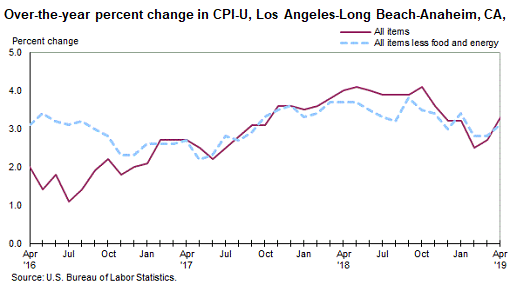

The CPI for the Los Angeles metro had been above 4% for part of last year, and after a brief dip late in the year and early this year has moved back up to 3.3% in April and appears to be heading back to 4%. The index for services rose 4.1% year-over-year, motor fuel 10.8%, food away from home 5.0% (chart via BLS):

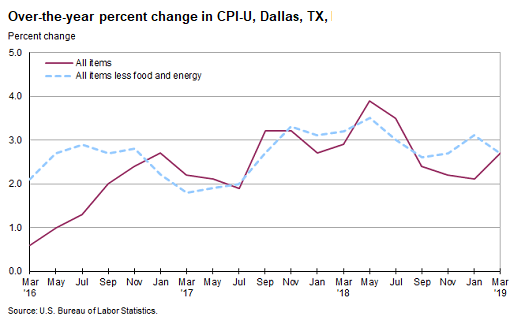

The CPI for Dallas-Fort Worth-Arlington nearly hit 4% early last year before tumbling to just above 2%, but that was clearly “transitory,” as Fed Chair Jerome Powell promised. In April the index was back at 2.7% and heading higher. Of note, compared to our prior entries, the index for motor fuel rose only 0.2% year-over-year, but the index for services rose 3.5%:

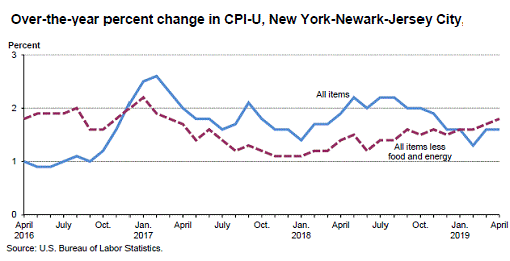

The CPI for the New York-Newark-Jersey City covers a vast and very diverse area, with some serious hotspots and some cooler areas. But averaged out, the CPI for the metro in April rose just 1.6%, with services up 2.3%, and motor fuel up only 0.8% (chart via BLS):

For some of these MSAs, the BLS releases monthly data. For others it releases data every other month. So most of the CPI data here are April-to-April comparisons but for the metros of Dallas, Boston, and Washington DC the comparisons are March-to-March.

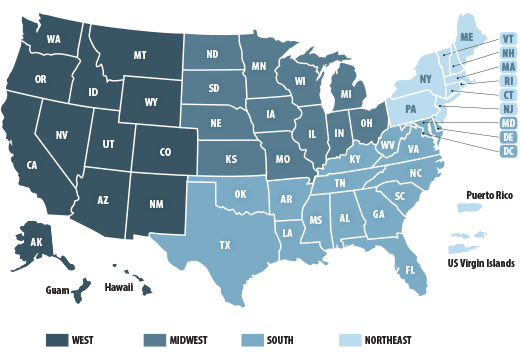

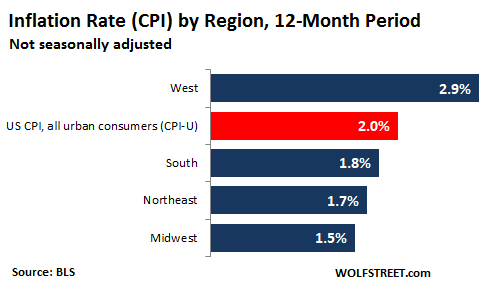

The regional CPIs fall as you would expect after seeing the differences above, from hotter in the West and cooler the Midwest (here’s a map showing which states are included in these regions):

{kind=link}

So it’s tough finding the right monetary policy for the whole country, when some areas, such as the San Francisco metro would need fairly harsh rate hikes that would push the federal funds rate above the rate of local inflation, and by a good margin, so about 5% — double where rates are today. But other areas might find the current monetary policy just right.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

According to these stats, if your lifetime savings are invested in long term inflation protected bonds (i.e. ibonds or tips), if you plan to retire in Detroit, you’re 1% ahead. However if you plan to retire in San Francisco, you’d be 2% behind and you’d need to rethink your savings strategy to make up for that loss.

If your retirement plan includes moving to SF, you have bigger problems than losing 2% a year on bond returns.

What would those problems be? Living in a world class city, in a world class region, in the center of the new economy, with amazing weather?

Parts of the city are disgusting but that is true of every city (except perhaps Bellevue).

For one thing, I don’t think the CPI is going to be high on my list.

There is a lot more to be happy about. And views are not that important to those who’d rather be close to their kids.

I don’t know about that. Most people would agree, LA and NYC are the only world class cities in the US. Most famous people have homes in both. Why would you live anywhere else? And, exactly what is the new economy?

A world class city? I resided there for forty years and tell you it’s been poorly managed since 1964.

It’s good enough for Wolf!

Well, for 1, human poop on the sidewalks…

…another: unaffordable housing

…another: crap schools (yea, there are some good ones, but we’re talking averages)

Old dog – Your retirement plan in a high inflation area is buying real estate. At any point, you can sell your house at a huge gain and move to a cheaper area. The optimal thing to do is to move to a big city with high income jobs and strong real estate appreciation when you are young, and then relocate to a cheaper area when you are raising a family and ready to retire.

Well I estimate my personal CPI, which includes Food, Utilities, and Gasoline is up about 10% this year. This is based on expenses in SoCal

Just depends on how you live. My personal CPI is about the same. I drive 5K miles a year, seldom eat out, watch METV. Stay away from the California made for tourists. Shop the mexican market with my homies.

Ethnic markets are total win.

Agreed. I shop at Aldi, Dollar Store, WalMart, eBay – lots of stuff delivered for $1.00 from China!?!?.

$6-$7 beers at brew pubs. The $3.00 double hamburger, small fry, soda meal I get at McDs, has gone up to $4.50.

For cheap lunches downtown it’s difficult to stay under $10, whereas 10 years ago, it was difficult but possible to stay under $5.00.

So it seems everything I shop in a store for / get online, is not moving up in price, but all of the services I pay for entertainment, are going up a lot.

Well my personal inflation rate is actually probably down this year. My property taxes fell more than 10% and my auto insurance dropped 5%. And no, I live in the same home and drive the same car. My health insurance premium stayed the same at $20 a month (only a $500 deductible) and has been that way for 5 years. Most people’s inflation rate for the last 10 years has been about 5 percent, not the 9 or 10 percent that John Williams or that flawed Chapwood Index state.

> There are no oil pipelines across the Rockies

Sure there are. They’re called railroads.

Every once in a while one explodes in a giant fireball, it’s quite pretty to watch.

Besides, California has lots of refineries. Oddly, they often have to go off-line for maintenance just before the Summer driving season – which lowers supply and raises prices. Odd coincidence, that.

In the spring (dates vary by region), California oil refineries are required to switch over to summer gas which evaporates at a higher temperature than winter gas. Since the switchover requires pulling down their storage to almost nil, they do thorough maintenance at the same time.

There are huge fines for refineries that ship gas that doesn’t meet the state’s evaporation standards.

No question prices in Socal are moving up, especially rent.

The inflation picture will change drastically for the worse in a few months once the tariffs work their way through the system.

There will be a market shaking inflation shock to the economy. We have not seen that in decades. Possible the inflation shock will slow the economy down in profound ways … it will limit QE options.

The $2 Tree soon coming to a neighborhood near by, as the Chinese winds circle the globe. Maybe General Dollar will buy them out : >{)

SocalJim – This is fake news. The tariff costs are being eaten by Chinese manufacturers to maintain market share. The cost of goods impacted by tariffs haven’t gone up much at all. The US and it’s consumers are winning big in this trade war.

Rent is not increasing in Socal. More rental units are being built each year and the population is declining. Landlords can’t find tenants at required rental rates so they are liquidating rental houses.

The Inflation Fraud Report is my current, recent realization. The Fed reports rigged inflation that comes in consistently low or just below on target, and this becomes the Fed’s reason the keep interest rates low.

But the reported inflation is false because it understands actual inflation because much of inflation is showing up in assets and other items not fully captured in the report.

In response to it’s lowish Inflation Fraud Report, the Fed suppresses interest rates because it wants inflation to go higher to avoid deflation. But lowering rates doesn’t increase inflation the Fed is measuring.

The Fed then traps itself into a straight jacket.

This straight jacket has been created by the Fed, to keep it trapped in eternal interest rate suppression.

I’m not particularly smart. Supposedly the boys and girls at the Fed are. So why hasn’t the Fed figure this out?

Why doesn’t the Fed Governors do and say something like:

“The inflation metric we use is not accurate for the best interest of the citizens of this nation. Our best guess is the normal, nuetral interest rate is 3%.

We are raising Fed rates to 3% effective immediately.

This is the Most Perfect Interest That Has Ever Existed. And if we change it, that new interest will be even more perfect.

The best way for the people of the United States to improve the economy at the Federal lever is through Federal Government spending. Interest rate manipulation is a very bad way to affect the economy. Federal government spending is a much more effective way to change your economy.

If you want to improve the economy, contact you Federal Government Representative and urge him to change policies. At the present time, it appears Federal Government spending is far too low regarding government worker pay, benefits, and social spending that will improve citizens daily lives.

And it is not the Fed’s job to make stocks or markets go up.”

Increases in general prices is greatest where the money velocity is highest. The inflation of the US currency has been going on for years now but the effects (increased prices) have been muted and uneven. The Fed knows this. The Fed’s primary challenge now is to try and get steady and relatively even price increases across the country and without bursting the main asset bubbles they helped create (housing and stock market). It’s largely an impossible task.

Not mentioned but probably more devastating around the country is stagflation; wherein prices rise but the result from no or low wage increases results in cutbacks by business and consumers that leads to a drop in overall economic activity.

Stagflation is what is creating a downward standard of living for those unlucky enough to be in jobs that have no pricing power in the market.

So we have this growing divide in the country. Hot economic areas with lots of “pseudo wealth” continue to inflate prices and wages and the rest of the country soldering on under stagflation with a slow but steady loss of economy. It should not be lost on any of us that this “pseudo wealth” essentially is being made on the backs of the rest of the populace.

The ending will not be pretty.

There seem to be golden corridors; Potemkin villages made shiny with paper money. But stray down some rural highway and you’ll quickly see towns caving in on themselves. What will these places look like in 20 more years? How do you maintain a 1st world infrastructure w/o a sufficient tax base? Answer: You don’t.

I don’t trust CPI numbers. Not because I think there’s some grand conspiracy to keep the numbers low. It’s because govt is incapable of doing anything competently.

Living in the Woodlands, TX i am surprised at the 1.8% number. Every restaurant, including the cheap chain ones, now charging $8 – $10 for a glass (6 oz. – min) of cheap Chardonnay. That used to be $5 a year or so ago.

While housing and gasoline may be inexpensive here compared to the nutty prices in the West, everything else is increasing in price way more than the 1.8% shown in the table.

Anthony Aluknavich,

People don’t notice when things get cheaper and better, such as TVs, laptops, smartphones, clothing, or services such as broadband and cellphone services. And they don’t complain when eggs get cheaper (as is the case this year). They only complain when certain prices rise because they stick out.

So looking at your restaurant checks, you have to look at the CPI for “Food away from home,” which in the Dallas metro rose 4.2% year-over-year, spread across all categories items in restaurants, cafes, and delis. So that’s a lot more than the 1.8% for the overall CPI.

And I doubt that you could get a decent glass of chardonnay at an average restaurant in Dallas for $5 a year ago. A long time ago, sure. The last time I spent any significant amount of time in Dallas was in 2005. Even then, a $5 glass of decent chardonnay in an average restaurant is not what I remember.

I might go five bucks for a nice head knocking cabernet…

Eggs lower?

Confirmed.

I bought a dozen at Aldi for $.49 the other day.

That’s a DEAL!

Pigeon eggs from downtown?

Aldi does have some decent stuff at good prices. I’d hate to be a supplier to Aldi.

Just want to point out that The Woodlands is part of the Houston metro, not Dallas metro. So using Dallas as the reference is incorrect. Houston “Food away from home” increased 2.8% year over year. Higher than the overall 1.8%, but not on the same level as the increase in Dallas.

Looking at the “big picture “, banksters agenda same as the other “deconstruction of America ” slugs !

On Friday, a financial app that I follow on my smart phone had an article about property tax increases in Jersey City. For people who had lived in their homes a long time, tax increases in 2018 of 50-75% were not unusual. It turns out, the article was a rehash of news from early 2018 on the city’s re-assessment of properties to current market values. From the 2018 version of the article: “In one neighborhood in Jersey City, New Jersey, the average tax burden will rise to $29,026 from $16,591, an increase of nearly 75 percent.” So the 1.6% inflation rate for New York-Newark-Jersey City does not mean very much if your property tax bill has increased by over 50%.

That property is probably worth well over a million. Either make it into a rental or sell. Those are good problems to have.

Easy Nicko, my story is marginal.

I bought a dump in SE Wisconsin that had sold by way of goomint guarantee for 134,000 in ’08, and I got it for 18,700 from the goomint in 2011. It had been only held by the buyer for less than 33 months.

The taxes were over 4,000 so I was paying 21.3% .

The place was a dump, but mostly sound. 55,000 to fix it up to being quite liveable.

My point is that the whole thing was fraud. I tried to get the local paper to cover such an obvious scam, but to no avail.

I couldn’t get much interest in this article, despite the great analysis, because in the real world I, and most of the people in know and interact with, can’t relate to it. This may be a useful statistic for the Federal central committee to use to justify their decisions not to raise social security, not to raise retirement benefits, but it bears little relation to the inflation that those of us in the bottom 90% have to deal with. In electrical engineering terms it is as if the CPI runs along the imaginary axis while those of us in the “real” world have to deal with an inflationary number that runs along the real axis. They are orthogonal (uncoupled).

It seems to factor in only the cost of a “package” (or quanta) of something and ignores the fact that the “package” size is continually shrinking. Although food has been a constant issue in recent years the cost of anything metal has skyrocketed in recent months. The cost of aluminum flashing, deck screws, wrenches has gone through the roof. And many small specialty woodworking tool manufacturers have cut back in the products they sell because the price has risen beyond what the average woodworking hobbyist will pay.

It is interesting that uses the CPI to justify not raising retirement benefit payments or social security payments. But it does not use the CPI in deciding to raise the cost of Medicare premiums or require the medical insurers to use the CPI when justifying their rate premium increases. Nor auto insurers or utilities in increasing rates. And it maintains the CPI within a low narrow range so that it’s value is truly irrelevant in it’s effects and to require any of the services I mentioned to use it would soon result in their bankruptcy.

So, Wolfe, though you do a great job in the discussion, it is pretty much an irrelevancy.

And the top 20% own 90% of stocks. The government is run by oligarchs, for oligarchs. Perhaps voters will choose wiser next time….

No matter which you select, owned by the oligarchs.

OE, and to a few comments in reply:

I agree. I’m doing okay but have found my attitude changing the last few years about rising costs. At age 63, I shrug my shoulders and say, (at the meat cooler), “Oh well, this price is criminal but it’s still 1/3 the price of eating out”. I’ll buy the big bottle of rum and say, “Oh well, a beer is 6 bucks a pint at the neighbourhood and we’re not going…so whatever”. Vegetables? I wanted some fresh bell peppers the other day so just bought them. Gas prices? “Oh well, our car is still cheap to fill”. It feels a little like giving up. Sometimes I say, “Life is short”….(because it is). The only things we do control is what our greenhouses produce, the amount we drive, heating costs, etc. But what if you have no control or excess cash, which is the situation for most?

News update for the WS community. Warning, off topic.

We have a forest fire going about 1 km from my house…maybe less as the crow flies. Some brain dead tenant decided to clear a little brush on his landlord’s property on a plus 30C day, with wind. He lit a brush fire. Then the winds started up. I have friends in the helicopter business so am presently getting the numbers of cost per hour to fight the blaze. There are 4 rotary on right now, rumoured to go to 7. There is also a 30 man crew, some fallers, and some heavy equipment trying to contain it. I live on the river they are bucketing from. They’re using a section just up from my son’s place to dip their buckets and it’s about a two minute turn for one complete dip/drop/dip. They are stopping just for fueling up. The renter lit the fire, but most likely the landlord will be financially responsible for it. This year a property owner in the interior was just assessed a bill for 750K for a fire he accidentally lit 2 years ago…and that was down from the original 950K original assessed fine.

We are okay at our house but I do have a high pressure water pump and 300′ of hose, just in case the wind switches. And this is May….not August.

Paulo,

I hope everyone will get through this sound and safe, and that your property will be spared. All the best!

Hey Paulo

I am south of you in sequim across the strait. Keeping fingers crossed for you. As I look out right now at the gorgeous vista of hurricane ridge and your island across the water. Everyday now my stomach clenched of the thought and fear of the coming smoke choked air in August of the last two years. We were housebound shut ins for almost two weeks last summer

I have my top tier particulate mask at the ready. I got it for my trip to China for their polluted air. Didn’t need it. But odds are most sadly I will for the coming summer of forest hell fires

God speed

I hope it’s contained soon and little is lost, Paulo! I hope everyone comes through OK!

Indeed, it’s only May and it’s hot as hell where I am. In fact I need to go get on the train up to Palo Alto to North Face for some of those “convertible” pants, see, the problem is, on Sundays I go to services at the local temple, but you’re not supposed to wear shorts, really. I mean, I’d hear some tutting behind my back… but I go everywhere by bike. So the idea is, to get some decent looking “convertible” pants, wear ’em to service, then afterward unzip the legs so I’m wearing shorts. My “winter” cotton Dickies are awful to wear in this weather.

I wish I had access to medical care …. I have a “smoker’s cough” I blame the abysmal air quality here for, but I notice not everyone’s hacking away, and would like to get it checked. Have actually been looking at how to do a sputum TB test myself; I’ve got a microscope or three and just need to know what stain to use.

The dollar deflates and so do short rates. The fed. will get their negative rates without appearing to do so as the dollar and the fed battle, and inflation persists until it can’t anymore.

Get the appetizers for the show; fed would rather you spend more money than a bag of popcorn would cost.

On second thought, just bring your own stuff in, it’s a hell of a lot cheaper. Deflate for yourself, no one else will do it.

Many companies, individuals and governments will not be able to pay their bills if rates move up over 4%, so it won’t for a while.

However, when the Fed. starts buying the short term bonds, and longer term ones are left to other private and public entities to purchase, the shenanigans at the fed could really turn-up; they cannot let the long end get away from them.

It’s true, the dollar is weakening slightly around the world. Perhaps foretelling what is to come….

Maybe I missed it but why is this list different from the report BLS publishes for All-Urban consumers, https://www.bls.gov/news.release/cpi.t02.htm, which shows a 10.7% increase in health insurance?

If multiplied by the “relative importance” does this mean the contribution of medical insurance premiums to the change in CPI is +12.1%?

That’s correct. Health insurance weighs 13% in the CPI for healthcare index and about 1.1% in overall CPI.

But telephone hardware and other consumer information products dropped 14%, TVs dropped 19%, video and audio products dropped 9%, dishes and flatware dropped 11%… when you look at individual items, you end up getting whiplash :-]

Wolf,

I might be missing something here. I’m not a retiree, but my parents pay an arm and a leg for supplemental health insurance. What’s the point of releasing an aggregate CPI number that weights health insurance at 1.1%, when healthcare is the single largest expense for our retirees?

Ididsa,

1. Health insurance is 13% of total health care cost – don’t conflate the two.

2. What’s the point of looking at ANY aggregate national numbers – since by definition, they never apply to you or your parents?

Our healthcare expenses are low and haven’t risen hardly at all. National averages balance out what your parents pay and what everyone else across the nation pays, from 18-year old to 80-year old. If you’re only interested in what your parents pay, look at their bills. If you’re interested in what we pay, well, you can’t look at our bills, but you can look at aggregate numbers for everyone in the US.

In estimating the price of “health insurance,” BLS attempts to measure just the cost of running an insurance operation (including insurance company profit). The actual cost of providing the services that the insurance pays for aren’t included in the BLS cost of insurance, but rather in the separate sub-indexes for professional services, hospital services, nursing homes, and home care of invalids. They explain this at

https://www.bls.gov/cpi/factsheets/medical-care.htm#A2

So of course the increase in what we pay the “insurance” company can be a lot different than what BLS recognizes. For the year ending April 2019, BLS estimates that the price of insurance, as defined above, increased 10.7%, which happens to be a lot more than any of the other medical costs they cover.

My wife and I paid $10K this year for Medicare, supplemental, and part D. That has increase from$7K 3 years ago. It is by far the largest single cost we have. It dwarfs food, utilities, auto insurance, and property tax. The only thing close is Federal Taxes which is in the same ballpark. The $10K insurance is about 40% of our total yearly expenses. And that doesn’t include copays for prescriptions. If we had a house payment it would be a smaller percentage of our expenses.

Like I said in an earlier post, there is no relationship between the CPI and reality. It is an indicator designed to reduce increases in the costs of government payments.

Old Engiineer,

Your reality is a million miles away from my reality. As engineer, you should know that CPI is not a reflection or your or my reality but averages out everyone’s reality.

@OldEngineer

My parents are paying 25% of their fixed income directly into insurance premiums. Not actual medical care, not prescriptions, not doctor visits, but in medical premiums for supplemental insurance. And these costs are going up 10-15% a year.

20% of the US population is 65 and presumably near or at retirement.

https://www.census.gov/newsroom/facts-for-features/2017/cb17-ff08.html

I am a statistician and work in quantitative analysis.

The statistic (which may be correct in aggregate, i honesty don’t know much about it)…. a statistic that has very very important social ramifications relative financial policy, becomes the problem. Especially when it impacts our marginalized populations like it is doing.

Politics and monetary policy inevitably gets involved in the discussion, and the statistic is not thrown out.

So my parents are at the tail end of the statistic chart and the aggregate does not adequately reflect their situation. So be it.

Perhaps the problem is with the medical system. That’s a completely different topic that we will be hearing much about over the next year and a half……

Wolf, is the elevation of the minimum wage in San Francisco a factor in cost-of-living rise in the city? Or is that factor hard to gauge because your stats are for SF-Oakland-Hayward (and minimum wages in Oakland, for example are around two dollars less than in SF)? Just curious. I support higher minimum wages, especially for anyone living out here, but I understand those increases will be passed on to consumers.

arcadia,

“…is the elevation of the minimum wage in San Francisco a factor in cost-of-living rise in the city?”

It’s the other way around. You couldn’t hire anyone for the national or the CA minimum wage anyway. No one is willing to work for these wages here. If you commute from far away (where it’s cheaper to live) and pay gas, bridge toll, etc., 1/3 of your paycheck would already be gone. Restaurants in SF have for years paid way above national min wage and even CA min wage, even for basic jobs.

$15 an hour minimum wage didn’t change much in SF. That was already near the market rate for hiring basic labor, and even then, it’s very difficult to find workers. This is one of the biggest complains of doing business in SF: you cannot find good workers at wages that the businesses can live with because SF is too expensive for these people at these wages, and they either leave, or they look for better paying jobs in SF, and you lose that employee, and you have to pay more to fill that slot.

So the cause and effect relationship is the other way around: the cost of living has pushed up market wages in SF because businesses have to staff their operations, and people refuse to work for wages that they cannot live with.

What has happened is that a lot of retail shops and small restaurants have closed over the past five years or so because landlords got too greedy when the 10-year lease was up — landlords doubled or more than doubled the rent from where it was 10 years earlier when the original lease was signed. This, combined with the high local wages for all jobs, along with the switch to online retailing, is killing the small merchants in SF. And so you see a ton of closed shops in SF. They’re everywhere. That has been a problem for years, that’s only getting worse.

High costs of living are a real economic problem for low-margin low-volume businesses.

https://sf.eater.com/2019/5/10/18566178/avedanos-meats-butcher-closing-bernal-heights-san-francisco

This is a great example of a local woman owend buiness who can no longer afford to keep it going.

“According to Wilson, the fact that she has a new landlord with plans for massive construction and renovation isn’t the real problem, though that project would effectively end their access to a kitchen for the foreseeable future.”

Hmmm…

I understand that the officially released inflation data must be muted, because further tightening would bury the economy. I understand the reflexivity aspect of inflation whereby if people don’t expect inflation to rise it will not rise as rapidly. The Fed has publicly acknowledged its firm belief in this concept. So keep the masses in the dark.

So I understand the motives behind the muted officially released inflation data. Assuming Dr Lacy Hunt is right (which he is), this doesn’t bode well for our purchasing power in the future. Not only have the central banks inflated financial assets, but there’s true stealth inflation in consumer goods and services. The American people, by and large, have been fooled. The 2.5% long term yields are actually already negative in many areas of the country. And when it comes to financial assets like real estate and equities our purchasing power is eroding on all fronts….

My tally (California)

Health insurance premiums up 10% and 15% last 2 yrs

Car insurance up 10% this year, just got the statement

Gasoline off the scale

Food up 8% yoy

As one comment stated above, the Fed lives in an imaginary world. The Administration Is all too willing to let them remain there. According to our Administration, rates need to be slashed ASAP as there’s very little inflation.

Ididsa,

In terms of insurance, you might want to switch to Kaiser. We’ve been with them for years now, and premiums barely went up. If you’re with Anthem (the worst), it’s your own fault. They doubled our premiums over a two-year span in 2007-2008. They’re just gangsters.

The average price of gasoline in California is just above $4. The first time the average price was above $4 in CA was in 2008 and went as high as $4.63 in 2008. Gasoline is cheaper today than it was 11 years ago. This is where this anecdotal cherry-picked stuff completely falls apart. That’s why you need to look at aggregate numbers and longer term to get away from these extrapolations that lead you to crazy results.

Cigna is the culprit here……No doubling, but like i said 10-15% a year. On a multi-hundred dollar policy and their fixed income, that’s a lot of money for them…..

They don’t want to go with an HMO (Keiser). They have primary doctors that they’ve become attached to. They won’t budge. I can have them go to the PCP to get the referral but they are elderly and don’t want to deal with change…..

Wolf,

I have Kaiser through Covered California but the premiums are within dollars of what Anthem offers for identical plans. I’d be happy to send you screenshots of the two options with similar costs. No matter the plan, the prices are outrageous! Also, this year my Kaiser premiums under Covered CA went up 15.7% for me and 23.6% for my son. (The total amount went from $746 to $879 per month, and I have to meet a $6,000 deductibe per person before a cent is covered. I do get one free physical a year – I call that my $16,000 check up.) I have looked into other options outside of Covered CA, but they all have lifetime caps, and I don’t want to take that risk.

When you advise people to “just go with Kaiser”, you give the impression that there’s an affordable option to get around the inflated prices. If you want a full-featured plan with no lifetime caps, you have to pay a lot. Also, Kaiser has many different plans, so it’s not really appropriate to refer to Kaiser insurance as one option.

The situation with healthcare has gotten to a state for me that I’m considering a move to Europe at some point. I’m fortunate that my son and I have “EU” (Irish) passports, but I know most of my fellow Americans do not have the option to make this move.

If you don’t have chronic illnesses, and if you’re in a high-income tax bracket, get a high-deductible plan (our max out-of-pocket per year is $4,500 each if I recall, or about $9,000 for both of us), plus an HSA that you max out. Contributions to the HSA are deductible from federal taxes, which saves about $2,000+ a year. Premiums for a high-deductible plan might save another $6,000+ a year, total savings $8,000 a year. If you get sick in a big way once every four years you save $24,000 in three years when you’re not sick, and pay the big deductible out of your fat HSA the fourth year. During that fourth year when you hit the max out of pocket, you then do all the elective stuff you’ve meant to do for years (cataract surgery, etc.), because it’s free.

This doesn’t work for everyone. But it works like a charm for us. We have that with Kaiser. And if the 2 ifs in the first sentence apply to you, it’s a deal.

Since my deductible is higher than yours, I think it’s safe to say that I do have a high-deductible plan. (Note, I’m not getting my insurance through an employer.) I’m assuming that you’re not going through Covered CA. And I suspect that you have a lifetime cap on yours – that’s unacceptable to me as I don’t want to go bankrupt if the “god forbid” happens to me. If you’re getting such a better deal than I, I suspect that there’s some catch.

You say you can use an HSA if you “get sick in a big way” once every several years. I have several issues with that:

1. The HSA account is funded with your hard-earned money. It “saves” you $2,000 but it still costs you money. (I currently spend 0 on an HSA).

2. Healthcare costs are so inflated that you don’t need to get sick in a big way to rack up high-priced bills. My teenage son has had various sports-related injuries, and the bills easily total over $2,000 if an ER visit is involved.

3. You probably take great care of your health, but what happens if you get in a bad car accident or you get unlucky with cancer? And what if the car accident happens at the end of December, forcing you to meet 2 yearly deductibles within days? You may find that your 24K will not go far. If you have a really high income, I guess this could work out, but the person with a modest income may face bankruptcy.

I don’t mean to be rude, but I find your cavalier attitude about healthcare expenses to be a bit off-putting. (I would never use the words “charm” and “healthcare insurance” in the same sentence.) This has been a big issue in this country for many people for quite some time, and apparently, it will be one of the top issues during the 2020 election.

One last point. You had this exchange with Ididsa:

What’s the point of releasing an aggregate CPI number… when healthcare is the single largest expense for our retirees? [The person got the details wrong, but the gist was that healthcare is expensive for some and weighs heavily on them.]

Part of your response:

National averages balance out what your parents pay and what everyone else across the nation pays, from 18-year old to 80-year old.

It’s interesting you respond this way because you’ve had a different response with respect to housing which, like healthcare, affects people unevenly. When people talk about national housing affordability, I believe your usual response is something like “it’s local”, you can’t compare, and it makes no sense to talk about averages. Why is it different with healthcare? Granted, the differences are not necessarily limited to a region; they instead vary widely from person to person depending on employment, income level, age. etc..

In summary, I’m trying to convey that if healthcare costs are not manageable for ALL US citizens, then we don’t have a proper system in place.

RoseN,

I’m not minimizing the issue of health care costs in this country. It’s a HUGE issue. What I AM saying that you cannot extrapolate from your personal experience to the nation overall. I’m using my personal situation to show that not everyone is in the same boat, and that national averages have to include everyone.

Some more thoughts:

1. Insurance gets more expensive as you get older and need more health care. This is unrelated to inflation. That’s how insurance works. As you get older, your premiums rise. This has nothing to do with inflation, but with how insurance companies price risk. If your turn 50, your insurance premium jumps because your insurer knows that statistically speaking someone over 50 is going to spend more on health care going forward. Then there’s 55, 60, etc.

For example, I’m looking at a price sheet here. Kaiser HSA for people under 30: $395 a month. Same Kaiser HSA for people 65+ $1,246 a month. This goes in 5-year increments. So on this price sheet, whether you pay $395 a month or $1,246 a month has zero to do with inflation, and 100% to do with your AGE.

So when you hit that age threshold, your premium jumps by a lot: For example, on this price sheet, when you turn 60, your insurance premium jumps 22%, from $801 to $981 — and this has ZERO to do with inflation, though you may perceive it that way.

This article was about different inflation rates in different cities, and not about the issues of insurance and the pricing of risk.

2. An HSA is a way to save income that is NEVER taxed by the federal government. It’s like an IRA only better because distributions (if you follow the rules) are not taxed, unlike an IRA. You can save tax-free income until you need it. Also you can invest this money in stocks or bonds or CDs or whatever, just like an IRA. To call the contribution into an HSA an “expense” is wrong. It’s only an expense when you spend it. But you never pay income taxes on the income that you put into the HSA. That’s the big benefit.

If an HSA cuts your tax bill by $2,000 a year, over 10 years, that’s $20,000 plus the tax-free income that you earn on that $20,000.

The combo of HSA and high-deductible health insurance pans is a gift from the Bush era. It’s part of our unfair tax system. It’s unfair because only people with relatively high incomes and good health can benefit from it in a big way. But just because it’s unfair doesn’t mean you cannot try to benefit from it.

@Rose

I am glad we are not the only one. 899.00 a month here. It is completely crazy

The hikes were as follows for Cigna (this does not include dental or vision supplemental)

2 years ago

720.00

800.00 last year

899.00 this year

So 11.1 % hike 2 years ago, and 12.38% hike last year….. They have not hit any major new age milestones although they are getting older :(

Kaiser option, which has much less favorable deductible, out of pocket max, copays, Rx coverage, and a lifetime cap, etc will save us around 89.00 a month. It is an HMO and the parents won’t go for that either…. The savings of 89.00 is simply not worth the risk and trade off in coverage. As yoiu said we need lifetime unlimited for any outlier situation.

@ Ididsa

Yes, my premiums also went up by double digits for two years in a row, suggesting the increase (at least one of the times) was not due to moving to a new five-year increment. Moreover, my 15-year-old son’s premium increased 23.6% in one year. Does a 15-year-old really incur that much more medical expense than a 14-year-old? Also, news stories on increases for Covered CA also matched what I experienced.

@RoseN

“One last point. You had this exchange with Ididsa:

What’s the point of releasing an aggregate CPI number… when healthcare is the single largest expense for our retirees? [The person got the details wrong, but the gist was that healthcare is expensive for some and weighs heavily on them.]”

Yes, I conflated two different items. Here’s my follow up response that I posted above. Statistics should always be applied in their proper context.

Here’s my post from above. Hope this clarifies the point I had originally intended to make. This emanates out of frustration with a 2% aggregate inflation statistic

===========

@OldEngineer

My parents are paying 25% of their fixed income directly into insurance premiums. Not actual medical care, not prescriptions, not doctor visits, but in medical premiums for supplemental insurance. And these costs are going up 10-15% a year.

20% of the US population is 65 and presumably near or at retirement.

https://www.census.gov/newsroom/facts-for-features/2017/cb17-ff08.html

I am a statistician and work in quantitative analysis.

The statistic (which may be correct in aggregate, i honesty don’t know much about it)…. a statistic that has very very important social ramifications relative financial policy, becomes the problem. Especially when it impacts our marginalized populations like it is doing.

Politics and monetary policy inevitably gets involved in the discussion, and the statistic is not thrown out.

So my parents are at the tail end of the statistic chart and the aggregate does not adequately reflect their situation. So be it.

Perhaps the problem is with the medical system. That’s a completely different topic that we will be hearing much about over the next year and a half……

I definitely prefer Kaiser to Anthem, but my experience with their premiums has not been so lucky, Wolf.

I offer Kaiser for all the employees of my small company. All employees are mid 20s – late 30s and all very healthy. I am in my late 30s. We’ve got 3 employees plus my spouse and child covered with Kaiser.

None of the employees or I see the doctor more than once a year.

Premiums went up 6.8% this year. Last year they went up about the same. If there were another option, I would consider it for my company, but I hated being with Anthem years ago.

So we just have to bend over…

American healthcare spending is on average DOUBLE compared to any other OECD country.

Indeed, breaking news from yesterday, US pharmaceuticals have been price fixing for years.

Case in point… a month supply of insulin in the US Costs 30 times more than Canada. American voters are chumps. ….and many are dying or going bankrupt needlessly.

Thanks for this, Wolf. It’s very enlightening.

When I taught business courses, I had students calculate their personal CPI to demonstrate that the national estimate didn’t necessarily apply to everyone. It also showed them which expenses they most needed to watch or trim.

I myself have been subject to Los Angeles’s 3.1% price creep. Eating out used to be affordable here. Twenty years ago, you could get a decent $8 meal and $6 glass of wine. (My cooking skills are limited to barbequing and boiling pasta, so I eat out often.) Nowadays, a tasty entree hovers around $18 and a drinkable pinot is $12. The customary tip is now 20% instead of the longstanding 15%. (When did we vote on this?)

I’m also subject to a kind of self-induced inflation. Disposable Bic razors met my needs for decades but I now feel compelled to buy the trendy Harry’s. (Truth be told, the shave is much better.) I used to spend $6 for a package of ten sock pairs at Kmart, yet just last month shelled out $60 for four sets of Bombas. (Never again. Socks is socks.) And that $2 jar of Prego has been replaced with $6 container of imported marinara made from hand-petted organic red plum tomatoes. Yes, I am in a much more secure financial position after decades of hard work, but I’m also ripe for parody.

Richard Bach (best known for Jonathon Livingston Seagull) had another book, Illusions, which contains one of my favorite lines: “Argue for your limitations, and they are yours.” If you just don’t want to cook and would rather spend the money eating out, fair play to you. But cooking isn’t difficult at all. There are plenty of easy-to-follow recipes on the net in any cuisine you care to name. Sure, some are really hard and tricky — don’t do those (unless you want a challenge!). You’ll save a fortune on wine, too.

My mother worked and had three hungry boys to feed. Dinner was usually casserole of some sort. I didn’t learn anything about cooking from Mom. After I left home I started to cook out of necessity. With the internet available these days that would have been so much easier!

The biggest fear most people have about cooking is that they are going to screw it up. So what? Unless you salt something to oblivion or burn it to a crisp it will still probably be edible. Just ask yourself after you make a dish, if I make this again how can I improve it (meaning more to your taste)? That will take you a long way. If it is inedible? Chalk it up to experience and go out for the evening. It cost you a little time and usually only a few dollars worth of ingredients. You’ll do better next time.

And I used to think socks were socks, too. Try wool socks. Any decent brand will do, doesn’t need to be some fancy shmancy one. They keep your feet warm in winter and dry in summer where cotton ones get wet and sticky (in Florida, anyway!). Just a thought.

Thanks for the encouragement, bemused. I’m familiar with Bach’s work, and while I appreciate his sentiment, he really is preaching “magical thinking.” (No matter how positive my mindset, I am never going to be able to dunk a basketball.) I’ve also tried cooking for friends a few times. Their honest reaction? “It’s best to focus on your strengths.” :)

Well, the overall book Illusions did, and you are certainly correct that there are many things that just are not possible no matter what your mindset. I couldn’t dunk a basketball, either! You need to make a judgement call — is this something that is impossible for me do to, or is there a reasonable chance that I’ve just convinced myself that I can’t.

In all cases don’t go out expecting to hit a home run the first time at bat. In the case of cooking, I would cook for myself (and partner if desired on both sides!) knowing I probably won’t get it right the first time. And that’s okay. Watch some cooking shows or youtube videos to see what the presenter does. The first time I make a new recipe I try to follow it exactly. Nothing sillier than reading comments about how somebody didn’t like a recipe — but swapped this for that, left this out, and added something else! Measure things carefully so you really are following it. If you mostly liked the dish but there were a few things off, then tweak it to see if you like it better. I like making Prudhome’s Chicken and Tasso Jumbalaya. He calls for 2 tsp cayenne. After making it for a while I decided that it was just too darned hot for my taste (and I like hot food) so cut it back to 1 tsp. That sort of thing. Only once you feel you really have a dish down invite others to try it. Otherwise you are just setting yourself up for negative feedback. Also, ask for constructive criticism. When I make something new I’ll usually ask my wife “how could this be better?” A much better question than “do you like it?”!

The most important thing is just to get out there and try something. And I can’t stress enough, failing is OKAY. You’ll have enough successes that you can chalk up the failure to either a bad recipe (it certainly happens!) or just one that isn’t to your taste. A restaurant or takeout is always there as a backstop if that happens. Usually, though, if you think you made it right but just don’t care much for the end result you wind up with “its okay, but I wouldn’t make it again.” Lesson learned (and money saved regardless).

When you do get one just right you’ll have the satisfaction of knowing you did it — and that you saved a bunch doing it. The only problem is that when I go out to eat, quite often I think — I could have done this better myself for a fraction of the price.

Just wanted to add…. Start small. You can boil pasta. There are so many pasta dishes out there. Try making your own spaghetti sauce. Its really easy. Or pesto. Carbonara. Once you gain confidence start branching out. My thoughts, anyway. Good luck.

Some folks surveyed the relative cost of eating the same meal, prepared at home vs in a restaurant, for about 100 dishes iirc. The average saving was around 80%. I’ll see if I can find that if only as a memory check.

Since we seem to be comparing lifestyles/processes……..One of the best assets I’ve inherited from both mother and father is/was the ability to cook. At the age of around 14 I was responsible for starting dinner for all….after school studies/music being taken care of. We (children’s mother and I) raised 7 healthy children whom ALL know how to cook and love it. Too many individuals/families waste so much money on eating out it is stupendous and pathetic. I was born and raised in SF where there was a first class restaurant and first class bakery all over the city. We also were fortunate because we were in a small grower/wholesale produce business. So even today if our family makes a salad it’s a SALAD and can be made a meal of. The only segment of the population I can sympathize with is the “food deficient” parts of living areas with no decent retail food stores. (Spent more than 30 years in that part of the economy). Americans are “eating themselves to death” at fast food outlets and even some of our so-called good restaurants.

As far as some of the other comments on healthcare and living expenses I’ve been fortunate to have decent health into my late 80’s (having survived prostate cancer 10 years ago); have a decent modest organized labor health insurance coverage that costs me between medicare and the labor coverage around $200 month. Have had Kaiser for more than 20 years and will stick with them until the end. My life in the Sierra foothills is simplicity; modest living quarters still paying modest mortgage; hardly ever eat out unless a friend wants to; driving around 10,000 or less miles in a 13 year old vehicle; enjoy nature.

I’ll close with what I quote often:

“In America, if you are healthy you are already rich”.

IMHO, an issue with TIP’s is that the government controls the calculation of inflation. Interested in other opinions on this topic. Thanks

The U.S. government has created over 4 trillion in new debt since the Great Recession adding to an already staggering National Deficit. They’ve done this to create Inflation at barely 3% today if those numbers are real at all. I don’t believe they are. Everything is manipulated to make it seem better than what it really is. The same with the “official” unemployment rate which includes guesses for the death-birth adjustment & doesn’t take into consideration how many able-bodied people have stop looking for work. Or the fact that many able-bodied can only find part time work.

Consider Trump’s latest raise of Trade Tarrifs. That’s an added tax for all Americans. One would think this will increase Inflation because the cost of goods and services will be much more expensive. This is true but global economic weakness is gaining steam and the demand for exports is declining. Ultimately this will decrease demand, the economy slides into Recession & a massive Deflationary environment ensues (a la 2009). People curtail buying & live on less, assest valuations crater & the spiral continues.

“Tariffs impact domestic consumers more than then impact to China. If tariffs impact China they stimulate their economy with massive credit injections just as we have seen them do recently. The U.S. doesn’t have that luxury currently which is why both President Trump and Vice-President Mike Pence have discussed the need to drop rates by 1% now while the economy is still expanding”.

Lance Roberts – Real Investment Report 05-10-2019 “Game of Thrones – Winter is Coming

So with Inflation in the sweet spot & the economy strong, why are they hinting at the need for further QE? Sharp declines occur due to an unexpected event. Unexpected to many except them.

What eats my lunch is the grocery store (pun intended) . Try to live with the majority of your income SS which started 12-15 years ago, which was about half what it is now and with the way they calculate it. I am getting less than I started with. I use a cash back card for groceries only to keep track. The groceries have doubled, the check goes down. With congestive heart failure I am unable to work now. I worked part time in the early years. I have to put some aside for property tax and car ins. It is busting my butt. I had to drop homeowners ins. years ago and have been doing my own maintenance. I need to do roof work now but don’t know if I will be able. I have a disabled son 49 yrs. old with no income that I have to take care of also. Anybody want to trade places?

Well, I’m in the camp of there not being inflation. What we think of inflation is really monopoly profit, from 30 years of antitrust failure, as well as a generational/international savings glut chasing yield via asset appreciation. But the inflation bogeyman is really good at keeping wages down.

The monopoly profits come from the assets that they own, The same inflated assets that the masses require to survive, like gas, electric rent/mortgage, insurance, banking, food and transportation.

….forgot heating, defense, education and transportation. I’m sure their are other requirements or needs according to individual situations and locations

Warren Buffett agrees with you! Warren has told us the max sustainable level of corp profits is 6% of GDP. It has been dropping for a whole but still at around 10%.

The squeeze on the middle class has been on for 30 years. Eventually, as noted by Ray Dalio and others, this will likely translate into political action. Let’s hope the pendulum doesn’t swing too far.

I believe CPI is misinterpreted. It’s a price index. Many things effect price. Inflation, supply and demand imbalances, productivity, a passing fad. So lets imagine all these factors placed in 2 groups: Inflation and Other. The CPI at 2% would be the overall average. Inflation could be the one that’s over the average. That would make Other below average. If Inflation and Other were equally weighted then Inflation could be at 7% and Other would be at -3%. So we would be living in a high inflation deflationary environment. Hhmm, I wonder which category wages and salaries follow.

Standard Political Fare: Scr** People

http://market-ticker.org/akcs-www?singlepost=3473963

Now the government just lies about inflation; for example, between goods and services Medical is allegedly 8.7% of the CPI while in fact medical is almost exactly 20% of the economy as a whole. This has been creeping up over the last few years but still understates reality by more than half!

The fraud called “Owner’s Equivalent Rent” remains; what you actually buy in a house is not “owner’s equivalent rent” but rather an actual house with an actual price. Actually counting house prices, on the other hand, would result in a MUCH higher inflation number.

@Winston

Regarding medical “inflation” costs, it is even worse for our elderly. Anecdotally, my parents are forking over 25% of their fixed income for supplemental policy coverage alone. And i have heard some elderly as high as 40% (i am assuming with much lower overall income)

Yet these marginalized populations fall outside the “norm” or average which the CPI gives us. Yet major financial, social (and political) policy decisions are based upon these aggregate statistics. I guess this is the best they can do ;) but it’s sure helpful in inflating financial asset prices…..

I really believe if you shop around and do your homework your nflation is muted but I live in rural America where I raise a lot of my own food and know people who work for a reasonable wage. The dollar has been strong for quite a while. At some point in time it will get weak and then inflation will wrack the country. But here again just look ahead and stock up on things that will protect you. And for goodness sakes get out of big cities and high tax states. I can’t stand whining.