February was bad. Housing market weakness is now spreading out from London.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

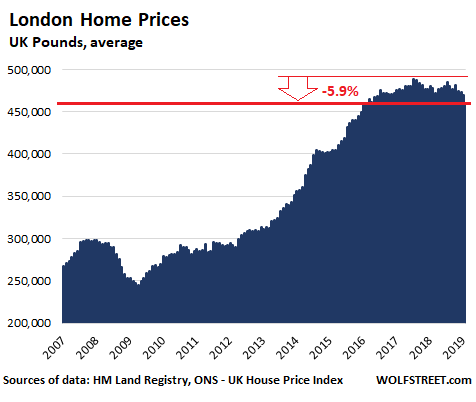

London home prices in February took their biggest one-off hit since the dark days of the last crisis, according to data published Thursday by the UK’s Office of National Statistics. The average price of a residential property in London tumbled 2% in February from January, the sharpest monthly drop since November 2008, when the City was grappling with the fallout from the Lehman Brothers bankruptcy. For the 12-month period, the average price dropped 3.8%, the sharpest year-over-year fall since August 2009, during the Global Financial Crisis. The average home in London is now worth £459,800 ($600,000), down 5.9% from the peak in July 2017:

But it’s still more than double the median UK home price (£225,000). In other words, while prices may have moderated somewhat they’re still well beyond the reach of average Londoners. Here are some more standouts from the ONS report:

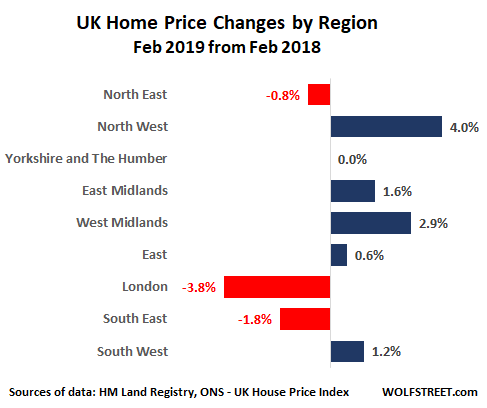

The slowdown is spreading out from London. Home prices in the south east of England recorded an annual decline (-1.8%) for the first time since 2011. Prices also fell in the North East and remained virtually unchanged in Yorkshire and the Humber.

Home price annual growth is slowing in England; prices tick down in Scotland. Home price growth has been gradually slowing ever since the summer of 2016, when a majority of British voters voted to leave the EU. Over the year to February 2019 the average home price in England rose by just 0.4% , down from 1.4% in January 2019. In Scotland prices slipped by 0.2%, down from a year-on-year rise of 2.4% in the previous month.

In the UK as a whole, the average home price increased by just 0.6% from a year earlier. It’s the slowest rate of growth since late 2012.

Prices did increase in a few places. Home price growth was strongest in Wales and the North West, increasing in both regions by 4.1% in the year to February 2019.

It’s a very different story in the capital, which during the first decade and a half of this century enjoyed much faster home price growth than the rest of the country but which is now suffering a much sharper slowdown. The most exclusive boroughs of the city center — often referred to as Prime Central London — have been hit hardest, with prices falling an estimated 14% from their 2014 peak.

“The London sales market is in a prolonged downturn and the current uncertainty surrounding Brexit is clearly impacting consumer confidence,” Foxtons, one of London’s largest real estate agencies, said in its latest annual report. “We do not expect market conditions to improve significantly until the political and economic landscape becomes clearer.”

There’s little sign of that happening any time soon. If anything, there is more uncertainty today surrounding the UK’s political and economic future than there was in February, before Brussels decided to grant the UK government and parliament an extra seven-month “Brextension” to try to get their house in order and finally pass Theresa May’s wretched withdrawal agreement.

Just about the only thing that is clear today is that the political, business and financial establishment on both sides of the English Channel will do virtually whatever it takes to avoid a no-deal Brexit. But that doesn’t mean a no-deal Brexit can’t and won’t happen. It is, after all, the default option. And given the chaos and division gripping Westminster, the intractability of the Irish conundrum and the persistent support for Brexit across vast swathes of England and Wales, it’s certainly still within the realms of possibility.

It’s not just the rampant uncertainty that’s causing London home prices to fall. There are also the recent hikes in stamp duty and other property taxes that were intended to dampen demand among non-resident buyers and investors in a market that had long gone haywire. And they seem to be working.

There’s also the yawning housing affordability gap. Despite the fact that London residential property prices have become less expensive over in the last two years, prices are still not nearly low enough to fall within the grasp of most first-time buyers. In London, the housing affordability ratio — what you get if you divide the median price paid for residential property in a given area to the median workplace-based gross annual earnings for full-time workers — can range from 9.8, which is already pretty elevated, to over 40 depending on the neighborhood.

In 2018, eight of the ten least affordable local authorities in England and Wales were in London, with the remaining two being in the surrounding South East region. Most London boroughs are in the 10-20 range (based on ONS data). In the least affordable local authority in London and the UK, Kensington and Chelsea, median home prices are 44.5 times workplace-based median annual earnings. In some parts of the UK such as the North West they can run as low as 2.5 times median annual earnings.

Andrew Goodwin, associate director at Oxford Economics, sees this huge disconnect between home prices and earnings in London as the prime cause of the recent downturn. He also believes that prices are likely to stay in a rut for some time to come, especially given the current low level of transactions. According to LonRes, transactions slumped by 9% between 2017-2018 for London properties under £1 million, by 25% for properties between £1 million and £2 million and by 12% for properties between £2 million and £5 million.

As the affordability crisis in the capital spurs Londoners to relocate in droves to other parts of the country or put off buying a home altogether, and as high net worth individuals and companies continue to spurn London real estate, at least until a decision is finally made regarding Brexit, the future of one of the world’s prime real estate markets remains very much in the balance. By Don Quijones.

Despite “the lowest interest rates in more than a year.” Read… House Prices in 12 of California’s Most Expensive Coastal Counties Fell in March from a Year Ago. Here are the Charts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Excellent article!

Damn you Brexit!!!!!!!!!!

Brexit – leaving the UK for Brussels and Strasbourg… or just leaving the UK. I knew there was a reason they allowed the referendum, in that it gives policy makers a ticket out from the mess they have created. I wonder how much longer they can direct from the continent, probably want to save the country from there once it gets bad enough. That gives a lot of options, remainers are welcome to come and go freely as long as Britain remains in EU and they keep ties in Britain, leavers can leave the UK to EU because Britain is still in EU :-/ or just leave the UK and EU altogether , joiners from afar are encouraged to go to UK because they might not be able to later but most want UK to stay in EU as well because of it’s rights scene, the northern Irish get to stare at an imaginary border that keeps moving and that really pisses them off on all sides so they’d rather not , the Scots… the Scots get to independently consider and participate on whatever side while doing their own thing.

What an amazing level of coordination this all takes, they really can organise between themselves when they choose to after all.

The housing bubble weren’t Brexit though, unless it were meant so as to cause crisis along with Brexit, or is that “Brexit”?

At least Derbyshire conservative members have rejected EU elections, and I think a lot of people see those elections as a cheap farce.

“No deal Brexit is the default” – very true in that it satisfies all readings.

And the ramifications for the USA are?

Does everything have to be measured/reported in terms of ramifications for the USA?

We have a global economy. Housing prices in London are interesting in the academic sense, but I live in the USA and I’m curious how this may reflect on, for instance, housing prices in the USA.

You are not curious about how events in other countries affect the circumstances in your country?

London is a global mega city, like New York, Hong Kong, Vancouver ect… unless you’re a high net worth individual, prices in these cities probably is irrelevant to you.

It depends on why you think people are buying at the above prices – home, speculating or investing in anything because of high cash for example. At a global level hot money will just move elsewhere if the environment in one place is not good enough, so could act upwards on prices in the US. On the other hand you have possible financial contagion if prices drop far, that would lower appetite for the US also probably. Then there is a UK resulting economic slowdown from that, which would go mostly via EU to US. It is very hard to make out how everything is stringed together nowadays though, and sure others can think of more. You had me searching on what foreign investment is up to in UK recently so :

” Foreign investment in UK property has in the first three months of 2019 fallen to its lowest level since the first quarter of 2016, the three-month period before the country voted to leave the European Union, according to data provider Refinitiv.

Cross-border spending on UK property – residential, non-residential, other real estate, real estate management and development, Reits, hotels and lodgings – reached US$598.3 million in the March quarter, a tenth of the US$5.9 billion reported in the fourth quarter of 2018, and a fifth of US$3.3 billion reported in the first quarter last year…..

Since 2009, full-year foreign investment in UK real estate has amounted to at least US$6.4 billion. In 2016, after the Brexit vote, foreign spending tumbled by 65 per cent to US$7.7 billion from US$22 billion the previous year. Last year, foreign investment amounted to US$15.9 billion.” 4/2019 SCMP

“In prime central London, ‘super prime’ properties priced at the £10 million plus mark had only dropped by 0.1% and 0.2% between £2 million and £5 million homes. Properties priced between £1 million and £2 million fell by just 0.3%. The largest decrease affected the sub £1 million market with a year on year fall of 6.5%.” Yearly 2/2019 , knightfrank.

“North American buyers have already invested a reported £2.7bn into commercial property in the country so far this year, according to research from online commercial property tool Datscha.” 9/2018 buyassociation

More people will leave San Mateo to go and live in Putney.

These stats seem to not tell the whole story. I sold my flat in South Kensington in late 2013 for 2 million pounds. The buyer spent 200k on it and then it sold in 2018 for 1.6 million. That’s a much bigger drop than is being reported here.

The market in UK and especially London is very local and property type specific, so the above chart will be aggregate of London prices, but an example of a terraced property in Kensington gives over 15% decline in your timeframe at

https://www.home.co.uk/guides/house_prices_report.htm?location=kensington&startmonth=10&startyear=2013&endmonth=10&endyear=2018

for example.

just saying..some cities in canada is not going brexit,and have bigger loss……………..

This is the go to website for England and Wales:

https://documentcloud.adobe.com/link/track?uri=urn%3Aaaid%3Ascds%3AUS%3A114e75cd-6666-4112-b06f-ce6641895eb9

You’ll note that even the sacred prime central is now becoming unravelled. House prices in Kensington, Chelsea and Westminster are down 24% y o y.

Median and average prices can paper over regionalised outliers and where transactions volumes are small (such as in prime central), one big (possibly rigged) sale can shift the annual average outside of the trend.

I am wondering whether in the final stage of a downtown, no amount of externalities (hot chinese money aka Van and Toronto and Sydney and London – Russian, Kazak dosh) can turn the trend. Like a liquidity trap unable to spark economic recovery.

At some stage, when the perception takes hold and book profits start to get threatened, one sees actuall liquidations – sell at best! Have we reached this ooint?

The other key indicator is volume of sales which would need to flatline for a while before the next buildup and rally.

Tory philosophy like in Canada has been heavily aligned with rich landowners – you win, we win. Until this psychosis is ruptured, it will remain a depressing scenario of ever increasing Gini chasm.

No, not everything is about the USA, but trouble in the UK, combined with trouble in many more countries, can send shockwaves through the world, including the USA.

In my village/town in Yorkshire/NW prices have risen or remained high, and buyers have mostly tended to be London/SE buying holiday properties/investments.

It’ll be interesting to see what happens as negative equity kicks in and and property needs to be sold.

With huge stocks of new build houses in the Yorkshire and surrounding regions coming to market, and planning rules now stopping builders land squatting, I’m of the belief that this bubble is going to pop fairly swiftly once it hits the minds of the proles.

As I’ve noted before, Brexit is the patsy for the next financial turmoil in the UK.

The last crash was so burned into the mindset of the UK population, a new bogeyman was needed.

This time it’s the people’s fault! (not)

There are equitable solutions to these problems.

Unfortunately there are too many people, particularly those with wealth, power, and ambition, who do not want equitable solutions. Therefore there will be inequitable solutions, or none.

Also unfortunately, the best solutions are typically disliked by most people and are either not implemented or implemented poorly. People typically oppose compromise, even when it is in their best interest, and oppose them for unworthy and often despicable reasons.

There are many such problems, and several of them are so severe as to ultimately be fatal to societies and even to civilization. The dynamics of the worst problems, and the opposition to their solution, absolutely guarantee the worst possible outcome. The exits are blocked, and there is no way out.

The London property bubble should never have occurred. It should have been prevented, and could have. Same with Brexit. And so forth. It is a mistake to try to solve large complex problems by cutting the Gordian knot, because that creates worse problems. The knot must be untied.

Oh well.

It should be telling and instructive and not merely ironic to note that Easter, the greatest Christian holiday, is actually named for a pagan goddess. A metaphor for many things.

Fake Yellen Bucks and fake Draghi Euros have found their places to die.

No bazooka can save them.

So prices drop what…. 30-40% worst case scenario? …..prices are still up over a ten year period. Those cities will remain Safe havens.

Lol. Safety deposit in the sky? This time is different

The bubble should deflate and stay deflated, and follow honest market forces thereafter. That would be best. Some predatory speculators would lose their asses, sure, but they deserve it. No downside there.

Problem solved. Next.

London is in deep trouble. Add in the tremendous number of under – occupied offices which are going to be converted to flats and another 25% drop is on the cards.

Why, why, why?? With the technology to work remotely are they still building the darn fool things???

It’ll be interesting to see where the bottom is for London, NYC, and other major international cities with poor climates and geography. Remote work and automation will continue to drive smaller office foot prints and higher vacancy rates. Fewer workers needing housing and the continued addition of new housing units adds up to collapsing real estate prices.

With the technology to work remotely are they still building the darn fool things

Power and Control. They *want, and need* you to suffer that debilitating 90 minute daily commute to their glass mausoleums located in Traffic Hell, because it shows who’s the boss and because this takes away more of your time from you and they don’t even have to pay for that time, it is extra. To the power-people mindset: “Idle hands is the devils workshop”, people might get ideas, set up their own business and stuff, better keep them mentally exhausted.

Working for Ericsson, we had working at home for a couple of years — until the bosses found out that:

1) Most people could keep up with their entire workload using four hours in the morning …

2) This was because of Motivation and because people would skip the big-crowd meetings, where managers were informing people about mostly irrelevant things, and those idiot colleagues, easily gaining 4-6 hours of productive time per week.

So, then, this went away. With Ericsson it is better to be In Control than it is to Succeed (in my opinion, any decent product Ericsson ever did was a result of management failing to control their people).

I’m getting disappointed when I pull up Wolfstreet and find yet another article on up and down ticks of home prices in cities like London, Boston, San Francisco, etc. . Other than drawing the obvious conclusion–ordinary people can’t afford to get on the property ladder–what’s the point?

Do you only want articles on “up-ticks?” Is it disappointing that home prices are now falling in some of the markets that had the biggest housing bubbles? I understand that this might make for some uncomfortable reading. But housing is HUGE in terms of the amounts involved. So we cover it. And what happened in London in February is something we haven’t seen in a decade. So it’s not one of the everyday “up and down ticks.”

The point is that the decline of a major asset class in a city where world wealth flows is an indicator of global money problems rather than mere local issues……

Queens birthday today. She is 93. That is 5 complete Saros cycles.

London or Costa Rica?

Costa Rica or Nicaragua Emerald coast ?

Have coastal Costa Rica been impacted from California’s fallout? How do I find out if real estate prices have dropped or remains overpriced?

Cyclops

London (and the UK) is a massive market. If (when?) it rolls over big time it threatens the UK financial system – and just like Greece threatened to be Lehman on speed crack and steroids, the UK matters to everyone.

Cost Rica not so much.

BTW, North Sea oil production is crashing

https://oilprice.com/Energy/Energy-General/UK-North-Sea-Oil-Production-Set-To-Resume-Decline-In-2019.html

Part of the reason why the UK economy is going to collapse.

London housing is a important market not only for London itself but also for the rest of Britain. Possibly the only reason for higher (over?) priced property sales in the rest of B is the knock-on effect of London owners selling up and moving out. Since other places look cheap compared to London, the seller/buyer is in a strong position.

It is not so easy when selling and buying in places where the price differential is uneven. We are planning to move to another county and for the price of our 4 bed detached 3 rec double garage own drive etc we could get the sort of property that in our area we wouldn’t be interested in.

But ultimately the snag with housing market statistics and percentages is lumping together hundreds maybe thousands of transactions as if the property is an homogenous commodity. Most properties differ from one another, unless retaining original features and designed to look-alike. The house opposite ours for example is the same spec but the driveway is narrower and the back garden not south facing so ours would fetch a higher price. But if both houses were to be sold at the same time and lumped together without identifying the spec then it could look like opposite has fallen in value.

Of course, in Britain London is not the only property market and the majority of the population does not live there so probably doesn’t care a jot.

I see a return to the great depression era where bank failure meant credit collapsed and house prices fell from $$$ to cents.

The effects on the fragile supply chain would also make cities a risky place to be. History always repeats and the growing list of risks, combined with political ineptitude and a hostile populace is a bad mix.

The current generation are about to find out that property is not a pension and government promises can’t be kept. Prepare accordingly.