Despite “the lowest interest rates in more than a year.”

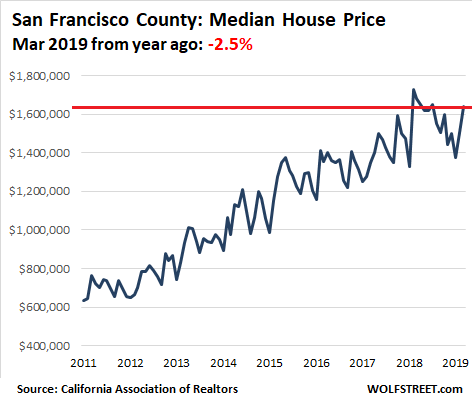

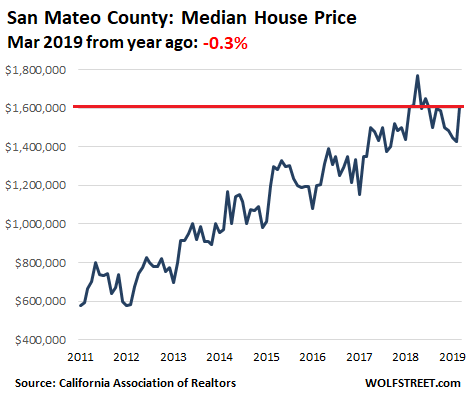

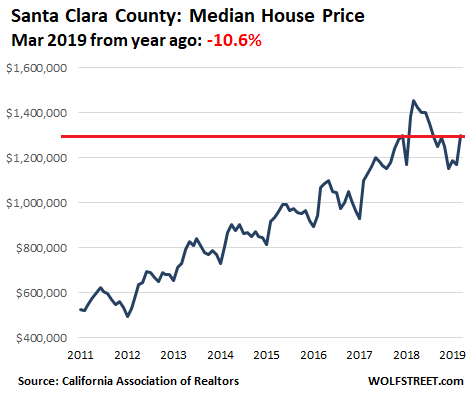

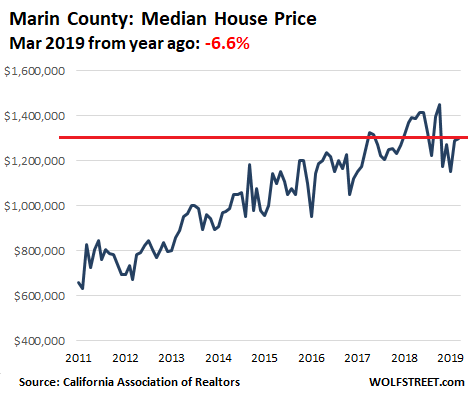

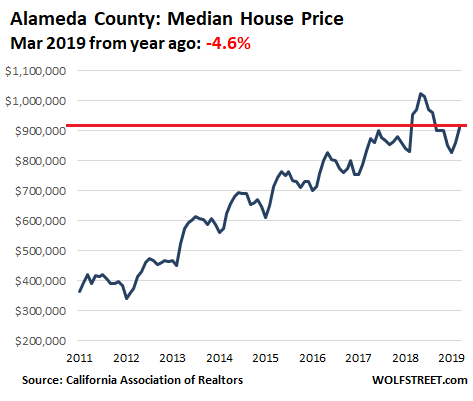

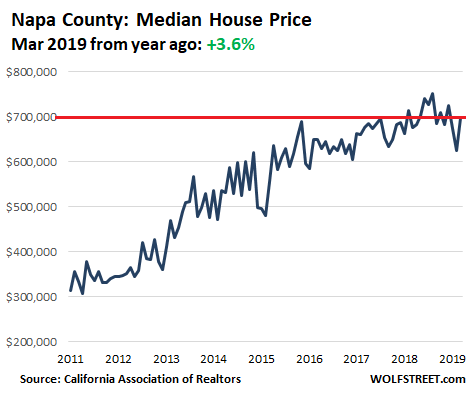

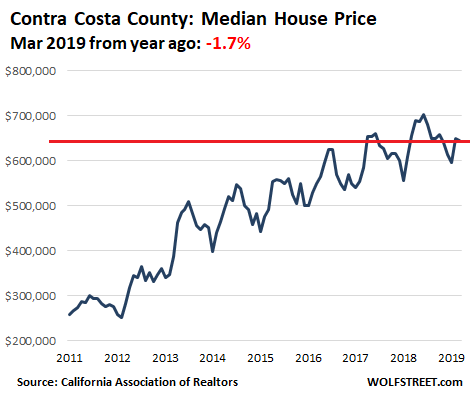

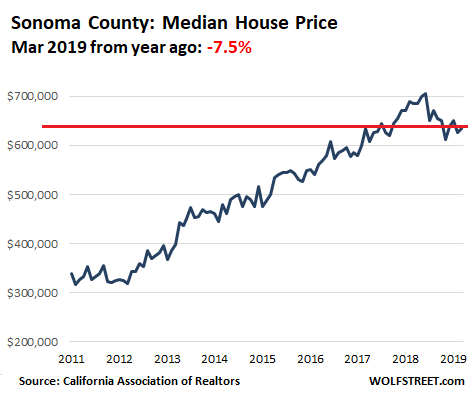

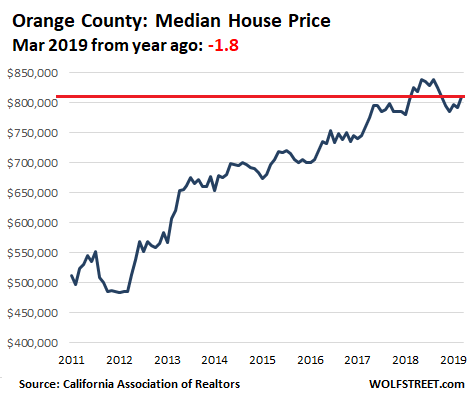

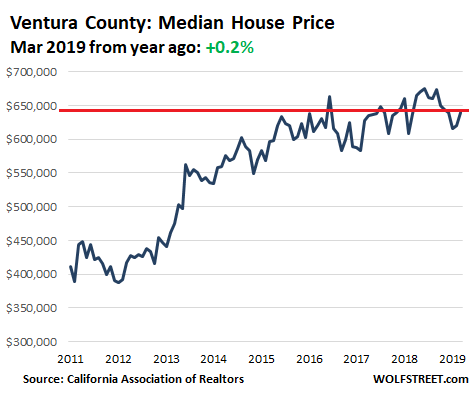

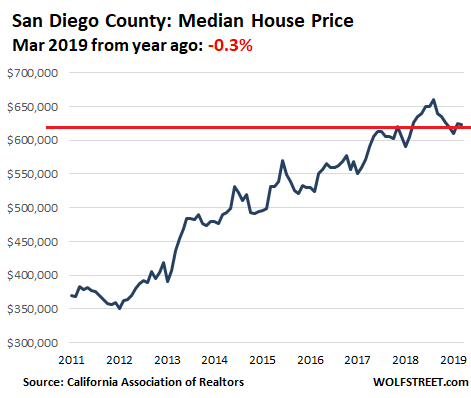

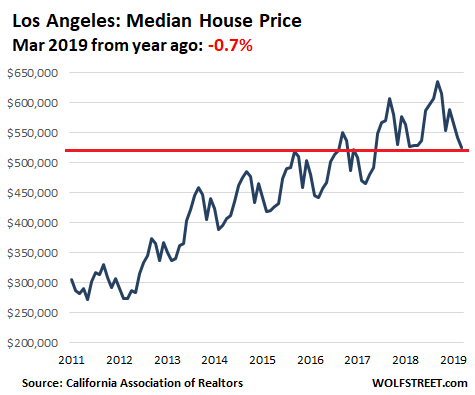

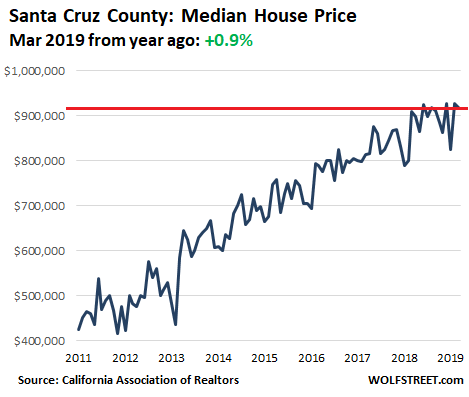

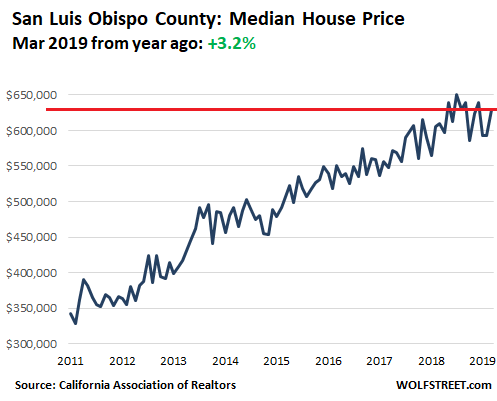

In California, the median house price in March was essentially flat with March last year at $565,880, according to the California Association of Realtors. But among the most expensive 16 coastal counties – those with a median price for a single-family house above $500,000 – there were only four counties where house prices ticked up compared to March last year: Napa +3.6%, Santa Cruz +0.9%, San Luis Obispo +3.2%, and Ventura +0.2%. In the other 12 counties, prices fell year-over-year. This year’s widespread decline in expensive counties is the first such event since the end of Housing Bust 1.

Despite “the lowest interest rates in more than a year,” sales volume in California dropped 6.3% in March, compared to March last year, to a seasonally adjusted annualized rate of 397,210 houses, according to the CAR.

Sales volume in March dropped in all major regions from a year ago (not seasonally adjusted), with single-digit declines in the Central Coast and Central Valley regions and double-digit declines in these regions:

- Nine-county San Francisco Bay Area: -10.8%, including a 27% plunge in Napa and a 20.4% plunge in Sonoma.

- Los Angeles Metro: -12%, topping out with a 15.4% decline in Ventura.

- Inland Empire region: -10.4%, with Riverside -9.3% and San Bernardino -12.2%.

And the median price has begun following volume. Especially in the Bay Area, median prices tend to rise sharply in the spring from the lows of January due to seasonal factors. But comparing prices from March this year to March last year eliminates the seasonal factors. Also note: “median price” means half the sales prices were above the median price, and half were below the median price. But the price range can be very wide.

Counties of the San Francisco Bay Area

Eight of the nine counties of the San Francisco Bay Area qualify for the “most expensive” label, with a median house price above $500,000: The counties of San Francisco, San Mateo and Santa Clara (Silicon Valley), Alameda and Contra Costa (East Bay), and in the North Bay, Marin, Napa and Sonoma. Only Solano County falls below it, with a median price of $438,500 (-1.5% year-over-year). So here are the eight counties, in order of median price in March 2019:

Southern California

Four of the six counties of Southern California qualify for the “most expensive” label with a median price above $500,000: The counties of Los Angeles, Orange, San Diego, and Ventura. The median house prices in Riverside and San Bernardino, at $412,000 and $309,000 respectively, missed the cut-off point. Los Angeles is a huge and diverse county, with a very wide range of home prices that include some of the most expensive properties in the world. But the median price means that half of the homes sold for more and half for less, and in a vast and very diverse market like this, the relatively few very pricey homes don’t move the needle much.

Central Coast

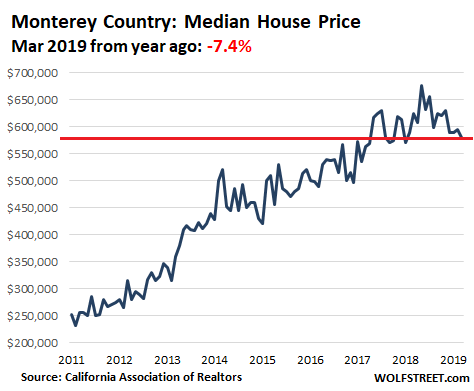

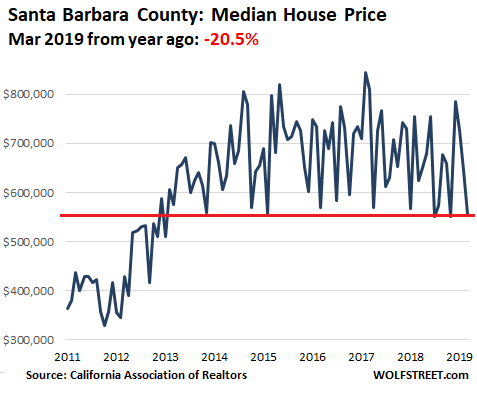

This long stretch of the beautiful California cost between the San Francisco Bay Area and Southern California is comprised of four counties: Santa Cruz, Monterey, San Luis Obispo, and Santa Barbara. All of them qualify for the “most expensive” label.

So what does this mean?

As the super-volatile chart of Santa Barbara shows, median prices can be noisy, and turning points are not always easy to see. But beyond the ups and downs: Most of the counties on his list have seen a blistering house price boom over the past seven years, and 2019 is the first time since Housing Bust 1 that in many of the most expensive counties, house prices have declined year over year. That’s what this means. It’s not a collapse. But it looks like a turning point.

The media has been busy publishing real-estate industry hype about how a tsunami of IPO millionaires is going to drive Bay Area home prices even higher. But not so fast. Read…. What’ll Happen to Home Prices in Silicon Valley & San Francisco after the Mega-IPOs? Last Two Times, We Got a Housing Bust

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It is all “priced to perfection.”

Even a flat market is now a disaster as folks have come to rely on the “sweet equity” to fund a lifestyle unsustainable by their income level.

Then sell, pay off the home loans and move to a far less expensive and less tax red state.

Priced to perfection. One hiccup and it tumbles.

The SB chart is laughable. Median home prices don’t jump up and down 20-30% every year like that. That’s some wack data.

The median prices of homes that actually sold in SB actually did jump up and down EXACTLY like that.

Looks like an artifact of two phenomena:

1) Relatively limited volume such that prices of houses sold did not match the distribution of all houses in the market

2) Graphing monthly(?) sales data appears to show high price & low price houses selling better at different times of the year

Speculation: on an annual basis (not monthly) it looks like prices actually peaked around 2014-15, and have trended down since then

“SB County” lumps together some very disperate housing markets. North County is much less expensive. You really need to separate out the South Coast area (SB-Goleta-Montecito-Carpinteria).

It’s a small sample size, and it depends on the mix of housing selling at any given time — big estates or tract homes. Since the debris flow that killed 25 people last year there are numerous Montecito mansions up for sale.

This is it exactly. We used to live in Goleta and thought about buying a home. When I tried to research it was a PIA because of the north county comparisons and the small south coast market. Fortunately Zillow has neighborhoods in their API.

SB County is very price diverse, but we are still measuring median price not average. Housing is very expensive and many are priced out.

It is better not to quote monthly figures because different segments of the market operate at different times of the year and price sensitivity is different for homes near the median price than it is for the extremes.

Great stuff, but I have a difficult time seeing on the graphs where March 2018 is….wish there was a marker.

I second that request.

I have been sitting on the sidelines now for 4 years and have been considering buying a house here in S.Calif, one thing that has really bothered me lately is our current Governor and his aggressive plans for taxing just about everything. Love the climate here but do not like the homeless,taxes,traffic and property prices. When I look at homes in Austin,Texas I really struggle on what to do, I was born here and all of my family is here so not so easy to just pick up and move.

Move and watch your family follow, they are waiting for a reason to leave.

If you have not bought a house here you should move out

The quality of life in other places in USA are much better as your dollar goes much farther..

I see no reason for middle class to stay in here in California

I keep doing the math and here’s what I come up with. If a house costs $1.4m and the purchaser puts down $400k their monthly payment (Principal , Interest, Taxes, etc) comes in around $7k/month at 4% over 30years.

How many people have $400k? How many households have $7k/m to send to the loan servicer? At 40% of net income an household would need to haul in $340k/year. Is this realistic?

Maybe I’m getting old and not realizing what people make these days. But $400k down and $340k/year income seems like a stretch for 99%

How is one supposed to save for retirement after the mortgage and property taxes?

From the New School for Social Research:

“Around 30% of people between the ages of 51 and 56 who earn more than $80,000 a year have less than $200,000 saved for retirement, while 15% of them have more than $700,000.

Just 3% of them have reached the $1 million savings goal suggested by experts.”

Senior housing and assisted living REITs are struggling because though people need these facilities, they cannot afford to pay for them. Those who can do not wish to move to them anyway.

I often wonder if that stat is actual saving? As in savings acct…Or if they count 401, IRA etc etc… I’ve worked for several different companies over my career (including my own) and have contributed to many of these type of plans….

There is a lot more of that out there than we think…I hope.

I have a few rentals that are paid off, so my retirement is hopefully going to be continuous.. I don’t raise rent just because I can on my renters, and for that, I get rewarded with a steady income from long term tenants…

It does blow me away thinking of the payments these folks are making every month.

I’m guessing that figure includes tax-sheltered retirement accounts.

As per a Northwestern Mutual study, one in three Americans has less than $5,000 in retirement savings.

Ass per the latest TransAmerica survey,

“the median retirement savings for all households in the U.S. is $50,000. This number is higher for older generations, with baby boomers having a median of $152,000 in retirement savings and Gen Xers having a median of $66,000. Millennials currently have the lowest median retirement savings at $23,000.”

and

“29% of Americans have taken early withdrawals from their retirement accounts”

Also,

“Americans are leaving $24 billion in unclaimed 401(k) matches on the table…”

All while paying ridiculously high mortgages or rents.

When I sold my house in Silicon Valley in 2004, I bought a house in Boise with cash and invested in an apartment and land in one of those “shithole countries” where it is illegal to sell aspirin to the uninsured for $100.

My Silicon Valley house is worth millions now but I have zero regrets.

The house is the retirement plan.

California real estate has gone up at an annualized rate of 5% for the past 50 years. The $1.4M house might be worth $2.8M in 15 years. Turning $400K into $1.8M over 15 years is a pretty good retirement plan especially considering you can buy a house for $400K just about anywhere else in the country.

In the meantime, you are living in a beautiful place with perfect weather and great food and wine.

The downside is you come up a little short in retirement savings? Who cares? I’d rather live well when I’m young then live in a crappy place and pinch pennies so that I can afford to give some nursing home all of my money before i die? F that.

Or it could become like Detroit and crash and then you don’t have a retirement plan at all.

Prop 13 will be slowly chipped away and this house of cards will fall down as renters become the overwhelming majority in CA.

Good for you Ed. Although I think housing is due for a good size tumble in CA, I couldn’t agree more with your assessment. You are only alive today. We should act like that more.

You don’t need $400K income to swing a $7K mortgage payment. $250-300K is sufficient. And yes, in the bay area, couples making $250-300K are a dime a dozen.

After taxes, $250K income is about $185K which is $15K a month. After paying the mortgage, the couple has $8K a month left over for everything else. If you can’t buy food, pay utilities, drive a car and put a little away for retirement on $8K a month, you’re doing something wrong.

But at 40+% of income going to housing – if that couple loses either of those two jobs for any length of time, they’re in world of hurt if they can’t sell that home without taking a loss.

2-income trap.

Now you’re moving the goalposts. The question was “who can afford it”. I said here is who can afford it. And then you moved the goalposts to “who can afford it with a job loss”.

Using your logic nobody should ever buy a house or a car or start a business or do anything, because at some point in the future something bad might happen. In other words, live in fear your entire life.

Sounds like a lot fun.

That’s not moving the goalposts, that’s setting a sensible standard of what “can’t afford it” means. And no, it doesn’t mean “don’t live your life”. It means being prepared for financial events that are quite common and might affect you, so that they aren’t disasters for your family.

On either single or dual income, the standard financial planners’ logic is that everyone should have a savings cushion to cover 6-12 months’ of expenses. That reserve covers the mortgage payment in case of job loss or a medical crisis, until a new job can be found. The medical side is especially important for anyone over 50.

But most dual-income couples don’t have that savings, so raising the question of “what would you do on 1 income?” is legit. In fact, it’s so legitimate that there’s a 2004 book “The Two Income Trap” on the whole subject. The data shows that two-income families end up being more, not less, vulnerable to financial crisis, because they aren’t prudent about their risks.

There were a lot of folks who lost all their savings in 2007-2010 b/c of loss of only one job. With the deep recession, even a 6-12 month cushion often wasn’t enough, so 401Ks were depleted and homes were jingle-mailed back to the lenders. Takes a lot longer to make all that back if you’ve had to pay the penalty taxes, lose the home. Toss in the stress and there’s a good chance of having to pay for divorce expenses too.

You wouldn’t buy a house without a roof or windows, because sometimes it rains. Your financial plan needs to be protected against the bad times in life too.

Terry

Having been a San Francisco homeowner before retiring to Florida, I saw a lot (unknown %age) of CA homes were bought using equity from previous CA homes.

As you observed, that still leaves a lot of people paying a lot of P&I + property taxes, and a good deal of that is no longer deductible for Federal taxes.

I would imagine doing taxes was a quite shock for owners of expensive (financed) homes in high-tax states (NY, CA, IL, CT,,,).

Well Terry, that sure puts it in perspective. Big time. After awhile you just get used to the big numbers and the shock is numbed right out of reality. My nephew lives down that way with a big mortgage and I hope it works out okay. I mentioned something similar to your post a few years ago and was met with a cold reaction from his mom so I just keep my mouth shut about it and recross my fingers. If nothing goes wrong he’ll be in the work saddle until 70 and then upon retirement won’t be able to afford the taxes and will have to move.

Terry – The numbers you are using need tweaking: Many homeowners put down 20% or $280k in your example. Those putting down more than 20% are usually second time buyers, at least.

For the monthly debt service ratios, the mortgage standalone is somewhere ~30% of gross wages and all debt around ~40% of gross wages. So $7k per month as ~30% = an AGI of ~$280k per year.

This is still a stretch for many people as you state.

You forget regular maintenance. Anyone have any formula to determine how much you usually put down in maintenance on a normal house. Also remember most houses, atleast where I am looking (east bay) are about 50-55 years old.

Add property taxes and insurance.

In the good old days about $6k of that $7k was tax deductible in CA. That helped a lot. The lose of that full deduction adds thousands to their average tax bill.

Interest on mortgage is still deductible up to $1M of mortgage.

Since older mortgages allowed the full deduction it also acts as a strong disincentive to sell. Looking forward to the first papers that analyze the impact of the tax law on pre-existing versus current mortgages on 750k or more

All my friends who live large like this live off the bank of mom and dad.

The prices should come down.

We are special in Socal

The prices in socal can never go down

This time is different:-)

Great research! This has happened not only at the same time with lower interest rates but also with the stock market coming back close to the all time highs.

At least one of them (interest rates or stock market) is likely very stretched – it will be interesting to see what happens to real estate prices when of them reverses the recent trend.

It would be interesting to do a comparison at some point of rent prices vs. mortgage payments (for the traditional 20% down) in these regions. A significant imbalance between these 2 levels is another factor that can impact real estate prices.

SoCAL Jim “This is old news”.

If you read the report, they say that, as a whole, Southern California prices are up, year over year, while they say the Bay Area prices are down year over year. Also, the small entry level beach close homes under 2 Million that are not on busy streets are hotter than heck. Beach close properties north of 3M, especially north of 5M is weaker. Realtors are saying the inland stuff, especially the more expensive inland stuff, is struggling. Mixed market. But, well located lower end beach close properties are the place to be.

Also, a report came out this week … rents in Socal are rising at 6% per year. Big stuff that will support prices. Once again, more data supporting slow economic growth with inflation.

I share with you that “stagflation” probability is near 100% in the future. Killing the middle class and convert them into rent surfs/slaves is a two step process. First price them out. Next rent squeeze them. Price move before rent (fundamental). Once you squeeze the middle class dry through rent seeking, they can NEVER buy houses any more. Now it is phase two. But that is the “plan”. With this much geopolitical instability and divide within the country with deep inequality and hatred, I am NOT sure the “plan” will happen smoothly.

My son rents a nice 2 bdrm apt w/ garage less than 1/2 block from the beach in Long Beach. It’s a pretty nice place and he just got his annual increase – $50 on $2100/month. He was quite pleased.

There is also a likely phase 3: Raise property taxes enough to cover pension deficits and other state and local government shortfalls.

Those increases, if they happen, in combination with Proposition 13 freezes, will tend to chill the market.

Adam Smith would approve.

Del Norte County (California’s most northern county) with a cool, wonderful coastal climate, no traffic, decent services, and NO-SALES- TAX Oregon just a few minutes away: 6 acres running down to almost the ocean, majestic beaches and soaring redwoods, daily planes to Oakland and 5 hours by car to fascinating Portland, rhododendrons and azaleas in bloom, 1800 sq ft, magnificent view, and awesome microclimate (read about The Chetco Effect or the Brookings Effect) …. $325,000.

“Life Is Suffering.” His Holiness The Dalai Lama.

I closed escrow yesterday on one of my rental properties in the Inland Empire. I priced it at the top end of the comps. It sold in less than a week for more than the asking price. I also had 2 backup offers! Sounds like a good time to unload, if you can.

Last week, mortgage purchase apps increased by 7% compared to the same week in 2018. Volume increased by 14%.

Where is this housing crash everyone’s talking about?

1. You’re talking about a housing “crash.” I’m not. In this article I pointed at price declines and said that it looks like a “turning point.” So read what the article says and don’t make up nonsense to fit your efforts to troll this site.

2. Yeah, the MBA purchase mortgage index is up a little year over year but it is still down 50% from the peak in 2005. This index says nothing about demand because it shows only buyers who apply for mortgages. It says zero about investors, including foreign investors, and cash buyers, of which there are many, especially in the places like the Bay Area.

Some observations:

1. The total number of extant mortgages is down since the housing recovery began in early 2012. This is a cash-investor market. Hence I’m not sure how relevant mortgage applications are, at least until mortgages break out of the 2012-2019 range.

2. Zillow tells me that my area is experiencing a ‘seller’s market’. Yet very few houses are being sold. Some neighbors have had their house on the market for 2 years, and despite a 15% reduction in the original price (tendered at the original Zillow valuation, but Zillow has flexibly reduced the valuation to track the lower offered prices even as the area supposedly continues to appreciate, suggesting the Zillow valuations are based on nothing more than fantasy) there are no bites. Seller’s market?

Another way to spot a housing bubble is looking at the NAR membership number. This organization can’t see a housing bubble if one hits it in the face. However, when the membership peak and go down, that is an indication of a housing bubble and a bust.

1926 24,166

1980 761,391

1990 810,607

2007 1,359,001

2018 1,359,208 (???)

Will 2019 forecast less NAR members? Sales has crashed YoY from 2019 to 2018. Sales has crashed YoY from 2018 to 2017. They blamed on lack of supply. However, inventory is exploding (esp. in the West Coast) but sales is dropping more. At some point, even with the lowest interest rate, sales need to pick up or you will have a record number of realtors fighting for table scraps.

https://www.nar.realtor/membership/historic-report

Canada and Australia housing busts is one year ahead of the US West Coast. The US West Coast is one year ahead of the US East Coast/Rest of US. This is coming soon. Be prepared REALTORS(R)!

“Market reports about the Greater Toronto real estate market often focus on whether buyers are on the sidelines or if sellers are biding their time as the region grinds through a generally slow period. Rarely does anyone mention the financial trouble that a lack of sales causes for the 52,000 realtors who are members of the Toronto Real Estate Board.”

“Sharon Soltanian worries about the realtors. Her independent brokerage, Soltanian Real Estate Inc., focuses mainly on the old city of North York. But, since peaking in 2016, Willowdale and the neighbouring Newtonbrook area have seen some of the sharpest declines in sales in Toronto, and she has seen agents who once had a decent living drop out of the business, go homeless, put their cars on lease-breaking websites and turn to side-hustles such as driving for Lyft or running an Airbnb.”

“‘I know for a fact, in our small brokerage, a few of our agents – and outside a lot more – they did not pay their taxes, their HST. They have huge problems with CRA because they don’t have income,’ Ms. Soltanian said. ‘Before … they had $20,000 income [a month], now they have $2,000 and they don’t know who to pay first.’”

“‘I know in the public eye, real estate agents are ruthless, heartless, all they want is to make money,’ she said. ‘The reality is, the majority of these people are educated people, immigrants. … I have Phd-from-Harvard agents. I had a dermatologist that cannot work here as a doctor. These are normal people, they become agents, it was easy a few years ago for them, but now it’s very difficult. I was talking to a few of the big brokerages in the area, and they are all saying the same thing: In this area, income is down maybe 50 to 70 per cent.’”

“Statistics from TREB help show how quickly the area fell. In 2016, the Willowdale East submarket sold more detached houses than anywhere in Toronto with 295. In 2018, only 86 houses sold in that market – a 71-per-cent drop. For realtors, that amounts to 200 fewer commissions to share, and average sale prices fell to $2.3-million from $2.6-million. Several other submarkets in the area had similar crashes: Willowdale West sales are down 52 per cent, Newtonbrook East sales are down 59 per cent.”

“‘The places that went crazier on the way up are the places that are crashing harder on the way down. Perhaps another way to look at it is that these areas became the most detached from value fundamentals,’ said Scott Ingram, a sales representative with Century 21 Regal Realty Inc.”

“In the meantime, struggling agents who are not dropping out of the business are finding ways to cut costs, leaving full service brokerages for lower-fee or discount brokerages that cost them less overhead, or trying to find ways to raise cash on the side.”

“‘Some are driving Uber because they can’t make ends meet. They are doing all sorts of alternative things to make some money,’ said Anita Soltanian, Sharon’s daughter and partner in their brokerage. She has colleagues in the industry who have put their leased luxury cars on Leasbusters.com, which indeed is packed with recent model BMW’s and Mercedes. But some who can’t get out of leases have embraced Turo, a ‘sharing economy’ app that lets 200,000 car-owners rent out their car for as little as $10 a day, like a mini-Enterprise or Budget rental.”

“And according to the younger Ms. Soltanian, it’s not just Willowdale that’s feeling the heat. ‘I know people downtown, in the condo market, they are suffering too. When the market slows you feel the ripples,’ she said.”

https://www.theglobeandmail.com/real-estate/the-market/article-in-a-slowing-toronto-housing-market-realtors-feeling-the-pinch/

Struggling RE agents are dropping out around here ever since the BC Govt passed a law that prohibits an agent acting for both seller and buyer. On surface it seems like a no-brainer good idea, but what is quite common is the drying up of listings. Why should someone now list their home just to give away the listing commission? An agent can bring around a buyer, and they will/do, but now homeowners advertise on FB, Craigslist, online sites, and egads…the local paper. The agents bring their clients around and the seller keeps what would have gone to the listing agent.

Years ago I contacted an agent and paid him good money for an honest market appraisal. I was up front and told him I had a buyer and was just looking for a fair and reaslistic price. I think I paid him $200 for his opinion. (1980s). He was satisfied and appreciated the honesty. Unscrupulous sellers get an appraisal by holding out the listing carrot, then go around the agent’s back. To me this is just plain old theft.

I wish more people would write about the speed at which a collapse occurs. Most people think it takes a year or months and you can see it coming, but you can’t. My husband had more orders than he could handle in Dec 2007, in Jan 2008 most orders were cancelled and then the bank pulled his credit line. It was over in weeks.

There are people in Australia and Canada who have been paying their mortgages for decades and now don’t qualify for a refinance. Most people will say they bought a house they couldn’t afford, but the truth is much different.

Yup. In ~15 years of working as a SW contractor, I had never seen things roll over and collapse as fast as they did in 2008/2009. We went from fully booked to nothing in about 6 weeks.

Then I was out of work for ~9 months. Even during the .com/telecom wipeout of 2001 I was only out for about 3 months.

We have always told our people to be able to ride for about 6 months with no income. (We are all 100% commission. So no billing, no pay.)

After 2008/2009 my new metric is you better be able to survive for 18 months…

It’s getting kind of wonky with our clients now. The big guys are pushing for net 90 terms or even net 120. We’ve always pushed back and they’ve folded, but it’s a pain in the butt to negotiate with them. (Our European and Asian clients never play the *finance* games the US companies play. Overseas usually pay net 30 or on receipt.)

I’m sorry but I can’t feel any sympathy for the realtors. My realtor has an automated system that sends me properties that hit MLS, just like Zillow or Trulia or Realtor would. If I like the property, she send me the disclosures from the MLS, and starts hassling me to put an offer. Wont even bother to put an offer at asking (forget about lower bid) and usually is very pessimistic about any offer unless I bump up the offer by 20-50K. Feels like she’s working for the seller. Couple offers she put for us, were all electronic. So I have to bust my behind working in front of a computer 8 hours / day, skip vacations, skip taking the kid to no more than 1 warriors game / year, to put together my down payment over 5-7 years, and she gets to take a huge chunk out of it for essentially opening a few doors, and forwarding some emails.

You need to look at the agreement(s). Don’t get into a dual agency relationship. (Agent reps both seller and buyer. In that case their responsibility is to the seller. As I understand things.)

I was in SFO last week and my Lyft driver was a realtor

He had a lot of marketing material talking about why this is the best time to buy a home in sfo…

You’re not going to spot a bubble with data points spaced every 10 years!

The NAR data (your link) give annual values and show steady increases in membership since the trough in 2012. The prior peak in 2006 came at about the CA market peak, but you wouldn’t have known until the 2007 data came out and by then you’d have been too late.

I never said that you can spot a bubble using the NAR number. However, you can clearly spot the BUST after the facts. Is this going to help you you try to time the market? No. However, this will help you avoid being a knife catchers!

Can someone please chime in on Santa Clara county? -10.6% What is going on down there?

Two comments:

1) It’s well known that median prices are heavily distorted by changes in the mix of sales.

2) Weather influences timing of house sales. I suspect the wet-and-cold second-February weather in March 2019 was considerably less realtor-friendly than the March 2018 weather.

Basically I think Wolf’s on to an inflection point in the market, but it’s too soon to get too excited.

When I look around and see the poor condition of many homes and the cheap construction of new homes, I can’t help but think we’ll have plenty of shoddy looking neighborhoods in 20 years, especially considering people have become house poor and can’t afford maintenance because of the highly inflated cost. What’s the warranty on a new house? One year?

The warning signs are in plain sight but to those who have never experienced a housing bust firsthand, it may seem like “this time is different”. In reality it isn’t. It couldn’t happen again could it? They’ll never let that happen again…right? But, next time will be much worse. Trillions of dollars of debt have fueled a frankenstein of a speculative bubble in real estate & other financial assets. That’s where we are today. With the stock market at all time highs, & valuations at all time time highs, “turning” point is analagous to “breaking” point.

The turning is being exacerbated for folks like us who live in Contra Costa county. The new Federal tax plan is a killer. No more maximizing Itemized Deductions like home mortgage interest & SALT now being limited to just $10k. Also, as I discovered this year doing our taxes, the $8,100 deduction we used to be able to claim went bye-bye. All told, our tax liability went way up. The standard deduction of $24,000 doesn’t cut it. And we own a modest size house right around the median price.

My wife & I had planned to spend the rest of years here. We are native Californians having lived most of our lives in So Cal. Most of our family & friends are there

Same here in San Diego

The new tax plan hit me.bad

What seems to be happening is housing sale volumes are down noticeably but housing prices are not down nearly as much.

Sellers are digging in while buyers are waiting.

Since the Fed is pushing free money I suspect sellers will be rewarded and buyers disappointed.

Housing market is like a titanic and takes time to turn around

You need to wait for a year or two

Also..it’s a game of comps.. some people must sell and this brings down the price in the whole neighborhood

con’t

but unfortunately we can’t afford to retire in CA. We need to stretch our retirement dollars farther. So cue Grand Rivers, Kentucky & 3 acres by 2 awesome lakes. We are selling our house here & giving what equity is left over to our 2 kids so we can see them enjoy it while we’re alive. Our plan is to move forward now before the SHTF.

Why can you stretch your $$$ farther in Grand Rivers?

I live in a cheap area. It is changing. Why? Because we have folks fleeing

from high taxed & regulated areas. Of course what do they AFTER they move here? Demand every service under the sun. Shocked that farmer Fred can spread manure, people are allowed to cut trees w/out a permit,

and of course…the **** neighbor just moved a single wide next to my

3500ft2 retirement house!! Now they need the services & the regulations.

And it starts all over again. Before ya know it, the cows will have diapers..cloth of course…and we will be hiring sh*t collectors from the bay area to keep our roads & sidewalks clean.

At least the RE prices will have appreciated nicely.

Tom:

Good comment. Too many hi-price homeowners flee to rural or semi-rural communities and don’t spend enough time “surveying” the areas and when they build their dream home on that wonderful hill with a view, several years later a junk yard forms around the lower levels. Having moved from Silicon Valley 20 years ago it was important for me to know the surrounding areas where I did move so as to avoid (so far) that kind of activity. You’d be surprised at how many homes in my area (Sierra foothills) seem to be wonderful places to live along that winding road, but just around the corner is just what was mentioned; a double wide trailer on blocks and scattered trash all over the place.

We lived in the Bay Area for the last 6 years, recently moving back to Chicago due to a family illness and our childrens’ school closing in San Francisco.

Looking back, selling our SFH in March/April 2018 time frame was perfect timing. We received 5 offers in 10 day offering period with 3 offers going 2x the $ amount we countered back with ultimately closing at 30% over List Price. While it was great for me and my family, all I could think about is the 5 families whom made offers both dual income, highly successful parents that were still unable to get a home in San Francisco. I just found that amazing, sad, and really hit home as how unsustainable it has gotten. At what point do those families pack up and leave, believe that is started and will continue to accelerate as jobs can be done remotely, which luckily was able to transfer mine and hop on a plane back to Bay Area as needed.