House prices in Miami eke out post-collapse record but fizzle in Las Vegas, Phoenix, Washington, DC; fall in Chicago. Cincinnati & Detroit tick down further.

There is a counterpart to “The Most Splendid Housing Bubbles in America,” as I have come to call the San Francisco Bay Area and the metros of Los Angeles, Seattle, Dallas, Boston and some others where home prices have surpassed, often by a wide margin, the crazy peaks of Housing Bubble 1 that imploded with such fanfare about a dozen years ago, even though some of those bubbles are now once again deflating. The counterpart to these bubble markets are markets where home prices:

- Are surging but haven’t reached Housing Bubble 1 peaks because those peaks were just so crazy that they’re hard to reach – such as in Miami, Phoenix, and Las Vegas; or

- Are meandering up but are not surging, and have not gone near Housing Bubble 1 peaks, such as the Chicago metro.

- Are now surging far beyond their modest Housing Bubble 1 but are not quite there yet to be promoted to “The Most Splendid Housing Bubbles in America,” such as Charlotte.

- Never experienced Housing Bubble 1 and are now not having a Housing Bubble 2 either, such as Detroit or Cincinnati.

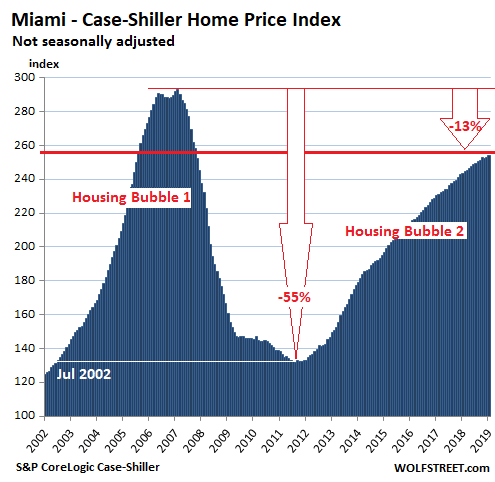

Miami

This is the epitome of Housing Bubble 1 and Housing Bust 1, and it’s now trying to complete Housing Bubble 2 in a hurry. Single-family house prices in Miami ticked up again in January, according to the CoreLogic Case-Shiller Home Price Index released yesterday, to a new Housing Bubble 2 record. And are up 4.4% from January last year:

In the seven years from 2000 through February 2007, the peak of Housing Bubble 1 in the Miami metro, single-family house prices nearly tripled, according to the Case-Shiller Index. That’s a price explosion of mind-boggling speed and magnitude, upon which prices collapsed 55%, and by 2012, were back where they’d been in July 2002. Then prices began to re-surge but remain 13.4% below the peak of Housing Bubble 1.

The Core-Logic Case-Shiller Home Price Index was set at 100 for January 2000; a value of 200 means prices as tracked by the index have doubled since the year 2000. A value of 300 means prices have tripled. At the peak of Miami’s Housing Bubble 1, the Case-Shiller Index stood at 293 – hence the near-tripling of prices in seven years. Even today, with an index value of 254, the index is up 154% from 2000. What is forming before our eyes is a beautiful Housing Bubble 2.

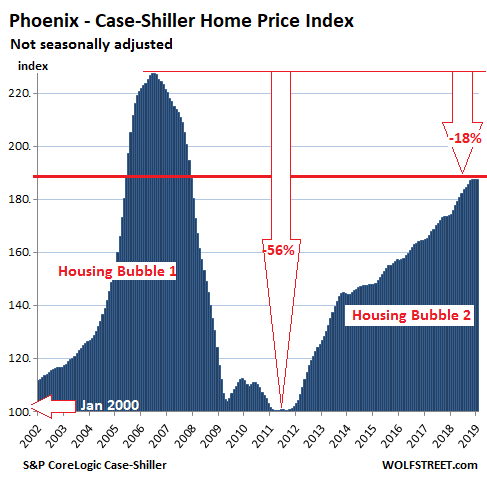

Phoenix:

Single-family house prices in the Phoenix metro began spiking in January 2004. By the peak of Housing Bubble 1 in July 2006, in two-and-a-half years, the Case-Shiller index skyrocketed 80%. Then home prices collapsed. By 2011, they revisited levels where they’d been in 2000. Then prices surged again. In January, the index ticked down below the November level, but is still up 7.5% from January a year ago. It remains 17.7% below the crazy peak of Housing Bubble 1:

The Core-Logic Case-Shiller Home Price Index is a rolling three-month average; this morning’s release tracks closings that were entered into public records in November, December, and January.

The index is based on “sales pairs”: It compares the sales price of a house in the current month to the prior transaction of the same house years earlier (methodology). This eliminates the issues that can skew median price indices (changes in mix) and average price indices (a few big outliers). By tracking changes in price of the same house (sales pairs) over time, it tracks how much more, or less, it takes to buy the same house, and thereby it tracks how fast the dollar is losing or gaining purchasing power with regards to buying the same house over time. This makes the index a measure of house-price inflation or deflation.

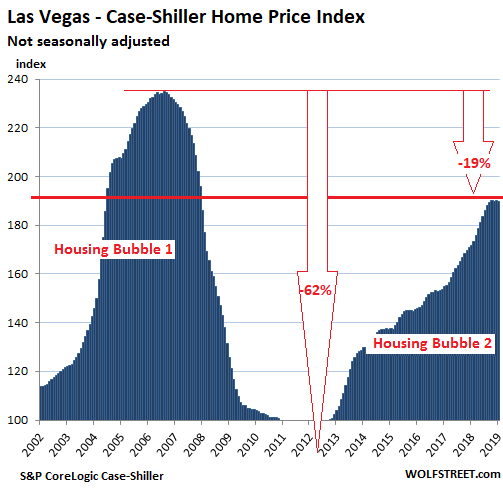

Las Vegas:

Single-family house prices in the Las Vegas metro jumped 10.5% in January from a year ago, according to the Case-Shiller Index. But since October, the market fizzled and the index for January is about flat with September. Las Vegas was of course one of the notorious Housing Bust 1 locations, and prices, which had peaked in September 2006, plunged 62% by February 2012, to levels not seen since the 1990s. But even after the price surge in recent years, the index remains 19% below the crazy peak of Housing Bubble 1:

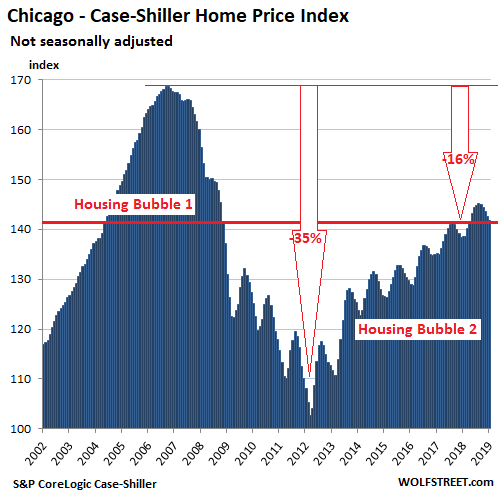

Chicago:

Prices of single-family houses in the huge and diverse Chicago metro ticked down again in January, for the fifth month in a row, and are 2.3% below the post-collapse peak of August last year. So far, this decline is in line with prior seasonal declines. Year-over-year, the index is up 2.4%. It remains 15.9% below its Housing Bubble 1 peak:

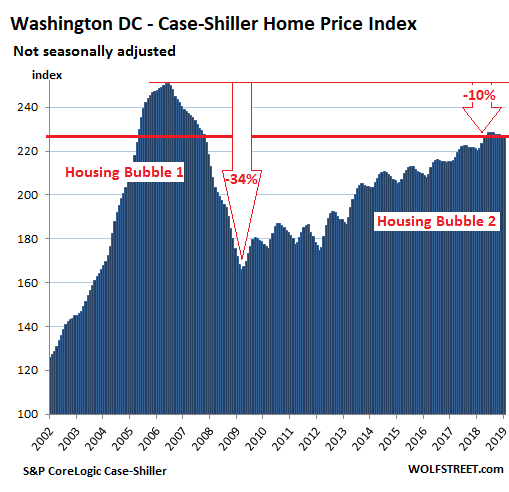

Washington DC:

The Case-Shiller Home Price Index for the Washington D.C. metro dipped in January to the lowest point since May 2018, but due to the strength early in 2018, is up 3.1% year-over-year. It is still down 9.6% from its ludicrous levels at the peak of Housing Bubble 1, under which prices had skyrocketed 150% in the six years from 2000 through the peak in May 2006:

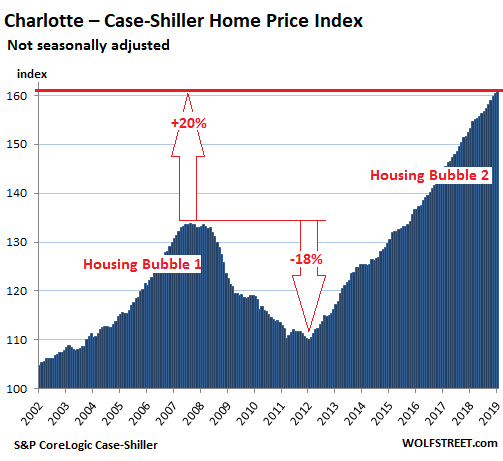

Charlotte:

House prices in Charlotte rose again in January, continuing a relentless multi-year series of month-to-month price increases. They’re now 20% above the peak of Housing Bubble 1. But Housing Bubble 1 in Charlotte was not as extreme as in other markets, with prices having surged 35% in seven years, instead of 200% as in Miami. So, Housing Bust 1 was milder was well. But over the past six years, prices have risen 40%. At this pace, once the index gets closer to 200, Charlotte will soon be promoted to a slot in the Most Splendid Housing Bubbles in America:

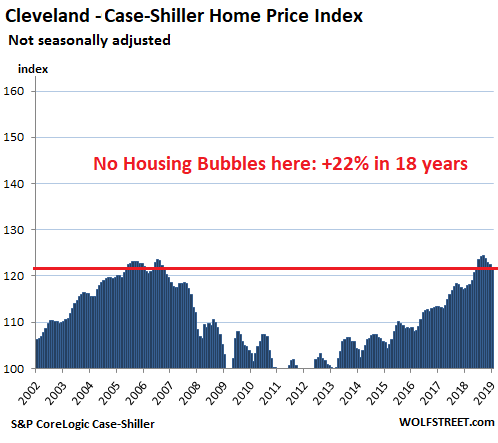

Cleveland:

House prices in Cleveland inched down in January to be flat with June 2018. The Case-Shiller Home Price Index is 22% above where it had been in 2000. And there are no signs of a housing bubble. There was strong price growth before 2006, then a relatively mild drop, and mild growth since 2012. I kept the left scale at the minimum range in this series, going from 100 to 160, such as Chicago, but almost half the size of Miami’s scale, which goes to 300. This shows how little prices have moved compared to a market like Chicago:

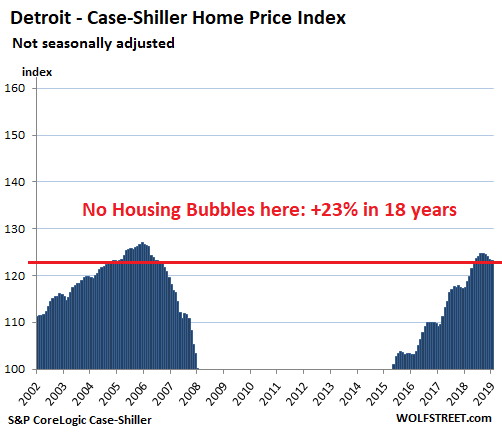

Detroit:

The Detroit metro includes the largest city that ever filed for bankruptcy in the US. The filing, expected for a decade, occurred in 2013. But by that time, home prices, which had plunged to levels not seen since the early 1990s, had already started recovering. For the whole metro, the Case-Shiller Index has risen 47% since 2013. Like Cleveland, I kept Detroit on the same minimum scale, with 100 being the bottom:

This is why national housing bubbles are rare: While there are currently many large markets in the US with housing bubbles — including deflating housing bubbles — there are plenty of other markets that don’t have housing bubbles. Some are depressed. Others are just healthy. Some markets have gone crazy. Others have gone nowhere. But thrown all into one bucket, they create the US housing market overall; and by this senseless measure, the US housing market is not as perilously overvalued as many individual markets.

San Francisco Bay Area house prices fell 4.3%, condo prices 5.7% since July. Seattle house prices fell 5.9%, most since Housing Bust 1; Los Angeles, San Diego, Denver, Portland, New York condos, and Boston all decline. Dallas ticks up. Read… The Most Splendid Housing Bubbles in America Deflate Further

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As I said in an earlier post, it is all “bass akwards” thanks to the FED games all these years. The FED tried to fool “mother economy” and there is going to be hell to pay. Like the old commercial said; “its not nice to try and fool mother nature”.

The Fed didn’t try fooling, it tried straight-up drugging.

The Fed “Bill Cosby’d” the economy?

You do realize we are about to have 5 to 10 thousand New millionaires this year with Lyft,Uber,and the rest of the unicorns going public.

Bay area

Daniel — Deja Vu … trace steps 15 years ago dot com created millionaires. Interesting to understand what has happened to them. https://www.businessinsider.com/where-are-they-now-the-kings-of-the-90s-dot-com-bubble-2014-8

https://www.moneycrashers.com/dot-com-bubble-burst/

“New millionaires?” No. This is media-hype BS. They’ve been already millionaires for a while — many of them for years. Their shares have been worth a lot for years. They could sell them, and they could use them as collateral. And they did. And they bought big houses with them and luxury condos. Most of that has been done and contributed to the housing bubble over the past few years.

Wolf is correct, those that are millionaires have been that way for a while. While Lyft is at about 5K employees now, it was only about 1500 a couple years ago, and only 350 just 5 years ago.

For example, for Lyft I’ve been made aware of various employment offers over the past 2-3 years. By my calculations an average person starting 2 to 3 years ago might clear 200-350K in stock comp after the tax man takes his cut. That assumes they can sell near the strike price. People that have just started in the last year will have a stock package that pays almost like any other public company.

I don’t think a lot of these people are getting rich, especially with COL. They will just get a bit of a balloon payment that brings their total comp (over a few years) in line with other large tech companies.

There is a very simple fix to all of this… There’s only one fee that is constant in both bubbles, and NO ONE wants to admit it.

Here’s a thought… Why have we been convinced that it’s okay for our industry (real estate builder), to have to reset it’s pricing structure every 10 years.

Simple. Take away real estate agents ability to only drive up appreciation, on both the buyer and seller’s side… until it pops and we have to start over.

They have no liability, no insurance in case someone dies on your work site, and is only required to have a two week course to do what they do. None of my other employees have that little skin in the builder game, but agents who use the “industry standard” 6% are putting all of our industry out of work, and doing it in a steady cycle under our nose. What happens when it bursts? They go on a vacation, and all my workers have to find new jobs for a couple years. It’s impossible to get them back after such a terrible experience.

No other asset only goes up in presumed value.

I am a builder, and I love my company enough to stop tying agent’s on both side’s to a higher sales price… it’s the only thing left causing the bubbles… Flat fee or nothing…

#noPercent

@mich

Amen.

Any thoughts on why, given the web / Netscape have been around since 1995, that real estate broker fees / biz model has hardly changed in ~25 years?

In 2019ish I tried using one of those flat fee MLS listing services, but to no avail. IMO it was just a terrible time to be selling. I’m not sure why in heady days ppl still

Give brokers a 6% cut.

You’re wrong Micah. I’ve been a Realtor for 31 years. Sellers love to set the price of their homes. That includes builders. We have little control over prices. If we push too hard to prove reality to a seller they simply go to another broker. Hence, brokers will take over-priced listing. But it’s not as if Buyer’s don’t shop. And any decent broker working with a buyer can point out over-priced listing to protect their buyers. Where I work (Oregon) the left leaning government has not backed off Oregon’s very restrictive land use ordinances. Those rules make the development of new homesites potentially much more expensive. “Free markets” are defeated by government sanction every time. it’s just a matter of time. We will see another housing bubble bust again and probably as soon as interest rates are driven higher.

I think the evaporation/slowdown of the hot China money is a bigger factor than the “new millionaires” story.

The RE industry and the press love the second one, as it’s a good story and gets clicks when you say another thousand millionaires will be created; to Wolf’s point, everyone has known these companies were going public for some time; anyone with stock could have walked into First Republic and used them as collateral. This should also be factored into prices already, and prices are still weakening even with these announcements (albeit slowly).

The second one still gets buried in the media, because I don’t think people around here (especially politicians and the media) want to know just how much nonresident money has skewed the CA market over the past 4 years. It’s a political third rail to all of a sudden wake up and say “Hey the reason you can’t afford a home is because the Chinese are parking their money here and using it as an escape hatch.” in a city that is 35-40% Chinese already.

Time will tell what wins out.

Always follow the Chinese money don’t follow interest rates. That’s how to know where prices are headed. So many people get sucked into following interest rates and end up losing their shirt. Always follow the Chinese money not interest rates.

In housing bubble#1, the slope rise matches the slope fall. Either two years to rise & two years to fall, or three years to rise & three years to fall (Charlotte). My guess is housing bubble#2 will have the same rise and fall slope. It’s been five years (or so) rising, so a slow and painful five years of falling.

Bobby – There is a difference between a bubble market and market adjusting to constantly fluctuating market conditions. The rise of many housing markets can be attributed to strong economic growth combined with historically low interest rates and rapidly climbing rental rates.

We are not in another bubble because there is strong fundamental support for housing valuation in the majority of markets. The fundamentals being rent is outrageously high, interest rates are incredibly low, and job growth is strong, and for professional services workers, wage inflation is keeping pace with housing inflation.

Some major markets are pulling back slightly to reflect higher interest rates and new rules from the tax reform act but this is just the market correcting to new conditions. It does appear that a recession may be on the horizon, which will impact some areas more than others, but I see no evidence that houses are dramatically expensive and overpriced everywhere.

I see loads of price reductions in Miami… I think the market needs to fall by a third and the old run down houses need to drop to a cleared plot valuation.

IMO, part of the Miami/Broward decline is being caused by decreased demand because potential home buyers are instead deciding to come over and ruin The Other West Coast.

We don’t need a wall at the Mexican border as much as we need one at the Broward County line on Alligator Alley.

What about the effect of sea level rise on Miami real estate values?

Generations away — probably some effect on Boom #7, but not in our lifetimes.

or the new FEMA floodmaps that should be out in 2020?

A lot of new waterfront real estate is being created daily. That’s one reason prices are surging.

I think the bigger demographic change is that there aren’t enough EchoBoomers that are able to live the full-pension retirement lifestyle. There’s a problem of too much supply AND too little demand for these 3K sq ft Florida McMansions.

And much of the sub-300K semi-beach houses (e.g. Treasure Coast) are butt-ugly.

Bingo on the new flood maps. At least here in eastern NC, they are out, and have affected prices and sales lead times greatly if a place is newly in the flood plain…

People in Chicago and Detroit have a real problem. In order to retire well, you need the big 3:

1) Decent 401K

2) Social Security

3) Big gains on your home

Miss any one of the 3, and you have a retirement crisis. Since the good old fashioned pension is long gone, how does the average joe retire without big gains on their home? Impossible. A retirement crisis is on the horizon in Detroit and Chicago.

Add Cleveland to the retirement crisis list.

Recent reports show about 30% of Americans have no retirement plan OR retirement savings.

Bubble in housing means appreciation will be muted or negative, so cashing out with appreciation will not be an option.

With two of the three legs of the stool broken, that leaves social security, which is scheduled to undergo a >25% haircut by 2033.

The Golden Years are looking less guilted, unless you are willing to leave the US for less expensive living.

Baby Boomers came in with a bang, but most will be leaving this planet with a whimper.

SocalJim – Unlike California, houses are reasonably priced in Chicago and Detriot( and most of the rest of the country for that matter) and workers can actually save money and invest in the stock market.

California is pretty unique in terms of playing the real estate ponzi scheme game in order to retire. Even in high cost of living areas like DC, it is possible to save $100K+ per year because your entire paycheck isn’t allocated to state taxes and a mortgage payment.

There are limits and surely we have reached them? I deleted my comment and instead post this 2 minute wonder which is a real flash from the past. Unfortunately, it is more applicable every day.

There was a recent article about softness in housing prices in affluent retirement areas in North Carolina and South Carolina. Boomers in those areas built large homes and now want to downsize.

Given the huge number of boomers , it is inevitable that supply of housing in the whole country will see a large bump as boomers die and downsize

I’m a GenXer and I remember reading, about oh maybe 15 years ago, how a gazillion boomers were about to retire early. And this was awesome news for the next generation, ie me. For you see, when all these boomers retire, guys like me would get promoted to take all the high level exec jobs they had. It was very exciting.

Except that mass retirement never really happened. Turned out all those boomers were in debt up to their eye balls and couldn’t afford to retire.

Boomers may downsize. Or they may not. Nobody really knows. These generalizations about what an entire generation will do are almost always wrong.

I’ve known a few Boomers who have upsized in their retirement. Its like they have always wanted that sewing room and 4 car garage and now by selling and moving to the South, they can have that.

My inlaws did that, sort of. My wife grew up in a 2000 sq ft home. Nothing fancy but a decent home for the family (parents, my wife and brother in law). Then my wife and brother in law left home, her parents retired and bought themselves a 2500 sq ft home, with a really high end kitchen (my MIL loves to cook). There are 2 spare bedrooms for when we visit or my BIL and his family visit or when we all visit together for Thanksgiving/Christmas.

The new home cost $150K more than what they sold the old one for.

On paper my inlaws should never have done that. They should have sold the house and bought/rented a 900 sq ft condo or something. It’s dumb to have 2 rooms that are used a few times a year, and have so much sq footage for 2 people. Or so the conventional thinking says. But life has a funny way of happening differently than what everyone thinks SHOULD happen.

Boomers may downsize, or might not. Many of them have delayed retirement after the 2009 lesson. Boomers may say they are delaying retirement, but physical and health issues typically move target dates closer than expected. I retired early, but have been shocked to see colleagues continue to work for financial and social reasons, even though in their heart, they would rather be doing fun things.

The thing that has surprised me most, is how careful I am about spending. My accountant says I can spend 4% of my savings, but I am shooting for 2.5%, so that I can afford to eat moist, instead of dry, cat food when I’m 90.

With zero and negative interest rates right around the corner it means boomers will go broke and have to come back to the workforce or never retire in the first place.

Rcohn,

I did some marketing work for developers in NC and SC during Boom #1. Most of the buyers (then, at least) were either coming from the northeast, from Atlanta, or were halfbacks from Florida. They were building second homes, so when Bust #1 started, that money dried up quickly.

Once again, if you can’t cash out of your current 5,000-foot house somewhere else, you aren’t buying a 3,000-foot house for retirement. We’re expecting a significant slowdown in Florida soon.

Living in Florida, I can tell you the slowdown has been grinding on for over a year. Homes over $4M are very slow to sell, and when they do, markdowns are hundreds of thousands. Sellers are digging in their heels, reluctant to lower prices, and buyers are waiting for prices to get softer, and for sellers to cave. Real estate agents have clients that are able to pay millions, but often these sales are contingent on the buyer unloading their primary overpriced residence in (fill in the blank: CT, NY, IL, or NJ). Prices may rebound in FL, but most of the “appreciation” is likely to be just dollar devaluation.

I’m outside Kiawah, in Charleston. Two Boomer trends that are accelerating pretty quickly. The first is the Retirement McMansion, usually on a golf course, or 30 minutes from a yuppie job center, are not selling at all without huge price reductions. It’s basically early Boomer selling to a late boomer. Because these communities are so far from jobs, it’s not practical for actual working professionals to buy.

The other trend is that of the vacation rental condo, either on the beaches or downtown Charleston. I guess the idea was to buy so you had a place to stay 3 weeks a year on your personal vacations, you could VRBO/AirBnB the other weeks of the year, and when you sold you could cash out the appreciation. Rental competition is brutal, these aspirational wealthy owners probably need the cash in their real lives, so there’s a real rush to the exits right now.

Rowan, that’s an interesting point about competition for vacation rentals. We use VRBO to go north and west (everywhere is north and west of us) during the summer and fall, and the number of available condos or cabins for under $150/ night is remarkable.

Boomers want to downsize but only into

something nice and affordable..Maybe Cleveland

could be a retirement city.Health care ,learning centers etc.

all set up.

Does Detroit still have $1 houses for sale? I remember that was a thing a few years ago.

$1 houses and $30,000 tax bills.

“this morning’s release tracks closings that were entered into public records in November, December, and January.”

____

Or put a different way, the index includes data from 6 month ago. And even further than that really. There’s a 30-45 day lag between a house going under contract and selling. Homes sold in November were bought in October and September. So in reality the index is telling us what the real estate market was like 7-8 months ago. Which is interesting to see, I suppose, but kinda useless data for what is happening right now.

“…kinda useless data for what is happening right now.”

The ONLY way for you to find out “what is happening right now” is to put your house on the market right now and see what happens. If you sell it and the deal closes eventually, then you will find out what happened in the market back then. Because that’s not “right now” either because you won’t know for sure until the deal closes. And it’s only a sample of one — and not market data.

Housing is not the stock market. There are few transactions, and they take a long time to transpire.

BTW, you screwed up your math intentionally. Kudos. What the January Case-Shiller data shows are transactions that went under contract in Oct-Jan, so about 2-6 months ago, depending on how long it took each deal to close (not “7-8 months”). Some deals close in days, others take weeks.

BTW-2, the median price data we got earlier this month for “February” represented deals where contracts were signed — to use your 30-45-day delay — in December and January. So today, that would be data from 2-4 months ago.

In the past, for retirement, if you wanted to extract cash from your home, you sold and downsized.

No more. Now we have reverse mortgages. Very desirable since, in retirement, you can extract money from your home. No reason to downsize. But, it gets better. Now you get to avoid capital gains that were triggered in the old fashioned downsize approach. And, your heirs get the property free of gains taxes in the estate.

Bottom line is reverse mortgages have made downsizing obsolete. Those waiting for a the boomers selling their homes in mass will have to look for a new strategy.

By way of illustrating that there is no such thing as a free lunch: From a Daily Herald Column – Jack Gutentag- 7/28/2018

The HECM reverse mortgage program has been bleeding red ink. Losses on transactions in which the loan balance at termination exceeds the net recoverable property value have been larger than the insurance premiums FHA collects from all HECM borrowers. According to news reports, the new FHA commissioner, Brian Montgomery, is considering measures that would reduce the amounts seniors could draw on reverse mortgages. Smaller draws would result in slower growth in loan balances and, all things being the same, in reduced losses to FHA.

Other things are not the same, however. Reduced draw amounts would make the program less attractive to potential new borrowers, especially to the type of borrowers needed to make the program self-sustaining. FHA needs to take another look at what needs to be done.

HUD already tightened up its rules/limits on HECMs.

You also need to have Income to qualify.

So, more require and income required now due to the heavy loses FHA took on these.

re: ” And, your heirs get the property free of gains taxes in the estate. ”

Uh, I thought the institution that issued the reverse mortgage claimed the property when the owners died?

Nope. The property is sold in the estate, and the lender gets what they are owed. Remaining profits go to the heirs.

OK, thanks. On average, do the lenders make money? I’ve heard, anecdotally, that longer lifespans are putting the hurt on at least some RM lenders* and, presumably, there won’t be anything left for heirs.

*There was an episode of ‘American Greed’–great show, BTW–where some sharpies were buying up life insurance policies from AIDS victims, assuming the afflicted would die in a few years. Along came lifespan-extending AIDS drugs, and the sharpies took it in the shorts.

There are a lot of reasons that boomers might move out or be forced out of their homes, such as being closer to family or needing expensive ’round the clock care. If the boomers leave the property for too long or let it fall into disrepair because expensive end-of-life care eats up all of their cash then the lender forecloses. Or the value of the house drops because the housing market is over-valued and the estate gets nothing from the proceeds.

Considering they can borrow up to half of the home’s equity and the rates on the loans are substantially higher than mortgage rates and they compound continuously with the principle of the loan because no payments are being made there’s a darn good likelihood that the children of any boomers who take this option aren’t going to get an inter-generational wealth transfer, which means the next generation down the line is going to end up poorer still. Spells out a nightmare for the future economy, but the lenders will be made whole thanks to FHA insurance (yaaaaaay…)

Many Thanks Wolf, Great continuation of housing market in america. Really puts in perspective the bigger picture.

Housing market has become more like horse gambling … which metro goes the highest and drops the lowest

I think this will be the last real estate bubble. Debt saturation on a personal, corporate and government level will create a new dynamic as we go down the slope again. It may be slow and gradual compared to last time but it will go on for at least a generation as home prices retrace all the way back to the days of Paul Volcker . The Japanese are the model and I don’t see anything we have done to allow us to us to escape from the same dynamic.

My base case is, in the long term, house prices will continue to move higher and higher because the only acceptable solution to the massive debt is a currency debasement with inflation. When we are older we will be telling stories of the good old days … when that little 1000 sq ft Manhattan Beach fixer could be bought for only 2M.

Maybe, but the only acceptable solution to state fiscal crisis will be RE tax increases. Owners of pricey RE have a target on their back.

Potential house buyers can qualify for a mortgage by having sufficient income or by having enough wealth(cash)

They can also inherit a house or pay all cash for a house.

In San Francisco a buyer needs an income of ~ $350,000 to afford a median priced house. With the median family income around $115,000, only the upper %15-20% reach this income level.

For prices to continue to rise incomes must also rise or all cash buyers must continue to pour in

That is a great theory, but as I noted it is disproved by the Japanese example. Massive money printing, massive government debt growth and protection of the banks has only lead to a 30 year deflation in real estate values.

SocalJim – There is very little chance California real estate will ever be higher in the future than it is today. Job automation, lack of water, continued mass out migration and other demographic problems including an aging population, the tax reform act, etc.

California real estate has been the massive beneficiary of ridiculous tax policies and constant influx of liquidity from the Fed. The tax reform act has already dealt a serious blow to real estate across the state and Fed has very little ammo left to prop up expensive housing markets.

It is much more likely that people are going to be laughing at the idea of paying $2M for a shack in Manhattan beach in 50 years. Ever consider what is going to happen when the northern half of the country cuts off the water supply to Socal?

Southern California has a larger population than Northern California, and Southern California has a larger GDP than Northern California. As long as Southern California remains the power center in terms of GDP and population, then they make the rules. The chance of the water gets turned off by the north is zero.

This is what realtors in SoCal says: Real estate in SoCal can never go down and it has not gone down ever so far barring 4-5 times in the last 50 years.

@SoCalJim-true, and SoCal had better hope to gawd that the annual Sierra/Rockies snowpack stays heavy going forward, or there will soon be no water to shut off. Upon reentering college in 1975 after my military service, I took my first course in physical geography (at Mesa JC in San Diego, where I was born/raised and where my family had been settled since 1910). One of the general questions about human/population-earth systems interface was: “how many people can naturally-occurring water resources in the LA Basin support?” – answer: prox. 80,000. The import of this fact had no small part in my leaving San Diego for the NorCal coast in 1977. Twain’s comment on water in the West looms larger with each passing minute. May we all find a better day.

I think, outside of the 5 miles from the coast eastward. Southern CA will be hostile environment with respect to soaring temperatures. Over the last few years temperatures in East county San Diego have soared to almost 120 degrees F in summer months. Even at the beach the temps felt much hotter than when I lived there. SF Bay Area will soon be the destination everyone will flock to as this exacerbates. People cashing out to move to Arizona & Nevada will regret that decision.

The opposite will happen, the Chinese are the world’s worst investors bar none they only buy highest then lose everything. Just like Japan they’ll all end up broke and no one will be left to buy homes in America.

I’m surprised RE is still rising in Illinois, given all the bad press. The pension and fiscal problems there appear to be insurmountable without a huge taxpayer bailout. There are proposals for big RE tax increases. Unfortunately for Illinois, tesidents can easily avoid this burden by moving to a different state, and that’s why the state population is shrinking. So how long can the price increases last?

How long will the real estate prices increases in Illinois last?

Well look at it this way (borrowing a modified famous line):

A Rising QE Lifts All Assets.

And that makes me just think of something else all to gether –

Our brilliant Ivy League educated Supremes were on the right track but didn’t go far enough and got it wrong. It’s not just corporations that should be treated as people with constitutional rights, but assets. Assets should legally be people, too.

“Assets should legally be people, too.”

And liabilities incurred to acquire those assets should be people too ;-)

Dogs, too? If so, I’ll take out a reverse mortgage on mine.

Boomers have longer life expectencies than previous generations. “Just some random guy “correctly pointed out that boomers are staying in the workforce longer with an estimated %19.6 of 70-74 year olds compared to %10.2 in 1987.

“Socaljim” is also correct that reverse mortgages have allowed many people to remain in their homes by extracting equity from their homes

But neither of these arguments can overcome the huge numbers;there are 75.4 million boomers with 10,000 reaching 65 every day .

A Freddie Mac 55+ survey listed less maintenance and more walkability as important factors in housing for boomers.A large majority of these boomers will INEVITABLY encounter health problems as they age.

These three factors , a desire for less maintenance , walkability and an inability to stay in their houses due to health issues combined with the INEVITABLE deaths of huge numbers of boomers will result in a huge supply of houses within 5-15 years.

Rcohn – You are correct. The houses are going to be in bad locations and terrible condition as well. Not many people are anticipating the glut of inventory that will hit the market in the coming years.

In fifteen years, the entire country will resemble Detroit. Vast swathes of vacant and boarded up buildings surrounding tiny pockets of massive wealth and vitality.

For those born in 1954, the full retirement age for Social Security is 66.

Gen Z (the generation after Milenials) is as big as Baby Boomers. Maybe even bigger depending on how you count GenZ. The widely accepted definition is those born 1997 and later, which is 60M people.

In 5-15 years when Boomers start offloading their homes (as you predict) these 60M strong generation will be right there to start buying them. In 5 years the oldest GenZers will be 27, in 15 years, they will be 37, right at peak home buying ages.

And this is nothing new by the way. Every generation gets old and dies off. And there’s always the next generation to buy their houses from them. There are houses in New England built in the 1700s for crying out loud that have been passed down from generation to generation for 250+ years.

Greetings from Seattle and Queen Anne, the (used-to-be) center of the glorious cargo cult that was Housing Bubble 2, mostly for QA’s suburban feel, right close to Amazon’s HQ. (delivered to us the FED)

The top was in last year when everything and everyone had a property over a million dollars. That all changed real fast.

First off, our brutal landlords (who are in the FIRE biz) raised our rent $400 in the course of a year, basically trying to force us out. Only thing that kept us from moving out was my wife’s stock options.

Second – Toll Brother’s came into the market, the high-end Queen Anne market. And they even saw the bubble popping and were getting ready to mothball the property, where they had planned 69 attached homes, each just around a million dollars.

(Off topic – Anyone want to know why we have such a terrible homeless problem in Seattle? Projects like this, built on the old home of Seattle Children’s, which basically kept 200 troubled kids cycling through the foster system from hitting the streets. You tell me where these kids went?)

Who intervened for Toll Brothers? The stock boys on Wall Street. They sold them on a self-financing project (another sign of the top) and instead of leaving the gaping hole to sit there until the economy turns around?????….

Toll Brothers came back to the market with the townhouses priced 1.46 million!!!!!! almost 500k more expensive than the initial offering.

Sold signs went up on a third of the inventory and the project started moving along.

Then late in 2018 stuff really ground to a halt. Less workers, fewer trucks and less sales signs, and then the 20% down stock market, killing most of the techies portfolios.

Known for their speed (not quality) Toll Brothers property is not finished nor will it ever really be completed. Even a 50% price cut (gasp) still leaves these mediocre starter homes in the 700k range.

What a shit show!

The City council, who oversaw this orgy of over-building and demand pull from the future, have, to the person, all quit, knowing what is coming next.

One even gave his two week’s notice and is leaving his post as density cheerleader on my birthday, April Fools’ Day.

What a joke!

10th and McGraw. I have been watching that unfold. There have been a LOT of buildings that have been bought up with intentions to build yet more poorly built, overpriced boxy dwellings. They have been sitting vacant for quite some time now. Once viable business that were there are gone and blight has moved in (Crown Hill / Greenwood) Sad state of affairs in this city and the “Progressives” that ran it into the ground are bailing out. This will not end well.

A friend of the family used to work for the Toll Brothers. The experience inspired him to create the following slogan:

Toll Brothers Homes: Guaranteed for Five Years. Then They Fall Apart.

My mother was quite fond of repeating that one.

I thought Bill Gates solved the homeless problem when he donated $500M to the cause.

Oh wait, was that just PR BS meant to virtue signal to his fellow liberals how woke he is?

Just like he “solved” the malaria problem by making sure DDT could never be sprayed in Africa again. He solved the problem with mosquito nets . .high tech . . . LOL

Wolf,

Although it’s not relevant to the above fine article I’m wondering if you’ve watched the recent crash in the price of palladium?

As you frequently write on auto- armegeddon issues , I’m wondering if you see the recent price crash in Palladium as being a harbinger for decreased global demand for automobile catalytic converters?

Or is it just a wacky market?

Pete,

The palladium spike has been hyped with this connection to the auto industry. But in reality, the spike was just a spike that fed on itself. Happens like about once every 20 years. It spiked because speculators thought it would spike further, and so they bought, and it spiked further, despite the downturn in auto production. And now auto demand is weakening further, but this is not responsible for the unwinding of the spike. What’s responsible for it is a bunch of speculators trying to unload their positions.

So yes, I love your profoundly correct and technical-jargon-infused explanation: “Or is it just a wacky market?”

Wolf

Thank you for posting the chart of the Miami housing market. I would like to understand how they come up with those median prices.

There are very few if any single family homes in that price point in any decent part of town. Like every big city Miami has a huge traffic problem. Our mass transit is lacking at best. Drive times are horrendous anywhere and at any time.

1st time home buyer who don’t want 3 hour daily commutes have difficulty buying 3/2 starter of 1950 60 70 vintage that need updating at a median price.

The less desirable areas where price below median can be found in our inner city areas are disappearing. The neighborhoods in those area being regentrified because they are in closer to the downtown less commute times.

At the high end SFH waterfronts and McMansion are still moving. The market is softer because price are high and Latin American buyers, our bread and butter, have been killed off by the strong $$$. We do have some NE coming because of the tax laws but they tend to go for the condos or the beaches. As do the Europeans. The local business owners and professional are more quite in the echo bubble than during bubble #1 when RE was the best investment one could make. There are a lot of homes of 2002/06 vintage big 8000 / 10000 sqft on the market. Most are from locals who are looking to downsize and reduce overhead. The thing time has passed so to have styles. Those barrel tiled arched stuccoed Mediterranean’s of the earlier bubble have given way to the square glass/metal Moderns. The week 2nd market for the previous bubbles home styles is what is keeping the locals from being active.

We need the a weaker $ to get our L.A. flight capital market going strong again. I can see it happening when MMT or QE for the people gets cranked up. Thank you Powel for 180 capitulation on QT auto pilot and higher rates. We know emergency measures can never be unwound. Asset purchases are now a permanent tool in the Fed’s box. Let the printing begin. Trump is the King of Leverage let’s get on with. MMT QE for the people. One crack up boom before the bust please.