Where Apartment Rents Fell & Where They Surged: March Update

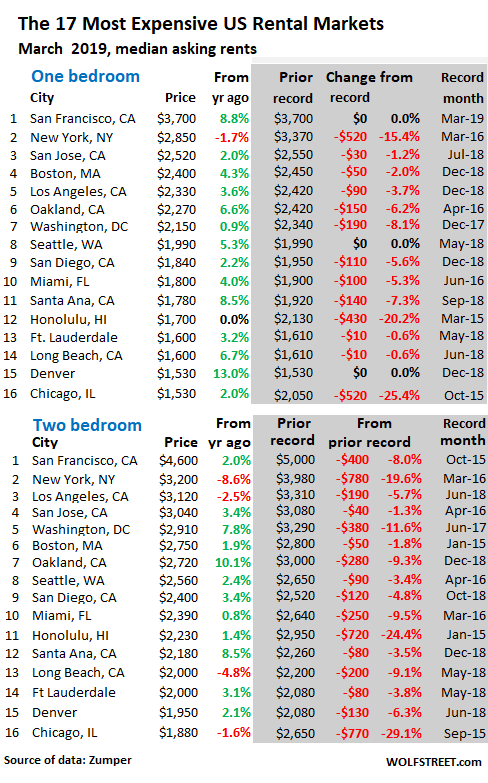

In San Francisco, the most expensive major rental market in the US, the median asking rent in March for one-bedroom apartments jumped 8.8% from last year to $3,700. This is a new record, beating by $30 the old record set back in October 2015. Median asking rent means half the apartments are advertised at higher rents, half are advertised at lower rents. After that peak in October 2015 came a long trough. By February 2017, one-bedroom rents were down 11% from October 2015. So in March 2019, the trough has been filled.

But in San Francisco’s two-bedroom segment, a different scenario emerges. The peak was also in October 2015, at $5,000. By December 2017, the median asking rent was down 15%. Rents then recovered in spurts and starts, and in September 2018 reached $4,800 — and started declining again. In March, 2-BR rents fell to $4,600, down 8% from the peak in October 2015.

This sort of peculiar noise of rents bumping into sky-high ceilings can be heard in other parts of the Bay Area.

In Oakland, sought-after by San Francisco’s housing refugees, the median asking rent for a 1-BR apartment edged down over the past few months. And in March, at $2,270 was 6% below its peak in April 2016.

Oakland’s median 2-BR asking rent had surpassed its April 2016 peak in December 2018 by $60, but has since dropped. In March, at $2,720 it was down 9% from the December peak.

In San Jose, the median 1-BR and 2-BR asking rents in March – at $2,520 and $3,040 respectively – were down about 1% from the peak last July.

In Southern California, where rents had been soaring over the past few years, a similar scenario emerges, including the sounds of rents bumping into sky-high ceilings.

In Los Angeles, the median 1-BR rent peaked in December 2018 and has since fallen about 4% to $2,330, back where it had been in May 2018; while 2-BR rents, at $3,120, are down nearly 6% from the peak in June 2018 and back where they’d been in August 2017.

In San Diego, the median asking rent in March, at $1,840, was down nearly 6% from the peak in December 2018 and back where it had been in May 2018. And 2-BR rents in March, at $2,400, fell about 5% from December.

In Long Beach, the median 1-BR asking rent, at $1,600, was down a smidgen from its record in June last year; but 2-BR rents, at $2,000, were down 9% from the peak in May, and 5% year-over-year.

In Santa Ana, 1-BR asking rents in March fell 7% from the peak last September, to $1,780. And 2-BR rents fell 3% from their peak in May last year.

The data is based on asking rents in multifamily apartment buildings. “Asking rent” is the amount the landlord advertises in the listing. Single-family houses for rent are not included. Rooms, efficiency apartments, and apartments with three bedrooms or more are also not included. Zumper collects this data from over 1 million active listings of apartments-for-rent in the 100 largest markets. This includes third-party listings received from Multiple Listings Service (MLS). Zumper releases this data monthly in its National Rent Report.

Also not included are incentives, such as “one month free” or “two months free,” which effectively slash the rent for the first year by 8% or 17%. The data includes asking rents from new construction, which other rent reports may not include.

In New York City, asking rents peaked in March 2016. Since then, 1-BR rents have dropped 15% to $2,850, and 2-BR rents have dropped 20% to $3,200.

In Chicago, rents peaked in the fall of 2015. By March, 1-BR asking rents have plunged 25% and 2-BR rents 29%.

The table below shows the 16 most expensive major rental markets. The shaded area indicates peak rents and the changes since then:

In Honolulu, rents seem to have stabilized last year and so far this year, after plunging from their peak in early 2015. The median asking rent for 1-BR apartments, at $1,700, remains down 20% from that peak, and 2-BR rents, at $2,230, remain down 24%.

In Washington D.C., rents are also marked by sharp declines with 1-BR and 2-BR asking rents down 8% and nearly 12% from their respective peaks in December 2017 and June 2017.

In Seattle, the median 1-BR asking rent in March, at $1,990, matched its record set in May 2018. But 2-BR rents, at $2,560, were down 3.4% from their peak in April 2016.

Clearly, in the most expensive rental markets in the US, rents – particularly those of the more expensive 2-BR apartments – are bumping into ceilings and are bouncing off these ceiling.

Post-hurricane rent-gouge falls apart: In Houston, rents surged after Hurricane Harvey had laid waste to some of the housing stock. By March 2018, the median asking rent for a 1-BR had shot up 12% year-over-year to $1,290 and for a 2-BR by 14% to 1,630. This catapulted Houston into 25th place in the list of the 100 most expensive rental markets.

But in March 2019, rents for 1-BR apartments plunged 12% year-over-year, to $1,130; and rents for 2-BR apartments plunged 14% to $1,400. These were the deepest year-over-year plunges on today’s list (below) of the 100 most expensive major rental markets, and it pushed Houston back down to 39th place.

Many “mid-tier” markets have massive rent increases:

Rents are booming in some “mid-tier” markets – “mid-tier” in terms of the amount of the rent, with many markets showing double-digit year-over-year rent increases. The list of the 100 most expensive rental markets (below) includes 12 with double-digit year-over-year increases in median asking rents for 1-BR apartments:

- #55 – Syracuse, NY: +15.3%

- #61 – Reno, NV: +13.8%

- #44 – St Petersburg, FL: +12.2%

- #50 – Fresno, CA: +11.1%

- #72 – Cleveland, OH: +11.0%

- #87 – Memphis, TN: +10.6%

- #35 – Chandler, AZ: +10.5%

- #58 – Boise, ID: +10.3%

- #83 – Indianapolis, IN: +10.3%

- #26 – Orlando, FL: +10.2%

- #57 – Milwaukee, WI: +10.2%

- #80 – Winston Salem, NC: +10.0%

Below is Zumper’s list of the top 100 most expensive major rental markets, in order of 1-BR asking rents. The percentages are price movements in March compared to March last year. Use the browser’s search function to find a city (if your smartphone clips the right side of the table, hold your device in landscape position):

| City | 1-BR rent | Y/Y % | 2-BR rent | Y/Y % | |

| 1 | San Francisco, CA | $3,700 | 8.8% | $4,600 | 2.0% |

| 2 | New York, NY | $2,850 | -1.7% | $3,200 | -8.6% |

| 3 | San Jose, CA | $2,520 | 2.0% | $3,040 | 3.4% |

| 4 | Boston, MA | $2,400 | 4.3% | $2,750 | 1.9% |

| 5 | Los Angeles, CA | $2,330 | 3.6% | $3,120 | -2.5% |

| 6 | Oakland, CA | $2,270 | 6.6% | $2,720 | 10.1% |

| 7 | Washington, DC | $2,150 | 0.9% | $2,910 | 7.8% |

| 8 | Seattle, WA | $1,990 | 5.3% | $2,560 | 2.4% |

| 9 | San Diego, CA | $1,840 | 2.2% | $2,400 | 3.4% |

| 10 | Miami, FL | $1,800 | 4.0% | $2,390 | 0.8% |

| 11 | Santa Ana, CA | $1,780 | 8.5% | $2,180 | 8.5% |

| 12 | Honolulu, HI | $1,700 | 0.0% | $2,230 | 1.4% |

| 13 | Anaheim, CA | $1,640 | -3.5% | $2,110 | -1.9% |

| 14 | Long Beach, CA | $1,600 | 6.7% | $2,000 | -4.8% |

| 14 | Fort Lauderdale, FL | $1,600 | 3.2% | $2,000 | 3.1% |

| 16 | Denver, CO | $1,530 | 9.3% | $1,950 | 2.1% |

| 16 | Chicago, IL | $1,530 | 2.0% | $1,880 | -1.6% |

| 18 | Providence, RI | $1,510 | 9.4% | $1,580 | 9.7% |

| 19 | Atlanta, GA | $1,470 | 2.8% | $1,810 | -1.6% |

| 20 | New Orleans, LA | $1,430 | 5.1% | $1,530 | 8.5% |

| 21 | Minneapolis, MN | $1,400 | 0.7% | $1,900 | 2.7% |

| 22 | Scottsdale, AZ | $1,380 | 7.0% | $2,080 | 3.5% |

| 22 | Nashville, TN | $1,380 | 5.3% | $1,390 | -3.5% |

| 22 | Portland, OR | $1,380 | 0.7% | $1,660 | 4.4% |

| 25 | Philadelphia, PA | $1,350 | -8.2% | $1,690 | 3.0% |

| 26 | Orlando, FL | $1,300 | 10.2% | $1,490 | 7.2% |

| 27 | Dallas, TX | $1,250 | -3.8% | $1,650 | -6.3% |

| 28 | Baltimore, MD | $1,230 | -6.8% | $1,500 | -1.3% |

| 29 | Charlotte, NC | $1,200 | 4.3% | $1,300 | 0.8% |

| 29 | Sacramento, CA | $1,200 | 2.6% | $1,400 | 0.0% |

| 29 | Madison, WI | $1,200 | 0.0% | $1,400 | 2.9% |

| 32 | Aurora, CO | $1,190 | 6.3% | $1,410 | 0.0% |

| 32 | Austin, TX | $1,190 | 2.6% | $1,470 | 1.4% |

| 34 | Tampa, FL | $1,170 | 2.6% | $1,360 | 1.5% |

| 35 | Chandler, AZ | $1,160 | 10.5% | $1,440 | 15.2% |

| 35 | Gilbert, AZ | $1,160 | 8.4% | $1,410 | 6.0% |

| 37 | Newark, NJ | $1,150 | 9.5% | $1,350 | 8.0% |

| 37 | Plano, TX | $1,150 | 2.7% | $1,510 | 0.7% |

| 39 | Irving, TX | $1,130 | -0.9% | $1,490 | -3.2% |

| 39 | Houston, TX | $1,130 | -12.4% | $1,400 | -14.1% |

| 41 | Fort Worth, TX | $1,120 | 5.7% | $1,270 | 0.8% |

| 42 | Durham, NC | $1,110 | 7.8% | $1,270 | 8.5% |

| 42 | Henderson, NV | $1,110 | 7.8% | $1,290 | 7.5% |

| 44 | St Petersburg, FL | $1,100 | 12.2% | $1,600 | -1.2% |

| 45 | Salt Lake City, UT | $1,070 | 4.9% | $1,370 | 8.7% |

| 46 | Pittsburgh, PA | $1,060 | 1.0% | $1,310 | 2.3% |

| 47 | Richmond, VA | $1,050 | 0.0% | $1,250 | 3.3% |

| 48 | Raleigh, NC | $1,020 | 1.0% | $1,150 | -1.7% |

| 49 | Virginia Beach, VA | $1,010 | -7.3% | $1,200 | 0.0% |

| 50 | Fresno, CA | $1,000 | 11.1% | $1,140 | 8.6% |

| 50 | Jacksonville, FL | $1,000 | 7.5% | $1,080 | 2.9% |

| 52 | Las Vegas, NV | $990 | 8.8% | $1,150 | 9.5% |

| 52 | Buffalo, NY | $990 | 0.0% | $1,180 | 2.6% |

| 52 | Chesapeake, VA | $990 | -4.8% | $1,240 | 3.3% |

| 55 | Syracuse, NY | $980 | 15.3% | $1,050 | 12.9% |

| 55 | Phoenix, AZ | $980 | 3.2% | $1,200 | 5.3% |

| 57 | Milwaukee, WI | $970 | 10.2% | $1,020 | 3.0% |

| 58 | Boise, ID | $960 | 10.3% | $1,100 | 15.8% |

| 59 | Kansas City, MO | $950 | -1.0% | $1,070 | 2.9% |

| 60 | Louisville, KY | $940 | 8.0% | $1,040 | 9.5% |

| 61 | Reno, NV | $910 | 13.8% | $1,310 | 12.0% |

| 61 | Mesa, AZ | $910 | 3.4% | $1,070 | 5.9% |

| 63 | Anchorage, AK | $900 | 4.7% | $1,130 | 2.7% |

| 63 | Colorado Springs, CO | $900 | 3.4% | $1,120 | 6.7% |

| 63 | San Antonio, TX | $900 | 2.3% | $1,120 | -1.8% |

| 66 | Corpus Christi, TX | $850 | -1.2% | $1,070 | 0.0% |

| 66 | Baton Rouge, LA | $850 | -5.6% | $950 | 1.1% |

| 68 | Rochester, NY | $840 | 2.4% | $980 | -2.0% |

| 68 | Omaha, NE | $840 | 1.2% | $1,050 | 8.2% |

| 70 | Laredo, TX | $830 | 5.1% | $940 | 0.0% |

| 71 | Arlington, TX | $820 | 6.5% | $1,090 | 6.9% |

| 72 | Cleveland, OH | $810 | 11.0% | $870 | 8.7% |

| 72 | Des Moines, IA | $810 | 6.6% | $860 | 7.5% |

| 74 | Norfolk, VA | $800 | 9.6% | $990 | 6.5% |

| 74 | Knoxville, TN | $800 | 3.9% | $900 | 3.4% |

| 76 | St Louis, MO | $790 | 5.3% | $1,150 | 8.5% |

| 77 | Glendale, AZ | $780 | 4.0% | $950 | 5.6% |

| 77 | Chattanooga, TN | $780 | 1.3% | $890 | 9.9% |

| 77 | Cincinnati, OH | $780 | -6.0% | $1,120 | 4.7% |

| 80 | Winston Salem, NC | $770 | 10.0% | $830 | 9.2% |

| 81 | Tallahassee, FL | $760 | 8.6% | $880 | 6.0% |

| 81 | Lexington, KY | $760 | 1.3% | $980 | 4.3% |

| 83 | Indianapolis, IN | $750 | 10.3% | $810 | 6.6% |

| 83 | Augusta, GA | $750 | 5.6% | $780 | -1.3% |

| 83 | Spokane, WA | $750 | 5.6% | $900 | 0.0% |

| 86 | Bakersfield, CA | $740 | -2.6% | $940 | 5.6% |

| 87 | Memphis, TN | $730 | 10.6% | $780 | 8.3% |

| 88 | Greensboro, NC | $720 | 5.9% | $840 | 3.7% |

| 88 | Oklahoma City, OK | $720 | 5.9% | $850 | 3.7% |

| 90 | Columbus, OH | $700 | 4.5% | $1,060 | 6.0% |

| 91 | Albuquerque, NM | $680 | 7.9% | $830 | 3.8% |

| 92 | Lincoln, NE | $670 | 9.8% | $890 | 9.9% |

| 93 | Shreveport, LA | $650 | 6.6% | $700 | 7.7% |

| 93 | Tucson, AZ | $650 | -3.0% | $880 | 7.3% |

| 95 | Lubbock, TX | $630 | 6.8% | $770 | 2.7% |

| 95 | Tulsa, OK | $630 | 5.0% | $790 | 5.3% |

| 97 | El Paso, TX | $620 | -1.6% | $760 | -1.3% |

| 98 | Detroit, MI | $610 | 8.9% | $690 | 9.5% |

| 98 | Wichita, KS | $610 | 1.7% | $710 | 2.9% |

| 100 | Akron, OH | $530 | -10.2% | $700 | 0.0% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My impression of the table is that certain large markets are beginning to peter out however certain other markets are still expanding. Is that correct or are these simply cyclical variations?

I think this is late-cycle when investors move into secondary markets seeking yields after saturating primary markets.

In the long run:

We are all Palo Alto.

[or insert whatever bubble market you like]

Huh?

Why?

I thought it was pretty clear but O.K.:

Because housing costs keep rising. First in the bubble cities, then everybody else catches up.

@gary

?

Yes, all/most USA real estate markets are positively correlated…

We all understand this.

Is it to be assumed all cities will become Silicon Valley w/respect to levels of pay?

Or will Gary, Indiana sustain $5,000/mo. Rents despite median wages below $30k?

To me it is obvious they won’t.

But I’m certainly open to persuasion

@RD

I think yes. This is 2015 map rent to income ratio which is all I could find for now

https://cdn-images-1.medium.com/max/1200/1*op_peR-I8Rk9Uz1wcoKWZQ.png

and I think that if you focus even on the most expensive localities r2i is not going to be much higher. If you take IN at 39% and CA at 42 %, that is really a very small difference, especially if you consider the remainder of a much higher initial income will be more even if you take away more ( e.g. 50% of 100k leaves 50k, 40% of 60k leaves 36k) , though obviously regional variations in other expenses would have to then be included.

As for Indiana property prices (fred.stlouisfed.org/series/INSTHPI)

But then this is all only a bubble if/when it deflates, until that time it is all sort of a de facto reality whatever anyone wants to call it, synthetic or not.

Even though other cities may eventually reach today’s bay area prices. The bay will keep ahead as long as they have a high concentration of highly compensated tech workers.

There are not too many Cities in the US where $180k a year is considered a starting salary among many large local companies. And a range of $250k to $500k is not uncommon for many of the engineers at Facebook, Google and similarly competative companies littering the bay.

Until something changes you can expect cities with large numbers of high paying companies to have elevated housing prices over the rest of us.

There is going to be widespread housing deflation in major markets. Washington DC is adding more units than it is new residents, rents have flatlined and major incentives are being pushed. The same scenario is happening is every major city. It is very easy to add 10,000’s of new high rise 800 sq foot rental units.

The other problem is the geo arbitrage is heavily in favor of buying/renting in the exurbs or smaller metros areas where prices are 1/5 as much as core downtown major markets. Entry levels workers cannot afford current prices, and higher income young families have a no brainer decision to move further out and slash housing and childcare expenses 75%. If you can cut your housing and childcare expenses 75% you are in a strong position to tell your employer to either let you work remote or you are finding another job. Employers are given concessions for flexibility because the labor market is so tight.

This recession is going to be the opposite of 2008. The decay is going to start from the top down and slowly bleed out into the exurbs.

A more interesting statistic.

Take average household income vs average household housing costs (renter or owner).

Be sure to factor in taxes (local, state and property).

“As a general rule, you want to spend no more than 30 percent of your monthly gross income on housing. If you’re a renter, that 30 percent includes utilities, and if you’re an owner, it includes other home-ownership costs like mortgage interest, property taxes and maintenance.”

https://www.cnbc.com/2018/06/06/how-much-of-your-income-you-should-be-spending-on-housing.html

Don’t forget to add in all the homeowner fees: HOA, Mortgage premium insurance, homeowner insurance (owner and liability), landscape, flood insurance (if applicable), all the “hard” utilities: gas, water, sewer, electric, internet. Also, don’t forget to amortize items in the closing costs across life of ownership: real estate commissions, title fees, inspections, appraisals, legal fees. Of course you could forget about those things, like the recipients of your funds to those fees would like you to do.

Following nofreelunch’s comment, renters often forget they are paying all the associated fees of homeowners and home ownership, it is just embedded in the rent payment. I am always aware of this because I actually have a rental I use as charitable vehicle. I charge a friend of mine a rent amount that just covers our property taxes on the acreage the rental sits on, and the property taxes of our primary residence. It is about 50% of the local going rate. One day this will change with a new tenant, but it will still be adjusted downwards to reflect the quality of the arrangement. In other words, the better the renter the better the deal they receive, and no bad tennants welcome. Ever.

You couldn’t get away with this in a populated center where no one knows anyone. Here, we know everyone and references are by reputation.

The rural advantage strikes again. :-) regards

My landlord bought a long time ago. I keep him happy. When I do the math (I could be wrong) on buying a similar place, it’s about $1000-1300/mo more than I pay now. Of course I don’t get the tax break or eventual equity.

The new townhouses around the corner that are just starting to be constructed (and seem similar to what I rent except no yard) have a “starting in the $600s” sign. I don’t earn enough to take on a mortgage like that. The immigrant neighbors that overpaid often seem to have 2nd families renting out ground floors or basements, it makes parking a mess. Neighbor does 4 spots on AirBnB — also annoying, but they’re renters.

Paulo – My observation is that buying at currently levels in a major cities the mortgage payments are 15%-20% higher than the going rental rate. The landlord is likely in at a much lower cost basis and low inventory has driven housing costs higher over the past 7 years. I can’t imagine any investors are purchasing units to rent out in the top big cities because the math doesn’t add up.

In addition, developers are adding more units than there are new residents in big cities and rents are down significantly when incorporating incentives of up to 2 months free.

Subjectively, I’m beginning to see a massive demographic shift as well. Millennials are starting to form families and realizing that raising a family in a big city is total insanity at this point. I except to see net migration population declines in every major city over the next 5 years.

Prices like that just go to prove how popular living in America is for Americans, certainly have decided to vote with your wallets there.

Nonsense. People have no choice. When you’re robbed at gunpoint and hand over your wallet, would you describe that as proof that life is popular? Is that the most astute observation given the situation?

Perhaps you were being sarcastic.

Perhaps I was .

It runs along the lines of doing a survey by phone to find out how many respondents have phones .

The biggest jump to rentals is with the under 40s

https://www.pewresearch.org/fact-tank/2017/07/19/more-u-s-households-are-renting-than-at-any-point-in-50-years/

Point 8 at national level (mysmartmove.com/SmartMove/blog/6-rental-statistics-landlords-need-know.page) on rent to income.

And for those wondering how the real estate market is (redfin.com/blog/2019-march-bidding-wars/) gives a rarer more up to date picture on sentiment.

I encourage all to stop looking at this, or anything for that matter, from the perspective of “the market”. What do market stats tell you? If I throw fifty people out of an airplane with seven parachutes thrown in, or sink a cruise liner with one air tank for every three people, or take the bride less not-so-young men of Chine… One can look at this as a market of who’s offering what to whom etc. but I claim that’s missing the point of what is going on. I go further and assert that the whole point of focusing on the market narrative is to miss the point.

Have to be cynical enough to watch the herd without becoming part of it, and all the info by the time you read it is outdated or generalised. I agree that it can be very distracting, I follow it to try to understand how different people are reacting in different circumstances, to try to figure out how the wider show is tailored, down to where narratives are fed to people and why. So maybe that makes me an exception I don’t know, but I don’t look at “the market” to tell me how things are, I look at it to see how other people think things are, and that includes data that is open to be discussed or refuted. Sometimes it matters though… if a person finds purchase expensive and rents high they might think that they are just short until they read up and realise that this is happening at a broader level to many hundreds of thousands of people . At that point they might just realise that they are part of the herd that is getting trapped. You might have the wit and energy or position to see your way through, others might not have that confidence or may be too easily sold a very false narrative. Look at the amount of people who have lost their own self esteem because they feel they have failed, when really they have just been (or allowed themselves to be) framed, you aren’t going to stop other people lifting their chins a little by pointing out that this is also how times are for many others at the moment.

I would agree that America is very popular. Lots of people from around the world are clamoring to get into America.

Not many countries have both a fair amount of wealth and a love for freedom.

“love of freedom”

I hope that is sarcasm.

I would be delighted to give up my U.S. citizenship, except for the fact that

1. The IRS has 100% discretion on whether I will receive ,my Social Security benefits that I have paid into ever year since 1995 if I give up my citizenship and move away. They have three sets of rules depending on which country you will be a citizen of and even there it is “discretionary”.

2. They will charge me an “exit tax” of 30% on my assets (this includes net assets held everywhere including outside the U.S.) I will be taxed at a 30% rate on all my assets including my Traditional and Roth IRAs even if I don’t sell anything.

3. As a U.S. citizen they tax me on assets held globally, not just in the U.S. The only other country to do this is Eritrea (Eritrea’s tax rate is measly 2%)

So if I am a U.S. citizen or live in the U.S. as a non-resident, I get taxed on my global assets. If I give up my U.S. citizenship, I am penalised for holding assets in the U.S. I have already been taxed on.

I know at least three others who continue to be U.S. citizens though they would like to move away and give up their citizenship.

So you prefer freedom also, and that is what I am talking about, but let’s not confuse company business with the mentality of a people. In many other countries taxes and contributions are much higher, you would not be where you are now in those countries I think. So (and I hope more or less impartially) I look on the restrictions placed on leaving the US as a disincentive to avoid its wealth being easily extracted and emptied into foreign nations. Not fair? Maybe, but that is the stance it takes to protect its position, not just to grab wealth of people leaving. I know Spain also taxes global assets, including resident. What the company gives it can also take away. In other countries if you give up citizenship you lose all claim to national benefits also.

The question becomes what happens if you take a second nationality, transfer your wealth abroad and then renounce US nationality. That is then a question of being on a blacklist with tax claims against you, so easier is to pay but make sure that the taxable wealth you own at that point is very little.

None of this is to take lightly, you dont move without recourse to outside of a system you are used to without first knowing that the one you are going to is acceptable, and a person really must live there some and do research on that as other countries might not live up to expectations. It really depends on reason for leaving, but there are many good destinations if you are in a position of already owning enough wealth. Panama nationality is said to be an easier choice.

Note I said both wealth and freedom – the US has a good combination in my opinion compared to many other countries, hence the appeal. That is not meant as an absolute comparison, one cannot be made.

What freedom? Freedom of what?

Save the platitudes.

Political? Economic? You gotta be joking. Freedom to be poor, neglected, uninsured and cast aside. Freedom to consume the industrial waste? Freedom to enterprise? You can do that in most of the world, but no healthy minded person actually aspires to either consume or enterprise to begin with.

People get up in the morning, go to work, build a few spacefaring pyramids, then go home anxious about how they’re gonna secure basic necessities of life: shelter, schooling, healthcare, also in old age.

All of this is of course 100x covered by available resources and labor rendered. The problem is that too few people are making decisions, rooted in a criminal principle, justified by a toxic ideology, as to the distribution of goods. That is the essence of this system. The mythical freedom that’s never clearly articulated is a cornerstone of that toxic ideology.

And don’t give me defence that it’s because people are sheep, so they get what they deserve. They don’t deserve it and they don’t get it from me, so they need not get it from anybody.

If you think there is anything positive about this country you need to get some perspective. That said, other countries share most of the awful traits, because the poison spreads, but most countries at least nominally try to do what they can to take care of their people. Not sure the US even qualifies as a country or nation for the lack of any effort in this regards. And that lack is your very freedom.

Maybe, although my brother renounced his US citizenship two years ago and had to pay a pretty penny to do so. There are many fine places in the the world to live other than egocentric America.

Every morning I wake up and thank God I’m not American

Gold is just..gold,

Concerning your other comment: it was so bad it got caught in a tripwire while I was asleep. When I got to it, I untangled it and threw it in the trash. It was purely a personal attack on another commenter and contributed zero to any discussion.

If can’t squeeze any more blood from a particular turnip, find new turnips.

Glad to see that my hometown (Syracuse) is making any positive list, though in this case it’s “went up from couldn’t get lower”. Now living on the SF peninsula, went to visit the area recently and thought “this isn’t actually that bad” (lots of great schools, great local beer)… I guess enough other people have cottoned on to all that.

Full disclosure: It’s still pretty rough.. let’s be real. Syracuse is not some undiscovered gem.

When Syraucse went to the Final Four in 1996 (or 97 something like that) a buddy of mine and I drove to Syracuse and hung out there for the weekend. One of his friends was a student there and we hung stayed with him. I have fond memories of that weekend. That school could party with the best of them!

Just moved to Solano County.

Although it does not snow and does not get below freezing, it has rained most days this year and is windy cold during the mornings. And everything from gas to restaurants (except real estate taxes)is more expensive than Northern New Jersey

The numbers for NYC seem way too cheap.

Folks forget that NYC isn’t just Manhattan. For example, the median 1-BR rent in the Bronx and Staten Island is $1,600. In Queens, it’s $1,900. In Brooklyn, $2,300. Manhattan $3,300.

Different source: https://streeteasy.com/blog/data-dashboard/

Fair enough.

But even $3300 seems kinda cheap. I lived in NYC in the late 90s. My first place, I was paying $2000 for a studio that was a sublet, from a friend of mine. 20+ years of inflation and that studio has to be at least $3000. It was an OK place, on west 34th. First apartment out of college. I owned so little back then, I could have packed and moved in an afternoon if I had too. Good times!!

My first salary was $55K, which at the time I thought was more money than God. So my rent was 44% of gross income. But how could that be? If one pays more than 30% of gross on rent, they will starve to death, right? Not really. I don’t recall ever thinking about it. NY is expensive. Always has been, always will be. That’s the bargain you make. Move to NY, and live in a tiny studio paying almost 50% of income on rent. It’s NY and it’s the best city in the world to be 23, single and starting a career. Well worth the money. I’d do it over again in a heartbeat.

I agree.

Wolf NYC numbers are always very misleading, not because he means it but because NYC doesn’t mean much. Even Manhattan doesn’t mean much. Remove north of 110 street and you get a better dose of reality.

In my neighborhood (Chelsea) a studio is 3k, 1 bed 4.5k and 2 bed 6k.

Cheaper is always possible (basement apt , shared walk up etc…) but definitely more expensive than San Francisco: by a lot.

These are “median” advertised rents, as I defined them in the article: 50% are higher, and 50% are lower. So yes, you will find apartments for a lot less, and you will find apartments for a lot more. So if there are 4,000 apartments advertised for rent, there will be 2,000 that are cheaper than the median rent, and 2,000 that are more expensive. That’s the concept of “median.”

That said, SF is about 1/10th the size of NYC. So if you want a cheaper place than what is available in Manhattan, you can go to the Bronx. In SF, you end up leaving the relatively small city and move across the Bay to Oakland, etc. So in that sense any comparison of city to city has these shortcomings of size, and variety that comes with size, and nothing in the US compares in size to NYC.

Given the unemployment rate, I wonder who is paying that rent here in Fresno, CA. I certainly can’t afford it.

Something to consider. Operating expenses for apartments are up 25-30% on many of these in town apartment properties since 2015. Most of these properties need 3-4% rental rate growth to hit their numbers.

What drove the operating expenses so much higher in the past 4 years?

Is it the slow March of local minimum wage hikes? Perhaps some of the “land appreciation” factoring in for taxes and/or lease payments? General hikes in utility rates? Would be interesting to know.

In my area, every contractor, repair person, handy man, electrician, plumber, etc., is busy and charging a lot more. Roofs, painters, decks & fences, kitchen and bath remodel are more expensive every year.

Im a PM with a big commercial tile contractor in LA, and I can confirm that our rates went up that much in recent years.

Great analysis Wolf.

Do rents ever go down long term?

They did in Tulsa when I was living there. They probably spent a decade or more going down, starting in the early 1980s. This happens on a city by city basis, not across the country.

wolf not sure where you’re getting your data but Houston is doing fine…

these are actual apt stats for Houston and they show an annual increase in effective rent of 1.3% not decrease. ALN actually calls and monitors the apts themselves NOT listings. the data from Zumper is suspect.

http://public.alndata.com/newmarketreview/HOU-177046.pdf

Apples and oranges. Your source is using a completely different measure, “effective rent.” My source is using “asking rents,” which are the current advertised rents (market rents “today”).

Your source seems to be averaging out all types of homes for rent, including single family, condos for rent, and apartments. My source is only using apartments.

I’m not sure if your source is including rents for new and still unoccupied apartments (just finished new construction), but my source includes those units as soon as they’re advertised.

The Rent is Too Damn High

Every landlord always cringes when mortgage rates fall because you lose good renters since the good renters with money become home buyers. I just lost a renter who bought and I need to find a new renter.

SocalJim is finally waking up to reality. Last month he was boasting about how strong the housing market was in Socal and how he could get $5K rent on his properties, etc, etc.

In recent posts he’s conceding that $2M+ homes and the luxury rental market are starting to soften. In six months one of his rental properties will be on fire sale. In five years he’ll be living in an apartment in Chandler, Arizona.

You have to wonder with the high level of corporate ownership what will happen, corporations don’t like to lower their prices.

These prices for San Jose just seem too high. We’re renting a 3-bed 2bath single family house for $3200 plus first one and a half months rent free. My husband can run to work in the inner South Bay.

If we move in 16 months, it’s about $3000 a month. Most landlords are making concessions like this. The rent per month is not going down per say, but it kind of is. We were not able to negotiate free months of rent before.

Of course this means we have to move in the near future. The plan anyway.

3200 per month for a 3/2 SFR is very reasonable.

Corporations will simply sell to the retail “investors” if they think the run is over.

The data points seem to suggest that in general: 1 Bedroom rents are stronger (going up more/going down less) than 2 Bedroom rents.

Could this divergence be due to millennials moving to suburbs when they have or contemplate having children?

Sales of entry level of housing has been stronger than the sales of “trade up” houses.

Comments welcome!

NativeNYer,

From what I can tell, a lot of folks who want a 2-BR cannot afford it and they make do with a 1-BR. This changes the demand dynamics.

Doesn’t rent per bedroom effect demand dynamics?

Singles who prefer to live alone, might consider having a roommate, if the rent per bedroom is significantly less in a two bedroom apartment than in a one bedroom apartment.

As someone who has rented his entire life, I would say to the data driven world that it is far more accurate to describe an apartment by its average “dollar per square foot” vs average dollar per apartment type. For example anything under a $1 per sqft in Texas is a deal. QE made Houston stupid expensive for what you get. Houston had always been a cheap town that only people born there could stomach. Why would anybody pay that much to live there is beyond me.

In my area this rapid rent appreciation has only happened over the past 3 years. The prior 7-10 rents where stagnant. Not sure they can go much higher, but they don’t really need to in my opinion If you bought the properties right!