The four account for 58% of global manufacturing value added. And the big exporters are getting hit.

The global slowdown in manufacturing progressed another notch in February. Among the top four manufacturing giants in the world, the US is the cleanest dirty shirt. Together, they produced 58% of the world’s “value added in manufacturing” in 2016:

- China: $3.08 trillion (26% of global total)

- US: $2.18 trillion (18% of global total)

- Japan: $979 billion (8% of global total

- Germany: $718 billion (6% of global total)

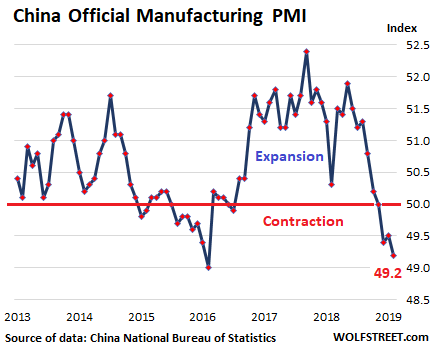

China’s small and mid-size manufacturers sink.

In February, manufacturing output declined for the third month in a row, and at the steepest rate since March 2016, according to the official Purchasing Managers Index (PMI), released by China’s National Bureau of Statistics. For these PMI measures, a value below 50 means “contraction,” and a value above 50 means “expansion”:

Small-sized manufacturers in China got hit the worst, with their PMI falling to 45.3, while the index for mid-sized manufacturers dropped to 46.9. Large manufacturers showed growth, at 51.5. And all combined, with the sub-index for employment, at 47.5, manufacturers were shedding jobs.

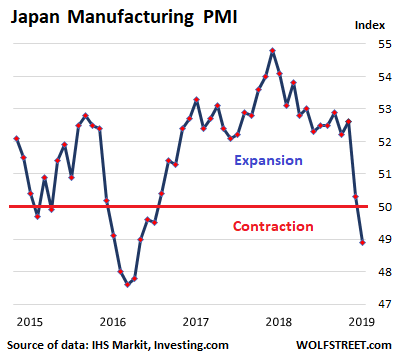

Japan dragged down by domestic demand & exports.

The Nikkei Japan Manufacturing PMI fell to a 32-month low of 48.9 in February. New orders declined at a quickened pace as new export orders continued to fall “amid lower sales to China.”

“Deteriorating demand conditions were signaled in the February PMI survey,” according to IHS Markit, which compiles the survey. New orders for Japanese manufacturers “dropped at the fastest rate in over two-and-a-half years.” And the decline in orders was “broad-based across both domestic and foreign markets, with falling new export sales also recorded.”

Businesses cut their output expectations for a ninth month in a row. The manufacturing executives on the panel cited “global trade frictions, downbeat demand forecasts, and the impending consumption tax hike” in Japan.

PMI measures are based on surveys of industry executives whose names and companies are not disclosed. These “panelists” are asked to rate various aspects of their companies – new orders, new export orders, employment, backlog, inventories, supply chain delays, input costs, etc. — by whether each of these aspects is increasing or decreasing. Their responses form the sub-indices, which are then combined into the overall headline index (the basis for these charts).

These PMIs are a quantified boots-on-the-ground view by panelists who see how their company are being impacted by economic developments. They can get outright gloomy in the run-up to a crisis, such as the European Debt crisis from 2010-2012, and have proven to be fairly accurate predictors of manufacturing data coming down the pike.

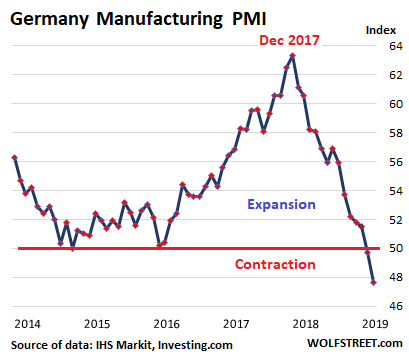

Germany dragged down by exports and cars:

The IHS Markit/BME Germany Manufacturing PMI in February dropped below 50 for the second month in a row, and at 47.6 to the lowest level – the fastest contraction – since December 2012, “showing a deepening downturn in new orders and the first drop in output in almost six years”:

All sub-indices except employment were in contraction mode. Hardest hit were the intermediate and capital goods sectors. Only manufacturers of consumer goods recorded an increase in output. IHS Market added that the downturn in new orders is “gathering pace, led by a sharp and accelerated decline in export sales. The level of new business from abroad fell the most since October 2012.”

The panelists blamed dropping car sales – a huge industry in Germany – weaker demand from Asia, and particularly from China, “Brexit anxiety among clients,” and increasing competition.

Due to the cut in output, manufacturers reduced their purchases for the fifth month in a row, “with the rate of decline accelerating to the quickest in over six years.”

But it’s not just in Germany…

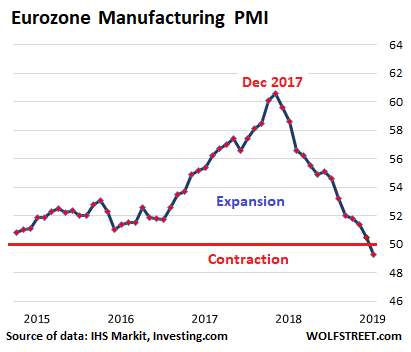

Eurozone dragged down by Germany, Italy & Spain:

The IHS Markit Eurozone Manufacturing PMI fell to 49.3. Germany led the decline. The index for Spain (49.9) entered contraction mode for the first time since November 2013. The index for Italy (47.7) was in contraction mode for the fifth month in a row, and at the lowest level since May 2013.

The chart below is on the same scale as the chart for Germany above; so you can see that the peak, and the decline from the peak, have been less pronounced than in Germany alone, with the manufacturing sectors in several Eurozone countries still in expansion mode – including in France, the Netherlands, Austria, Ireland, and Greece:

IHS Markit observed that new orders fell the most since April 2013; inventories of finished goods were rising for the fifth month in a row; manufacturers were reducing their backlogs for the sixth month in a row, “and to the greatest degree since April 2013.”

And there is a bifurcation, with a downturn in the in the intermediate and capital goods sectors, while the consumer goods sectors continued to expand, though at the weakest pace since July 2016. The report added:

Euro area manufacturing is in its deepest downturn for almost six years, with forward-looking indicators suggesting risks are tilted further to the downside as we move into spring.

Most worrying is the downward trend in new orders. Orders are falling at a faster rate than output to a degree not seen for seven years, meaning production is likely to be pared back further in coming months unless demand revives. The new orders to inventory ratio has also fallen to its lowest since 2012, with many companies reporting excess warehouse stocks.

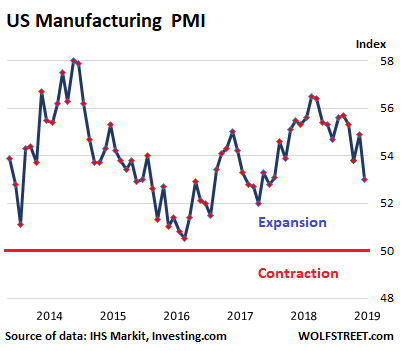

The US, the cleanest dirty shirt, so to speak:

Operating conditions in the US manufacturing sector in February showed “softer, but still solid improvement … amid slower expansions in output and new orders,” according to the IHS Markit US Manufacturing PMI. Backlogs were still increasing, as was employment. The index, at 53.0, shows the slowest expansion in 18 months, “with firms reporting a marked easing in production growth in February, linked to a similar slowdown in order book growth:

The survey “suggests that factory production and orders growth rates are close to stalling mid-way through the first quarter,” the report said. “Export markets remained the principal drag on order books.”

The manufacturing PMI from the Institute for Supply Management comes to similar conclusions – decent but slowing growth in the US, and was a notch or so more upbeat: “Comments from the panel reflect continued expanding business strength, supported by notable demand and output, although both were softer than the prior month.”

These PMIs are a scale for global demand and regional within the goods-based economy, giving an advance glimpse of official manufacturing data one or two months later. And for now, the US manufacturing sector is hanging on, even as manufacturers in China, Japan, and Germany are losing grip.

These unsettling tidbits about sudden problems on the demand-side in China keep piling up. Read… Oops, Imports by China, Emerging Asia Plunge Most Since 2008

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I seen the German PMI this morning, they are currently where they were at when Bear Stearns collapsed, by April they will be at same point as when Lehman Collapsed. It’s crazy!

This won’t be a repeat of 2016, China can’t bail out major exporters this time around, there consumers are tapped out… Things are unravelling fast

Would have been nice if the charts went back to late 90s for perspective.

I thought it would have blown up five or more years ago – I am over the end-of-the-financial-world thing at this point, just enjoying the ride as best I can.

That said, I still think a Bufford Pusser axe handle is comin’ at us any day now …

Regards,

Cooter

Lemko,

The article above features the German PMI including a chart (third chart from the top). It includes a link to the original PMI report. So take a gander above.

There is no comparison to where the German PMI was during the financial crisis, or during the euro debt crisis. It simply entered a contraction three months ago.

Comparing the US and Europe the big difference in input is energy prices.

German industry pay about 3 times as much as in the US, and it`s similar all over the EU at least compared to purchasing power. The failed “Energiewende” and the shutdown of nuclear is much to blame in this situation. The same goes for natural gas, much cheaper in the US. Also for Germany and France, Italy in particular the uncertainty about cars and technology must be taking its toll with the demonization of diesels and the uncertainty which future technology will prevail. Add to that Brexit and you have a toxic cocktail.

German public sector pay rises announced, will help domestic demand a little.

Sheer expenditure needed by automotive to electrify and automate is massive. Some stress expected as volumes shipped falling at same time. Ride share deal between Merc-BMW one response to a threat.

Germany will be keen to pivot to Russia for energy and resources.

EU looking to Africa but will threaten some EU agriculture on price so usual EU will manipulate to protect southern Europe and France. Will want Africa as a customer and supplier of only basics. Africa only close place with positive demographics for next 25 years but $/head low.

Lots of change coming.

While we are comparing Germany and the US let’s not forget that the US has four times Germany’s population, putting it comfortably ahead of the US in output per person.

This is all the more remarkable for having to to pay much more for energy.

True. China has 4.5 times US population. We are talking about growth here.

– The US can’t remove itself from the developments in the rest of the world. When the rest of the world “slows-down” then that will show up in e.g. lower commodity prices. Lower commodity prices are good for the consumer but bad for the commodity producers in N.-America.

– Lower commodity prices are going to reduce the US Trade Deficit and the US Current Account Deficit. And – contrary to common perceptions – both Deficits shrink, then that’s actaully detrimental for the US economy/financial system.

Wolf, thank you very much for your work. This site is my favorit!

The solution is obvious – Maybe Europe, Japan, and China should consider using low interest rates and QE to help their economies. After all it’s worked here in US and our Fed just told us they need will use and need those to fix future down turns. Oh…..wait……

A+ ARTICLE – THANKS !

Would have been nice for charts to go back further to get a comparison to the past two financial crises…….

No need to compare. Manufacturing doesn’t matter any longer. The new economy is in the cloud. Cloud stocks make new highs every day. It doesn’t matter people hardly understand what the cloud is.

Next up, the new generation of cult following stocks – AI, machine learning, and blockchain.

Click on the links, all charts go back to the 90s. The short form charts in the article only show this to be a correction to 2016 levels when you see the full chart in each link.

Just click those links, you can trust them on here, they won’t hurt you.

Other than our need for food and the occasional car buying, I’ve peaked on accumulating Chinese Junk (not the actual boat). In fact, we’re throwing away more at the dump than we’re buying. I’ve gotta believe there are many families doing the same. I guess that bodes well for US food manufacturers and for Mexican, Canadian and French ones, too. We’re just getting older. And maybe Indian generic drugs is on the list, too.

You are correct. Goodwill, the church, Salvation Army, the SPCA resale store are great beneficiaries of our “stuff”. Love getting rid of “stuff “. We do not even eat that much anymore. Downsizing has been wonderful for us. Kids are gone, just waiting for the dog to die now and we are free to do even more traveling. Next, get one new car, sell off the 2 and go to one is happiness for us.

Wife and I agree that the only thing that comes into our home is edible.

Don’t buy clothes anymore. In winter I wear sweatshirts and jeans. In summer I wear t shirts and shorts. Have 1 blazer and decent pants for going to special events.

Lordy, I love this!

We had beautiful furniture. Surprised that our children didn’t want it when we downsized from 3600 sqft to 1800sqft. This was expensive and quality furniture. They wanted their own.

The SPCA took what we did not want and sent a truck to pick it up.

Cannot tell you the joy of a more simple lifestyle!

This is not an advert of any kind.its information regarding all the western world having too much stuff. If you go on to the alibaba website that is called aliexpress and search for prices on say men’s watches or ladies

or shoes……. You will see the future of retail and retail property.

As I said this is from a reader of one of the best websites from MR.WOLF

BTW, it Europe, China, and the U.S. are truly interested in how to ignite economic growth for all the people (they aren’t put let’s take them at their word), they might take back their collective advice and follow Portugal’s Socialist example of spending public tax dollars on working people instead of corporations and the rich. Even the Young-ins are returning to Portugal according to this, because things are so good…maybe someone should ask Herr Angela Merkel if she takes back her words and why she things she be giving advice to actions with surging growth compared to her spectacular 0.00000000000000000000% growth rate?

“Miraculous economic recovery

It’s been more than three years since the socialist party assumed the reins of government. The scepticism of the early days has virtually vanished. The entirety of Europe seems impressed by the success story of António Costa:

The Portuguese economy has been booming for 4 years. 2017 marked the largest national economic growth of the century.

The Portuguese are not only showing the feasibility of socially conscious policies, but demonstrating the significant potential for success.

“The budget deficit has dropped to its lowest ever since the change to a democratic system in 1974 – simply because the government re-established and strengthened the social welfare state, leading to the Portuguese people having more money to spend.”

The socialists raised the once slashed wages and pensions, reintroduced paid vacations and retracted many tax raises, all while raising wealth taxes which affect only the rich parts of the population. The government also introduced a property and real estate tax designed not to target the homes of average citizens. Costa’s socialists also put an end to the catastrophic privatizations that were once instructed by the EU and resulted in selling state assets at absurdly low prices.”

It always works in the short term. I am not against what is happening in the Portugal but there is always a price to pay for social and financial engineering in BOTH directions.

Darn those commies. What will the neighbors think? NATO will have to invade on phony pretexts to ‘liberate’ the Portuguese.

Sadly, you may be true. Brussels cannot allow a success story like this to continue, for long………..

They don’t forget this

https://en.m.wikipedia.org/wiki/1980_Camarate_air_crash

which was CIA Iran contra (hostage delay maybe) , coverup. Like new right wing in Spain is/was heavily NCRI funded also raises concern . So far a clear version of for what a large quantity of military equipment was taken in Tancos then returned is waited.

CIA, Nato and Brussels sleep in the same bed, even if they don’t always like each other.

Portugal is also providing considerable tax incentives for wealthy Americans to relocate. Hmmm.

Reminds me of a Twilight Zone episode called to “To Serve Man”. Aliens brought what appeared to be a benevolent book encouraging everyone to relocate to their paradise of plenty. People were moving there in large numbers until they realized it was actually a cook book.

Portugal is still its own. The boom bust is evident in the country, so you have the remnants of was been. I say to a local “It seems a bit depressed?” and he says “People are working hard not like in the north, so it seems tired”. He is right because the crack up is illusion and the Portuguese know what they are. This is the reality that other countries have forgotten. Setarcos, another saying from Portugal is that from Spain only comes bad wind and bad marriages. But Costa government is not immune to outside, China buys infrastructure and I think they sell oil rights at poor price also, I think to US but not sure. The Portuguese are also hard done by EU, but so . Many times they were invaded in history and always ended in frustration for those that tried.

A hundred years ago, the standard of living in Argentina was the same as the US.

Most very true !

Indeed 40 years ago there was a saying in South America about that:

“As rich as an Argentine”

Till Socialism/Populism took over.

Argentineans REALLY said that in 1978?

Imagine that! And right in the middle of (yet another) Argentine military coup bringing in dictator Jorge Rafael Videla.

And all this magical stuff happening a mere 4 years before the Falkland Island war.

Somehow this sets off my BS detector.

The timeframe may be wrong!

I read it several times, didn’t Google it to be clockwork!

But still TRUE that saying.

You can Google the expression

“As rich as an Argentine”

“Tāo rico como um Argentino”

See for yourself

https://www.google.pt/search?client=ms-opera-mobile&channel=new&espv=1&ei=EN98XKiMDYyCUcTvntAK&q=tao+rico+como+um+argentino&oq=tao+rico+como+um+argentino&gs_l=mobile-gws-wiz-serp.12…0.0..14412…0.0..0.0.0…….0.FCqXoF1wdFo

This has a clear enough presentation of how that happened

https://en.m.wikipedia.org/wiki/Economic_history_of_Argentina

WW1 through WW2 was the turning point, the following protectionism and state run economy as reply then “sort of worked”, or at least was not a disaster up to mistakes in the 70s, poorly arranged liberalisation and further endless over/mis management then seems the order. I am not sure the country alone is to blame, it just could not adapt to changes in global order after WW1, though it does not seem to have done itself many favours.

In Portugal also there are some who feel the country should be shifted into gear a bit more, but really for now I think there is no great new direction available and so the country is patient and just taking care of its own.

I worked with some Argentinians, and they mentioned a few things about their economy. First, they have always really depended on extractive commodities. There were huge distortions where they protected their markets by building non-competitive manufacturing (non-competitive with imports). That was classic misallocated capital.

A part of that problem was evidently that unlike the other (mostly ag) commodities, there was not cheap energy to aid in “organic” domestic industrialization.

The government (e.g. Peron) moved back and forth with several centrally planned models, from something that was practically corporate fascism to socialism/communism over a couple of decades- again classic misallocation of capital.

There are still enormous agricultural commodity riches in Argentina. Along with a fairly well educated population.

That’s what I was told anyway.

Wolf

Fisrt of all,

Thanks for your hard work, it’s a delight to read your articles!

I barely write on the comment section, usually I’m aligned of what is writen!

But now I must say there is an “inflitrated” on the comments section

The Portuguese economy has been booming for 4 years!

Lie!!! it’s booming since 6 years, but the hard work done under the previous PM is erased, as always!

https://tradingeconomics.com/portugal/gdp-growth

Portugal is Booming right now thanks to tourism with which pillars have been launched by previous government.

But nevertheless economic numbers improving , those “poor tax-mules” in Portugal are having the worst days ever

https://www.jornaldenegocios.pt/economia/impostos/detalhe/ine-confirma-carga-fiscal-em-maximos-mas-portugal-continua-abaixo-da-media-europeia

They want to make a Florida out of Portugal, low taxes for foreigners and the “naturals” pay the big bills!

https://www.jornaldenegocios.pt/economia/impostos/detalhe/-florida-da-europa-portugal-atrai-reformados-ricos-e-divide-europeus

Public workers earn more and have more pension benefits.

https://zap.aeiou.pt/na-funcao-publica-ganha-500-euros-do-no-sector-privado-180594

https://observador.pt/2018/12/24/salario-medio-no-publico-subiu-duas-vezes-mais-do-que-no-privado-em-seis-anos/

I dream we could return to a world without confetti money and we would be able, to really see who is swimming naked.

That is why I also consider the USD the least dirty shirt.

I was an entrepreneur in Portugal, but you can’t beat them!

So I went Galt doing my algos

Kind regards Wolf

Don’t want to be negative for you but there are still a lot of Portuguese arriving in Switzerland to do gardening and farming jobs still.

Socialism works for a while but the government debt always rises that used to be a concern but doesn’t seem to worry governments or financial markets anymore.

timbers, is “Portugal’s Socialist” example not what the Greeks were/are doing for many years?

I’m still wary of manufacturing accounting stats and how accurate they are.

http://www.iariw.org/copenhagen/thage.pdf

has a look at value added and the need for proper geographic representation of activity as opposed to corporate residency.

PMI data I think is ok though.

If you think admins are past inventing new disguises then I suggest you read

3doubleudot epi.org/publication/what-is-manufacturing-and-where-does-it-happen/

which describes an attempt to have factoryless production shifted to national manufacturing accounts. That was protested and withdrawn eventually.

Not sure if you looked at the supply inventory of some commodities such as copper, zinc, nickel but they are all hitting 5yr+ lows..

Oops, that reply was meant for J.M .Keynes

Correlates with the inventory buildup?

Tax pre-funds already spent through lower withholding?

Is the US hanging in there because of reports delayed by the government shutdown?

Maybe. But the PMI is not based on government data and was not delayed by the government shutdown.

I’d be curious to know how the oil and gas industry is weighted/represented in Markit’s data. Not just production but refining as well, since the u.s. does plenty of that. If the industry has a significant weighting in the survey, it would certainly account for our

PMI being in better shape than Germany or China.

the difference from the Eu and the USA is that the US is willing to deficit spend. the EU is not. In fact, Germany has allowed its vaunted ins fracture to decay in the name of the alter of zero fiscal deficits.

“Germany has allowed its vaunted ins fracture to decay in the name of the alter of zero fiscal deficits.”

Yes. But the US too, which has massive deficits, has allowed its infrastructure to decay, and refuses to build it out and modernize it.

– The US can’t repair its infrastructure. And that’s the result of e.g. increased productivity.

– As a result of productivity growth producers can produce the same amount of goods/stuff with fewer workers. (It’s a bit more complicated that this but this is the bottomline).

– When the amount of workers shrinks then the revenues of e.g. Payroll taxes shrink as well.

You are correct, but your article was wandering why the US PMI was growing why the EU’s PMI ‘s is contracting. You can plausibly point out to the difference in fiscal policy.

I cannot believe any statistics any government wants to claim. Period.

German yield curve

http://www.worldgovernmentbonds.com/country/germany/

“Total government spending, meanwhile, has risen around 10 percent since 2014. At 45 percent of gross domestic product, it is 9 percentage points higher than in the US.” – Seekingalpha

So Germany has a large “saving” from the low rate environment (easy money) and prefers to keep its debt to gdp in slightly better order than spend even more. If or when rates rise it would be paying new costs to roll its debt if it increased it, spending is already high. That German allocation of redistribution and spending is not satisfying people is a different problem, a political one. Just printing/deficiting more is not really any solution to that beyond beyond being a roundabout way to tax people more and direct them.

FUNDAMENTALS

Seems the “fundamentals” don’t matter any longer.

At least to the markets, when they ignore basic economic signs.

The US consumer sentiment unexpectedly declined.

Month-over-month real personal consumption expenditures have crashed, back to levels last seen in… You guessed it! 2009

Some very big retail actors have announced store closings amounting to 465 closures within the past 48 hours!

Real Estate Investment Trusts (REITs) have been mauled.

The stock markets continue climbing in spite of lousy fundamentals.

Full speed ahead in equities and damn the economic torpedoes!

Sooner or later the fundamentals will matter, because… Well they are after all fundamental.

http://www.dlacalle.com

Fundamentals?

You may ask timbers!

Yields

USA 10y = 2,75%

Portugal 10y = 1,5%

Don’t know if I should Laugh or Cry!

Demographics are important. The populations in both Germany and Japan are skewed towards older people who have enough manufactured goods already, and China is close behind – although they’re still catching up on consumption.

In the US, the millennial generation is relatively large, and still need to set up households. They may be held back by student debt and a poor job market, but that is still their goal. So we should see better demand for a while.

German GDP = $3.677T

German gov debt = $3.677T x 64% = $ 2.35T

German 2018 CPI averaged = 2%.

German front end & mid of the yield curve = (-) 0.5%. All rates under 8Y under water.

The German gov pay investors : $2.35T x (-) 2.5% y/y = $(-) 58.8B,

or : investors are paying $58.8 B to park their money for the safety of Germany, in 2018.

The German economy is not safe, because their export = 37%

of GDP. Most Germans rent, have little RE assets.

Wolf, your blog is getting better, covering a wider spectrum, hope

u do well.

Couldn’t find any technical or troubleshooting contact link on your site; so, I hope someone reads this:

I see your “please turn off AD Blocker” message each time I visit your site, and each time I make sure AdBlockPlus is set to not block your page, but I always get the message and I never see any ads. “Whitelisting” your page also doesn’t make a difference. Refreshing the browser also does nothing.

Today I disabled AdBlockPlus altogether and the “please turn off AD Blocker” message disappeared, but THERE ARE STILL NO ADS!!

Very strange…

I am using a recent version of FireFox on a 32-bit Win 7 PC and I don’t see any reason for this – though I’ve seen the same behavior on a couple other financial websites.

And ideas?

Firefox started blocking nearly all ads by default a few years ago.

However, we do not use “please turn of Ad Blocker” messages. I don’t know what you’re seeing there. But it’s not from us.

The US is not a manufacturing giant. A manufacturing giant does not run enormous manufacturing trade deficits with China, Mexico, South Korea, and other countries.

It’s a manufacturing giant alright — second largest in the world. But it’s also the largest economy, and is importing more than it exports. Smaller economies China, Japan, and Germany are exporting more than they import.

Wonder how real some of these manufacturing numbers are. I hear companies bring in products that are almost completely ready and just do a few assembly steps in the US, which counts as local manufacturing.