But deposit-taking banks have pulled back.

Lovingly known as “shadow banks,” nonbanks have come to dominate the mortgage market. And they originate the riskiest mortgages. The government — mostly the Federal Housing Administration (FHA) — is on the hook. Nonbanks do not take deposits and are not regulated by banking regulators (Federal Reserve, FDIC, and OCC). Their funding is derived mostly from selling the mortgages they originate, but also from bank loans and other sources. During the mortgage crisis, a slew of them got in trouble and, because they did not hold deposits, were allowed to collapse unceremoniously.

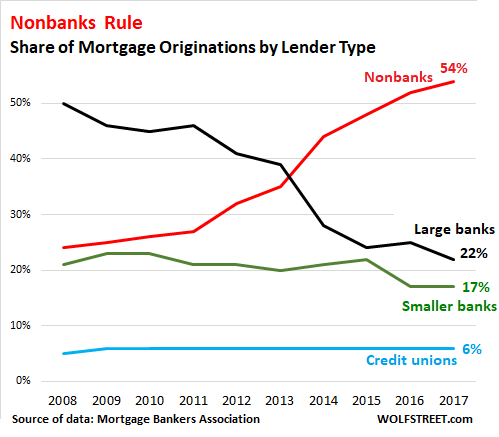

Today, there’s a new generation of shadow banks dominating mortgage lending. According to a February 2019 report by the Mortgage Bankers Association, the share of mortgage originations by nonbank lenders has surged from 24% in 2008 to 54% in 2017, while the share of large banks has plunged:

The largest nonbank mortgage lender, Quicken Loans, originated an estimated $86 billion in mortgages in 2017, according to the MBA’s February 2019 report, giving it a market share of just under 5% of all mortgages written during the year.

These shadow banks are unlikely to get bailed out in a crisis, and investors will take the loss. From that perspective, taxpayers are off the hook. But their counterparties are also at risk of losses – with the government by far the most exposed. These counterparties fall into two groups:

Large banks extending “warehouse financing” (short-term credit lines secured by mortgages) to nonbanks to fund the mortgages temporarily until they’re sold into the secondary market.

The US government, through government agencies such as the FHA which specializes in riskier mortgages that it insures and guarantees but does not buy, or Ginnie Mae which buys and guarantees mortgages; and government sponsored enterprises Fannie Mae and Freddie Mac which buy and guarantee mortgages.

In its wide-ranging report and briefing materials (February 25, 184 page PDF) on the housing market and government involvement in it, the American Enterprise Institute (AEI) outlines how surging home prices push lenders to take ever greater risks. And as deposit-taking banks have pulled back from those risks, shadow banks have plowed ever deeper into them.

I will focus on a small aspect of the report: The increasing role of shadow banks in the mortgage business and the exploding role of the FHA in insuring and guaranteeing their mortgages that are becoming riskier and riskier.

FHA insures mortgages on single-family and multifamily homes to high-risk borrowers. It operates on the revenues it receives from the mortgage insurance premiums that borrowers pay upfront and monthly. To qualify for FHA insurance, mortgages must meet certain requirements. When homeowners default on their mortgages, the FHA covers 100% of the lender’s loss. It currently insures nearly 8 million single-family mortgages and about 14,500 apartment buildings.

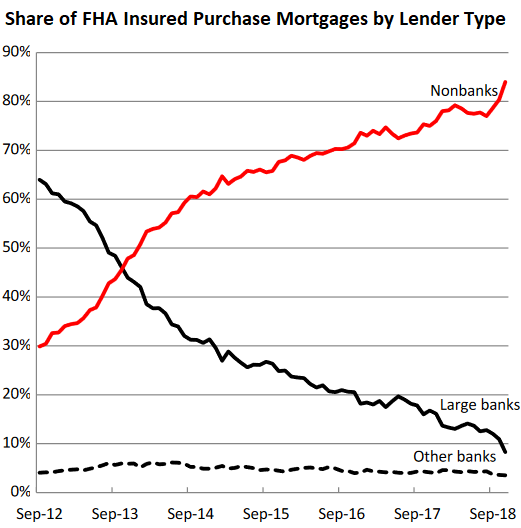

The chart below by the AEI shows how nonbanks completely dominate FHA-guaranteed “purchase mortgages” (we’ll get to “refinance mortgages” in a moment). The chart excludes mortgages by State Housing Finance Agencies and Credit Unions, accounting for 4% of the FHA purchase-mortgage market. In November, the share of originations by nonbanks of FHA-insured mortgages surged to 85%:

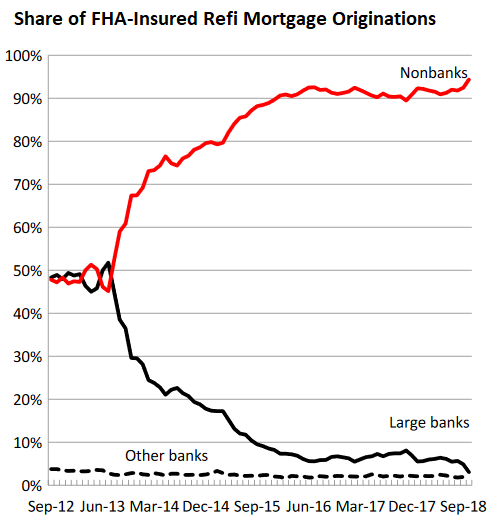

In terms of FHA-insured refinance mortgages, the shift to nonbanks is even more striking. In 2012, nonbanks and banks originated about the same volume. By November 2018, nonbanks originated 94% of all FHA-insured refi mortgages:

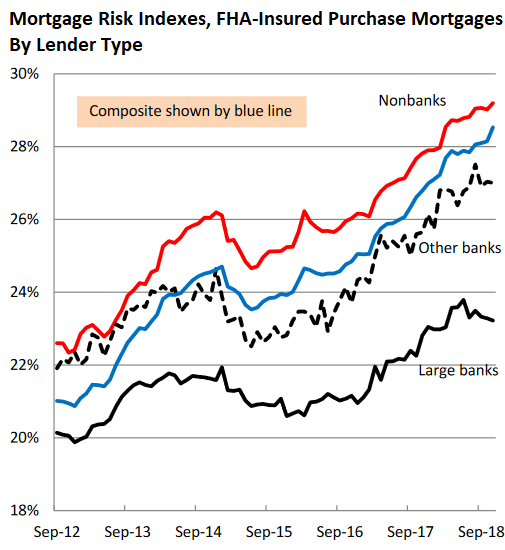

“Migration to nonbanks has boosted overall risk levels, as nonbanks are willing to originate riskier FHA loans than large banks,” the AEI says. This is shown by two risk measures.

The first is the Mortgage Risk Index (MRI), a stress test that measures how the mortgages that were originated in a given month would perform if subjected to the same stress situation as mortgages originated in 2007, which experienced the highest default rates as a result of the Great Recession.

The AEI’s chart shows how risks of FHA-insured purchase mortgages, as measured by the MRI, have risen across the board, but much less at large banks than at nonbanks:

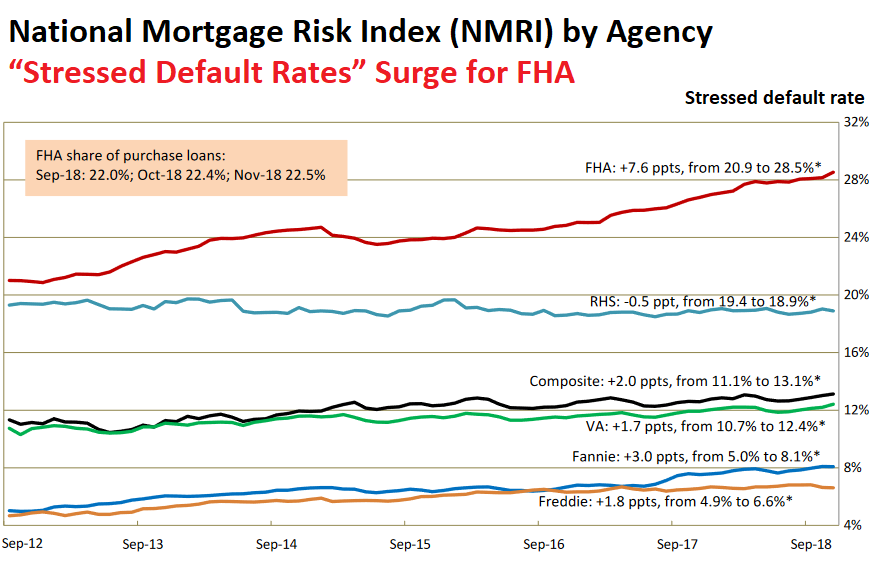

The second risk measure the AEI uses is the National Mortgage Risk Index (NMRI), a standardized quantitative index for mortgage default risk based on the performance of the 2007 vintage loans with similar characteristics. NMRI is expressed in a percentage, the “stressed default rate”:

- A higher rate means increasing leverage and looser lending standards and therefore higher risk of default;

- A lower rate means decreasing leverage and tighter lending and therefore lower risk of default.

The composite NMRI (black line in the chart below) has been trending up since mid-2013, with all agencies except the RHS drifting higher. While Fannie and Freddie guaranteed mortgages are at the bottom with stressed default rates of 8% and 6%, the stressed default rate for FHA-insured mortgages have surged, including a 7.6-percentage-point jump over the past 12 months, to 28.5% (click to enlarge):

Since nonbanks originated most of the FHA-insured mortgages over the past few years – in November, 94% of all FHA refi mortgages and 85% of all FHA purchase mortgages – the “stressed default rate” for the FHA reflects mostly the risks of mortgages originated by nonbanks.

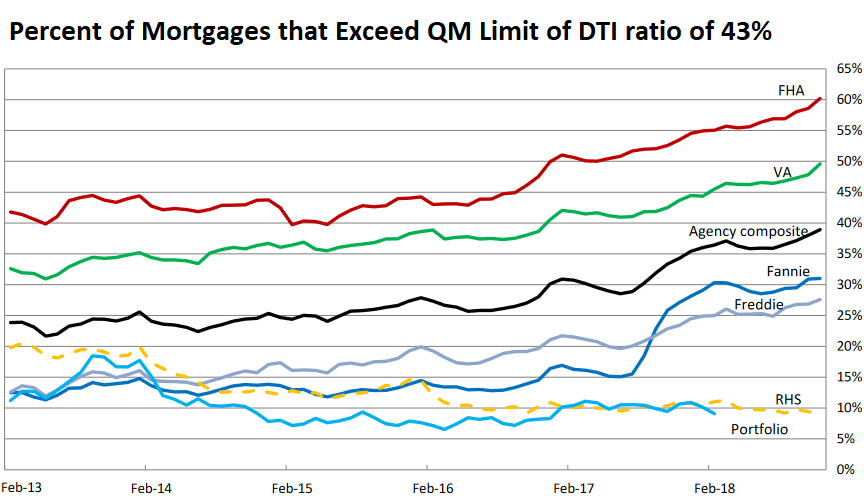

The debt-to-income (DTI) ratio shows a similar scenario. It gauges the ability of a borrower to repay a mortgage by measuring the income consumed by servicing all outstanding debts of that borrower.

The upper limit of the DTI ratio for “qualified mortgages” (QM) under the Dodd-Frank Act is 43%. A mortgage that meets the QM requirements provides legal protection for lenders against a claim that the mortgage was made without due consideration of the borrower’s ability to repay. But Fannie Mae, Freddie Mac, FHA, VA, and RHS are exempt mostly from the QM requirements, and so here we go:

- In November, a record 60% of FHA-insured purchase mortgages exceeded the QM limit for DTI.

- 50% of VA mortgages exceeded the QM limit.

- But Fannie and Freddie mortgages are well below the limit, at around 30% (click to enlarge):

So there are two dynamics that would be needed for future support of the housing market, according to the AEI:

- Accelerating household incomes

- “Further increases in leverage from an already high level.”

The first has been arriving too slowly and has been outpaced by home price inflation; and the second – increased leverage – would have to happen at the low end of the household-income scale where the FHA and shadow banks are most active, and where the risks are already the highest, and the borrowers the most vulnerable.

The San Francisco Bay Area and Seattle lead with biggest multi-month drops in home prices since 2012; San Diego, Denver, Portland, Los Angeles also show declines according to the Case-Shiller Index. Others have stalled. A few eked out records. Read… The Most Splendid Housing Bubbles in America Get Pricked

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

They are gonna need to charge a lot more than 200bps over 10Y to make money. I’m not sure how they make it. Even if they get money at the wholesale market at > 2.4% there is not that much spread left.

Look at an amortization schedule, you’ll see how they make money.

I have tried looking at a few, there are some standard non-payment fees/conditions and queries .. but was not able to find any “exploiting” clauses or of fishy nature. I wonder what am I missing. Can you please point out ? thanks.

Are you guys referring to the premiums FHA collects?

If so, 1.75% of loan amount up front (financed into the loan), and 80-85bps annual premium, collected monthly.

When a bank or financial holding company has a mortgage origination subsidiary, is the mortgage sub considered a nonbank since it’s legally distinct from the depository institution?

I don’t believe so, as the bank itself is the investor to many of the mortgages (aka they “balance sheet” the loan).

That’s not to say the bank is the investor on every loan. The bulk of originated mortgages, even by large banks, are sold to Fannie Mae, Freddie Mac, or institutional investors.

However, the banks usually keep loans that don’t conform to the above mentioned investors standards if they are deemed safe as a profit center. Depending on the bank, this could make up a majority of the originated mortgages, or a vast minority. It depends on the bank’s business model.

In 2014 roughly 21% of non-agency RMBS mortgage loans were delinquent by more than 5 years. Meaning these mortgagees had skipped paying their mortgage payments for over 5 years! Long term delinquent.

By 2015 62% of these delinquent mortgages had been modified.

When a loan is “modified”, it is no longer considered to be delinquent.

However, roughly 40% of these modified loans are now re-delinquent.

An estimated $160 – $200 billion of these delinquent loans are on properties that are likely still underwater after more than 10 years!

So that big real estate lump in the snake, is slowly working its way through the system.

As a citizen lobbyist during the Global Financial Crash, I told the WA legislature there will be Crash II, and all the loans being modified with large balloon payments will be in foreclosure again. The Elected, responsible for the horrible WA Foreclosure Fairness Act, looked me in the eye and said, “Yes, I know.”

So, there it is. Your Electeds could not give a sh!t about the vulnerable populace.

I wonder about all the rocket mortgage radio ads I hear. But how economical can they be for the middle level class of buyers to consider such an option. It would be interesting for a home buyer in the middle range to do a comparison. Either it is comparable to the real banks or it isn’t.

Our mortgage is currently with a third party. I wonder how the banks decide when to sell off these mortgages.

In the 4 homes I have owned over the years, my mortgage has been assumed/re-assumed 11 times from the original lender. Not one was with my permission. Just another poker chip in a high stakes game.

I think you want to get your mortgage to high ground. (whatever that takes).

Not sure what it means to be on high ground… my definition is paid off.

But is there any real difference between a bank vs a 3rd party loan unit?

Insightful commentary and original thinking. Truly thoughtful

– Right. And those banks have to go out and borrow the money they are lending out. That’s fine as long as Mr. Market is willing to lend those shadow banks money.

– Is there any sign of rising interest rates for those lenders in the bond market ?

“These shadow banks are unlikely to get bailed out in a crisis”.

Quicken Loans. Quick-in Chapter 11?

Another bummer for the good citizens of Detroit if Housing Crash 2.0 happens.

Didn’t Charles Schwab partner with Quicken Loans? Wonder how that affects everything?

https://www.schwab.com/public/schwab/banking_lending/mortgages/faqs_popup.html

I doesn’t look like Schwab puts any of its own money up for mortgages in this partnership – probably just marketing with a small commission.

You would think that customers with brokerage accounts would be a better credit risk, too…

I just want to know ultimately how does this affect the bottom line?

Bottom line: college basketball is broken.

-Dick Vitale

Not as broken as these dodgy mortgages it would seem ;)’

Why does the USA government gives insurance to these risky mortgages anyway? I am sure ince the defaults start that will be one of the questions asked.

Because at the end of the day the Government employees don’t pay, the Banks don’t pay (in fact they both get paid), the taxpayer does pay.

The FHA’s official mission since the Great Depression has been to advance homeownership among low income borrowers. It has stayed as such through various democrat and republican administrations. Basically it’s official government policy to provide this insurance.

Since the housing meltdown and the disappearance of private mortgages the FHA has pretty much been the only game in town as far as making loans to, oh, let’s call them “credit challenged” populations.

As long as the housing market has been on an upswing as it has been for the past 7-8 years it’s been great for the government as it has been collecting insurance premiums without too much to pay out. However, in the next recession the taxpayer is likely to take a gigantic hit on FHA and Ginnie Mae morgagaes (Fannie and Freddie will probably survive the next downturn as they have much stricter qualification standards).

Max Power

Insightful explanation (ie government policy); frankly, I didn’t realize that.

My question would be how many times do American taxpayer have to go thru the high risk, low underwriting standards time machine just to give low income people (many of whom apparently can’t afford home ownership) yet another shot at the brass ring?

As per Einstein “The definition of insanity is doing the same thing over and over again, but expecting different results”.

Actually, it hasn’t happened yet.

In prior crises there was plenty of private mortgages available to these individuals and as such the massive losses were not all guaranteed by the government.

And while yet there was some government guarantee in place, the fact that the goverment has cornered basically the entire mortgage market since, coupled with the housing market’s robust recovery has meant that taxpayers have more than made up for any monies lost during the housing meltdown through insurance premiums on that “cornerned” market since.

The problem will come during the next recession becuase unlike last time, this time basically ALL subprime mortgage lending now is government guaranteed.

Fannie and Freddie will probably limp along but in the long run survive this cycle due to their more stringent qualifications and the fact that the current housing bubble, as bad as it is, in real terms is actually still not as bad as the previous one.

The FHA and GNMA on thier other hand, with their super-loose lending standards and teensy weensy downpayment requirements will likely not survive and it will be interesting to see how the politicians handle that hot potato. This said, this would be the first time that the goverment owns this entire market segment so the real insanity as you describe it is really only about to begin.

One should note that there is no doubt that by guaranteeing these subprime loans, the goverment has contributed greatly to the housing “recovery” itself by providing an important marginal source of housing demand to the housing market from a significant number of house buyers that would have otherwise would have likely not participated in it. Since the last crisis, fully-private lenders won’t touch these “credit challenged” buyers with a 100-foot pole. This may have helped the housing market just as much as those ultra-low rates gifted to the market by the Fed.

This whole situation BTW is not unlike the student loan market as well where the goverment pretty much took over the entire market too since the financial crisis.

So, basically, it’s all about the gubbamint nowadays. Now so far given the recovery it’s actually worked out in the government’s (and by extension, taxpayers’) favor but this situation of the goverment owning the ENTIRE market across all risk profiles hasn’t been tested in a downturn. That is yet to come. To prepare, I suggest taxpayers begin practicing bending exercises now. The skills acquired will likely come very useful later.

Taxpayers need to begin

Taxpayers will be on the hook for as long as mortgage origination companies are allowed to bribe Congressmen.

The answer to your question is: “Not until working people are allowed to organize unions (something that currently exists on paper only) and remedy the gross imbalance in national income and political power between Capital and Labor.”

When that happens (not that I’m holding my breath, since mainstream Democrats want it no more than Republicans) you’ll see far fewer mortgage delinquencies, foreclosures and related financial panics.

It’s no accident that the “Golden Age” era of post-WWII affluence, home-ownership, declining inequality accompanied tight regulation of Finance, and saw no financial panics/crises.

This article

https://www.rstreet.org/2018/01/04/what-have-the-massive-guarantees-of-mortgages-by-the-u-s-government-achieved-2/

explains it quite well. It is a model, the question is is it a good model. The trouble I have with it is that it offers a means, along with rates, to completely financialise housing as an asset. Sure people go along with it, some for profit, others because they have to, but the result is that housing inflation becomes a major source of money entering the economy, and that gives a tremendous leverage to policymakers over how society perceives the wider economic reality. There is quite some moral hazard in this.

Only AGENCY debt is guaranteed by Uncle Sam. PRIVATE MBS isn’t.

That’s why Lehman Bros. collapsed. They were issuing private MBS based on sub-prime.

Federal mortgage insurance primarily benefits creditors and sellers.

The borrower gets stuck with a note on inflated asset prices.

Honestly the federal government should abandon the FHA/VA loan programs and just build more public housing or increase Section 8 subsidies. Those folks have no business borrowing that kind of money and they don’t even have the room in their budgets to properly maintain the houses they are financing.

With all due respects, I know a dozen VA Loan individuals. They may not be well off financially, but have earned a chance in home ownership through their service. Not one of them has defaulted on their contract.

So quick to comment and not think first. *****Nice reply by Dawns early light!! Well said. Not everyone is deadbeat like the 6 time bankruptcy expert who is supposedly a ‘President’.

Many people dont make high incomes and pay their bills on time. Such cannot be said for many rich or in power can it….

It’s kind of interesting b/c VA mortgage are 0 down and have similar underwriting standards to FHA; high debt to income ratios and lower credit scores; but, have a pretty low default rate.

Not sure why that is? More discipline for the vet?

Raxadian:

“Why does the USA government gives insurance to these risky mortgages anyway?”

To support Free Market Capitalism! LOL!

Let’s face it, nonbanks are just a new way for large banks to make money out of dodgy mortgages with less risk than last time. They’ve found a legal and regulatory loophole and piled in. And with less directly attributal responsibility and less risk than last time, the lending standards will be ignored to an even greater degree as the end approaches.

Who set these nonbanks up? Who’s on their boards? Why are the large banks so happy to lend to them?

*Who set these nonbanks up? Who’s on their boards? Why are the large banks so happy to lend to them?*

That should be the questions answered in a different Wolf Street report.

In fact Wolf could make it into one of his youtube podcasts.

TruckMan,

For example, the largest one, Quicken Loans, was set up back in the day… In 1999, Intuit bought it. Then in 2002, Intuit sold it to Rock Ventures, Dan Gilbert’s investment vehicle, which continues to own it, and Gilbert is still the chairman.

Thank you. Looks like the Quicken Loans team have been there a long time. I suspect they aren’t the problem. It’s the post 2009 dudes I am concerned about.

Just the government’s idea of crony “free” markets hard at work!

This explains why mortgage lenders like Citizens Bank is offering CD rates ,25% or above Treasury Direct.

Well don’t let Broker Dan see this. Everything is awesome.

Maybe you have wrong guy? I find Broker Dan’s comments very balanced and informative. In fact he made the point the other day that if you have a problem with all the risk being put on taxpayers then you need to look at the GSE’s and VA and FHA guidelines.

Lenders are just exploiting a dumb system that is guaranteed by design to run itself up and over a cliff.

Or, as the 184 page AEI report concluded, we could solve the problem by having everyone accelerate their income!

I absolutely NEVER said everything is awesome. I merely explained how the lending side works and also commented on the difference in loan quality now vs the previous run up to the crash. Furthermore, loan quality is only 1 variable in the overall picture as it relates to housing and a crash.

I am not in any 1 camp: crash vs to the moon. Although I hate when someone reads 1 article in relation to lending when the author knows very little on how it really works and begins to spread mis-information.

While I do know a good amount about lending; I do not claim to know everything and just try to inject as much factual information on the subject as I can.

Broker Dan,

Meant to say this earlier… Thank you for chiming in on mortgage questions. Mortgage issues and rules are complex. And it’s good to have a mortgage broker on board, so to speak :-]

Quote:

During the peak years, private label MBS issuance topped $1 trillion. In 2017, only $70 billion of private label RMBS were issued, although that is a big increase from 2016.

Looks like the GSEs have the whole mortgage market. All we are talking about are the originators or servicers. They don’t keep the risk.

What is the total dollar value of risky mortgages -I- and other taxpayers are involuntarily insuring via FHA?

1.4 t according to the article I linked above.

Also Fannie, Freddie and Ginnie back 59% of all mortgage debt according to that …so no picking on FHA maybe…?

The lending guidelines for FHA are set by FHA and are universal

regardless of who originated the loan. If the loan does not get an

automated approval through FHA’s AUS system it cannot be booked. So to

say the problem is broker led or shadow bank led is not right. Non

bank lenders and brokers dominate the mortgage industry because they

are customer oriented. The large banks are disastrous in that

department. Because the large banks cannot compete with small banks

and brokers they constantly shift the blame for mortgage issues to

them and lobby to put us at a disadvantage. The gateway to approval

runs straight through FHA. If they want to mediate risk they can alter

the AUS system.

JimmyO,

Bingo.

Imagine the difference between going in to a DMV office and sitting all day and filling out paperwork and waiting in order to re-new your license

vs

Completing a renewal license online in 5 minutes.

Thats big banks vs streamlined brokers/lenders.

Best charts ever Wolf. For people nearing retirement who have been on the REFI cycle for a long time, what do they do? I just don’t believe that when mortgages are repackaged to investors that they are firewalled off from a wave of deleveraging. The courts tried (vainly) to address the problem last crisis, I think this time they will. (and Congress will not be creating new bailout packages) No matter how you slice or dice your chickens, they come home to roost. Even with low interest rates falling asset values will cause a wave of readjustments (bank notices to come up with more collateral) Berkshires earnings were down 90%, but he still has Quicken and WFC.

Why do I keep seeing people say the government is not going to do a bailout next crisis? Why wouldn’t they?

They won’t have to bailout any banks since the banks don’t have any exposure this time. What Obama did was socialize this exposure so that it is directly on the taxpayer. Trump has made it even worse by reducing lending standards. Everybody wants to keep the water swirling in the bowl as long as possible. Because once reality sets in, the current national will have to double or triple to keep housing prices at their current levels.

How did Trump reduce lending standards? Please elaborate?

Please cite source.

Dale,

I will help you; the opposite happened. I remember as I am in the industry.

In late 2016 and early 2017, HUD (under outgoing Obama) was planning to cut FHA mortgage insurance premiums which would have made payments cheaper and increased purchasing power (also cutting FHA’s income stream) but the Trump administration put a freeze on that plan and after close examination scrapped it. This basically was the opposite of loosening standards.

This is the telling nugget within the context of this post:

“In November, a record 60% of FHA-insured purchase mortgages exceeded the QM limit for DTI.”

At 40% DTI people are pretty much locked into debt for the rest of their lives. If you have ever seen these balance sheets it is pretty alarming unless there is some form of big payday in the future – inheritance, lottery, etc. So FHA in November made 60% of their business from people who can never hope to pay back what they have borrowed.

The “large banks” have mostly limited themselves to making QM loans. Sure they make some non-QM loans in their wealth groups, but are largely avoiding anything but QM after all the payouts and grief when the housing bubble burst.

JimmyO and BrokerDan there is a lot of paperwork and steps in a QM, but at least the large banks aren’t the ones burying people in debt they will never be able to payback. Securitize them if you’ve got ’em.

Can’t comment on the trapped in debt forever statement; however, here is the QM rule, and it’s not bound by 43%:

https://files.consumerfinance.gov/f/201312_cfpb_mortgage-rules_fact-vs-fiction.pdf

To be a Qualified Mortgage, the loan:

• Cannot have excessive upfront points and fees;

• Cannot be longer than 30 years;

• Cannot have certain risky features, such as paying only interest and not principal, or paying less than

the full amount of interest so that the total debt grows each month; and

• Must be in one of three categories:

1. The monthly loan payment, plus the borrower’s other debt payments, does not exceed 43

percent of the borrower’s monthly income; or

2. The loan qualifies for purchase or guarantee by a government sponsored enterprise (Fannie

Mae or Freddie Mac), or is insured or guaranteed by a federal housing agency; or

3. The loan is made by a small lender that keeps the loan in portfolio.

You can blame broker and wholesale lenders or “shadow banks” all you want, but, the truth is that they ONLY adhere to Fannie Mae, Freddie Mac, and FHA guidelines. These lenders will NOT lend outside those guidelines; and those are ALL QM mortgages.

Now many lenders have their own “overlays” or internal company rules that further layer risk; so, not all lenders will lend on QM eligible files due to risk.

Lastly, it would be interesting to see a history or graph of DTI (debt to income ratio) lending parameters over the past few decades.

Just so I understand, you are saying that the lenders are all making QM loans, but that a QM loan does not have to meet the 43% DTI threshold (and is free to exceed it as long as it still qualifies for purchase or guarantee by a GSE). Am I getting that right?

Correct.

Is the DTI ratio using “gross income” for its calculation?

In addition, is this DTI ratio using front end or back end calculations?

Yes; Gross always.

This is the “back end” ratio; which is the new PITIA + all other debts on the credit report and any other court mandated debts (alimony, child support, etc..)

PITIA = Principal , interest, PMI, taxes, insurance, HOA

To further clarify this topic of DTI and credit score underwriting. Not ALL loans with low credit scores and high DTI’s are approveable. What I mean is that lenders MUST run these loans through a universal computer algorythem called Desktop Underwriter, which is developed by Fannie Mae. It takes the entire financial profile of the buyer and the details of the transaction into account and renders a decision.

If it’s a decline; the loan is not happening b/c lenders (for conventional) will not close a manually underwritten loan where Desktop Underwriter doesnt approve. With FHA and VA it is more flexible in that lenders can manually underwrite them but to a more stringent degree with added layered risk guidelines.

Here is an example:

Buyer attempting to purchase a 700k property

20% down

640 credit score

40% DTI

The desktop underwriter (DU) declined the loan and therefore the buyer CANNOT use conventional financing to purchase the property. The algoryhtym just didn’t like the credit profile (depth, tradelines, etc…)

Another aspect of FHA to ponder is that it is a bridge to conventional. What I mean is that nobody keep FHA loans for the life of the loan. Why? B/c when you only do 3.5% down the PMI is for life and most borrowers want to get out of that, so, they focus on the issue that kept them from getting a conventional loan.

Meanwhile, once they refinance, FHA gets a windfall. See below scenario:

My buyer that has 20% down but avg/poor credit profile got declined conventional and now must go FHA. But, with 20% down once he fixes his credit profile (with my help) in 5-6 months, he can refinance into conventional and eliminate over $400 PER MONTH in PMI.

So; let’s see what FHA made off the deal:

1.75% 1 time up front PMI = roughly $10k immediately

0.85% annual PMI = $5100/yr so after 6 mos; FHA got around $2500.

So; FHA received $10k + $2500 for helping this borrower get the house and then get into a conventional loan. Not a bad deal.

I see a lot of buyers start with FHA to get in the door; and come back in 6 mos to a few years ready to refinance into a standard conveitonal loan.

So, FHA certainly is useful in many respects.

Having dealt with banks and non banks (loan depot) I find the non banks to be FAR more efficient, direct and easier to communicate with than bureaucratic banks (who seem to always put their PC hired people to deal with customers, barely literate and only able to read from script).

And I’m talking here about simple conforming stuff.