San Francisco Bay Area & Seattle lead with biggest multi-month drops since 2012; San Diego, Denver, Portland, Los Angeles decline. Others have stalled. A few eke out records.

San Francisco and San Diego are catching the Seattle cold, and others are sniffling too, as the most splendid housing bubbles in America are starting to run into reality.

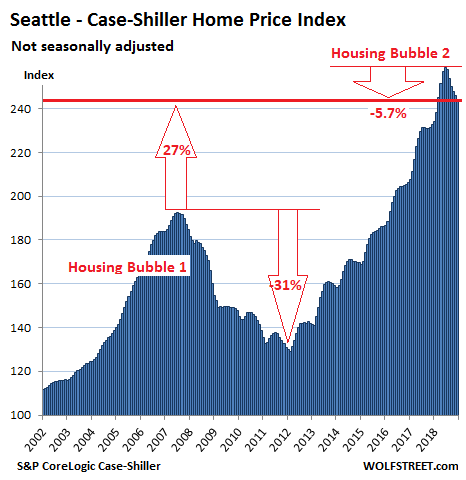

House prices in the Seattle metro dropped 0.6% in December from November, according to S&P CoreLogic Case-Shiller Home Price Index, released this morning, and have fallen 5.7% from the peak in June 2018, the biggest six-month drop since the six-month drop that ended in February 2012 as Housing Bust 1 was bottoming out. The index is now at the lowest level since February 2018. After the breath-taking spike into June, the index is still up 5.1% year-over-year, and is 27% higher than it had been at the peak of Seattle’s Housing Bubble 1 (July 2007):

So Seattle’s Housing Bubble 2 is unwinding, but more slowly than it had inflated. Many real estate boosters simply point at the year-over-year gain to say that nothing has happened so far — which makes it a picture-perfect “orderly decline.”

San Francisco Bay Area:

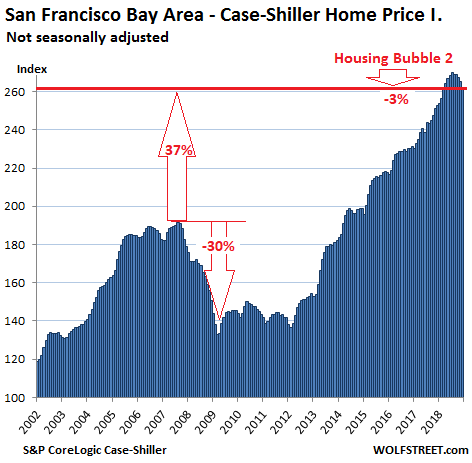

The Case-Shiller index for “San Francisco” includes five counties: San Francisco, San Mateo (northern part of Silicon Valley), Alameda, Contra Costa (both part of the East Bay ), and Marin (part of the North Bay). In December, the index for single-family houses fell 1.4% from November, the steepest month-to-month drop since January 2012. The index is now down 3% from its peak in July, the biggest five-month drop since March 2012.

Given the surge in early 2018, the index is still up 3.6% from a year ago and remains 37% above the peak of Housing Bubble 1, fitting into the theme of a perfect orderly decline:

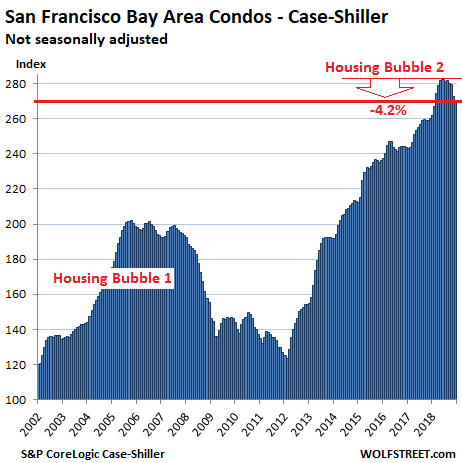

Case-Shiller also has separate data for condo prices in the five-county San Francisco Bay Area, and this index fell 0.9% in December from November, after an blistering 2.4% drop in the prior month. From the peak in June 2018, the index has now dropped 4.2%, the steepest six-month drop since February 2012:

The Case-Shiller Home Price Index is a rolling three-month average; this morning’s release tracks closings that were entered into public records in October, November, and December. By definition, this causes the index to lag more immediate data, such as median prices, by several months.

The index is based on “sales pairs,” comparing the sales price of a house in the current month to the prior transaction of the same house years earlier (methodology). This frees the index from the issues that plague median prices and average prices — but it does not indicate prices.

It was set at 100 for January 2000; a value of 200 means prices as tracked by the index have doubled since the year 2000. Every index on this list of the most splendid housing bubbles in America, except Dallas and Atlanta, has more than doubled since 2000.

The index is a measure of inflation — of house-price inflation. It tracks how fast the dollar is losing purchasing power with regards to buying the same house over time.

So here are the remaining metros on this list of the most splendid housing bubbles in America.

San Diego:

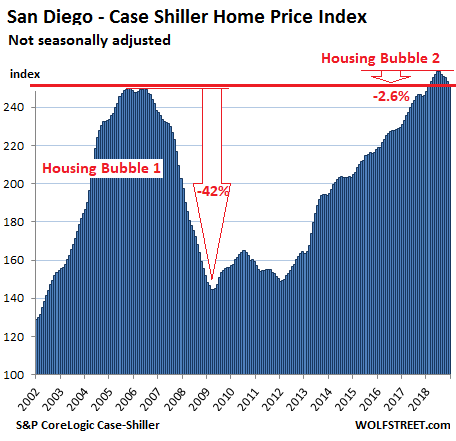

House prices in the San Diego metro declined 0.7% in December from November and are now down 2.6% from the peak in July, the biggest five-month drop since March 2012, leaving the index at the lowest level since February 2018, and just one hair above the peak of Housing Bubble 1:

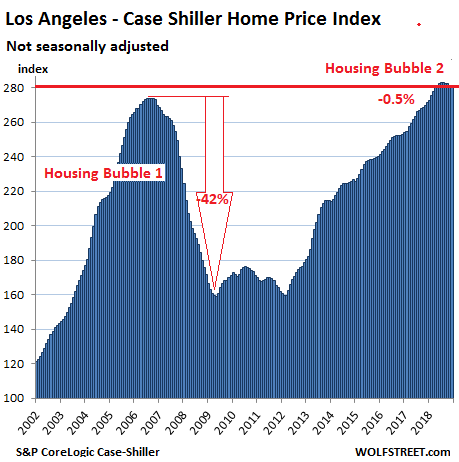

Los Angeles:

The Case-Shiller index for the Los Angeles metro was about flat in December with November but down 0.5% from the peak in August — don’t laugh, the largest four-month decline since March 2012. What this shows is just how relentless Housing Bubble 2 has been. The index is up 3.7% year-over-year:

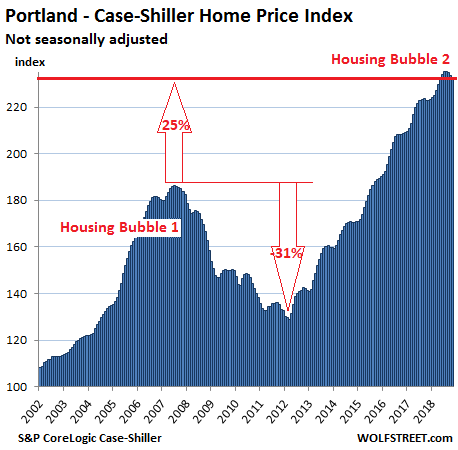

Portland:

The Case-Shiller Index for the Portland metro inched down in December from November for the fifth month in a row and is now down 1.4% from the peak in July 2018. And that was the steepest five-month drop since March 2012. Year-over-year, the index was up 3.9%:

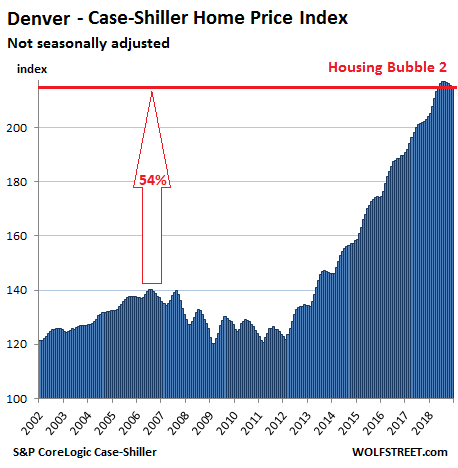

Denver:

House prices in the Denver metro edged down in December from November for the fourth month in a row, after an uninterrupted 33-month run of monthly increases. The four-month drop amounted to 0.9%, which, you guessed it, was the steeped such drop since March 2012. The index is at the lowest level since May 2018 but is still up 5.5% year-over-year:

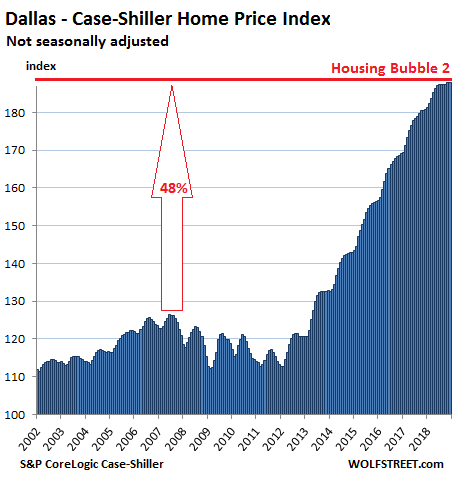

Dallas-Fort Worth:

The Case-Shiller Index for the Dallas-Fort Worth metro in December ticked up by less than a rounding error to a new record, leaving it essentially flat for the seventh month in a row. The index is up 4.0% year-over-year:

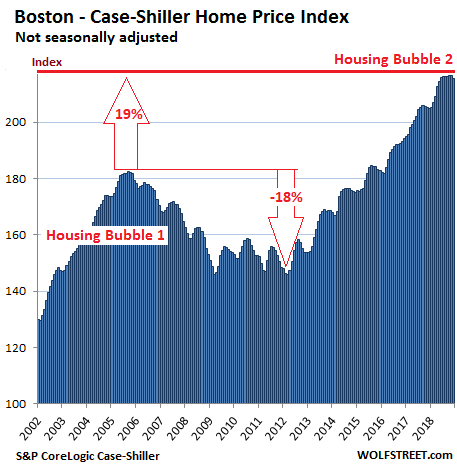

Boston:

In the Boston metro, house prices dipped 0.5% in December from a record in November and are now back where they’d been in June. The Case-Shiller Index is up 5.3% from a year ago:

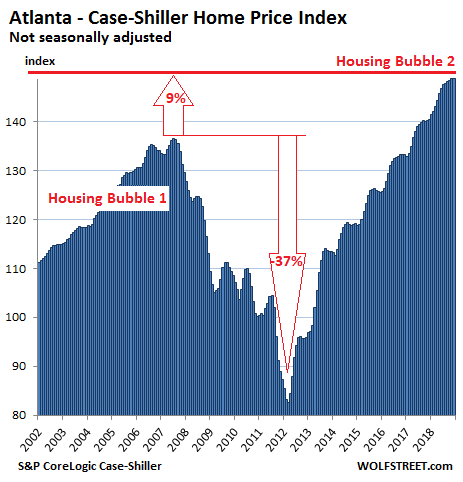

Atlanta:

The Case-Shiller Home Price Index for the Atlanta metro inched up a smidgen in December, to a new record, and is up 5.9% from a year ago:

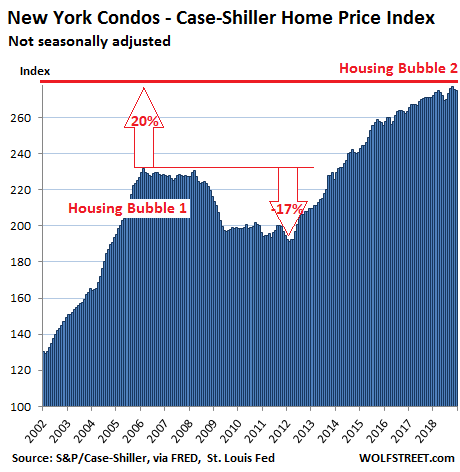

New York City Condos:

The Case-Shiller index for condo prices in the New York City metro ticked down in December for the second month in a row after a mighty bounce in September and an uptick in October. This index can be volatile, but after all these bounces and declines, the index was up just 1.5% from a year ago, the smallest year-over-year price gain on this list of the most splendid housing bubbles in America:

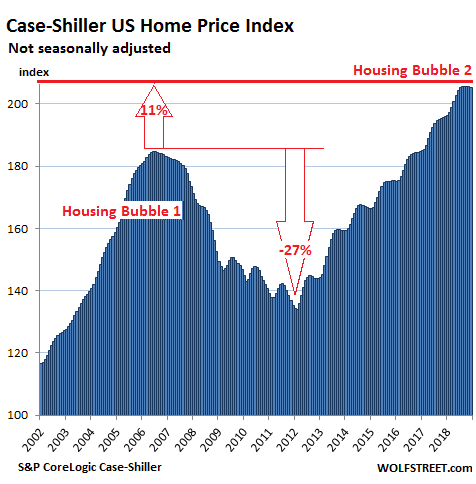

On a national basis, these individual markets get averaged out with other markets that didn’t quite qualify for this list since their housing bubble status has not reached the ultimate splendidness yet. Some of those markets, such as the huge metro of Chicago, remain quite a bit below their Housing Bubble 1 peaks and are now declining, while others are shooting higher.

So the Case-Shiller National Home Price Index has been about flat since July, but is still up 4.7% year-over-year and is 11% higher than it had been at its prior peak in July 2006 during Housing Bubble 1:

It always boils down to this: Regardless of how thin you cut a slice of bologna, there are always two sides to it. When home prices drop after a housing bubble, there are many losers. But here are the winners – including a whole generation. Listen to my latest podcast, an 11-minute walk on the other side… THE WOLF STREET REPORT

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Any knife catcher who buy now deserve what’s coming. Housing Bubble 1.0 is the “Fool me once, shame on you”. Housing Bubble 2.0 is “I’m an idiot if I buy now”.

I am waiting for SoCaljim to put on the positive bravado spin on this…

But the fed will come in with qe!!!!!

Confucius say net worth of man who catch falling knife gonna lose digits.

not everyone in the market now was in during bubble 1. i have a feeling a large amount of millennials are gonna be the ones caught off guard. not saying its an excuse for them skipping the research but theyre more on the “fool me once, shame on you” stage. just a thought.

My question is, who is willing to buy into an orderly decline?

The People who have no reason to fear an orderly decline are usually those buying their last Home or people who simply have enough $ that it doesn’t matter.

Will it stay orderly? How much will it decline?

I’m happy to. For the same reason people buy stock on the way down. You don’t know where the bottom is and eventually it will turn around.

In my metro, I don’t see how the price collapses long-term:

-Crime and poverty pushed those who could afford it into enclaves protected by high prices; these people have a strong voice and protect their turf.

-Outside these neighborhoods, the municipality actively acquires or condemns and demolishes older and larger structures to reduce police, fire, and public works costs and is resistant to any dense development out of fear that the cycle will be repeated.

-Almost nothing new is built unsubsidized by some level of government, directly or indirectly, apart from some single family homes and far-flung apartments.

-The “middle class” moves to ever-farther out new constructed bedroom communities with an expensive commute.

-These new subdivision are much harder to develop than 15-years ago because costs have outpaced what people can afford and speculative projects are much harder to finance and nearly impossible to without overly involving the local politicians

-The price ratio between a respectable starter home and a ranch spec in the sticks has move from 2/1 to 3/2 (i.e. the price difference has narrowed because people can’t come up with that the last 50k they need).

From what I read in the academic journals, this seems to be a common narrative. I think prices will move lower like a bond would as conditions tighten, but I can’t see a collapse.

Look at Australia or Canada….people there were saying the same thing in 2017.

Regardless of how thin you cut a slice of bologna, there are always two sides to it. : ]

On an aside are these still mild declines the result of the QE unwind, cheap credit beginning to dry up, consumers finally beginning to wisen up, investors getting cold feet, all of the above, or none of the above?

Rising interest rates + QE unwind + new tax laws + Mel Watt retiring = the beginning of the housing bubble imploding

I prefer the term correction, implosion sounds too ominous. : ]

That was before Trump forced Powell (hammerlock behind the back) to do a complete 360.

You do realize that a 360 puts you right were you started right?

Pretty certain bologna can be carved into continuous Mobius strip with a single side, thin or orherwise.

I still think we are going to see an uptick heading into Spring with choppiness the rest of the year. I believe the Fed is going to do anything and everything it can to keep the market afloat. They still have rate cuts and QE to help them control rising interest rates. Even since their recent capitulation I have seen an uptick in listings going pending and the open houses I’ve attended have been pretty well attended. Of course, whatever the Fed does is not going to work in the medium term because, even with rock bottom interest rates up and down the yield curve, the bubble at its current level is about at the limit that many high earning professional couples can afford, and many folks like myself will balk at what they get for putting down a very large down payment and still having an enormous mortgage. When I see a seller who bought within the last five/six years trying to walk away with double what they paid, or a cool $500K (the markup I often see on SF condos), I just roll my eyes and move to the next listing. I’ve waited this long, I can afford to wait another few years for the real bottom. Once the demographic shift really starts taking place, watch out…

I agree with you except change real estate to stock market. Powell’s 180 turn from Pretend Hawk to Dove had nothing to do with cross currents & uncertainty related to trade or whatever his latest double speak is. We know this, because that existed for some time prior to his flip, yet he did not act until – and only until – Mr Market did it’s allowed 10% hissy fit. And Powell will obey Mr Market again – and again and again, each time relaxing rates and QE each and every time Mr Market commands him to.

I can’t listen to him anymore. One week they are well below the range of neutral, and the next week they are patient. One week he doesn’t care about Trump, and the next week he does exactly what Trump wants. He’s a lying mouthpiece who only creates more uncertainty as his plans change with the market.

The funniest part of his testimony was when he was talking about the US being on an unsustainable fiscal path. Gee Jerome, not something that you and your bubble addict buddies at the Fed helped to create, right?

Exactly! He is like someone babbling about fire safety one minute and throwing gasoline on the fire the next minute. How can anyone have the slightest respect for these guys? Or listen to their pompous nonsense without laughing in their faces?

@timbers-

>Powell’s 180 turn from Pretend Hawk to Dove…

Powell said that debt is rising faster than GDP, much faster. That admission alone should ring fear in the heart of main street especially with a recession looming.

He may be talking like a dove, but he is still commiting to 2 more rate hikes this year. IMO This thing is going south before year end.

Is this just a slowdown, a correction, or are looking at an impending correction?

That’s how markets move, not in smooth waves.

This housing market is not similar to the meltdown we experienced in the US in 2007-2010. The banks did not give loans to NINJ borrowers during the past 10 years. While I agree it is a buyers market in some submarkets, please don’t wait for the floor to fall out. Do your homework and if you need a place to live make numerous offers and buy a house.

It’s different this time…

There are multiple ways to inflate a bubble. If you give a bunch of “qualified” borrowers a 10% down jumbo loan with a shadow bank at a very low interest rate, which is very prevalent in CA, you will drive up housing prices while keeping payments relatively low. However, you can only drive them up so far before the payments are no longer low, and before those people no longer have 10% to put down. That is a very perilous place to be as a market. One shock to the system and that shiz will crash.

Where I live in southern california the discounted housing in 2012 was mostly bought up by institutional money and foreign money. Individual Americans couldn’t even get loans. It has since rapidly reflated and these investors have done quite well. Now its two income professionals spending >50% of their after tax take home pay on their mortgages. You can only rationalize that if you think it covers your retirement. Economic downturn? Employment disruption (of even just one partner)? Capital flow reversal toward Asia? All three? Look out below…

CNBC front page: “Beijing’s capital controls are weighing on Chinese investors looking to buy property abroad“

That explains the CA and Seattle trend more than mortgage rates, IMO. That is also the wild card as to whether this is an orderly decline, or if said investors are forced to sell to bring money back to China. If that happens, you’ll have some real fireworks.

Good luck to the shadow banks giving those 10% down loans at low rates. I live in FL and I am used to see those those 10% down loans at high rates with mortgage insurance. Apparently the shadow lenders in CA have a different model than the rest of the country.

Timothy, even at 10% down rates from places like Quicken have been way below historical norms, i.e. less than 5%. Yes, the borrowers have to pay mortgage insurance and they do until they can’t.

Check here: https://www.nerdwallet.com/mortgages/mortgage-rates/jumbo

I believe Quicken is the largest jumbo mortgage lender in CA and their average down payment for jumbo loans is 10% down.

There is a lot of mis-information happening here in regards to lending.

As a mortgage broker (and direct lender) let me clarify.

The 10% down jumbo programs are actually typically offered by Big Banks: Chase, US Bank, Citi, BofA, Wells

Need 700 min credit score and 43% max debt to income ratios (all total debts vs gross income)

You usually need reserves as well: 6-12 months.

That will get you a current rate in the mid 4’s w/ NO PMI

Have a lot of assets to transfer under Big Bank management; you can get a lower rate or get an “exception” for something outside of normal guidelines.

The jumbo market is dominated by the big bank players, NOT “shadow banks”.

Quicken is NOT a player in this sphere; they live in the conventional and FHA world.

The “shadow banks” or wholesale lenders do not lend hold loans; they have large credit lines through big investors and fund the loans according to Fannie, Freddie, FHA and VA guidelines; and then sell the loan to their investor (secondary market). They don’t make up guidelines, these are created by Fannie, Freddie, FHA and VA. Got a problem with their guidelines? Go to those entities.

These wholesale lenders do need to practice “responsible lending” or they could get buy-backs for poor quality loans or have their HUD approvals cut and no longer able to lend on FHA. They absolutely serve an important function in the market by providing liquidity and a more streamlined process vs big banks. Think in person DMV vs. online registration renewal.

Lastly; almost all loans in the past 10 yrs have been underwritten according to VERIFIABLE income AND stable employment. 2 elements that were non-existant in the previous run-up. If you think employment and income stability is worse now than 10yrs ago, then that’s fine as that is a debate worth having; but, loan quality is NO COMPARISON to what it used to be. Trust me; I see it all day every day.

“…loan quality is NO COMPARISON to what it used to be.” Since about year 2000, you mean. Go back further and you have PMI for ANY loan under 20%, while conforming loans have more than quadrupled since 1980, for example. So jumbo loans now start at $450K plus vs. $93K. Do you think that that provision may have had something to do with the massive housing inflation that has taken place?? And, debt to income levels were maxed at 35%, give or take, back in the day, not 43% as now. So, it appears that loan standards have declined while loan amounts have vastly inflated. It’s nice to know that income is again being verified. Whew.

For the “free market” ninnies, they only have to look back a few years to learn that, if there were really a free market, the financial industry would have completely blown-up the economy years earlier. Regulations keep the trains running on time, in spite of the invisible hand voodoo.

Hownow – you cannot compare any of the last fifty years as being free market. The invisible hand is just a way of saying how you choose how you choose. Market managed choice vs. political managed choice. I understand votes are free, but maybe they aren’t worth as much as made out.

Bankers,

“Free markets” probably came to a close with the first civilization, maybe with the rise of the Sumerians. Since then, it’s been a pipe dream and used by lobbyists, of one stripe or another, to rationalize things they want rationalized. Time to stop pretending .

@Broker Dan – thank you for the thoughtful and insightful reply, although I am not spreading mis-information. Please see this article: https://seekingalpha.com/article/4189254-irresponsible-mortgage-lenders-created-second-housing-bubble

SoFi was the lender I was thinking of, and apparently they are not subject to the same regulatory framework as traditional bank lenders. I believe I saw an article at one point that SoFi has a large (maybe the larges) portion of CA jumbo loans with 10% down and “flexible” DTI. I also wonder whether they included equity comp in the DTI calculation, as that picture can change quickly with a stock market crash. Have to wonder about the qualifications at a place like that.

Bottom line there are plenty of HENRYs (highly educated not rich yet) with good credit scores, student debt and 10% down jumbo mortgages in CA. It may be a smaller group of people inflating the bubble this time (on much lower volume), but that doesn’t mean there is not a bubble in the absence of NINJA and Liar loans. I believe the HENRYs are at their limit and even a blip in interest rates will make many go underwater. A job loss recession will crash the market as all the headwinds come to bear.

This market can maybe party on in 2019 but eventually the real price will come due. I believe The 2020s are not going to be pretty for housing especially with the oldest boomers approaching their 80s.

Something is telling me that HowNow is a New Yorker, greatly inflating the importance of the role of infallible government officials and presidential decrees which tend to benefit the NYC businesses, which should be commodities. Yes, driving up home prices to record levels benefits everybody and is a good long term strategic plan for the country, right?

I think that this time it will be worse than 2007-2010. We don’t have NINJ loans but incomes ( including high incomes) are much more fragile than they were 12 years ago. But the big difference is that last time banks, and investors buying up distressed housing for use as rentals put a floor under the market. This time the overbuilt rental glut ( well documented here on Wolfstreet) will foil a price floor based on rentals.

How Now,

You may be right as I cannot comment on the industry pre-2002 (I was in college at that time), however, I have heard conflicting stories from friends and family on the “tightness” of underwriting guidelines back then.

I.e. “when I bought my first house….”

Broker Dan.

This time is NOT about no income loans go bad. This time is about double income lose one or two jobs because? You guessed it. Lots of businesses are fake money losing business that will NEVER turn profitable and these “insolvent” zombies create jobs because of “liquidity”. In short, verified income is fake and NOT lasting just as last time’s NINJA. This time is NOT about subprime go bust, this time is about middle class becomes subprime.

Broker Dan, so you think 2008 was a time where both NINJAs went bankrupt and middle class got hit at the same time and “this time in 2019”, we only have middle class squeezed working for zombie companies without NINJAs, therefore 2019 is much better than 2008?

I have news for you.

What saved 2009? China pumped trillions, deflated the world, FED ZIRPed and went Betserk on QE123, EU was still holding together.

This time? the disease is the same. Debt/GDP in 2019 is more than 2007 world wide. But the cure is much less. Central banks have 0% and 2.5% to work with and in 2009, they have 5% to work with and they had lean balance sheet.

Not only CBs have less to work with, unlike 2009 when the world was cooperating and China was leading the reflation, nowadays, the counties are trying to break each other. Cooperation becomes competition.

There is more. Who bought the houses in 2012? Invitation homes, American Hines for Rent…. They swollowed all the single family inventories that should have flooded the market. SFR renting is a lousy business and it can NOT be scaled like apartment complex. How can those companies make it work? ZIRP and leverage. Once ZIRP stops, their business model breaks. Who is going to swollow their inventories? Thise millions of houses that should have flooded the market in 2012 would flood the market 10years later.

And there is more. 10 years ZIRP not only created those single family rentals, they also created lots of money losing businesses or businesses running on bubble demands. The economy is rotten to the bone and the market will creash if it is left to investors. Market now must be managed by politics using coercive forces or it will crash on its own debt.

Now you still think 2019 is better than 2008 simply because there is NO NINJA loans?

Clay Dennis – This is absolutely right. From 2009-2011 we had trouble finding rentals in DC and were hit with 5%-10% rent increases every year. That drove us to buy in 2012 and the rest is history. We sold in 2018 because we were scared the market was going to implode given all of the headwinds and the fact that there is now a glut of luxury apartments all over the country.

We are just going to keep moving from one 2 month free rental deal to the next until there is some sort of clarity as to what the hell is going to happen with the housing market after 2-3 years of price discovery. This is a scary time to bet on housing especially when plenty of luxury rentals with resort amenities keep hitting the market.

JZ,

There was a huge job loss event in 2008. The crash of the financial system plunged the economy into major recession which further ate away at the housing market.

I on the other hand see contract engineers on 6-month contract and no green card buy close to a million dollar houses. Must be the above average credit scores.

That’s not happening; please don’t exaggerate. Show me the lender offering a loan on that situation.

Look up places like Livermore or Mountain House, CA. I know numerous examples like this situation. Houses go for 750-850K. People even take second morgage for downpayment on the first mortgage.

Broker Dan – no loans are involved, it’s suitcases full of cash.

I don’t know how it’s happening but it’s common in my neighbood (Dublin, CA). Many foreign workers in my neighborhood (90% purchased by foreign workers). They start at $900,000 and with a few “upgrades” are purchased at $1,000,000. My next door neighbor works for a large company as an engineer and she said her company gave her the down payment for her home, provided she signs with them for x years (I think it’s seven). Another neighbor indicated the same at an HOA meeting.

How many need someone to help with a down payment? That would be an interesting stat. Can’t be a good thing.

There’s a sucker born every minute. Don’t be one.

Very true comment.

Yes on lending

Yes on housing as a place to live

Yes if it fits your budget and you plan on being there long term go for it.

My reply was to: Timothy J McLean

“This housing market is not similar to the meltdown we experienced in the US in 2007-2010”

Yeah, it’s even worse. Unless you think the corporations that bought houses in mass in some of the bubbliest cites are going to hold on to depreciating assets…..couple that with the mom and pop “investors” that took 2nd’s to buy that rental property (I know a few) and we have the exact same scenario only worse. Nobody can really afford a house (90% of the people I know couldn’t buy the home they live in now with the incomes they make) and falling prices means everyone heading for the exits.

Not to mention demographics which is a another topic that will be putting pressure on prices.

Lastly, when and IF (who knows if the FED will throw more welfare at RE) the reductions get bad enough then the skeletons will be coming out of the closet on WTF is really going on in some markets. I wouldn’t be surprised if it turns out money laundering has been rampant.

I just had this conversation today actually.

interesting – I also suspect money laundering has been a contributing factor in the top tier of every major metro area. The number of sales over $1.5M certainly isn’t supported by local incomes or any other fundamental.

It’s also pretty amazing how fast the party suddenly came to an end. Late spring 2018 was gangbusters and then by Fall everyone sobered up at the exact same time all over the country. The entire run up and cool down seemed WAY to orchestrated across the country at peak employment.

“This housing market is not similar to the meltdown we experienced in the US in 2007-2010. The banks did not give loans to NINJ borrowers during the past 10 years.“

End-user shelter buyers aren’t the principal problem and never were regardless of loan quality. It’s all due to the speculators who don’t even live in the houses and will walk away from loans if they feel they’ve made a bad bet. You could also argue that if the last bubble was more “democratic “ and helped along by all the NINJA borrowers, then this one is even more vulnerable to a rapid collapse because it has been blown up to even more absurd levels by a much smaller pool of participants.

Those investor loans require substantial down payments, not, like the speculation in 2002-2008, where you could speculate with no “skin in the game” aka 0 down programs.

I don’t doubt there are flippers or investors that buy based on assumed appreciation, but, know that those loans have a good amount of Equity built in at closing due to down payment requirements.

Hate to disagree, but prices in many areas are above 2007. It is not subprime that implodes a market, its speculaton. We have plenty of speculation in this market.

My observation is that yes housing prices will decline lower but will still remain higher than previous cycle lows.

That is simply because it takes a bigger wheelbarrow to cart the increased amounts of devalued paper money needed to buy a house thanks to constant central bank money printing!

In other words, inflation hard at work!

This is why I look at the CS index CPI adjusted. I completely understand why Wolf does not do this, since it conflates two types of inflation, but I find it useful because it reflects more closely what I’d feel out of pocket compared to the last bubble.

“This is why I look at the CS index CPI adjusted”

the amount I can charge and bill hasn’t adjusted for me in decades, not even close to inflation no matter how you count it.

And I know quite a lot of folks just like me so why bother “adjusting” anything…….that $400K home is just as expensive now as it was in 2000…….just saying.

I know quite a few folks *not* like you. Some people are seeing inflation, others do not. Look at prices curves across sectors over time… Healthcare and education = inflation. Computers = deflation. Seems reasonable to consider the aggregate load of price changes over time when considering the biggest purchase most people will make.

CPI is the wrong measure to adjust home prices with. The CS is itself a measure of inflation – house price inflation.

What you need to compare it to is wage inflation because that’s what is relevant to housing costs.

And not the national index, which is irrelevant, but the local indices, so for example, compare the Seattle CS index to Seattle household incomes; and the San Francisco CS index to San Francisco household incomes.

Pretty good point.

Kinda like all RE is local, wages are local.

Yes, I know your stance on this. Like I said, I understand why *you* consider this invalid and my comment was clear that using CPI conflates two types of inflation measures.

But it is useful, whether or not you agree. Since they are two different measures, using CPI allows you to see house asset inflation normalized by the aggregate price changes (to the degree you trust the numbers). Like any statistical normalization it is an effort to isolate the true signal by removing noise. You could use DPI, sure, but that is more properly used as a predictor… the rate of change, not absolute value. Also, it is noisier because of legal changes over time.

Of course… you look local when you are interested in local. You look national when you are interested in national analysis. There is a reason these exist: https://fred.stlouisfed.org/series/CUURA423SA0

WES – You will do well to bet on long term deflation. The number of bankruptcies that will occur over the next 30 years will be staggering. Housing values have been inflated by massive amounts of debt that will never be repaid. The frantic rush to pay down debts will cause a liquidity crunch and real estate will go up in smoke.

Detriot is a great preview for what will happen to the rest of the country over the next 20-30 years.

I often look over the recent sales column on Zillow here in Portland. Right now the only things that are selling are fair condition family homes with prices below the FHA limit and above a million dollar homes that are in perfect condition, with slick renovations and large price reductions. The listing pages are jammed up with new homes being sold by the big builders that are not moving at all. The market is flooded with inventory and is just waiting for something to push it down the stairs. I think when the oncoming glut of rentals comes on the market late this spring it will shake things up.

What is the glut of rentals in Portland? New apartment buildings like Seattle, or are you talking about SFH? If the latter, why do you anticipate a rental glut. Just curious. Thanks.

Portland is just like Seattle in overbuilding of apartments, it is just behind a year or so in time. The number of new basic and luxury apartment buildings coming on line in the next 6 months or so is astounding. We are already at the 2 months free stage and many new buildings that have already come on line are 50% empty or relying on Air BNB to keep the tumbleweeds out of the halls.

According to the Oregon Office of Economic Analysis (OEA) and wolfstreet, there’s a glut in luxury apartments in the Portland area (consistent with my anecdotal observations, towers with high rents are going up like dandelions), while more affordable housing is drying up. However, according to the data ALSO published by the OEA population is also on the rise and building permits are falling, meaning that even if luxury apartment sloughs into the rest of the rental market and lowers rent for a time we’re still butting up against a shortage.

SRC: https://oregoneconomicanalysis.com/2019/01/29/oregons-housing-supply/

Thanks Wolf, I love it! Finally it looks like San Diego is actually beginning to correct to something realistic. This spring will be interesting as I doubt there will be an uptick here. I expect that the flippers have seen the writing in the wall and the rest of any would be buyers are happy to sit in the sidelines waiting for some sign if bottom.

Once we pass the spring buying season any it sinks in that the buyers aren’t there then we will see a real correction. Bring it on.

SD down 2.6% from the peak is not necessarily a “correction”, but, something to keep an eye on.

Real estate market is like a titanic unlike stock market

Its gonna take few years

People are sick and tired of these prices despite very low mortgage rates and supposedly strong economy and historically low unemployed rate

Let’s see when then recession hits

I do not see San Diego correcting all that much. Reason being is there has been no construction boom. San Diego still has a massive housing shortage and no new construction in the pipeline. It also has a very stable employment base. Cities where construction has been going gangbusters is where I believe the huge corrections will occur.

According to CoreLogic, the median price of a San Diego County home was $542,000 last month, up from $529,000 in January 2018

Well, you know what a New York City bargain is: A residence that is worth ~$250,000 gets reduced from $3 million to $1 million. I think it would take the 4 horsemen of the apocalypse galloping thru Times Square to drive down housing costs here to reasonable levels that would support a healthy middle class. This city is becoming a third-world nation where everyone is either supremely rich or dirt poor.

Speaking of Zillow :

I saved 25 Seattle Townhome listings (excluing new construction) between 10 and 12 days ago. These were mostly fresh listings that went to market within the previous week.

The only criteria i used was 2br and 3br resales between $200k and $700k.

What i see :

4 of those 25 homes have gone pending as of this evening. Keep in mind that all of these listings are at least 10 days old.

Also, not all pending sales make it to closing. Plus, Seattle had a week of snow in the prior week that should have created pent up demand during the last 10 days.

Lastly, mortgage rates have been inching down over the last couple of months.

I find this quite troubling for the recent condo buyers in Seattle.

I can see possible Principal reductions and home loan modifications on the horizon.

What else will US.Gov do ?

My nephew graduated from UW last spring, got a job at Google, started in November and purchased a $2.7 million condo downtown Seattle. His dad gave him $100,000 for a down payment; Google gave him money as well. We were visiting him when he received the news that he DID NOT qualify to refinance his mortgage. The game is take out some money on the equity. Part of the problem is that the value of his condo went down 12% so far. Also, his dad is trying to sell his Lake Washington home for more than he paid for it. He’s getting multiple offers, but at least $1,000,000 below what he paid for it. This is an interesting observation. Don’t know if it’s the trend or just another anecdote.

What’s his starting pay?

Florida country club communities that require memberships are getting crushed. Buyers have to pay cash for the memberships because they can’t be amortized + sellers dumping RE just to recoup the refundable part of the memberships

Does this have anything to do with the fact that the upcoming “water hazards” are going to be the whole golf course?

Nah. The owners in the golf communities down here won’t be alive when an inch of rising ocean shows up.

Also, interestingly, most of the “best” golf communities are way inland (at least here on The Other West Coast)…so that threat is a long, long way away.

From Bloomberg:

“More than 800 golf courses have closed nationwide in the last decade, as operators grapple with declining interest in the sport and a glut of competition. Many of those shuttered courses were built on land proscribed from redevelopment by local zoning codes seeking to preserve open space—”

https://www.bloomberg.com/news/features/2016-08-15/america-s-golf-courses-are-burning

My son-in-laws family are all golfers. They have mentioned the collapse of developments for at least 10 years….all over north america.

A golf course location is definitely NOT a selling feature for RE. I presume this goes for other un-named golf resort developments more political in nature. :-)

The full retirement lifestyle “appreciated” on the front side of the boomer retirement cycle, especially with those Boomers who had generous pensions and health care packages.

As these early retirees are dying out, or being moved to assisted living, the pool of available replacement buyers has drastically shrunk for various reasons. Many are still paying off their first homes. Others have multigenerational households back home, so are unable to move to Florida.

Finding the bottom will be interesting because a lot of these communities (e.g. Naples) exist almost solely on retirement incomes. There are no “median income” jobs for younger folks who would want to move there.

Rowen, the better jobs are growing here, but only in specialized fields like medicine and, surprisingly, IT. It’s still cheap enough here that remote work is growing quickly.

What you say is right, especially about Naples. Everything west of the highway (not just on the Gulf) is overpriced elite/gated, and most everything east of the highway is jungle.

An eye-opening link Paulo – I had no idea!

There is a strong cognitive dissonance in American culture regarding house prices. On one hand everyone recognizes the benefits of low housing costs like any other living cost to the population at large. On the other hand many Americans have a large part of their wealth tied up in their house or don’t want to hear they bought a depreciating asset using $100s of thousands in borrowed money. A much larger part of the U.S. population would benefit from affordable housing prices, which would be considerably lower in almost all areas nationwide.

A good deal of this is blowback from the government shutdown.

I live in the SF Bay Area, born and raised. I was sitting at a cafe on Courtland street in Bernal Heights neighborhood of San Francisco which once was a diverse community of people and cultures, but has become extremely gentrified to high income mostly tech people. A real estate person was talking to a couple about some housing options for them. Among the many things she talked about how SF is “so much safer now” and “the schools are improving” she talked about how home prices don’t come down. The couple was asking about a “housing bubble” and why homes go on and off the market so often. She talked about her properties being connected to bio-tech. She said her clients come to the SF Bay Area for high paying jobs buy a house for 5 years and sell it when they get a better offer some where else. She said the same is for other tech areas in SF. Its clear Bay Area is the magnetic for high paying tech jobs. I wonder if there is a shake up in the tech world (Bio, social media, etc.) how much influence will this have in the housing market in San Francisco? Will there be a shake up? Also, how much is the giant VC money that poured into Silicone Valley and Bay Area connected to all this talk on this site about the FED and the money they have allowed to be pumped in this country at some low interest rates? Thank you

Personally, I know a lot of “tech” people. They are not making all that much money. The Bay Area people keep talking about the tech millionaires, but, normally, that is not the case.

Most tech people buying homes in the bay area are struggling for a down payment, are getting the largest mortgages possible, and are stretched making payments for 30 years. That is what is going on in the bay area.

Jim I have to agree with you on this one. 500K double income households buying 3 million, does max out mortgages. A linked-in/facebook couple literally dumped all their income and get 2.4million 3bed in Palo Alto, 1.4million in Mountain view and that’s NOT enough, they get another 1.4million house in Santa Clara to rent as well. They literally went through all the banks in order to give them loans for the 3rd one. Yes, 500K couple levered to get 4.8million, with two rented out. Let’s long houses, short dollars, why? Because inflation will increase rent, because inflation will give you salary raise, because everybody wants a piece of bay area so let’s front run everybody. Let the Uber’s, Lyfts IPO suckers spent all their IPO money prying a house out of my hand.

JZ – that sounds like an irresponsible couple. I don’t know many couples who are levered basically 10:1. However, I know plenty of $600K + income couples, and $1.5 million – $2 million place for them in SF is not unreasonable. That is the price point for most couples I know in that income bracket. That is why I think RE in the Bay Area will stay more elevated than other markets even in a downturn. Long term the Bay Area is one of the greatest spots on the planet and there is so much money here.

When I was young, I levered up a bunch of fixers near the beach. In the end it worked out and I am wealthy. But, let me tell you it was a rough rough ride. Twice I was living on fumes … almost went bust. Not until this last real estate rally did the money pile up. But let me tell you … it was a big bet and now that I am just several years short of the 50 year old mark, I am glad to be semi – retired. But, i don’t recommend my approach to anyone. I lived with nothing for 26 years to get to this magic place. Many or perhaps most people that followed my game plan would have gone bust.

There was a guy working for SiPort back in 2008. He levered up and he shot his CEO, HR, VP the day he was fired. Roadkill, right? Here is the thing about over levered strategies. If you play it multiple times going through all kinds of scenario like Depression, two world war, 1970 inflation, 2002 crash and 2009 recession, those overleverred stratigies will fail you. But everybody just live once. If you are lucky, over lever can make you rich. If you are NOT lucky, you are the road kill.

Income X 3 to 3.5 for a house is prudent and will serve one well. In bay area, none-IPO W2 earners are paying income X 5 to 7. Is this the rich place awash with money or is this a prison for debt slaves hoping they will be able to transfer wealth from the IPO folks?

Atherton California, the richest zip code in US has “average” house hold income of 480K. I know 600K double income families exist, but how many are there? I know some but I also know all the people sleeping under bridges, street with feces and syringes, preschool teacher keeps moving and takes on 3 hour commutes because they can’t afford a place to live in bay area. The inequality makes me worry.

The US census data shows very few households in the Bay area making 500k. To say that people like this are going to move the needle in housing is dumb. Unless these Uber yuppies own 1000 houses each I guess

Hi frisco lens, my take on the FED and low interests is that all investments…stocks, bonds, etc…became saturated due to easy money. So people looked to put money into other things and there was an influx of investment money into residential markets in global cities. It was called “golden concrete” and returned a mean of 10% annually over the past five years.

Now there’s a great backlash and the headlines are full of articles about affordable housing and inequality. Soon cities and states plus the federal government are going to be forced to step and and regulate. A good report to see is the UBS Global Real Estate Bubble Index 2018.

I read a Gizmodo article yesterday regarding the anticipated Tech IPOs of 2019 which suggested that the resulting financial windfalls will greatly increase Bay Area real estate prices. I’m curious to hear opinions on how this may or may not affect the pricked housing bubble.

Much of this is already priced into the housing market. I know a banker who works at a large bank at the San Francisco office. This unit specializes in extending very large mortgages to borrowers whose wealth is based on stock options and shares of startups that are not publicly traded. This type of lending is a huge business here. A lot of lenders are into it. If you sit on $200 million in Uber shares or options, you probably already took out a $10 million mortgage to buy a decent home. When the IPO happens, you’re unlikely to buy another home.

Also, many of the startups already use a system where employees can sell some of their non-publicly traded shares.

True, those programs exist and early employees probably took some of that $ off the table. At these companies, however, you will also have rank and file that will receive much lower but still large amounts, e.g. $500K – $1.5 million, that probably are not leveraged. These are large companies by the time they go public and the number of people receiving that kind of payout adds up. Assuming share prices don’t tank during the lockup period, I would expect many of them to go bid up the market with very large down payments. Almost everyone in the Bay Area wants to stay in the Bay Area if they can afford it. It is God’s country.

Only a handful of workers are getting substantial money from the IPOs. Most tech people bounce from job to job and get no payout. The big money is in finance and wall street … not tech.

@Socaljim – right, that’s why SF real estate is so affordable.

@SocalJim –

See this article: https://www.businessinsider.com/twitter-ipo-created-1600-millionaires-2013-11.

Twitter IPO alone created 1,600 new millionaires. That number probably went down a bit as Twitter declined during the lockup period, but you get the point. And that is just Twitter. Uber, Lyft, Slack, Palantir, Pinterest, AirBnB. That is a lot of liquidity coming to the SF real estate market.

I don’t care how many “tech people” you think you know, you are dead wrong about the amount of $ being made in tech (although maybe not in your circle).

Bay Area housing prices will be the last to seriously decline, and the first to recover. It is a great place to live for many reasons.

So what if businessinsider found 1600 new millionaires in the bay area due to IPO. I don’t doubt the number but be careful what you read and how and why it is presented in news media. As of 2018, there are 7.7 million people in the Bay Area. The medium household income is $96,265. There are over 2.5 million households, 1.5 million are owner occupied with a median house value of 353K (2010 number so extrapolate to now), 1.1 million renting. So say 5K newly minted IPO millionaires in 2019 is really just a drop in the bucket. And like what somebody said, most tech workers get little to nothing out of these IPOs and bounce around from job to job. It’s still a good living, better than most but like any like any other field of work, only the a small percentage get rich at it.

$10 Million is “decent”? =:-O

oooh, so what happens if the market tanks those IPOs get delayed or never arrive and lose value after they come to market?

I have another take on it. The market tanked late last year. These would be IPOs got scared and decided to get out this year. Rats leaving a sinking ship.

The Cal association of realtors (CAR) recently estimated that it takes an income of $333,000 to buy a house in San Francisco.

HUD considers family(of 4) incomes below $117,400 to be low in San Francisco.

Although no other city has numbers this high, the reason for the current and ongoing decline in housing prices nationwide is simple, prices relative to incomes are unsustainable high.

There are so many people in SF who make way more than that. I really don’t see how $333,000 is enough for a house in SF. Maybe a shitty house if you have help from your parents with the down payment.

The Los Angeles area has more million dollar plus sales than the SF bay area.

Just to give you an idea,

Last year, in LA county, more than 17000 homes closed at over 1M dollars. SF county was less than 4000. If you go county by county, then add them all up, you will see the LA/OC/SD area is the leader in 1M+ home sales.

SF county is only 49 square miles; LA county 421. LA county population > 10 million; SF county 850,000

SF makes LA look cheap by comparison.

The numbers of million and especially multi-million dollar home sales is higher in Southern California. How do you explain that?

SoCal is bigger? You get a whole house in SoCal for what would get you a 2 bedroom condo in SF.

Here’s a good graphic for you:

Mortgage, student loan, auto loan, and credit card debt in the U.S.

https://en.wikipedia.org/wiki/Household_debt#/media/File:US_consumer_debt.png

You can see how mortgage loans have just shot up.

Shocking Florida House prices in Clearwater apparently down 40%

https://www.movoto.com/clearwater-beach-fl/market-trends/

Seattle doesn’t look good either

https://www.movoto.com/seattle-wa/market-trends/

Wolf:

I love reading your blog especially on Housing Bubble 2.0 topic specifically as it relates to SF housing prices. I would like to believe that a real change is happening, but I do not see firm concrete data yet. I can see your graph showing moderate decrease from peak, but can’t corroborate it with my experience watching the market and at various open houses. This decrease feels like its a combination of seasonality, interest rate hikes from the fall, tech market melt down in Dec, and rush of new condos to hit the market last Oct (one broker told me it was a new record) . In other words I don’t expect it to last, and with the onslaught of new IPO millionaires, the demand should continue to increase. Please tell me otherwise.

I wish you would develop a graph with 3 lines over time: $/sq ft for 1 bed condo, 2 bed condo and SFH. One thing the data is masking is the fact that new condos are shrinking as far as I can tell. One bed condos built a few years ago were about 850 sq ft , new 1 beds are around 650 sq ft, so unit rates are closer to $1200/sq ft in the city. The bottom line is paying much more for far less.

Scott,

The Case-Shiller data compares the two sales of the same house or condo. So price changes are based sales pairs of the SAME home. A condo that sold in November might have last sold in 2005. The CS compares the two sales and extrapolates price changes from those sales of the same unit over time. So there is no need to go into square footage.

Note that by definition, the CS cannot look at new built sales prices. It has to wait until the second sale of the same unit occurs years later to get a sales pair.

Median prices are a very different measure, and I cover those occasionally. And square footage is one way of looking at them. I think this is what you’re referring to.

Scott,

You can mine Zillow data with all of the things you are asking for.

https://www.zillow.com/research/data/

Lolz. I see some people here who a desperate to catch a falling knife..

I won’t even be looking at open houses or zillow, until, I start seeing people on the news crying and wiping about to be foreclosed.

I see a load of people LOADED with debt.

*Students loans,

*Big auto loans on Teslas, big SUVs, and trucks (72-84 mo loans)

*High balances on Credit cards.

*High Rent or High Mortgage pmts

*Property Taxes issues with SALT

A Recession will eventually Hit (I don’t know when) but all it takes is a period of 4-6 months of unemployment to sink into hole of no return for a lot of people.

Sorry to rain on your parade. Yellen already told us that there’ll never be another recession. So everybody who owns a place will keep getting richer and richer until they run out of assets to buy here on earth. Then they’ll buy a ticket to mars where assets await to be bought.

The FED’s Ombudsman ([email protected]) just sent me a few links on Federal Reserve’s reporting on affordable housing, which I’d thought I would share here:

https://www.federalreserve.gov/econres/notes/feds-notes/assessing-the-severity-of-rent-burden-on-low-income-families-20171222.htm

https://www.federalreserve.gov/econres/feds/files/2018035pap.pdf

https://www.stlouisfed.org/~/media/files/pdfs/community-development/policy-insights/dts_policy_insight_final_9_7_18.pdf?la=en

https://www.newyorkfed.org/medialibrary/media/research/epr/2018/epr_2018_housing-affordability_dokko.pdf

I know financially it makes more sense to rent. I owned a house 10 years ago and spent a lot of money on repairs. But most of the houses I might want to live in are owned by Chinese landlords. They are horrid. Cheap, cheap, cheap. I just left one and want to buy a house this fall. I had to use stinky hot water because the owner refused to replace a rusty water heater.

I want to live in far north Dallas, zip code 75252. I’ve been researching property records and have found that most homes have price increases of $100K since 2015. They are still selling like hotcakes. Anything close to $300 to $300K sells within a month.

I don’t know if we are the top of a bubble or not. Dallas has a lot of jobs and a huge influx from all over the place. So the question is, are you a lunatic if you buy right now? If you buy and stay there 5-10 years, will the cycle even out?

I have been wondering if it is better to go straight to a builder and build a home rather than purchase one from an agent. Something tells me that cutting out the middleman is beneficial. The builder can make a little more money by selling to Joe Schmoe, and Joe gets to save some money by not paying for a realtor. What do you think?

Wolf

The market here in Miami for high end custom homes is fluid. Many of the top end homes are moving with more NE coming in than South Americans. The strong Dollar has really killed the flows currently versus 2014 /15. The NEers tend to want the beach’s rather than the nicer suburbs of Miami like the Gables and Pinecrest. There is a lack of supply of new waterfronts . The bay fronts are much more in demand (much higher $) than the canal waterfronts.

The large McMasions non waterfront have more supply. Price 6mm – 2mm. The sweet spot for homes moving are in price point of less than $3mm. In between $ 3.5/4mm where most of the supply is priced is softer given the inventory. Above 4.5mm to 5mm is strong and seems to be the sweet spot .

While I am in the high end where things are fuild. The lower priced homes are still in short supply. I have many friends that have millennials looking for SFH in decent areas but ithey are really unaffordable for the majority. A starter home 4/2 in a decent neighborhood $400m/450mm. Under $300m you have to go to the sticks looking at multi hours of commute times. Most millennials are renting condos cause they can’t afford to buy. But it is tough to save with 2000 3000 payments. Here there is no public transportation to speak of so you need cars. It is kind of an unsustainable situation here for young adults. We are not like NYC or SF where the wagers are higher to support these prices. The flight capital from SA and the tax flight from high tax stars is a real burden on young families trying to get started.

Wolf could you please produce a chart like those of above for Miami on average. While are medium home price are near the previous cycle. The high end here is so far above the prior peak it is downright scary.

Paco Garcia,

Concerning your last paragraph: great idea! There are a bunch of large markets, such as Miami and Chicago, that have not reached their Housing Bubble 1 highs and that therefore are not included in this list of the most splendid housing bubbles in America. But it would be nice to have a list of some of the biggest markets that didn’t make it back… I’ll post an article on this over the next few days.

The bubble trend in CA real estate, and SF in particular, refers to tech workers, etc. and omits several local trends: People on rent control, Chinese money laundering, Russian money laundering, Americans who made a bundle elsewhere and want to retire in CA, the 28% decline in the Chinese stock market last year, and off MLS cash sales. It seems to me that we have enough of these to offset the traditional metrics.

When we were renovating and disposing of items in 2013 prior to selling, a Chinese chauffeur in a limo with his boss offered us a bag of cash just based on the fact that a dumpster was out front. We declined as the offer was 20% below what we knew we could, and did, get 3 months later. This is not that unusual. Vancouver is the poster child for this kind of buying trend. Hopefully it will end soon, but given the raw number of people in China and India, if even 1% of them buy in the USA it’s a startlingly large number of people.

There are way too many average income speculators in RE these days. Las Vegas and Phoenix are fertile ground, IMHO. I can’t understand why people keep buying rentals in SF area, but clearly they can break even within a few years and Trump has just made it even easier.