The Fed has warned about them, and investors fear a run-on-the-fund.

The $1.3 trillion “leveraged loan” boom is coming unglued: Not because the junk-rated, highly leveraged, cash-flow-negative companies that issued these loans are massively defaulting – they’re not yet – but because investors are fleeing these instruments that had been super-hot for years, until October. They’re fleeing from loan mutual funds that hold these loans because they want to grab the “first-mover advantage” in an illiquid market; they want to be the first out the door before they get caught in a run-on-the-fund – with potentially catastrophic consequences for their cherished money.

These investors yanked a net of $3 billion out of US loan mutual funds and $300 million out of exchange-traded loan funds during the week ended December 19, in total $3.3 billion, the biggest outflow on record, according to Lipper. In the prior week, investors had yanked out $2.5 billion, which at the time had also been a record. It was the fifth week in a row of net outflows exceeding $1 billion, also a record.

Since the week ended October 31, the week all this started, the net outflow has reached $11.3 billion.

Loan-mutual funds sit on some cash with which to meet redemptions because selling a loan to meet redemptions can take a long time even in good times, but investors can get out of a mutual fund with the click of a mouse. This “liquidity mismatch” is very risky: When redemptions pick up momentum, the fund becomes a forced seller into an illiquid market where only a few vulture hedge funds (set up precisely for that opportunity) are willing to buy at cents on the dollar, even if the loans have not yet defaulted. Forced selling, the associated losses, and the inability still to meet redemptions can cause open-end mutual funds, such as these loan funds, to collapse.

Now these funds are flooded with record redemptions, and they’re selling loans to stay ahead of redemptions and maintain a cash cushion in order to avoid the fate that afflicted a number of open-end bond mutual funds during the Financial Crisis and during the oil bust a couple of years ago: a collapse of the fund when there is a run-on-the-fund.

This selling by these mutual funds has caused prices of these loans to drop. Note that “leveraged loans” carry a floating interest rate, pegged to Libor. In a rising interest-rate environment, the interest that a leveraged loan pays rises with Libor. So in this environment, these loans maintain their value, unlike fixed-rate bonds, whose prices decline as yields rise. That’s why these leveraged loans have become so hot among investors over the past three years.

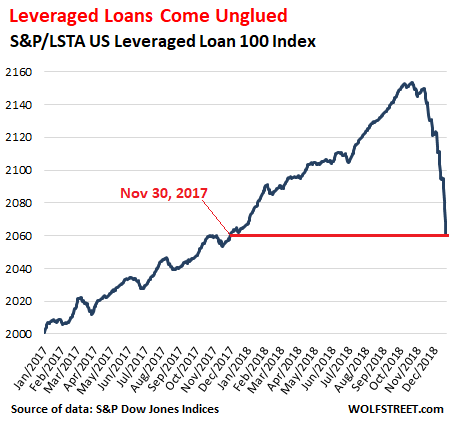

But on October 22, this market peaked, and then it began to fall apart. The S&P/LSTA US Leveraged Loan 100 Index, which tracks the prices of the biggest and most liquid loans, has since dropped 4.3%. That might not sound like a lot, compared to the declines in the stock market, but these loans are investments with a fixed face value and rising interest payments, and their price is not supposed to drop unless they’re at risk of default! These eight weeks of price declines wiped out the price gains of the prior 11 months, putting the index back where it had been on November 30, 2017 – and the wave of defaults hasn’t even started yet:

The Fed has warned and fretted about leveraged loans with increasing intensity since 2014, broadsiding them in ever greater detail and emphasis, including most recently:

- On October 24, when the market peaked, with a very specific warning about how companies that issue leveraged loans are dousing investors with risks via four tactics: “Cov-lite” leveraged loans, “Incremental Facilities,” “EBITDA add-backs,” and “Collateral Stripping.”

- On December 2, in its first-ever Financial Stability Report, in which the Fed fingered business debts as the potential source of the next financial crisis, with leveraged loans being specifically cited as one of the major risks in that group.

Until October 22, investors have brushed off any concerns, and since 2014, when the Fed started warning about them, leveraged loans outstanding have doubled to $1.3 trillion.

A lot of times, leveraged loans are issued to fund:

- Leveraged buyouts (LBOs) where the acquirer, usually a private-equity firm, makes the acquired company borrow the money to fund its own buyout (hence “leveraged buyout”).

- Special dividends by the acquired company back to its PE firm owners. This form of asset stripping is called ironically, “recapitalization.”

Leveraged loans are traded like securities, but securities regulators don’t regulate them because they’re loans. Bank regulators consider leveraged loans too risky for banks to keep on their balance sheet, so banks arrange them with other leveraged loans, structure them, package them into Collateralized Loan Obligations (CLOs), and sell them to institutional investors. Or they sell the loans to loan mutual funds, pension funds, and other institutional investors, domestic or foreign. And all along, they collect hefty fees.

Thus, most of the risk of leveraged loans are with investors, not the banks. But banks are exposed to some extent, particularly when the market changes, and suddenly they cannot offload the loans and are stuck with them, which happened during the Financial Crisis; or when they cannot offload them at the prices envisioned and then have to sell them at big discounts and better terms for investors. And this is happening now. Rather than take a loss of this type, some banks are now choosing to hang on to the loans, hoping for better days.

According to Bloomberg:

A group of banks led by Goldman Sachs had to hold onto a $500 million loan backing the acquisition by First Reserve, a private equity firm, of a stake in Blue Racer Midstream LLC, a pipeline operator, people familiar with the matter said. A mix of direct lenders and infrastructure funds have expressed interest in the debt and Goldman is now likely to sell the loan to a small group of buyers separate from the syndicated market, one of the sources said. Barclays and RBC are also involved.

That delayed transaction, combined with others, means the banks will have to bear the risk of the loan prices falling further, as well as costs associated with holding the debt on their balance sheet.

This will be another cold shower for earnings at the biggest banks that arrange leveraged loans. But investors will eat the lion’s share of the losses, and to avoid this fate, these investors are now selling. There is always someone on the other end of each sale, and in this manner, the risks are getting shuffled around, and each time they get shuffled around, the prices drop.

But these are still the good times. The economy is growing, and companies are not yet massively defaulting on these loans. Credit is tightening, and it will be harder and more expensive for junk-rated companies to refinance existing debts when they come due, and a wave of defaults is expected, but hasn’t happened yet, and the impact of those defaults on leveraged loans is scheduled for later. What we’re seeing now is investors getting cold feet. It’s the first step.

Under tremendous pressure, the Fed sticks to its guns, mostly, and the crybabies are having a cow. Read… Stocks Tank 3% in 2 Hours after the Fed Refuses to Flip-Flop

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

There ought to be an ETF called LELO, as in “LELO is in a stitch”.

Being serious again: The term “Junk Bonds” is commonly used. I think it would be entirely fair to use the name “Junk Loans” for Leveraged Loans. Why isn’t anybody saying that? Because banks would be very displeased by such language?

Thanks for the encouragement. I will start using this term. Not sure though if WOLF STREET is big enough to make this term stick in the financial media.

Some of our terms have stuck. Others have not. It’s always fun to try though :-]

I see MSNBC last night catching up to your concerns about share buy backs. First time I’ve heard MSM portray them as other than positive.

Normally they are presented as a buy signal.

A thought re: buy backs. They resemble the way an embattled currency uses up its reserves, usually with no long- term positive result.

@nk Great analogy

It’s a rare day I don’t repost one of you articles, especially now that the world is turning upside down or is it coming back to reality?. I wanted to be the first on the west coast (probably not but what the heck) to highlight your new phrase, “junk loans”

Let’s see if we can get it into the comments section of the Journal. Those are usually more informative than the articles anyway…

GMAC and New Century had plenty of Junk loans in the past….

Santander Bank has lots of junk loans at this very moment. Now one of the biggest subprime auto lenders in the country. Santander verifies income on well less than 15% percent of borrowers while writing 72 month loans on used cars. What could possibly go wrong?

Hey Wolf!

Could you please provide some example of companies that issued these loans.

Or maybe there i a whole list of them somewhere on the internet?

Thank you!

Many companies have, including Musk’s SpaceX

Uber did two of them, the last one for $1.5 billion.

Name a major junk-rated company, and there is a good chance it issued a leveraged loan.

teensie bit of Google-Fu, search on:

leverage loan site:businessinsider.com

I intentionally left off the d in the leverage term.

Does anyone have any thoughts on how this could affect the availability for and pricing on loans for commercial real estate going forward?

All thoughts and comments are appreciated.

I have a mattress for sale

“…a few vulture hedge funds (set up precisely for that opportunity) are willing to buy at cents on the dollar, even if the loans have not yet defaulted. ”

Are there any specific funds you have in mind? Perhaps being patient is where the profit in these loan sales will be.

Older and Wiser,

I don’t remember the names off the top of my head, but they got a good amount of publicity when they were set up recently. There are all kinds of strategies to buy “distressed credits,” which includes loans, junk bonds, and other credits. You might want to try googling: distressed credit hedge fund — and see what comes up. There may be better key words.

Wolf,

Isn’t Oak Tree out in LA big into distressed debt? I also thought Tepper played a bit in that space?

Follow The Money

Or should that be, whatever liquidity is left in the system.

The “smart money flow index” continues to tank.

These folks “knew” something was up back at the end of January 2018, when the index started to nose dive and has not stopped diving since!

As many say; “Its better to be early rather than late”.

http://www.confoundedinterest.net/2018/12/20/breaking-bottom-sp-500-down-15-since-september-as-the-fed-grinch-speaks-smart-money-flow-index-keeps-tanking/

As you stated Wolf, these are still good times with the economy growing. In general, the institutions have gotten their fees and sold the junk loans to retail investors, who were just chasing yields in the era of ZIRP. Wall Street will frantickly try to sell a few more large Zombies to the public in early 2019(i.e. Uber, Lyft, etc) before the doors close. My guess is it may be too late.

>They’re fleeing from loan mutual funds that hold these loans because they want to grab the “first-mover advantage” in an illiquid market; they want to be the first out the door before they get caught in a run-on-the-fund – with potentially catastrophic consequences for their cherished money.

Sounds like a good idea to me.

CDO -> CLO … Time for “The Big Short” sequel?

You’ll know it’s hitting the fan when

the phrase Good Bank /Bad Bank starts

being thrown about

Smart Money Exits First

SPLN SPDR Blackstone GSO Senior Loan Fund (ETF)

Fund withdrawals began in December 2017, and the draw down has continued without interruption for the past year.

The age old adage: Better to be early rather than late.

http://www.investmentresearchdynamics.com

“Smart Money Exits First”

There’s another kind of money – might call it “Rest-easy money”

It never entered in the first place.

Privately negotiated stock buybacks get to the front of the line…

Great article on bank loans, or junk loans, especially on the liquidity mismatch inherent in the retail funds.

The warning signals were becoming clear. I did liquidate all positions in BKLN and LFRAX 5 months ago. This one is hard to watch. People get desperate for any kind of decent yield after 10 years of drought. Hopefully in the end, the yield on this junk debt will more appropriately reflect the extreme risk of these loans. The yield on these loans should be well above 7-8%. I don’t think we will ever get there. 4-5% average yield is not and has not been appropriate.

If you are correct then the Fed should raise, and keep raising, more than 1/4 pt. In 2008 they should have raised rates to accurately PRICE RISK. Now they are still on the dovish side of a phony rate hike policy. The Volcker moment is at hand, few people appreciate that was done to get interest rates and inflation to correlate. And higher interest rates always portend higher inflation, (which is dropping in this instance) Am I the only one who can do the job?

How many employees do these zombie companies have?

Hope they don’t have to hit the streets, especially this Christmas season.

Well, Iamafan, since you asked:

(Caution: the following numbers were self-reported by companies who have extreme difficulty balancing their corporate checkbooks. Caveat Emptor):

Netflix: 5,400

BlueApron: 1,800

Uber: 10,000 non-drivers + 750,000 USA drivers + 1,250,000 global drivers

Lyft: 1,600 non-drivers + 1,400,000 USA & Toronto drivers

AirBnB: 3,100

Snap: 2,600

The above is only 6 (albeit unicorns) of the hundreds of the current crop of “profitless” start-up companies, but you get the drift…

Let’s not forget Amazon and its millions of employees, though that company is in slightly better shape than Netflix.

Jessy

2018 Amazon had 615,000 employees.

BlueApron will I believe soon be struck from this list and placed onto either the bought-out or bankrupt list. Stock at around $.63/share last I checked.

I equivocated about including Tesla (25,000+ employees)

Thanks. I hope the employees don’t get hurt.

I always get depressed when we drive by the shuttered ToysRUs.

I was under the impression that working at Tesla was a soul-crushing experience, full of unpaid overtime, and unrealistic demands.

Just like every retail company uses Amazon to justify layoffs, the auto manufacturers are starting their round of layoffs, blaming EV.

Really, it’s secular stagnation (which requires a political solution, not a monetary one)

What solution would you propose?

It’s not like EVs have any significant market share. Most buyers are upper middle class or richer, and live on the west Coast where extreme weather is not an issue.

Wonder what prompted ‘investors’ to chase yield and take on a lot of risk *cough* ZIRP *cough*

Who has taken out these ‘junk loans’ in size

If by “junk” you mean “leveraged”, PE firms such as BlackStone are the most enthusiastic issuers: the buyout of Thomson Reuters financial data division (henceforth Refinitiv) earlier this year by a group of PE firms was worth $30.5 billion, mostly financed by preferred stock and new equity.

Preferred stocks are a particular class of stocks with a higher claim on assets and earnings than common stocks. This means that, say, dividends are paid out to holders of preferred stocks before to holders of common stocks.

But $13.5 billion are being financed through a combination of leveraged loans, mostly of the cov-lite variety. While all loans have built-in covenants to protect the lenders, cov-lite do away with part or even most of these covenants in return for a higher yield.

As cov-lite loans go, this is huge.

If the FED cares so much it should start “hinting” that LBOs should be made illegal. But I honesty don’t see that happening, not in the USA.

Leveraged loans are only tenously connected to leveraged buy-outs (LBO): a leveraged loan is a loan extended to companies and/or individuals who already have a large debt load and/or a poor credit history.

A LBO is the acquisition of another company using a large amount of borrowed money to finance the acquisition. This borrowed money may come from loans (leveraged or otherwise), security markets, existing lines of credit etc.

What the US Federal Reserve (Fed) and other august bodies such as the International Monetary Funds have been fretting about for at least three years are not LBO, but leveraged loans as a whole, a veiled way to say they are worried about both debt loads and the poor nature of a large part of that debt, which carries high risk in form of cov-lite (see my reply above), incremental facilities (adding additional debt with equal seniority as existing ones without seeking consent) and other assorted hijinks, all of this for small yields.

I suspect these august bodies, which have incentivated any form of lending behavior to stimulate short-term demand and hence nominal GDP growth since at least 2009, did not expect the whole world to jump so enthusiastically on their offer…

Wolf, as far as these ETF and loan mutual funds are concerned, in what category would they be listed in the Callan Periodic Table Chart?

Re: http://time.com/money/5124387/investing-callan-periodic-table-investment-returns/

Also, pls correct my analysis since I believe those CLO’s have been purchased mainly by pension funds managers…

https://www.bloomberg.com/graphics/2018-collateralized-loan-obligations

“…and the wave of defaults hasn’t even started yet:”

Why would it?

Guess you missed the memo about rising interest rates on all loans (for the record: includes leveraged loans).

Usury is usury no matter what fancy names/acronyms are invented to describe the behaviors and the ‘products’ which result from the desire to exploit vulnerable human beings for gain (debt is now strangely a ‘product’, of course).

It’s a term uncomfortable for those who indulge in it, so has been removed from the lexicon, in the same way as ‘greed’ (which is now ‘aspiration’); but it’s the same old same old, just as the desire for money and ‘stuff’ is still greed as it always has been and will be.

Right on!

And the reward for those who eschew greed, as best they can?

Well, virtue has to be its own reward. For those who have planned well and prudently acquired financial security without begging their neighbors:

https://www.zerohedge.com/news/2018-12-15/festering-social-rift-over-pensions

“…the ‘products’ which result from the desire to exploit vulnerable human beings for gain.”

So, you refute the notion of the time value of money?

Without questioning the theme as presented, especially the dubious value of junk loans, I wonder if retreat from the arena is not also partly liquidity drying up across the board. If investors are tanking on the stock market for example, they might draw down on other investment to cover.

On the non variable price of junk loans, well if the S&P/LSTA US Leveraged Loan 100 Index goes up, it will also be able to descend, no matter if interest is Libor pegged. In other words the price of the loan is an additional parameter that will increase or decrease total yield according to how investors (sorry, speculative lenders) value the junk loan.

Ultimately the Fed will lower rates and junk leveraged loans and high yield will come out smelling like a rose. BUT the sheer volume of credit leads to a deflationary crash.

Why are so many companies doing share buybacks rather than investing the money into new products?

“Why are so many companies doing share buybacks rather than investing the money into new products?”

That, Mr. Clayton, is the right question.

There’s more to it than simply to boost stock prices so execs can cash in their stock options most profitably. Taken to its logical conclusion, what would happen if everybody did it? What has already happened to certain companies that have adopted this practice? That should give you a clue.

I gave the answer. Nobody liked it. Nobody believed it.

Because creating truly good, innovative, profitable products is hard. It is risky, and for large scale companies the risk is multiplied by the scale on which the product has to be produced and sold.

This difficulty is also aggravated by the current economy, where most of your potential customers are hurting for cash.

As a senior executive or a board member, your incentives are to see your stock share price go up, which is not necessarily tied to deployment of new products. Driving up the share price through buy-backs is much less risk, and it transfers the damage to the company into the future (to be dealt with by others).

I would also add, that should your new product turn out to be successful, it will be immediately copied by the manufacturing base that was transplanted to China.

This means, while the innovator is bearing the full risk of the product failing, its success is shared by imitators.

Thanks guys for your thoughts. Quite sad that innovation is no longer a big plus for a companies standing nowadays. In that sense we are going backwards due to Company Executive greed. Always use the Concorde as an example since the 80s we’ve never come close to something as good as that was.

Yes. Once a firm is established it becomes too risky to do true innovation. It’s safer to protect the product you have. Innovation in your domain becomes an enemy, so you keep an eye out for it and buy it up ASAP. True innovation doesn’t come from the incumbents, but from the upstarts. It is going on but, as ever, is not recognized as such. But that’s good, as innovation often needs time to get some roots down, all the more so if it’s highly disruptive and so will be heavily resisted by the status quo. And no, I’m not talking about blockchain, but am happy if others are ;-).

It could be that the world is saturated with consumer products and that the consumer is already over indebted. Plus the demographics and societal changes including environmental issues have changed outright consumption needs and desires.

What needs to be done is not the next generation of cell phone but major infrastructure changes which require government intervention and planning which we have little or none. So what’s a company to do? The system gave them money they don’t really need so they just waste it.

What is needed to be done requires lots of money and a functioning government while the current belief and faith in corporate capitalism is all about small government, low taxes and even corporate subsidies which is the opposite of what is needed so that society can move forward.

So our society is wasting our resources in speculative frenzies and trying to support a few elite rather than building what’s needed.

Because share buybacks, especially through private transactions, are a way for big shareholders to get HUGE CHUNKS OF CASH out of a company legally, without liquidating into the market.

Part of the con is to control the language. Don’t think of it as a “share repurchase”. Think about it as a “cash-out refinance.”

Could Powell be fired? I am no fan of the Fed but after 30 years you get a Fed chief who does what has to be done (rightly so) and it is being reported that Trump will fire him.

Just curious what do you replace him with?

That is easy. Bullard!

Mick Mulvaney.

Kudlow will probably get the nod.

Setting aside whether or not it could technically (or legally) be done, I expect that it would create utter chaos in the markets. In other words, exactly the opposite of what The Trumpertunist wants.

Agree.

I’ve been reading a lot of pieces/comments along these lines this afternoon… is Wall Street already that desperate?

Lots of shells on that beach …

A lot of shell companies syphon off profits off a company through various mechanisms to loan back the profit to the main company at the start of the fiscal year , of course the shell sells the service and gets paid interest rates. Call it classical mom and pop shell .

Where it get interesting is that those shells secure leveraged loans to finance buybacks that we have seen quite the few bit lately AND the owners of the shells get issued prefered stock such as B shares the shell getting a larger revenue of the main company etc.

The banks here are not too watchful about the activity and ask a 20 percent down , pretty much like a mortgage here , yes , the practice has become THAT common !

Those loans are then packaged and sold to mutual funds , most of which hungry for profits do not read through most of the documentation which is scantly available anyhow as to the organization of those shells.

So we might actually be looking at a much much larger problem than what the print of leverage loan itself since the product gets diluted into other parts of the financial overall activity.

We might be looking at an unwind the size of 2008 … may be even grimmer on the credit side. Time term might actually get much shorter as those cov-lites get recalled. Keep in mind that as the risk increases cov-lites can be recalled on a simple notification.

Fascinating article Wolf,

I would be intrigued with exactly who were the last ones to try to get out the door in 2008 but received broken noses instead? I have no specific reference or data that would reflect the biggest losers, but having a brother in the upper echelon’s of a large bank that was closed (on a Friday of course!) in 2008, suggests banks and pension funds. I clearly remember discussing with him his utter lack of knowledge of where all these bad loans were when credit locked up. He was terrified….and ultimately justified, as he lost his job about 90 days later.

they make etf’s out of that crap? jeez, who would have thought people are that stupid.