After the blood has been let, the feeding frenzy subsides, which is also brutal.

The price of natural gas futures (January Nymex NGF19) gapped lower at the open this morning and plunged 7.8% as of this afternoon to $3.53 per million Btu. Everyone blamed the weather, specifically a new forecast this morning of warmer-than-normal temperatures across much of the US for December 22 through 26.

But it’s not just this weather forecast. Over the last six trading days since December 10, natural gas futures have plunged 21%. Since the 50% spike during the first two weeks of November, culminating on November 14 with an intraday high of $4.93 [WTF Just Happened with Natural Gas?], natural gas futures have now given up 28%. It has been a wild ride back to where the price had been on November 8 (daily open, high, low, and close, data via Investing.com):

When natural gas spiked in early and mid-November culminating in the phenomenal one-day 20% surge on November 14 to an intraday high of $4.93, a hedge fund — OptionSellers.com — that specialized in writing commodities options for a few hundred high net-worth clients and that had promoted selling “naked” options in books and articles, blew up unceremoniously, and its trading accounts at the brokerage INTL FCStone that cleared the trades were liquidated.

Writing (“selling”) naked options in the volatile natural gas market is like placing your first-born in the middle of a busy freeway and praying that the worst won’t happen. It might work out for a while, but then suddenly it doesn’t. To communicate the collapse, the hedge fund founder and owner James Cordier lamented on YouTube the fate of his clients who had lost their entire account balance in the blow-up, after having paid him hefty fees for years. And not only that, but they could also owe additional funds to the brokerage that cleared the trades. This will wend its way through the courts.

Natural gas has a tendency to blow up hedge funds. OptionSellers.com was small fry compared to the now legendary Amaranth Advisors, a hedge fund that collapsed at the end of September 2006 after losing $6 billion on natural gas futures, or about 65% of the $9 billion in assets under management.

The Amaranth collapse ended in all kinds of allegations and charges, including by the Commodity Futures Trading Commission (CFTC) and by the Federal Energy Regulatory Commission (FERC) that charged Amaranth and some individuals with market manipulation. In other words, this was a mess.

Natural gas is infamous for gigantic, irrational one-day moves that can wipe out speculators in no time. But the fundamentals in natural gas play out over years, except for the impact of the weather. Demand, which has been rising for years regardless of the weather, boils down to these factors:

- Residential and commercial customers – demand heavily impacted by winter weather (heating)

- Power generators – demand impacted by the weather in winter (electric heating) and in summer (AC). Over the past 20 years, power generators have transitioned more and more from coal to natural gas, and demand for natural gas has steadily increased.

- Industrial users

- Exports via pipeline to Mexico and to Canada

- Exports via LNG to Mexico and the rest of the world, which is surging with each new export terminal that becomes operational.

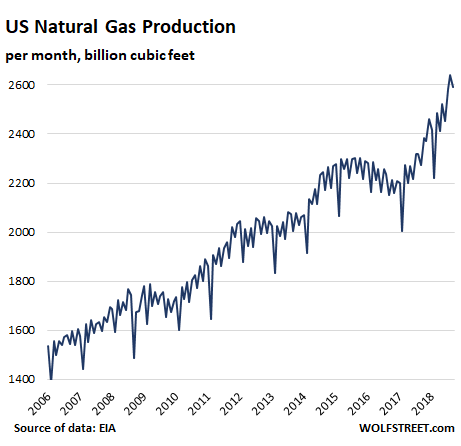

Supply is powered by the fracking boom that has caused natural gas production to surge by 75% over the past 12 years:

The US also imports some natural gas from Canada. Over these 12 years, the US has become less and less reliant on these imports, even as demand in the US and exports from the US have risen.

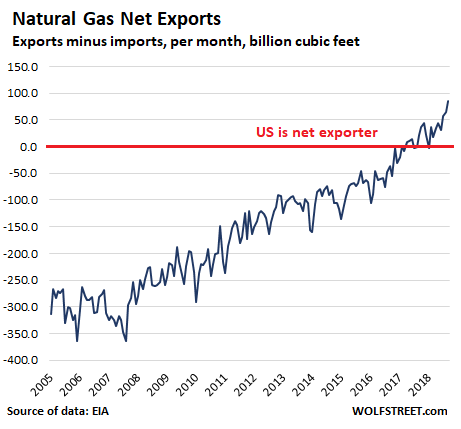

And in 2017, the US became a natural gas net exporter for the first time ever, where exports via pipeline and LNG exceed imports from all sources. In 2018, the trend has steepened:

Speculators deal with these long-term implications of production, consumption, imports, and exports as well as with the short-term conditions of weather and natural gas in storage, all the while, and more than anything else, exposing themselves to the vagaries of other speculators.

And when these speculators see a hedge fund in trouble that has to liquidate a position, a feeding frenzy ensues. This can get brutal, as the clients of OptionSellers.com have found out the hard way. And then, after the blood has been let, the frenzy subsides, which also can be brutal as the winddown of the spike shows.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The SHALE miracle. Indeed.

I wonder how well those LNG exports will do when other supplies come on line from countries that don’t pick trade war fights?

Doesn’t this make you wonder though? I thought that the price of NG would be the same worldwide, but that isn’t true. It seems like there is a huge variation in you are in Japan for example vs the US.

I would have thought that NG traded like oil, with one price across the board, well, at least with respect to one type of crude, for example WTI or Brent.

Is market forces simply not working here? Shouldn’t that work itself out somehow and seems like there should be an arbitrage opportunity here.

Often transported by pipelines, LNG isn’t as easy as oil tankers.

https://www.csis.org/analysis/gas-global-yet

The cost to transport NG is much higher than oil, so different prices in different parts of the world is to be expected. The energy required just to make LNG (need to liquefy it to transport it by ship) is 30% of the energy in the NG getting shipped. This would raise the price by 40% before adding anything for equipment and transport costs. It if way more complicated and expensive to ship than oil.

And dangerous,the first ships ordered out of ports before a storm are LNG tankers

If you look at how Canada’s energy industry has been marooned the next question is who stands to gain. And which country is not cutting output….quite the plot churner

MCH,

Check out RagnarD’s comment below. NG prices vary widely even within the US, depending on all kinds of conditions.

MCH, even goo does not trade a single

price. WTI, is a general price. Prices like

natty have quite a variance.

https://twitter.com/TomKloza

https://www.naturalgasintel.com/newsletters/1-dailygpi

I believe that a “spot market” for demand of product in Japan (and other countries) could result in prices of the commodity to be higher in Japan and elsewhere.

I watched that Optionsellers youtube video with awe. A lot of financial guys would not have even said they were sorry. “That’s the breaks… everybody loses money at some time”, or crickets is the only sound most investors would have heard. Clearly they knew there were risks, and now that the whole thing collapsed, there will be lawsuits, which is a shame, since the investment was like a bomb disposal team, all good, and full of bravado, until something unexpected happens–a black swan, if you will.

All these schemes work for a period of time, and like Long Term Capital Management, they draw in more investors, as the success rate increases, and then there is disbelief when it explodes. What made this even worse is the fact that that investment was lost, and they still owed additional money. This, boys and girls is not investing, and it is not even speculating, it is financial Russian roulette. At least the guy that spun the cylinder, and handed them the gun, had the decency to feel bad for his players.

I’m a power / electricity trader at a major utility. I trade the Midwest power hubs: MISO’s Indiana Hub and PJM’s AEP-Dayton Hub contracts.

This NYMEX contract is for delivery of natural gas at the Henry Hub (HH) in Louisiana. But there daily and forward prices at gas pipeline points all over the country.

It gets most interesting in the winter when natural gas (NG) power plants have to compete for NG with the heating load in houses. It usually loses. That is, the price of power on the grid at X location has to compete with residential heating demand for natural gas at location X.

During normal times the price of gas along a major pipeline that runs from Henry Hub up to NY and Boston will have a relative small increase in price as the gas is delivered up the coast. But when we have something like the polar vortex, the price spread, which in summer might be $3.00 at HH to $4.00 at NY, can go to $6.00 at HH and $30 at NY. So power that would normally cost $4 x 10 Heat Rate = $40MWhr at NY, will not cost $30 x 10 = $300/MWhr.

And if that’s not bad enough for the power producer, the natural gas utility will likely have a firm delivery contract on the pipe for its residential customers heating load, while the power generator will likely only have an interruptible contract. And during the polar vortex, that is definitely going to get interrupted.

This makes for a lot of uncertainty and volatility during cold weather spikes in winter in both the domestic NG and power markets.

Nice follow thru comment, the gap…NG is resting on pretty strong support here but a gap below is open since 1-2018…if it gaps down to 3.31….its a pretty darn good setup for another spike…more cold temps coming downstream….the chart and setup is looking sweet….

Thanks for that insight. Question though: why don’t power producers have long term contracts as well? After all, rates are set yearly so it shouldn’t be a problem to calculate an appropriate NG cost and hedge to that number, no?

@ Lune

They do have long term contracts. They have implicit contracts with their residential customers i.e. $X fixed costs, and $Y/MWhr for consumption. And with industrial and commercial they will have a different contracts, and they also have contracts with Rural Electric Co-ops / Municipalities in the form of “Full Requirements contracts”, meaning they will follow the customer load. And they will also have fixed price and volume contracts between all sorts of trading counterparties.

However, with respect to hedgiing / fixing costs…

A large component of what a utility does is based on “what it can recover” That is, if the utilities govt regulator will make the utiltiy whole on all fuel price moves via fuel cost riders on customer bills, the utility might not hedge. Or the regulator might require the utility to hedge X MWs of its load in the forward market.

A utility might not do what would seem most prudent to a rational actor, if the utility will not be compensated for the hedge if it loses money.

re: below. I wasn’t clear… The 10-year contracts I referred to I meant to make clear.. are in the Natty…not leckky

Much more volatile instrument as Electricity can’t be stored. If you want to see volitility, try the “day ahead” elex mkt! Some action.

Also long term contracts are there… and can be hedged in the swaps market, which goes out 10 years+… still its the near term market that takes real management

@ MooMoo

The ICE exchange may have power contracts 10 years out, but there is no liquidity there. They are not that liguid even for the current year. Back in the Enron days – Pre 2005 it was much better. The Nymex NG market is probably a somewhat better way to to hedge – probably more liquid for out years, though not great either. But, yeah, that’s a “dirty hedge”.

Actually the Real Time power market is where the real volatility is, literally $1,000 oen 5-minute tick and $30 the next 5-minute tick. (The Real Time power markets trade / move in 5 minute increments) Granted thats rare, and usually at specific points on the grid, but it happens several times every year when units trip under tight conditions.

Unceremoniously? I’d say the Cordier youtube video was a ceremony. At least that’s as much ceremony as these things ever have. I thought it was more eulogy than apology. Anyway, it was more than that MF’er Corzine did.

When the article says “writing naked options” is that analogous to naked short selling, which entails selling stock you don’t actually own??

~yes, sort of. But it’s a lot more perilous, if that’s the right word.

Shorting is one way to try to hedge certain types of naked option plays but this is not for newbies. And most retail investors do not receive the timely data feed needed to duck and Dodge. In this case the experts came a cropper so if this happened to them…not a strategy for most

…its the right word (lol)

No, no one except a “market maker” can legally engage in naked short selling. The rest of us have to “borrow” and then sell short shares if we are so inclined. That is the reason that anyone who trades on margin agrees to have his shares “hypothecated.”

Off topic, Wolf: I read Testosterone Pit in a hospital waiting room this weekend. As a sales-side guy who has done car dealer marketing, I was amused and horrified — great job.

Clete,

I hope all went well at the hospital.

Thank you getting and enjoying my book on the car business, TESTOSTERONE PIT

And thank you for sharing your thoughts on it here.

I love hearing from insiders. The book made quite the rounds in the city where I ran a big Ford dealership over two decades ago, with everyone trying to figure out who’s who, but everyone instantly identified the general sales manager, “Ferronickel.”

Some of the commodities markets are total insanity. Natty is to cheap and the producers are an insolvent train wreck. Inventories are down 20% YOY and against the 5 year averages. Prices in the $4-$5 range an MCF are justified. If the market doesn’t let producers may a few shekels then asses will freeze in the longer term. When my palace was built in the mid 70’s natty was $11- $12 an MCF. What the heck can you buy now at +50% discount to 1970’s prices. That the wads at the overly manipulated exchanges have it so effed up…no surprise.

There was a time in the great land, where the people and government and industry leaders all knew it was in their best interest to dampen financial speculation; particularly in those things that people have to have.

Like natural gas for heat and power. The futures market was structured such that only players that bought and sold the actual commodity were allowed in, plus a small number of others for liquidity reasons.

The rules were changed so that anyone can speculate in futures whether your business actually buys or sells the underlying commodity.

This single change was done so that big players (including the government) can manipulate and control the markets (say gold for example). Natural gas futures were short squeezed under the weak pretext of cold weather and lower inventory stocks. Meanwhile, the frackers are flaring gas to the atmosphere because they can’t move it down the pipes. There is no real shortage of natural gas that couldn’t be handled with a few small price moves here and there.

But as I stated before, the government is supporting fracking and oil is plummeting. Therefore, to help out, natural gas was short squeezed to improve the frackers margins. It is small but something. If oil stays down for a long time, it will be very interesting to see where the money will come from to save the frackers. It will come for sure, just may not be visible to most prying eyes.

David Cordier was right.

We should all be selling naked calls on natty right now. It’s free money!

If the premium is collapsing, then lever up! Use margin! How much room do you have on your credit cards? Take the bacons!

Guy doesn’t walk on the lot unless he wants to buy. Sitting out there waiting to give you their money! Are you gonna take it?

Are you man enough to take it?

Couple takeaways, price goes up while supply goes up. which means NG is achieving economy of scale, (it has been at half price in terms of BTU due to uneven distribution channels). Volatility like this at the end of a long narrow price range is usually resolved to the upside. The first pullback is often the place to buy. Whatever the arguments on infrastructure, (fiscal spending bill languishes because lawmakers don’t want to build more freeways – the political will to build out CNG stations has failed to gain cognitive mass, meanwhile buses and trucks and muni government enjoy the benefits.) I have solar and NG at my house, and if I had to drop one it would be a tough choice.

um, the pipelines and the spigots.

uh, and storing the stuff.