The myth of the “blackout period.” And the price of “unlocking value.”

Share buybacks weren’t happening today. Shares fell, after three days of rallying that followed the worst October since 2008, which had wiped out $4 trillion in overvalued market capitalization in the US, Europe, and Asia.

Shares fell today in part because Apple [AAPL], the giant in the indices, gave iffy guidance for the holidays Thursday evening; and with product sales not going anywhere, and only price increases boosting revenues, it said it would no longer disclose unit sales. This combo worked like a charm, and shares dropped 6.6%.

So where are the corporate share buybacks when you need them? This is when companies buy back their own shares in order to prop up their price and thereby the overall market. Where is this panacea that was considered securities fraud until 1982?

Throughout October, Wall Street gurus promised that shares would rise as soon as companies emerged from their “blackout” period that prevents them from buying back their shares.

Alas, there is no federally mandated “blackout” period. There are only some rules that companies should follow in order to be protected from securities fraud liability. SEC Commissioner Robert Jackson Jr. explained earlier this year:

Those rules, first adopted in 1982, provide companies with a safe harbor from securities-fraud liability if the pricing and timing of buyback-related repurchases meet certain conditions. After experience proved that buybacks could be used to take advantage of less-informed investors, the SEC updated its rules in 2003, though researchers noted that several gaps remained.

These rules as updated in 2003 for share buybacks are easy enough to meet. They include:

- Buybacks cannot happen in the last 10 minutes of the trading day or after-hours, except under certain conditions.

- A company has to use a single broker, rather than multiple brokers, for the trades, so that it cannot easily engage in a bidding war with itself to drive up the price.

- A company must buy shares at the market price.

- A company cannot buy back on a given day over 25% of the shares’ average daily trading volume, as measured over the previous four weeks.

Then there’s an issue with insider trading – and a way around it. Executives have access to inside information, particularly at the end of the quarter when the quarter’s data are being gathered and put together. To remain in the “safe harbor” against securities fraud accusations, companies have established “blackout periods” for share buybacks. The periods normally restrict buybacks from shortly before the quarter ends until two days after the results are released. For many companies, this “blackout period” is somewhere between four to eight weeks.

However, a separate rule (Rule 10b5-1) says that share buybacks during the “blackout” period are just fine if companies have a pre-established plan with scheduled buybacks. For example, the company can schedule in advance heavy share-buybacks on the three days following its earnings releases. It must specify a minimum and maximum price and the number of shares. And then no problem.

Nevertheless, Wall Street gurus keep expressing their fervent believe that massive buybacks would kick in after the blackout period and bail out these rotten markets.

Alas, companies have massively bought back their own shares in October, even during the blackout period, most likely by following the rules to the T.

Over the period of October 1 through 29, companies blew $39 billion on share buybacks, according to preliminary estimates from JPMorgan Chase, based on the average drop in share count across the S&P 500, FTSE Russell 1000, Datastream US, and MSCI US indexes, cited by The Wall Street Journal.

This was up from $30 billion in September. Based on these estimates, over the first 10 months, companies bought back about $350 billion of their own shares, an average of $35 billion a month. So in October, yes that terrible October “blackout” period, share buybacks were 11% above average for the year so far.

To help things along, numerous companies, as their shares plunged upon reporting earnings, have come out with new promises of big-fat share repurchases – though they’re not obligated to buy back those shares, and it could be just all share-manipulation hype. The WSJ lists some candidates:

Cosmetics firm Estée Lauder Co s., whose shares dropped by as much as 14% during October, on Wednesday announced plans to buy back 40 million shares, or 11% of the total outstanding. The New York-based company had spent more than $240 million buying back its own stock over October, it said.

Semiconductor-equipment maker Rudolph Technologies Inc., based in Massachusetts, pointed to “undervalued market conditions” on Monday as it announced it had spent $14.3 million completing a buyback plan. The firm’s shares dropped as much as 20% in October.

This week, International Business Machines Corp. authorized $4 billion worth of buybacks, and financial-exchanges operator Intercontinental Exchange Inc. announced a plan for repurchases worth $2 billion.

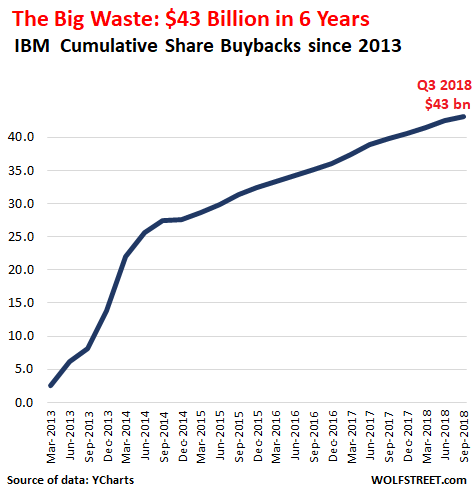

Let’s take a gander at International Business Machines [IBM], one of the biggest share buyback queens. Since 2000, it blew $146 billion on share buybacks. The chart below shows the cumulative amounts since 2013 that IBM wasted on share buybacks: $43 billion (data via YCharts):

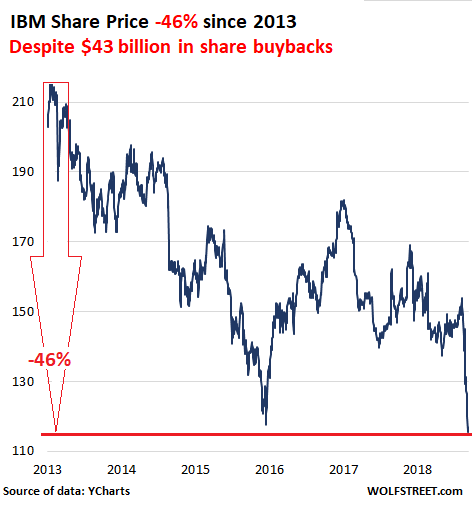

Wall Street gurus keep hyping that share buybacks “unlock shareholder value,” or “return cash to shareholders,” or some such thing. But here’s what IBM’s share buybacks did to shareholder value, as measured by the stock price:

IBM has been buying back the shares it issued its own executives as part of their stock compensation plans, and the shares it issued to buy other companies, including minuscule privately-owned startups for billions of dollars. Buybacks covered up the dilutive effects from those actions.

IBM could have spent this money on research and invented something cool. But that would have been too hard. Far better to farm out much of the work to cheap countries like India, shut down US operations, waste money on share buybacks in a vain effort to manipulate up its shares, and instead watch them go to heck.

Infamous share buyback queen Sears Holdings, which blew, wasted, and destroyed $5.8 billion on share buybacks between 2005 and 2010 to manipulate up the share price, is now bankrupt and will likely be liquidated, with zero value for shareholders.

But companies appear to be backing off their share buybacks: $156 billion in buyback plans were announced in Q3, down from $437 billion in Q2 and down from $242 billion in Q1, according to TrimTabs, cited by the WSJ.

Despite their miserable performance record, these share buybacks have been the only thing that was – if barely – holding up the stock market. But where are they when you need them the most?

Another share buyback queen is GE. Since 2012, it wasted a breath-taking $40 billion on share buybacks (YCharts data), much of it between 2015 and 2017, despite a huge hole in its pension fund, deteriorating operations, and its sick finance division. But its shares have collapsed, and it is now in the process of dismantling itself. Read… What General Electric Is Doing to Dodge the Question: “When Will GE File for Bankruptcy?”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This data doesn’t quite add up.

1. The linked WSJ article describing the amount supposedly spent on stock buybacks in October is from mid-September, before October even started.

2. $350 billion spent so far on buybacks doesn’t jive with what companies announced would be purchased through October.

Thanks. My bad. I accidentally inserted a link to an old WSJ article (from Sep). I now inserted the correct link to an article from today.

Also, there is the problem that many (half?) of the announced Share Buy-Backs never actually happen. The corporation gives some lame excuse, or just says nothing and hopes that nobody notices.

Whether or not you think that buy-backs are a stupid idea, this sort of thing comes very close to securities fraud.

I thought the different rises in Oct were short squeezes, particularly the last 3 days. If so, it smells a bit desperate.

“IBM could have spent this money on research and invented something cool. But that would have been too hard.”

Well, the share buyback maroons are only following what the greatest philosopher in human history had to say:

“Bart, if it’s too hard it’s not worth doing.”

—Homer Simpson

Dogbert consulting:

“You need a dashboard application to track your key metrics. That way you’ll have more data to ignore when you make your decisions based on company politics.”

“Will the data be accurate?”

“Okay, let’s pretend that matters.”

Let’s be serious for just a while longer:

-> Where is this panacea that was considered securities fraud until 1982?

Share buybacks are a signal to short-sellers to come and get it and mind your elbows there’s plenty for everybody be careful you don’t bite off your fingers, depending on the stock.

Since 1982 there has been a high correlation between stock index levels and innovation in financial fraud, exceeded only by the correlation between innovation in financial fraud and severe market corrections. Between them a speculator can grift beyond the dreams of avarice, which should be denied unequivocally under oath.

Homer: Good things does not end with “ium”. They end with “mania” or “teria”

Well, Dogbert would be the greatest philosopher in human history if only cartoons didn’t require high-level reading abilities. But, comprehending Homer Simpson’s collected works only requires that one not be hearing impaired and possess a rudimentary grasp of spoken English.

->Well, Dogbert would be the greatest philosopher in human history if only

Well, business philosophy, and yet, for all of Dogbert’s merits I still prefer WR. He is actively promoted to become a MacArthur fellow. Nobody on the WWW approaches the quality and probity of research and presentation that I’ve seen, but I am only an egg. Besides, he lets commenters like yourself provide the punch lines with patience and grace, even if I’m Unamused and never get the joke.

Whitehead believed all philosophy to be mere footnotes on Plato, which ruined my estimation of Whitehead. I myself am content with my settled status as chopped liver.

(Unamused… i have NO words no words…!!! this is all just so EXCITING as it’s been years and everything before was HISTORY..i haven’t seen/felt such current events RIGHT NOW poetry that twists around the ankles, yanks you upside down and sideways and best of all leave shreds of all kinds of OH MY GOD in all the readers’ teeth.. i feel it… i’m tripping over it in morning thank god AWE… no words but i managed a few croaks of KEEP GOING MORE OF THIS NEEDED EVERYWHERE ANYWHERE DON’T STOP THIS FEELS NECESSARY LIKE AN INOCULATION)

I’ll take Professor Farnsworth: {to Fry) “If the space-time continuum doesn’t care if you are your own grandfather, then neither do I.”

Financial engineering is all they know. I read somewhere this week that Dell is now looking to do an IPO.

As for poor GE, that company is one slowly dying piece of work. It did not have the cash to pay $4b in annual dividends from operations this year even though it is carrying $100 bilion in net debt.

GE’s Jeff Immelt was such a fountain of wisdom and a real industrial titan …not. That a US President actually chose him of all people to lead the economic turnaround of the US is very revealing.

This same us President, who cannot give a five-minute speech without mentioning himself multiples of ten times, now claims he is the one who caused the recently increasing U.S. jobs creation.

Wolf, you would think that if a corporation was reducing it’s outstanding shares through buybacks and if the revenue/income remained constant the dividend yield would increase. However, with warrants, convertible bonds and executive stock options the fully diluted share price should reflect the underlying value of the stock. A corporation may also recycle their treasury stock by buying it back and reissuing it, hopefully at a higher price. The buybacks and executive stock options can be used for tax aversion. Not to be confused with tax evasion.

Maybe that 1982 law should be dusted off and brought back.

I agree! Wishful thinking…

Amen! The examples of GE and IBM remind me of William K. Black’s sage advice on banking and corporate looting. Buybacks should be illegal, but Wall Street loves them because it makes the CEO’s running the accounting control frauds filthy rich. It’s an inside job of organized theft on a grand scale.

https://utpress.utexas.edu/books/blab2p

I don’t mind companies buying back their shares under conditions when it makes sense to do so.

In 1982, stocks were almost ludicrously undervalued with the S&P500 sitting at a PE of 9 and a dividend yield of 6%. Boosting the PE ratio through a buyback rather than raising the dividend allows the shareholder to build value without that value being taxed immediately, like a dividend would be.

Today, the S&P500 is very richly valued with a historically low dividend yield. Buying back stock isn’t a great play for the mom and pop shareholders at these prices. If companies can’t find any more productive use for their profits, increase the dividend.

Corporate Lobbyists write our laws, why would they allow a law that would stop stock manipulation. Congress allows corporate lobbyists to write whatever laws they please and they will vote in favor so long as they receive the required “contributions”.

Here in Washington state we have a corrupt Senator for life, Maria Cantwell, she is currently running non-stop campaign adds showing cute contraband sniffing dogs at the airport – people up here go gonzo for dogs and will give a thumbs up (vote) to anything with a cute dog – nothing to do with lawmaking she just wants to show cute dogs to win votes. As long as lobbyists pick up the tab to run cute-dog campaign adds Maria will vote for any laws she is told to.

People vote for the politicians they see in adds, based on name recognition, and if cute dogs appear in the adds… well that’s just spiking the football. Welcome to the lowest common denominator.

It’s simple Wolf. They are not buying back shares because they see it’s a waste of capital and they know that hard times are coming and they’ll need the cash. This isn’t brain surgery. The market always wins.

Good luck getting this administration to enforce it, except maybe as leverage to extract a campaign contribution.

One important aspect of the various (but admittedly minor) restrictions on buybacks: the SEC doesn’t check!

Yes, these restrictions are the difference between buybacks being legal or illegal. But the SEC doesn’t care. They have admitted it.

It would be interesting to see statistics on buybacks vs their various restrictions. But don’t look to the SEC. They don’t check!

In other words, buybacks weren’t legalized by means of establishing firmer rules. They were legalized regardless of how they manipulate the markets.

Don’t worry, FedGov is shoveling more money towards Wall Street. Even with increasing deficits, it’s increasing the IRA contribution limit $500.

More can-kicking, since they’ll never be able to replicate the demographic trends that made the Great Asset Bubble of the last 70 years possible. Lord knows the Japanese have tried every trick in the book.

Re demographic trends: Could understanding the implication of the decline in births in “advanced” societies be behind their elite’s insistence on open borders? Plenty of new serfs to be got, that way?

absolutely 100% correct

Very good article. I was drinking the cool and listening to MSM thinking buybacks would potentially help prop up the market. Nice to see some data and numbers. Also, really sad to see companies waste money on financial engineering like IBM, as interest rates rise, this will not end well for some companies. Buybacks should not be allowed, the original rules served a purpose.

“IBM could have spent this money on research and invented something cool”

US corporation have been eating their seed corn for decades. The main problem with modern capitalism is the reliance on financial innovation as opposed to making things world markets wanna buy.

It’s been pretty obvious that innovation stalled because making money from money is way easier. Most new innovation is really just making what already exists better. I watched a Peter Thiel video where he says something similar, at least to my ears.

Indian Bowel Movement would rather lay off most of their smart people in Western countries and hire cheap people in Asia with bogus degrees, because it looks good on a spreadsheet.

Having expelled almost everyone who cares about products and services, manipulating financial numbers is their number one mission now, and it shows.

Share buybacks: the self-immolation of corporate America. China is licking its chops.

Can someone explain to me how the book keeping records for share buy backs are carried out.

Are the repurchased shares bought by the SE quoted Company itself and cancelled? Bought with money from fresh interest bearing loans to the Company where in most cases the loan interest is less than the dividend?

Or are the shares repurchased by a separate or subsidiary Company that is funded from the Holding Company and hence the total shares on issue remains unchanged?

In the latter case the subsidiary Company could even resell the shares if the share price continues to rise. Then repeat the process ad infinitum.

These differing accounting methods would greatly influence the publicly available balance sheets.

\\\

Technology development requires dedicated and competent management with a skilled labor force supported by good pension funds and competitive salaries over longer periods of time. I am pretty sure that is not what the employer had in mind, when at the interview they say “it’s a challenging and dynamic work environment”.

\\\

It is important to note that it is always the american market , through it’s pragmatic approach, that accepts and enables new products and technologies first. This is partially due to the legal system; the EU requires proof a product is not harmful from the vendor, where as the US allows use of products and later deals with consequences. With the ever-increasing income disparity and increasing cost fo loans, this market which is the main driving force of US innovation will stagnate making innovation harder to reach the market. The more time a product needs to reach market the higher the development cost.

\\\

I don’t want to talk about the grant system that should supposedly drive innovation through universities, I will only tell you that the results are evaluated in a room filled with academic achievers reviewing reports written by the grant receivers. There is no checking up on grant receivers, no going to their labs looking at the devices, there is no nothing…just reports written by the grant receivers. I always wondered why the US government, when it gives out grant money for research, does not entitle itself to 30% of the resulting patents, but instead forfeits all ownership rights to the inventor.

\\\

IBM is not the exception, it’s the product of its environment…the age of financialization.

\\\

Novartis, the pharma giant, announced a 5bn buyback program in July – and has just announced it is slashing its research program by 20%.

I guess we can only speculate as to whether the latter is in order to fiance the former; however, this myopic focus on short-term stockholder returns (driven by the fact that investment funds have become way too large and powerful) is not the way to order an economy which generates general prosperity.

Novartis revenue peaked in 2011 at a little more than ChF 59 billion and have been declining ever since. This year they are estimated to be in the ChF 50-51 billion range. Not inflation adjusted and they cannot blame the spinoff of Syngenta as it’s ancient history now (2000-2001).

In the same time share price has gone from ChF 45 to the present ChF 87.

Think about this: the second largest pharmaceutical group in the world, with both the domestic and US markets experiencing the usual obscene drug price gouging, hasn’t been able to increase revenues despite a buying spree of epic proportions which included GlaxoSmithKline’s cancer drug division in 2014.

So how do we justify that obscenely bloated stock price? This is a company that is contracting, the bane of modern stock markets which richly reward business models such as Netflix’s.

The answer is buybacks! All backed by that pillar of monetary soundness and integrity, the Banque Nationale Suisse.

The highest yielding ChF denominated bonds Novartis issued will pay you all of a massive 1.05%… with a 20 years maturity. 10 years yield will set you back 0.625%.

Perhaps Netflix should consider moving to Zurich. Santa Clara traffic is not so different…

Very interesting analysis, MC01. Same for your contributions on the shipping industry and other transports. Thanks for sharing your perspective(s).

Syngenta is now safely in Chinese hands.

“In a recent interview, Chairman Michel Demaré was asked whether Syngenta could remain independent. He responded, “If you have the patience to wait for cycles to materialize, then it would be possible. But in these circumstances, where our shareholders have a kind of a benchmark share price, what they think this company is worth, it is very difficult to say that we can deliver this.”

Thanks Wolf. This is a great article among your many great articles.

Congratulations Wolf. You have the best financial reporting website in the known world!

My (slightly embarrassed) bad.

I thought the blackout period was real and might fuel some kind of tradeable bounce.

Buybacks were the only purchases I could see that might move markets up again. There seems to be no real conviction from the bulls as there was with buying dips in the past.

If not then who are the greater fools here?

Gold is rising in the face of a strengthening USD. This is unusual and everyone is acting as if it’s just noise.

I believe gold is telling us something here and its become the bell at the top of the market, although there is some churning yet to do.

The coming US dollar crisis should be fuel for US equities.

“Market” FIFY

Seriously …. I can’t fathom why anybody would’nt include quotation marks around the word “markets” whenever the word is used.

Warren Buffett’s Berkshire Hathaway bought back nearly $1 billion of its own stock.

https://www.cnn.com/2018/11/03/investing/berkshire-hathaway-earnings/

Buffett has been a very INfrequent buyer of his stock, and BRK is one of the very few stocks that is truly undervalued. Most share buybacks occur when the companies run out of organic growth near the end of an economic cycle. They buy back their shares to keep the price up, but most of it goes to offset the massive stock options they’ve given themselves. I did a study on Dell’s earnings for three years near the end of the dotcom bubble. The company reported 15.1% and 29.5% earnings per share growth in that period. When you look at the footnotes, you see that most of the share buybacks in that period were buying back stock issued for exec stock options. At that time, companies were not required to reveal stock option expense, but you could calculate it if you knew where to look in the cash flow statement. I’m an accountant, so I did. Dell actually lost 5 cents a share over the two years shown. So, as Wolf has shown, there are two issues here. 1) The “non-cash” (as they claim in “adjusted” earnings) options expense that companies and their cronies in the finacial media tell us to ignore, and

2) the fact that the vast majority of these buybacks occur when the stock is way overpriced. The almost always buy near the top and lose money, yet never buy near the bottom. The reason for this is to give the illusion of growth and to beef up their stock options.

Great piece, Wolf. I’ve been complaining about this scam for 20 years. The financial media are as much to blame as the companies. They pander to Wall Street instead of informing the public. Keep up the great work.

Buying a share or your own stock confers X dollars of market cap, while a 20% drop in the value of that asset still leaves you with 80% of your gains. When a stock doubles in price it gains 100%, when it loses that value it loses 50%. Albeit when a companies shares are closely held, the shorts are at their mercy. Can I borrow some sir, please? One strategy is to issue those proceeds through dividends, while the share price depreciates. Of course if interest rates are too high, investors buy CDs, and the dividend gambit is lost. Hence economists call for an end to rates hikes, so consider the possibilities before you write them off carte blanche.

BIG SELL SIGNAL !

CNBC is full of ‘buy now’ confidence- game boosters.

Cramer of course but he doesn’t count.

One headline says bull market is ‘in middle age and has 20 years to go.’

But they can’t have it both ways. They want to tell us this is a buying op for a Buffet- type contrarian. How to know we’re at the bottom?

All the negative sentiment silly!

But CNBC isn’t negative it is full of froth.

So when will a bottom be in ?

About 2 years after Cramer screams (literally)

SELL! Sell now at the market! Raise cash before it’s too late!

Cramer is a clown. Has always been a clown. Pushing McDonald s now as a can’t lose. Yes sure, a stock that has been a trading range under 30 dollars for a decade or two the suddenly ramps to about 180 dollars. As Cramer says. The sky is the limit now for MCD. …… not

Everyone knows it’s JACK.

End of cheap credit = Less and less share buybacks due to those becoming more and more expensive.

Is not rocket science guys.

“Sell to expand, buy to contract.”

Many of the professionals I know and have worked with don’t believe in the financial markets anymore. The only reason they ‘invest’ through 401k’s is to manage taxes and even then it’s only into Vanguard or Fidelity index funds (not ETFs). They/we know it’s all a sham.

These are professional traders, risk managers, software developers, and mathematicians who operate large institutional trading books for money center banks.

At the end of the day it’s a fools game and the people who run it know…

My advice to everyone is to play the game but go into it with your eyes open. Be smart and don’t take unecessary risks. Understand that financial assets are just claims on real assets and the rules of the game can and will change faster than you can adjust your exposure.

As a small retail investor one of the biggest advantages you have is speed of exit. So don’t tie yourself up with esoteric investments to earn an extra 25 or 50 bps. There are teams of people on the other side of that trade who, I guarantee, are far smarter than the average person. Look for high probability investments that offer multiple paths to profit and exit.

Estee Lauder owns a boatload of cosmetics companies, most of which are not worth owning. Instead of buying back their stock, they should dump the dogs, which are about 80% of the companies they own. I buy a couple of their brands, but wouldn’t use the rest even if they were free.

You haven’t even looked at the balance sheets.

Let’s take a peek at AutoZone, widely hyped as a company that has made its stockholders rich through buybacks.

Total assets $9.37 billion

Total liabilities: $10.867 billion

The liabilities are mostly:

Accounts payable: $4.409 billion

Long-term debt: $5.108 billion

When you add it all up,:

Stockholders equity: NEGATIVE $1.52 billion.

OK, the stockholders own nothing. The entire assets of the company are smaller than their trade debt and what they owe lenders.

What is the market cap? $19.94 billion!!!

The main assets are the stocks themselves !

Excellent. Thanks Wolf. Another mother of all scams using SBB scheme.

Even with the massive SBB, i wonder why the stock price of these companies are dropping like a free fall. Is the market or company insane?

think of the economy wide ramifications:

OLD-SCHOOL FINANCE:

* shares are prized because they are claims on growing income

NEW MILLENNIAL SCHOOL FINANCE:

* shares are prized because they are growing claims on the same or slightly falling income, insofar as the level of claim grows faster than income falls.

Summa cum Laude Honorees of the MILLENIAL SCHOOL :

Bed Bath and Beyond, Mallinckrodt, Viacom, AIG, CIT, Wyndham,……the list is endless. Remember that Gas explosion by a Boston Utility a short while back? Also huge buybacks of stock….not investments in pipe.

Remember how all those wonderful tax cuts were supposed to create more jobs and better benefits for American workers? They are instead using them for buybacks.

Pfizer: In December 2017 announced $10 billion buyback in addition to a dividend hike. also laid off 300 people after halting research into drug treatments for Parkinson’s and Alzheimer’s.

Kimberly Clark: $2.3 billion buyback and a dividend increase followed by “restructuring”, which amounts to 5,000 lost jobs.

So much winning.

But they’re the Job Creators!

No wait, they’re the job cremators.

IBM must be reading this blog, and the relentless critic of buybacks and did something innovative: bought RedHat Linux for 34B, in a desperate move.

Overpay for innovation, then smother it into mediocrity with big corporate bureaucracy. I’ve seen it happen to too many little tech companies, the villain usually being Dell or HP.

Wolf, really enjoy reading your articles, very educational for me

Can you make a link to the share buybacks and a short squeeze, ss of a century?

Thanks

“IBM could have spent this money on research and invented something cool. But that would have been too hard.”

Wolf – I completely agree.

Strategies that emphasize supposedly quick gains like stock buybacks, and others like rent extraction have been crowding out new product innovation in the corporate world for a few years now. As a result, the 2000 ‘teens are beginning to look like a lost decade or dark ages with regard to meaningfully new technological innovation. To better highlight how this has contributed to a shocking lack of recent innovation, I think it might be helpful to list a short timeline of commercial innovation over the last few decades:

1970s:

First Commercially available Microprocessor Computer Chips

Gene Splicing / Recombinant DNA ( the Central Technology behind Genetic Modification & Genetic Engineering )

CT, MRI, and PET Medical Imaging Devices

Fiber Optic Telecommunications

Balloon Angioplasty

Color Photocopiers & Laser Printing

Email

Hand Held Electronic Calculators

1980s:

Home PC Computers

Computer Networking Routers

Space Shuttle

DNA Fingerprinting

MiR Space Station

MagLev Trains

Computer Software Companies

Computer Gaming Companies

Consumer Handheld Video Cameras

Home Video Cassette Recorders

1990s:

Commercial Internet

Mobile Telephones

Commercial Release of Rechargeable Lithium-Ion Batteries

International Space Station

Mapping the Human Genome

First Cloned Animals

Thin / Flat Screen Television and Video Monitors

CDs / DVDs

2000 – 2010:

Film-Less Digital Cameras

Wireless Data Networks and Technology ( Wi-Fi & Bluetooth )

Touch Screen Smartphones, and Music Players

Tablet Computers

Commercial GPS

USB Flash / Thumb Storage Drives

Text Messaging

Digital Video Recorders

2011 – Now:

???????

2011-Now:

Virtual Reality

Self-driving vehicles

Reusable rockets

etc.

I’m not quite sure what problem Virtual Reality solves, and I think much of its technology is based on the miniaturization and software integration which have been already achieved by smartphones:

https://en.wikipedia.org/wiki/Google_Cardboard

There are currently no self driving cars which are ready for commercial release. Autonomous vehicles, however, have been around in mining and agriculture for over 10 years now:

https://www.i-q.net.au/top-tech/autonomous-haulage-technology-reaches-10-year-mark

https://www.fwi.co.uk/machinery/review-of-john-deere-s-new-itec-pro-steering-system

Reusable rockets are are a nice feature, but I doubt that anyone would consider these vehicles a technological step forward from their predecessor space shuttle program.

Reusable rockets? Some Musk followers aren’t old enough to know apparently that the Space Shuttles started flying in 1981. The last flight was in 2011… 30 years.

What ultimately matters is the price at which a company can put a satellite into orbit and make a profit doing so.

The shuttle was a failure. Each orbiter was supposed to fly 20 times a year, and cost between $20-$50 million per flight. It was wildly over budget, hideously unreliable, and a technological dead end.

Also, it killed a bunch of people.

Space X has already dropped the cost of your basic “10 tons in low earth orbit” mission by a factor of two, and looks set to reduce that number substantially in the next 10 years.

I was opposed to the Space Shuttle back in the day. I would have built the X-20 instead. Oh, well. . .

Reusable Rockets

First-Generation Quantum Computers

Incremental Improvements in Robotics

Incremental Improvements in Battery Technology

Mass production of Optical Chips

Major cost/benefit reduction in electro-optical devices.

None of these are as cool as a Moon Rocket, but real money will come out of them.

None of the FAANG’s would have anywhere near their current revenues without the smartphones and Wireless Data Networks which I mentioned were produced just a decade ago. Most of the NASDAQ would not even be in existence without the big computer, router, and internet innovations which occurred over the last 30 or so years. Big innovations do make big money. More importantly they advance society.

Share buybacks at the highest valuations in history equals a first class trip to chapter 11 bankruptcy.

John Maynard Keynes talked about something like “by-products of a casino”-curious to know what would he have said if he is still alive today ?Perhaps we should ignore him-Nowadays.with so many more animal spirits,it is a much more fun game and besides the brits are not known for their ability to have real fun by the use of opioids

Then I just don’t get it. CNBC has this article today (11/8)…

The bull market’s biggest buyer is back — companies are buying back stock at a record pace this month.

This is a quote from the article: November is shaping up to be the strongest buyback month on record.

Your article says just the opposite. So who do we believe?

No, my article doesn’t say the opposite. Read it!! It says share buybacks never left! Look at the October share buybacks I cited in the article. This is what the entire article was about: that the “blackout period” for share buybacks is a myth.

Reading only the headline is not enough to get an understanding. But commenting on the article after only reading the headline is silly.

So this is the state of “finance” education:

CFO: “I would like to borrow $100 billion”

Banker (really, Wanker) : ” purpose?”

CFO” “I would like to take on higher order liabilities to invest in lower order liabilities”

Wanker: (briefly calculating commission and fees on transaction…) “Sir where do i wire it?”

Meanwhile, the scene at SEC HQ: ______slumber party_______followed by preening of suits and ties in the mens room before going home from work.