But ballooning inventories point at risks next year.

If stock market pundits were hoping for a disappointing GDP print today that would give the Fed second thoughts about its rate-hike path, they didn’t get it. The economy, as measured by GDP, is hopping right along, not at an extraordinary never-before-seen speed, but at a very good clip.

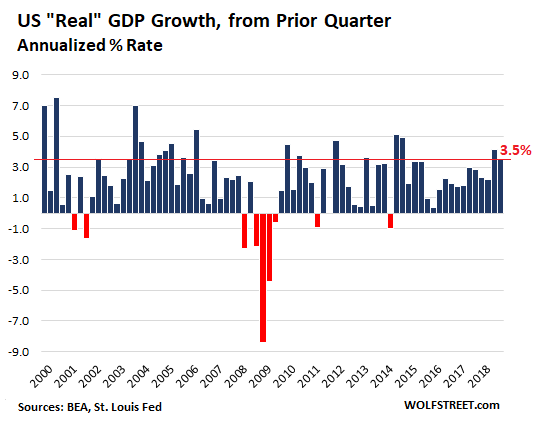

Third-quarter “real” GDP (adjusted for inflation) increased at a seasonally adjusted annual rate of 3.5% from the prior quarter, the Bureau of Economic Analysis reported today. Annual rate means that if GDP continues to increase for four quarters in a row at the current rate, the 12-month GDP growth would be 3.5%, the eighth fastest since the Great Recession, and down slightly from the Q2 rate of 4.2%:

The above measure of “real” GDP – the change from prior quarter, but at an annualized rate – is the most volatile measure, producing the biggest-looking results, both up and down (note the 8.4% plunge in Q4 2008). No other major country I know of uses this measure for that reason.

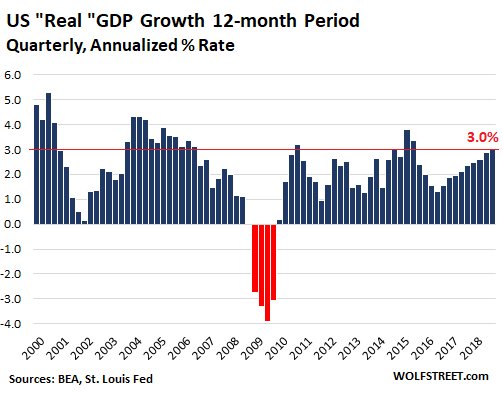

A less volatile measure and producing less big-looking results, up and down, is the 12-month change in “real” GDP, which the BEA’s data set also provides. This is the inflation adjusted, seasonally adjusted rate of GDP growth over the past 12 months. It’s the measure used by the Fed in its discussions of the economy and in its “projections,” such as those from the last meeting. For the 12 months ending in Q3, it rose 3.0%, the fourth highest growth rate since 2010:

Nominal GDP (or “current dollar” GDP), which is not adjusted for inflation, rose 5.5% over the past 12 months, the highest growth rate since Q4 2006. In these current dollar terms, the size of the US economy, as measured by spending, reached $20.66 trillion a year.

This data is the BEA’s “advance estimate” to be revised several times as more data for Q3 accumulates. The next revision will be released on November 28 (“second estimate”).

The BEA outlines some factors that contributed to GDP growth:

- Increase in consumer spending (or “personal consumption expenditures”) – yes, consumers are spending, even if they have to borrow some of what they spend, but hey, it’s a deal.

- Ballooning inventories (“private inventory investment”), a phenomenon that has been going on since late 2016 and picked up speed recently. More on that in a moment.

- Increase in government spending at all levels, particularly at the federal level as we have seen.

- Increase in nonresidential fixed investment, such as office buildings, warehouses, or factories with their assembly lines.

And it outlined some factors that subtracted from GDP growth:

- Sliding exports (in the calculation of GDP, exports add to GDP).

- Rising imports (in the calculation of GDP, imports subtract from GDP). This led to a record merchandise trade deficit in September.

- Lower residential fixed investment. Growth is slowing, as Q3 was down from Q2, but it was still up over the 12-month period. This could take a turn for the worse.

Overall, it was a strong report on the US economy, even if it backed off a smidgen from the blistering pace in Q2.

A worrisome element in it is the continued buildup of inventories. While this adds to GDP mathematically, it can have a negative effect on GDP in the future when businesses are beginning to whittle down those inventories.

The US economy went through this cycle in 2014 and early 2015 with a large buildup of inventories. Eventually, businesses began whittling them down by reducing their orders. This caused a recession in the goods-based sector, including a very visible “transportation recession” (see the red bars in the charts) that brought GDP growth down to 1.6% in 2016. GDP growth was kept in positive territory by the massive US service sector that continued to grow strongly at the time.

This cycle in the goods-based sector will play out again, possibly starting sometime next year. And as last time, the service sector will have to be strong enough to prevent a recession

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“this data is the BEA’s ‘Advance Estimate’.”

To be revised many more times going forward.

First revision due November 28th.

So there you have the long and short of it.

Meanwhile, party on Garth!

China published its Q3 GDP report days ago. It’s edged in stone, even before it’s published. And it’s never revised as new data comes in. In fact, they don’t even wait for the data before they publish their GDP report.

BTW, the US revisions are normally small. For example, the original “advance estimate” of Q2 GDP (nominal) was $20.402 trillion. The revised estimate now is $20.411 trillion. That’s $8 billion difference in a $20 trillion number. This amounts to a difference between advance and current estimate of 0.04%.

So yes, measuring the money that gets spent and invested in the vast and complex US economy is not easy, and the estimates get more accurate as more data becomes available over time. The other options are to do what the Chinese do, or to make up your own number in your mind and go with that, or to fly blindly altogether.

Meanwhile, back at the ranch –

Total US public debt is growing faster than nominal GDP.

Yes, as is consumer debt and corporate debt. It’s all a debt-fueled binge.

“Total US public debt is growing faster than nominal GDP.”

I find this to be an interesting concept. If the government borrows $10 billion, it is going to spend that $10 billion. Both entries add an equal amount to debt and GDP.

What are the situations in which the government borrows the money but doesn’t spend it? Or at least doesn’t spend it in a way that adds to GDP. Purchasing imported products? Paying off treasury bonds?

Maybe the American people can buy imported products faster than the federal guv can borrow and spend money…

Kent,

The federal and local govts collect pools of money that can only be used for a specific purposes. Sometimes they cheat and spend the gas taxes in the general fund instead of on the highway. Sometimes the proceeds of bonds sold for a specific purpose, like a dam project, doesn’t happen as fast as they thought or not at all.

There are also local govts with huge piles of reserves but still borrow for new projects. This was an extremely abused strategy in south FL. Coincidentally, the number of financial types in local FL politics is very high.

Don’t mean to be a grammar nazi but I think you meant “etched in stone”.

:-]

“China published its Q3 GDP report days ago.”

Unless I’m mistaken, you’re referring to the People’s Republic of MadeUp :)

Not a big deal, but…”edged in stone”. Correct idiom is…. “etched in stone”.

Yes, as Bookdoc already pointed out.

I’ve known from day one how to spell etched in stone and double-edged sword. I was a fine arts major in college (before I switched to English, ha!), and we did etchings (intaglio and lithography) all day long, and I knew back then how to spell it, and when I asked girls if they wanted to come up to my apartment “to see my etchings,” it wasn’t a lie. But that doesn’t mean that when I write comments — and I write a lot them — in my special comment software with tiny typeface, that I’ll notice it the next time. This comment section is full of typos, some of them hilarious and very meaningful, and that’s part of its charm.

:-]

p.s.

Historically the Fed can be depended on to do the right thing at the exact wrong time! Like now. Raising rates and tightening going into what looks like a severe downturn, or even a full blown recession.

Party on Wayne.

“the 12-month GDP growth would be 3.5%, the eighth fastest since the Great Recession,”

This sentence seems to say that there have been plenty of 12 month periods since 2008 where the GDP growth was at least 3.5%. Looking at the first chart, I can only see one possibility, and that is from the 2nd qtr of 2014 thru the 1st qtr of 2015 (~3.9%).

You have to read the whole paragraph: 3.5% refers to a single quarter (Q3) and its growth from Q2, which was “annualized” — to show the annual rate of growth. This is a “rate” or a speed. It changes every quarter. So Q3 ran at this speed, and 7 other quarters since the Great Recession ran at a faster speed.

Drawing a line across those tops it doesn’t look so good, but I am just a kid with a ruler

Hold your ruler up against the charts one more time. The trend in the second chart looks quite good. My wooden ruler says so.

I would like to think Fed rates have a huge effect on the economy.

I also think Fed doesn’t have knobs to fine tune the economy – only blunt instruments.

Why would Fed raise rates now when economy has barely started registering > 3% quarterly GDPs?

Is it due to inflation targeting? If so, why not adjust the target (as Paul Volcker says here: https://www.bloomberg.com/opinion/articles/2018-10-24/what-s-wrong-with-the-2-percent-inflation-target)

As I suspected before reading the Bloomberg piece, one time ultra-hawk Volcker, who famously drove the Fed rate well into double digits, has not changed his stripes.

He is arguing against setting a target of 2 % inflation, and is only willing to consider it as an UPPER limit. One percent is fine with him. He points out that even at 2 % : ‘prices double in a generation’.

He is emphatically against the idea of raising the limit to ‘three or even four percent’ adding, ‘I am not a making this up’ about some central bankers floating the idea.

Yes, he disagrees with a target of two percent. The direction of his disagreement can be seen in his statement:

‘I have yet to hear, in the midst of a strong economy, that maybe the inflation target should be reduced!’

Of course anyone can disagree with Volcker.

Good observations. Yeah, that’s even worse :)

Fed created this huge asset bubble by keeping rates near zero for almost a decade – disincentivizing savings and encouraging borrowing. As Wolf says ‘debt-fueled binge’.

Perhaps Fed expects a real-time feedback loop. For example, raising rate by quarter percent and expecting mildly lowered consumer debt levels. But that never happens. Improvements happen too slowly and corrections too quickly.

For a lot of borrowers (businesses, individuals) there isn’t much between ‘everything is awesome’ and ‘sky is falling’.

So Fed can keep raising rates until one day they are suddenly forced to slash it to zero.

The Fed needed to prop up assets (especially real estate) after 2008 in order to keep the banking system alive (LTV ratios etc). This is because the asset values were marked on balance sheets at bubble values. Real estate doubles in value approximately every 10 to 15 years; so by inflating the values temporarily they kept the banks ‘solvent’ for a decade until normal inflation could catch up. Housing prices are rich right now but are not in a bubble (except some parts California which are in bubble territory).

Now the FED will try and delicately back out of this situation and normalize things as much as possible before the next blow up so they have some ammo to work with.

I really don’t care if they hike another 10K basis points. They can hike all they want, it doesn’t affect me until it goes up higher than 25%, my credit card rate. My finances aren’t good enough for a mortgage, so they can hike that too. My financial profile is probably the biggest segment of the country, a parallel reality.

In the mean time, I am spending the tax cut money, new computer, new eye glasses, stuff I have needed for a long time.

“Why would Fed raise rates now when economy has barely started registering > 3% quarterly GDPs?” Because they had previously driven rates to near zero – far below normal – and held them there for 6 years. If they are going to have any room to reduce them again come the next downturn, they need to move them up while growth is improving.

Without Trump and the introduction of hope and animal spirits again, this economy never would have given the Fed to get to where they are now.

Haha. That’s rich. As if Trump or Obama or Bush or Clinton can just make the economy work at will. These guys are mostly just figureheads and diplomats while in office, riding the waves of history their predecessors create. This economy is the result of 0 rates for the past 10 years and a huge influx of millenials hitting prime earning years.

Yes when the SNB prints money to buy NYSE stocks they all repeat the mantra about hope and animal spirits.

Consumers and their individual/personal debt management is also quite solid, reflecting ability to learn and prepare (& scar tissue). The increases in consumer spending, reflect the strongest employment scenario in half a century + wage growth and are accompanied by reasonable personal savings and only modest growth in card and mortgage debt. The banks have provided the credit lines, but consumers are more prudent.

On the other hand, the management of the govt credit card hasn’t been responsible for half a century.

Never a good time to have a tariffs war, but this appears to be as good a time as any to try to level the field.

“Consumers are more prudent”

Which country are you referring to?

https://www.newyorkfed.org/microeconomics/hhdc.html

He’s not saying they’re prudent in an absolute sense, just that they’re more prudent than the banks trying to lure them into debt traps.

And more prudent than they were 10 years ago when the bankers successfully lured them into debt traps and asset-stripped them blind for trillions of dollars. Which the bankers then blew, and then charged the taxpayers and savers for bailouts…

Getting charged twice over for the privilege of losing your job and then your home does wonders for increasing financial prudence…

P.S. Apropos of your link, “household” to the central bankers often doesn’t mean what you think it means; it includes nonprofits and various other entities that have nothing to do with people living in houses.

Also note that the chart is not normalized to inflation, nor per capita or per jobholder, all of which makes a significant difference in the picture. According the FRED graph linked below, which factors in both inflation and the number of workers covered by unemployment insurance, Americans are about 20% more prudent now than in 2005.

https://fred.stlouisfed.org/graph/?g=lLDX

The USA. We just got back to the consumer debt levels of a decade ago and that isn’t even inflation adjusted.

->Consumers and their individual/personal debt management is also quite solid . . . consumers are more prudent.

Sarcasm, right?

Half of US adults can’t balance their checkbooks, 80% live paycheck to paycheck, most carry a balance on their credit cards, averaging over 6K (and rising), US household debt breaks records every year with no end in sight, and US student debt has become a national crisis. Forbes projects the US middle class will largely disappear within ten years.

Your claims are quite simply absurd.

The American consumer’s “prudence” makes my jaw drop.

From the latest Federal Reserve Board’s Division of Consumer Affairs 5th annual Survey of Household Economics and Decisionmaking covering 12000 households:

“On average, people answer fewer than three out of five basic financial literacy questions correctly, with lower scores among those who are less comfortable managing their retirement savings.

“Housing prices in the United States can never go down? (True or False)”: Correct – 60%, Incorrect – 19%, Don’t know or no answer – 22%.

“Buying a single company’s stock usually provides a safer return than a stock mutual fund? (True or False).” Correct – 46%, Incorrect – 19%, Don’t know or no answer – 50%.

https://www.federalreserve.gov/publications/files/2017-report-economic-well-being-us-households-201805.pdf

The test you refer to is here:

http://www.usfinancialcapability.org/quiz.php

I would expect every visitor to this site to find it trivial.

Other tests can be found by googling “financial literacy test”. I’ve found the more advanced tests to be instructive.

Most people stumble on questions about bond prices, not understanding why bond prices move inversely to bond yields.

A lot of people are under the mistaken impression that they need to carry a balance on their credit card to keep up their FICO score. I would be very interested to know where this misinformation comes from. It’s a pet peeve.

It seems obvious that a lack of financial literacy goes a long way towards explaining how a large proportion of the population has become victims of financial predators. Everybody needs to come to this site in order to start fixing that.

Unamused, consumer debt management is noticeably different, e.g. less inclined to take on new debt. Again, total debt is basically where it was a decade ago. Delinquency is low. Credit lines are not utilized to the same extent. Home Equity Lines are no longer used as ATMs.

Student loans are an exception, but the govt has taken over student lending so it is not surprising that is out of control.

Versus the govt spending and versus a decade ago, consumers are MUCH more prudent. Sorry to bring good news, albeit perhaps temporary.

->Sorry to bring good news, albeit perhaps temporary.

Your ‘good news’ has already been debunked, and repetition does not improve it. If you want to apologize, do it for the phony cheerleading.

Unamused, Debunked just because you say so? I don’t think so.

Looks like something magical happened in 2016 to break a downward trend of GDP growth.

Hard to pinpoint exactly what that could have been…it is a mystery

To quote: “It’s all a debt-fueled binge.”

Mystery solved!

A mystery of the ages.

Call it the Trump dump.

The recession in the goods-based sector ended in 2016 (this includes the oil bust, which hit bottom in early 2016). See my recent articles about transportation; the charts show the transportation recession that was part of it. Now inventories are building up again, as they had in 2014 and 2015, which led to the recession in the goods-based sector. So the same cycle will play out all over again, starting sometime next year. I will cover it, so you’ll see it right here.

There was a whale placing bets at around 11:30 am EDT and it completely reversed the market for a while today. So a very big one or two thinks this market is a buy at these levels.

Got my attention as I was feeling good about being short at the time with the S&P off maybe 2.6% or so …and trading the chop pretty well. Now wondering who had that much $ to throw in all at once and do they know someone at the Fed.

There are people who have to put money to work, this is a market like any other. Watching those buy programs kick in and get slammed was interesting. The market held the Wed lows and that is a good sign for the bulls. Leveraged bull and bear ETFs have liquidity, and these securities allow players to value the market at any time. So the great reset is upon us, the real question in any bear market is judging the rallies. That’s what it is all about.

I been told for many years by wallstreet that the markets lead the economy by six to nine months …. so… batten down the hatches and prep

Wolf,

Can you please comment for the readers on how rate increases will impact the multi family real estate market?

MF is currently a very hot market, often run by newbie syndicators, where deals are done on razor – thin spreads. Figure an avg covg ratio of 1.25 – 1.3 on an io loan. I believe it was via one of your links that showed 73% of all CRE loans are io and my guess is that over 80% of multifamily are io. Many of these deals were completed ’13 – ’17 on 7 yr terms, with rates in the mid 3’s. What are your thoughts when the resets happen?

I would like to hear your thoughts on this market, ways to potentially short it or play it

Thanks

The easy part upfront: I don’t know how to short directly the MF market. But some regional banks are heavily exposed to it in a concentrated manner, where a relatively large part of their loan book is MF (this we know from the Fed). If you can identify those banks, it might be something to look at.

Since most of the new MF is high-end, here’s something a landlord told me: In this game, a building has a greater value in the market with high asking rents but lots of vacant units, than filled after cutting asking rents in order to fill those units. Obviously, this won’t go on forever, but it’s going on now.

the inventory build may be a result of front running the tariffs and pending trade tensions escalating. If holiday sales are lackluster look for great deals . this may be the season to be jolly

Yes, some of it has to do that. Tariffs became real this spring, but the inventory buildup started in late 2016 and really got going in 2017. So it looks like part of a normal cycle.

->Tariffs became real this spring

They’ll get even more real in 2019

https://www.washingtonpost.com/business/2018/10/09/trumps-tariffs-will-harm-growth-imf-predicts

Expect vehicle sales to climb before the end of the year, before prices take off in 2019, and then drop like a rock.

https://worldview.stratfor.com/article/how-trumps-tariffs-would-disrupt-north-american-auto-industry

– I look at interest rates when I want to know whether or not the FED is going to hike or not.

– The yield curve seems to have finally turned to a steepening trend. It’s still too early to tell but if/when this trend continues in the next week or two then I also expect the 3 month T-bill rate to fall.

– And then Powell is in a bind. He sounded hawkish when it comes to interest rates but when the 3 month T-bill rate falls the FED will be forced to eat crow and cut rates.