But outside Italy, credit markets are sanguine, and no one says, “whatever it takes.”

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

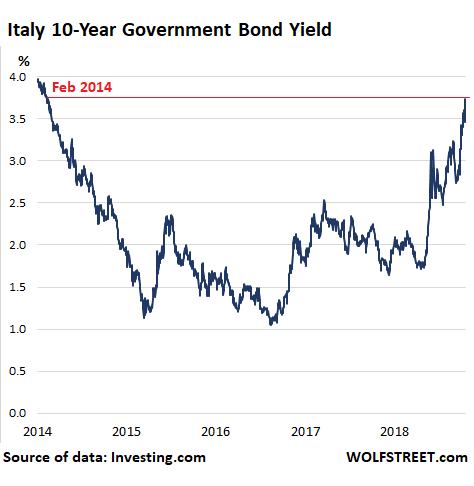

Italy’s government bonds are sinking and their yields are spiking. There are plenty of reasons, including possible downgrades by Moody’s and/or Standard and Poor’s later this month. If it is a one-notch downgrade, Italy’s credit rating will be one notch above junk. If it is a two-notch down-grade, as some are fearing, Italy’s credit rating will be junk. That the Italian government remains stuck on its deficit-busting budget, which will almost certainly be rejected by the European Commission, is not helpful either. Today, the 10-year yield jumped nearly 20 basis points to 3.74%, the highest since February 2014. Note that the ECB’s policy rate is still negative -0.4%:

But the current crisis has shown little sign of infecting other large Euro Zone economies. Greek banks may be sinking in unison, their shares down well over 50% since August despite being given a clean bill of health just months earlier by the ECB, but Greece is no longer systemically important and its banks have been zombies for years.

Far more important are Germany, France and Spain — and their credit markets have resisted contagion. A good indicator of this is the spread between Spanish and Italian 10-year bonds, which climbed to 2.08 percentage points last week, its highest level since December 1997, before easing back to 1.88 percentage points this week.

Much to the dismay of Italy’s struggling banks, the Italian government has also unveiled plans to tighten tax rules on banks’ sales of bad loans in a bid to raise additional revenues. The proposed measures would further erode the banks’ already flimsy capital buffers and hurt their already scarce cash reserves. And ominous signs are piling up that a run on large bank deposits in Italy may have already begun.

It’s not just the banks that are panicking; so, too, are Italian insurers which could face having to shell out more in advance taxes on their premiums as a result of the new budget, assuming it is ever given the green light by Brussels. “We need to be very careful dealing with these issues … because we are one of the pillars of the national system,” the chairman of Italy’s biggest insurer, Generali, said on Tuesday.

Global investors also have big reasons to worry. Italy’s government faces an eye-watering €270 billion worth of bond redemptions in 2019 alone. With interest on Italian government debt rising to its highest level in five years and its biggest margin buyer of the last three years, the ECB, exiting the market, it’s looking like a tall order.

The Bank of Italy is afraid that a vicious cycle is forming over the country’s debt costs. If market tensions don’t ebb, it warns, interest spending could surge above government estimates in 2019-20. Interest expenditures had fallen to €65.5 billion in 2017 from a high of €83.6 billion in 2012, helped along by the ECB’s buying of sovereign bonds as part of its QE program.

In 2012 the yield on Italy’s ten-year bond smashed through the 7% mark. Markets were in a frenzy. And then, Mario Draghi gave his “whatever it takes” speech and unleashed the world’s largest ever QE program.

But that program is ending this year, and at some point next year, the Eurozone’s benchmark interest rates are supposed to begin the long arduous path toward “normalization,” which makes the timing of this gargantuan showdown between Brussels and Rome even more auspicious.

The new big fear is that this month, either or both, Moody’s and S&P, will downgrade Italian debt two notches into junk territory. The potential implications of such a move, not only for Italy but for the European project as a whole, are so huge that many market players are discounting it as a possibility altogether.

“A downgrade to junk could trigger a full-blown (euro zone) crisis,” said Nicola Mai, a portfolio manager at PIMCO, the world’s largest bond investor. “…Which is why I don’t believe the agencies will do it, I don’t think they will want to be the ones causing a crisis in Europe.”

Iain Stealey, a fixed income portfolio manager at JP Morgan Asset Management, concurs. “It would be a very, very big decision, just given the size of the Italian bond market; it makes up something like a fifth of government bonds in the euro zone,” he said. In other words, contagion would spread across the Euro Zone like wildfire.

For the moment, however, that’s not happening. Whereas at the height of the Euzo Zone’s sovereign debt crisis Italy and Spain’s bond yields moved virtually in tandem, today a gulf has opened up between the two.

Since suffering political turbulence in 2016, Spain’s fortunes have diverged from Italy’s. The Catalonian crisis has deescalated. The new minority government, while perilously fragile, is staffed to the rafters with former senior eurocrats who can be counted on to take orders from Brussels. According to the FT, the country is even regarded by some investors as “semi-core,” in light of its strong economic growth, structural reforms and credit rating upgrades.

That may be pushing it a little. But it’s not just Spain that’s weathering the tide. Former crisis-country Ireland’s 10-year yield is just below 1%, while Portugal’s 10-year yield at 2.04% remains near historic lows — nothing compared to the wild gyrations it saw during the sovereign debt crisis when at one point it had spiked to 16%.

That the peripheral Eurozone bonds are not moving in sync with Italy’s this time might seem to suggest, as the FT posits, that investors do not regard Italy’s crisis as an existential threat to the Eurozone. That may be the best-case scenario — given how interconnected the Eurozone is and how large a footprint the Italian economy has. But if it plays out that way, and contagion remains contained, there may be no rescue forthcoming for Italy, just as the ECB’s Italian Chairman Mario Draghi warned last week. Of course, if Italy’s government backs down and agrees to play by Brussels’ rules, that may change, but for now there’s no sign of that happening. By Don Quijones.

The ECB has hired BlackRock, “a market power that no state can control anymore.” Read… Why’s the World’s Biggest Asset Manager Advising the ECB on the Health of EU Banks?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Leave the bonds, take the cannolis.

This whole thing looks like a Greek tragedy, except it’s in Italian. Let’s see if we can cut to the chase & predict what happens over the next few months:

1) Italian dudes say they’re gonna give Italian voters what they want (lots of free stuff & ridiculously early retirement)

2) EU says no

3) Italian dudes say yep, gonna do it

4) Merkel says hard working Germans won’t subsidize lazy-ass Italians

5) Strange-looking lady from IMF says a bunch of stuff and offers cash (a lot of which has come from USA taxpayers) if Italians behave

6) Italy dudes say no and IMF lady gives Italians cash anyway

7) Italy gets a whole bunch poorer (look at what happen to Greece)

8) At no point in time does anybody pay anything back to anybody

…Rinse & repeat…

There is no way Italy gets IMF cash without a massive austerity program. The IMF is not the ECB. It’s a lender of LAST resort.

It kind of sucked into the Greek tar pit and is not looking for another one.

The IMF is not looking to get re-elected.

Past IMF practice doesn’t comfort me (how reformed is Argentina?).

The Italian tar pit is (at least) 6 times as big as Greece’s steaming hot mess, and the IMF spends half its time looking for tar pits to get sucked into (example: Greece)…

Factoid: The Greek bailout cost $310B for 10M Greeks ($31,000 for every man, woman and child). If that same ratio (or anything close to it) holds for 60M Italians, that’s a cool $1.86 Trillion.

The IMF doesn’t have a road show of sales guys hawking loans.

You approach the IMF, they don’t approach you. Lately it has more applications than money.

Argentina’s problems predate the existence of the IMF, which was originally set up to deal with the problem of currency manipulation, or its nice name, competitive devaluation.

The factoid is apt: why on earth would the IMF bankrupt itself

bailing out Italy for 1.86 trillion? It has nowhere near that available.

I think that is a polite way of saying Italy would not accept IMF involvement.

I just don’t see the bond market as a proper reflection of country risk anymore in Europe. Aside from accusations of purposeful manipulation, such as Berlusconi has claimed, and the known ECB private threats used at certain times, for example Trichet’s letter to Zapatero, the market itself is self contained. In other words investors seem to move between bonds of various European countries in an almost Pavlovian manner, acting to profit on the speculative effect of any news. They do not seem to act due to the possibility of a default which in the case of Italy would not be contained, and quite possibly lead to exit. The figures seem to show it is mostly foreign investors involved in the sell off, with some shorting occurring for good measure, moving to positions in more secure European countries, which clearly would also be loss making if the confrontation with Italy were for real, and it well might be, it is hard tell. For the same reason I cannot give great faith to any of the other “relatively saved” countries, the only thing that stands in their favour seems to be that they are willing to play the game, whether with some arm twisting, commotion, or in an almost dignified compromise.

The Italian question will be resolved by next year’s EU Elections.

Salvini has already said as much.

Both the Italian people (& EU people for that matter) will render their verdicts on the likes of Merkel, Macron, Juncker, Draghi & Tusk and I expect it to be less than favorable.

We shall see.

7 months.

The idea that elections can provide solutions to economic problems is problematic.

We can note one thing with objective certainty: there is a VERY high correlation between populist governments and disaster. See Venezuela etc.

In 2012 Italian bonds hit 7 %, effectively bankrupting the country. Then rascal Draghi and ECB rode to the rescue and cut them by 70 %, giving these wackos a breathing space to form their anti-ECB party.

Fine. Go for it. See how much the world is anxious to exchange oil etc. for lira.

It was a second- tier currency IN ITALY before the euro. Real estate was priced in $US.

Today it might not be money outside Italy. As in Greece when they were staging their Greek tragedy referendum and the cash machines ran out of money, the Red Cross had to scramble to line up supplies of insulin that Greece does not produce.

Some agreed to supply on credit. Swiss giant CIBA: cash

The 60+ years of relative calm in Europe since the two world wars, only 20 years apart, seems to have engendered the concept of a ‘net’ a fairy godmother who prevents nasty things from happening.

She doesn’t exist. The closest thing for Italy is the EU and what seems like tough love from the ECB.

“that investors do not regard Italy’s crisis as an existential threat to the Eurozone.”

Smells of Ben Bernanke and his stupid housing comment in 2007

“there may be no rescue forthcoming for Italy, just as the ECB’s Italian Chairman Mario Draghi warned last week.”

You can bet your last penny that when push comes to shove, Draghi will do whatever it takes.

The way the speed Italian bank shares are dropping especially in the last month they’re going to be in deep trouble especially with all the government debt they possess.

“Italy’s government bonds are sinking and their yields are spiking. There are plenty of reasons, including possible downgrades by Moody’s and/or Standard and Poor’s later this month.”

…add incompetence, arrogance, and hawkish presumption of the leaders of the green-yellow coalition and stir well.

Contrary to Greece, Italy is a rich country with private savings well in excess of public debt. Therefore, when Italy finally defaults on public debt, guess who pays the bill?

That depends where people have their savings, and a lot of savings are really just not being so much in debt :-/ . Most Itaian bonds are held by institutions

https://insights.abnamro.nl/en/2018/05/global-daily-who-owns-italian-bonds/

and what was learned by Greece and Cyprus was not that the little guy came off better. Oh well, you always have the Macro/vici European budget to look forward to

“Having a euro zone budget is absolutely decisive if we want to address the populist challenge, the burning question of inequalities…

The European crisis is no more an economic crisis. It is an inequality crisis. It is a political crisis. It is a crisis of delivery. We need to deliver more. That is what euro zone reform is about. It is not technical. It is highly political,”

That being his fairness the more equal than other yet admitedly unpopular “ex-communist” union economics comissar delivering his self-serving bid for attention…or maybe just on a last ditch attempt to mess up anyone’s thinking in the most technical manner possible : It’s for everyone, even if you disagree, except if you disagree.

New European alliance to form underpopulist banner.

The recent surge in voter participation across Europe has awakened a number of its politicians to the necessity of creating an opposition party capable of drawing off the newfound enthusiasm.

Martin Hardhammer interviews Pierre Moscovici on the meaning and aims of this new political group.

M.H. Hello Pierre, it is good to see you active once again .

P.M. Yes, well you know politics is a delicate balance. Sometimes it is better to just not be seen.

M.H. You mean when you appear better off than everyone else.

P.M. Yes, and that.

M.H. Now let us talk of your re-appariton, the new party you are forming, its aims and ambitions.

P.M. Yes, certainly. Many of us have watched with consternation as other would-be leaders have increasingly won over the popular vote across Europe, posing significant challenge to the development of the communal sentiment we represent. We think it necessary to act to calm this surge, which is clearly an emotional product.

M.H. Yes, I understand your feelings, please continue.

P.M. As perpetual representatives of the downtrodden and less fortunate , we now find it fitting to found this new political party . We are aware that our mission is near impossible, because we rely on both creating this unfortunate class as well as maintaining its belief that we represent some kind of solution. So we have taken the unprecedented step of being absolutely transparent in the naming of our party…

M.H. Which is?

P.M. … please, let me finish, the naming of our party. Firstly you must, you will, understand that our title is reactionary. We do actually want people to be inclined to vote for us , those poor rejected people we are nurturing. Secondly, we will not pretend our policy will be liked, it is impersonal and not designed to satisfy anyone in particular but rather the management of the whole.

M.H. Which would be you.

P.M. Yes.

M.H. You seem to have forgotten to give us the name Pierre.

P.M. No, you interrupted me. The deliberation was tedious on the choice, something that further reflects the difficulty of relating to the overall lack of inspiration we represent. Eventually an anonymous member of the naming committee had an idea and it stuck out as being the only available suggestion. That moment of unseen humility gave us both our initials, P.U.T.A.I.N. and their meaning, People’s Unpopular.

M.H. …..And the T.A.I.N. ?

P.M. Yes, that has been a problem. Someone suggested Front, but it did not fit. So we just leave it at that, OK?

M.H. Yes, well Pierre that has been as inspiring as always to speak to you and we wish you all the success you deserve. Thank you.

P.M Thank you Martin, a pleasure as always.

Is this a satire or a real interview?

“According to the FT, the country is even regarded by some investors as “semi-core,” in light of its strong economic growth, structural reforms and credit rating upgrades.” – sums up why I find reading the FT mostly a waste of time and rather come to read blogs like this. Including the delightful irony following that FT quote.

Also consider The Telegraph and the quoted author an official propaganda channel. Talking about a bank run may well threaten one, which might be the very intention. Greece rinse and repeat – or so the EU bureaucrats hope.

Thanks Don Quijones for this very informative analysis of the Italian debt crisis.

The difference in Spanish and Italian yields are likely political as opposed to financial. As long as Italian pols refuse to play ball with the EU there will be little support for their bonds. But Merkel will soon be gone, and Macron is despised in France, so the politics inside the EU will be markedly different soon enough.

Slightly O/T , Spain’s supreme court suspends yesterday’s sentence on bank liability for mortgage setup fees, after said banks got pummelled. It says it recognises ” the enormous social and economic repercussion ” of the previous sentence.

This article was a little premature. Spainish banks are sinking now, Deutsche Bank following German car sellers down lower. There is no escape if the Europeans don’t stick together. But the southerners want never ending breaks and the northerners won’t give a half percent leeway on what is and always has been a fictitious budget. Europe is a giant bureaucracy, nothing more. I still think China will be the first house of cards to come down, but Europe will give creditors a run for their money.

Ha, if I need to look every 5 minutes maybe this isn’t such a good investment? Anyways, somebody must have their Court don’t rock the boat, because the water line is too high (or is it too low). I’m not an expert by any means, but I wouldn’t touch a European Bank, especially Spanish ones, with a ten foot pole nor even put my money in Euros. Every time I go over to Spain, I wonder what the heck holds the place up….

Italy has a similar debt to GDP ratio as the US. They also have roughly similar bond yields. The Italian government is hostage to two opposing partisan groups, like the US. We have both have, or had, a “bunga bunga” president. Both economies are held up by the EU, (SNB buys our stocks by printing cash and depreciating their currency to bolster exports, otherwise their liquidity manipulations benefit our market). We both have immigration problems. The youth in both countries live in their parents basement until they are forty. We were both once great empires. We both have strong religious institutions. Debt forgiveness is probably less likely in the US while the US may break up on a state by state basis. All debt is not created equally.

What we have that Italy doesn’t have is control over our currency. Huge difference.

Ambrose Bierced

Don’t know where you got your “Italy has a similar debt to GDP ratio as the US” comment. 2017 numbers:

Italy 131% debt to GDP

USA 105% debt to GDP

Yea, and they’re both going up.

“A downgrade to junk could trigger a full-blown (euro zone) crisis,” said Nicola Mai, a portfolio manager at PIMCO, the world’s largest bond investor. “…Which is why I don’t believe the agencies will do it, I don’t think they will want to be the ones causing a crisis in Europe.”

This quote really bothers me, especially after everyone the ratings agencies bungled the ratings of MBS ten years ago.

All that pain, and they still haven’t learned anything?

Can they really be called “ratings agencies” if they rate securities based on the outcome people are hoping for?

I suppose the real question is: we know the system is corrupt, and we can’t change that, so how can we profit from it?

PokerCat

“Can they really be called “ratings agencies” if they rate securities based on the outcome people are hoping for?”

This explains the problem: rating agencies GET PAID BY THE ISSUING AGENCY.

At the very least, this is a huge conflict of interest. Suggestions for eliminating the conflict range from simply eliminating rating agencies (leaving investors in the dark) to expecting investors to do their own research (don’t know about you, but even as a retired CFO, I sure wouldn’t be able to do that in a timely & accurate manner).

Charging a one-time fixed fee at issuance (0.001% = $100,000 per $100 million face value?) technically might work, but getting everybody to agree to it would be like herding cats.

Just read this in NYT:

“The rating on Italy’s debt was slashed on Friday by Moody’s Investors Service to one level above junk in a reaction to the Italian government’s decision to accept higher budget deficits in coming years.”

Shuold we all be worried now?

Frank

Moody’s definition of Baa3 (quoting): “Baa3 – medium grade”.

You should;d only be worried if you didn’t find that rating laughable.