It shot up 240% from long-run average and 500% from a year ago.

Reading the purposefully repetitive and strategically mind-numbing minutes of the FOMC meetings, such as the minutes that the Fed released today, can be a brutal affair. But it’s where the Fed discusses the economy and vaguely hints at risks balling up in it. It sprinkles in clues about its decisions on interest rate hikes. So these minutes are a link in understanding where interest-rate policy might go in the future, and they’re designed to communicate precisely that.

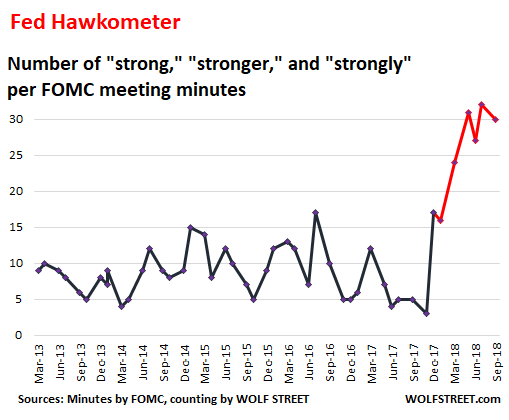

To allow everyone to dodge the torture of having to sort through it all manually, I have designed a nifty Fed Hawkometer – pronounced haw-KO-meter. It’s untested, and results may vary, as they say. If it appears slightly tongue-in-cheek, that’s OK. It measures how many times the minutes use the word “strong,” “strongly,” and “stronger” to describe the economy:

The average frequency of “strong,” “strongly,” and “stronger” between January 2013 and December 2017 was 8.7 times per meeting minutes. In the minutes released Wednesday afternoon of the Fed’s meeting on September 25-26, it was 30 times. The average over the past four meeting minutes (May, June, August, September) was also 30 times. That’s an increase of 240% from average!

And the frequency in today’s minutes shot up 500% year-over-year. In other words, the Fed Hawkometer is now redlining.

Here’s a sample of those 30 occurrences in the minutes, released Wednesday afternoon, of the Fed’s meeting on September 25-26 (bold added):

- Equity markets had posted strong gains

- GDP appeared to be rising at a strong rate in the third quarter

- Total nonfarm payroll employment increased at a strong pace, on average

- Real PCE [Personal Consumption Expenditures = consumer spending] appeared to be rising strongly in the third quarter

- Stronger-than-expected average hourly earnings

- Stock prices increased for many sectors in the S&P 500 index, as the second-quarter earnings reports for firms that reported later in the earnings cycle came in strong

- In part because of strong earnings

- Economic activity rose at a strong rate

- Job gains were strong, on average, in recent months

- Household spending and business fixed investment grew strongly

- Recent data pointed to a pace of economic activity that was stronger than they had expected earlier this year

- These included strong labor market conditions

- Recent strong growth in GDP may also be due in part to increases in the growth rate of the economy’s productive capacity

- Participants generally characterized consumption growth as strong

- Business fixed investment had grown strongly so far this year

- Input prices had been bolstered by strong demand

- Greater-than- expected effects of fiscal stimulus could lead to stronger-than-expected economic outcomes

- Real economic activity rising at a strong rate

- Strong labor market conditions

In my Fed Hawkometer above, you can see that the post-crisis economy was running along recovering, and things were “strong” in some areas and still waiting for inspiration in others, but starting in December 2017, the mentions of “strong” started piling up massively.

This is an indication of how the Fed – given the data it looks at and what its contacts in the business community are saying – thinks about the economy and where it is going, and by extension, where monetary policy should go.

There were a few tidbits in the minutes that gave a clue as to what is on the Fed’s worry list, including risks to financial stability due to inflated assets prices that are used as collateral. The reference this time was to one of our favorite topics, “leveraged loans,” an asset class the Fed and other bank regulators have been warning about for four years:

Some participants commented about the continued growth in leveraged loans, the loosening of terms and standards on these loans, or the growth of this activity in the nonbank sector as reasons to remain mindful of vulnerabilities and possible risks to financial stability.

And relatively new references started to crop up in larger numbers, namely to the “stimulative” effects of fiscal policy, including:

- “Stimulative federal tax and spending policies”

- “Stimulative effects of the changes in fiscal policy”

- “Fiscal stimulus”

- “Recent changes in federal tax policy”

In the prior minutes from the August meeting, “stimulus” or “stimulative” appeared just once, in the phrase, “stimulative federal tax and spending policies.” So clearly, these stimulative effects of what I have come to call a stupendous spending binge and big-fat tax cuts are keeping the Fed Hawkometer at the redline.

As a flood of US debt washes over the globe, someone is buying these Treasury securities. Here’s who. Read… Who Bought the $1.6 Trillion of New US National Debt Over the Past 12 Months?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The real question is whether these rates highs would balloon the cost of servicing our debt and the ramifications of these actions. Also, the Universal Postal Service might get renegotiated likely will affect Amazon, however, more leaves to be seen!

Yes. When FED tighten, they will suck up world savings into US treasuries to fund US debt. The world will be sucked dry and die. When US can NO longer service it’s own debt, FED can always print to pay debt. But by then, the rest of world is already in waste. So there is no worry about the US. It would inflict some pain on itself but mike the rest of the world. That, ladies and gentalman, is what means to be the world reserve currency.

Some relatively recent history: In 1978 the US dollar almost collapsed.

US tourists around the world were asked to pay in local currencies including Italian lira. US citizens also fled dollars: seeking gold. D-Marks. Swiss francs, art. etc. US inflation was double digits.

The US had to issue bonds denominated in Swiss francs.

Why not issue bonds in the world reserve currency? Because no one wanted it. No one believed it would continue to have that status.

Arrive Paul Volcker who brings down the hammer. The Fed starts rising a whole percent at a time! And then does it again.

The US annual deficit in 2018 is now a trillion a year. That amount, one thousand billion, was the accumulated total DEBT of the US when Reagan became President. After two World Wars.

He doubled it in 4 years, courtesy of tax cuts supposed to pay for themselves (the ‘Laughter Curve’ )

And now we’ve just had ANOTHER huge tax cut. And lo! the deficit is up. Again.

All we know is that if the dollar collapses AGAIN, the problem can’t be solved by printing dollars. If the Fed seems proactive, or ahead of the curve, it’s because it’s been there.

This Fed chairman seems to have guts to stand up to the leader of his party. Few Republicans these days seem to possess that much courage.

It is still hard to trust a banker. Moreover, after helping banksters enrich themselves at the expense of the public for decades with covert aid and ultra low interest rate loans to insolvent banks, the Fed had little wiggle room left.

If there is a loss in faith in our treasuries or dollar the interest rate spike could quickly render the US government unable to meet its current liabilities. It is only a matter of time and just a little bad luck.

Parasites like the banksters will suffer too if their host (US government/economy) collapses, like tapeworms in a dying man. Poor little Fed banksters; the end of their parasitic lives (since they “coincidentally” always help the billionaire banksters) may be near.

Poor fuhrer of the rich… He just wanted to give his billionaire cronies some return on their money by tax cuts funded by money printing-digital creation. Powell is no longer helping him. They may have to actually pay taxes… Some sad day.

So, let’s say the fed starts inflating away its debts again. Where do all the investors go? D-Marks is gone, YEN will continue its death by demographics, swiss can only absorb so much before rates go deeply negative, few would rather take a gamble on emperor Xi, eurozone its not clear what you are buying, and GBP is in the process of shooting itself in the foot (possibly head).

On the other hand, US is a big economy with very good demographics (lots of babies, easy to immigrate more workers if they want), is still an industrial powerhouse, has the most powerful military in the world, and is largely resource self-sufficient.

After the GFC many of my suppliers wanted payment in EUR. Everyone was saying it was the end of the USD as reserve currency. Then the eurozone crisis started, and everybody went back to USD to take their beating there. Perhaps that was all engineered by the deep state, or perhaps the US got lucky, but either way I do not see any country threatening US hegemony for the next couple of decades.

Emerging markets are volatile… but their returns are more than double that of the US. No risk, no reward.

“….courtesy of tax cuts supposed to pay for themselves”.

Tax revenues did not decline with the tax cut; tax revenue actually increased. So if I bring in more money and still get deeper in debt …

The tax cut is one reason why Powell and crew have to stay the course. They cannot relent, even for a second. Three Fed insiders (Greenspan, Fisher, Lindsay) spelled it out in 2015. If the excess reserves are allowed to be translated into reserves (i.e., turned into credit = debt) then the economy will burn super hot, and massive inflation — and possible bond collapse — will be inevitable.

Onto this scenario is overlaid massive fiscal stimulus (tax cuts). The only tools readily available are the FFR = IOER and reduction of excess reserves = QT.

Those who don’t like long bonds falling by 4% should consider the impact if they fall by 40% or 80%.

The link:

https://www.bloomberg.com/news/videos/2015-05-19/greenspan-fisher-lindsey-on-interest-rates-economy

Amusing: The panel coordinator has no idea what the panelists are talking about. A fine candidate for the mainstream financial media.

It will really affect eBay, not Amazon.

The Fed sees things the rest of us must miss.

You’re just jealous because The Voices only talk to them.

I’m trying to decide whether the Haw Kometer may predict a Market Cascade Triggering Event by comparing it to complementary data series, or whether it may be useful in indicating the right conditions for a Cascade Event, or both, or neither.

My brain is full. I am quiet now.

I am frequently concerned that I may be totally out of my league and just don’t know when to shut up.

and the Hawkier the Fed gets the more the flock of global doves draws quarters; EU, BOJ and PBOC. All the Fed can do is separate US monetary policy from ROW creating more distortions until vibrations shake the machine to pieces. Coordinated global CBs got us out of one mess and lack of same will get us back in.

Yes. Their vision has been remarkable. Historically, the Fed leaders saw how to enrich their sponsors with ultra low interest rate loans to insolvent banks for decades that could not have gotten other such GIGANTIC loans from any other lenders (without more frauds), who knew of their massive liabilities all while successfully deceiving the American people.

Supposedly, however, many of them were too blind or stupid to realize that tens of thousands could not afford to pay for adjustable interest rate loans on expensive homes without keeping such low interest rates given their relatively low, not-growing income. Brilliant nobel prize winners all or unindicted, well-connected crooks? You decide.

Yep. The Fed sees things that the rest of us miss. Best economic forecasters money can buy. :)

“We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though.” Ben Bernanke – July 2005

Yes, the FED is full of high IQ employees and yet the housing collapse caught them by surprise. And yet they are still running the show and sounding super smart.

Central planning at it’s finest. Luckily 1/1024 isn’t good enough at the Fed.

Wolf, you might want to do an article on how QE unwind helps to reduce debt because some people are not getting it.

Of course that reduction is not much overall but it does help.

QE unwind does not reduce debt. It just rolls it over from the Fed to the general public.

To see why, consider the Treasury has to pay off the bond held by the Fed. To do that, the Treasury has to sell a new bond to the general public (mostly in the US).

If the taxpayer paid for QE going in and going out then there is a lot more liquidity in the market than is generally perceived.

?? QE unwind doesn’t reduce debt. All it does is put back some of that check kiting money that the Fed gave to the Treasury when the QE started, back on the books as interest paying bonds which are sold to investors. That debt should have been paying interest as bonds on the open market back when the Federal debt was originated.

So QE is a way to reduce Federal Debt, by not paying interest on that debt until the QE is unwound. QE unwind will increase Federal debt because now that debt has to pay interest, extra money which the Federal government already does not have, so it will have to borrow even more

raxadian,

The opposite is the case. The QE unwind turns a former buyer (Fed) into someone who is walking away from the market, and other buyers have to be lured with lower prices and higher yields to take its place. The Treasury market faces two big headwinds: the QE unwind and the simultaneous huge supply coming on the market.

Wolf, there was no crowding out of capital for the last ten years, which was accommodated by QE, as compared to the 1980’s – 1990’s when government spending competed with private capital spending. Will the gradual phasing out of QE force government spending and private investment to compete in the market place for shrinking capital. In your recent post you stated that 70% of government debt was being financed within the US. Will the huge government deficits restrict private investment in businesses or will capital come from some other external source?

Good questions!!

:-]

If most of our debt is financed internally and deficits are large while rising interest rates attract foreign investment, it doesn’t add up.

Interest on excess reserves at the fed killed the overnight lending business of banks, which was a decent revenue source for many banks. If you want to see where money will come from in the future, you need to keep an eye on the contraction of excess reserves. An increase in the overnight lending business will spill business into the rest of the funding world. If the banks keep their money at the fed, that’s not a positive sign for the expansion of lending.

While Wolf is correct…the timing however is the key. The Fed is ok walking away now because it KNOWS there are (European) replacement buyers for U.S. Treasury debt AND the U.S. economic numbers support a rising interest rate…..regardless of the servicing issue higher rates creates.

The same thing is happening in Europe…but their gov’t bond market is so jacked up by previous ECB intervention/manipulation, that there are NO alternate buyers lined up…..partially because they are WAY behind the curve on interest rates than the U.S. Because of the inevitable Euro devaluation/political upheaval, smart European investors won’t buy Italian/Spanish/Greek/etc gov’t debt (even if interest rates jump 5% higher…due to the FX risk if the Euro breaks)….so THERE IS NO TRUE ABILITY TO ROLLOVER their existing debt if the ECB doesn’t buy it….which they can’t due to treaty limits. (Private investors will demand interest rates jumps that crush any possible budget for those states in deep trouble already.) Defaults are inevitable imo…..which pushes investors to invest elsewhere.

Since most of the investors are REQUIRED to be in fixed income securities….the U.S. treasury market is one of the few places it can turn to when the European treasury markets starts melting down (plus our interest rates and the FX effects make it comparatively attractive from the alternate.) This provides the underlying buying of U.S. Treasuries even as/if U.S. deficits continue to increase.

Eventually, interest rates in Europe will rise high enough and FX gyrations will calm down such that the risks are worthwhile and the international money flows will reverse…..and THEN the U.S. public debt market gets to go through its default cycle.

->There were a few tidbits in the minutes that gave a clue as to what is on the Fed’s worry list

Unless they’re feeding you red herrings.

Second-guessing and keeping up with the devious and clever can be tedious. They like to frustrate people by misleading them into dead ends in the maze, and they cunningly alter the maze for good measure. Sometimes even I get fooled.

“Sometimes even I get fooled.”

All the time, even I get fooled.

Powell knows that the BIS has issued warnings to raise rates since 08 GFC. Trillions upon trillions have been invested over the last decade and now the FED is forced to make a concerted effort to normalize what’s left of the Western empire of Central Banking before the next crash in asset bubbles leaves them financially unprepared to increase stimulus as they did throwing everything but the kitchen sink at the post-Lehman debacle.

Now they only have the kitchen sink to throw at the next crash which should be due right about now if we listen to the latest BIS depression forecast which is accurate IMHO.

MOU

– Nonsense. The FED is overturning every stone to justify a new rate hike. By using the words “STRONG” as much as possible they are trying to convince the public that the economy is still strong. And that, in turn, seems to hoodwink investors to think that the current “correction” is just that (“A correction”) and that investors should continue to buy more stocks.

– And that seems to be working. The 3 month T-bill rate surprisingly continues to rise and has become VERY “overbou”ght”.

“Surprisingly” only to you.

– In the last months of 2017 and january of this year the stock market kept rising. Along with the stockmarket the 3 month T-bill rate kept rising. But a divergence emerged in january of this year. The 3 month T-bill rate no longer rose and remained flat. That was for me the warning sign that something was “afoot”.

– Right now there’s another divergence that tells me that something is “afoot” as well.

– A rising 3 month T-bill rate in february 2018 and right now tells me that the dopes are still in a “buy the dip” mood.

The top of the US markets in January aligned pretty well with the 10Y treasury note bucking out of the ~30 year long descent channel. Coincidence? https://i.imgur.com/uQd6fXR.png

Weary Patience,

Well… if you go back a few more years to the beginning of the descent and then draw a line, you see that the 10-year yield broke out of its descent channel in August 2016 and has been breaking out ever since. This 35-year bond bull market died two years ago:

Thanks for further info, Wolf. The charts site I use only went back to ~1988 availability. :)

The fiscal stimulus is enabling the Federal Reserve’s tightening.

It’s possible that this is actually good policy. It may well be better to have 2% inflation and 3-5% interest rates, than sub-1% inflation and 0% interest rates.

However, with total Federal debt increasing as fast (or faster) than nominal GDP, the credibility of the currency is at risk.

Well, with debt accelerating and the cost of maintaining the debt accelerating you have a vicious cycle of increasing debt. Does not strike me as good policy, worse once the sugar high is worn out there is no way to stimulate the economy if recession comes down the pike.

They also may be signalling a .05% increase is next

Baby steps are over

The fact is that income derived from investment interest is liable to be taxed in many cases. If the average effective tax rate averages out at say 25%, then long term a ‘level playing field’ comparison between inflation and bond yields should be a ratio of 3:4. As an example inflation 3% bond yields 4% . Obviously this is over simplistic and can only be a general guide.

Historically bonds have yielded CPI-Inflation + 3%. TIPS used to do that. Then then went negative for a bit, but now the yields are back up to CPI-Inflation + 1%.

The notion that bonds should only yield inflation after taxes is interesting.

The puzzle of why over a decade of interest rate reductions failed to stimulate the Japanese economy is solved by equation (15). Nominal GDP growth is determined by credit creation used for GDP-based transactions. Interest rates do not appear in equation (15). Further, an inspection of the link between credit growth and interest rates shows that there is not a robust negative correlation between the two (Werner, 2005). In other words, it is not surprising that lower interest rates are not able to stimulate the economy, if the key variable driving growth – credit for GDP- transactions – is not growing. Likewise, raising interest rates should not slow the economy as long as credit creation for GDP transactions continues to grow. It could be that interest rates are not only an ineffective tool to reduce or induce inflation or deflation but Fed policy is a reaction and lagging both growth and the time at which these data are calculated. Surprisingly the evidence that interest rates work like the Fed says it does has hardly ever been studied according to Werner.

Who has said or concluded that lower interest rates have not and did not stimulate the US economy? “Stimulate” is a relative term. If low interest rates kept the economy from deep depression but little growth was seen over a decade; well I’d say that was pretty good “stimulation”.

People and economists who use formulas for understanding the world will always be applying the last insight to the latest new twist. The Japanese experience has more to do with the culture and near Depression they experienced than ZIRP ineffectiveness. Likewise, the US current experience with inflation and unemployment does not fit the past models of Phillips as well as the mind numbing regurgitation of the inverted yield curve rule. Too many key variables have changed.

Powell is fighting the last war. He will send the economy into recession; one that was coming anyway. It’ll just be quicker and deeper.

By my litmus test, it is already happening. Several mail orders were filled in quick time when 1.5 years ago they took 7 weeks. They are building related so draw your own conclusions. Also, real estate in our once hot market is sitting unsold now for many weeks. Somewhat overpriced, but not that much. Autos have been slowing as all the bubbas have bought (on paper) their monster dually diesel stomping pickup trucks for their construction business that is soon to fall into bankruptcy.

Perhaps all true, but how do you prove a negative? (excuse the play). Seriously, the argument always goes like this, “But if we hadn’t have done____________, there is no telling how bad things would have been”? Or my favourite, “By doing ____________, we most likely averted__________,. We’re not _________. (fill in the blank with Italy, Greece,….).

I agree with you, they are lagging and most likely winging it, at least I took this from your comment.

“…raising interest rates should not slow the economy as long as credit creation for GDP transactions continues to grow.”

That free money entering the system loses its ability to be stimulative … year after years of ZIRP failing to lift anemic sub-3% GDP growth would support that notion. However, higher rates have been followed by recessions and not linking any causality there is surprising. In any models, rising rates would weight heavily as an independent variable – Timing is a more difficult dependent variable.

Q3 gdp estimates are again 4%+, e.g. Atlanta Fed and the predictability of the rate hikes helps economic participants prepare, but even a FED pawn gains power as it is pushed down the board ….and will ultimately become a queen. Hopefully, not a pregant one.

Barry you are right. Raising interest rates will pull money out of assets, but not the economy. The Fed’s interest rate control is ineffective for GDP transactions. They can only create a false wealth affect-an illusion of wealth.

The Fed controls short term interest rates. Which in turn influences an unknowable amount of global decisions where Trillions of Dollars are influenced either directly or indirectly. I liken it to pulling on the emergency brake on a car going 100 miles an hour that’s almost out of gas. Pull too much and the car stops and no one is sure there is enough gas to get it going again. Don’t pull enough and the car might hit a tree or go off a cliff at 100mph. I think the Fed’s true motivations are misrepresented. Stimulus programs provided by the Trump administration are temporary. Interest rates changes have a massive and mostly an unpredictable effect on the global economy. I think the Fed is raising interest rates to attract global funds back into short-term Treasuries. They don’t have a choice. The government needs funding, consequences be damned. Trump knows the Feds actions create unpredictable consequences. He’s already tweeted out who to blame. The Fed’s ivory tower image prevents them from deflecting the blame. Should the economy implode or explode for any reason…thanks to Trump the Fed will be left holding the bag.

this is the last chance to normalize the economy. it’s going to be very painful with a lot of naysayers but it is the only possible way back to some semblance of a market economy.

The only way to “normalize” the American ecomony is to fess up that we are a lot less productive than we make believe. This in turn means that our standard of living is way beyond what we can support. This in turn means the entire military big stick industry needs to be slashed, housing needs to return to what it always was (a roof over your head) and of course the financial industry and all its BS cut to the bone. This also means we have to produce alot more of what we consume including all or most food, equipment, etc.

Smaller cars and trucks would be a nice start too. This country is such a dumb ass!

Normalizing requires that the USA reinstates Glass-Steagall Act and that manufacturing is fully restored across the continent of North America. Given that the Central Banks fail to fully grasp what a balanced economy really is, it is highly doubtful that mere interest rate incremental rate rises will suffice to ameliorate the difficulties that the GFC has imposed since Bear was merged with JPMorgan Chase back in 08.

The debt based economy since manufacturing was sold off to Mexico & China back in the 80s is not sufficient to fuel the economic engines of growth as envisioned by the planners that decided to eliminate manufacturing from North America due to the cheap costs on serf labour in Mexico & China. Wall Street mistakenly thought that China could be the manufacturing hub of the world and the eternal slaves to Wall Street hegemony but over the last 35 years China has overtaken the USA as a worldwide powerhouse of manufacturing that Americans can only wish they had today due to their incompetence on decision making back in the 80s.

Without the tripartite post-WW2 market structure & architecture of a solid manufacturing base to support a robust financial market economy and defence industry there can be no resolve for average market players who now understand the need to have a balanced economy after 35 years of a failing debt based economy with requisite service sector employment that has failed to undergird that incompetent business model otherwise known as a debt based economy.

Man cannot live on debt alone. And Central Banks cannot function in a zero interest rate environment. Normalcy is desired after three decades of abnormality at the top.

Lastly, markets & market participants all base off of expectation. If Powell projects clear expectation unequivocally it is best for markets.

If that guy in the White House disrupts the rate normalization & telegraphs unilateralism and FED indecision we will evidence weaker potential for normalized market economics in the future.

Powell is effectively taking a page from Paul Volcker’s tenure in contradistinction to the incompetence evidenced by Dr. Greenspan’s tenure. Clearly, everyone reading this would say that Volcker was the most responsible FED Chair in the history of so-called ‘Capitalism’. Unfortunately, Powell is mired in Hyman Minsky’s Late Stage Ponzi Capitalism whereas Volcker did not have to deal with that at all.

Powell has the worst mess in the history of Capitalism to clean up and the last thing he needs to deal with is an idiot like Trump.

MOU

MOU

Maybe the addition of stronger language gives the Fed more ammunition to defend itself against Trump’s criticisms. It may just be a political move.

I’m still not convinced.

As long as the Fed confines itself to a maximum rate increase of just 0.25% in a “strong” economy times 30, can it every described as “hawkish”?

Hawkish? Nope, but there is a wise tale of the straw that broke the camels back. Absolutely applies here as well. Of course, it will not be the last straw that gets the blame.

It would be a just world if the media, and the Fed for that matter, were forced to communicate by playing music. The truth would be so much easier to detect.

More like their “experiment” (pulling demand forward) failed as predicted by many to produce lasting results. The entire premise of inventing the future is absurd, they simply rescued special interest groups from demise at the expense of the remainder of society.

I made a quick script to count the words, here are few more that appear most frequently:

(‘monetary’, 21),

(‘Committee’, 21),

(‘growth’, 21)

(‘policy’, 41)

(‘economic’, 47),

(‘rate’, 51),

(‘inflation’, 51)

Ups, I think I used text from September 25-26, 2018

Here is count for same words from current meeting, just having some fun learning basic programming and trying to have computer do some work ;-)

(‘monetary’, 10)

(“Committee’s”, 17)

(‘market’, 24)

(‘growth’, 27)

(‘policy’, 29)

(‘economic’, 36)

(‘inflation’, 48)

(‘rate’, 50)

“the Fed discusses the economy and vaguely hints at risks balling up in it.”

The Lord giveth and the Lord taketh away.

In retrospect, this whole QE thing was a long term bad idea, done for very short term gain, just like the recent corporate tax cuts.

That Federal debt could have been marketed off with much lower interest rates back when the QE was done. Now it will just add even more to the Federal debt as interest rates go up and these bonds get sold at the higher rates

https://www.accountingtoday.com/news/banks-brace-for-fasb-cecl-credit-loss-standard

Looks like the banks will not be able to carry non-performing assets in 2019 like they did in the past i.e. FASB 157 carrying asset values at historical value.

During the last recession people complained that the banks were not lending. The new FASB will make it significantly worse next time around. Very hard to hit the banks with everyone else getting a beating.

https://www.ispyetf.com/view_article.php?slug=The_Simple_Trick_That_Skewed_the_S%26Ps_P%2FE_Ratio_Fo&ID=368#rkBld6p6yvTm3tkF.97

FASB 157 suspended by Congress to aide banks in 2007. Mark to market suspended to mark to make believe. Now you know the rest of the story.