Nightmare scenario for the markets? They just shrugged. But homebuyers haven’t done the math yet.

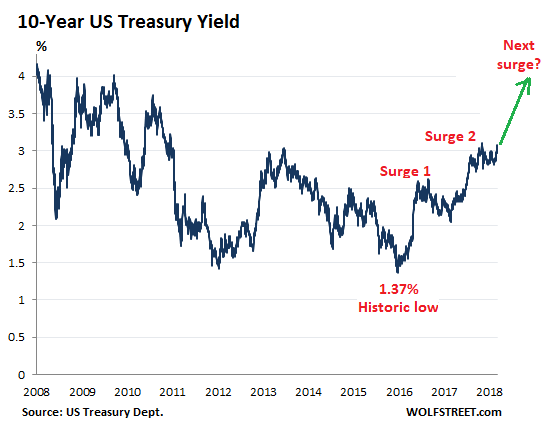

There’s an interesting thing that just happened, which shows that the US Treasury 10-year yield is ready for the next leg up, and that the yield curve might not invert just yet: the 10-year yield climbed over the 3% hurdle again, and there was none of the financial-media excitement about it as there was when that happened last time. It just dabbled with 3% on Monday, climbed over 3% yesterday, and closed at 3.08% today, and it was met with shrugs. In other words, this move is now accepted.

Note how the 10-year yield rose in two big surges since the historic low in June 2016, interspersed by some backtracking. This market might be setting up for the next surge:

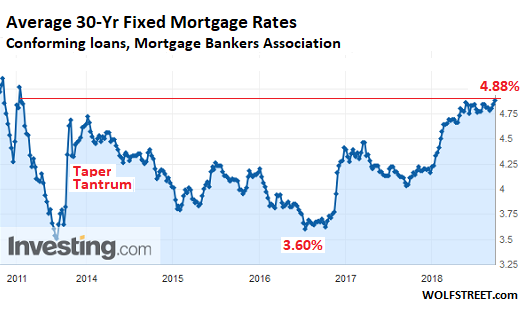

And it’s impacting mortgage rates – which move roughly in parallel with the 10-year Treasury yield. The Mortgage Bankers Association (MBA) reported this morning that the average interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) and a 20% down-payment rose to 4.88% for the week ending September 14, 2018, the highest since April 2011.

And this doesn’t even include the 9-basis-point uptick of the 10-year Treasury yield since the end of the reporting week on September 14, from 2.99% to 3.08% (chart via Investing.com; red marks added):

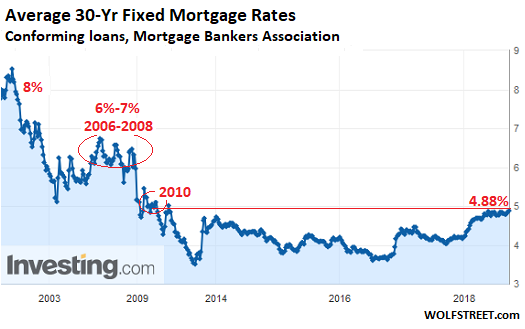

While 5% may sound high for the average 30-year fixed rate mortgage, given the inflated home prices that must be financed at this rate, and while 6% seems impossibly high under current home price conditions, these rates are low when looking back at rates during the Great Recession and before (chart via Investing.com):

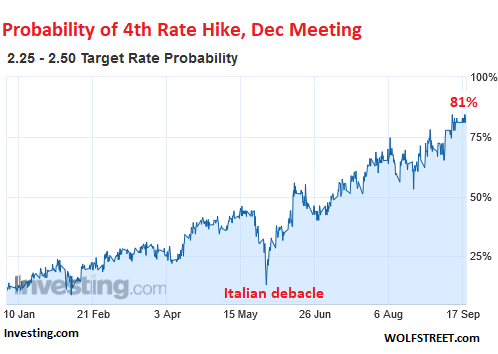

And more rate hikes will continue to drive short-term yields higher, even as long-term yields for now are having trouble keeping up. And these higher rates are getting baked in. Since the end of August, the market has been seeing a 100% chance that the Fed, at its September 25-26 meeting, will raise its target for the federal funds rate by a quarter point to a range between 2.0% and 2.25%, according to CME 30-day fed fund futures prices. It will be the 3rd rate hike in 2018.

And the market now sees an 81% chance that the Fed will announced a 4th rate hike for 2018 after the FOMC meeting in December (chart via Investing.com, red marks added):

The Fed’s go-super-slow approach – everything is “gradual,” as it never ceases to point out – is giving markets plenty of time to prepare and adjust, and gradually start taking for granted what had been considered impossible just two years ago: That in 2019, short-term yields will be heading for 3% or higher – the 3-month yield is already at 2.16% — that the 10-year yield will be going past 4%, and that the average 30-year fixed rate mortgage will be flirting with a 6% rate.

Potential homebuyers next year haven’t quite done the math yet what those higher rates, applied to home prices that have been inflated by 10 years of interest rate repression, will do to their willingness and ability to buy anything at those prices, but they’ll get around to it.

As for holding my breath that an inverted yield curve – a phenomenon when the 2-year yield is higher than the 10-year yield – will ominously appear and make the Fed stop in its tracks? Well, this rate-hike cycle is so slow, even if it is speeding up a tiny bit, that long-term yields may have enough time to go through their surge-and-backtracking cycles without being overtaken by slowly but consistently rising short-term yields.

There has never been a rate-hike cycle this slow and this drawn-out: We’re now almost three years into it, and rates have come up, but it hasn’t produced the results the Fed is trying to achieve: A tightening of financial conditions, an end to yield-chasing in the credit markets and more prudence, and finally an uptick in the unemployment rate above 4%. And the Fed will keep going until it thinks it has this under control.

Investors are buying anything to get higher yields. Today’s megadeal, the ninth-largest ever, is one of the riskiest, and reminiscent of the deals in 2006 and 2007. And they’re still blowing off the Fed. Read… Just How Wildly Exuberant is the Junk-Credit Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It shows in stagnating home sales despite falling prices where I live. Boise, incidentally, is the place to be for flippers.

https://www.idahostatesman.com/latest-news/article215832555.html

My veteran flipper friend says things are not lucrative any more.

Boise area prices have gotten into nose bleed territory. I have been looking to retire there and have been monitoring the market for more than 5 years. The prices are so high now, I am looking at alternatives.

Wolf,

Is this the way of saying that we’re slowly raising the temperature in the pot so that the guys in the mix don’t realize they are getting boiled alive until it’s far too late? I wonder how bad the withdrawal symptoms will be when people finally realize that the mortgage rate will never be as low as it was three years ago again for the rest of their lives.

MCH,

I think that’s a pretty good analogy :-]

“Well, this rate-hike cycle is so slow, even if it is speeding up a tiny bit, that long-term yields may have enough time to go through their surge-and-backtracking cycles without being overtaken by slowly but consistently rising short-term yields.”

You think the Folk’s at the fed with all that taxpayer funded computing power and all those Taxpayer funded annalist didnt perhaps game this one out?

“There has never been a rate-hike cycle this slow and this drawn-out: We’re now almost three years into it, and rates have come up, but it hasn’t produced the results the Fed is trying to achieve: A tightening of financial conditions, ”

Perhaps on wall street but many on main street are starting to run out of available credit.

I will take non noticeable creeping change over noticeable change movement every time particularly if its personal cash flow negative.

Outside America, the fed’s actions are producing some VERY Noticeable change.

In this Global financial system America is defiantly close to the center, the edges will be burned, before America is even heated.

Agree. We are not going to see mortgages below 4% again for at least 30-40 years. Depending on how old you are, this could easily be “the rest of your life”.

I am old enough to remember Regulation Q, when the Feds had price controls on bank deposits and loans: 8% for a mortgage, 5% on a savings account, and 0% on checking. It was illegal for a bank have any other interest rates.

Ah, the good old days?

The next time mortgages get below 5% is a long way from here, and will probably involve a major financial crisis along the way.

I wonder how bad it will be when homeowners realize that 2017/2018 was the high water mark for the asset class, and prices will fall for the foreseeable future due to ever tighter financial conditions. Asset prices and interest rates are negatively correlated when interest rates decline as well as increase. Higher interest rates —-> lower asset prices.

The 30 year mortgage rate is 4.88% now, it will be closer to 5.5-5.75% by next year’s home shopping season if the Fed continues on this path. Look out below!

Year from now when Ben and Janet gets vilified like Alan was ten years ago, people will wonder what would have happened if the Fed had only raised rates sooner. I think realistically, the Feds are always looking at the last battle. Bernake was a student of the Depression and my guess was that he was so focused on that lesson and the mistakes then, he didn’t look at the situation in 2010 and think it was different from before. He had successfully saved the economy, and then decided to inflate the asset bubble.

Now the question is if Jerome is smart enough to slow bleed the bubble so that asset prices won’t deflate to another crisis level.

You’re pretty close. The Fed/Powell wants to get the federal funds rate closer to the inflation rate without imploding asset values.

I believe you are making a false assumption. One that the vast majority of market commentators make. That is, if Bernanke had a different view, he would have raised rates, and we would not have a money printing FED.

Why is this incorrect?

Answer these:

Who chose Bernanke and why? Why wasn’t he removed? Why hasn’t a hard money person like James Grant been made head of the FED?

I’m sure the powers that be are quite amused that all of us FED haters are railing at Bernanke for not doing the right thing. He was just their puppet. He simply would not have been in that seat if he was a hard money / interest rate raising kind of guy.

Was Bernanke elected? Did he throw money around to get himself elected? Was he able to pull strings to get elected?

No.

He’ was simply a college professor.

Essentially, a smart monkey / puppet put in charge of driving the bus – as he was expect to. ie. just another useful (High IQ) idiot.

Its the system that is the problem. Apparently there is ZERO accountability that the dollars that are in our pockets are printed away. In this great democracy, how do we VOTE / ACT to have this stop? It seems to be to have been put outside the publics power, barring its resorting to pitchforks and torches.

“if the Fed continues on this path”

The Fed will not raise rates much further before they reverse course. It’s too late, they held rates too low for too long and now enormous mountains of money have been lent out at ultra low rates and the Fed needs to keep rates low forever, there is simply no way to service the debts the Fed encouraged without blowing everything up. How will Americans service their $22 trillion (and growing fast) government debt if aggregate treasury yields go back to 6% – they can’t.

The Fed can never normalize rates, they must continue to subsidize government spending, consumer debt and bank balance sheet assets. When the market figures this out a trap door will open under the dollar.

If LT yields start to head to 6% the Fed can always cut the cap on Treasury rolloffs from QT, there’s your bid on Treasurys. Similar story with mortgage backeds. The balance sheet is so large the Fed can basically set housing prices and US Government borrowing costs at whatever level earns a consensus on the FOMC.

Plenty of ammo. Yeah, QE3 and Housing Bubble 2 were a pointless gift to the idle wealthy and a generational swindle, but the Fed has thought of the obvious consequences of slowing the gravy train. QT needed to happen and Powell’s Fed ought to be applauded for staying the course.

The same people said the Fed was going to NIRP and ZIRP, but, look, rate hikes every few quarters

The US cant service its debt at current rates (runs a deficit).

Agreed it has no hope at 6% (bigger deficit).

it is bankrupt. it can never repay in purchasing power even if it can in dollars (not the same thing).

“The Fed will not raise rates much further before they reverse course.”

Right. They are just storing up ammo for the next recession.

“The Fed can never normalize rates, they must continue to subsidize government spending, consumer debt and bank balance sheet assets. When the market figures this out a trap door will open under the dollar.”

Like they haven’t already, but you have? It’s a confidence game – as long as everyone “believes” the charade will continue.

Van your comment pretty much sums it up. The stock market isn’t unseeingly heading for a wall to hit it once rates reach such-and-such. The Fed’s talk about continued raising is consciously shrugged off because the market expects the Fed to buckle and reverse at the next episode serious trouble. The central banks are in too deep and the markets know it.

I am pretty sure you have said rates are going to stop climbing over the last 3 rate hikes. Wake up, the hikes will continue to go up until the everything bubble pops. The tax cuts have given the corporations enough breathing room to keep going ahead and pumping up the markets. Even in Canada the Bank of Canada has scoffed at the yield curve claiming this time is different. The people at the helm of these financial markets will not stop until the collapse, they never stopped in the past until after the b.s. hit the fan.

They always do the same thing, drive the family vehicle off a cliff. Pull out a parachute for themselves and then act shocked that the car blew up at the base of the cliff with all the children in the back seat.

It is an endless cycle. Let the sheeple get too far in debt with low rates and then raise the rates to bankrupt them and repossess their assets. A few years later you sell them to them again and they start all over. What is truly amazing is they never learn. The FED works for the banks, and the banks own the sheeple. The cycles are how they sheer them.

Like your analogy, but I’m not sure I buy the premise that mortgage rates will never be as low as they were three years ago. Looks like the Fed wants to push the envelope until they break something, and break something they will. I’m still in the camp with Dr. Hunt in that the low in yields hasn’t yet been seen in the current market cycle. It a word…it’s the debt!

The emperor has no clothes, and little (if any) credibility.

You’re probably right since I used the word life time… because it would assume that there is no major financial crisis that forces the Feds to go through the interest rate reduction and QE cycles again. Perhaps trips to QE land and NIRP will become the norm on decade long cycles. May we all live in interesting times.

“the mortgage rate will never be as low as it was three years ago again for the rest of their lives.”

It is probably a little early to say this.

“mortgage rate will never be as low as it was three years ago again for the rest of their lives”

Who fucking cares dude? Prices are so out of wack that the interest rate is meaningless……it could be zero and i’m still priced out.

This may be part of the problem. If there are buyers willing to pay cash (no mortgage), does it really matter what interest rates are? The only people that are priced out are the ones that depend on mortgages.

Welcome to the new America my friend. We are descending into a third world hell hole. College means nothing anymore. Owning a home is so far off for most young people. Our government socializes losses, illegal immigration, corporate and Wallstreet fraud, bloated military industrial corruption and contracts, etc.

Never say never.

Yes, 10’s are up–but so are 2’s, and JUST AS MUCH.

The real key is that the corporate yield curve is already inverted–including the CLO markets which are another GFC waiting to happen.

Seeing credit curves in structured finance is hard because of the complexities involved in carving cash rflows, but looking at the AAA’s and the equity retuns as a proxy (like 2-10’s) shows just how bad things are right now in what is a 2 Trillion asset class that is keeping the plates spinning in much of corporate credit globally.

The AAAs are up with LIBOR and more picky Japanese flows now that 2-3 year UST now offer good rates (they are not direct competitors), and this means that the equity returns require fully ramped portfolios of higher yielding loans FAST– in a market awash with down-stack cash– and this is causing the “stretch” that has given total pricing power over to borrowers.

They are taking FULL advantage with zero covenant deals (look at the ridiculous Refinitive that just FLEW off the shelves with the ability–and I am not kidding, I wish I was–to pay dividends even in default) and adjustable rate pricing flexes– LOWER– on refi’s, even as LIBOR explodes.

What this means is that the QUALITY of the CLO arbitrage is awful –and getting worse– and soon the securitization window will just CLOSE, just like it did for SP MBS in 2008.

That will strand Billions in collateral in warehouses with little patience for prices that must then reflect hard money lender pricing when the stupid CLO money stops, and that is the GFC all over again but this time it is the non-banks and MREITs that get wiped out.

The FED wants it this way, but that is another story.

Anyway, there are all kinds of yield curves with all kinds of slopes.

Don’t be too distracted by where the UST borrows.

RD:

Where can one find the data that the corporate yield curve is inverted?

I was just looking at 10 year high quality market corporate bond spot rate versus the 2 year high quality market corporate bond spot rate on FRED’s website…the spread is still positive ~100 basis points.

As I said you have to look hard to see it.

The comparison of points along a curve have almost no value. What matters is where–and how–managers borrow and the actual yields–adjusted for quality in many dimensions beyond simple ratings–that are attained on what they buy with the $.

This is made more difficult by the ABS structure bid that is driving pricing especially in loans–which now dwarf high yield bonds. TRILLIONS.

The AAAs liabilities are LIBOR based and are rising FAST.

The assets they buy with this cheap leverage are mostly junk loans with zero covenants that also float–but they float DOWN (see 2017) when pricing power resides with borrowers because there is so much demand for loans to get CLOs ramped up and flowing return to all the tranches–especially the lowest where the managers get paid.

This curve is what matters to the whole market right now.

It won’t go absolutely flat–it doesn’t need to.

Just like in 2008 (with SP MBS) you just get a point where all in returns to the equity are so low that no manager can stomach the risk (say 5%) given the explosive downside and 99 out of 100 bad outcomes a given and then the securitization exit door slams shut and all the loans sitting around waiting to included are liquidated.

as justme indicated below, the banks will simply take them (they provide the warehouse) at, say 80 cents on face and hit the non-bank mangers (Blackstone, Apollo, STWD, LADR hedge funds etc etc) with 20 cent losses that they either survive or do not.

The FED doesn’t care.

The banks are actually fine this time around–they get all the candy at cheap (actually sane) prices and the non-banks that the FED hates because they can’t regulate all go bye-bye.

That is the plan, anyway.

get your popcorn…

>>. ..and that is the GFC all over again but this time it is the non-banks and MREITs that get wiped out.

>> The FED wants it this way, but that is another story.

Exactly. The FRB and the banks WANT a crash now, and after the crash, banks will buy up everything and be masters of Wall St AND Main St again. That is the mission.

Moral Hazard

“Nothing can be truer in theory than the economical principle that banking is a trade and only a trade, and nothing can be more surely established by a larger experience than that a Government which interferes with any trade injures that trade. The best thing undeniably that a Government can do with the Money Market is to let it take care of itself.”

Walter Bagehot

“Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate…It will purge the rottenness out of the system. High costs of living and high living will come down. People will work harder, live a more moral life. Values will be adjusted, and enterprising people will pick up the wrecks from less competent people.”

Andrew William Mellon

The central bankers should read this, understand what it implies and act accordingly. We will all be better off.

Instead they see themselves as saviors of the world. What a pity!

Yes, well, this time IS different. They did not have run away populations, massive immigration imbalances, out of control monopolies, physiological retraining of the masses, lopsided trade, “just-in-time markets”, the internet, and O’don’t get me started on this list. Those men were in an exceptional position, the public then was not. Mellon had one million dollars in his hand as he stared out the window from his NY building, watching the public in the streets banging on the door to get their money from a closed bank. Think he knew was coming, you bet he did.

Friends in high places send the warning before you ever get them. The rich are liquidating right now. Yet the public continues to long for a roof., the new phone, a bigger TV. Americans are determined to be uninformed as if a career, it is a good way to defend yourself when you get hit with foreclosure….”if I’ only known”.

Looking at the past, when rates begin to go up, there is a dash to buy real estate. Not this time, but why? Because the hucksters who sell it, have priced real estate to the edge of lala land, and then push some more with pie-in-the-sky promises on flipping.

The demand for paper is near thru the roof. Why? There has been so much corporate repatriation of dollars, an extra 100 per month in ordinary consumers pockets since the tax cuts, real estate in he doldrums, etc., that the rates should be going down.

Modern Money Theory? Is that a possible explanation? Some say, yes.

Continuing in Bagehot (those words “in theory” were a tell):

“But a Government can only carry out this principle universally if it observe one condition: it must keep its own money. The Government is necessarily at times possessed of large sums in cash. It is by far the richest corporation in the country; its annual revenue payable in money far surpasses that of any other body or person. And if it begins to deposit this immense income as it accrues at any bank, at once it becomes interested in the welfare of that bank. It cannot pay the interest on its debt if that bank cannot produce the public deposits when that interest becomes due; it cannot pay its salaries, and defray its miscellaneous expenses, if that bank fail at any time. A modern Government is like a very rich man with very great debts which he cannot well pay; its credit is necessary to its prosperity, almost to its existence, and if its banker fail when one of its debts becomes due its difficulty is intense.”

That is, unless the Money Market is Too Big To Fail.

Also, I guess, “modern” doesn’t mean post-Bretton-Woods here.

Could you repost this under the Credit Freeze article so readers have these comments in one place? Thanks.

yes sir, i’ll do it now.

“There has never been a rate-hike cycle this slow and this drawn-out” — Same goes for the so-called economic recovery, a.k.a. Fed-sponsored Asset Price Bubble 3.0

In an uncommon disagreement with Wolf I think buyers are very aware of the likely rise in rates to 6%.

They are certainly responding to the 25% difference between 4% and 5% here in Sonoma County as was remarked in a recent Press Democrat article.

August sales are down 10% YoY and 60% of active listings have been on the market at least two months.

Inventory hasn’t been this high since 2011 and new listings are coming on at a steady pace, from what I heard at today’s broker’s meeting there’s no sign that’s about to slow.

There hasn’t been a surge of new listings this year, just a steady accumulation and a lot of price reductions.

Sellers may have gpt the memo, but they haven’t read it, I saw all 4 homes on today’s broker’s tour and one property ( A beauty) was priced to sell.

I was out all day playing golf, so when I saw on Cramer that the Dow was up 154, I checked my portfolio.

I was down $13K for the day! All the utilities, REITs, preferreds, and telecoms took a big hit, even as the rest of the market continues to rise.

But this is only the beginning. Higher rates will lower the NPV of the earning of all companies, and eventually they will start to turn down.

One thing about the stock market is that things can happen fast. In the housing market, people are not going to try to dump their houses when house prices go down – there’ s not such thing as being ‘out of the housing market’ if you need a place to live. But in the stock market, nothing stops everyone from heading for the exits.

If will be the sophisticated traders first, followed by everyone else. When the bottom is reached, naive retail investors will sell out their positions. It’s almost as good as having them blow a horn at the bottom!

The analysts are starting to murmur already.

https://www.msn.com/en-us/money/savingandinvesting/the-great-bull-market-is-dead-and-heres-whats-next-bank-of-america-merrill-lynch-says/ar-BBNyHY3

I thought the sophisticated traders already hit the exits? To your comment, (and I do not have money in the Market), I also checked the numbers today and was astounded at the rise. Astounded. Everyday, all day long, all I hear is how great the economy is. It is so great people cannot afford homes, rents are astronomical, households require two wage earners, and millenials are questioning having kids….ever. But apparently all is well in Whoville.

regarding: “and while 6% seems impossibly high under current home price conditions,” . Yup. I would like to see 7%, and 7% is a helluva lot less than I had to pay when I bought my first home.

What will 7% bring?

* Hope for savers and a modest return

* More affordably priced homes as the speculation subsides

*Smaller homes with less bling

*Realistic expectations

*Hopefully, higher priced automobile financing charges and smaller simpler more practical buying options.

It will slow this hamster wheel down.

I remember my Dad’s home in rural Minnesota. Two parents and 5 kids in a modest 950 sq ft bungalow. Grandparents (folks) downstairs, two bedrooms up with a bed tucked under the stairs. They were happy. Everyone turned out well and had good lives. Summer evenings the grandparents sat out on the screened porch when the evening cooled down and neighbours went for a stroll before bed. They stopped in to visit and say hello.

Of course, they had already weathered the Great Depression and as a result understood how blissful their simple life really was. It looks like that lesson might be repeated before too long if I had to make a guess.

regards

I live in the Toronto, Canada area and none of the landed immigrants or local immigrants have any kids anymore. The real Canadians are older and all their kids have grown up but they also don’t have kids as no one can afford it anymore.

No one can afford kids anymore because everyone has decided keeping up with the Joneses and defining their life by material and financial wealth matters more. We are all responsible for what is happening in America. We teach our young people in college that a piece of paper matters more than anything. 90% of kids have no business even going to college. But there are no other jobs. Hell, there are barely any jobs for those with degrees. We are brainwashed by government, corporations, our neighbors and friends, to live this massive all consuming lifestyle in America based on sports, shopping, convenience, etc. A bunch of mice on the wheel as someone said. It’s exhausting and we are suffering because of it. Our country is divided, our kids are on drugs, our elderly are warehoused in “facilities” visited by kids that should be taking care of them and should have the time to take care of them.

“understood how blissful their simple life really was.”

Yep!

Luckily for me I have discovered how blissful a simple life is and I intend to stick to it.

I did post something similar on nakedcapitalism once (https://www.nakedcapitalism.com/2018/02/will-take-political-revolution-cure-epidemic-depression.html#comment-2930349).

Re: “But in the stock market, nothing stops everyone from heading for the exits.” –

Everyone might head for the exit, but they can’t actually get out, because for everyone trying to “exit”, there has to be someone “entering”. The stocks in the market ain’t going away, and they always have an owner. So every would-be seller has to find a buyer.

When the rush for the exits happens, only lower prices will encourage people to enter, and discourage people from exiting, to balance the market. (The bag holders will get government to restrict short sales and other Calvinball shenanigans, but that will only make things worse.)

If the markets drop substantially does the Fed continue raising

rates ?

What’s “substantially?” -20% no problem, Fed stays on track. -50% in two months? Probably some serious discussions going on at the Fed. But -50% over five years may not trigger the Fed to do anything differently because it’s “gradual.”

The market isn’t going to drop just 20%.

If the market dropped 20%, it would destroy many trading strategies that have worked over the past 8 years. Faced with gigantic losses, many traders would have to sell their ‘good’ stocks to raise cash to pay their margin debt. This would set the dominoes a-runnin’.

I won’t end until the 401K ‘long-term investors’ dump their index funds at the bottom of the market.

The “market” would never fall so far so fast. Central Banks and Governments would never allow it. That choice was made in 2009. and since. We simply don’t have time for markets to run their course. Heavy intervention and regulation is necessary. US indexes must keep going up for our entire economy to work.

Dave Ramsey says you should dump your CDs and buy growth and income mutual funds to get the guaranteed 12% annual returns. Look, the guy is rich and has his own radio show. How could he be wrong?

Wolf,

50% in 2 months will cause panic not serious discussions. The asset price rises saved the banks, saved pension funds for the time being, etc. A 50% increase in 2 months would be a financial nuclear bomb. Think about it.

This depends on who is holding the bag. The FED serves the banks, if the banks are not exposed to the market, then the FED does not care how much it falls. If the banks are exposed, as they were to the housing crash, then the FED must act to make sure they do not incur a large loss.

“Potential homebuyers next year haven’t quite done the math yet what those higher rates, applied to home prices that have been inflated by 10 years of interest rate repression, will do to their willingness and ability to buy anything at those prices, but they’ll get around to it.”

They will have no choice but to buy. In my urban metro area a crappy 2 bedroom costs $2500/month. That’s thirty thousand a year out the door. I imagine when even more people want to rent that will send things even higher as availibility is scarce.

People seem to be very creative in coming up with money they don’t have. There seems to be no limit to the amount of credit banks are extending to people. I imagine that banks are approving those 20k limit credit cards with 20% interest rates at fever pitch again.

P.S- what ever happened to the Seattle rental market? Did it crash as predicted?

I’ve got more data on Seattle in terms of rental supply and vacancy rates. So hang tight.

Do you know anyone who “predicted” Seattle’s rental market would “crash?”

Anyone who says, “They will have no choice but to buy,” will soon be taught a lesson by the market about “choice” :-]

One has only to follow the Chinese money in any city worldwide to know the future of the said housing market.

Are you implying that people will take cash out of credit cards for the down payment on a house?

That’s one way to get your application turned down.

Mortgage fraud is still rampant. Not as bad as the early 2000’s but it is still happening, and the liar loans are still being sold off to pension funds.

Please cite evidence for this claim.

Oh right, you have none, thanks.

“They will have no choice but to rent…”

There, fixed it for you.

When choice disappears, it’s not the renting option that is out of reach, it’s the buying option. Always.

Also if the rents surpass the income expect “They will have no choice but to move…”

The crash in the inflated markets will happen when the people migrate to more stable living situations. People don’t look for a pay raise if they can find a decrease in expenses to balance the books. They just want to be net positive.

Nah if rents surpass the median income in any area, the rents come down. There’s no leverage to rent so rents have an equaliser.

It is only buying that has leverage so house prices will go higher as banks get greedy. This is why this the option that gets cut when people have no choice.

And yes the past four to five trading days have been brutal for rates I’ve been quoting rates in the mid-to-high 4s and low-to-mid 5s depending upon the credit score

The rig artists, crooks, criminals, shysters and central bankers yes the ones that manipulate and rig Wall Street are the same ones who rig the 10 year treasury note. I’ll tell you one thing its headed below the 3 percent threshold because the central bankers won’t allow it to go higher… ever yes ever.

The Fed WANTS it to go higher. That’s why it’s raising rates and unloading the securities on its balance sheet.

The past 2 years the Fed has done exactly what so many have claimed would never happen….. Raise rates.

Nirp, ZIRP, painted itself into a corner, etc….. That’s all we heard about and now they’re doing the very thing nobody said was possible. So now when they claim “fed cannot possibly raise more” it feels like the boy who cried wolf.

Hmm, let’s see… Alan and his predecessors built the IED (improvised exploding device) Ben worked out a way to delay it, Janet watched, and now its Jerome’s turn to disarm it.

My guess is that the real estate market will be a lot messier in Canada where 30 year fixed rate mortgages are virtually unavailable and the typical “fixed rate” mortgage has its interest rate reset after 5 years.

My son just refied for a 5 year term at 5%. (Vancouver Island). The quoted 5% was high due to an outstanding LOC he was carrying in order to pay off a failed relationship. He finally did the refy to clear that up. His balance owing is 1.5X his annual salary. Apparently, without the LOC history he would have obtained a lower rate. 5 years is the longest term available at his bank.

It is quite shocking for everyone to see the mortgage rates head to 4.88% in September month while it was below 4% since the past 7 years. It is the highest mortgage rate since April, 2011. Surprisingly, FED keeps going on to hike the mortgage rate up to 6% in the coming months of 2018.

According to me, the mortgage rates will never going to be as low as it was 3 years ago. Also, according to FED reports, it will be closer to 5.5% to 6% by the next year. It is undoubtedly a bad news for the home-owners because the prices will fall due to tighter financial conditions.

But when we look on a different scenario, FED will not raise the mortgage rates as much higher because for that, they have to reverse the course which is quite difficult for them. There will be no way to service the debts if they hike it to the 6%. Even they cannot normalize the mortgage rates and they must continue to subsidize the consumer debt. So it is quite early to say all this. May be their planning would be different. We should wait and let’s see what will happen in the coming future.

just a thought : the feds have enabled the us government to accumulate large deficits via low interest rates. Maybe they feel that rate normalization well deter more reckless fiscal borrowing ?

It seems that the cause of this rise in the 10yr is not the Fed and its minor tinkering with overnight rates but the overseas debt market in dollars being liquidated. When LIBOR goes on a bend it says credit freeze and most agree Europe is ground zero in the crash. The scary thing here is the correlation has no causation.

Look, the dollar LIBOR tracks the equivalent US Treasury yield, only slightly higher.

The 3-month dollar LIBOR is 2.3%. The 3-month Treasury yield is 2.17%. It doesn’t mean credit freeze at all, it means rising short-term rates in the US because the Fed is hiking them.

In a credit freeze, junk-bond yields would skyrocket. But spreads are at 11-year lows and yields remain in la-la land, even in the euro area: the ICE BofAML Euro High Yield Index Effective Yield shows an average euro junk-bond yield of 3.37%!!! This still ludicrously low.

And huge risky junk-debt deals fly off the shelf in dollars and euros. See my article on Refinitiv.

We’re a million miles away from a credit freeze

The housing data on Redfin for the Los Angeles area is very interesting. It appears that higher interest rates are definitely starting to have an impact.

After interest rates, the next leading indicator of a turn in the housing market would be buyer interest, ie, tours, inquiries, etc. Redfin’s demand indicator has absolutely cratered to 100 since the high of 175 in Nov 2017. In other words, buyer interest was a whopping 75% higher last November than it is now for the LA area.

Demand appears to now be filtering into price drops, which are steadily ticking up year-over-year, according to Redfin’s data.

Check out the charts for yourself here: https://www.redfin.com/blog/data-center.

For the price drop chart, filter by State, Region, and Show Values As “Year-Over-Year Change”, then click the Price Drops tab.

Scroll down the page for the Housing Market Demand indicator, then filter by city.

Very interesting!

Via QT the Fed is simply rolling over the mountain of QE Debt to individuals and institutions in the US. And they are buying with hand and fist – to the tune of $1.4T last year (see Wolf’s recent article).

The summer has come and gone in San Diego and home sales at least in our neighborhood were notably more suppressed than 1 year ago. The most sales appeared to be in summer 2016, 2017 was okay, and so far in 2018 barely anything appears to have sold.

No surprise really given interest rates are a full point higher than this time last year. Roughly. And on top of that there is practically zero tax break for having a conforming loan under $450k unless you are single owner with no family or spouse.

The tax break before the law changes was significant for DINKs. For me the child tax credit changes out weigh the old tax law…

Haven’t really seen price drop yet. I guess that wont happen until there is a glut of sales or people feel pressure to sell. Slow sales and a lack of sales is a bad sign in and of itself.

I am in the thick of things in san Diego

I am witnessing multiple price reductions and homes sitting in longer to be sold

The sales volume is gone down and inventory would go up over time then more price reductions would come

Housing is like a titanic which takes time to turn.. not gonna happen in few months

I think current homeowners are doing the math correctly, but they are using 3% annual appreciation because they think home prices only go up. If you get near guaranteed appreciation like the old days, 6% interest is no problem.

So, I need a mortgage because I choose NOT to tie up my hard cash assets in a house. I am actively looking for the lowest cash down mortgage as I dont see wisdom in establishing equity in something I believe has a high probability to go down in value. The only reason I am even considering buying a house is to shut my wife up. Do I buy now or try to catch the falling knife next year? Or just keep renting, stack Ag/Au and wait for a fair all cash purchase? Houses where I am are selling for a ridiculous $130/sqft and up.

“DO I buy now or next year…?”

No, the logical thing would be to ditch the wife?

Powell, keep unwinding the Fed’s balance sheet and raise them interest rates higher, faster. Socialism for the rich has to end, and real free market interest rates and price determination will make the foolish and greedy rich folks poor and the poor man rich. It will be beautiful when you can buy stuff on sale, just like grandma use to say.