But the cost of shipping surges, no holds barred.

The signs that the infamous cyclicality of the transportation industry is changing direction once again are still timid. This industry is a thermometer of the goods-based economy. And it has been hopping! But the first such signs are appearing, even as activity is at record highs, amid complaints of equipment and driver shortages, bottlenecks and delays in the supply chains, and a massive double-digit surge in pricing.

Freight shipment volume across all modes of transportation – truck, rail, air, and barge – rose 6.0% in August, compared to a year earlier, according to the Cass Freight Index. The index covers merchandise for the consumer and industrial economy but does not include shipments of bulk commodities, such as grains or chemicals.

That 6.0% increase is only about half the double-digit year-over-year increases in six of the seven prior months, and the smallest increase since October 2017.

The chart below shows how the index changed compared to the same month a year earlier. It also shows the cyclicality of the business (the above chart shows the seasonality of the business). Clearly, these monstrous year-over-year increases in shipments so far this year cannot keep increasing at the same rate. Exponential increases cannot last. Cyclicality always wins:

Another aspect that surging demand is starting to back off is visible in the DAT Dry Van Barometer, cited in the Cass report. The barometer tracks demand for van trailers compared to available capacity. This type of trailer is an indication of consumer goods moving across the country. The barometer shows the cyclicality in the business, including the “transportation recession” in 2015 and 2016. The horizontal blue line (50) indicates equilibrium between demand for vans and capacity. Values above it indicate demand exceeds capacity. The enormous spike in the demand-capacity imbalance since late last year has now started to back off (click to enlarge):

Demand from the industrial sector shows up in demand for flatbed trailers that haul equipment and supplies for oil-and-gas drilling, construction, manufacturing, etc. As demand surged late last year and capacity tightened, the DAT Flatbed Monthly Barometer, cited by Cass, spiked to historic highs. But there is no endless spike, and the demand-capacity imbalances are now being worked through (click to enlarge):

The Association of American Railroads (AAR) reported that shipments of most commodities by rail were fairly strong in August. US railroads originated 3.8% more carloads in August than a year earlier.

Intermodal traffic – containers and piggybacked trailers – rose 5.1% in August year-over-year. But that increase was down from a 6.9% year-over-year increase in July, and it was below the year-to-date total increase of 6.0%

But in terms of pricing, it’s no holds barred….

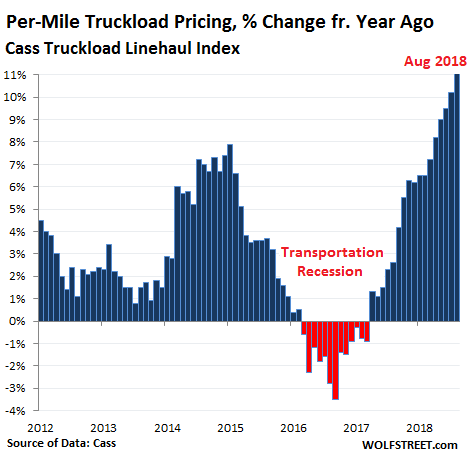

The Cass Truckload Linehaul Index, which tracks per-mile full-truckload pricing but does not include fuel or fuel surcharges and is therefore not impacted by diesel price increases, jumped 11.1% in August, the largest year-over-year increase in the data going back to 2005:

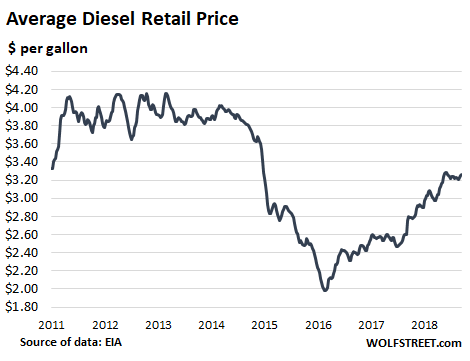

The price of diesel does not impact the Linehaul Index above. But it impacts the broader indices below. According to EIA data, the average price of diesel at the pump, at $3.26, is up 16% from a year ago but remains below the $3.80 to $4.20 range that prevailed between 2011 and 2014:

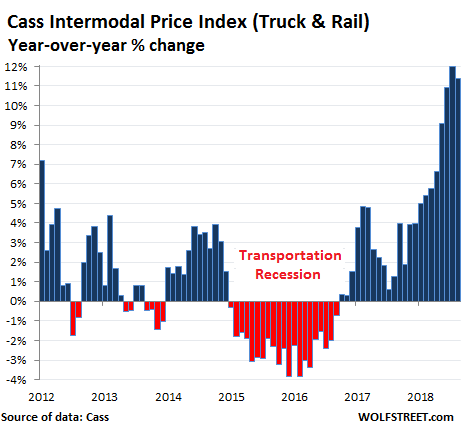

The Cass Intermodal Price Index includes fuel prices, and it jumped 11.4% in August compared to a year ago, the 23rd month in a row of year-over-year increases:

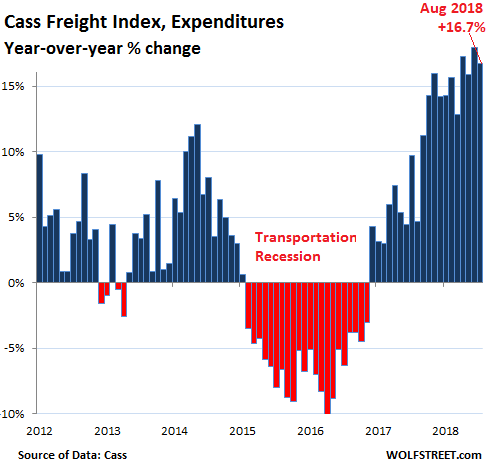

The total amount companies spent on shipping their merchandise via all modes of transportation surged 16.7% in August compared to August last year, according to the Cass Freight Expenditures index. This increase is a result of higher shipment volumes at much higher prices:

Shippers are going to be out of luck for a while. Capacity is still tight despite the first indications that some of the constraints – whether demand or additional capacity – are loosening up. Freight rates and expenditures for shippers will continue to rise as long as the industry operates at capacity. But when slack appears in the system, truckers will start to lose some of their pricing power, a process that shippers are eagerly looking forward to.

The trucking industry is expediting this process with a historic effort to increase their fleets and add capacity. So orders for Class 8 trucks in August jumped 153% from a year ago to a new record, after blistering increases all year. Read… What the US Heavy-Truck Market is Saying

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

a lot more trucks on the road than a couple of years ago. the paucity then was kinda spooky.

methinks i’m gonna lighten my railroad load. but i like seeing my trains go by. what to do, what to do.

What do these kinds of increases in shipping rates equate to in terms of increases in inflation or, since “inflation” seems to be dependent on interpretation and political or central bank agendas these days, at least increases in consumer prices?

When shippers are starting to pass on the increases in shipping costs to consumers via higher prices, they will show up in CPI. But it’s a slow process for transportation costs to make it through to the retail prices. There are many other factors at work, such as competition.

Shippers do run quite lean, earning profits from volume. However, this trend can’t go into perpetuity. Perhaps this capacity will come crashing down, hopefully not in the near future.

Tax cut rat being digested and then its gone!

http://www.polb.com/economics/stats/latest_teus.asp

TEUs for LA-Long Beach Port

The thing about living in these insufferable economic bubbles is that all around you you see frantic, frenzied “economic activity” with less and less fundamental justification other than CHEAP MONEY.

Truly, they go faster and faster in circles, but the circles are getting smaller and smaller…

Race to the next stop sign. It’s the American way.

Isolation eventually fails.

The US economy is isolated from the remainder of the world.

World trade has collapsed. Emerging market countries are beginning to drop by the wayside, victims of debt, Fed global tightening and rising interest rates.

The EU cargo growth year-over-year is now negative.

The Suez Canal net passage tonnage has sharply declined.

Asian ports are experiencing continuing declines in container shipments.

Global air freight growth has turned negative. Even the grand old indicator BDI has turned down!

The only thing holding up the US transport sector, is this bulge in the amount of freight working its way through to a destination. Once this wave of shipments is complete, watch for the cows to come home!

http://www.gainspainscapital.com/2018/09/11/9466/

Trannies confirm the new high. I just read how Amazon abuses its drivers, http://www.businessinsider.fr/us/amazon-delivery-drivers-reveal-claims-of-disturbing-work-conditions-2018-8 some of this is hyperbole. I recall a UPS driver putting it succinctly about the gripes about work conditions -some years back they went on strike and won, but the drivers then had to deliver anything up to 150 pounds, without help, he said “if you don’t like it Del Taco is hiring..”

We run hotshot across the US delivering freight out cars back, I can personally attest to the slowdown in our business. It’s still good mind you but the pressure is off, just a few months ago NYC outside of Manhattan was paying $3.50/mile plus $200 toward tolls. I am in the process of buying 2 rebuilt cores as backups as used 1-tons are not depreciating like they used to. I think business will still be good just not breakneck balls to wall like it has been.

maybe this up cycle is a result of a large inventory build before new tariffs are instituted . Dollar high , Yuan devalued ,

front run before any more price increases occur . might show up in 3rd quarter GDP.

Its always something! Last time it was inflation from Olympic build out of China 2006 and this time its just the opposite? 25% on 265 billion in goods a dozen years later? I hear three , can i get four ? Four rate hikes….cadaver says yeah!

CNBC is usually a relentless booster of stocks with their Trading Nation bandwagon hype.

But in the last few days and today (15) the site is suddenly full of doom warnings. Headline at the moment: We never fixed the problem in 2008.

A common thread in these warnings: we’re ok for now. Even JP Morgan’s head quant (Ph.D in Physics) who thinks we’re in for the worst crash in 50 years, figures: “we’re probably ok till late 2019′

(So let’s see. If I told you this bus will crash in the next 50 minutes, but I’m not sure when, would you ride it for another minute and a half ?)

This was a thread in 1928. A New Yorker bit was titled: Overstaying a bull market’

This lays the ground work for the stampede: thinking it’s coming but not now, then realizing that maybe this is it. In a play or drama this is called ‘the rising action’.

– A few sources on the internet say that US companies are afraid of the consequences of the (upcoming) trade war(s) and fear the impact on prices (i.e. going higher). In anticipation of (expected) higher prices, companies have ordered (much) more than they need for their production in the next few months. And all that stuff needs to be transported from and to factories. Hence the rising transportation index.

– At some point companies will be running out of storage space to store the increased inventory. And then demand of those companies will shrink, pushing economic activity back down and (much) lower.

– More inventory also means higher costs. At some point these increased storage costs will come to bite those companies in the rear end. Are companies already feeling the financial pinch of higher (inventory) costs ?

– This dynamic is similar to what happened in the 1919 & 1920 and in the late 1960s and early 1970s. I never thought I would see a repeat of what happened in those earlier periods. And in both previous periods a (deep) recession followed. Doesn’t bode too well for the (near) future …………….