Cash extraction at the peak of a long housing bubble, via multiple mortgages on the same property: Does that ring a bell?

By Daniel Wong, Better Dwelling:

Canadian real estate price spiked in 2017, and a lot of homeowners have already spent that equity. Canada Housing and Mortgage Corporation (CMHC) numbers show a huge number of people are taking out multiple mortgages on their homes. The trend now represents over 1 in 10 mortgages issued in the country, and nearly half are in just 3 cities.

Multiple Mortgages Holders

The term “multiple mortgage holder” can have a lot of meanings, so let’s just run over the CMHC definition. These are mortgage holders that took out a new mortgage on a home with at least one existing mortgage. These numbers from the CMHC only include loans that result in a balance increase of more than 10%. The total number is likely higher, but even excluding smaller loans we get some giant numbers.

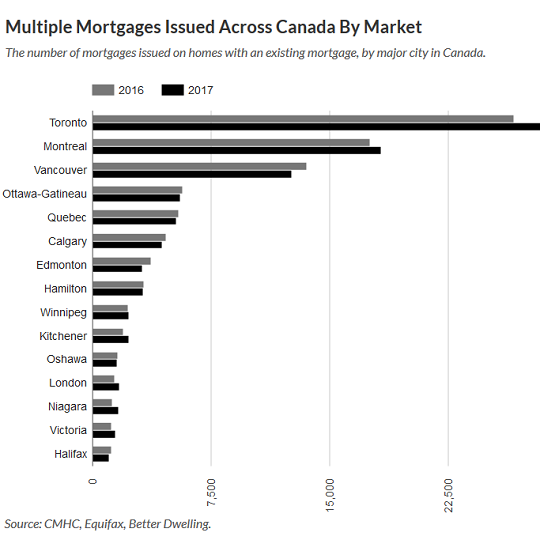

The Canadian Real Estate ATM

Canadians taking out multiple mortgages on the same house made a huge jump. There were 145,013 new loans issued on already mortgaged homes in 2017, a 4.16% increase from the year before. That represents 15.12% of originations that year, or over 1 in 10 mortgages across the country. That’s a lot of people in a rush to use their home equity all of a sudden.

Toronto Real Estate

Toronto real estate is the number one spot in Canada for multiple mortgages on a single property. There were 28,364 new loans issued on already mortgaged properties in 2017, up 6.4% from the year before. This represents 17.4% of all originations in the city, a 2.6% increase of market share from the year before that. The volume and market share of multiple mortgages is on the rise in Toronto.

Vancouver Real Estate

Vancouver is home to the third largest market of multiple mortgages. There were 12,597 new loans issued on already mortgaged properties in 2017, down 7% from the year before. This represents 18.1% of mortgages in the city, a 2.2% increase in market share from the year before. The volume of multiple mortgages is on the decline, but the share of total originations is on the rise.

Montreal Real Estate

Montreal is home to the second most multiple-mortgage holders in the country. There were 18,270 new loans issued on already mortgaged properties in 2017, up 4% from the year before. This represents 17.4% of mortgages in the city, a 2% increase in market share from the year before. The volume and market share of multiple mortgages is on the rise in Montreal.

Debt by itself isn’t a problem, but the current setup makes it an interesting one. A significant number of these loans are in markets that recent price acceleration. In the event of a correction, these borrowers will be with less cash than they expected. This becomes more complicated with rising rates, increasing the cost of servicing these (variable-rate) loans. By Daniel Wong, Better Dwelling

A massive survey of recent homebuyers in Canada reveals all. Read… Foreign Buyers Made Me Do It: Canada Reflects Back on its Housing Bubble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

You take out a second when the bank wants more money after the first mortgage goes underwater?

That’s part of it, you also take out a second, third or fourth for:

Buying another property to take advantage of rents.

Buy another property to flip like those renovation shows, because it is guaranteed profit. /sarc but still happens

Buy a new car or toy or camper to keep up with the neighbours.

Pay for the trips every year so the neighbours don’t think you are broke.

For the most part, these over extended decisions have to do with gambling on the bubble speculation. Being apart of the rat race and keeping up with friends and neighbours is likely a part of it. There are a few outside the norm that might need to cover sudden medical costs also. But I wouldn’t be surprised if it was mainly for “income property” purchases(look at the top 3 locations). A downturn in housing will crush these investors.

I reckoned that the 25K average personal debt would cover the cost of keeping up with the Joneses, does it not?

The nice car in the driveway usually costs more than 25k. A new diesel truck for 2019 just arrived at the local dealer, priced at $94,000 before taxes. Might have to check my coat pocket for that kinda money.

Lol that’s just credit cards.

These free wheeling loan granting financial organisations, are also answering the call for more “product” by the derivative sector.

These freshly minted HELOC’s find their way into CLO’s quickly and sold on to pension funds etc. in their desperate search for yield.

Which in turn generate their opposite in the derivative sphere, the CDS and ETF’s of an equity options form.

Do you hear echos from 2006-07 just before Lehman?

That’s alright I bought a 17 acre parcel in Sag Harbor village at a bankruptcy auction in 1992 and the owner a lawyer from Manhattan had four loans on the property as well as a IRS lien and lots of back property taxes and interest Needless to say a lot of people lost a lot of money

The IRS seldom loses.

That’s correct Harold the IRS got paid first The second third and forth lienholders didn’t fare so well though

“At $67 billion, current HELOC dollar volume pales in comparison to its 2006 heyday of $140 billion. But some, including Freddie Mac, say they expect it to continue its steady climb thanks to rising interest rates and home prices. In its 2018 forecast report, Freddie Mac said borrowers tapping their home equity will be a major trend driving the market forward this year.”

Considering the American appetite for debt is insatiable, I think it’s safe to assume that we will MEW to our eyeballs again. What could go wrong?

Canada is different man.

RofL.

If the HELOC is backed by a real estate, what happens when the HELOC defaults?

Bank calls in the line and if they can’t pay negotiate then foreclose.

The Median net worth of Canadian households is over three times larger than comparable American households. That is to say, the average Canadian is quite a bit wealthier than the Average American. Canadian middle-class wealth has risen over time….while the American middle class has been decimated. Top 20% of Canadian households are worth over a million, double the amount compared to the US.

Of course, there are many more wealthy Americans in the upper 1% region as wealth inequality in the US has surpassed historic highs.

You need to compare things in relative terms.

US: median home price/median household income = 3.5x

Canada: median home price/median household income = 7.2x

Now which of these two markets are in a bigger bubble?

Canadians might be wealthier but it seems to me that wealth is on somewhat shaky ground.

Does that net worth include their home values? If so, it’s misleading.

Nicko – “Top 20% of Canadian households are worth over a million.”

Yeah, all on real estate. ROFL

Canada didn’t have the downturn like the States did; they sold their country out to corrupt foreigners instead.

I assume this net worth includes the artificially high price of their primary residence, meaning this is just a number on a piece of paper. And, an American with a net worth of US$760K is the same as a Canadian millionaire. Just numbers manipulated with smoke and mirrors to give the appearance of wealth.

When the RE bubble blows, which it will the net worth of Canadians will drop very quickly Count on that

Here is some shady investment advice.

Take a 500K HELOC on your primary residence and buy a 500K house with cash and rent it out. As opposed to having 2 mortgages on 2 houses.

When the economy crashes, and you lose your job, walk away from your primary residence, kick the renter out, and live mortgage free for the rest of your life.

Anyone see anything wrong with this approach other than it should be criminal?

Your mortgage in Canada has to be renewed every 5 years or less (they have 7 and 10 year mortgages but they are expensive). The bank has the right to refuse your business whenever they feel like, especially at your mortgage renewal.

Right now most investors are not making enough to cover the mortgage and housing costs with the rent they receive. Which is why they are dipping into their HELOC.

As I understand it, mortgages in Canada (except Alberta and Saskatchewan) are full recourse. You can’t walk away from the debt like you can in America. The bank can and will pursue you forever to get the money you have borrowed against the house, even if the value of the property has dropped way below the mortgage amount.

Not quite. In the US, there are only 12 states that are non-recourse. The rest of the states are recourse, just like in Canada. Florida, which had one of the biggest mortgage crises, is full recourse.

I hear this a lot that what happened here cannot happen in Canada, but here are the details on why that’s a myth (this includes a list of the 12 states that are non-recourse):

https://wolfstreet.com/2018/06/20/us-style-housing-bust-mortgage-crisis-in-canada-australia-recourse-non-recourse/

Florida has the Homestead Law, where you can keep your home. I wonder how this jives with foreclosure.

Someone familiar with Florida’s homestead law should respond to this. This has come up here before.

But I’ll give it a shot: The homestead law does NOT protect you from foreclosure if you don’t make the mortgage payments. But in a bankruptcy, other creditors cannot take your home. In other words, I can buy a home in Florida, pay cash for it, then default on my other debts, but the money I put into the Florida home is shielded. That’s my understanding.

That’s why many wealthy highly leveraged people have a big estate that is free and clear in Florida. It’s one of the ways to protect your capital.

I really love that. That’s a way to get em. But I can’t do that because even my first home is grossly unobtainable. That’s something I would do though.

To know when things are out of whack, it is helpful to compare to less bubbly times, but data is only shown for 2016/2017. I’m not sure how to parse this as the YOY increases are marginal.

->Being apart of the rat race and keeping up with friends and neighbours is likely a part of it.

So people are willing to go into debt, risking their financial security, to spend money they don’t have, to buy things they don’t need, to impress people they don’t like. Guess that blows the ‘rational economic animal’ theory right out of the water, doesn’t it?

There’s no need to imagine how this ends for a lot of the players. The last relative who came to me to bail him out now direct deposits his paycheck into an account I control, and he gets an allowance until he resurfaces again out of the depths in five or six years. In the meantime his rehabilitation proceeds with the acquisition of useful skills, like Household Budgeting For The SemiIndigent. And he’s happy with that. And you wonder why I’m always Unamused, although Damnannoyed would also work.

Thus is the nature or usury…exploiting those without the smarts to realize the potential problems they may be putting themselves in, or are to reckless to care even if they do realize. Greed is the most powerful of drivers, rationality hasn’t got a cat’s chance in that fight for 80% of the human race.

Hence the reason usury used to be a crime…now it’s them main driver of economic growth (temporarily of course, as it’s illusory growth based on illusory prosperity) throughout much of the developed world, and there appears to be no moral outcry when TV adverts offer money to the struggling at 1000+% APR. The fact that activity such as this is even legal is astonishing – or at least, it should be. Now appears to be normalized.

That says a great deal about the decline in morals and values that has been going on since greed was unleashed in the 80s.

Nature OF usury I meant to say

Usury is a euphemism for risk, used by people who want to buy votes.

it scares me tbh. i cant wrap my head around the idea of using money i dont have t\just to impress/keep up with the neighbours, i really think that logic and economy should be taught in every school and kindergarden.

RE: Does that ring a bell?

Well, they say that no one “rings a bell at the top”, but maybe HELOCs count in this case. :)

I’m guessing the same behavior currently in U.S., but I don’t have the data to show this.

“It’s déjà vu all over again.” – Yogi Berra

Haven’t we seen this movie before? Say, around 2007?

But I’m sure the ending will be different this time.

Canadian here:

These articles slay me, especially the part about keeping up with the Joneses using borrowed money. In my circle of friends and family, keeping up with the Joneses means you have your house paid for and owe nothing on toys or travel.

There is also lender malfeasance going on behind the scenes, and not just stupid borrowers.

My 34 year old son just re-upped his mortgage after paying for a breakup and deciding to keep his home. The value of his home is $550,000. He earns just over $200,000 per year. His new mortage is below $300,000 but also also includes funds for a new drilled well and water purification system, all which add value to existing property. The bank kept pushing he borrow more, to the limit of what he is eligible for. Instead, his outstanding mortgage is 1.5X his yearly earnings and he can pay off lump sums in order to pay it totally down, asap.

My 39 year old daughter was going to re-mortgage in order to renovate, as opposed to move into a larger home with associated costs. They crunched the numbers and compared them to their lifestyle and retirement planning, and instead decided to make do with what they have and renovate using cash; staying within the house existing footprint…..no permits or financing required and taxes will stay the same. But, the value of the property will be increased with the improvements.

This Dad kept his mouth shut and offered no unsolicted advice. It was hard, and my bit tongue is still sore. But I feel they have matured and will be able to face any downturn that may arise.

I am astounded and embarrassed at how so many Canadians have grabbed on to the debt and consumption wagon of our times. This is not the Canada I know, and I am afraid there will be some very tough lessons to learn as this unfolds. We’ve had it too good here for too long, and our smug attitude has produced many many poor decisions by people who should know better.

regards

Rest assured that it’s absolutely the same across the vast majority of the developed world, because everywhere is subject to the same predatory behavior of the deregulated financier, complicit central bankers and a political class who very much have their eyes on highly-paid, cushy jobs in the financial sector following the end of their political careers…

The financial coup d’etat we have undergone (if I listen close I can hear Marx spinning away in Highgate) poses far more danger to stable, safe, prosperous society than any hyped-up Muslim terrorist threat or the nasty Russian boogieman.

..which is precisely the reason so much time and money is spent trying to make us all scared of the latter, of course – the financiers can carry on with the plunder whilst we all fixate on Mohammed or Vlad.

Canada has changed just like the rest of the world. Some people have made out very well (at least on paper) taking on a lot of housing debt. How it all ends for each individual depends on when you got in, when you get out and if you can weather the ups and downs in between.

Also, what you value will have a lot to do with the decisions you make. Do you want a big house, new car(s), trips and the latest gadgets?

Do you sleep well knowing that you owe a lot of money and you cant afford to lose your job.

Do you sleep much better knowing that you are living below your means and you have some buffer and can come and go as you please?

All of us are just passing through but we can decide how we want to live.

It’s very annoying going into banks these days. They no longer offer financial advice, they just upsell more debt. Do you want another credit card? Would you like more credit on your existing card? If you ask for a loan of a certain amount they counter with a higher number and a higher interest rate to go with it, even if you can’t afford to pay your current balance off on existing debt. At least your son didn’t bite that hook, I know a few 20 somethings that have taken that bait because they don’t know better.

For sure….another example. I got rid of a mastercard that rewarded points in exchange for an in house credit union card…that pays % cash back. This card is brand new to our credit union. We pay the balance every month and it can be handy for online etc. We usually use it for just gas and like to have it for an emergency travel fund if a relative gets sick and we have to quickly travel. On a whim I phoned them up to see what the limit was, as I could not find the information in the package. It was $25,000. I had to ask, and then verify the request, to have the limit lowered to $10,000.

I can only guess they want the big limits to hook users on impulse purchases.

You don’t escape if you avoid visiting a local branch; it’s coming through mail or phone, too. Would I want a $20,000 line of credit at just 6%? They don’t even bother to do they home work. To my knowledge, the once stodgy, old RBC is the worst offender.

Huh, I just accepted one of these ($20,000 LOC from Scotiabank) — I checked to make sure that it has no annual fees, and no cost unless I use it. Why not? If for some reason I suddenly need $20,000, then it’s there. In the meantime, I can carry on saving money each month.

Hi Paulo, great article, appreciate the examples of your family also. It also highlights that in Canada just as any other country there are sensible people who don’t take on too much debt. Regards Steve.

They just updated crane count in major north American cities…… 97 in Toronto, second place is Seattle at 65, Chicago at 40….. Home prices rose in Canada an average of 1% last month. Boom times will continue.

Crane counts might rise if projects get delayed for lack of funding or other reasons.

Seeing how these multiple loans on a house is structured must be an interesting read. Who is f’ing who???

Loan counts are interesting and surely indicative of important trends. But wouldnt it better to look at trends in average ltv, and especially compared to trend in change in value?

Canada is very vulnerable to a major housing corection. Lots of houses for sale around me here in Calgary, but they do sell…slowly. Too many condos going up though. Our deficits are rising, but governments continue to raise taxes and ham string business with regulations and minimum wage increases. Inflation is running hot even making it into the official government numbers now. Interest rate increases and increased mortgage costs are coming down the pipe. On top of that officialdom think we can beat Trump in a trade war ( I kid you not).0ur Prime Minister Trudeau ( we elected him, we own him) likes to say “Canadians are polite”. It’s not politeness but smug self-superiority on our part, or pride. So, you all know what “comes before the fall”. Here in Canada the shadows are growing on the Summer of Smugness as we head to Labour day. “Fall is coming” to Canada

“I am astounded and embarrassed at how so many Canadians have grabbed on to the debt and consumption wagon of our times.”

Human nature. You can’t fight it.

It is interesting. The central banks are just like the social media companies. They find a basic human weakness, and they have made exploiting it a science.

A lot of people are going into debt right now because they think they have rising incomes. Lots of millennials would be in that category, but also lots of others that see their stocks and RE rising. Once they see more wealth or income, they attach a multiple to it in their mind, and they go on a spending spree.

If it turns out those multiples are invalid, lots of people will be eating crow.

I would wish that stats like these are first normalized to filter out the absolute size of the housing market in each city. Comparing numbers of multiple mortgages in Toronto with Halifax is meaningless.

Most of these people will take out new loans till the music stops at the market top. Then they will walk with the money and leave the bank/taxpayers holding the bag.

These Canadians are channeling their inner Elon Musk i.e. “Funding secured!!” but in actuality it’s more “Bondage secured!!!”