Even the last doves are coming around to more rate hikes.

“In June, most of the rise in the index for final demand is attributable to a 0.4-percent advance in prices for final demand services,” said the Bureau of Labor Statistics in the release of its Producer Price Index data. The PPI and its numerous sub-indices measure inflation further up in the pipeline before it filters through to consumer prices.

Services account for 65.3% (“relative importance”) of the PPI. Energy prices soared, but they account for only 5.6% of the PPI. In the overall picture, services matter the most.

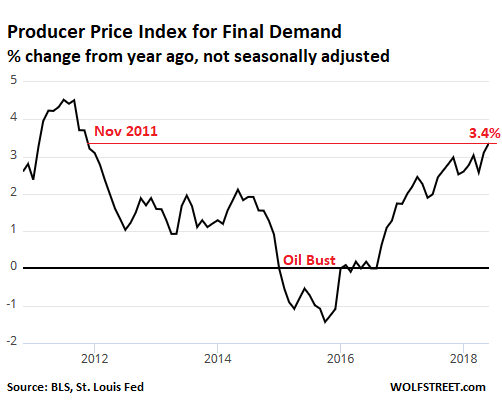

The PPI for “final demand” (as opposed to “intermediate demand,” which is further up the pipeline) jumped 3.4% in June compared to a year ago, the largest year-over-year increase since November 2011. This measure includes goods and services:

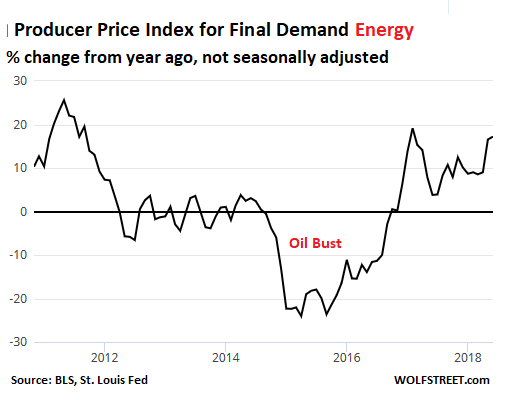

The PPI for final demand energy jumped 17.2% in June compared to a year ago. Note the deep plunge of the index during the Oil Bust. But for consumers, this was a “transitory” relief, to rephrase Yellen:

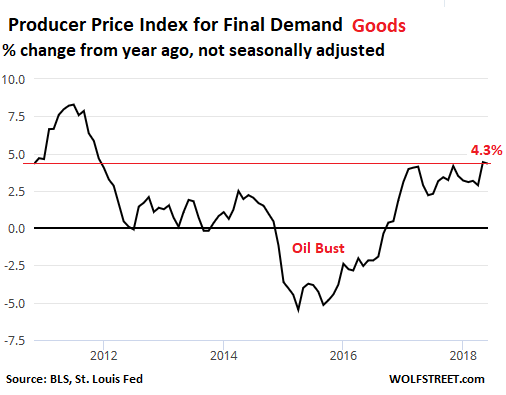

The PPI for final demand goods — includes energy but excludes services and has a relative importance of 33% — rose 4.3% from a year ago. May (+4.4%) and June marked the sharpest increases since December 2011:

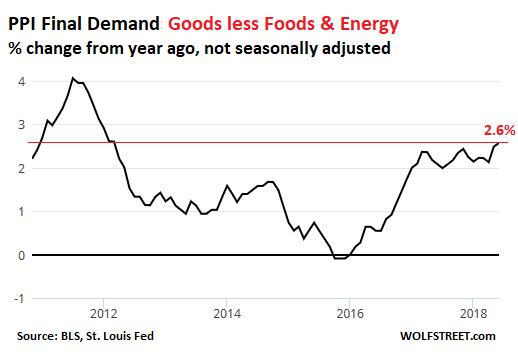

The PPI final demand for goods without food and energy, which has a relative importance of 21.7%, rose 2.6% from a year ago, the largest year-over-year increase since March 2012:

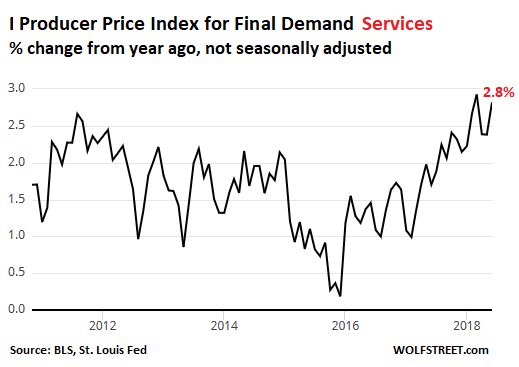

Over the past few months, even the PPI for final demand services has begun to move higher. Due to its relative importance in the index of 65.3%, it matters! It jumped 0.4% from May to June and is now up 2.8% year-over-year. This and the March increase of 2.9% are the largest year-over-year increases in this data series going back to 2011:

This inflation data balling up in the pipeline will work its way into consumer price inflation and add to it. Already, different measures of consumer prices have been on the rise:

- PCE price index without food and energy, the Fed’s favorite: +2.0% in May.

- PCE price index with food and energy: +2.3% in May.

- Consumer Price Index:+2.8% in May; we’re eagerly awaiting the June release.

So inflation is on the move — and folks are wondering if it’s finally the time when investing in silver makes sense again, after years of brutal punishment.

At the Fed, even the last doves are coming around.

Inflation “looks quite good,” Chicago Fed President Charles Evans told the Wall Street Journal. Consumer price inflation whittles down the purchasing power of labor – and for companies, the cost of labor – and only someone focused on whittling down the purchasing power of labor and the cost of labor could call rising inflation “quite good.” But that’s the twisted system we’re in. He was one of the last remaining “doves” on the policy-setting FOMC and voted against the rate hike last December.

Now he has changed his tune. The economy is strong enough to where businesses and consumers “can live with more neutral financial interest rates,” he said.

“And so we’re raising short-term interest rate policy in a gradual fashion, and I think the markets understand this quite well,” he said. “Whether or not you think we should do it three times in 2018 or four times in 2018, it’s really not going to make a big difference.”

That’s quite a change for someone who voted against the rate hike six months ago.

And where is “neutral?” In the eye of the dove, it’s “100 basis points away” – so four more rate hikes to a target range of 2.75% to 3.0%, and that’s just neutral. Anything above that would be tightening. Evans’ idea of “neutral” for the Fed’s target range will likely be reached in the first half next year. For other Fed governors, “neutral” maybe higher. Wherever “neutral” is, the higher it is, the more rate hikes it takes to get there. And when it’s reached, at that point, the discussions about “tightening” commences.

Interest rates are rising, and are expected to rise further, and these rising interest rates have a peculiar effect. Read… Leveraged-Loan Risks Are Piling Up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– Jerome Powell and one Wolf Richter seem to be overturning every (inflationary) stone in search of a justification for a ratehike. I am still betting on “No rate hike” in spite of the all the rising (price) inflation because (up to now) the 3 month T-bill rate didn’t go above 2%. I still have to see the first evidence that interest rates are driven by (price) inflation.

– Rising price inflation in combination with flat wages (to put it friendly) means that the consumer gets squeezed more and more. (= recession).

Rate hikes are coming, QE is dead. Canada is in a debt crisis and after baulking at the spring rate hike, they finally went up to 1.5%, wow so steep.

Down in the USA the economy looks so much better in comparison that I can’t see them stopping until a bank officially collapses from the weight of the debt, that will be 2019 or 2020 so you will have to keep denying the obvious for a few more quarters.

The FED’s front job is price stability(what ever that means) and full employment(what ever that means). Their true job is bank bailout and wage financial wars in other nations.

They need 3% rate in order to have room to move either way. Going below zero does NOT sell EASILY. So they will keep getting to 3 and then they get their power back.

They do NOT know what will happen, so they pull the trigger slowly but surely.

Interesting quote from a piece by David Rosenberg in today’s (13 th) Globe and Mail.

‘Since WWII there have been 13 Fed tightening cycles and 10 resulted in a recession. None of the recessions were forecast.’

The last seems a bit odd…you would think that after recession number 7 the correlation would be noted.

Clearly the ‘this time it’s different’ has been around a while and is still in fashion.

Rosenberg thinks that rate hikes and QE reversal will add up to a de facto 5 per cent rate hike. ( I guess he thinks that when rates were near zero, QE made them in effect negative.)

Here is my take: it was the urge to avoid recessions that got the Fed into this mess. When Greenspan was cutting rates at the mere hint of a downturn ( e.g. Y2K) he was lauded as ‘having tamed the economic cycle’

In reality he was burning the Fed’s dry powder before it was really needed.

Recessions are necessary to correct the over spending and ‘irrational exuberance’ that human ‘animal spirits’ are prone to. They can be brief and shallow but if artificially delayed, people forget they can happen. They double down and get even more overextended.

In the end no mere garden- variety recession is sufficient to create ‘regression to the mean’, a return to normality.

As the inevitable recession arrives, watch Trump try to take control of the Fed. If he succeeds, brace for REAL disaster.

Wolf, thanks for your incredibly insightful pieces!

Is there a relatively method to find a meaningful way to interpret individual inflation?

As you know, inflation is a broad concept. If you are 20, inflation affects you in a way that is vastly different from when you’re 80. Likewise, if you live in Fairfield, CA, inflation could mean something vastly different than if you live in Fairfield [pick your state]. Every family has its own economic reality. How does one go from, let’s say, a 2% increase in CPI, to a personally meaningful figure? I’m not even sure whether CPI is the best aggregate of inflation.

Old dog,

Housing is the single largest cost for most households. So start there:

Do you rent? Is YOUR rent going up up 10% a year in the SAME place (it is in some cities, but it’s declining in others).

Did you buy your home a decade ago, and refinance it at a lower rate without cash-out? Yes? Then your mortgage payments declined, and that part of your household expenses actually shrank. Over 60% of the households in the US are homeowners, so this is important.

So it’s really important to start with your personal housing situation. But if you have moved to a different place, your personal data is no longer comparable in terms of inflation. So it gets complicated very quickly.

If you spend more on clothing because your kids are suddenly more demanding… that’s not inflation.

If your insurance premium jumps because you just turned 50 (oh how I remember that day!), it’s not inflation either.

If your mortgage payments dropped because you refinanced at a lower rate, that’s not deflation… you’re just saving money on interest.

So on a personal level, you know you’re spending more money, and some of it is inflation, and some of it is not inflation but is due to other reasons (bigger apartment, more kids, nicer clothes, 50+ insurance premiums, etc.).

As you can see, these kinds of calculations end up all over the place.

Thanks Wolf. You’re right. It’s very difficult to make an apples to apples comparison.

Worse. A dollar printed in 2018 represents quite a different reality from a dollar printed in 1998, 1978 or 1958. A house sold today is not quite the same house one bought 50 years ago. In some neighborhoods it can be a radically different house so a value-comparison of the same asset would be dubious.

The difficulty in finding a concept representing “constant value” against which to measure price fluctuations makes the effort a fool’s errand.

But I understand that gauges of inflation are needed, no matter how imperfect they are. If it weren’t for them, the economists at the Fed would have to go back to reading a pig’s entrails.

What Will the Fed Do? They will acknowledge that the CPI and it’s related statistical tricks bear no relation to cost of living increases. Inverted yield curve is also not a problem. Way to go FED.

“With this Inflation, What Will the Fed Do?”

Congratulate themselves on successfully fudging the numbers and taking the rest of the summer off.

The outdated and old American value of paying off one’s debts and saving as well has been “butchered alive” by the FED in particular. Only the heavily indebted have been and remain favored by our government.

That is true, to a large degree, and certainly savers have been financially punished by the Fed’s actions of the last decade. But I live my life in a manner that I favor and not by what our government may or may not favor; therefore I live within my means with absolutely no debt.

Old Dog brought up a great point in his comment, and being a person who has a pretty stable routine in terms of expenditures, I simply measure inflation by how much it costs me to live each month. My best guess is about 12% to 15% more from one year ago.

I wish that interest rates would go up to 5% for 30 year notes, 4% for 10 year, and 3% for an 18 year note. If you want to borrow money there should be a price paid, and lenders should be rewarded. Unfortunately we have a $21 trillion national debt that gets in the way, eh?

The FED gets it wrong at times – timing the availability of the punch bowl is never perfect – but the conspiracy that the FED favors borrowers is just wrong. When Volcker hoisted the FED rate to 20% to shut down inflation (the belief at the time was that MONEY SUPPLY was causing inflation), had “savers” known that the top was in, they could have loaded-up on bonds and been riding high for the next umpteen years. At the time, the fear and widespread belief was that inflation could NOT be controlled; many “savers” were unwilling to commit to long-term bonds fearing the inflationary erosion of value into the future.

I remember a college instructor who was teaching a real estate investment class I was taking back during the recession of 81-82, and he was railing about the FED destroying the real estate market with it’s “outrageous” interest rates.

I don’t know about that. Debt is slavery!

I paid off one loan and a decent portion of my mortgage so my fixed expenses are like 10% of my salary. Now I save the money I used to pay on the mortgage.

Knowing that we will be okay if someone gets fired means that I can do a better job because I don’t get pushed around and we have no stress over work or money.

There is no point carrying all that load one carries when saddled with debt, “cheap” or not, it’s a bad way to live.

So lets look at the latest debt slave report https://www.federalreserve.gov/releases/g19/current/, consumers bumped up their credit cards by an 11% annual rate while paying over 1.5% more in interest rates on their balances YoY. How many more billions will they be paying after the interest rate hikes? It is the lower 30% that are trapped. I feel bad for them, buying into the “roaring economy” crap with lower real wages, while they dig themselves deeper into debt.

Lance Manly – Indeed. The credit card co’s favorite trick is to offer something like 3% interest and then if you run up a balance and start paying it down, or trying to, they increase it to 37% or more.

Older folks like me know their tricks but there’s a new crop of suckers every few years. And financial literacy is NOT taught in US schools.

“inflation looks quite good” quote from Fed’s Charles Evans tells you all you need to know about the Fed.

Now that they cling to the narrative that inflation is wonderful, they will sing that tune to the bitter end.

Imagine how much easier Paul Volcker’s job would have been if he just decided to announce: “look everyone, inflation is wonderful, so quit all your bitching”.

It would seem Paul Volcker’s actual courage to act only postponed the inevitable death of the currency long enough for a self serving coward to begin killing it off again.

It’s remarkable that they still refer to their oppressive inflation as if it’s a great accomplishment – what a bunch of crooks and cowards.

“Imagine how much easier Paul Volcker’s job would have been if he just decided to announce: “look everyone, inflation is wonderful, so quit all your bitching”.”

To be fair, there is in fact a little bit of a difference between 15% inflation and 2% inflation.

In the late 60s, inflation averaged 5-6%. In the 70s, it averaged over 7%. In the 80s, it averaged 5%. It averaged 3% in the 90s. In the 2000s, it averaged 2.5%. And from 2010 – today, it’s averaged under 2%.

Even if you believe inflation is double what the Fed says it is, it would still be in the normal range for inflation.

Price of milk, 1995: $2.50/gallon

Price of milk, 2014: $3.60/gallon

Price of milk, 2018: $2.90/gallon

Oh, it’s soooo oppressive, the inflation, the dollar has been destroyed.

People who drag out an individual example like milk — whose price is very volatile — to prove one point or another about inflation make themselves look silly. I get your point, but good grief, milk!

And an inverted yield curve is fine! :o

Inflation is making me wait….and wait and wait.

Oil barely holding $70, the entire commodities complex was red, and prices look like crap.

We are beginning more asset deflation as the Fed desires- the only way to sustain relatively higher interest rates is through absolute contraction of capital.

Yet, everybody pulls the 70s commodity push at the end of inflation as the big sign- yet we have interest rates that are so low they force savers to enter the big casino.

And once again, nobody seems to expect a long dry stock market, and a long dead bond markets. House prices only rise, right?

In short, the entire boomer investment strategy is bust- run out it’s string.

The old play book is wrung out.

And yet everyone still thinks it will be so easy.

The only inflation that will help will be rising wages, and that only will happen with really tight labor markets for legal employment.

And still, everyone thinks it will be easy to live off the investments, when everyone else is going to try the same thing.

What a disaster this is going to be, higher taxes through tariffs, (which does function like a consumption tax until enough onshores).

Lower returns to capital, and a lot of wasted capital coming out in the wash.

All I have to do is contemplate all the folks who think they can live off of their investments in retirement….

Someday this war’s gonna end…

“All I have to do is contemplate all the folks who think they can live off of their investments in retirement….”

Citizen…

That was me! Then I started spending principal….

AllenM, good to see you again!

You’re 100% right, if the older 1/3 of the nation attempted to “retire”, and have that retirement funded by “savings” or “investments”, they would quickly discover that there aren’t enough interest and dividend payments to cover everyone’s needs. Because another 1/3 is kids and students and so all those interest and dividend payments would be coming from the debt payments and surplus production of the middle 1/3, and that would require a lot more surplus than we have.

Or put another way: Roughly speaking, stock market cap = GDP, total debt = 2-3x GDP. Real estate about the same. Total of all investment assets if maybe 5X GDP. Assuming average asset pays out 3-5% after inflation, the total of all investment payouts is 16-25% of GDP. The interest and profits are wealth transfers from debtors and workers to bondholders and owners. But even if investment ownership were evenly distributed, there’s not enough in payouts to support 1/3 of the population to retire without them selling off assets. And we know ownership is far from evenly distributed.

The capital stock and the investment markets aren’t deep enough to allow everyone to retire who wants to, and they simply can’t be, because at the end of the day it’s the workers whose actual production supports the retirees. You can’t have more retirees unless the workers are paying more out in interest, or giving up potential pay to feed higher profits and dividend payouts. (Or paying more in Social Security taxes, same idea, just a different pipeline from the workers to the retirees.)

Your analysis needs to consider foreign investments. There’s lots of workers out there beyond U.S. Borders, particularly in 3rd world. They will be just as productive as US workers shortly.

You’re right that some countries will provide surplus production to support retirement of investors in other countries. But that of course is basically economic colonization…

One can apply the original analysis on a global scale rather than just for the US, and reach essentially the same conclusions. The population is aging in nearly all countries with large economies, and there’s not enough total return on aggregate global assets for all elderly citizens to retire. Distribution being uneven, a lot of asset returns go to non-retirement age people as well.

Also note that the foreign investment issue cuts both ways; there’s a lot of foreign investment in US assets too, and it is steadily increasing, since that’s the obligatory flip side of having a trade deficit.

@Wisdom Seeker — your logic is sound. I can update some of your rough estimates. The stock market is currently at 190% of GDP. Total financial assets (which does *not* include real estate owned, but does include mortgages owned, for example) amount to about 530% of GDP. All real estate is purportedly another 150% of GDP, so just with these assets you have 680% of GDP (though we should probably only include rental real estate so this is an overestimate, maybe 580% is better).

As you point out, there is a limit to how much unearned income can be squeezed from these assets without destroying the economy. In my analysis, we are already there at about 27% of GDP– the highest in 70 years. 27% / 580% = about 5% aggregate return, which is much less than seen historically. Lots of pension plans are likely to have big problems, especially in the public sector where 7.5% return is still an expectation.

All figures except estimate of real estate value % of GDP from the Federal Reserve’s latest Z.1 report.

Thanks Dale! I really like how you use the analysis to pull out an estimate of maximum aggregate returns.

It could be double-counting to include both real estate and mortgages on said real estate, depending on whether the rental income from the real estate was gross, or net of the mortgage interest.

Anyway, that doesn’t change the big picture.

What could change the big picture is how much asset prices fall when the current credit bubble pops. I think the 27% of GDP in unearned income is not sustainable. The longer-term (full-cycle) average is probably substantially lower, don’t you think?

I agree that asset deflation should be taking hold as boomers retire, downsize, and finally pass on. However, the Fed seems to be dead set on flooding the world with liquidity at the first sign of trouble.

The whole process seems designed to crush you at the first misstep.

Continuing QT seems to contradict this notion as explained by Wolf

What’s the rate of inflation if you include the cost of housing, healthcare, and college? The cost of living has gotten so high in parts of the US you have to wonder why people bother to keep breathing.

In the US, health care costs have gone up 50 times faster than wages since 1960, proving that the Medical Industrial Complex has become the fourth most successful extortion racket in US history.

It’s nice that Thailand has government-funded medical care. If 13 boys and their coach got stuck in a cave in the US they would have been better off staying there instead of getting sent to a hospital.

Wow! You really seem to get it, so few people seem to understand or care about what the medical industry has become in this country. You are exactly right they are an extortion racket.

People need to drastically cut back on their use of medical “services” and throw away most of the damn pills. Doctors are getting paid handsomely for acting the part of a doctor, wearing a white lab coat and stethoscope, but they don’t seem to accomplish much and they charge through the nose for their mostly ineffective care and treatment.

Actually, effectively harmful.

Funnily enough, the increases to how much medicare costs exactly tracks inflation over the lifetime of the program according to the official numbers. Some argue that many of the support services such as IT are borne by other parts of the government’s budget, but economies of scale and synergies are exactly why we should want the government running health care.

My point is, private healthcare is only about money and as long as it remains in the hands of private companies, we will continue to pay exorbitant amounts.

As pointed out, those of us who save and have no debt (luckily) are the real losers here. We should spend it all, borrow like crap as money is cheap, and with inflation the size of the debt shrinks and hopefully one day we’ll be able to pay it back easily.

Or we’ll die in debt and the banks can write it off or chase the next generation for it. But I’m ok so no problem there. If interest rates were rising fast it would be an issue, but I can’t see the banks doing that as they have so many people who will default, better for them to get some payments than none, which ill happen if rates rise to quickly. They have dug themselves a hole they now have to figure out how to get out of. Oh yes, forgot, the taxpayer………again!

ShrinkFlation and statistical lies.

I have to add something to the sidebar in the article concerning silver for those that read it. Silver is a commodity that is inelastic in responding to supply and demand since over 2/3 of new metal that enters the market comes as a by-product of other metal ores, gold, zinc, lead, copper, etc. Also, the pure silver producers have multiple mines that produce silver at different price points, so when the price rises greatly they will move operations to a mine that only can be profitful at the high price and yields less silver per ton of ore dropping output. It’s the only commodity that I know that is truely inelastic in production.

The Fed shouldn’t be targeting inflation. They shouldn’t be targeting anything. Legislators should be targeting income distribution through tax policy. A consistent income distribution is what keeps the system in balance. The thing falls apart when a few people at the top take all the money.

All anyone would ever have to do is read Article I and Article II of the Constitution to see that Congress holds all the cards in our system, yet for 75 years they have been surrendering, and the courts have been endorsing their surrender, of their powers to the Executive branch or the Federal Reserve. When America went from being a republic to being an empire the legislature simply could not or would not administer the new system, so they have shed as many responsibilities as they can while occasionally petulantly obstructing things if they don’t like the president. Positive action and guidance are simply beyond their mental ken these days.

The Cold War brought about the concept of the executive office as “Unitary Decider”. There was no time to wait for a committee decision (in say the Cuban Missile Crisis). Now we have a (sigh) Deep State apparatus which makes the decisions, better than any one individual. It brings back the idea of government by committee or checks and balances. In matters of economic policy you can’t switch things like tariffs off and on, these are policies which have slow turn around times. The effects of a lot of the (policies?) being made right now won’t show up until later, probably including the rate hikes.

Rate hikes are also a $-protection measure. Inflation is just an excuse, a good one.

With the 10 and 30 year treasury yields still below 3%, the market does not anticipate a significant rise in inflation at anytime in the near future. Perhaps they are trying to jawbone the long end of the curve higher with fears of inflation, but so far it hasn’t worked that well. “Dr. Copper” is in an 8+ year bear market that has remained in a $1.50 to $4.50/lb channel, and is currently closer to the bottom than the top of that channel. It is possible (and perhaps likely) that we will see a continued drain of liquidity with QT and pressure on asset prices but little change in long term interest rates, reflecting slow growth and low inflation.

It is more than likely that it is because the market, despite rate hikes, is not too far from ATH that emboldens Evans. It is when market drops we will get to know who blinks. That said, the market has been very resilient since Feb. despite trade wars.

It didn’t occur to me when I initially read the article, but I experienced a couple of examples of inflation recently and it was a big shock. We’re all used to the major increases in healthcare, education, housing, but many of the take-out lunch establishments in Boston have recently raised their prices. Many have been significant percentages, exceeding the percentage increase in their wages, which really add up for people. If they average a $1 increase and assuming 250 workdays a year, that means that increased lunch prices would consume over a quarter of the post-tax “raise” for someone making $50K a year (at 2.5% increase). Because this is something that is purchased daily, it hits home in a way that other inflation doesn’t.

That’s why I packed a lunch my entire life. Better food, and the money saved added up to the thousands. When I eat out it is a treat, not fuel to get through the day. I told my son-in-law, who was a student at the time, that his daily stop for a coffee and doughnut on the way to his summer job would be enough for a house down payment by the time he graduated U. He stopped the practice and they bought the house. It will be paid off by age 50 and he will be able to retire at 55 and do whatever; maybe work a second career.

You can still get ahead despite inflation and the manipulations by others.

regards

“So inflation is on the move — and folks are wondering if it’s finally the time when investing in silver makes sense again, after years of brutal punishment.”

Silver is mostly an industrial metal, eg 75/25 Ag/Cu solder. Careful with such investment speculation – if Dr. Copper is going down, industrial use may be declining also.

The rollback of the Healthcare Bill has to have some effect. Before Obamacare health services were considered consumer spending, and they went on the CC. By 2007 HC costs accounted for a lot of REFIs, as consumers tried to consolidate their bills, and the consequences. A lot of people ended up handing their assets to Medicaid and they own nothing, but then you live like a teenager, all your income is discretionary! Now you contemplate supply/demand, benefits of outsourcing, and you can see the big picture. Inflation as an economic indicator worked back in the last century when the economy was vertical and rising costs (or loss of confidence) surged through the system in a loop. Now the loop is bigger but its still a loop and many more links in the chain prone to failure. Being interrelated is good, being interdependent is bad. Monetary inflation is way ahead of extended global economic demand, which implies the opposite, deflation. Why deflation? The world is getting smaller faster than the old economy can grow. Push comes to shove, a couple CPI points means diddly. My father had a USPS savings account in the 30s that paid 2%

“Interest rates are rising”

Hmm… where have I seen that before…

May 15, “Today the US Treasury 10-year yield broke out of its recent range and surged 8 basis points to 3.08% at the close, the highest since July 2011.

The difference (spread) between the two-year yield and the 10-year yield widened from 45 basis point to 50 basis points (0.5 percentage points), as the 10-year yield rose faster today (by 8 basis points) than the two-year yield (3 basis points).”

And yet today, July 12, the 10 year is yielding 2.85 and the 2-10 yield curve is sitting today at 25 basis points.

Short rates are rising, but long rates haven’t budged– in fact, they look like they’ve topped out for the year. Huh, funny how that works… those who believe everything is grand in the economy, and that inflation is really picking up this time (we’re serious guys!), have been saying that crossing the 3% yield in the 10-year meant the death of the multi-decade bull market in bonds. And yet… no.

Market is either not buying inflation or signaling stagnant growth in spite of inflation. Fed is going to hike right into an inverted curve, but don’t worry– the Fed doesn’t believe the yield curve is a relevant indicator any more.

Global growth is slowing, and the US economy is going to roll over. Tax cuts delayed the inevitable, but trade wars will accelerate the deflationary shock that will cause the next global recession.