Rising interest rates have a peculiar effect.

US junk-bond issuance in June plunged 31% from a year ago to just $14.5 billion, the lowest of any June in five years, according to LCD of S&P Global Market Intelligence. During the first half of the year, junk bond issuance dropped 23% from a year ago to $110.6 billion.

Is investor appetite for risky debt drying up? Have investors given up chasing yield? On the contrary! They’re chasing harder than before, but they’re chasing elsewhere in the junk-rated credit spectrum: leveraged loans.

Leveraged loans are another way by which junk-rated companies can raise money. These loans are arranged by banks and sold either as loans or as Collateralized Loan Obligation (CLOs) to other investors, such as pension funds or loan funds. They’re a $1 trillion market and trade like securities. But the SEC, which regulates securities, considers them loans and doesn’t regulate them. No one regulates them.

In the first half, companies issued $274 billion of non-amortizing leveraged loans, and $97 billion in revolving and amortizing leveraged loans, according to LCD, for a total of $371 billion, on par with the record set in the first half last year.

This is well over triple the amount of junk bonds issued in same period ($110 billion).

Many of these loans have floating interest rates, typically pegged to the dollar-Libor. And in an investment environment where the Fed has been trying to push up interest rates, Libor has surged, and floating-rate loans, whose interest payments increase as Libor ratchets higher, are very appealing to investors – despite the additional risks these higher interest payments pose for the companies that are already struggling with negative cash flows. LCD:

The U.S. leveraged loan market, which is accessed by speculative grade debt issuers, has been exceedingly hot over the past two years or so as investors pour money into the asset class in anticipation of rate hikes by the Fed. Such moves usually boost interest in floating rate asset classes.

Given the “sustained investor appetite” for this type of debt, companies have been able to issue these loans with lower spreads over Libor, making it cheaper for companies to borrow – until rates rise further. That’s when this debt gets more expensive for these companies that already have a high debt load, often combined with money-losing operations – the combination that gives them a non-investment grade or “junk” credit rating (my cheat-sheet on credit rating scales).

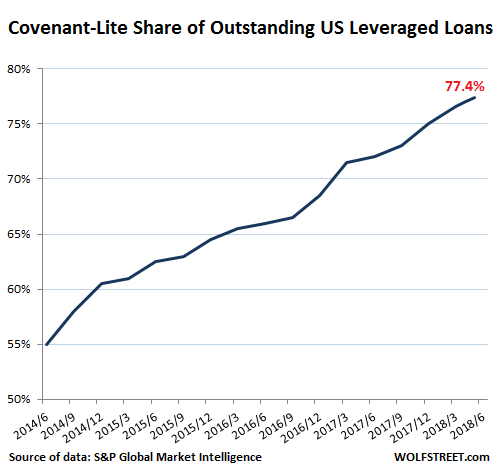

Leveraged loans come with covenants that are supposed to protect investors during the term of the loan and in case of default. With strong covenants and good collateral, leveraged loans tend to be less risky than junk bonds issued by the same company.

Alas, investors have the hots for this debt, and companies are taking advantage of it by weakening covenants, giving investors fewer protections and the company more leeway – such as paying interest with more debt rather than cash if it runs out of cash (payment-in-kind or PIK); normally, not being able to pay interest would constitute a default, but not with these “covenant lite” or “cov-lite” loans. The boom in cov-lite has started years ago and has surged to massive record proportions. When these loans default, investors are exposed to much greater losses.

As of the end of May, a record 77.4% of the $1 trillion in leveraged loans currently outstanding are cov-lite, the 13th month in a row of records, up from 55% in June 2014:

This is one of the many distortions of years of easy-money policies around the globe.

“The rapid growth of cov-lite has raised eyebrows, to say the least, as the current borrower-friendly credit cycle enters its tenth year (that’s a long time between spikes in defaults),” LCD noted in June. And it’s even more eyebrow-raising:

But it’s not just the sheer volume of cov-lite outstandings that are important. LCD recently looked at the debt cushion of outstanding loans – the amount of debt in a borrower’s capital structure that is subordinated to the senior loan – and found that, increasingly, today’s cov-lite deals have little or no debt cushion beneath them. This is important because, as LCD research has shown, the lack of a debt cushion significantly lessens what an investor will recover on a loan, if that credit defaults.

How much has this debt cushion eroded? As of May 31, 23% of all cov-lite loans did not have any debt, such as a mezzanine tranche, high yield bond, or other, below the cov-lite facility. That’s an all-time high, and is up from 18% five years ago, and from just 10% at the end of 2007 (shortly before the financial crisis), according to LCD.

So not only is issuance of cov-lite loans booming, and the total amount outstanding of cov-lite loans is setting record after record, but a larger and larger portion of these loans have no debt cushion beneath them, and the risks are higher than ever.

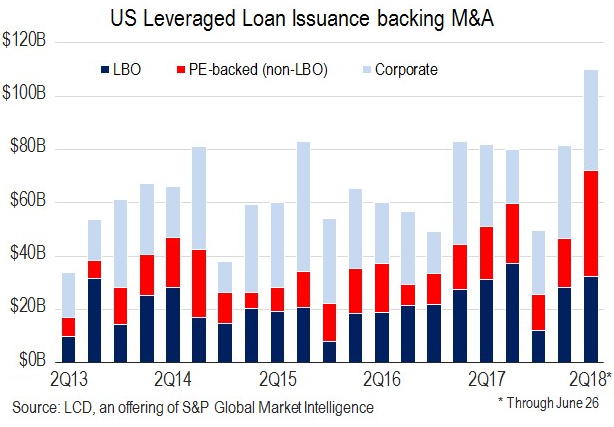

And what is one of the drivers? Mergers & Acquisitions by junk-rated companies. Leveraged loan issuance to fund M&A deals soared to a record of $83.9 billion in the second quarter, accounting for 58% of all issuance, beating the record set in the second quarter of 2007 ($82.9 billion), just before it all came apart.

This chart via LCD shows quarterly leveraged loan issuance since Q2 2013, with the three purposes color coded: leveraged buyouts by PE firms (dark blue), other M&A by PE firms (red), and for non-buyout corporate purposes (light blue):

But it gets even better.

In Q2, fired up by this wave of M&A, issuance of leveraged loans with only a second-lien – a riskier type of debt that gets repaid only after first-lien debt has been repaid – surged for the second quarter in a row, and hit $12.2 billion. Second-lien leveraged loans are appealing in good times because their yields are higher than those of first-lien debt. But, according to LCD, “They are one indication of a hot leveraged loan market.”

It’s all flying off the shelf these crazy days. Including at Asurion. Its PE firm owners are extracting $3.75 billion from it to fund a special dividend, one of the largest ever. The package of leveraged loans includes a $1.5-billion second-lien tranche. Read… This is Proof the Junk-Credit Market is Still Irrationally Exuberant

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

No wonder the venture capitalist and merger companies are making a killing. So easy to issue debt, get the purchased firm to pay for it, charge a massive rate of interest and then take a dividend, which can be financed by more debt. A spiral to the bottom as we know. But they make a killing so must all be ok.

Seems to me that these spiral to the bottom deals work like a spring. The VCs and Merger folks are at the top of the spring and we regular folks are at the bottom providing soft landings for the risk takers. Even when the risk takers are taking on insane amounts and kinds of risks. Of course these risks are not insane, because they know we “regulars” are here to underwrite their greed.

So easy to get debt? That can’t be right, I hear the Fed has embarked on a super-duper money tightening cycle. That must mean money is really tight and hard to come by. How would it be possible for a bunch of poor quality loans to be bundled together and sold to eager buyers if easy money was not still plentiful – must be fake new.

The Fed funds rate is still below the level it is lowered to during most recessions (all but the last two) – so should I assume, given the emergency level of the Fed Funds Rate (1.875%) that the Fed thinks we are still in a recession or is something in fact different this time (entering the era of the death of fiat).

The FACT is, there are still not enough available assets in the world to soak up the continuous flood of currency. These leveraged loan obligations are purchased for a reason – central banks have forced investors into this crap. Central banks have given governments a license to spend (after all they need never pay back the debt). Central banks have bid up the cost of housing, having flooded the mortgage market with excess trillions. If the Fed decided to do these things they must believe these to be good things – therefore the Fed says overpriced loan obligations are good and those guys are experts so who ya gonna believe.

This is NOT the game that venture capitalists play… rather what the PE (Private Equity) firms do…big difference

Who’s buying the end product?

Loan funds, pension funds of all stripes, diversified funds… there is huge demand from those entities. And they’re good investments as long as we remain in the good times.

Yes the ‘good times’ never end….do they :)

Holy crap, Batman!

I’m sure that Wall Street, and the government they purchased, have only our best interests at heart ……

“But the SEC, which regulates securities, considers them loans and doesn’t regulate them. No one regulates them.”

Quite so.

A careful look under the bonnet and in the boot should be enough to persuade anybody that the SEC doesn’t actually regulate. Its job seems to be to take hard-fought legislated regulatory mandates and unwind them. It’s a stealth deregulatory machine posing as some sort of enforcer.

To wit:

https://www.nakedcapitalism.com/2018/07/sec-knifes-whistleblower-program.html

Very disturbing. Congress regulates, the SEC deregulates, and nothing changes. Because it’s not supposed to. It’s just the ying and yang of financial rapacity. It protects the miscreants with a smokescreen while pretending to righteously deal with them.

As for the present article, it’s clear that we’re well into the latest boom-bust cycle, the usual mechanism your overlords (and overladies) use to consolidate the wealth of the underlying economy upwards to themselves. You engineers can think of it as a two-stroke machine, with debt as the working fluid and corruption providing lubrication.

The worker bees who generate the wealth (that would be you, gentle reader) actually contribute twice in the process: (1) wealth is stripped as it is generated by skimming profits off the bubble, and (2) the system is bailed out at the expense of the workers bees in order to restore it, allowing the cycle to begin anew.

What Our Illustrious Host cannot tell you is exactly where you are in the cycle and when the Bust phase will begin. That’s because your O & O’s want it to be a secret, because it would reduce their profits if everybody knew. It’s just better for them if they don’t give you any way to save yourselves.

The people who operate this two-stroke boom-bust machine know exactly what they’re doing and what the end result of it is going to be:

Now that’s what I’m talking about. It takes ‘disturbing’ to the next level.

Now for the disclaimer: I plan to ditch you all too when the time comes. I’m all packed and ready to go. Thanks, it’s been nice, at least for me. The parameters of your impending demise support my theories, so there’s that, at least.

you’re funny. i hope you’re not keeping your insightful rage to yourself out there in the world.

That Rushkoff article is something else. Thank you for sharing.

The overlords, which have always existed, are wise enough at getting the goose to provide golden eggs without also slaughtering the goose. Therein lies a common interest. There are also those who are mad enough to slaughter the overlords and the goose.

I once managed a business with a large number of employees – went to the restroom one day, politely asked the lady who was cleaning it if I could interrupt her work and asked how she was doing. She had the biggest heartfelt smile and and I realized she possessed something I didn’t …happiness.

Gold can’t buy that my friend …with only a smile and pleasant demeanor, she taught me one of the most valuable lessons of my life. Happiness can be had for free …and we can choose to possess it.

Setarcos – She knew full well that if she told you how she *really* felt, or was doing, she’s be fired immediately.

Happy peasants – feh!

Alex, At that moment, I would have gladly switched places with her :-)

“Beam me up, Scottie”

Get me outa here!!

Cheap Money = Cheap Risk.

However, consequences remain the same. Ultimately.

Isn’t a Cov-Lite “non-amortizing” PIK 2nd-lien loan basically the same thing as an interest-only second mortgage on the whole company? After the Housing Bubble, what could possibly go wrong with such an arrangement! (OMG…)

I suppose it’s also similar to a preferred stock, except without the SEC regulation and investor protections…

However, issuance isn’t the whole story. Some loans actually do get paid off. It would be really valuable to know what’s the total net outstanding in this class of loan, and how has the total changed over the past 10-20 years?

From the linked reports, it looks like the default rate is creeping up over 2%, on the high end of “normal”; if it passes 2.5% that could be a leading indicator for the next credit crisis.

Between this and Housing Bubble 2.0, a lot of people stand to lose a lot of paper “wealth” in the next crisis…

Wisdome Seeker,

All “term loans” are “interest only.” That is normal for corporate term loans, regardless of how high the credit quality. A term loan comes due on a certain date and has to be paid off. On that date, the company will normally have lined up new funding, either another loan, or maybe it sold bonds and uses the proceeds to pay off the loan, etc. This part it normal.

PIK means that instead of making interest payments, the interest gets added to the principal, and the loan balance grows. Creditors aren’t getting paid in cash for the interest, they’re getting “paid in kind.” PIK is a toggle that can be switched on and off.

PIK loans have been around for a long time. Normally creditors/investors don’t go for them, or they charge huge interest rates to be compensated for the risks, and they’re not common. But toward the end of the credit cycle, when everyone is chasing yield, PIK becomes very popular among risky companies, and creditors/investors don’t care. That’s state we’re in now.

Wolf, thank you very much for the clarifications. I remember PIK-toggle being a thing in 2006-2008.

Apropos of the total size of the Leveraged Loan market, I dug through the other articles from the linked reports and found this:

> The leveraged loan asset class recently became a $1 trillion market

…

> upwards of $800 billion of cov-lite loans outstanding, according to LCD.

http://www.leveragedloan.com/leveraged-loans-cov-lite-volume-reaches-yet-another-record-high/

$1 Trillion is enough to have “contagion” effects when the crisis stage hits. Together with Junk, the Leveraged market is the “subprime” market for corporate bonds. >$1T outstanding is about where subprime mortgages were in the 2007 crisis. Actually the potential risk could be larger in corporate Cov-Lite: when the wave of defaults arrives, lenders can’t simply foreclose on the company and pray for recovery, like they could with the foreclosed housing. So recovery levels could be much smaller than in the residential real estate crisis.

Also note that in the 2007 crisis, it was the floating-rate subprime loans that defaulted the most. I’d bet it won’t be any different for the corporate cov-lite leveraged loans.

Hopefully the Cov-Lite issuance isn’t based on fraudulent paperwork, like much of subprime was, but that leads to the next question: what assumptions are the lenders currently making that will prove horribly wrong this time??

“”– until rates rise further. That’s when this debt gets more expensive for these companies that already have a high debt load, often combined with money-losing operations – the combination that gives them a non-investment grade or “junk” credit rating “”

Maybe it´s the market´s perception, that the Federal Reserve will back out from raising interest rates “too much” down the road (to alleviate financial risks) what makes “investors” pile up on these risky debt instruments even more.

So investors must be doing it not because of future higher returns, but future business-as-usual.

Or, maybe just greed and envy (TINA and FOMO), wtf do I know?

At what point do these guys extract more value from their company than could ever possibly exist? With the paltry level of inflation, and (all) governments pale efforts to keep real inflation and asset inflation inline. I don’t fault them pulling off this sleight of hand, wealth effect and all but if they are whistling past the graveyard of all deflationary crashes, how’s this going to work?

The fed is acting like the party is playing keep away with the punchbowl?

Toys R Us is what happens. Credit was burnt long and slow, sales declined at the same pace. So they ran out of cash coming in and credit coming in.

Once the well runs out of water, the pail can no longer be refilled.

“how’s this going to work?”

In the long run, it can’t. But they’re only interested in short-term profitability. After all, as Keynes pointed out, in the long run, we’re all dead. Keynes certainly is. This is how things are in the post-Keynesian financial world.

Besides, when it all blows up, they get bailed out, so in that sense there is no risk. (See my earlier comment.) So much for ‘moral hazard’. And since everybody’s doing it, nobody can be blamed.

You get to help bail them out, just like last time, and the time before that. Your permission is not needed. How does it feel to be an unwilling insurance policy for rich greedy people with no concept of ethics or morality?

Not that they care. All they care about is saving themselves when the worst happens by leaving their victims to hold the bag. It does not occur to them to do anything to prevent it, because that could compromise their profits. My earlier comment addressed that also.

When all the world is flooded

And I’m about to die,

I’ll stand upon old Walter’s wit

Because it is so dry.

I had a chuckle at your above linked article. The rich ‘group’ were/are nuts, as far as I’m concerned. Don’t they know we’re all in this together? A good little illustrative movie about this is “Snowpiercer”. It is very thought provoking. If the sh%! hits the fan as mentioned, and the connected move to their redoubts, they will find the poor locals who live there have already called dibs on what they thought they owned. Unbelieveable. When strangers come around and check out our property, or my son’s, the neighbours living on the way in have made note of it, for sure. Two days ago some sketchy people were driving around looking at property, supposedly to buy. Our friend, tenant, and neighbour checked them out, noted their vehicle and plate number, and then drove down to my son’s place 3 times and made sure it was okay. (he is away working).

Those who live rural know the following: It is tribal. You have to live there, and you have to be part of the community. You can’t be a phony or hide your assets, and you have to be willing to share/lend. Everybody already knows almost everything about you. Plus, you better have some friends. Outsiders are vulnerable and always will be.

Paulo – I esteem your posts greatly, however, there are some caveats to living in “the rurals”.

I lived in/on a survivalist place and there were tons of other survivalists, End Times, etc type people around too. They … all pretty much keep a “to shoot” list, at least in their minds, of which of their neighbors are “sinful” or “evil” or “probably funded by Soros” or whatever crack-brained excuse they can dream to equate to; “I’m a’gonna take their stuff”.

Ferfal, a name that will be familiar to those in survivalists circles, wrote about this. That being out and away from the crowd often just meant it was much easier for baddies to invade your place, hold you hostage and torture all of your secrets (where’s the gold hidden? Where are the MRE’s?) with a nice long time window before it got noticed. And sure enough, where I was living, a guy got horribly tortured, only managed to untie himself and hobble next door (was supposed to die, tied up) in time – barely recognizable – to get taken to the hospital and not die.

This was two. streets. over.

You’d think the hardest worker, most conscientious worker, would be valued. At least I thought that! Even after working in American workplaces for decades, I actually believed that.

Nope! It’s the person who’s a combination of the best at bamboozling others and a healthy dose of psychopathy.

Ferfal finally gave up on moving to the USA (you dodged a bullet there, pal!) and is in Ireland, and not in some “the hills have eyes” area too, but in a city where his kids get decent schooling and you don’t have to “pack iron” to walk to the mailbox.

Yeah, it’s nice to have a tribe but keep in mind, hunter-gatherer tribes tended to have very, very high homicide rates. It really was a thing that Aboriginal Americans used to wait for the next tribe over’s menfolk to go out hunting and then do their best to kill off or enslave the women and children. There are tribes living quite sustainably in the Southwestern Pacific, whose praises are sung by Green types, who have followed practices like head-hunting and cannibalism until very recently.

You can get a great guy/gal, always ready to help, etc etc yadda yadda, and in the rurals still end up with rumors or a whispering campaign against you.

A classic example is the American war hero Alvin York, who went back up to the “holler” he hailed from, set up a hospital, etc. and still had several attempts made on his life. Nice, well-liked guy, not some scoundrel.

I can’t find anything online that backs me up; I got this information on York from a book I had when I was into collecting books on guns and shooting in general; it was a little book that was printed in the 1950s so no ISBN, printed on an old-fashioned press (you could see the letters indented into the pages) and it talked about the “hillbilly” culture where anyone who was even thought to have slighted another might have a little accident in the woods. … it was (is?) a rough place. It was considered pretty remarkable that York elected to go back there instead of staying the hell out once he’d gotten out.

I wish I still had that book! I’d gladly scan it to put on archive.org

Spreads are widening and Powell would say transitory! There is a lack of supply in I.G. But keep that on the down low.

Powell is covering his eyes, “there is no yield curve, there is no yield curve..”

I don’t see these loans from the shadow banking system as a problem. The Federal Reserve will flood the market with a tsunami of cash way before any pension fund sees a loss on these loans.

BTW lets all just keep repeating the mantra: “in an investment environment where the Fed has been trying to push up interest rates” Trying to push up interest rates? If the Fed wanted to push up interest rates they would simply do it – this “maybe we will or maybe we won’t” occasional 1/4 point raise stuff is going nowhere. 30 year fixed mortgage interest rates are still under 4.4% – raising interest rates?!!!! You gotta be kidding me.

Inflation is getting worse and worse every day and we have a central bank that believes this is fantastic. Hey! ordinary houses, in any city with job growth, are going for a million bucks! Isn’t that great, Bernanke made ordinary people millionaires! Of course this came at the expense of making wage slaves out of the half of the population without a house, no biggie – their fault for being born during the wrong era.

Bernanke trashed the currency and trying to save it should be a hair-on-fire emergency down at the Fed but instead those cowards just stay the easy money course and people play along and pretend we are in some kind of tightening cycle – nonsense.

And that is why assets will continue the inexorable rise. Assets are not going up in real terms – but currencies continue to fall so assets rocket higher in nominal terms.

Wake up, money is as loose as it’s ever been – what tightening? Leveraged loan obligation have zero chance of putting their investors at risk, ZERO. Money floods into these investments because money is plentiful everywhere – Bernanke made sure of it.

Sell your dollars before your losses get worse – you have been warned.

Not a problem? It depends on who you are.

Buffet closed out short puts written years ago.

https://www.zerohedge.com/news/2018-07-09/buffett-cashes-out-equity-index-puts-he-wrote-nearly-decade-ago

Think about it. The guy has Wells Fargo in his pocket. He is part of the crony capitalist gang that runs the Fed. If he wants the loosest financial conditions, then he gets the loosest financial conditions, money gushing in all directions, running in all directions looking for anyone that can fog a mirror to borrow money. And so his short puts gain big time, as various channels bid up markets, that he also controls because he has so many companies in his pocket. Buy backs etc under his dictate. There are no accidents in that game.

And so shadow banking no problem? Which way does Buffet and the gang want things to go? Every so often, down is the new up. When? Ask Buffet. Maybe they don’t ever want things to go bad. I would not bet on that, since down is a big profit center for insiders, just as up is.

Of course, the short puts are just a little profit extra for Buffet, not the main thing.

So when Buffet says don’t bet against America, what he really means is don’t bet against his machine.

All I can say is I wish I had been a Partner in a PE firm during my career rather than a lowly Mechanical Engineer in industry.

You’re better off being an engineer. You can do things. And what you don’t know you can figure out or you wouldn’t have made it through your program.

Check out the old classic from the ’60s, Flight of the Phoenix. The rich investors will be staggering around with handfuls of worthless money and you’ll be building whatever you might need, maybe even an airplane!

Paulo – (insert exasperated sigh here) you know Flight Of The Phoenix was a movie, based on a novel, right?

https://en.wikipedia.org/wiki/The_Flight_of_the_Phoenix

I used to run into this in the survivalist crowd. It was all “Things are gonna go ‘this’ way because in ‘that’ movie they went that way…”

Movies as reality.

The saddest thing is there’s no way to short these!

I heard the dark lord Lloyd on tv saying they are relying on algos to assess the risks of lending because they have such good data and they know people always pay if they can. Such is the state of risk management these days.

I keep getting loan offers from the dark lord Lloyd and others, outrageous amounts at more outrageous interest rates, up to 40K at 30%+. They know my credit is bad because they buy the names from the credit bureaus. With all the govt agencies supervising the financial industry, you would think this wouldn’t be permitted, but I guess that’s not what they do.

You realize industry is more or less the gov now and has passed legistlation that your privacy and personal data are for sale. Thanks Trump and Republicans and the death of net neutrality. If the US folks knew how much better privacy is in other places they would be shocked. Enjoy it.

50 bps increase next?

“No, it will blow the market up”. I am always amused when someone in this blog gives me this answer as if increasing 25 bp at a time is not encouraging this kind of risk taking behavior.

50 bps drop in rates much more likely.

This article finally did it! It literally made me dizzy trying to understand the corkscrew twists about these “debt instruments”.

“Just give me an ol’ Paint!”

(Line from movie Crimson Tide; Gene Hackman to Denzel Washington)

Come now, Wolf. Janet Yellen, the most peerless economic prognosticator of the new Millennium, has given us her assurances that there will be no new economic crisis “in our time.” So firms and speculators can lever up with wild abandon, knowing our debt-fueled prosperity will continue on a permanently high plateau, as our all-wise, all-omniscient central planners and their inerrant computer models at the Fed will surely steer us clear of the icebergs.

/sarc

Bloomberg has a viewpoint essay out today on this same topic, which agrees with Wolf’s article. The total of the Leveraged, Junk, BBB and “true investment grade” bonds is around $7.5T, and the better-than-BBB rated slice is only 1/3 of the pie, with BBB being another 1/3 and Leveraged & Junk being about 1/6 each:

https://www.bloomberg.com/view/articles/2018-07-10/corporate-bonds-are-getting-junkier

For the individual investor, any suggestions on some ways to specifically short the leverage loan market?