And its eerie exhortations to the banks to prepare for a downturn to avoid “undue disruption to the financial system.”

The FDIC’s quarterly report on commercial banks and savings institutions was cited in the media mostly for the $56 billion in profits that FDIC-insured commercial banks and savings institutions made in the first quarter, which was up 27% from a year ago. An estimated $6.6 billion of the profits were due to the tax-law changes.

It remained mostly unmentioned that this increase in profits came after the huge charge-offs banks took in the fourth quarter mostly due to write-downs of tax assets, also a result of the new tax law. These write-downs slashed bank profits in Q4 to $25 billion, the worst quarter since the Great Recession.

Overall, Q1 was really exciting. Banks were firing on all cylinders, according to the FDIC: Net income jumped, loan balances rose, net interest margins improved, and the number of “problem banks” edged down. But worries are creeping up:

The interest-rate environment and competitive lending conditions continue to pose challenges for many institutions. Some banks have responded by “reaching for yield” through investing in higher-risk and longer-term assets.

Going forward, the industry must manage interest-rate risk, liquidity risk, and credit risk carefully to continue to grow on a long-run, sustainable path.

The industry also must be prepared to manage the inevitable economic downturn, whenever it comes, smoothly and without undue disruption to the financial system.

I added the bold. This is a goodie. We had an “undue disruption to the financial system” during the last downturn, and we don’t want another one, the FDIC says.

“Undue disruption” would be when banks stop lending. That’s when credit freezes up in a credit-dependent economy. Everything comes to a halt. Paychecks start bouncing. So, don’t do that again.

The long-term objective for banks should be to position themselves during periods of good economic and banking conditions, as exist today, to be able to sustain lending through the economic cycle so that the industry can play a counter-cyclical role, and not a pro-cyclical role as occurred during the financial crisis.

“Pro-cyclical role” means banks made things worse during the last downturn. So don’t do that again, it says.

These warnings about the end of the credit cycle don’t come out of the blue. We have seen in other data that defaults in subprime auto loans and subprime credit card loans are already surging. Those are early flags that the credit cycle has entered the next phase.

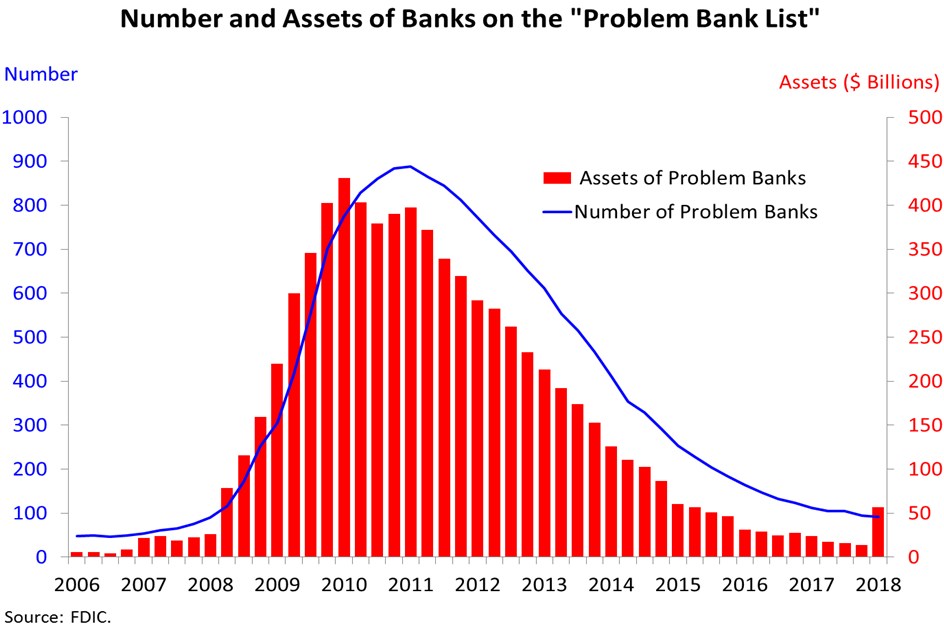

The FDIC also reported that the total number of banks on its “Problem Bank List” declined by 3 to 92 banks. Which banks are on the list is a secret. It said that three institutions were added to the list. Thus, five must have made if off the list. None of the banks toppled in Q1, which is a good thing, after six bank failures in 2017 and five failures in 2016. All this is benign compared to the 148 bank failures in 2009 and 157 bank failures in 2010, or the 534 failures in 1989.

And then comes “Chart 8” in the FDIC’s presentation, which depicts the nicely behaved number of banks on the FDIC’s “Problem Bank List” (blue line, left scale), and the red bars… OOPS! The “Assets of Problems Banks” (right scale) more than tripled in the quarter to $56.4 billion:

This doesn’t mean the financial system is going to collapse in Q2. But it does show that the three new banks that were added to the “Problem Bank List” were bigger banks with a lot more assets. This is the same kind of jump seen in 2008.

It confirms the other early indications that the credit cycle has definitely moved on to the next phase. The FDIC is not oblivious to it, and its risks:

[A]n extended period of low interest rates and an increasingly competitive lending environment have led some institutions to reach for yield. This has led to heightened exposure to interest-rate risk, liquidity risk, and credit risk.In addition, with the current expansion in its latter stage, the industry needs to be prepared to manage the inevitable downturn, whenever it may occur, in order to avoid financial system disruption and sustain lending through the economic cycle.

I added the bold. The FDIC just cannot stay away from the phrase, “avoid financial system disruption.”

Subprime is already calling. Read… Credit Card Delinquencies Spike Past Financial-Crisis Peak at the 4,788 Smaller US Banks

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

does it say which banks were added to the problem list?

Oil and gas exposed?

assuming the correlation between interest rates and oil prices or production and supply, it would seem so. Bonds may be making their own market, hence volatility, so the Fed keeps pushing short term, (and LIBOR continues rising due to credit constraints, and in the US any way fiscal juicing of the economy) while long term rates come down, result of US denominated EM bonds being dumped, and the yield curve inverts. Armstrong says the 30yr could go to 10% instantly. Volatility usually precedes a big move.

from the article: “Which banks are on the list is a secret.”

Naturally. “For every one that doeth evil hateth the light, neither cometh to the light, lest his deeds should be reproved.”

Nope. Singling out banks publicly is a no no, even the relatively tiny banks on their current problem list.

Many banks that remained profitable during the great recession were actually forced to take TARP and this was one of the reasons. So instead of conservatively and/or well run banks being able to tout their strength, they were lumped in with the banks that have failed and been rescued multiple times (e.g. Citibank).

Now what is the lesson? Running a small bank is for losers. Running a larger bank that is safe/sound is for bigger losers. Instead, leverage up, take more risk, roll the dice and know there are people in Washington that will take your fat out of the fryer. Washington knows they have painted themselves into this corner, so all the tooth gnashing about regulation and all them attempts to micromanage banking (which adds costs for all to bear).

Washington style = put food out for all the dogs in the neighborhood, then build a fence to contain them and finally, walk around with a stick beating them …all while blaming them for coming for the food to begin with in the press.

Lovely analogy, thanks for the laugh, but sadly it’s not so funny for most. Dogs sometimes bite back if pushed too far.

The micromanagement resulted from the needless complexity of the law, which suggests to me it was ultimately intended to fail.

Simplicity works. Think Glass-Steagall: you can be a commercial bank, or an investment bank, but not both. Lotsa problems prevented or solved…

Needless complexity is not just wasteful, but often disguises one set of interests exerting power over others.

I love your analogy – full marks.

Is it that a certain number of players are necessary to maintain the game / success of the game / the capacity to play the game / the cover story – “to pull it off” – mode ???

Or else ???

The excess would be dispensed with ???

The game players my feel that there is safety in numbers.

Is it possible that all the banks should be on said list ???

Sadly, the folks at ProblemBankList.com, who did such good service for the community during and after the last crisis, appear to have given up a year ago, just before their voices became relevant once more:

http://problembanklist.com/problem-bank-list/

The FDIC doesn’t name names. However, at least back in 2008-2010 there were good sites that compiled the relevant financial data so that one could judge a bank’s strength on one’s own.

One I remember, that seems to have stuck around, is Weiss Ratings: https://weissratings.com/banks

The FDIC does have some public Statistics on Depository Institutions:

https://www5.fdic.gov/sdi/main.asp?formname=standard

For Credit Unions, the NCUA has complete financial reports available here: https://www.ncua.gov/analysis/Pages/research.aspx

Individual credit scores are used to determine whether or not a bank will loan money to those individuals, no secrets here. Yet, we are kept in the dark about a bank’s financial worthiness (“Problem Bank List”) when we decide to deposit our hard-earned money, which they in turn loan out at 5 to 10 times our return. We should have the same right to examine a bank’s financial strength as they do ours.

Agreed. But at least for Credit Unions, we do. See my reply above with NCUA link.

To be fair, though, if a government agency with oversight authority were to create media hype declaring a bank unsound, there would be a run on the bank overnight, and it would certainly become unsound.

This reminds me that given the amount of hostile ink directed, justifiably, at Wells Fargo’s criminal business practices, it would seem prudent for anyone banking there to seek alternatives, or at least to have a Plan B in place to cover essential transactions, should Wells’ business get disrupted. I can’t imagine the government would deliberately shut them down, but much can happen when panic hits.

And then there’s that bank in the UK that shot themselves in the foot with the IT disaster…

As a final thought – for any bank you rely upon, keep a close eye on the stock price. Somehow the insiders always know, and the stock price always knows.

Every FDIC insured bank is required to file quarterly Call report of condition. Public info. Available on UBPR website. Regulators generally will assess overall financial position based on the tier I rbc ratio, but there’s other reasons a bank can find itself on problem list.

“To be fair, though, if a government agency with oversight authority were to create media hype declaring a bank unsound, there would be a run on the bank overnight, and it would certainly become unsound.”

If the hype is honest and built on facts then that would be a good thing. People seem more than happy to boycott a fast food chain over a viral video but seem sluggish to move finances from one weak bank to a safer spot.

Bankers are not very smart people, which is why Washington has to hold their hands and put up smoke and mirrors to obscure their misbehavior. Like Ralph Wiggum on the Simpsons, bankers are the type that like to stick forks in light sockets.

An example of Washington’s infinite wisdom, $ Billions are spent annually by banks trying to comply with the Patriot Act. One example …banks are required to report any “suspicious activity”. If the teller is unsure if your activity is suspicious, you get a report written about you (and telling you about it is a crime). So when you sell something on craigslist, don’t take the cash to the bank. The irony is there are sheep who believe they are being “protected” by laws such as this; totally clueless about the motivations.

The catastrophically-misnamed “Patriot Act” was never about fighting terrorism. It was always about total information awareness and Orwellian systems of surveillance and control, as well as identifying any source of wealth worth stealing via taxation or civil forfeiture. And the sheeple graze on.

Fractional-reserve banking is a fradulent business, where legal tender is hypothecated to multiple parties at the same time. Bank panics were very common before the powers that be decided to interfere and micro-manage a fundamentally flawed business model.

And this is why we can’t have nice things. ;-)

No new graves were dug at the FDIC Cemetery (aka Failed Bank List) in 2018:

https://www.fdic.gov/bank/individual/failed/banklist.html

“Happy Days are Here Again!” (Ben Selvin and the Crooners, 1930)

https://m.youtube.com/watch?v=gqsT4xnKZPg

try here first

https://www5.fdic.gov/EDO/DataPresentation.html

but it will take some to decipher the query options

They provided a primer on how to use EDO-Enforcement Decisions and Orders.

https://www5.fdic.gov/edo/help.html#searchform

Kind of meaningless whack-a-mole game.Trivial cases are ruthlessly pursued while the big things are getting out of hand with no remedy in sight. Reminds me of Court TV and Judge Judy.

All they can do is to produce plaintive white papers “Oy vey ist mir.We can’t control shadow banking !”

Fractional-reserve banking is legal fraud. FDIC is part of the proverbial duct tape and bailing wire that holds it together, sometimes.

Ahh Just “pull it “

We had to, Frederick…

Get your short positions in first Fred, then we’ll “pull it.”

Consolidation pains ? The Fed has never not bought bad paper from shadow banking entities having cash flow headaches! The federal reserve is nimble and has a mandate to stick the taxpayer with any loss via congress? It wont be as messy as 2008 and yet it will be another end of the world event where banks win and taxpayers lose? 1.9 trillion in excess reserves is more efficient than immanent domain?

Looking at the histogram, it looks like we are about at Q1-2, 2008.

Does this portend a crisis this year perhaps, ceteris paribus?

Austrian Peter Ja, genau

Thanks Frederick, at least someone agrees. Perhaps I’m not off the wall after all, since this is what my family thinks!

In Q2 of 2008, RE prices had been falling for several quarters. I recall that RE was beginning to drop pretty hard in Q3 of 2007 because I was looking for a house then.

We haven’t seen any of those RE drops yet, so I think our current position is different in that respect. Also, this time around it seems a lot of the risk has been transferred from residential mortgage loans to corporate loans. There is a lot of corporate debt out there, and it’s doubtful that debt can be renewed at higher rates without difficulty.

So true, it’s the excess corporate debt that could be a trigger in the next recession.

In terms of the credit cycle, your estimate of the timing is probably close.

But the big banks are very different now than they were then, and they have a lot more capital (thanks to 10 years of not paying savers) than they had then. The big banks can take large losses.

More exposed and imprudent smaller and regional banks are going to be at greater risk, but they’re not a threat to the financial system.

The next financial crisis will not be like the last one, and it will have a different source, and it will likely sprout in a different country — my top picks are Canada and Australia. But those countries are much smaller than the US, and so the global impact will be smaller.

whatever happened to China being the canary in the coal mine ? i am not saying that you ever offered up that notion but a lot of learned pundits who do similar work to you started saying that as far back as 2011.

It boggles my mind when i think back of all the false red flags that caught my attention over the last 9 years.

It reminds me of the IMF warning about speculation in the Irish property market in 1998. That property market continued onward and upward – virtually uninterrupted – for another 9 years.

“It reminds me of the IMF warning about speculation in the Irish property market in 1998. That property market continued onward and upward – virtually uninterrupted – for another 9 years.”

The IMF, Meredith Whitney, Janet Yellen, and myself on several occasions, have shown many times, its easy to be wright.

Its very difficult to be wright and on time.

9 years, is not that long, in the time frames of the IMF/FED, and National/Global Financial Systems.

china is kicking the can by being repressive, and among other things, dictating to target banks (normally with larger private shareholding of those who do not support Xi) that they convert NPl’S into Equity. At rates determined by the CCP. Then hold that “Equity” at values determined by the CCP until the CCP permits them to sell it, some decades into the future.

Have increased the “Asset’s” of the target Bank, and decreased the NPL ration, the CCP then instruct the target Bank to open a new line of credit to the “Entity” they just took “Equity” in as it is obviously credit worthy and has few Debt’s. Rinse and repeat, many times. Thus china can keep Zomibies afloat, as long as it wishes to.

china can stave off the day of reckoning in so many ways, the west can not, as the law in china, is what the CCP want it to be, on any given day, and the judge will rule, in anything, as the CCP wants.

Just as CCP, can, and does, prompt defaults and bankruptcies, when it suits it to do so. Normally to send a message to some people, or a sector.

I do not know what will trip CCP china up or when, as by all western rulers it should have imploded by now. Just that It will happen and the longer they stave it off, the bigger the bang will be. Probably prompted by an outside forces, unforeseen incident, they can not control.

Those who think the reverberations will stop at the borders of china, or even Asia, when it happens, are sadly deluded.

I personally hope not the countries you mentioned, but Europe not a problem? If you have to pay the bank to keep your money, who is going to have money in the bank to provide a cushion during a recession? But agree, still better than being in debt up to your eyeballs, like Canada and Australia.

“The next financial crisis will not be like the last one, and it will have a different source, and it will likely sprout in a different country — my top picks are Canada and Australia.”

Care to expand on your thought as to why AU could trigger a GFC, Canada I can understand.

Traditional, at the first n of possible trouble in AU, the AU banks tighten savagely in NZ, where they control and dominate the banking industry. The first signs of this are normally in apartment and rental property lending ratio’s. Followed by Auto loans.

As like in the US now. The Big AU banks fund (in many cases own) the second tier auto lenders.

There is a school that considers one of the major NZ spec apartment crashes was caused by unnecessary AU bank tightening in NZ.

We are not seeing any hints of this sort of behavior yet. Which we should be for the normal September October crash schedule.

The last crisis had its origins in derivative securities, what Warren Buffett has called “financial weapons of mass destruction.” The highest profile failures last time were investment banks like Lehman Brothers, Bear Stearns, and AIG. Goldman and Morgan Stanley would have probably failed too if the government hadn’t stepped in. Commercial paper markets seized up causing pain. Traditional bank lending didn’t play a significant role in causing the last crisis, despite the media’s attempt to blame it on subprime borrowers.

I expect the crisis will play out in a similar way as last time, with commercial banking as collateral damage, but not the ultimate source of the crisis. Now Congress just passed a law the other day neutering most of Dodd-Frank, as if sending a cue to markets to start melting down.

Cause => Effect, not Effect =>Cause. The origins of the crisis go back to laws passed in the 70s, which got real teeth with regulatory enforcement actions in the 90s. Prevailing public policy was = home ownership believed to be a cure for many social ills. So Washington wielded and showed their big sticks, some banks were beaten and all took notice …and adapted accordingly.

Example – Banks generally sold off the mortgage loans they knew were marginal or worse, so the toxic mortgage-backed securities that were productized were a reaction to a previous cause. Many associated derivative use-cases were also a reaction. And yes, all the related systems designed to make money reflected these incentives and disincentives that developed from the genesis of public policy.

And these systems were self-reinforcing though dependent upon an impossibility …perpetually rising real estate prices. There were other lesser factors that also contributed to the crisis, such as Greenspan’s monetary policies. When it all blew up, the media explained in all with only 1 word -” greed”. Ha, as if bankers discovered their greed for the first time in history. And bigger “Ha”, as if only bankers possess greed.

Banking was remarkably stable, and asset bubbles tame, during the 40 or so years while most of the New Deal regulations were in place. The Clinton and Bush II regimes were a disaster for banking, allowing banks to gamble with deposits, engage in financial alchemy (derivatives), and causing moral hazard when the TBTF banks understood that they would get bailed out and their a**es saved.

Not a single banker went to prison under Obama, and Robert Rubin still walks a free man. These are crimes against humanity.

“And bigger “Ha”, as if only bankers possess greed.”

Real bankers are not greedy, as greed leads to excessive risk taking.

Excessive risk taking, leads to untenable losses.

Most banks in America, are in fact Gambling institutions, using their clients money. In a “heads we win tails you loose” scenario.

AFSD is not good if they changed it to FSDA it would work.

But sound like an agency.

The FDIC could have titled this report, “Don’t do what Deutsche Bank did.” Counterparty banks in China, Japan and Europe are the biggest threat to American banks, because it’s the trade surplus countries that jury rigged the dollar system to their own advantage. Unfortunately for them, the Fed isn’t going to reward them for gaming the system by bailing them out when the time comes to pay the price. It will be interesting to see which American banks will pay the price for playing along.

It will be interesting to see if the dollar survives the next imminent crisis:

Jim Rickard’s book: “The Road to Ruin” explains all in his view of this world.

Maybe the dollar is the problem. A reserve currency like the dollar is not the best way to finance international trade. A truly international currency not tied to one country would benefit everyone, and avoid the kind of financial instability that reliance on the dollar causes. As it is, we keep lurching from one financial crisis to another. The world has a dollar addiction, and like every addiction, it usually doesn’t end well.

For the Love of Money

https://www.nytimes.com/2014/01/19/opinion/sunday/for-the-love-of-money.html

https://www.nakedcapitalism.com/2018/05/heres-money-destroying-world-addiction.html

Very little research is needed to show that every major problem in the world can be attributed directly to the greed of the rich. In policy circles it is taken for granted that they deliberately instigate wars that kill hundreds of millions for the simple reason that they are profitable, including both world wars.

These people are on course to destroy civilization in the blind pursuit of avarice. Some will even admit it. They have the will, and they have the means, and they will use them. There is nothing to stop them, and less every day to even slow them down. And so they will succeed.

The rest is commentary, and not very interesting, really.

Gather ye rosebuds while ye may,

Old Time is still a-flying;

And this same flower that smiles today

Tomorrow will be dying.

Hello all,

I have been a voracious reader for some time. I am a debt slave and the walking debt. I have net negative $44,000, $10,000 in interest sensitive debt. I’ve only ever made $11 an hour.

The banks and creditors have spilled over into my world of the real economy and helped me pay for living. It seems every time I get $500 emergency saved I have to take it out for another car insurance bill every six months. Or as my moldy trailer rots around me and the ceiling leaks into the cupboards and around the windows, we replace siding and maintain it but it is a 22 year old trailer. It is horribly inefficient. But it was my grandmothers trailer and the only reason I am not living directly with my parents at 28.

I’m holding on without defaulting but I understand the weight of debt. The banks will not have the reserve ratios, the free/ cheap money stimulus never reached me and I am considerably more in debt now due to… everything. I guarantee you, most people will not be like me. You will not ever see that money again, and they won’t care.

I have never missed a payment.

They have come to me. Citi Bank in particular.

You know I can only earn so much.

I graduated in 2007 and I wondered for a decade, why am I not getting raises? Why have I broken myself and given my best for less in return than I am putting in. Why after 15 years of work am I still only making $9-$11 an hour? Why can’t I even get cleaning for $13 an hour even when the upper management/ owners has to do it themselves? Now here in Maine the fight is really on to lower minimum wage. Yes I realize this isn’t a good economy here but all the rich lovelies come and summer here. All the imported workers, all the land owners, all the money. Why can’t I get a fair wage, why is this the low end standard of the economy, and rich people get to use the limited amount of economy in the world to buy luxury goods and still pay the same amount for a tomato as me? The prices of the world are completely out of whack.

I can’t go without car insurance, or a car. I am trapped in America because I don’t have savings to leave. I am trapped in debt. I am trapped to take care of my family here as well. But it could be so much better where pay ratios are better, where debt doesn’t fuel life. I never used a cent for anything non essential.

I have an associates degree in Hospitality and Tourism Management from community college I graduated in 2014. I still owe $5,000 on that. I’ve applied hundreds of places, and never got anything. And wages are poor.

Hopefully comes the reckoning brought to this economy, and the reality will become clear.

But the best to you, Wolf, you empathize with us like we’re human and not just making stupid choices. You can see the noose they have made for us. Thanks.

I also see that Wolf has empathy for the little guy/gal, and he is compassionate whereas most are coldly calculated by comparison.

With respect to age & wages, you are likely best off if you can start your own business repairing residential homes or cleaning them. In brief, contractor rates are 5x 11.00 per hour, and the margins of profit accrue to you if you are nimble about work & estimates.

And here is how to do it:

1)..Purchase a print advertisement in the local community newspaper that outlines the work you can do. Painting, window cleaning, chimney repair, screen window & door repair, et cetera.

2)..Purchase quotation/estimate books at Office Depot, and articulate that you do FREE Estimates as well as offer 2 year guarantees on all work.

2a)..Purchase a Contract/Proposal book at Office Depot, and make sure to always have a signed contract for all the work you do.

3)..Purchase business cards with your business name and telephone # and email on it. Get a lot of 1000 or 500 to start.

4)..Sit by the phone & wait for estimates.

5)..Study small business practices every day.

Try this out for 1 year and then determine if you have made more money as a private contractor than as an employee.

MOU

Your grandma will not mind if you sell the trailer and move in with your parents. She left it to you to help you, not hinder you. Move back home and save as much as you can, while you look for work, in a better paying area. Don’t be afraid to ask for relocation expenses, they can only say no thanks.

We left Florida when the choice became eat or pay rent. In a lower cost area we are doing better. Don’t be afraid to take a chance, maybe your family will follow, somebody has to be the first to break the pattern.

Best of luck.

Take a look at plumbing. It is not hard to learn the basics. Try to get on as a plumbers helper, or (as fed up as you are with courses) there might be hands- on short course near you.

Unlike other trades involved in building a house, there is an ongoing need for plumbing.

BTW; the ‘service plumber’ who responds to a leaky toilet call will almost never be a journeyman or papered plumber.

This is a VERY well paid trade but maybe because it isn’t glamorous there is always a shortage,even of helpers.

PS; re debt . Look into a ‘consumer debt proposal’

This is an alternative to bankruptcy. I don’t know the law where you are but here in BC Canada there is a public adviser for this, as well as dozens of private outfits (Four Pillars etc.)

Basically the lender is advised that you are unable to pay

and do they want something or nothing.

I know someone who got 80 K down to 30 K.

Step one: a new bank account that only you can access.

see, Wolf? this isn’t just a “money” site.

Kelsey- yeah. it sucks real bad. it’s not in your head. none of it. i love everyone else reaching out to you. all i can tell you that i know for sure is to get healthy stay healthy.

treat working out like a religion because this “not-fitting-into-america-ANYWHERE” stuff WILL seriously mess with your head and you need to be solid and strengthened and …what’s the word?… GROUNDED… pick whatever helps you sweat, lose sense of time, get in the flow and shake off “civilization” for an hour or so.

Wolf goes swimming. most intense people need to balance out the “fight” and immense WAVES of b.s. out there with some kind of return to reality and physics that only being offline and in the real world will bring.

but Petunia’s right; any gifts are never meant to HINDER but help. and flying and jumping into the unknown IS terrifying but we need realists now more than ever, and you are in one of the first stages of realization that this all is …really BAD. cosmically bad.

it’s not your fault. that’s the crux of this site. it’s radical because Wolf seems like “just a money guy” (he’ll say so himself but that’s a diversion)–but this site undermines all the b.s. and myths this world is running on and has been running on.

hang in there. this despair is a stage that we need more empathetic fighting people.

that’s what i was told 8 years ago when i was wandering the streets of nyc high and enraged and full of despair and fantasizing about a desiccated suicide found in the desert, smeared in eyeliner.

You have touched my heart. Your treatise is a condemnation of our crooked system and I thank you for your courage to share your distress with us and the world, as a salutary lesson for us all. Our youth today are ‘dying’ on their feet, as you say, trapped in a debt stranglehold.

You are in debt, my dear, because nobody can live reasonably on your measly wage unless you change you lifestyle altogether and camp out in the backwoods, off-grid, and follow the Preppers.

I am retired and here in UK worked as a volunteer for the British, Citizens Advice Bureau (CAB); an amazing organisation set up at the beginning of WW2 to help people survive the extreme privations of wartime. I remember rationing and having to manage with little in food and supplies, not to mention the bombs and destruction. We found ways to live, and be happy too!

Have a look at our website – there are many pages for helping people manage their debt and I am sure that the methods do not change in differing countries that much – debt is international and transcontintental.

https://www.citizensadvice.org.uk/

Then search the web for UK survival recipes for cooking and living in wartime Britain etc.

If your debt is totally unmanageable, which it appears to be, then bankcruptcy is an option which is not as terrifying as it seems. I have accompanied many Brits to the court and they have been, without exception, totally relieved by being able to start with a clean sheet and with CAB help, go forward to a happy and prosperous future.

You seem to have the courage: So remember St Augustine’s prayer:

using the word ‘God’ as you understand it:

” God grant me the serenity to accept those things I cannot change, the courage to change those things I can, and the wisdom to know the difference.”

I say it every morning – it starts the day off for me and gives me strength to battle on through the hours in enjoyment and pleasure. Duly assisted by Wolf’s embracing writing.

@Kelsey,

All of the above are great ideas. I only add: move to a low cost area in Florida. It is the center of the world for hospitality.

Try Daytona Beach, New Smyrna, Cocoa Beach areas. Stay away from South Florida. Work is booming and a trade job will make you a mint.

Another thought for you, this is good advice from John Whithead:

https://rutherford.org/publications_resources/john_whiteheads_commentary/when_things_fall_apart_a_graduation_message_for_a_dark_age_short

Make sure you have your essentials covered before paying any of your debts, especially the credit cards. They will squawk, but let them. Then, I would schedule an appointment with an attorney to consider filing bankruptcy.

IMHO, claim bankruptcy, get rid of the leaky trailer, and relocate to somewhere….anywhere, other than Maine. You may have to leave the family, but that’s what internet is for. And when you find a better job, you’ll be able to send back more money to support them. There must be someone, somewhere looking for a -still- young person with degree in Hospitality. You may have to go to the ends of the earth, but there are better prospect out there — but you’ll have to relocate.

Kelsey,

Thank you for sharing.

I know your plight.

My GM vehicle’s service bill tripled at the dealership today—something happened to it in their hands and they limped it along until I turned the steering wheel once out of their garage and onto their parking lot—“not our problem”. Like you, I can’t keep doing this.

I could offer you some rosy words, but I’ll just be frank and truthfully say “I understand”.

Hi Kelsey,

I think you touched on the key with the phrase, “trapped in America”. I am friendly with a number of hotel GM’s in Asia, where I live and own a couple of Western food restaurants. Many GM’s have worked their way up through the ranks – majority of them starting in F&B. If you can get out of the U.S., I think you will find a far more merit-based work environment where advancement is not just possible, but likely – especially for someone smart enough to be reading WolfStreet :).

If you’re young enough, to get out of the U.S. fast – consider a Club Med G.O. position. Incredibly hard work, but tons of fun, and if you can do it for 2 or 3 years, there’s probably no better resume builder than that. (Plus you can save most of what they pay you!) I would never hesitate to hire someone with good references from Club Med.

Key to getting out of the U.S. isn’t cash – it’s having basic proficiency in speaking a 2nd or 3rd language – the more the merrier. Spend the next 18 months learning Chinese in (much of) your spare time, and 2 years from now you’ll be flying somewhere. (Chinese speaking Westerners are a relative rarity, and should be in-demand in the hospitality biz for years to come – and not just in China, but all over the world).

In addition, I have friends in other lines of work, with limited educations who became millionaires on fairly modest salaries, just because they came to Asia/Middle East for work when they were younger and stayed, enabling them to save and invest – instead of paying for outrageously overpriced heatlh insurance, car insurance, and rent/mortgage.

Just had dinner with a manager from the local Hilton/Conrad, and he totally agreed with the language thing.

I sympathize with the commenter. But, through circumstances beyond your (and mine and everyone else’s) such as accident of birth in any place on this planet…….you have been living within the most selfish, embracing of all the “Seven Deadly Sins” kind of society on the planet. Survival of the fittest, modified in some small ways by “progressive” politics. But, the system is hell bent to destroy all that gets in its way…..come hell or high water. That’s all the system “accomplishes” in the long run. It is not based on “kindness”, “forgiveness” (except for the super rich), “benevolence”, etc.. You either make it or you don’t. Tough “you know what!”

The system does have it’s “genius”. It winnows the strong from the weak. It rewards the basics of the system itself: Outright Greed and “no mercy for those who don’t understand what’s going on!”

For the salve of the spirit there is always religion of one sort or another: “You will gain your credits in the Here-After…..”…..the opiate of the masses.”

The end result of this system is predictable: Total resource/environmental destruction of this beautiful crust of dirt hurtling thru space to “God knows where”……..

So, count yourself fortunate; You have roof over your head, albeit a leaking one (a metaphor for your life in the system); you are not literally “out in the streets” with the homeless. You might have decent health…In this capitalist system if you are healthy you are already “rich”.

There is so much more to add but this is Mr. Wolf’s blog (and one of the very good ones) and not mine.

Count your blessings. I wish you luck.

Sierra, you need to expose yourself to the eastern way of being. The western is all about break through limitations while the traditional eastern is all about livin in harmony within the limitations. In game theory, the western thinking is alpha strategy and will lead to the predictable ruin in the end while keeping you winning before that happens. It is like alchohol, making you feel good before your liver is ruined. The eastern recommend you drinking water. Who wants water when there is booz?

Based on what you said, the $5K student debt is the critical debt and cannot be discharged in bankruptcy.

In making a guess here, I am assuming you own the land where the trailer is located. If so find the nearest Land Bank, which is a lending institute for just land, to see if you can get a loan to consolidate your debt at a lower interest rate. A $44K to $10K debt to interest seems extremely high running on average 22.7% versus 4.5 to 5% at the Land Bank. Almost any farmer can tell you where the nearest Land Bank is located. You mentioned Citi Bank, which is notorious for using payment processors that post payments late or not at all and charge exorbitant interest rates of double or triple the market rate. I hope you are requesting your payment schedules on an annual basis as there was a huge lawsuit over Greentree, their payment processor, whereby Obama’s cronies were just allowed to pay a fine and change their name. Warren then use the money as a slush fund instead of remitting the money to those ripped off. Hate to make it political, but it is the truth.

If you don’t own the land, then you might try some debt consolidation of your necessary debt like car payments, pay off one credit card and walk on the rest. I don’t personally ever recommend bankruptcy, because as a person who has always paid their bills with a medium to low debt load, my credit score has always been lower than people who just stopped paying, walked away and never filed bankruptcy. It wasn’t until I was totally out of debt that my credit score was raised to where it is almost perfect. It is a very unfair game the banksters play to make the younger people pay higher interest rates. Now if you live in a debtor state that garnishes your wages, then plan accordingly by moving out of state within 30 days after you stop paying to a non-garnishment state, i.e., Texas. But I will tell you that by moving out of state, you will lose close family ties. It is almost like out of sight, out of mind.

Otherwise, you might want to shelter in place and get a 2nd job or start a business as suggested. If you start a business, book evening and weekend appointments only at first, which your customers will greatly appreciate and wait to see if things take off before quitting your day job.

Your time to upgrade your life style is not coming until you are about 43 years old or later as 2033 to 2037 are going to pivotal years for the U.S. The slide starts in 2033 and bottoms out in 2037, the UK will come much sooner as Italy and Turkey are already in the slide. So make a purchase that is conducive to your retirement. While there will be some dips along the way in the economy, the biggest one is mentioned above so you can maximize your purchase and/or life style.

I am speaking from experience. I moved from western NY in 1981 on the down hill slide of the economy and didn’t buy my first real estate until the bottom of 1987, which was a foreclosure, waited for the rebound, sold for a profit and brought my second piece of real estate in 1998 at an auction with an eye towards retirement. Twelve years later I was completely out of debt and have never looked back, but it did take sacrifice, research and scrounging. It takes constant mental exercise of do I need it or do I want it. My needs came first with many wants left behind.

In the meantime to keep a roof over your head, you can either live with your parents or start watching Craigslist or go to garage sales for free to cheap recyclable material to continue fixing your trailer to get it to a sell-able condition. Then get out of and stay out of any state with a state income tax to avoid having to pay for their debt binge. Only morons would think of lowering the minimum wage when the state is in debt.

Banking is the best pro-cyclical business model ever invented. Think of where we’d be without it, still living in the stone age?

Ummm, you must be a banker then?

The fact we ever escaped from “the stone age” was thanks to the fact that banks did NOT exist then and that people cleverly invested in profitable projects with the means they HAD ( liquid assets ) and not with the means they might have 25 years from now ( loans ).

Until recently, any lunatic could get big loans at near-zero interest rates to be paid back over 30 year time spans for projects with imaginary payouts.

Pro-cyclicality always to crashes ( read von Mises, Human Action ).

‘to be able to sustain lending through the economic cycle so that the industry can play a counter cyclical role’

Huh? Sounds like the FDIC hopes the commercial banks, which are responsible to share holders, are supposed to take on the role of the Fed in a downturn.

They won’t. They will pull in their horns in a recession and tighten lending. And that is probably their best strategy to avoid the FDIC’s real fear, having to bail them out.

A pretty odd statement.

FDIC is worried about the Minsky moment that could occur after banks tighten lending during a downturn.

The same banks will end up holding worthless “assets” again.

Reading the FDIC statements, I am astonished by how spineless the FDIC has become. Is this all they can do – make half-hearted attempts to warn about dangers they know will lead to disaster?

If they see a problem, they should clearly address it, or they are not doing their job.

The FDIC insures the banks. It should be demanding changes in behavior rather than making subtle suggestions from the sidelines. They should be proposing increases to FDIC insurance rates to address the clear risks they have identified. But, they aren’t proposing to do anything. Spineless.

Reminds of when Hillary Clinton had a “talking” with those banks that were up to no good, thinking that would change behavior. She told them bad things would come of it. Good job, Hillary.

Perhaps they are afraid to upset the banks, which apparently run this country. It’s about time they start worrying about taxpayers instead. Boot them all out.

Amazon and Google are venturing into the banking, lending and currency systems so they will be the disruptors very soon

It’s a seriously regulated biz with monster fines. See Wells just getting a billion dollar fine. No comparison with the static Google gets re: monopoly on search.

By that chart the rise in problem assets and problem banks postdates the financial crisis, so those thinking we are still several bars removed from trouble think again. I would say the Fed would rather have (or even engineer) a financial crisis, rather then wait until economic forces are out of their control, because their playbook last time worked so well, that they are comfortable with this style of crisis.

And that doesn’t correspond well with my definition of change.

When a meager growth has been achieved by increased debt, could the next recession be just a traditional recession?

It’s no longer an economic cycle, it’s a credit cycle.

You got it in one – agreed

A recession always begins with a tightening of credit. The economic cycle is the credit cycle.

Nothing THEY can do about growth on the fiscal side, but they can levitate asset prices and maintain a constant bias of 2% inflation. The next crisis will involve the Fed buying stocks (the float becomes closely held, shares are taken off the market squeezing supply and raising the competition for available shares in a super accommodative monetary system. They can really get the squirrel cage going to maybe Dow 40000 in a few years) They have the tools to guide a market which now sees a rate hike policy in stone, when it suddenly turns nobody will miss that signal. It may be that the market is already one step ahead of them, and putting the market into a dive won’t work, there’s the rub, with economic stagnation and the Fed with no interest rate leverage left, up or down. There’s a good interview with Armstrong about that, rates don’t matter.

“If the Fed is hiking rates, unwinding their balance sheet through Quantitative Tightening – selling their bonds – and with inflation already at 2.5% and rising, why are investors buying 10-year bonds only yielding 2.99%?

Inflation alone is killing the ‘real’ gains – for instance, a 2.99% yield minus 2.5% inflation equals only 0.49% ‘real’ profit.

That’s more than an 85% ‘real’ loss. . .

AND

Shouldn’t investors be selling their bonds and asking for higher yields to protect themselves from the coming inflation and rate hikes?

The only answer I can think of is that the bond market is calling the Fed’s ‘economic growth’ bluff.

They understand that the U.S. economy is fragile. And that the chance of deflation and recession is very likely within the next few years.”

https://palisade-research.com/calling-the-feds-bluff/

Perhaps the Fed or the bankers can answer Palisade Research’s questions?

Indeed. Why are my banks paying 0.7% and 1.1% on high-interest saving accounts, when central bank rate is higher, and inflation still higher?

How about a challenge: can someone find anything that still makes sense?

Yep, I’ve tried to find just that person – IMHO they don’t exist although Wolf does his best to ressure us and for that I am thankful.

American Express Bank now pays 1.6% on its savings account. Goldman’s Marcus pays 1.7% on savings. 12-month CDs are now available for over 2.2%. 12-month “brokered CDs”, last time I looked, ran up to 2.35%.

If you have a lot of cash you need to put to work but keep relatively liquid, consider Treasury bills. The 3-month yield is now over 1.9%. You can start here: https://www.treasurydirect.gov/indiv/myaccount/myaccount.htm

Use Google to find banks with higher rates. They’re out there :-]

Rate-shopping is fine for those with spare credit, but for god’s sake folks be careful who you lend to! When you lend money you are implicitly supporting whoever you lend it to. Force the bastards to at least pay higher rates by only lending to the good guys!

I’d rather die than lend to Goldman, “Marcus”, Wells Fargo or any mega bank.

I refuse to save in “Money Market” funds or accounts, because when I read the fine print I almost always see that all the paper in them is from those big banks.

Find places that don’t make you cringe. Lend to them only!

I recall the day my father bought a CD yielding 16%. Remember the 70s.

Ambrose Bierce,

Yes, was that the day inflation was 15%?

Except, who does the FED work for? We know they’re well paid by someone but whom?.

The governors on the Federal Reserve Board of Governors (currently Powell, Brainard, and Quarles, plus four vacant slots) are employees of the US Government and are paid by the US Government.

The presidents of the 12 Regional Federal Reserve Banks are in the private sector, employed by and paid by their reserve bank, which is owned by the financial institutions in its district.

Neither Bernanke nor Yellen are super rich. But they were immensely powerful, and in some ways, they were figureheads for a system.